Lecture2.ppt

44

Llad Phillips 1 Introduction to Economics Elements of Personal Elements of Personal Finance Finance

Transcript of Lecture2.ppt

Llad Phillips 1

Introduction to EconomicsIntroduction to Economics

Elements of Personal FinanceElements of Personal Finance

Llad Phillips 2

Outline: Lecture TwoOutline: Lecture Two

car loanscar loans the economic approach to problem solvingthe economic approach to problem solving personal financial planningpersonal financial planning

Economics 109 Llad Phillips Fall 1998Introduction to Economics

Hour, Location: 2:00-3:15, Phelps 1260Instructor: Llad PhillipsOffice Hours: NH 3032, 9:30-10:15 TuTh and 3:30-3:50 TuTh, and by appointment,

Texts:Kenneth Morris and Alan Siegel,The Wall Street Journal Guide to Understanding Personal Finance, Revised(1997)

Arthur O’Sullivan and Steven Sheffrin, Economics, Principles and Tools(1998)

Labs(sections) in the Micro Computer Lab(MCL)11189 F 9:00-9:50 P333 Lab, Phelps 1526, JD11197M 7:00-7:50 PM P333 Lab, Phelps 1526, JA11205W 8:00-8:50P333 Lab, Phelps 1526, JD11213 M 5:00-5:50 PM P200 Lab, Phelps 1525, JA62646T 4:00-4:50 PM P333 Lab, Phelps 1526, LP66381TH 4:00-4:50 PM P333 Lab, Phelps 1526, LP Teaching Assistants: Joshua Anderson, Office Hours:NH 2036 Th 3:30-4:30, F 3-4;John Davis, Office Hours:NH 2032Exams: Quiz: Thursday, Oct. 15,. You will need a

scantron sheet and a #2 pencil Midterm: Tuesday, Nov. 3, 2:00-3:15 PM. Scantron & #2 Final: Tuesday, Dec. 8, 4:00-7:00 PM, Scantron & #2

Problem Assignments: At least half of the questions on the 25 minute quiz will be from the assigned problems. Due at the next Lab(section).

Standing Assignment: Read the business section of the Los Angeles Times

Course Home Page: http://www.econ.ucsb.edu/econ109

Lecture Topics and Reading List

Part OnePersonal Finance: Economics in Everday Life

1. Tuesday Sept. 29, Lecture One: "Choosing a method to finance a car"Buying or Leasing a car

The choice between:paying cashleasingbuying on time

Reading Assignment:Guide to Understanding Personal Finance,

Ch. 2, "Credit"O’Sullivan and Sheffrin: Ch.1, “Introduction:

What is Economics?”emphasis: concepts of scarcity and production possibilities curve

O’Sullivan and Sheffrin: Appendix to Ch.1, “Using Graphs and Formulas”

Problems O & S Text: p.14: 1, 2, 3, 4, 5.p. 21: 1, 2, 3, 4, 5, 6

Llad Phillips 8

Outline: Lecture TwoOutline: Lecture Two

car loanscar loans the economic approach to problem solvingthe economic approach to problem solving personal financial planningpersonal financial planning

Llad Phillips 9

Elements of Personal FinanceElements of Personal Finance

Economics in every day lifeEconomics in every day life loansloans

car loanscar loans

Llad Phillips 10

Example: Buying a New ‘96 TaurusExample: Buying a New ‘96 Taurus KnownsKnowns

advertised price + tax + documents: advertised price + tax + documents: $17,760$17,760

down payment: $2,137down payment: $2,137 loan amount: $15,623loan amount: $15,623

loan amount = $17,760 - $2,137loan amount = $17,760 - $2,137 annual interest rate: 6.9%annual interest rate: 6.9% loan term in months: 24 monthsloan term in months: 24 months

UnknownsUnknowns monthly paymentmonthly payment

Using Excel 5.0 for a Solution Using Excel 5.0 for a Solution Price + tax + documents 17760 17760 17760down payment 2137 2137 2137loan amount 15623 15623 15623annual interest rate 6.9% 6.9% 6.9%loan term in months 24 36 48

monthly payment ($698.77) ($481.68) ($373.39)

total payments 16770.58 17340.44 17922.61

total interest 1147.58 1717.44 2299.61

Excel: select cell for monthly payment, click on Function Wizard

select Financial and PMT

Excel: click on the help button in the previous window for examples

Using Excel 5.0 for a Solution Using Excel 5.0 for a Solution Price + tax + documents 17760 17760 17760down payment 2137 2137 2137loan amount 15623 15623 15623annual interest rate 6.9% 6.9% 6.9%loan term in months 24 36 48

monthly payment ($698.77) ($481.68) ($373.39)

total payments 16770.58 17340.44 17922.61

total interest 1147.58 1717.44 2299.61

http://www.fordcredit.com/calculator/calcbuffer.html

Llad Phillips 17

Choice: LeaseChoice: Lease drive-off costs(payments due at lease drive-off costs(payments due at lease

signing): $2,136.77signing): $2,136.77 total of 24 monthly payments: $7248 = 24 total of 24 monthly payments: $7248 = 24

months * $302 per monthmonths * $302 per month monthly Payment: $249 + taxmonthly Payment: $249 + tax tax + documents = $1237 + $35 = $1272, or tax + documents = $1237 + $35 = $1272, or

$53 per month$53 per month total: $9384.77total: $9384.77

Example

249 + tax24 months

5,976 + tax

Llad Phillips 19

Increasing the Length of the LoanIncreasing the Length of the Loan

monthly payment amount decreasesmonthly payment amount decreases amount of total payments increasesamount of total payments increases amount of total interest payments increasesamount of total interest payments increases total interest as % of total payments total interest as % of total payments

increases increases

Using Excel 5.0 for a Solution Using Excel 5.0 for a Solution Price + tax + documents 17760 17760 17760down payment 2137 2137 2137loan amount 15623 15623 15623annual interest rate 6.9% 6.9% 6.9%loan term in months 24 36 48

monthly payment ($698.77) ($481.68) ($373.39)

total payments 16770.58 17340.44 17922.61

total interest 1147.58 1717.44 2299.61

Llad Phillips 21

Interest as a Fraction of CostInterest as a Fraction of Cost

Term inmonths

24 36 48

Fraction .068 .094 .128

Llad Phillips 22

Interest as a Fraction of the Monthly Payment

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0 5 10 15 20 25Payment Number

Fraction

Llad Phillips 23

Equity in a '96 Taurus Vs. Payment Number

02000400060008000

1000012000140001600018000

0 5 10 15 20 25Payment Number

Equity, $

Llad Phillips 24

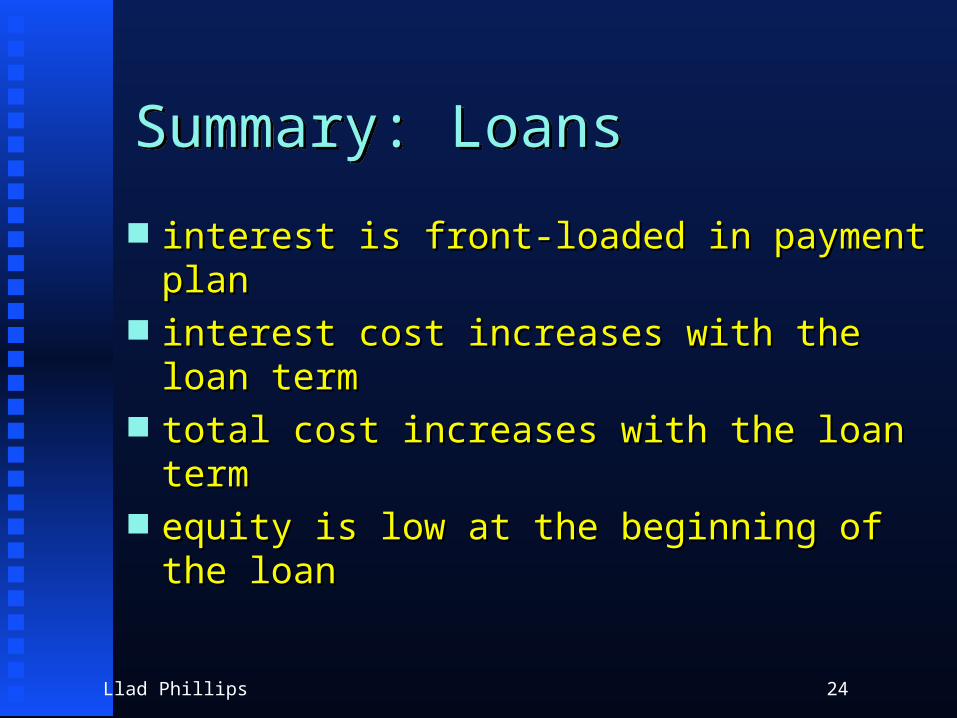

Summary: LoansSummary: Loans

interest is front-loaded in payment planinterest is front-loaded in payment plan interest cost increases with the loan terminterest cost increases with the loan term total cost increases with the loan termtotal cost increases with the loan term equity is low at the beginning of the loanequity is low at the beginning of the loan

Llad Phillips 25

The Economic Approach to Problem Solving

The Economic Approach to Problem Solving

The Economic ParadigmThe Economic Paradigm

Llad Phillips 26

The Economic ParadigmThe Economic Paradigm

describing the alternatives to choose amongdescribing the alternatives to choose among pricing the alternativespricing the alternatives choosing the best alternativechoosing the best alternative

Llad Phillips 27

The Economic Paradigmexample: buying a car

The Economic Paradigmexample: buying a car

describing the alternatives to choose amongdescribing the alternatives to choose among cash: the opportunity cost of losing interestcash: the opportunity cost of losing interest lease: depreciation included in paymentslease: depreciation included in payments loan: sell the car to account for depreciationloan: sell the car to account for depreciation

pricing the alternatives: valuationpricing the alternatives: valuation Oscar Wilde- economists know the price of Oscar Wilde- economists know the price of

everything and the value of nothingeverything and the value of nothing choosing the best alternativechoosing the best alternative

best: lowest costbest: lowest cost possibly subject to a constraint: having the $possibly subject to a constraint: having the $

Llad Phillips 28

Personal Financial PlanningPersonal Financial Planning

Financing Life EventsFinancing Life Events

Llad Phillips 29

Life Event* ApproachLife Event* Approach marriagemarriage childrenchildren

financial security: insurancefinancial security: insurance housinghousing educationeducation

retirementretirement long term carelong term care estateestate

*reference: Ernst & Young’s Personal Financial Planning Guide, 2nd Ed. John Wiley

Life Cycle Approach: Learning & Earning

AgeInfancy

Nurturing

Adolescence

High SchoolEducation

Young Adult

College

Adult

Work

Senescence

Retirement

Activity/Phase:

Life Cycle Approach: The Planners

AgeInfancy Adolescence Young Adult Adult Senescence

100%

50%

0 %

You

Parents

Life Cycle Approach: Planning

Age

Nurturing High SchoolEducation

College Work Retirement

Education: Investment in Human Capital or Earning Power

Accumulating Assets cars appliances furnishings--------------------- house financial assets

Spending

Llad Phillips 33

Planning ToolsPlanning Tools

Assets-Liabilities StatementAssets-Liabilities Statement Assets Minus Liabilities = Net WorthAssets Minus Liabilities = Net Worth

measure of wealthmeasure of wealth

Income-Expenditure StatementIncome-Expenditure Statement Income Minus Expenditures = SavingIncome Minus Expenditures = Saving

measure of change in wealthmeasure of change in wealth

Llad Phillips 34

Assets-Liabilities StatementAssets-Liabilities StatementAsset Amount Liability Amountcash bank loanstocks margin loanbondsinsurance(surrender)

policy loans

other card balanceshouse equity mortgagepersonalproperty

car loan

Total Total

Llad Phillips 35

Income-Expense StatementIncome-Expense Statement

Income Amount Expenditure Amountown salary taxesspouse “ life insuranceinsurance carsdividends foodinterest clothingrent housingother otherTotal Total

http://www.fordcredi.com/fplanner.cgi

Llad Phillips 37

Income-Expense Statement: US Population 1988Income-Expense Statement: US Population 1988Income Amount Expenditure Amountown salary taxes excludingspouse “ life

insuranceinsurance cars 20%dividends food 16%interest clothing 6%rent housing 31%other other 27%Total Total 100%

other: health, 5%; pensions & Soc. Sec., 7%; other, 15%Source: Guide to Understanding Personal Finance, p. 87

Llad Phillips 38

Strategies for Meeting Future ExpensesStrategies for Meeting Future Expenses

Buy a HouseBuy a House Tax-Sheltered Savings PlansTax-Sheltered Savings Plans Stocks and BondsStocks and Bonds

Llad Phillips 39

Buying a HouseBuying a House

PositivesPositives provides spaceprovides space builds equitybuilds equity interest is interest is

deductibledeductible

Negatives?Negatives? down payment down payment

requires saving for requires saving for this goalthis goal

interest payments interest payments are front-loaded, are front-loaded, equity growth equity growth delayeddelayed

opportunity cost of opportunity cost of not investing in not investing in stocksstocks

Llad Phillips 40

Summary - Vocabulary - ConceptsSummary - Vocabulary - Concepts economic paradigmeconomic paradigm down paymentdown payment loan termloan term monthly paymentmonthly payment annual percentage rate or annual percentage rate or

APRAPR equityequity personal financial planningpersonal financial planning life event ananysislife event ananysis

human capitalhuman capital assetsassets liabilitiesliabilities net worth, wealthnet worth, wealth incomeincome expendituresexpenditures savingssavings

Llad Phillips 41

2. Thursday, Oct. 1, Lecture Two: " Car loans; the economic paradigm; personal financial planning"

Car loansThe economic approach to problem solvingPersonal financial planning

Reading Assignment:Guide to Understanding Personal Finance, Ch. 4, "Financial Planning"O’Sullivan and Sheffrin: Ch.2, “Key Principles of Economics”

emphasis: concepts of choice and opportunity costProblems O & S Text

p. 35: 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13

Llad Phillips 42

The Principle of The Principle of Opportunity CostOpportunity CostThe Principle of The Principle of Opportunity CostOpportunity Cost

No matter what we do, there are always No matter what we do, there are always tradeoffs.tradeoffs.

Scarcity -- limited resources -- is the Scarcity -- limited resources -- is the reason.reason.

The opportunity cost of something The opportunity cost of something is what you sacrifice to get it.is what you sacrifice to get it.

Llad Phillips 43

Opportunity Costs and Production Opportunity Costs and Production PossibilitiesPossibilitiesOpportunity Costs and Production Opportunity Costs and Production PossibilitiesPossibilities

The production possibility curve illustrates The production possibility curve illustrates the principle of opportunity cost for an entire the principle of opportunity cost for an entire economy.economy.

-- shows all possible combinations of goods -- shows all possible combinations of goods and services available to entire economy.and services available to entire economy.

--- principle of opportunity cost explains why --- principle of opportunity cost explains why production possibility curve is negatively production possibility curve is negatively sloped.sloped.

Llad Phillips 44

THE MARGINAL PRINCIPLETHE MARGINAL PRINCIPLETHE MARGINAL PRINCIPLETHE MARGINAL PRINCIPLE

Marginal Benefit Marginal Benefit

The extra benefit resulting from The extra benefit resulting from a small increase in the activity.a small increase in the activity.

Marginal CostMarginal Cost

The additional cost resulting The additional cost resulting from a small increase in the from a small increase in the activity.activity.