Lecture notes in quantitative methods for economists ...

158

Lecture notes in quantitative methods for economists: Statistics module Appunti per il corso di Metodi Quantitativi per Economisti, modulo di Statistica Antonio D’Ambrosio Draft 1 Napoli, Ottobre 2020

Transcript of Lecture notes in quantitative methods for economists ...

Lecture notes in quantitative methods for economists:Statistics module

Appunti per il corso di Metodi Quantitativi per Economisti, modulo diStatistica

Antonio D’Ambrosio

Draft 1

Napoli, Ottobre 2020

Preface

Questi appunti raccolgono gli argomenti che vengono trattati al corso diMetodi Quantitativi per Economisti nell’ambito del corso di Laurea Magis-trale in Economia e Commercio dell’Universita degli Studi di Napoli FedericoII.Non si pretende di fornire agli studenti un materiale migliore rispetto ai tantieccellenti manuali presenti in letteratura, molti dei quali sono consigliati perlo studio di questo insegnamento. Si esortano anzi gli studenti a far riferi-mento alle fonti consigliate durante il loro percorso di studio. Il proposito epiuttosto quello di fornire un indice degli argomenti trattati durante il corso,riunirli tutti in un unico corpus e fornire una breve (e non esauriente) guidaalla riproduzione degli esempi riportati attraverso il software R.Questi appunti sono stati volutamente scritti in lingua inglese per una seriedi motivi:

la letteratura sul tema e quasi interamente disponibile in lingua inglese;

gli studenti frequentanti un corso di laurea magistrale devono esserein grado di studiare e approfondire i temi studiati da fonti in linguainglese;

in virtu della crescente internazionalizzazione delle Universita, e semprepiu frequente avere in aula studenti stranieri, magari frequentanti ilprogramma Erasmus.

Gli argomenti trattati riguardano il modello di regressione lineare ed unaintroduzione all’analisi della varianza. Un programma del modulo statis-tico dell’insegnameto di Metodi Quantitativi per Economisti tarato in questomodo dovrebbe preparare gli studenti allo studio di altre discipline quanti-tative in ambito sia economico che statistico, quali ad esempio econometria,modelli lineari generalizzati, data mining, analisi multivariata, categoricaldata analysis, ecc.Si suppone che gli studenti abbiano frequentato sia un corso di Statisticanel quale si siano affrontati i temi principali dell’inferenza statistica ed una

III

introduzione al modello di regressione lineare, sia un corso di Matematicagenerale in cui si siano affrontati problemi di massimizzazione di funzioni euna introduzione all’algebra delle matrici.Questi appunti sono dinamici: potranno cambiare di anno in anno, potrannoincludere nuovi argomenti, potranno escluderne taluni. La loro struttura simodifichera a seconda delle esigenze didattiche del corso di Lurea, ma soprat-tutto seguendo i commenti degli studenti dai quali mi aspetto, se lo vorranno,consigli e critiche costruttive su come modificare e migliorare l’esposizionedegli argomenti proposti.Anche se l’impostazione di questi appunti a prevalentemente teorica, sono ri-portati diversi esempi riproducibili in ambiente R attraverso una operazionedi ”copia-e-incolla” delle funzioni utilizzate. Si precisa pero che lo scopo none quello di imparare ad usare un linguaggio di programmazione: per questovi sono insegnamenti appositi. Laddove non specificato espressamente, i dataset utilizzati, tutti con estensione .rda (l’estensione dei dati di R) sono scar-icabili dal sito http://wpage.unina.it/antdambr/data/MPQE/.Queste pagine contengono sicuramente errori e imprecisioni: saro infinita-mente grato a chi vorra segnalarli.

IV

Contents

Regression model: introduction and assumptions 1

1 Regression model: introduction and assumptions 1

1.1 Regression analysis: introduction, definitions and notations . . 1

1.2 Assumptions of the linear model . . . . . . . . . . . . . . . . . 2

Model parameters estimate 7

2 Model parameters estimate 7

2.1 Parameters estimate: ordinary least squares . . . . . . . . . . 7

2.2 Properties of OLS estimates . . . . . . . . . . . . . . . . . . . 9

2.2.1 Gauss-Markov theorem . . . . . . . . . . . . . . . . . . 9

2.3 Illustrative example, part 1 . . . . . . . . . . . . . . . . . . . . 11

2.3.1 A toy example . . . . . . . . . . . . . . . . . . . . . . . 11

2.4 Sum of squares . . . . . . . . . . . . . . . . . . . . . . . . . . 13

2.4.1 Illustrative example, part 2 . . . . . . . . . . . . . . . 15

Statistical inference 19

3 Statistical inference 19

3.1 A further assumption on the error term . . . . . . . . . . . . . 19

3.1.1 Statistical inference . . . . . . . . . . . . . . . . . . . . 21

3.1.2 Inference for the regression coefficients . . . . . . . . . 22

3.1.3 Inference for the overall model . . . . . . . . . . . . . . 22

3.2 Illustrative example, part 3 . . . . . . . . . . . . . . . . . . . . 23

3.3 Predictions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

3.4 Illustrative example, part 4 . . . . . . . . . . . . . . . . . . . . 29

Linear regression: summary example 1 31

V

Contents

4 Linear regression: summary example 1 314.1 The R environment . . . . . . . . . . . . . . . . . . . . . . . . 314.2 Financial accounting data . . . . . . . . . . . . . . . . . . . . 31

4.2.1 Financial accounting data with R . . . . . . . . . . . . 36

Regression diagnostic 43

5 Regression diagnostic 435.1 Hat matrix . . . . . . . . . . . . . . . . . . . . . . . . . . . . 435.2 Residuals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 455.3 Influence measures . . . . . . . . . . . . . . . . . . . . . . . . 51

5.3.1 Cook’s distance . . . . . . . . . . . . . . . . . . . . . . 525.3.2 The DF family . . . . . . . . . . . . . . . . . . . . . . 535.3.3 Hadi’s influence measure . . . . . . . . . . . . . . . . . 545.3.4 Covariance ratio . . . . . . . . . . . . . . . . . . . . . . 545.3.5 Outliers and influence observations: what to do? . . . . 55

5.4 Diagnostic plots . . . . . . . . . . . . . . . . . . . . . . . . . . 565.5 Multicollinearity . . . . . . . . . . . . . . . . . . . . . . . . . 59

5.5.1 Measures of multicollinearity detection . . . . . . . . . 60

Linear regression: summary example 2 69

6 Linear regression: summary example 2 696.1 Financial accountig data: regression diagnostic . . . . . . . . . 69

6.1.1 Residuals analysis . . . . . . . . . . . . . . . . . . . . . 706.1.2 Influencial points . . . . . . . . . . . . . . . . . . . . . 786.1.3 Collinearity detection . . . . . . . . . . . . . . . . . . . 83

Remedies for assumption Violations and multicollinearity: ashort overview 87

7 Remedies for assumption violations and Multicollinearity 877.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . 877.2 Outliers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 877.3 Not independent errors and hetersoscedasticity . . . . . . . . . 88

7.3.1 GLS . . . . . . . . . . . . . . . . . . . . . . . . . . . . 887.3.2 WLS . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89

7.4 Collinearity remedies . . . . . . . . . . . . . . . . . . . . . . . 897.4.1 Ridge regression . . . . . . . . . . . . . . . . . . . . . . 89

7.5 Principal Component Regression . . . . . . . . . . . . . . . . . 907.6 Practical examples . . . . . . . . . . . . . . . . . . . . . . . . 90

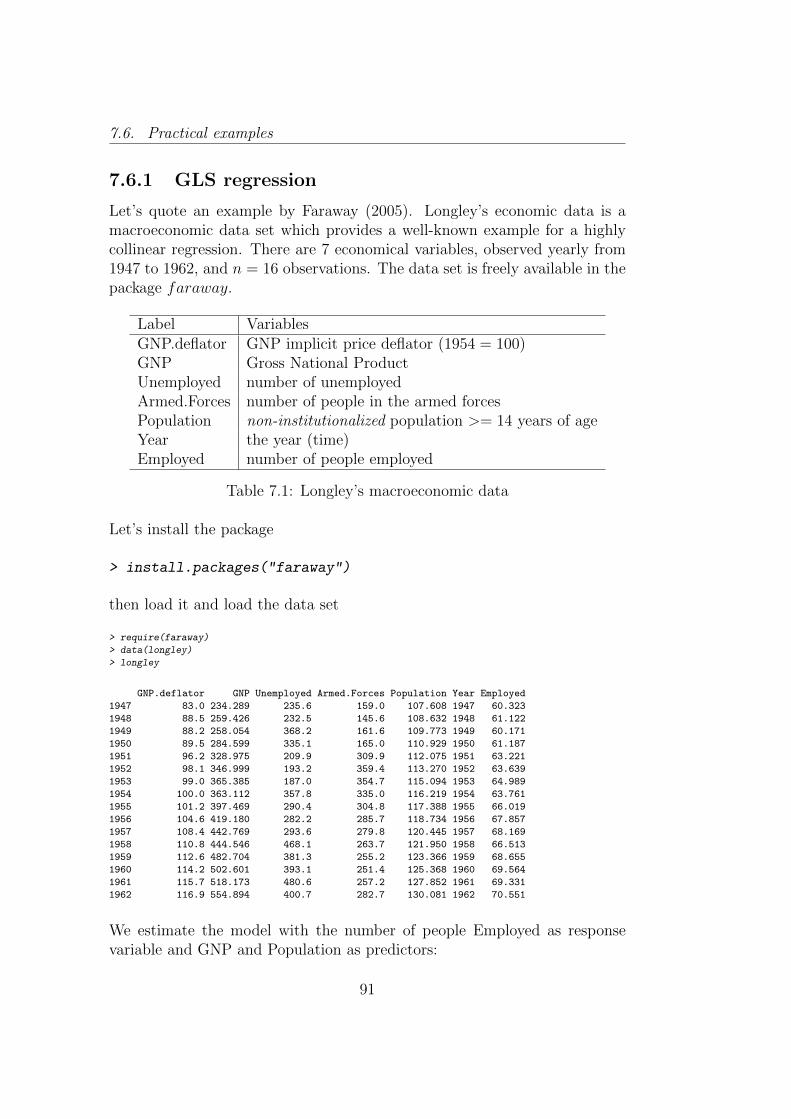

7.6.1 GLS regression . . . . . . . . . . . . . . . . . . . . . . 91

VI

Contents

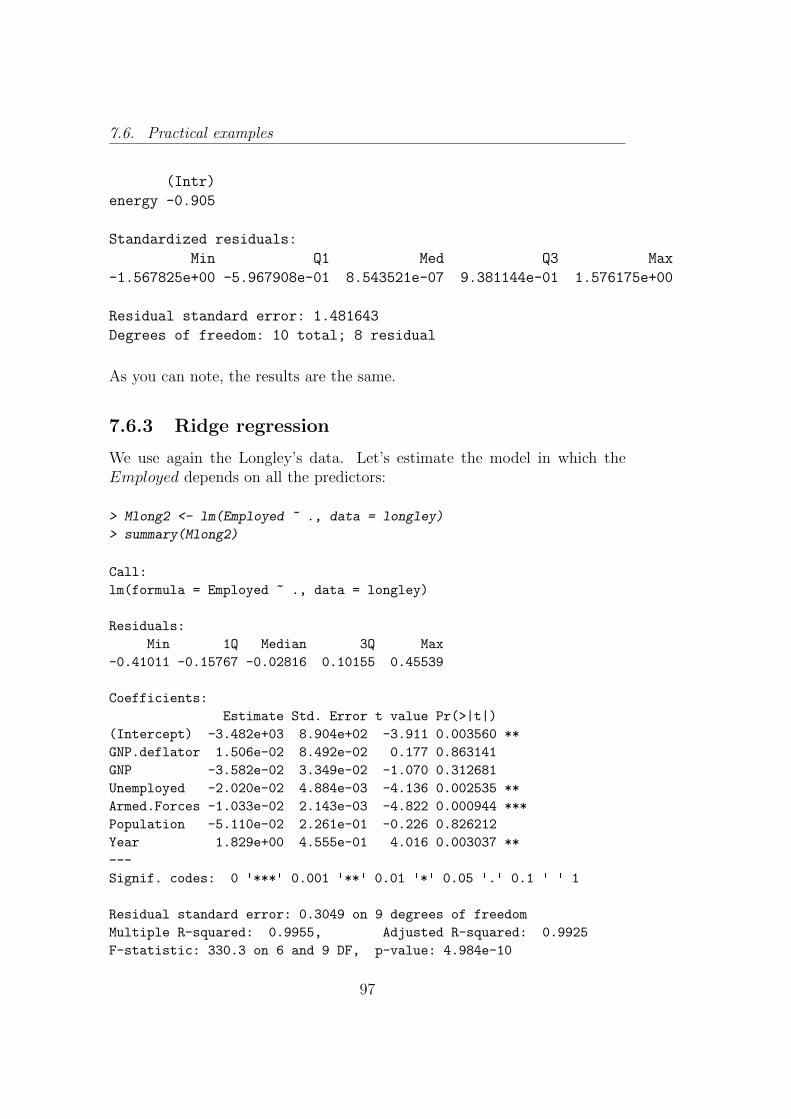

7.6.2 WLS regression . . . . . . . . . . . . . . . . . . . . . . 947.6.3 Ridge regression . . . . . . . . . . . . . . . . . . . . . . 97

7.7 Principal Component Regression . . . . . . . . . . . . . . . . . 104

Categorical predictors and Analysis of Variance 107

8 Categorical predictors and ANOVA 1078.1 Categorical predictors . . . . . . . . . . . . . . . . . . . . . . 107

8.1.1 Multiple categories . . . . . . . . . . . . . . . . . . . . 1158.2 Analysis Of Variance . . . . . . . . . . . . . . . . . . . . . . . 115

8.2.1 One way ANOVA . . . . . . . . . . . . . . . . . . . . . 1168.2.2 Multiple comparisons . . . . . . . . . . . . . . . . . . . 1208.2.3 Regression approach . . . . . . . . . . . . . . . . . . . 121

8.3 Two way ANOVA . . . . . . . . . . . . . . . . . . . . . . . . . 1228.3.1 Balanced two way ANOVA: multiple regression approach1288.3.2 ANOVA: considerations . . . . . . . . . . . . . . . . . 130

8.4 Practical examples . . . . . . . . . . . . . . . . . . . . . . . . 1328.4.1 Regression with categorical predictors . . . . . . . . . . 1328.4.2 One way ANOVA . . . . . . . . . . . . . . . . . . . . . 1408.4.3 Two way ANOVA . . . . . . . . . . . . . . . . . . . . . 144

VII

Chapter 1

Regression model: introductionand assumptions

1.1 Regression analysis: introduction, defini-

tions and notations

Regression analysis is used for explaining or modeling the relationship be-tween a single variable Y, called the response variable, or output variable, ordependent variable, and one or more predictor variables, or input variables,or independent variables or explanatory variables, X1, . . . ,Xp.The data matrix is assumed to be derived from a random sample of n obser-vations (xi1, xi2, . . . , xip, yi), i = 1, . . . , n or, equivalently, an n× (p+ 1) datamatrix.When p = 1, the model is called simple regression; when p > 1 the modelis called multiple regression or sometimes multivariate regression. It can bethe case then there are more than one Y: in this case the model is calledmultivariate multiple regression.The response variable must be continuous as well as the explanatory variablescan be continuous, discrete or categorical. It is possible to extend the linearregression model to response categorical variables through the GeneralizedLinear Models (GLM): probably you will study GLM in the future.Let’s define some notations and definitions.

Let n be the sample size;

Let p denote the number of predictors;

Let Y = (Y1, Y2, . . . , Yn)T be the vector of the dependent variables.

Regression model: introduction and assumptions

Let y = (y1, y2, . . . , yn)T be the vector of the sample extractions fromY.

Let X be the n× (p+ 1) matrix of the predictors.

Let ε = (ε1, ε2, . . . , εn)T be the vector of the error random variables εi.

Let e = (e1, e2, . . . , en)T be the vector of the sample extractions fromε.

Let β be the vector of the (p+1) parameters to be estimated β0, β1, . . . , βp.

The linear regression model is

Y = Xβ + ε,

or, equivalently,Y = β0 + β1x1 + . . .+ βpxp + ε.

1.2 Assumptions of the linear model

The relationship between Y and the (p+1) variables is assumed to be linear.This relationship cannot be modified because the parameters are assumedfixed. The linear model is:

Yi = β0 + β1xi1 + β2xi2 + . . .+ βpxip + εi

in which the εi, i = 1, . . . , n are values of the error random variable ε, mu-tually independent and identically distributed, E(εi) = 0, var(εi) = σ2. Inother words, the error random variable has null expectation and has constantvariance (homoscedasticity).The distribution of ε is independent of the joint distribution ofX1, X2, . . . , Xp,from which it follows that E[Y|X1, X2, . . . , Xp] = β0+β1X1+β2X2+. . .+βpXp

and var[Y|X1, X2, . . . , Xp] = σ2.Finally, the unknown parameters β0, β1, , . . . , βp are constants. The modelis linear in the parameters, the predictors do not have to be linear.

Of course, in real problems we deal with sample observations. Once therandom sample has been extracted, we have the observed values y sampledfrom Y. Hence, on the observed sample, we have

y = Xβ + e,

2

1.2. Assumptions of the linear model

in which the vector e contains the sample extractions from ε. Note that if weknow the β parameters, than e is perfectly identifiable because e = y−Xβ.

The regression equation in matrix notation is written as:

y = Xβ + e (1.1)

yn×1 =

y1y2...yn

Xn×(p+1) =

1 x11 . . . x1,p1 x21 . . . x2,p...

......

...1 xn1 . . . xn,p

β(p+1)×1 =

β0β1...βp

en×1 =

e1e2...en

The X matrix incorporates a column of ones to include the intercept term(now it should be clear the meaning of the notation in which the predictorsare said to be p + 1: p predictors + the intercept). Let’s see the (classical)assumption of the regression model.

Assumption 1: linearity

Linear regression requires the relationship between the independent and de-pendent variables to be linear. It means that this assumption imposes that

Y = Xβ + ε

.

Assumption 2: the expectation of the random error term is equalto zero

E[ε] =

E[ε1]...

E[εn]

=

0...0

.This assumption implies that E[Y] = Xβ because

E[Y] = E[Xβ + ε] = E[Xβ] + E[ε] = Xβ.

The average values of the random variables that generate the observed valuesof the dependent variable y lie along the regression hyperplane.

3

Regression model: introduction and assumptions

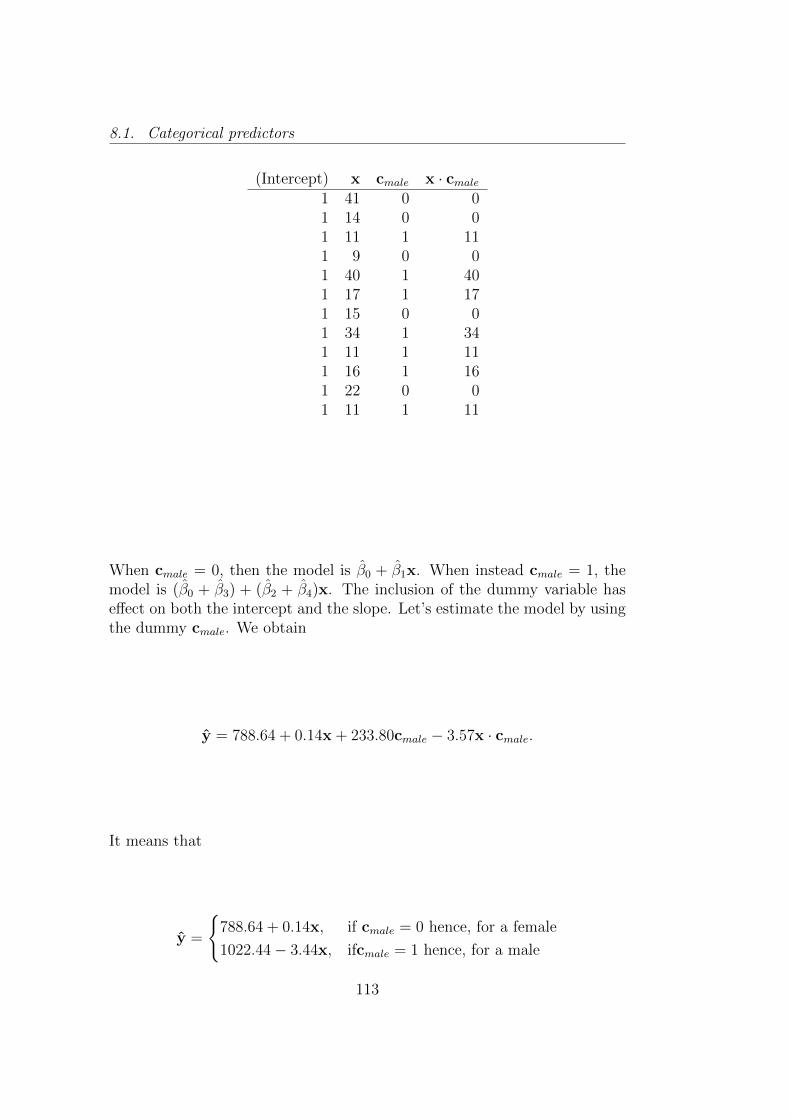

Figure 1.1: Regression hyperplane. the response variable (Album sales) isrepresented on the vertical axis. On the horizonal axes are represented thetwo predictors: Advertising budget and Airplay. The dots are the observedvalues. The regression hyperplane is highlighted in gray with blue countour

Assumption 3: Homoscedasticity and incorrelation between ran-dom terms

The variance of each error term is constant and it is equal to σ2, furthermorecov(εi, εj) = 0 ∀i 6= j.

var[ε] = E[εεT ] = σ2I, namely

4

1.2. Assumptions of the linear model

var[ε] = E[εεT ]− E[ε]E[εT ]

= E[εεT ]

=

E[ε1ε1] E[ε1ε2] . . . E[ε1εn]

E[ε2ε1] E[ε2ε2] . . . E[ε2εn]...

.... . .

...

E[εnε1] E[εnε2] . . . E[εnεn]

=

σ2 0 . . . 00 σ2 . . . 0...

.... . .

...0 0 . . . σ2

.

Assumption 4: no information from X can help to understand thenature of ε

When we say that the nature of the error term cannot be explained by theknowledge of the predictors, we assume that

E[ε|X] = 0

Assumption 5: the X matrix is deterministic, not stochastic

Assumption 6: the rank of the X matrix is equal to p+ 1

By saying the X must be a full-rank matrix, it is clear that the samplesize n must be less of equal to p + 1. Moreover, the independent variablesXj, j = 1, . . . , p are supposed to be linearly independent, hence they cannotbe expressed as a linear combination of the others. If the linearly indepen-dence of the predictors is not assumed the model is not identifiable.

Assumption 7: the elements of the (p+ 1)1 vector β and the scalarσ are fixed unknown numbers with σ > 0

Suppose to deal with a random sample, starting from the observed y and Xthe goal is to obtain the estimate β of β. The model to be estimated is

yi = Xiβ + ei, i = 1, . . . , n ,

where ei = yi − yi is called residual, with yi = Xiβ. We can resume theexpressed concepts in this way (Piccolo, 2010, chapter XXIII).

5

Regression model: introduction and assumptions

Y = Xβ + ε ⇒ ε = Y −Xβ Teoretical model

y = Xβ + e ⇒ e = y −Xβ General model

y = Xβ ⇒ e = y −Xβ Estimated model

Remember: the vector ε contains the error random variables εi; the vector e,given any arbitrary vector β, contains the realizations of the random variablesεi; the vector e contains the residuals of the model after the estimate of β,that is denoted with β.

6

Chapter 2

Model parameters estimate

2.1 Parameters estimate: ordinary least squares

Let y = Xβ + e be the model. The parameter to be estimated is the vectorof the regression coefficients

β = β0, β1, . . . , βp.

Least squares procedure determines the β vector in such a way that the sumof squared errors are minimized:

n∑i=1

e2i =n∑i=1

(yi − β0 − β1x1i − · · · − βpxpi)

=n∑i=1

(yi −Xiβ)2

= eTe

= (y −Xβ)T (y −Xβ)

We look for β for which f(β) = (y −Xβ)T (y −Xβ) = min. Let’s expandthis product:

f(β) = yTy − βTXTy − yTXβ + βTXTXβ

= yTy − 2βTXTy + βTXTXβ

The function β has scalar values, being β a column vector of length p + 1.The terms βTXTy and yTXβ are equal (two equal scalars), then they can

Model parameters estimate

be summarized with 2βTXTy. The term βTXTXβ is a quadratic form inthe elements of β. Differentiating with respect to f(β) we have

δf(β)

δβ= −2XTy + 2XTXβ,

and setting to zero

−2XTy + 2XTXβ = 0,

we obtain as a solution a vector β such that we obtain the so-called normalequations :

XTXβ = XTy.

Let’s give a look to the normal equations. We have

XTX =

n

∑ni=1 xi1

∑ni=1 xi2 · · ·

∑ni=1 xip∑n

i=1 xi1∑n

i=1 x2i1

∑ni=1 xi1xi2 · · ·

∑ni=1 xi1xip∑n

i=1 xi2∑n

i=1 xi1xi2∑n

i=1 x2i2 · · ·

∑ni=1 xi2xip

......

......

...∑ni=1 xip

∑ni=1 xi1xip

∑ni=1 xi2xip · · ·

∑ni=1 x

2ip

.

As it can be seen, XTX is a (p + 1)× (p + 1) symmetric matrix, sometimescalled sum of squares and cross-product matrix. The diagonal elements con-tain the sum of squares of the elements in each column of X. The off-diagonalelements contain the cross products between the columns of X.The vector XTy is formed by these elements:

XTy =

∑ni=1 yi∑n

i=1 xi1yi∑ni=1 xi2yi

...∑ni=1 xipyi

.

The jth element of XTy contains the product of the vectors xj and y, hencethe vector XTy is a vector of length p + 1 containing the p + 1 productsbetween the matrix X and the vector y.

Provided that the XTX matrix is invertible, the least squares estimate of βis

8

2.2. Properties of OLS estimates

β = (XTX)−1XTy.

Of course, the solution β depends on the observed values y, which are ran-domly drawn samples from the random variable Y. Suppose to extract allthe possible samples of size n from Y: as the random sample varies, theestimates β vary too, being extractions of the Least Squares Estimator B:

B = (XTX)−1XTY.

2.2 Properties of OLS estimates

If the assumptions of the linear regression models are verified, the OLS (Or-dinary Least Squares) estimator is said to be a BLUE estimator (Best LinearUnbiased Estimator). In other words, within the class of all the unbiased lin-ear estimators, the OLS returns the estimator with minimum variance (best).This statement is formally proved with the Gauss-Markov theorem.

2.2.1 Gauss-Markov theorem

The estimator is linear.The estimator B can be expressed in a different way:

B = (XTX)−1XTY

= (XTX)−1XT (Xβ + ε)

= (XTX)−1XTXβ + (XTX)−1XTε

= β + (XTX)−1XTε

= β + Aε

= AY,

where A = (XTX)−1XT and AAT = (XTX)−1. The estimator is linearbecause B = AY, then it is linear combinations of the random variableY.

The estimator is unbiased.The assumption 1 (linearity) implies that B can be expressed as β+Aε(see the point above). Then from assumptions 2 (Average of errorsequal to zero), 4 (deterministic X) and 6 (Constant parameters) itfollows that

E(B) = β + (XTX)−1XT E(ε) = β

9

Model parameters estimate

The estimator is the best within the class of linear and unbiased esti-mators.The first thing to do is determine the variance of B. From assumption3 (Homoscedasticity) we know that E(εεT ) = σ2I. Hence (by recallingthat we can express B = β + (XTX)−1XTε)

var(B) = E[(β − β)(β − β)T ]

= E[((XTX)−1XTε)((XTX)−1XTε)T ]

= E[(XTX)−1XTεεTX(XTX)−1]

= (XTX)−1XT E[εεT ]X(XTX)−1

= (XTX)−1XT (σ2I)X(XTX)−1

= (σ2I)(XTX)−1XTX(XTX)−1

= σ2(XTX)−1

Result 1: var(B) = σ2(XTX)−1.

Suppose that Bo is another linear unbiased estimator for β. As it is alinear estimator, we call C a generic ((p+1)×n) matrix that substitutesA = (XTX)−1XT . We define Bo = CY.It is assumed that the estimator Bo must be unbiased. By recallingthat (first assumption) Y = Xβ + ε, it must be that

E[Bo] = E[CY] = E[CXβ + Cε] = β,

which is true if and only if CX = I.Let’s introduce the matrix D = C − (XTX)−1XT . It allows first toexpress C = D + (XTX)−1XT , and then to see thatDY = CY − (XTX)−1XTY = βo − β. It immediately follows that

10

2.3. Illustrative example, part 1

var(Bo) = σ2[(D + (XTX)−1XT )(D + (XTX)−1XT )T

]= σ2[DDT + DX(XTX)−1 +

+ (XTX)−1XTDT +

+ (XTX)−1XTX(XTX)−1]

= σ2[(XTX)−1 + DDT

]= var(B) + σ2(DDT )

Result 2: var(Bo) = var(B) + σ2(DDT ).

By combining the previous results 1 and 2, it can be seen that

var(Bo)− var(B) = σ2(DDT ),

which is positive semidefinite matrix (i.e., it has non-negative values onthe main diagonal).It is clear that σ2(DDT ) = 0 if and only if D = 0. It happens onlywhen C = (XTX)−1XT producing Bo ≡ B.The conclusion is that, under the assumptions of the linear regressionmodel, the OLS estimator B gives the minimal variance in the class ofunbiased and linear estimators. In a few words, the OLS estimator isa BLUE estimator.

2.3 Illustrative example, part 1

2.3.1 A toy example

Computations by hand

As illustrative example, consider first a toy example in which the computa-tions can be made (if you want) by hand. Suppose to have the following data:

11

Model parameters estimate

y =

64.0561.6468.4375.8586.7751.0377.3852.2751.1284.13

; X =

16.11 714.72 316.02 415.05 416.58 415.22 813.95 314.71 915.48 913.78 3

.

We have n = 10, p = 2. The first to do is add a column of one to the Xmatrix, obtaining

X =

1 16.11 71 14.72 31 16.02 41 15.05 41 16.58 41 15.22 81 13.95 31 14.71 91 15.48 91 13.78 3

.

Let’s compute the XTX matrix:

XTX =

10.00 151.62 54.00151.62 2306.31 824.1754.00 824.17 350.00

.By calling the columns of X const, X1 and X2 respectively, we can see thaton the diagonal we have exactly

∑10i=1 const

2i = n = 10,

∑10i=1X

2i1 = 2306.31

and∑10

i=1X22i = 350.00.

On the off-diagonal elements we have the cross-products∑10

i=1 constiX1i =151.62,

∑10i=1 constiX2i = 54.00 and

∑10i=1X1iX2i = 824.17 (check by your-

self).The determinant of XTX is equal to 4086.68, the cofactor matrix is

(XTX)c =

127946.15 −8560.97 418.94−8560.97 584.00 −54.36

418.94 −54.36 75.04

, yielding to

12

2.4. Sum of squares

(XTX)−1 =

31.31 −2.09 0.10−2.09 0.14 −0.01

0.10 −0.01 0.02

.Now we have to compute the (3× 1) vector XTy:

XTy =

672.6710191.133380.77

.The regression coefficients are computed in this way:

β =

31.31 −2.09 0.10−2.09 0.14 −0.01

0.10 −0.01 0.02

× 672.67

10191.133380.77

=

57.762.24−4.52

In summary, we have β0 = 57.76, β1 = 2.24 and β2 = −4.52.

2.4 Sum of squares

The results obtained with the least squares allow to separate the vector ofobservations y in two parts, the fitted values y = Xβ and the residuals e:

y = Xβ + e = y + e

Since β = (XTX)−1XTy, it follows that:

y = Xβ

= X(XTX)−1XTy

= Hy

The matrix H = X(XTX)−1XT is symmetric (H = HT ), idempotent (H ×H = H2 = H) and is called hat matrix, since it ”puts the hat on the y”,namely provides the vector of the fitted values in the regression of y on X.The residuals from the fitted models are

e = y − y = y −Xβ = (I−H)y.

13

Model parameters estimate

The sum of squared residuals can be written as

eT e =n∑i=1

(yi − yi)2 = (y − y)T (y − y)

= (y −Xβ)T (y −Xβ)

= (yTy − yTXβ − βTXTy + βTXTXβ)

= (yTy − βTXTy)

= yT (I−H)y

This quantity is called the error or (residual) sum of squares and is denotedby SSE.

The total sum of squares is equal to

n∑i=1

(yi − y)2 = yTy − ny2

The total sum of squares, denoted by SST, it indicates the total variation iny that is to be explained by X.

The regression sum of squares is defined as

n∑i=1

(yi − y)2 = βTXTy − ny2 = yTHy − ny2.

It is denoted by SSR.

The ratio of SSR to SST represents the proportion of the total variation iny explained by the regression model. The quantity

R2 =SSR

SST= 1− SSE

SST

is called coefficient of multiple determination. It is sensitive to the magni-tudes of n and p especially in small samples. In the extreme case if n = (p+1)the model will fit the data exactly. In any case, R2 is a measure that doesnot decrease when the number of predictors p increases.In order to give a better measure of goodness of fit, a penalty function canbe employed to reflect the number of explanatory variables used. Using thispenalty function the adjusted R2 is given by

R′2 = 1−

(n− 1

n− p− 1

)(1−R2) = 1− SSE/(n− p− 1)

SST/(n− 1).

14

2.4. Sum of squares

The adjusted R2 changes the ratio SSE/SST to the ratio of SSE/(n−p−1)(an unbiased estimator of σ2

ε , as it will be clear later), and SST/(n− 1) (anunbiased estimator of σ2

Y , as it should be already known).

2.4.1 Illustrative example, part 2

Let’s compute the sum of squares of the model built for the toy example.Remember that the estimated regression coefficients were β0 = 57.76, β1 =2.24 and β2 = −4.52. We then obtain

y = Xβ =

1 16.11 71 14.72 31 16.02 41 15.05 41 16.58 41 15.22 81 13.95 31 14.71 91 15.48 91 13.78 3

×

57.762.24−4.52

=

62.1577.1275.5173.3376.7555.6575.4150.0051.7275.03

.

The residuals are

e = y − y =

64.0561.6468.4375.8586.7751.0377.3852.2751.1284.13

−

62.1577.1275.5173.3376.7555.6575.4150.0051.7275.03

=

1.89−15.49−7.08

2.5210.02−4.62

1.972.27−0.60

9.10

We are ready to compute the sum of squares. We have

SSE =10∑i=1

e2i

= eT e

= 513.80

15

Model parameters estimate

In matrix form:

SSE = eT e

=[

1.89 −15.49 −7.08 2.52 10.02 −4.62 1.97 2.27 −0.60 9.10]×

1.89−15.49−7.08

2.5210.02−4.62

1.972.27−0.60

9.10

= 513.80

The mean value of y is y = 67.27. The total sum of square is then

SST =10∑i=1

(yi − y)2

= yTy − ny2

= 1633.14

In matrix form:

SST = yTy − ny2

=[

64.05 61.64 68.43 75.85 86.77 51.03 77.38 52.27 51.12 84.13]×

64.0561.6468.4375.8586.7751.0377.3852.2751.1284.13

− 10× 67.272

= 1633.14

SSR is then equal to SST − SSE = 1633.14− 513.80 = 1119.34. Indeed wehave

∑10i=1(yi − y)2 = 1119.34.

We are ready to compute the coefficients of multiple determination:

16

2.4. Sum of squares

R2 =SSR

SST=

1119.34

1633.14= 0.69,

R′2 = 1− SSE/(n− p− 1)

SST/(n− 1)= 1− 513.80/(ntoy − ptoy − 1)

1633.14/(ntoy − 1)= 0.60.

17

Chapter 3

Statistical inference

3.1 A further assumption on the error term

We can add a further assumption to the classical assumptions of the lin-ear regression model: the errors are independent and identically normallydistributed with mean 0 and variance σ2:

ε ∼ N (0, σ2I).

.

Since Y = Xβ+ ε, and given assumptions 5 (X has full rank) and 7 (vectorβ and scalar σ are unknown but fixed), it follows that:

var(Y) = var(Xβ + ε) = var(ε) = σ2I,

meaning that

Y ∼ N (Xβ, σ2I).

The assumption of normality of the error term has the consequence thatthe parameters can be estimate with the maximum likelihood method. Theassumption that the covariance matrix of ε is diagonal implies that the entriesof ε are mutually independent (as already known). Moreover, they all havea normal distribution with mean 0 and variance σ2.The conditional probability density function of the dependent variable is

f(yi|X) = (2πσ2)−(1/2)exp

(−1

2

(yi − xiβ)2

σ2

),

the likelihood function is

Statistical inference

L(β, σ2|y,X) =n∏i=1

(2πσ2)−(i/2)exp

(−1

2

(yi − xiβ)2

σ2

)

= (2πσ2)−(n/2)exp

(− 1

2σ2

n∑i=1

(yi − xiβ)2

).

The log-likelihood function is

log(L) = ln(L(β, σ2|y,X))

= −n2ln(2π)− n

2ln(σ2)− 1

2σ2

n∑i=1

(yi − xiβ)2

Remember that∑n

i=1(yi − xiβ)2 = (y − Xβ)T (y − Xβ), namely the sumof the squared errors. The maximum likelihood estimator for the regressioncoefficients is

β = (XTX)−1XTy.

Moreover, the maximum likelihood estimator of the variance is

σ2 =1

n

n∑i=1

(yi − xiβ)2 =1

neT e.

For the regression coefficients, the (mathematical) results are the same: theOLS estimators and the ML estimators have the same formulation. For thevariance of the error terms, the ML estimate returns the unadjusted samplevariance of the residuals e.Why it is important the distributional assumption? It is necessary to as-sume a distributional form for the errors ε to make confidence intervals orperform hypothesis tests. Moreover, ML estimators are BAN estimators:Best Asymptotically Normal.Assuming that ε ∼ N (0, σ2I), since y = Xβ + e we have that

y ∼ N(Xβ, σ2I

).

Then, as linear combinations of normally distributed values are also normal,we find that

B ∼ N(β, σ2(XTX)−1

),

namely

βj ∼ N(βj, σ

2(XTX)−1(jj)

),

20

3.1. A further assumption on the error term

where with (XTX)−1(jj) we indicate the element at the intersection of the j-th

row and the j-th column of the matrix (XTX)−1 (the jth predictor).In a few words, if the errors are normally distributed, then also Y and B arenormally distributed.

3.1.1 Statistical inference

As in practical situations the variance is of course unknown, we need toestimate it. After some computations, one can show that

E

(n∑i=1

e2i

)= E

(eT e)

= σ2(n− p− 1).

In order to show this result, remember that we defined the hat matrix as H =X(XTX)−1XT . Let’s define now the matrix M = I −H. The matrix M has thefollowing properties:

M = MT = MM = MTM.

Moreover, M has rank equal to n − p − 1, as well as tr(M) = n − p − 1. We canwrite the vector of the random variable residuals E = Y −XB as

E = Y −XB = Y −X(XTX)−1XTY = (I−H)Y = MY.

We are able to express the r.v. residuals through the r.v. error:

E = MY = M(Xβ + ε) = MXβ + Mε = Mε.

Hence,

E[ET E] = E[(Mε)T (Mε)]

= E[(εTMTMε)]

= E[tr(εTMTMε)]

= σ2tr(MTM)

= σ2tr(M)

= σ2(n− p− 1).

21

Statistical inference

The conclusion is that

s2 =eT e

n− p− 1=

∑ni=1 e

2i

n− p− 1

is an unbiased estimator of σ2 because

E[S2] =σ2(n− p− 1)

n− p− 1= σ2.

The model has n− p− 1 degrees of freedom. The square root of s2 is namedstandard error of regression and can be interpreted as the average squareddeviation of the dependent variable values y around the regression hyperplan.

3.1.2 Inference for the regression coefficients

Inferences can be made for the individual regression coefficient βj to test thenull hypothesis H0 : βj = β∗j using the statistic

t =(βj − β∗j )√s2(XTX)−1(jj)

,

which, if the null hypothesis is true, has a t distribution with n−p−1 degreesof freedom. Usually, β∗j = 0.A 100(1−a)% confidence interval for βj can be obtained from the expression

βj ± tα/2,(n−p−1)√s2(XtX)−1(jj).

Keep in mind that the inferences are conditional on the other explanatoryvariables being included in the model. The addition of an explanatory vari-able to the model usually causes the regression coefficients to change.

We will denote ESβj as√s2(XtX)−1(jj).

3.1.3 Inference for the overall model

The overall goodness of fit of the model can be evaluated using the F -test(or ANOVA test on the regression). Under the null hypothesis

H0 : β1 = β2 = . . . = βp = 0,

the statistic

22

3.2. Illustrative example, part 3

F =(SSR/p)

(SSE/(n− p− 1))=MSR

MSE

has a F distribution with p degrees of freedom in the numerator and (n−p−1)degrees of freedom in the denominator. Usually the statistic for this test issummarized in an ANOVA table as the one shown below:

SourceDegrees

of freedom

Sumof

SquaresMean Square F

Regression p SSR MSR=SSR/p MSR/MSEError (n− p− 1) SSE MSE=SSE/(n− p− 1)Total (n− 1) SST

3.2 Illustrative example, part 3

Remember the toy example introduced in Chapters 2.3.1 and 2.4.1. Wecomputed the following quantities:

(XTX)−1 =

31.31 −2.09 0.10−2.09 0.14 −0.01

0.10 −0.01 0.02

,β0 = 57.76; β1 = 2.24; β2 = −4.52

SST = 1633.14; SSE = 513.80; SSR = 1119.34.

First we can compute the residual variance:

s2 =SSE

n− p− 1=

513.80

7= 73.40,

from which we get the standard error of the regression

s =√s2 =

√73.40 = 8.57.

The sample covariance matrix is

23

Statistical inference

s2(XTX)−1 = 73.40×

31.31 −2.09 0.10−2.09 0.14 −0.01

0.10 −0.01 0.02

=

2297.99 −153.76 7.52−153.76 10.49 −0.98

7.52 −0.98 1.35

.By taking the square root of the diagonal elements of the covariance matrix,we obtain the standard error of each regression coefficients:

ESβ0 =√

2297.99 = 47.94; ESβ1 =√

10.49 = 3.24; ESβ2 =√

1.35 = 1.16

We are ready to compute the t statistics t = βj/ESbetaj :

tintercept =57.76

47.94= 1.20; tX1 =

2.24

3.24= 0.69; tX2 =

−4.52

1.16= −3.89

We know that the degrees of freedom are (n − p − 1) = (10 − 2 − 1) = 7,so these ratios are distributed as a Student distribution with 7 degrees offreedom. We perform a two tails test by setting the probability of the type-1error α = 0.05. The critical value for a t distribution with 7 df is equal to|2.365|. We can summarize the results in a table as the one displayed below:

Predictor Coefficient Standard error t-ratio Significant?Intercept 57.76 47.94 1.20 no

X1 2.24 3.24 0.69 noX2 -4.52 1.16 -3.89 yes

As it can be seen, the intercept as well as the regression coefficient of the X1variable are not statistically significant.We also have the necessary information to perform the test on the over-all model (F-test). We know that SSE = 513.80, SST = 1633.14 andSSR = 1119.34. Moreover n = 10 and p = 2. We can build the Anova table:

SourceDegrees

of freedom

Sumof

SquaresMean Square F

Regression p = 2 SSR=1119.34 MSR=1119.34/2 = 559.67 MSR/MSE=7.63Error (n− p− 1) = 7 SSE=513.80 MSE=513.80/7 = 73.40Total (n− 1) = 9 SST=1633.14

24

3.3. Predictions

The critical value of a F distribution with 2 degrees of freedom in the nu-merator and 7 degrees of freedom in the denominator, by setting α = 0.05,is equal to 4.737. Under the null hypothesis we have:

H0 = βj = 0 ∀j = 1, . . . , p.

We cannot accept this hypothesis: it means that there is at least one regres-sion coefficient statistically different from zero.

3.3 Prediction, interval predictions and infer-

ence for the reduced (nested) model

Prediction

The least squares method leads to estimating the coefficients as:

β = (XTX)−1XTy.

By using the parameter estimations it is possible to write the estimatedregression line:

yi = β0 + β1xi1 + . . .+ βpxip = xiβ.

Suppose to have a new observed value x0, namely a row vector with p columns(the same variables of X). To obtain a prediction y0 for x0, we compute

y0 = β0 + β1x01 + . . .+ βpx0p = x0β.

What is the meaning of y0? Remember that yi = yi + ei, hence y0 = E[y|x0].

Intervals

Confidence intervals for Y or Y = E[Y], at specific values of X = x0, aregenerally called prediction intervals. First, let’s introduce the variance of y.By remembering that the hat matrix is idempotent (Chapter 2.4), we obtain

var(y) = var(Xβ)

= var(X(XTX)−1XTy)

=(X(XTX)−1XT

)s2

= s2H,

25

Statistical inference

hence var(yi) = s2(xi(XTX)−1xTi ).

When the intervals are computed for E[Y] they are sometimes simply calledconfidence intervals, and they reflect the uncertainty around the mean pre-dictions.The intervals for Y are sometimes called just prediction intervals, and giveuncertainty around single values.A prediction interval will be generally much wider than a confidence inter-val for the same value, reflecting the fact that individuals at X = x0 aredistributed around the regression line with variance σ2.

0

50

100

5 10 15 20 25

speed

dist

Figure 3.1: Regression line, confidence interval and prediction interval for asimple regression of the speed of cars (Y) and the distances taken to stop(X). In blue there is the estimated regression line in blue. Confidence intervalbands (for E[Y]) are reported in the gray area. Prediction interval bands (forY) are reported in red. Note that the red bands include the gray area.

The 100(1− α)% confidence interval for E[Y] at X = x0 is given by

y0 ± tα/2;(n−p−1)√s2(x0(XTX)−1xT0 )

The 100(1− α)% prediction interval for Y at X = x0 is given by

y0 ± tα/2;(n−p−1)√s2(1 + x0(XTX)−1xT0 ).

26

3.3. Predictions

This result is due to the fact that, as y0 is unknown, the total varianceis s2 + var(y0). Of course, if there is more than one new observation, we

must take in account the diagonal elements of√s2(1 + X0(XTX)−1XT

0 ) and√s2(X0(XTX)−1XT

0 ).

Note that we consider the new individual as a row vector x0 =[1, x01, . . . , x0p]. For this reason we use the notation X0(XX)−1XT

0 ). Ingeneral, we should consider the new observation as x0 = [1, x01, . . . , x0p]

T ,hence usually the notation is (XT

0 (XX)−1X0).

Inference for the reduced model

Usually in a multiple regression setting there will be at least some X variablesthat are related to y, hence the F-test of goodness of fit usually results inrejection of H0.

A useful test is one that allows the evaluation of a subset of the explanatoryvariables relative to a larger set.Suppose to use a subset of q variables, and test the null hypothesis

H0 : β1 = β2, . . . , βq = 0 with q < p.

The model with all the p explanatory variables is called the full model, whilethe model that holds under H0 with (p − q) explanatory variables is calledthe reduced model :

y = β0 + β(q+1) + β(q+2) + . . .+ βp + e.

If the null hypothesis H0 : β1 = β2, . . . , βq = 0 is true, then the statistic

F =(SSR− SSRR)/q

SSE/(n− p− 1)=

(SSER − SSE)/q

SSE/(n− p− 1)

has an F distribution with q and (n − p − 1) degrees of freedom. Thistest is often called partial F test. In the above formulation, SSRR and SSER

represent the regression and the residual sum of squares of the reduced model,respectively.The same statistic can be written in terms of R2 and R2

R, where R2R is the

coefficient of multiple determination of the reduced model:

F =(R2 −R2

R)/q

(1−R2)/(n− p− 1).

27

Statistical inference

This procedure helps to make a choice between two nested models estimatedon the same data (see, for example Chatterjee & Hadi, 2015). A set of modelsare said to be nested if they can be obtained from a larger model as specialcases. The test for these nested hypotheses involves a comparison of thegoodness of fit that is obtained when using the full model, to the goodness offit that results using the reduced model specified by the null hypothesis. Ifthe reduced model gives as good a fit as the full model, the null hypothesis,which defines the reduced model, is not rejected.

The rationale of the test is as follows:in the full model there are p+ 1 regression parameters to be estimated. Letus suppose that for the reduced model there are k distinct parameters. Weknow that SSR ≥ SSRR and SSER ≥ SSE because the additional parame-ters (variables) in the full model cannot increase the residual sum of squares(R2 is not decreasing when the number of predictor increases).The difference SSER − SSE represents the increase in the residual sum ofsquares due to fitting the reduced model. If this difference is large, the re-duced model is inadequate, and we tend to reject the null hypothesis. In ournotation, we used q to denote the subset of variables of the full model wewish to test their simultaneous equality to zero.If we denote with k the number of parameters estimated in the reduced model(hence, including the intercept), then q = (p+ 1− k).

The meaning of the partial F test is the following: can y be explainedadequately by fewer variables? An important goal in regression analysis isto arrive at adequate descriptions of observed phenomenon in terms of asfew meaningful variables as possible. This economy in description has twoadvantages:

it enables us to isolate the most important variables;

it provides us with a simpler description of the process studied, therebymaking it easier to understand the process.

The principle of parsimony is one of the important guiding principles inregression analysis. Probably, you will study many techniques of model se-lection and variable selection (stepwise regression, best subset selection, etc.)in studying other quantitative disciplines.

28

3.4. Illustrative example, part 4

3.4 Illustrative example, part 4

Consider the toy example introduced in section 2.3.1. Suppose to have a newobservation x0 = [15.18, 2]. Remember that

(XTX)−1 =

31.31 −2.09 0.10−2.09 0.14 −0.01

0.10 −0.01 0.02

, and β =

57.762.24−4.52

.Moreover, from Chapter 2.4.1 we know that SSE = 513.80, and from Section3.2 we know that s2 = 73.40 and the covariance matrix is 2297.99 −153.76 7.52

−153.76 10.49 −0.987.52 −0.98 1.35

.Hence, we can made the prediction:

y0 = x0β = β0 + β1x01 + β2x02

=[

1 15.18 2]×

57.762.24−4.52

= 57.76 + 2.24× 15.18 +−4.52× 2

= 82.66

Let’s determine both the confidence interval and the prediction interval. Firstwe set the confidence level to be, say, equal to 95% and determine the quantileof the t distribution with n− p− 1 = 7 degrees of freedom that leaves 2.5%probability on the tails. This value is equal to t0.025,7 = 2.36. Then wecompute the quantity, that we call C,

C = t0.025,7

√s2(x0(XTX)−1xt0)

= 2.36×

√√√√√73.40×

[ 1.00 15.18 2.00]×

2297.99 −153.76 7.52−153.76 10.49 −0.98

7.52 −0.98 1.35

× 1.00

15.182.00

= 11.35

The confidence interval for Y0 is then

29

Statistical inference

y0 lower bound upper bound82.66 82.66 - 11.35 = 71.31 82.66 + 11.35 = 94.01

To compute the prediction interval we must compute C in other way:

C = t0.025,7

√s2(1 + (x0(XTX)−1xt0))

= 2.36×

√√√√√73.40×

1 +

[ 1.00 15.18 2.00]×

2297.99 −153.76 7.52−153.76 10.49 −0.98

7.52 −0.98 1.35

× 1.00

15.182.00

= 23.22

The prediction interval for Y0 is then

y0 lower bound upper bound82.66 82.66 - 23.22 = 59.44 82.66 + 23.22 = 105.88

As you can see, the prediction interval, for the same point estimate, is widerthan the confidence interval.Inference for the reduced model will be seen in the next chapter.

30

Chapter 4

Linear regression: summaryexample 1

4.1 The R environment

In this chapter we try to practically see what we defined in the previouschapters. All the computations have been made in R environment (R Devel-opment Core Team, 2006). R is a language and environment for statisticalcomputing and graphics. Students can reproduce the reported examples bycopying and pasting the reported syntax. For an introduction to R, studentscan refer to Paradis (2010).

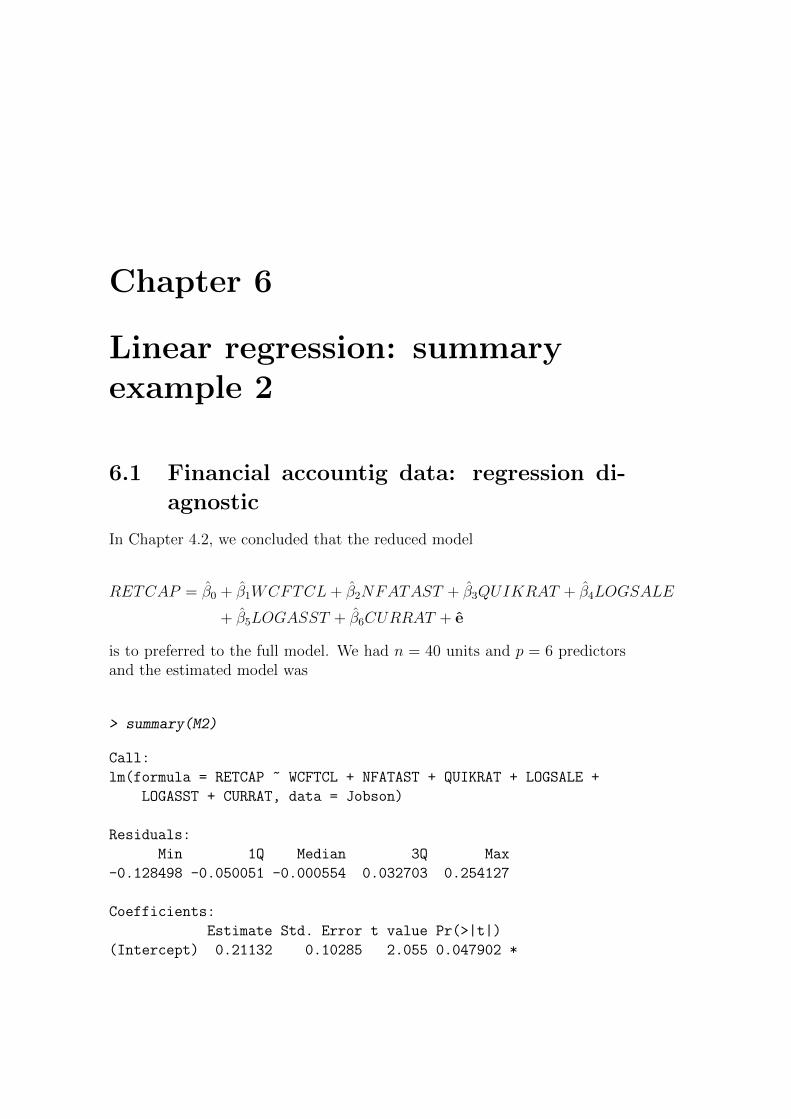

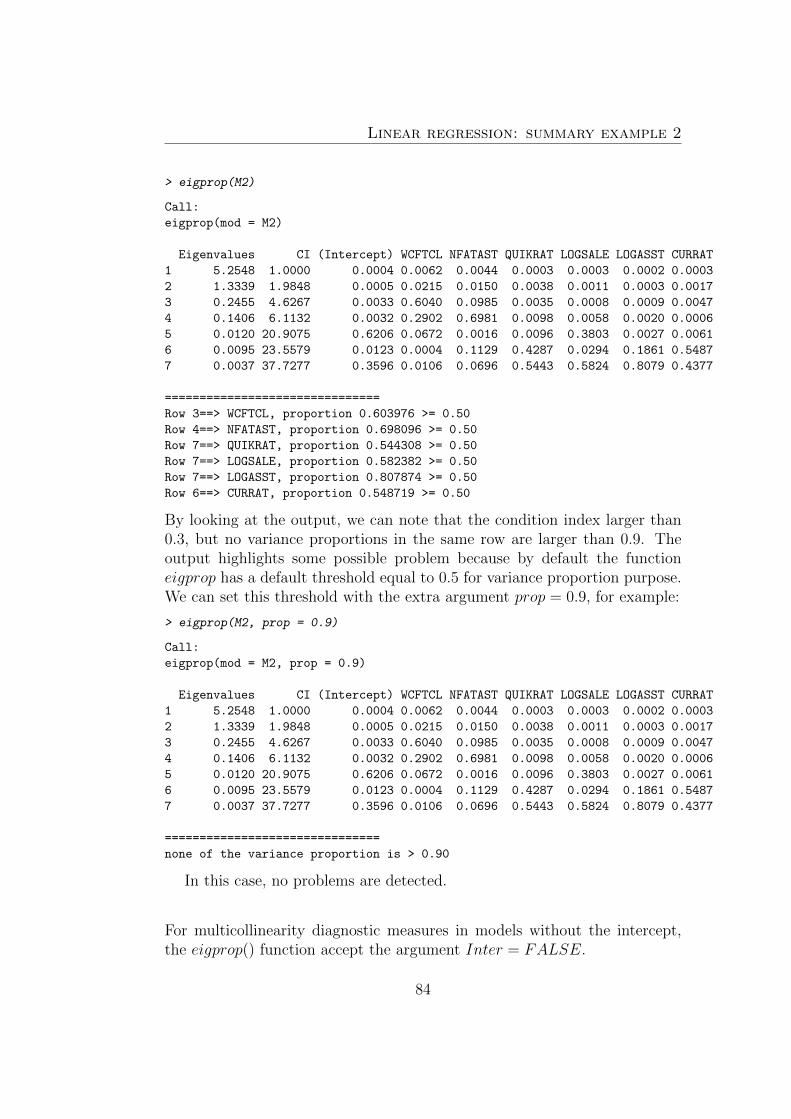

4.2 Financial accounting data

Financial accounting data (Jobson, 1991, p.221) contain a set of financialindicators for 40 companies in UK, as summarized in table 4.2. We assumethat the Return of capital employed (RETCAP ) depends on all the othervariables.Data can be accessed by downloading the file Jtab42.rda from http://

wpage.unina.it/antdambr/data/MPQE/. Once the file has been downloadedin the working directory, the data set can be loaded by typing

> load("Jtab42.rda")

Linear regression: summary example 1

Variable DefinitionRETCAP Return of capital employedWCFTDT Ratio of working capital flow to total debtLOGSALE Log to base 10 of total salesLOGASST Log to base 10 of total assetsCURRAT Current ratioQUICKRAT Quick ratioNFATAST Ratio of net fixed assets to total assetsFATTOT Gross fixed assets to total assetsPAYOUT Payout ratioWCFTCL Ratio of working capital flow to total current liabilitiesGEARRAT Gearing ratio (debt-equity ratio)CAPINT Capital intensity (ratio of total sales to total assets)INVTAST Ratio of total inventories to total assets

Table 4.1: Financial accounting data

Let’s give a look to the results first. The estimated regression coefficients are

Predictor Estimate(Intercept) 0.1881

GEARRAT -0.0404CAPINT -0.0141

WCFTDT 0.3056LOGSALE 0.1184LOGASST -0.0770CURRAT -0.2233

QUIKRAT 0.1767NFATAST -0.3700INVTAST 0.2506FATTOT -0.1010PAYOUT -0.0188WCFTCL 0.2151

Each βj should be interpreted as the expected change in y when a unitarychange is observed in xj while all other predictors are kept constant.The intercept is the expected mean value of y when all xj = 0.In this case each coefficient of an explanatory variable measures the impactof that variable on the dependent variable RETCAP, holding the othervariables fixed. For example, the impact of an increase in WCFTDT ofone unit is a change in RETCAP of 0.3056 units, assuming that the other

32

4.2. Financial accounting data

variables are held constant. Similarly an increase in CURRAT of one unitwill bring about a decrease in RETCAP of 0.2233 units, if all the other ex-planatory variables are held constant.

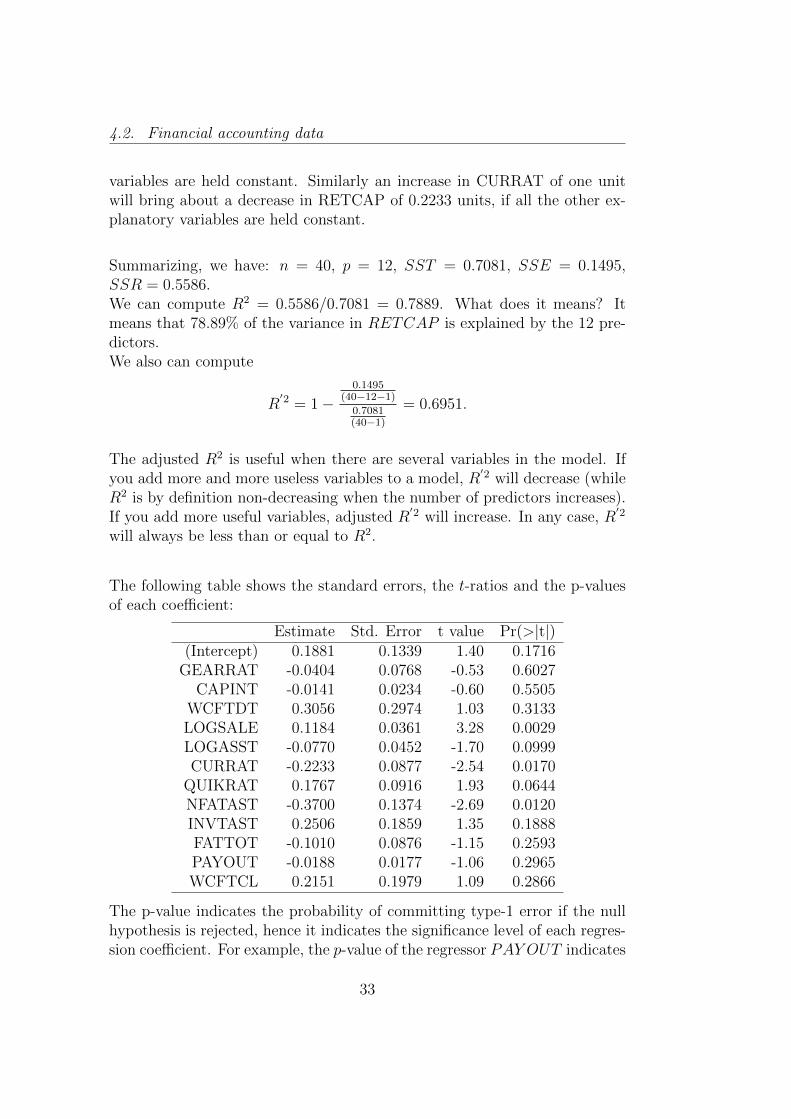

Summarizing, we have: n = 40, p = 12, SST = 0.7081, SSE = 0.1495,SSR = 0.5586.We can compute R2 = 0.5586/0.7081 = 0.7889. What does it means? Itmeans that 78.89% of the variance in RETCAP is explained by the 12 pre-dictors.We also can compute

R′2 = 1−

0.1495(40−12−1)

0.7081(40−1)

= 0.6951.

The adjusted R2 is useful when there are several variables in the model. Ifyou add more and more useless variables to a model, R

′2 will decrease (whileR2 is by definition non-decreasing when the number of predictors increases).If you add more useful variables, adjusted R

′2 will increase. In any case, R′2

will always be less than or equal to R2.

The following table shows the standard errors, the t-ratios and the p-valuesof each coefficient:

Estimate Std. Error t value Pr(>|t|)(Intercept) 0.1881 0.1339 1.40 0.1716

GEARRAT -0.0404 0.0768 -0.53 0.6027CAPINT -0.0141 0.0234 -0.60 0.5505

WCFTDT 0.3056 0.2974 1.03 0.3133LOGSALE 0.1184 0.0361 3.28 0.0029LOGASST -0.0770 0.0452 -1.70 0.0999CURRAT -0.2233 0.0877 -2.54 0.0170

QUIKRAT 0.1767 0.0916 1.93 0.0644NFATAST -0.3700 0.1374 -2.69 0.0120INVTAST 0.2506 0.1859 1.35 0.1888FATTOT -0.1010 0.0876 -1.15 0.2593PAYOUT -0.0188 0.0177 -1.06 0.2965WCFTCL 0.2151 0.1979 1.09 0.2866

The p-value indicates the probability of committing type-1 error if the nullhypothesis is rejected, hence it indicates the significance level of each regres-sion coefficient. For example, the p-value of the regressor PAY OUT indicates

33

Linear regression: summary example 1

that the risk of committing the type-1 error if we reject the null hypothesisis about 30%. So we cannot reject the null hypothesis.

The F-test for this model is summarized in the ANOVA table:

Source Df SS MS F-stat P-value1 Model 12 0.5587 0.0466 8.4075 <0.00012 Error 27 0.1495 0.00553 Total 39 0.7082

The p-value is smaller than 0.0001, then we reject the null hypothesis thatall the regression coefficients are equal to zero.

Inference on the reduced model

Suppose that the reduced model involves the following variables: WCFTCL,NFATAST, QUIKRAT, LOGSALE, LOGASST, CURRAT.The estimate parameters of the regression model for this subset of variablesis

Estimate Std. Error t value Pr(>|t|)(Intercept) 0.2113 0.1028 2.05 0.0479WCFTCL 0.4249 0.0587 7.24 0.0000NFATAST -0.5052 0.0747 -6.76 0.0000QUIKRAT 0.0834 0.0413 2.02 0.0518LOGSALE 0.0976 0.0251 3.90 0.0005LOGASST -0.0709 0.0323 -2.19 0.0354CURRAT -0.1221 0.0406 -3.01 0.0050

We have k = 7, R2R = 0.741, SSRR = 0.5247 (remember that with the

subscript R we refer to the measures for the reduced model). Remember thatR2 = 0.7889, SSR = 0.5586 and SSE = 0.1495. Hence we have

F =(0.5586− 0.5247)/6

0.1495/27=

(0.7889− 0.7410)/6

(1− 0.7889)/27= 1.0200

The p-value associated to the F statistic is equal to 0.4332. We cannotreject the null hypothesis. Hence, with respect to the reduced model, the

34

4.2. Financial accounting data

coefficients for GEARRAT, CAPINT, WCFTDT, FATTOT, PAYOUT andINVTAST are not significant. It means that the null hypothesis is

H0 : βGEARRAT = βCAPINT = βWCFTDT = βFATTOT = βPAY OUT = βINV TAST = 0,

or, alternatively,

H0 : Reduced model is adequate

Predictions, confidence and prediction intervals

Think about the reduced model. Suppose there are 10 observations for whichwe do not the values for the response variable.

LOGSALE LOGASST CURRAT QUIKRAT NFATAST WCFTCL1 4.42 4.27 1.78 0.96 0.41 0.232 3.90 3.80 1.08 0.77 0.59 0.133 5.67 5.60 1.60 1.12 0.51 0.564 4.49 4.33 5.02 2.42 0.16 0.795 4.77 4.64 2.48 1.47 0.29 0.276 4.93 4.98 1.41 0.07 0.29 0.157 4.26 3.89 3.20 1.47 0.09 0.178 3.71 3.59 1.48 1.33 0.52 0.389 4.30 4.44 1.38 0.02 0.01 0.10

10 5.02 4.48 1.30 0.50 0.32 0.10

Estimate, confidence intervals and prediction intervals are summarized in thefollowing table:

35

Linear regression: summary example 1

Observation y095% Confidence interval 95% Predicion intervallwr upr lwr upr

1 0.09 0.06 0.13 -0.06 0.252 0.01 -0.04 0.07 -0.15 0.173 0.25 0.18 0.31 0.08 0.414 0.19 0.03 0.34 -0.03 0.415 0.14 0.09 0.18 -0.02 0.296 0.09 0.02 0.16 -0.08 0.267 0.11 0.02 0.20 -0.07 0.288 0.15 0.08 0.21 -0.02 0.319 0.19 0.11 0.26 0.02 0.3510 0.15 0.11 0.18 -0.01 0.30

4.2.1 Financial accounting data with R

A linear regression can be done in R with the command lm(y ∼ x1 + x2 +x3), which means ”fitting a linear model with y as response and x1, x2 andx3 as predictors”. Once the Jtab42.rda data set has been downloaded, theregression model is built by typing

> # R command for linear regression

> M <- lm(RETCAP ~ ., data = Jobson)

In the above syntax, we call M the R object containing the model, theresponse variable and the predictors are separated by a tilde. In this case, aswe assume that all the predictors must be included in the model, we placea dot after the tilde to indicate to the program that all the variables exceptfor RETCAP are the predictors. The downloaded data set is a data framenamed Jobson. A data frame is a particular object of R representing data.It allows to represent numeric, character, complex or logical modes of datasimultaneously in the same object. The function summary() is a generictool used to produce result summaries of the results of various model fittingfunctions. The following command tells R to show the detailed summary ofthe model that we called M , belonging to the class of lm (linear models)function:

> summary(M)

Call:

lm(formula = RETCAP ~ ., data = Jobson)

Residuals:

36

4.2. Financial accounting data

Min 1Q Median 3Q Max

-0.126501 -0.043091 -0.002002 0.036908 0.201047

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.18807 0.13392 1.404 0.17160

GEARRAT -0.04044 0.07677 -0.527 0.60270

CAPINT -0.01414 0.02338 -0.605 0.55048

WCFTDT 0.30556 0.29737 1.028 0.31328

LOGSALE 0.11844 0.03612 3.279 0.00287 **

LOGASST -0.07696 0.04517 -1.704 0.09994 .

CURRAT -0.22328 0.08773 -2.545 0.01696 *

QUIKRAT 0.17671 0.09163 1.929 0.06437 .

NFATAST -0.36998 0.13740 -2.693 0.01202 *

INVTAST 0.25056 0.18587 1.348 0.18884

FATTOT -0.10099 0.08764 -1.152 0.25932

PAYOUT -0.01884 0.01769 -1.065 0.29645

WCFTCL 0.21513 0.19788 1.087 0.28658

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.07441 on 27 degrees of freedom

Multiple R-squared: 0.7889, Adjusted R-squared: 0.6951

F-statistic: 8.408 on 12 and 27 DF, p-value: 2.555e-06

Let’s give a look to the summary. All the relevant information are summa-rized. First, the function that generated the model is displayed. Then thelist of all the estimated regression coefficients with standard errors, t-ratiosand p-values are visualized. In the end, we have information about the resid-ual standard error (namely, the square root of the residual variance) with theassociated degrees of freedom, R2 and R

′2 and the F statistic with associatedp-value.

* * *

There is not a built-in function in R to visualize the ANOVA table as ithas been shown in the previous section. The function anova() computesanalysis of variance (or deviance) tables for one or more fitted model objects.Given a sequence of objects, anova tests the models against one another in

37

Linear regression: summary example 1

the specified order. In order to obtain a result similar to the one previouslydisplayed, let’s estimate a model with only the intercept (just put a 1 afterthe tilde):

> # R command for linear regression with only the intercept

> M1 <- lm(RETCAP ~ 1, data = Jobson)

Then we can use the anova() function:

> anova(M1, M)

Analysis of Variance Table

Model 1: RETCAP ~ 1

Model 2: RETCAP ~ GEARRAT + CAPINT + WCFTDT + LOGSALE + LOGASST + CURRAT +

QUIKRAT + NFATAST + INVTAST + FATTOT + PAYOUT + WCFTCL

Res.Df RSS Df Sum of Sq F Pr(>F)

1 39 0.70820

2 27 0.14951 12 0.55868 8.4075 2.555e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

In this case, we in fact perform a partial F test that compares the reducedmodel (the model with the intercept we call M1) with the complete modelthat we called M . We have in the first row SSER = SST = 0.70820 with 39degrees of freedom. Then in the second row we have SSE=0.14951 with 27df and SSR=0.55868 with 12 df . Why SSER = SST? Because the reducedmodel in this case has only the intercept (k = 1), then yi = β0 = y ∀i =1, . . . , n, hence SSER =

∑ni=1(yi − yi)2 =

∑ni=1(yi − y)2 = SST .

On the other hand, the null hypothesis is that β1 = . . . = βp = 0 because thecomplete model has p predictors. The degrees of freedom in the numeratorare p because in this case the subset of variables we called q coincides withall the predictors.

38

4.2. Financial accounting data

The meaning of this procedure is really similar to the one we have seen whenwe introduced the F -test on the reduced model. Here the reduced model isthe model with only the intercept. The number k of distinct parameters tobe estimated in the reduced model is smaller than the number of parame-ters to be estimated in the full model (with p+1 parameters). Hence, we test

H0: Reduced model is adequate against H1: Full model is adequate.

Note that the reduced model must be nested. A set of models are said to benested if they can be obtained from a larger model as special cases. To seewhether the reduced model is adequate, we use the ratio

F =(SSEreduced − SSEfull)/(p+ 1− k)

SSEfull/(n− p− 1)

In this special case, we have that in the reduced model β0 = y, henceSSEreduced = SST. Also in the reduced model k = 1 because we estimateonly one parameter, hence we have

F =(SST− SSE)/p

SSE/(n− p− 1),

hence F = MSR/MSE, the classical F test. Of course, as the p-value isextremely low, we reject the null hypothesis: it means that the reduced modelis not adequate with respect to the full model. In other words, at least oneregression coefficient is statistically different from zero.

Now we estimate the reduced model as in the previous section. We call thismodel M2:

> M2 = lm(RETCAP ~ WCFTCL + NFATAST + QUIKRAT + LOGSALE +

+ LOGASST + CURRAT, data = Jobson)

> summary(M2)

Call:

lm(formula = RETCAP ~ WCFTCL + NFATAST + QUIKRAT + LOGSALE +

LOGASST + CURRAT, data = Jobson)

Residuals:

Min 1Q Median 3Q Max

39

Linear regression: summary example 1

-0.128498 -0.050051 -0.000554 0.032703 0.254127

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.21132 0.10285 2.055 0.047902 *

WCFTCL 0.42488 0.05866 7.243 2.62e-08 ***

NFATAST -0.50515 0.07470 -6.762 1.04e-07 ***

QUIKRAT 0.08335 0.04130 2.018 0.051768 .

LOGSALE 0.09764 0.02506 3.896 0.000451 ***

LOGASST -0.07095 0.03234 -2.194 0.035387 *

CURRAT -0.12210 0.04062 -3.006 0.005034 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.07455 on 33 degrees of freedom

Multiple R-squared: 0.741, Adjusted R-squared: 0.6939

F-statistic: 15.74 on 6 and 33 DF, p-value: 1.927e-08

Let’s use the anova() function to perform the partial F -test, namely to doinference on the reduced model

> anova(M2, M)

Analysis of Variance Table

Model 1: RETCAP ~ WCFTCL + NFATAST + QUIKRAT + LOGSALE + LOGASST + CURRAT

Model 2: RETCAP ~ GEARRAT + CAPINT + WCFTDT + LOGSALE + LOGASST + CURRAT +

QUIKRAT + NFATAST + INVTAST + FATTOT + PAYOUT + WCFTCL

Res.Df RSS Df Sum of Sq F Pr(>F)

1 33 0.18340

2 27 0.14951 6 0.03389 1.02 0.4335

We obtain the results highlighted in Section 4.2. We cannot reject the nullhypothesis: namely, the reduced model is adequate because the regression co-efficients of the remaining p− q variables are statistically not different fromzero.

* * *

The function predict() is a generic function for predictions from the results ofvarious model fitting functions. When the object belongs to the lm class, this

40

4.2. Financial accounting data

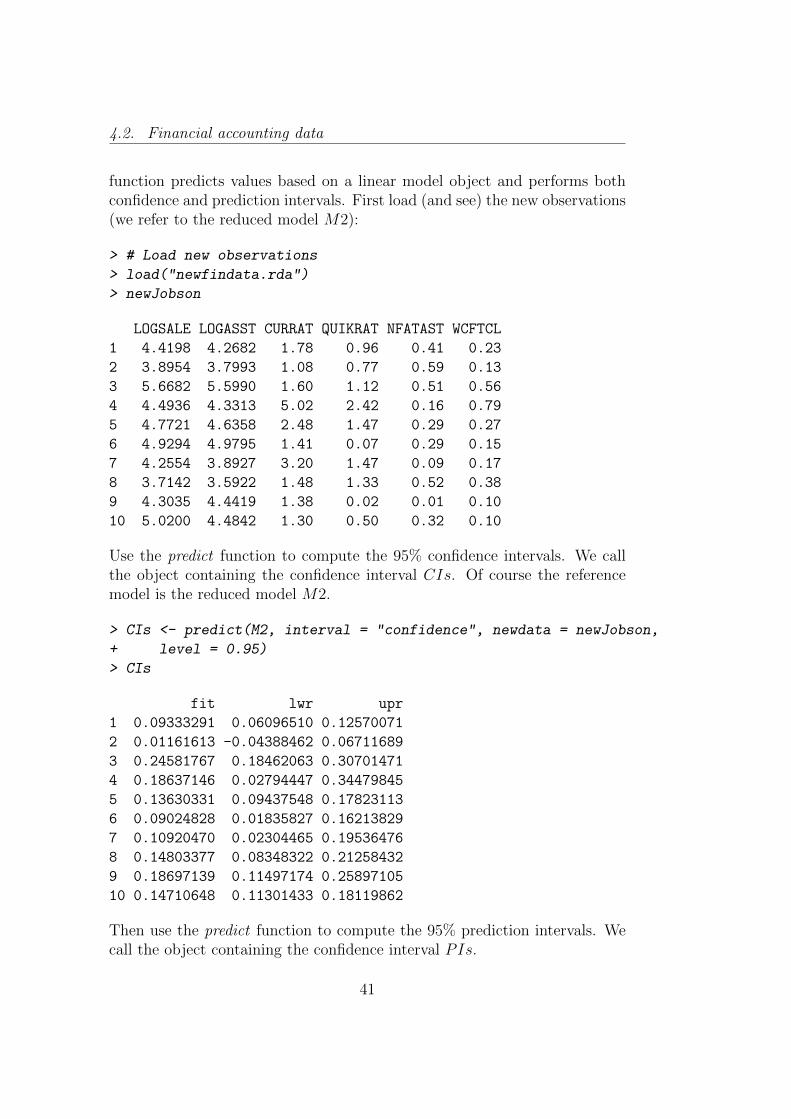

function predicts values based on a linear model object and performs bothconfidence and prediction intervals. First load (and see) the new observations(we refer to the reduced model M2):

> # Load new observations

> load("newfindata.rda")

> newJobson

LOGSALE LOGASST CURRAT QUIKRAT NFATAST WCFTCL

1 4.4198 4.2682 1.78 0.96 0.41 0.23

2 3.8954 3.7993 1.08 0.77 0.59 0.13

3 5.6682 5.5990 1.60 1.12 0.51 0.56

4 4.4936 4.3313 5.02 2.42 0.16 0.79

5 4.7721 4.6358 2.48 1.47 0.29 0.27

6 4.9294 4.9795 1.41 0.07 0.29 0.15

7 4.2554 3.8927 3.20 1.47 0.09 0.17

8 3.7142 3.5922 1.48 1.33 0.52 0.38

9 4.3035 4.4419 1.38 0.02 0.01 0.10

10 5.0200 4.4842 1.30 0.50 0.32 0.10

Use the predict function to compute the 95% confidence intervals. We callthe object containing the confidence interval CIs. Of course the referencemodel is the reduced model M2.

> CIs <- predict(M2, interval = "confidence", newdata = newJobson,

+ level = 0.95)

> CIs

fit lwr upr

1 0.09333291 0.06096510 0.12570071

2 0.01161613 -0.04388462 0.06711689

3 0.24581767 0.18462063 0.30701471

4 0.18637146 0.02794447 0.34479845

5 0.13630331 0.09437548 0.17823113

6 0.09024828 0.01835827 0.16213829

7 0.10920470 0.02304465 0.19536476

8 0.14803377 0.08348322 0.21258432

9 0.18697139 0.11497174 0.25897105

10 0.14710648 0.11301433 0.18119862

Then use the predict function to compute the 95% prediction intervals. Wecall the object containing the confidence interval PIs.

41

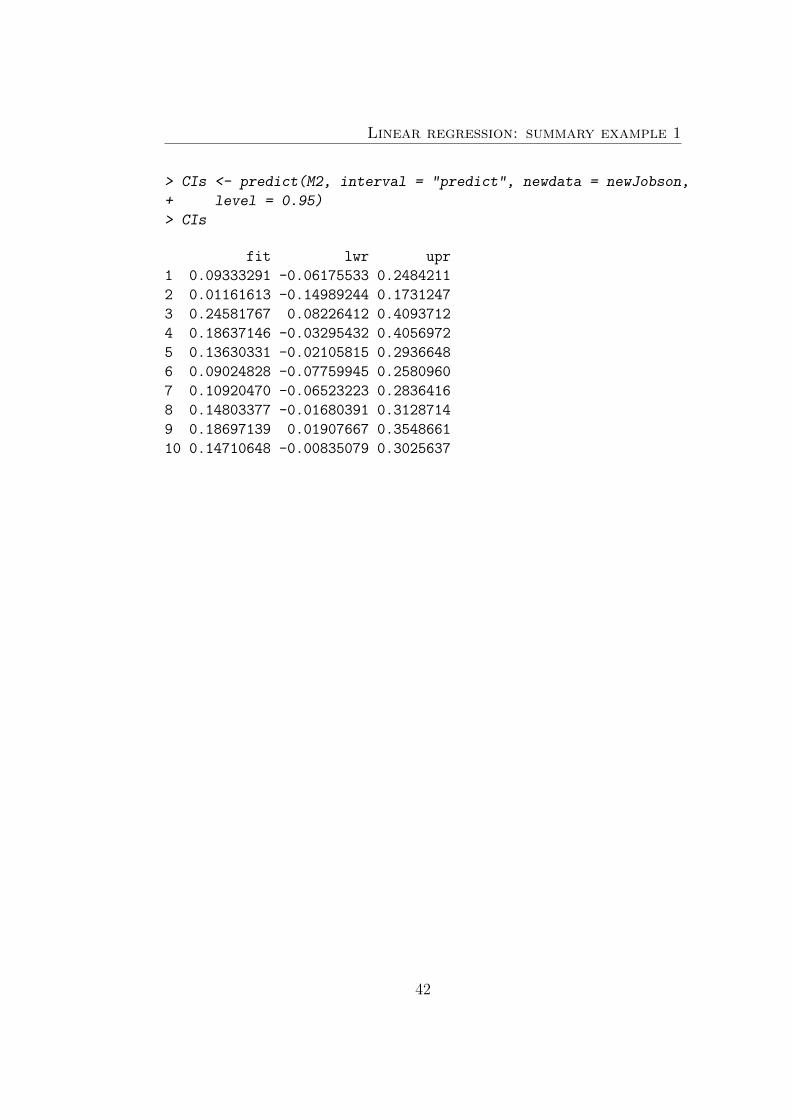

Linear regression: summary example 1

> CIs <- predict(M2, interval = "predict", newdata = newJobson,

+ level = 0.95)

> CIs

fit lwr upr

1 0.09333291 -0.06175533 0.2484211

2 0.01161613 -0.14989244 0.1731247

3 0.24581767 0.08226412 0.4093712

4 0.18637146 -0.03295432 0.4056972

5 0.13630331 -0.02105815 0.2936648

6 0.09024828 -0.07759945 0.2580960

7 0.10920470 -0.06523223 0.2836416

8 0.14803377 -0.01680391 0.3128714

9 0.18697139 0.01907667 0.3548661

10 0.14710648 -0.00835079 0.3025637

42

Chapter 5

Regression diagnostic

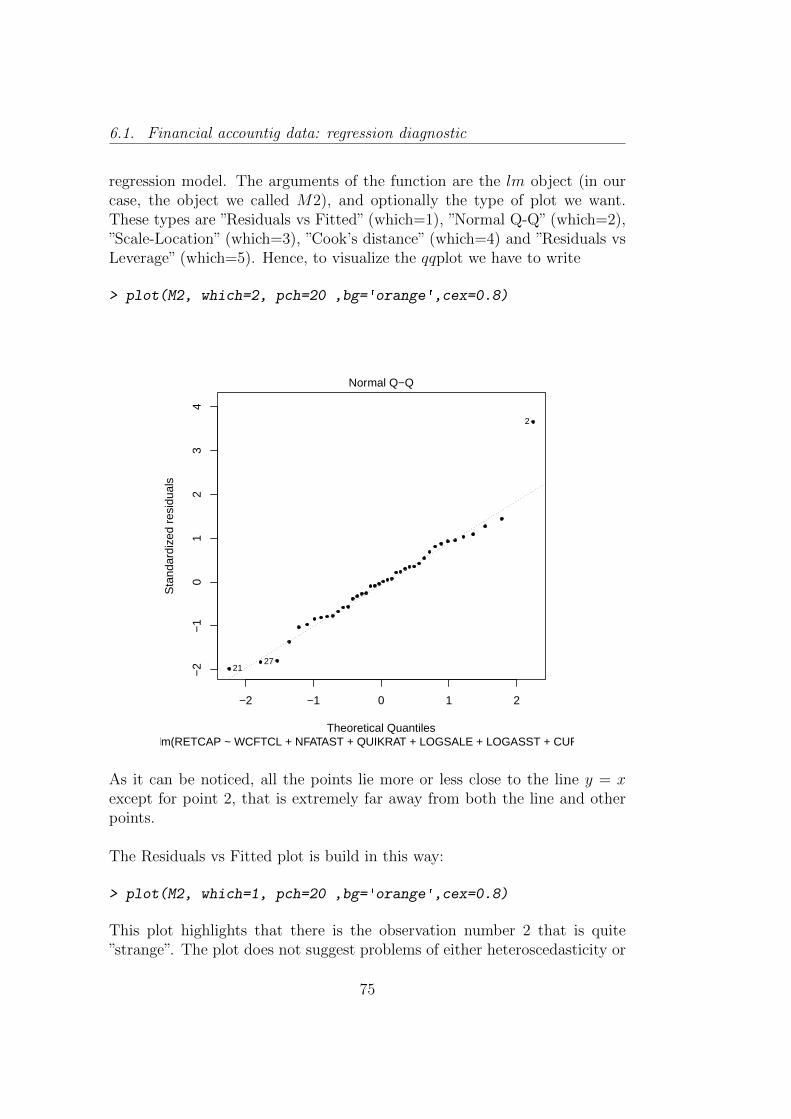

5.1 Hat matrix

Think about the regression model:

y = Xβ + e = y + e.

Since β = (XTX)−1XTy, it follows that:

y = Xβ

= X(XTX)−1XTy

= Hy

The matrix H = X(XTX)−1XT is symmetric (H = HT ), idempotent (H ×H = H2 = H) and is called hat matrix, since it ”puts the hat on the y”,namely it provides the vector of the fitted values in the regression of y on X.Let hij (i, j = 1, . . . , n) be the generic element of the H matrix, and let hiidenote its diagonal element. Let X = X−C be the mean deviation from X,where C = 1

n11TX is the centering matrix and 1 is the (n× 1) unit vector.

The hat matrix can be expressed in this alternative way:

H = X(XTX)−1X =1

n11T + X(XTX)−1XT .

It allows to better understand the properties of the hat matrix:

hii = xTi (XTX)−1xi = 1n

+ (xi − x)T (XTX)−1(xi − x).The second term of the expression describes an ellipsoid with center atthe center x. All the points xi that are in the ellipsoid are said to havethe same Mahalanobis distance from x (Jobson, 1991). hii is then large

Regression diagnostic

or small depending on how far xi is away from x. This distance takesinto account the covariance matrix matrix (XTX)−1XT .

When the model is estimated with the intercept,∑n

j=1 hij = 1.

|hij| ≤ 1 ∀i 6= j

When the model is estimated with the intercept 1n≥ hii ≥ 1, otherwise

0 ≥ hii ≥ 1.

hii = 1 iff hij = 0 ∀i 6= j.

If X has full rank, tr(H) = p + 1. It means that the average of hii is(p+ 1)/n.

yi =∑n

j=1 hijyj. It means that each yi is related to all yi through thehij values.

Think about a simple regression model (only one predictor). It can be seenthat

hij =1

n+

(xi − x)(xj − x)∑nj=1(xj − x)2

and

hii =1

n+

(xi − x)2∑nj=1(xj − x)2

.

The further the observation xi is from the center of the data, X, the greaterthe weight placed on the corresponding yj observation in the determinationof yi. Each yj observation has an impact on each value of yi and thus anextreme value of yj influences all yi. The least squares fit is thus very sensitiveto extreme points. It is clear that hii = 1

nwhen xi = x.

The diagonal elements of H, hii, are called leverage. The leverage is a measureof how far the observation xi is from the center of X. When the leverage islarge, yi is more sensitive to changes in yi than when the leverage is relativelysmall. High leverage of y observations corresponds to points where (X− X)is relatively large. Outliers tend to have a large leverage value and hence amajor impact on the predicted values yi.But a high leverage necessarily means problematic observation? Let’s give alook to the following figure.

In Figure 5.1, the point M represents the center of the data (and the pro-jection of the mean of X). The three points N , 0 and D are all distant from

44

5.2. Residuals

Figure 5.1: Leverage, outliers and influence

the main cluster of points with center at M . There is difference among thesepoints? The points 0 and D have large leverage (they are quite far awayfrom M), while the point N yields a leverage equal to 1/n (more or less, itgets a X value extremely close to X). Points 0 and D are distant from thecenter of the data in both the directions, point N is at the mean of the Xvalues but is distant from the Y mean. Suppose to fit a least square line tothe main cluster of data. Suppose to compare the obtained fit with the leastsquares fit including only one of the points 0, D and N . If we include eitherN or 0, both points will have a large influence on the estimated regressionparameters. The slope of the fitted line will change considerably. If we in-clude the point D, it will not have great influence in the estimated regressionparameters: the slope of the regression line will not change at all. ProbablyD is the point with the greater leverage. But it is not a influence point atall. The leverage value is only a partial measure of the impact of observationon the parameters.

5.2 Residuals

A way of judging outliers is to determine whether the extreme point is withina predictable range, given the linear relationship that would be fitted withoutthis extreme point.

45

Regression diagnostic

The residuals from the fitted models are

e = y − y = y −Xβ = (I−H)y,

the residual for the ith observation is then ei = yi − yi.Let’s denote with e(i)i = yi − y(i)i the so-called deleted residual. It is theresidual obtained by taking the difference between the observed yi and theleast squares prediction y(i)i obtained after omitting the point (xi, yi) fromthe least squares fit.

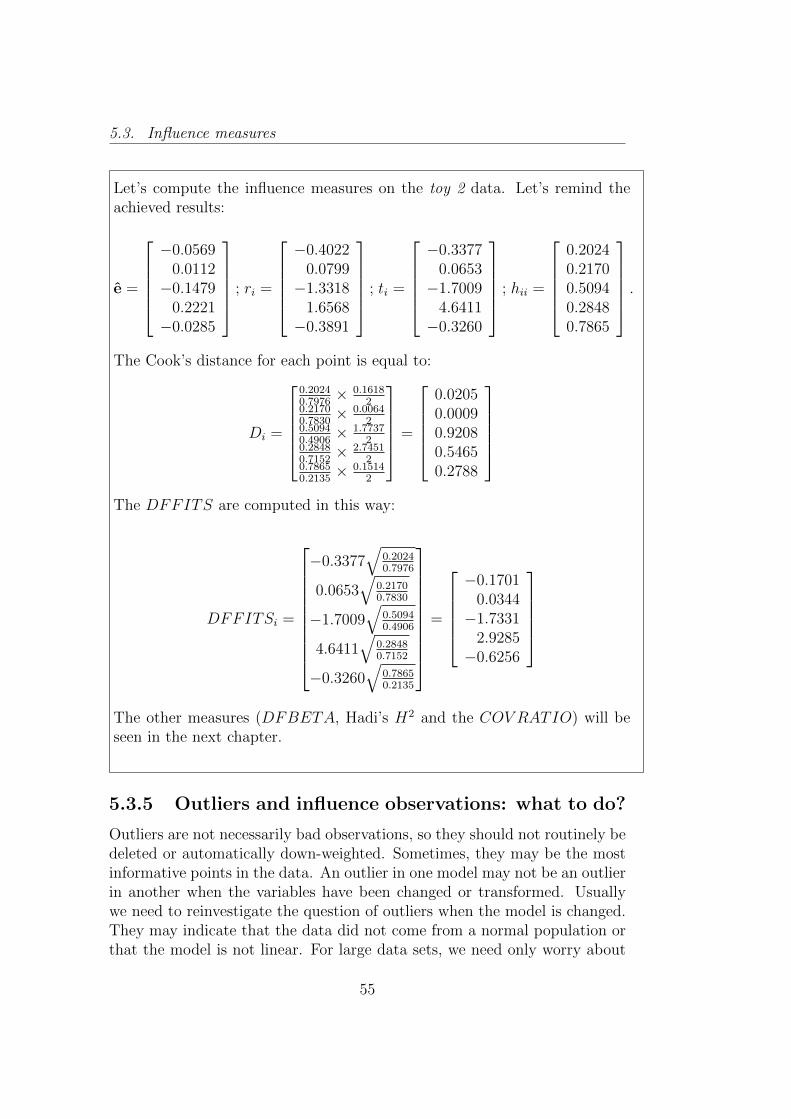

Suppose to have these data, that we call toy 2 data:

y =

8.66239.01997.75198.5500

10.0064

; x =

3.37063.72912.35582.88605.0000

The estimated regression coefficients, the fitted values and the residualsare

β0 = 5.998, β0 = 0.807, y =

8.71929.00877.89988.3279

10.0349

, e =

−0.0569

0.0112−0.1479

0.2221−0.0285

If we re-estimate the model omitting the third observation, we obtainβ0 = 6.349, β1 = 0.724.Hence, y3 = y(i)i = 6.349 + 0.724× 2.3558 = 8.0533.Finally, e(i)i = yi − y(i)i = 7.7519− 8.0533 = −0.3014

The procedure should be delete point i for each i, then refit the model, pre-dict yi obtaining y(i)i and get the residuals e(i)i. Theoretically, we should fitn models to get n deleted residuals. Fortunately, there is a precise relationbetween the residuals of a model and the deleted residuals:

e(i)i =ei

1− hii.

It means that every time we fit a model, we immediately know the deleted

46

5.2. Residuals

residuals for each value.

The hat matrix of the model previously estimated is:

H =

0.2024 0.1936 0.2272 0.2142 0.16260.1936 0.2170 0.1275 0.1620 0.29990.2272 0.1275 0.5094 0.3619 −0.22600.2142 0.1620 0.3619 0.2848 −0.02300.1626 0.2999 −0.2260 −0.0230 0.7865

.

Remember that the residuals of the model are e =

−0.0569

0.0112−0.1479

0.2221−0.0285

. The

diagonal elements of the hat matrix (the leverage points) are hii =0.20240.21700.50940.28480.7865

, with the consequence that

e(i)i =

−0.0569/0.20240.0112/0.2170−0.1479/0.50940.2221/0.2848−0.0285/0.7865

=

−0.0714

0.0143−0.3014

0.3106−0.1335

.Look at the third deleted residual: We get, of course, the same resultpreviously obtained without estimating a new model. We obtain all thedeleted residuals by estimating only one model.

In Figure 5.2, ”a scatterplot of values (xi, yi) is shown with an ordinary leastsquares line y. A second least squares line y(i) denotes the fitted line obtainedafter omitting observation (xi, yi) at point A. The corresponding values of yi,y(i)i, ei and e(i)i are also shown in the figure. In this case the point A appearsto have an impact on the magnitude of the residual” (Jobson 1991, p.152).

As hii is the leverage, it is clear that if the leverage is large for a given pointthen the deleted residual tends to be large for the same point. We expect thatin (large) data sets the omission of a single data point from a least squaresfit should have little impact on the residual for the omitted data point. In

47

Regression diagnostic

Figure 5.2: Residuals and deleted residuals. Figure taken from Jobson, 1991,p.152

other words, we expect that ei and e(i)i are quite similar. Similarly, we expectthat the sum of squared residuals

∑ni=1 e

2i and the sum of squared deleted

residuals∑n

i=1 e2(i)i =

∑ni=1

e2i(1−hii)2 should also be of similar magnitude.

The PRESS (Predicted REsidual Sum of Squares) statistic gives a summarymeasure of the fit of a model to a sample of observations. Probably you willuse this statistics in the future as model selection method (leave-one-out-cross-validation). It is equal to the sum of squared deleted residuals:

PRESS=n∑i=1

e2i(1− hii)2

.

The contribution of each point to the PRESS statistic can be determined,identifying dominant values of e(i)i. Such dominant values can therefore berelated to the leverage values.The ratio of PRESS to the ordinary sum of squared residuals∑n

i=1e2i

(1−hii)2∑ni=1 e

2i

gives an indication of the sensitivity of the fit to omitted observations. Out-liers can often cause this ratio to be much larger than unity.

48

5.2. Residuals

Remember the random variable residuals we introduced in Chapter 3.1.1:

E = Y −XB = Y −X(XTX)−1XTY = (I−H)Y = MY.

We can write:

E = (I−H)Y

= (I−H)(Xβ + ε)

= (I−H)Xβ + (I−H)ε

= Xβ −X(XTX)−1XTXβ + (I−H)ε

= (I−H)ε.

It immediately follows that E[E] = 0 and, by remembering that H is idem-potent and that H ×H = H, var(E) = var((I −H)ε) = (I −H)σ2, hencevar(ei) = σ2(1− hii). This evidence highlights that although the errors mayhave equal variance and be uncorrelated, the residuals do not.Let’s introduced the standardized residuals, known also as internally studen-tized residuals, useful for studying the behavior of the true error terms:

ri =ei

s√

(1− hii).

If the model assumptions are correct var(ri) = 1 and corr(ri, rj) tends to besmall. Any abnormal observation will inevitably affect s, and thus also thestandardized residuals. In the above formulation, we could note that ei isnot independent of s2. Also for this reason, the standardized residuals arecalled internally studentized residuals.

If we were able to compute the sample variance in a model fit without theith observation, then we could obtained a sample variance independent ofthe ith residual.Let s2(i) denote the residual variance after eliminating the i-th observation.The Studentized (or externally Studentized, or Jackknife) residual is definedas

ti =ei

s(i)√

(1− hii).

The externally studentized residual is distributed as a t distribution withn − p − 2 degrees of freedom if the error terms are normal, independent,mean zero and with constant variance. Also in this case we do not have toperform additional regressions because

s2(i) =[(n− p− 1)s2 − e2i /(1− hii)]

n− p− 2.

49

Regression diagnostic

An easy way to compute ti is

ti = ri

(n− p− 2

n− p− 1− r2i

)1/2

i = 1, . . . , n.

The sample variance of the model estimated with toy 2 data is s2 = eT e/(n−p−1) = 0.0754/3 = 0.0251. The PRESS statistic is

∑5i=1 e

2(i)i = 0.2104, while

PRESS/eT e = 2.7911.Let’s compute the standardized (internally studentized) residuals. We have

ri =

−0.0569/(0.1585

√0.7976)

0.0112/(0.1585√

0.7830)

−0.1479/(0.1585√

0.4906)

0.2221/(0.1585√

0.7152)

−0.0285/(0.1585√

0.2135)

=

−0.4022

0.0799−1.3318

1.6568−0.3891

.

If we want compute s2(i), we must compute [(n− p− 1)s2− e2i /(1−hii)]/(n−p− 2) for each observation:

s2(i) =

[3× 0.0251− (−0.05692/0.7976)] /2[3× 0.0251− (0.01122/0.7830)] /2

[3× 0.0251− (−0.14792/0.4906)] /2[3× 0.0251− (0.22212/0.7152)] /2

[3× 0.0251− (−0.02852/0.2135)] /2

=

0.03570.03760.01540.00320.0358

.Then, we are ready to compute ti:

ti =

−0.0569/

√(0.0357 × 0.7976)

0.0112/√

(0.0376 × 0.7830)

−0.1479/√

(0.0154 × 0.4906)

0.2221/√

(0.0032 × 0.7152)

−0.0285/√

(0.0358 × 0.2135)

=

−0.3377

0.0653−1.7009

4.6411−0.3260

.

Of course, we are able to compute ti without computing s2(i), but only knowingri:

ti = ri

(n− p− 2

n− p− 1− r2i

)1/2

=

−0.4022×

√(2/(3− (−0.4022)2))

0.0799×√

(2/(3− (0.0799)2))

−1.3318×√

(2/(3− (−1.3318)2))

1.6568×√

(2/(3− (1.6568)2))

−0.3891×√

(2/(3− (−0.3891)2))

=

−0.3377

0.0653−1.7009

4.6411−0.3260

.

50

5.3. Influence measures

5.3 Influence measures

In a linear regression, a point is an influential point if its deletion, singlyor in combination with others (two or three), causes substantial changes inthe fitted model. Hence, high leverage points need not be influential andinfluential observations are not necessarily high leverage points.Observations with large standardized (or studentized) residuals are outliersin the response variable because they lie far from the fitted equation in thedirection of y. Since the standardized residuals are approximately normallydistributed with mean zero and a standard deviation 1, points with stan-dardized residuals larger than 2 or 3 are called outliers (Chatterjee & Hadi,2005).Outliers in the predictor variables space can also affect the regression results.They are evaluated through the leverage hii. Hence, hii can be used as ameasure of outlyingness in the space of predictors because observations withlarge leverage are to be considered as outliers compared to other points inthe space of the predictors. As the average size of the leverage is (p+1)

n, a way

to consider large a leverage value is to check if hii > 2 (p+1)n

.Hence, there are outliers in the space of y (to be evaluated with standardizedresiduals) and outliers in the space of X (to be evaluated with the leveragevalues).

However, the idea of leverage is all about the potential for an observationto have a large effect on a fitted regression, as well as analyses that are basedon residuals alone may fail to detect outliers and influential observations.First, there is a relationship between leverage and residual so that

hii +ei

σ2/(n− p− 1)≤ 1.

It means that high leverage points tend to have small residuals. Therefore,in addition to an examination of the standardized residuals for outliers, anexamination of the leverage values is also recommended for the identificationof troublesome points.

Second, the use of residuals from a fitted linear relationship to identifyoutliers has the disadvantage that an outlier can mask itself by drawing theline toward itself, as a result the residual is considerably smaller than itwould have been had this point been omitted from the data set (swampingphenomenon). The masking phenomenon occurs when the data contain out-liers, but we fail to detect them: some of the outliers may be hidden by otheroutliers in the data.

51

Regression diagnostic

For this reason, several measures of influence of observations have been pro-posed.

5.3.1 Cook’s distance

The Cook’s distance combines the notions of outlyingness and leverage. Forthe ith observation, it is defined as

Di =(yi − y(i)i)T (yi − y(i)i)

s2(p+ 1)

=(β(i) − β

)T(XTX)

(β(i) − β

)/s2(p+ 1)

=

[hii

1− hii

]e2i

(p+ 1)s2(1− hii)

=

[hii

1− hii

]r2i

(p+ 1)

=

hii

1− hii

r2i( 1

p+ 1

),

where yi and β are the fitted value and the estimated vector of regressioncoefficients in a model that includes the ith observation, and y(i)i and β(i)

are the prediction of the ith observation and the least squares estimate of βwithout the ith observation.The Cook’s distance measures the difference between the fitted values ob-tained from the full data and the fitted values obtained by deleting the ithobservation. If we better give a look to the last term of the equation,

Di =

hii

1− hii

r2i( 1

p+ 1

),

we can note that Cook’s distance is a multiplicative function of two basicquantities (Draper & Smith, 1998, p.212): the ratio (variance of the ithpredicted value)/(variance of the ith residual), also called potential function,and the squared standardized residual. Remember that in Chapter 3.3 wedefined the variance of the predicted value as var(y) = s2H, then it is clearthat var(yi) = s2hii. The variance of the ith residual is, as we know, equalto s2(1− hii).Di will be large if the (squared) standardized residual is large and/or if theleverage is large. We know that observations with large absolute standardizedresidual or leverage points are potentially influential: points that are bothare the most influential. High Di values indicate influential observations

52

5.3. Influence measures

on the vector of β parameters. As a rule of thumb, points with Di valuesgreater than 1 could be classified as being influential. Really often, it isbetter evaluate the Cook’s distance graphically through a, say, dot plot thanevaluating each single point using a rigid rule.

5.3.2 The DF family

The influence measures belonging to the so called DF (Difference in) familyare somewhat related to the Cook’s distance. Let’s start with the DFFITS(Difference to fit):

DFFITSi =(yi − y(i)i)s(i)√hii

= ti

√[hii

1− hii

]This measure is the difference between the ith fitted value obtained fromthe full data and the ith fitted value obtained by deleting the ith observa-tion scaled by s(i)

√hii. Points with DFFITS > 2

√pn

need to be investi-gated. Also in this case, instead of having a strict cutoff value, generally theDFFITS are used in a graph (dot plot, boxplot, etc) to detect points ofabnormally high influence relative to other points. Generally, the informa-tion given by the DFFITS are equivalent to the ones given by the Cook’sdistance.

Let β be the vector of regression coefficients and let β(i) be the vector ofregression coefficients after extracting the ith observation in the data. Thequantity

DB = β − β(i) =(XTX)−1xi

T ei(1− hii)

measures the difference in each parameter estimate with and without ithpoint. Let β(j)i be the estimate of the jth regression coefficient after deletingthe ith observation. The DFBETA (Difference in beta) measure is definedas

DFBETAj,i =βj − βj(i)

s(i)√

(XTX)−1(jj)

,

where the subscript (jj) denotes the diagonal element of the matrix (XTX)−1