LEGAL CONCEPTS – FSMA 2000 Principles of FSMA … · Monday, 6 July 2009 THE TAX JOURNAL 21 LEGAL...

3

20 THE TAX JOURNAL Monday, 6 July 2009 LEGAL CONCEPTS – FSMA 2000 corporate transactions – these often involve communications to shareholders regarding the tax consequences of the holding, sale, and/or disposal of their investments. Regulated activities FSMA, s 19 sets out the general prohibition that no person may carry on a regulated activity in the UK unless he is an authorised or an exempt person. ‘Regulated activity‘ is defined in FSMA, s 22 as being ‘activity of a specified kind carried out by way of business in relation to investments of a specified kind’. The FSMA (Regulated Activities) Order 2001 (RAO) specifies those activities which will be regulated activities. It is wide-ranging and covers buying, selling or subscribing for investments as principal (Article 14), making arrangements for another person to buy, sell or subscribe for a particular investment (Article 25), managing investments in circumstances which involve the exercise of discretion (Article 37) and advising on buying, selling or subscribing for a particular investment (Article 53). Financial promotion FSMA, s 21 stipulates that a person must not, in the course of business, communicate an inducement to engage in investment activities unless that person is an authorised person or the content of the communication is approved by an authorised person. This prohibition covers communications made or directed from the UK to recipients in the UK, and communications made or directed from overseas into the UK if they are capable of having effect in the UK. A number of important exceptions to the prohibition on financial promotion are provided by the FSMA (Financial Promotion) Order 2005 (FPO). Employee share schemes While the RAO, Articles 14 and 25 provide that dealing in securities as principal and making arrangements for another person to deal in securities are regulated activities, a specific exemption is made in the RAO for employee share schemes. Article 71 provides that a company, a group company or a ‘relevant trustee’ (broadly, any person who holds shares as trustee for the purposes of an employee share scheme) does not carry on a regulated activity where the transaction is to enable or facilitate transactions in shares issued by the company for the benefit of bona fide employees, former employees of a group company, or their spouses, civil partners or dependants. The FPO, Article 60 provides a similarly worded exemption for communications made by a company, group company or relevant trustee for the purposes of an employee share scheme. Figure 1 illustrates the scope of the definition of a ‘group company’. There are limitations to the scope of the employee share schemes exemptions both under the RAO and the FPO, where participation is extended to a non-executive director or other non-employees, or options are granted over existing shares held by shareholders other than an employee benefit trust. As a consequence, careful analysis may be required where participation is extended or options granted in these ways. Prin cip le s o f FSMA 2000 Continuing our Legal Concepts series, Natalie Smith and Nick Thody, Osborne Clarke, consider the main provisions of the Financial Services and Markets Act 2000 (FSMA) and their relevance to tax practitioners T he FSMA is the primary source of legislation governing financial and investment services in the UK. It confers statutory and regulatory powers upon the Financial Services Authority (FSA) and is supplemented by an extensive body of secondary regulations, together with the rules of the FSA. The FSMA provides a wide range of rule-making, investigatory and enforcement powers in order to meet its four statutory objectives, which are to: maintain confidence in the financial system promote public understanding of the financial system secure the appropriate degree of protection for consumers and reduce financial crime. With these objectives in mind, the most important components of the FSMA include: a general prohibition on the carrying out of regulated activities (which are described in the FSMA) in the UK except by an authorised or exempt person an authorisation regime to enable firms and individuals to carry on regulated activities a requirement that certain individuals within authorised firms must be approved by the FSA a regime governing the making of financial promotions and a civil offence of market abuse. C ompliance with the FSMA and its regulatory regime is essential; sanctions for contravention include civil penalties and a criminal conviction. Tax practitioners are most likely to encounter the FSMA in the context of: employee share schemes – the FSMA’s broad scope means that the establishment and operation of share schemes may fall within the definition of regulated activities and communications regarding these could be financial promotions collective investment schemes – certain fund-based arrangements can fall within the FSMA definition of a collective investment scheme and so require FSMA compliance and LEG A L C O N C EP T S If any readers feel they need guidance on a legal topic which is relevant to their tax work, or would like to write on a particular topic, could they please get in touch with the E ditor at alison.lovejoy@ lexisnexis.co.uk.

Transcript of LEGAL CONCEPTS – FSMA 2000 Principles of FSMA … · Monday, 6 July 2009 THE TAX JOURNAL 21 LEGAL...

20 THE TAX JOURNAL Monday, 6 July 2009

LEGAL CONCEPTS – FSMA 2000

corporate transactions – these often

involve communications to shareholders

regarding the tax consequences of the

holding, sale, and/or disposal of their

investments.

Regulated activitiesFSMA, s 19 sets out the general prohibition

that no person may carry on a regulated

activity in the UK unless he is an authorised

or an exempt person.

‘Regulated activity‘ is defi ned in FSMA,

s 22 as being ‘activity of a specifi ed kind

carried out by way of business in relation

to investments of a specifi ed kind’.

The FSMA (Regulated Activities)

Order 2001 (RAO) specifi es those activities

which will be regulated activities. It is

wide-ranging and covers buying, selling

or subscribing for investments as principal

(Article 14), making arrangements for

another person to buy, sell or subscribe for a

particular investment (Article 25), managing

investments in circumstances which involve

the exercise of discretion (Article 37) and

advising on buying, selling or subscribing

for a particular investment (Article 53).

Financial promotionFSMA, s 21 stipulates that a person

must not, in the course of business,

communicate an inducement to engage

in investment activities unless that person

is an authorised person or the content

of the communication is approved by

an authorised person. This prohibition

covers communications made or directed

from the UK to recipients in the UK, and

communications made or directed from

overseas into the UK if they are capable

of having effect in the UK.

A number of important exceptions to

the prohibition on fi nancial promotion

are provided by the FSMA (Financial

Promotion) Order 2005 (FPO).

Employee share schemesWhile the RAO, Articles 14 and 25 provide

that dealing in securities as principal and

making arrangements for another person to

deal in securities are regulated activities, a

specifi c exemption is made in the RAO for

employee share schemes.

Article 71 provides that a company,

a group company or a ‘relevant trustee’

(broadly, any person who holds shares as

trustee for the purposes of an employee

share scheme) does not carry on a regulated

activity where the transaction is to enable

or facilitate transactions in shares issued

by the company for the benefi t of bona

fide employees, former employees of a

group company, or their spouses, civil

partners or dependants. The FPO, Article 60

provides a similarly worded exemption for

communications made by a company, group

company or relevant trustee for the purposes

of an employee share scheme.

Figure 1 illustrates the scope of the

defi nition of a ‘group company’. There are

limitations to the scope of the employee

share schemes exemptions both under the

RAO and the FPO, where participation

is extended to a non-executive director or

other non-employees, or options are granted

over existing shares held by shareholders

other than an employee benefi t trust. As

a consequence, careful analysis may be

required where participation is extended or

options granted in these ways.

Prin cip le s o f FSMA 2000

Continuing our Legal Concepts series, Natalie Smith and Nick Thody, Osborne Clarke, consider the main provisions of the Financial Services and Markets Act 2000 (FSMA) and their relevance to tax practitioners

The FSMA is the primary source of

legislation governing fi nancial and

investment services in the UK. It

confers statutory and regulatory powers

upon the Financial Services Authority

(FSA) and is supplemented by an extensive

body of secondary regulations, together with

the rules of the FSA.

The FSMA provides a wide range of

rule-making, investigatory and enforcement

powers in order to meet its four statutory

objectives, which are to:

maintain confidence in the financial

system

promote public understanding of the

fi nancial system

secure the appropriate degree of

protection for consumers and

reduce fi nancial crime.

With these objectives in mind, the

most important components of the FSMA

include:

a general prohibition on the carrying out

of regulated activities (which are described

in the FSMA) in the UK except by an

authorised or exempt person

an authorisation regime to enable

fi rms and individuals to carry on regulated

activities

a requirement that certain individuals

within authorised fi rms must be approved

by the FSA

a regime governing the making of

fi nancial promotions and

a civil offence of market abuse.

C ompliance with the FSMA and its

regulatory regime is essential; sanctions for

contravention include civil penalties and a

criminal conviction.

Tax practitioners are most likely to

encounter the FSMA in the context of:

employee share schemes – the FSMA’s

broad scope means that the establishment

and operation of share schemes may fall

within the defi nition of regulated activities

and communications regarding these could

be fi nancial promotions

collective investment schemes –

certain fund-based arrangements can fall

within the FSMA defi nition of a collective

investment scheme and so require FSMA

compliance and

LEG A L C O N C EP T S

If any readers feel they need guidance

on a legal topic which is relevant to their

tax work, or would like to write on a

particular topic, could they please get in

touch with the E ditor at alison.lovejoy@

lexisnexis.co.uk.

Monday, 6 July 2009 THE TAX JOURNAL 21

LEGAL CONCEPTS – FSMA 2000

For transactions with non-employees,

the following exemptions may be helpful:

the RAO, Art icle 28 exempts

arrangements for a transaction to which

the arranger is a party, either as principal or

as agent for another person

the FPO, Article 28 exempts one-off

communications which are made only

to one recipient or group of recipients in

the expectation that they would engage

in any investment activity jointly, relate

to a product or service which has been

determined having regard to the particular

circumstances of the recipients, and are not

part of an organised marketing campaign

and

in addition, the exemptions for fi nancial

promotions to ‘sophisticated investors’

and ‘high net worth individuals’ might be

applicable (see Figure 2).

Where individual shareholders agree to

grant options over their shares, the RAO,

Article 15 exempts a person who enters into

any transaction relating to a security where

he does not hold himself out as willing to

deal, or engaging in the business of buying

investments with a view to selling them, or

does not regularly solicit members of the

public to induce them to deal.

C ollective investment schemesThe ROA, Article 51 provides that the

establishing, operating or winding up of a

collective investment scheme is a regulated

activity.

Subject to certain exemptions, a

‘collective investment scheme’ (C IS)

is defi ned in FSMA, s 235 as a scheme

comprising arrangements:

with respect to property of any kind

(including cash or shares), the purpose or

effect of which is to enable the persons

taking part to participate in, or receive, profi ts

or income arising from the acquisition,

holding, management or disposal of the

property or sums paid out of such profi ts or

income

where the participants do not have day-

to-day control over the management of the

property and

which involve a pooling of investors’

contributions and profi ts/income and/or the

property being managed as a whole by, or

on behalf of, the scheme operator.

This could potentially include

arrangements commonly found in private

equity, venture capital and real estate funds

whereby executives become limited partners

in a ‘carried interest’ partner. If the fund is

successful, after investors’ contributions

have been returned and any priority profi t

share paid out, the carried interest partner

will participate in the balance of the profi ts.

Whether such an arrangement is a C IS

will depend on how the carried interest

scheme is structured. If it is a C IS, the

UK regulatory impact will depend on the

jurisdiction in which the carried interest

arrangement is managed and where its

participants are based. For example, if it is

managed in the UK it may be necessary for

an authorised person to be appointed as the

operator of the scheme in order to comply

with the FSMA.

C ommunications to participants in

carried interest arrangements may benefi t

from the exemptions in the FAO for

knowledgeable investors (see Figure 2).

C orporate transactionsC orporate transactions may require

communica t ions to be made to

shareholders and/or potential shareholders

of the parties concerned (and, in some

cases, participants in employee share

schemes) regarding the tax consequences

of the acquisition and/or disposal of

shares.

In addition to the exemptions already

discussed there are further exemptions

available from the prohibition on fi nancial

promotion in the context of corporate

transactions, which include:

the FPO, Ar t ic le 19 exempts

c o m m u n i c a t i o n s m a d e o n l y t o

recipients whom the person making the

communication believes on reasonable

grounds to be investment professionals,

or which may reasonably be regarded as

directed only at investment professionals

the FPO, Article 43 exempts certain

communications made by a company

where the communication relates only to

an investment issued or to be issued by

that company or by a member of the group

and is made to a creditor or member of the

group, or to a person who is entitled to a

relevant investment which is issued, or to

be issued, by the group

the FPO, Article 62 provides an

exemption for a communication by or on

behalf of any body or person where the

communication relates to an acquisition

or disposal of shares in a company, or is

entered into for the purposes of such an

acquisition or disposal – the transaction

N atalie S mith N ick T hody

The defi nition of ‘group’ for the purposes of the FSMA is found in FSMA, s 421 and includes not only parent and subsidiary undertakings but also any undertaking in which there is a ‘participating interest’.

FSMA, s 421A defi nes a ‘participating interest’ as ‘an interest held by one undertaking in another undertaking on a long-term basis for the purpose of securing a contribution to its activities by the exercise of control or infl uence’. A holding of 20% or more of the shares is presumed to be a participating interest unless the contrary is shown.

This wide defi nition of ‘group company’ extends the benefi t of the employee share scheme exemptions given under the RAO and FPO to a potentially broad group of companies.

Figure 1 – G roup companies

22 THE TAX JOURNAL Monday, 6 July 2009

LEGAL CONCEPTS – FSMA 2000

will qualify for the exemption where

either the shares to be sold carry at least

50% of the voting rights, or the object

of the transaction nevertheless can be

regarded as being the acquisition of day-

to-day control of the affairs of the target

company

the FPO, Article 67 exempts certain

communications which relate to the

securities permitted to be traded or dealt

on a relevant market and which are

required or permitted to be communicated

by the rules of, or a body which regulates,

that market.

M ark et ab useSeven types of behaviour are classed in

FSMA, s 118 as market abuse where they

relate to shares traded on a prescribed

market (such as the Main Market or AIM

market of the L ondon Stock E xchange).

These types of behaviour are:

insider dealing

improper disclosure of inside

information

misuse of information

manipulating transactions

manipulating devices

disseminating information likely to

give a false or misleading impression

market distortion.

Some acts could fall within more than

one class of behaviour. For example,

if a director is aware of an impending

announcement and discloses that

information to the person responsible

for granting options in order to infl uence

the timing of the option grant, this action

could be both an improper diclosure of

inside information and /or a misuse of

that information.

The FSA can take enforcement action

regarding market abuse and impose an

unlimited fine, although there are

several safe harbours, exceptions and

defences.

N a t a l i e S m i t h ( n a t a l i e . s m i t h @

osborneclarke.com and tel: 020 7105

7508 ) and N ick Thody (nick.thody@

osborneclarke.com and tel: 020 7105

7566) are professional support lawyers

at E uropean law firm Osborne C larke.

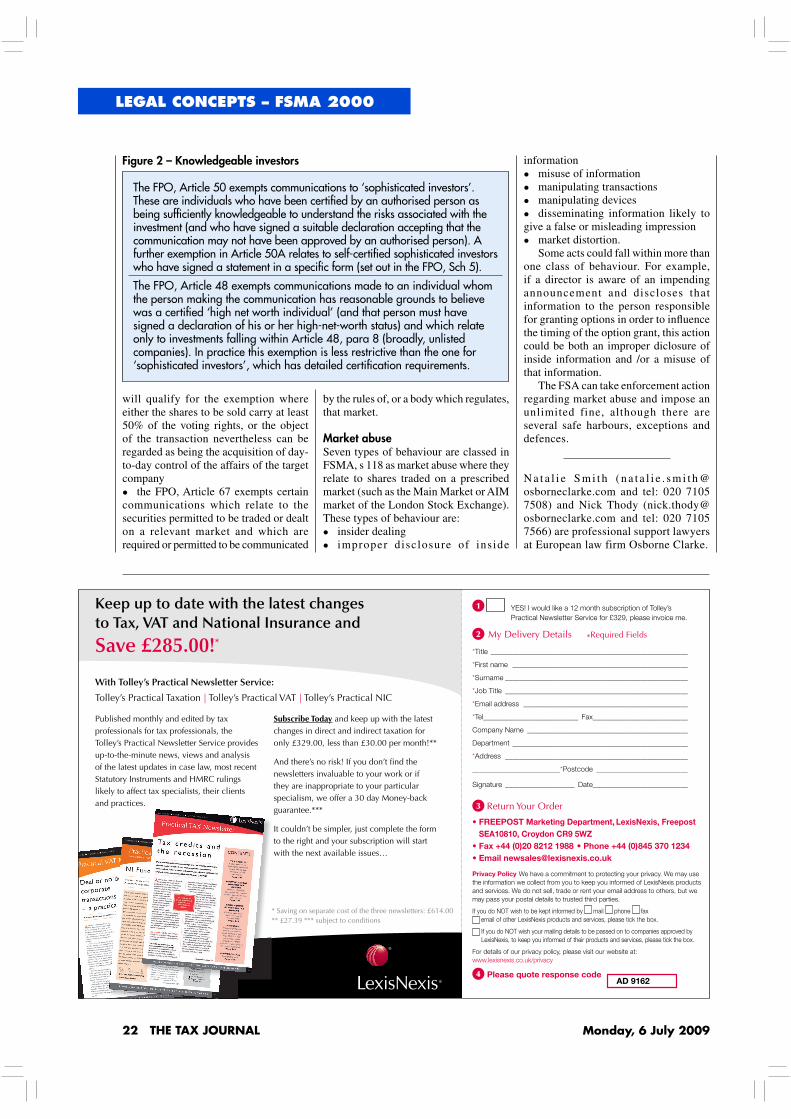

The FPO, Article 5 0 exempts communications to ‘sophisticated investors’. These are individuals who have been certifi ed by an authorised person as being suffi ciently knowledgeable to understand the risks associated with the investment (and who have signed a suitable declaration accepting that the communication may not have been approved by an authorised person). A further exemption in Article 5 0A relates to self-certifi ed sophisticated investors who have signed a statement in a specifi c form (set out in the FPO, Sch 5 ).

The FPO, Article 48 exempts communications made to an individual whom the person making the communication has reasonable grounds to believe was a certifi ed ‘high net worth individual’ (and that person must have signed a declaration of his or her high-net-worth status) and which relate only to investments falling within Article 48 , para 8 (broadly, unlisted companies). In practice this exemption is less restrictive than the one for ‘sophisticated investors’, which has detailed certifi cation req uirements.

Figure 2 – K now ledgeab le investors

YES! I would like a 12 month subscription of Tolley’s

Practical Newsletter Service for £329, please invoice me.

M y D e liv e ry D e ta ils *R e q u ire d F ie ld s

*Title _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

*F irst name _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

*Surname _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

*J ob Title _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

*Email address _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

*Tel_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ F ax _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

C ompany Name _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

D epartment _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

*A ddress _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ *Postcode _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

Sig nature _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ D ate _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

R e tu rn Y o u r O rd e r

W e have a commitment to protecting your privacy. W e may use

the information we collect from you to keep you informed of L ex isNex is products

and services. W e do not sell, trade or rent your email address to others, but we

may pass your postal details to trusted third parties.

If you do NO T wish to be kept informed by mail phone fax

email of other L ex isNex is products and services, please tick the box .

If you do NO T wish your mailing details to be passed on to companies approved by

L ex isNex is, to keep you informed of their products and services, please tick the box .

F or details of our privacy policy, please visit our website at:

www.lex isnex is.co.uk/privacy

With Tolley’s Practical Newsletter Service:

T o lle y ’s P ra c tic a l T a x a tio n | T o lle y ’s P ra c tic a l V A T | T o lle y ’s P ra c tic a l N IC

* S a v in g o n s e p a ra te c o s t o f th e th re e n e w s le tte rs : £ 6 1 4 .0 0

** £ 2 7 .3 9 *** s u b je c t to c o n d itio n s

P u b lis h e d m o n th ly a n d e d ite d b y ta x

p ro fe s s io n a ls fo r ta x p ro fe s s io n a ls , th e

T o lle y ’s P ra c tic a l N e w s le tte r S e rv ic e p ro v id e s

u p -to -th e -m in u te n e w s , v ie w s a n d a n a ly s is

o f th e la te s t u p d a te s in c a s e la w , m o s t re c e n t

S ta tu to ry In s tru m e n ts a n d H M R C ru lin g s

lik e ly to a ffe c t ta x s p e c ia lis ts , th e ir c lie n ts

a n d p ra c tic e s .

S u b s c r ib e T o d a y a n d k e e p u p w ith th e la te s t

c h a n g e s in d ire c t a n d in d ire c t ta x a tio n fo r

o n ly £ 3 2 9 .0 0 , le s s th a n £ 3 0 .0 0 p e r m o n th !**

A n d th e re ’s n o ris k ! If y o u d o n ’t fi n d th e

n e w s le tte rs in v a lu a b le to y o u r w o rk o r if

th e y a re in a p p ro p ria te to y o u r p a rtic u la r

s p e c ia lis m , w e o ffe r a 3 0 d a y M o n e y -b a c k

g u a ra n te e .***

It c o u ld n ’t b e s im p le r, ju s t c o m p le te th e fo rm

to th e rig h t a n d y o u r s u b s c rip tio n w ill s ta rt

w ith th e n e x t a v a ila b le is s u e s …

K eep u p to d ate with the latest chan g es to Tax , V A T an d Nation al In su ran ce an d

Save £ 2 8 5 .0 0 !*