Lehman Brothers Pedersen Explaining the Lehman Brothers Option Adjusted Spread of a Corporate Bond

Upload

quarterlyearningsreports3Category

view

430download

0

Bank of AmericaGrowth Opportunities in Global Consumer & Small Business Banking

Liam McGeePresident, Global Consumer & Small Business Banking

Lehman BrothersSeptember 10, 2007

2

Forward Looking StatementsThis presentation contains forward-looking statements, including statements about the financial conditions, results of operations and earnings outlook of Bank of America Corporation. The forward-looking statements involve certain risks and uncertainties. Factors that may cause actual results or earnings to differ materially from such forward-looking statements include, among others, the following: 1) projected business increases following process changes and other investments are lower than expected; 2) competitive pressure among financial services companies increases significantly; 3) general economic conditions are less favorable than expected; 4) political conditions including the threat of future terrorist activity and related actions by the United States abroad may adversely affect the company’s businesses and economic conditions as a whole; 5) changes in the interest rate environment reduce interest margins and impact funding sources; 6) changes in foreign exchange rates increases exposure; 7) changes in market rates and prices may adversely impact the value of financial products; 8) legislation or regulatory environments, requirements or changes adversely affect the businesses in which the company is engaged; 9) changes in accounting standards, rules or interpretations, 10) litigation liabilities, including costs, expenses, settlements and judgments, may adversely affect the company or its businesses; 11) mergers and acquisitions and their integration into the company; and 12) decisions to downsize, sell or close units or otherwise change the business mix of any of the company. For further information regarding Bank of America Corporation, please read the Bank of America reports filed with the SEC and available at www.sec.gov.

3

Global Consumer & Small Business Banking

• Continuing track record of growth

• Truly differentiated franchise

• Growth opportunities: Deposits and Consumer Credit

• Understanding the contemporary retail environment

4

2004 2005 2006

Revenue

32% 36% 38%

68% 64% 62%

Noninterest IncomeNet Interest Income

Growth Recap

Track Record of Growth

Deposit Households

22.7

24.6

26.1

Dec 2004 Dec 2005 Dec 2006

7% CAGR

Customer Delight

2001 2005 2006

42.5%

49.6%50.3%

17% improvement

2004 2005 2006

Net Income

Footnotes:1-Pro forma with Fleet and MBNA ($ in billions)2-Bankruptcies reform impacted provision expense by $0.6B in 2005 and ($0.9B) in 2006 on a Net Income basis.

$9.1

$11.5

$9.3

11% CAGR

5

Momentum Continues: Sales and Balance Growth

2004 2005 2006

CAGR = 13.8%

34.3

41.544.9

Total Sales Units (MM)*

*Pro forma with Fleet and MBNA

Track Record of Growth

2Q07 vs 2Q06

% Growth

Retail deposit balances 1.3 %

Consumer card balances 3.6 %

Home equity balances 24.1 %

Small business credit 37.2 %

6

Through…• 5,700+ banking centers• 17,000+ ATMs• 5,000+ affinity relationships • 66% all online bill payers• 63% handhelds reachable

We Are Where Customers Want Us To Be

In our footprint…• 76% of U.S. population• 75% of small businesses

Differentiated Franchise

7

Adding Density in Important Markets

Chicago Market BAC LaSalle Combined

Banking centers 56 141 197

ATMs 231 450 681

LaSalle

Michigan Market Detroit Other Michigan

Banking centers 160 110 270

ATMs 632 418 1,050

Differentiated Franchise

8

Unrivaled Distribution System

Customer

5,700 Banking Centers

17,000 ATMs

5,000 Affinity GroupsAlmost 23MM Online Users

2.6B Contacts

Can reach 63% handheld devices

Differentiated Franchise

9

Innovation

Differentiated Franchise

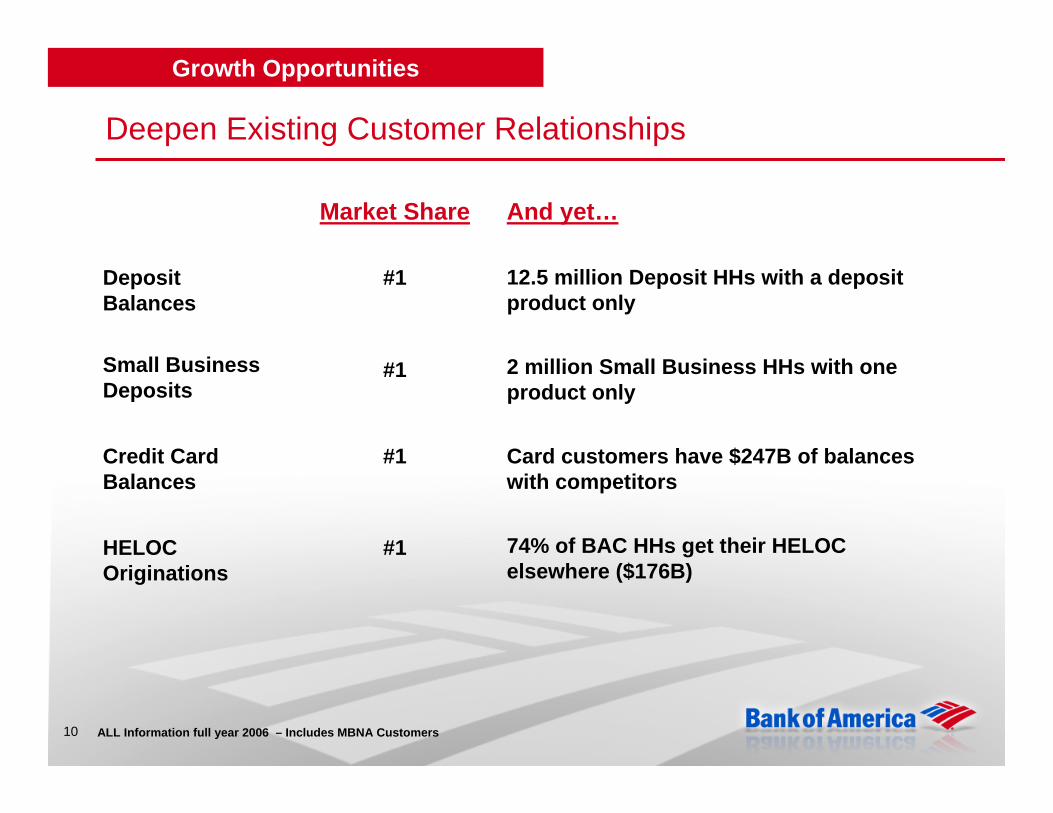

10 ALL Information full year 2006 – Includes MBNA Customers

And yet…

12.5 million Deposit HHs with a deposit product only

2 million Small Business HHs with one product only

Card customers have $247B of balances with competitors

74% of BAC HHs get their HELOC elsewhere ($176B)

#1HELOC Originations

#1Credit Card Balances

#1

#1

Deposit Balances

Small Business Deposits

Market Share

Deepen Existing Customer Relationships

Growth Opportunities

11

$-

$50

$100

$150

$200

2002 2003 2004 2005 2006Debit Purchase Volume

Deposit Success

$ in

bill

ions

**Market Share 13.3%13.9%14.5%14.3%

$ in

bill

ions

16.5%15.7%15.5%15.7%14.7%

Retail Balances * Debit Purchase Volume

26% CAGR

$-

$100

$200

$300

$400

$500

2003 2004 2005 2006-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Retail Balances Deposit Spread

*Retail Balances – Pro forma for Fleet & MBNA & Excludes US trust – Market Share includes BAC footprint only** Market Share estimates as of December for each period. Includes Fleet and MBNA, excludes US Trust.

$463$169

Growth Opportunities

12

Consumer Credit: Strength With Room to Grow

32%17% 9%

21% 12%

68%83% 91%

79% 88%

Credit Card Home Equity Mortgage Unsecured Total Credit

On Us Off Us

Total Credit of BAC Customers

$4.3 trillion opportunity within existing deposit customer base

$425B $507B $3,836B $70B $4,837B

Growth Opportunities

13

U.S. Card – Focused on Lower Delivery Costs

• Leveraging banking center and Internet channels• Greater convenience, lower cost, higher return

$109 $100 $84 $70

* Actual 2006 cost to acquire by channel was utilized to calculated 2004-2005 estimates shown and are not actual historical values . The value will therefore reflect change in mix only.

16% 12% 11% 9%

5% 8% 12% 16%

21% 19% 13% 10%

41%37%

27%24%

17%24%

37% 41%

2004 2005 2006 2007

FranchiseDirect MailOtherInternetMedia Marketing

*Cost to Acquire

Growth Opportunities

14

Delivery channels

Customer credit needs

Credit Solutions Continuum

Relationship-based Common Decision Engine

Banking Centers Mobile BankingE-Commerce Call Centers ATM

Student Loans Credit Card ULOC First Mortgage Home Equity

Growth Opportunities

15

Consumer Credit

• Credit losses remain within expected ranges in 2007

• Exited subprime loan origination business in 2001

• Consumer real estate loss ratios remain below industry averages

• Expect card losses to have peaked in 2Q for the year

Growth Opportunities

16

Consumer Purchasing Behavior

AwarenessFrom . . . To . . .

Market-GeneratedMedia

Consumer-GeneratedMedia

Contemporary Retail

17

Consumer Purchasing Behavior

From . . . To . . .

Consideration

Institutions Social Networks& Communities

Contemporary Retail

18

Consumer Purchasing Behavior

From . . . To . . .

Purchase9 to 524/7/365

Shop online, pickup in-store

Company-DefinedOptions

Customer-DefinedOptions

Contemporary Retail

19

Bank of Opportunity™