LECTURE 2 FORMS OF BUSINESS ORGANIZATION AGENCY RELATIONSHIPS.

30

LECTURE 2 • FORMS OF BUSINESS ORGANIZATION • AGENCY RELATIONSHIPS

-

Upload

lynette-sutton -

Category

Documents

-

view

213 -

download

0

Transcript of LECTURE 2 FORMS OF BUSINESS ORGANIZATION AGENCY RELATIONSHIPS.

LECTURE 2

•FORMS OF BUSINESS ORGANIZATION•AGENCY RELATIONSHIPS

1-2

Alternative Forms of Business Organization

Sole proprietorship An unincorporated business owned by

one individual Partnership

An unincorporated business owned by two or more persons

1-3

Sole proprietorships & Partnerships Advantages

Ease of formation—just start! Subject to few regulations No corporate income taxes

Disadvantages Unlimited liability Difficult to raise capital Limited life Difficult to transfer ownership

1-4

Corporation A legal entity, separate & distinct from its

owners and managers, having unlimited life, easy transferability of ownership & limited liability

Advantages Unlimited life Easy transfer of ownership Limited liability Ease of raising capital

Disadvantages Double taxation Cost of set-up and report filing

1-5

Value Maximization If organized as a corporation, the

business value will most likely be maximized

Reasons: Limited liability means lower risk and

therefore, higher value Easy access to funds results in growth

opportunities Easy transfer of ownership means

investors are willing to pay more Some tax differences are beneficial for

corporations

1-6

Agency relationships An agency relationship exists

whenever a principal hires an agent to act on their behalf

Within a corporation, agency relationships exist between: Shareholders and managers

Shareholders and creditors

1-7

Shareholders versus Managers Managers are naturally inclined to

act in their own best interests. They may want more perks whilst

shareholders want an increase in the stock price

1-8

How to motivate Managers?

The threat of firing The threat of takeover

Hostile takeover: instances in which management does not want the firm to be taken over

How to prevent takeovers? Poison pill: an action the firm takes

that can practically kill it and makes it unattractive, e.g. giving huge retirement bonuses if the management changed

1-9

Motivating managers… Greenmail: like blackmail. The target

company offers to buy the stock from the potential buyer at a price above the market

Managerial compensation plans Allows managers to purchase stock at

some future time at a given price

1-10

Shareholders versus Creditors Shareholders (through managers) could take

actions to maximize stock price that are detrimental to creditors.

E.g., stockholders might push management to take up a project that has high returns but also high risk

If the venture is successful, all the benefits accrue to shareholders; creditors just get a fixed return

If things go bad the creditors will have to share the losses

Practice Questions: Chapt 1

CHAPTER 2The Financial Environment: Markets, Institutions, and Interest Rates and Taxes

Financial markets Types of financial

institutions Determinants of interest

rates Yield curves

1-13

What is a market? A market is a venue where goods

and services are exchanged. A financial market is a place where

individuals and organizations wanting to borrow funds are brought together with those having a surplus of funds.

1-14

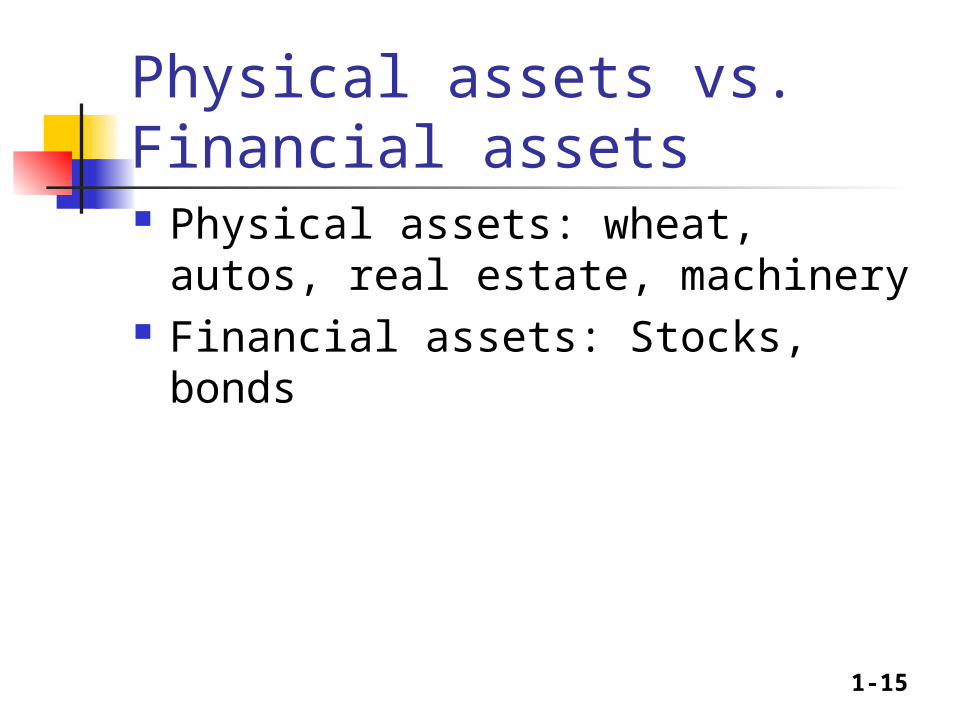

Types of financial markets Physical assets vs. Financial assets Money vs. Capital Primary vs. Secondary Spot vs. Futures Mortgage vs. Consumer credit

1-15

Physical assets vs. Financial assets Physical assets: wheat, autos, real

estate, machinery Financial assets: Stocks, bonds

1-16

Money vs. Capital Money mkt: for debt securities with

maturity of less than 1 year Capital mkt: for long-term debt

AND common stock

1-17

Primary vs. Secondary Primary mkts: in which

corporations & governments raise new capital

Secondary mkts: in which existing, previously issued (already OUTSTANDING) securities are traded

1-18

Spot vs. Futures Spot markets: where assets are

bought or sold for “on the spot” delivery (immediately or within a few days)

Futures markets: where assets are bought or sold for delivery at a later date (e.g. six months or a year into the future)

1-19

Mortgage vs. Consumer credit Mortgage mkts: loans on

commercial, residential, industrial real estate & farmland

Consumer credit markets: loans for autos, appliances, education etc.

1-20

How is capital transferred between savers and borrowers?

Direct transfers Investment

banking house Financial

intermediaries

1-21

Capital formation process

Business sells stocks or bonds to savers w/o going through any financial institution

1-22

Capital formation process

Intermediary obtains funds from investors, issuing its own securities

The intermediary might lend to business

Intermediaries create new forms of capital (e.g. certificates of deposit)

Efficiency of financial mkts increases

1-23

Capital formation process

Investment bank buys & holds securities for a period of time—so it is taking a chance

Investment bank deals with the issuance of securities not loans and deposits

1-24

Types of financial intermediaries

Commercial banks Savings and loan associations Mutual savings banks Credit unions Pension funds Life insurance companies Mutual funds

1-25

Physical location stock exchanges vs. Electronic dealer-based markets

1-26

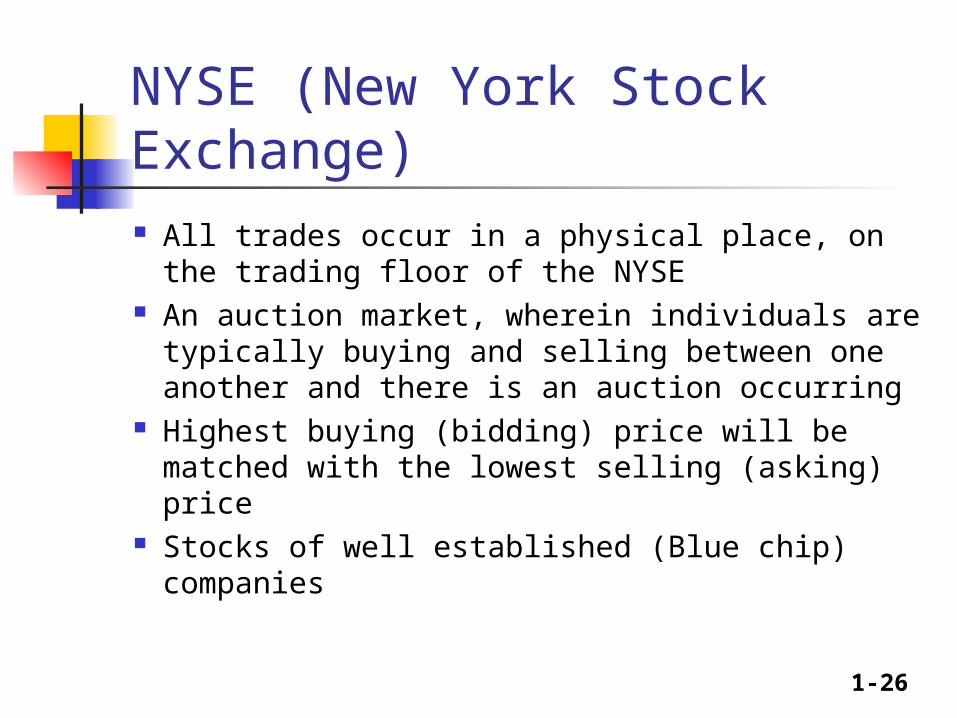

NYSE (New York Stock Exchange) All trades occur in a physical place, on the

trading floor of the NYSE An auction market, wherein individuals are

typically buying and selling between one another and there is an auction occurring

Highest buying (bidding) price will be matched with the lowest selling (asking) price

Stocks of well established (Blue chip) companies

1-27

NASDAQ (National Association of Securities Dealers’ Automated Quotations)

Located on a telecommunications network. Dealer's market, wherein market

participants are not buying from and selling to one another but to and from a dealer

He is the market maker Stocks of firms dealing with the Internet or

electronics. Stocks are more volatile

1-28

Differences have narrowed NASDAQ exchange was listed as a

publicly-traded corporation, while the NYSE was private corporation.

In March 2006 the NYSE went public after being a not-for-profit exchange for nearly 214 years.

The shares of these exchanges, like those of any public company, can be bought and sold by investors on an exchange.

1-29

Organized exchange vs. OTC market

Organized exchange: Physical place

Over-the-Counter market: Brokers and Dealers connected over an electronic network

Give an example…

1-30

Video Clip: Key Takeaways Primary and Secondary markets Public financial markets

Where govts borrow money Corporate financial markets

Where corporations borrow money Organized security exchanges vs.

virtual networks Most people think of the stock

market when we talk of financial markets