LEARNING UNIT 1: Legal requirements of contractual …€¦ · Web view · 2016-09-21If a...

35

Page | 1 Module 2 Legal requirements for tour operations Component 2: Contractual requirements and legal compliance Copyright and database rights protection exists in this publication and all rights are reserved. © MGT Training Solutions 2016 Version 1.8:16

Transcript of LEARNING UNIT 1: Legal requirements of contractual …€¦ · Web view · 2016-09-21If a...

P a g e | 1

Module 2Legal requirements for tour

operations

Component 2: Contractual requirements and legal compliance

Copyright and database rights protection exists in this publication and all rights are reserved.

This publication or any part thereof may not be reproduced, transmitted, and conveyed, communicated or used in any form or by any means, whether in whole or in part, without prior written permission.

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 2

LEARNING UNIT 1: Legal requirements of contractual agreements

Some contracts must be in writing in order for them to be enforceable such as marriage contracts,

sale of real estate, etc.

It is advisable to always write up some kind of simple contract.

To be legal, a contract must contain the following elements

1. Offer and acceptance

The most important feature of a contract is that one party makes an offer for an

arrangement that another accepts.

2. Consideration

Both parties to a contract must bring something to the bargain. Money is often recognized

as consideration.

3. Consent to contract/Reality of consent

The two parties must voluntarily agree to all the terms of the contract.

4. Contractual capacity

This is the legal ability to enter into a contract. Once a person reaches the age of 18, they

are considered a legal adult. Minors, the mentally impaired and intoxicated people,

convicts, and aliens lack the capacity to enter into a contract.

5. Intention to be legally bounded

This indicates that courts assume that parties to an agreement wished it to be enforceable

by a court. It reflects a court's general policy to uphold agreements in the commercial

sphere of life (www.wikipedia.com).

6. Legality of the purpose/object

An agreement is only legal and enforceable if it complies with the law of the country and

public policy. Any agreement entered into for an illegal purpose is not legally binding

(www.businessdictionary.com).

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 3

Termination of contract may be achieved by means of the followingMGTMGT Performance: When the parties to the contract fulfil their obligations as agreed. MGTMGT Agreement: When both sides agree to terminate even though the contract is incomplete. MGTMGT Frustration: When an unseen event (e.g., death) prevents the contract from being completed. MGTMGT Breach: When a condition (an essential term of the contract) is broken, the innocent party does

not have to fulfil the contract and may sue for damages. If a warranty (a non-essential element

of the contract) is broken, the contract remains valid, but the innocent party may receive

damages.

Terms and conditions

This defines how a contract is implemented for a customer organisation such as the tour operator.

This follows the most common terms that apply when a client books a tour with practical examples

of the provisions. This will vary according to the organisational requirements of each company.

Definition of basis or subject matter of the contract

All services, e.g. the tour itinerary, should be described in detail (including the dates) or reference must be

made to the web site/other document.

Payment terms

This should include all variations and circumstances as well as provisions for increase.

MGTMGT Tariffs/fares/prices

E.g. all tours include an experienced and knowledgeable guide. Unless specifically stated, tariffs

exclude beverages, transfer fees and gratuities and all costs of a personal nature (please refer to

your specific itinerary). Happy Safaris will endeavour to maintain prices quoted, but reserve the

right to change prices without incurring obligations.

MGTMGT Deposits

E.g. 30% with booking of a tour balance payable 2 weeks prior to the commencement of

the tour. It is non-refundable. (Since April 2011 the Consumer Protection Act (CPA – see

elsewhere in study guide) has changed non-refunding slightly. Do check before you

refuse to refund point blank).

MGTMGT Payment methods

E.g. payment may be made by bank guaranteed cheque, cash or electronic

transfer. Kindly note that we do not have any credit card facilities.

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 4

MGTMGT Refunds

E.g. neither deposit nor full payment will be refunded unless a replacement is found by the client.

No refunds are given if a person leaves a trail before it ends. (Check CPA)

Changes

E.g. name changes can only be done before tickets are issued and are subject to airline approval.

Also see Conditions for Changes and Cancellation.

Cancellation

E.g. once travel documents have been issued, cancellation fees apply to any cancelled bookings.

Happy Tours charges 6% cancellation fee for domestic flight bookings and 10% cancellation fee

foriInternational flight bookings and package holidays.

Also see Conditions for Changes and Cancellation.

Indemnity

E.g. all participants in the balloon flight are required to sign a standard indemnity form on arrival

and international visitors are advised to obtain medical, travel, etc., insurance before leaving their

country of origin. All participation in activities is at the guest's own risk. Also see Liability and

Indemnity Form.

Insurance

E.g. travel Insurance (against cancellation, illness and loss of baggage) is strongly recommended.

Happy Tours will not be liable for any costs incurred as a result of inadequate travel insurance.

Passports, Visas and Vaccinations

E.g. it is the customer’s responsibility to obtain a proper, current and valid passport, visa and

relevant vaccinations. Happy Tours shall not be held responsible or liable for any consequence of any

nature arising from the customer failing to ensure that they have complied with all these

requirements.

Unscheduled Extensions

E.g. in the event of an unscheduled extension to the holiday caused by flight delays, bad weather,

strikes or any other cause beyond the control of Happy Tours, it is understood that the expenses

relating to these unscheduled extensions (hotel accommodation, transport, etc.) will be for the

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 5

account of the passenger.

Responsibility and Liability

E.g. Happy Tours acts as agent for local and international ground operators as well as airlines and

accepts no liability whatsoever for any loss, damage, injury, accident, delay or any other irregularity

arising. It is the client’s responsibility to check that all reservations are correct, before payment is

made. Amendment fees thereafter will be the client’s responsibility.

Also see Liability and Indemnity Forms.

Privacy

E.g. it is our policy to ensure complete confidentiality of all information provided to Happy Tours. No

contact or other details will be disclosed to any third parties.

Changes to these Terms and Conditions

E.g. the company has the authority and right to, at any time, change or amend any part of these

Terms and Conditions.

Cancellations and changes

Conditions for cancellations and changes of tours vary from company to company in the industry.

If a reservation is cancelled, a cancellation fee is usually calculated as a percentage of the total tour

price. The client will then be charged based on how long before the tour it was done. Here follows

an example:

At least 30 days before departure – 25%

15-29 days before departure – 50%

8-14 days before departure – 75%

Less than 8 days – 100%

The non-refundable deposit is usually retained in addition to any airline-imposed fees or penalties.

(Check CPA)

In the event that a booking includes a special fare, up to 100% of the total fare may be applicable

regardless of when the cancellation was made.

Where the booking is for a package, the client will usually be responsible for all cancellation charges

of whatsoever nature imposed by the suppliers providing the component parts of the travel

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 6

arrangements.

For example, Thompsons charges a cancellation fee equal to 10% of the package price on any

finalised booking. Thompsons also reserves the right to charge a cancellation fee of up to 100% of

the total package, in its sole discretion, in particular circumstances. (Check CPA) Any money that the

client has already paid the company is then taken as payment or part payment of any cancellation

charges.

This cancellation clause is only an example – it is advisable not to use this clause but to use the

cancellation clause of your most expensive supplier, which is usually accommodation – if you

marry the two clauses or make yours slightly more expensive in order to cover yourself. For

instance, if your accommodation establishment states that their cancellation 15 days prior would

be 50$ and your cancellation clause says you want 25%, you will be out of pocket.

Conditions for changes requested by the clientMGTMGT Changes can be made where possible. The client is to pay all charges imposed by the

supplier that provides that particular component of the travel arrangements when a booking

is amended any time prior to departure.MGTMGT Fares are re-quoted at the time of amendment.

An administration fee per person may be payable per person for each amendment. MGTMGT After departure, extra expenses incurred as a result of any change will be for the passenger’s

account and any unused service will not be refunded.

Amendments and cancellations en route must be made with our operators directly.

After the trip has commenced, no refunds are usually made for unused services due to your early

departure, late arrival, or missed days on tours.

The Booking Form/Reservation is considered a legal binding contract.

Online reservations and bookings are widely used today by airlines, car rental companies,

accommodation facilities, etc. Before submission, the client is requested to read the Terms and

conditions and cannot proceed without first checking a box indicating that they did read and

agree with the stipulations.

For example...

I have read, understood and agreed to the terms and conditions and can confirm that I am

authorised by my organisation to make this booking. I accept the above registration charges.

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 7

No

Yes

The following might also be stated on a booking form: This booking form constitutes a legally

binding agreement.

Act of God and insurance

Insurance contracts often exclude acts of God from the list of insurable occurrences as a

means to waive their obligations for damage caused by the onset of permanent illness,

lightning, hurricanes, floods or earthquakes; all examples of acts of God

(http://www.duhaime.org/LegalDictionary/a/actofgod.aspx).

The force majeure clause in a contract excuses a party from not performing its contractual

obligations due to unforeseen events beyond its control. These events include natural

disasters such as floods, earthquakes and other "acts of God," as well as uncontrollable events

such as war or terrorist attacks. Force majeure clauses are meant to excuse a party provided

the failure to perform could not be avoided by the exercise of due diligence and care.

However, it does not cover failures resulting from a party's financial condition or negligence.

(http://www.allbusiness.com/legal/contracts-agreements/541-1.html).

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 8

LEARNING UNIT 2: Risk and insurance

Indemnity claims and the law

“A clause excluding the liability on the part of a person or company, whether it be a hospital,

shopping centre, Security Company or fairground, can be incorporated into an agreement between

two parties, either as an agreed term in a contract, or in a notice displayed on the premises. When it

is contained in the written agreement, it is referred to as an exemption or exclusion clause, and when

it is displayed, it is referred to as a disclaimer notice” (Murray, J).

Although exclusion and indemnity clauses are recognised by South African law, it will depend on the

circumstances of each particular case if it would be upheld in court. It is the duty of the institution to

bring the disclaimer under the attention of the public by displaying a disclaimer notice at a

prominent place. The notice should also be clear and concise with regards to exempting the owner

from liability.

Even if the word 'indemnity' is nowhere to be found on a document, there may be an agreement to

'indemnify' another party. For example, a tourist agrees not to hold the tour operator company

responsible for any accidents or injuries that they may suffer while participating in an adventure

activity. "Swim at your Own Risk" signs at an unguarded swimming pool are indicators of an implied

indemnity. If you choose to swim and suffer any injury, you may not be able to sue the owner of the

swimming pool for medical expenses. If you understood the sign's meaning at the time, you agreed

to indemnify the owners. Sometimes an indemnity claim will hold up in court proceedings, but not

always.

Claiming indemnity from damages does not always mean protection from liability. It is therefore

imperative that tour operators and guides do everything in their power to ensure that all activities

and venues comply with high safety regulations. It is also important to take out Liability insurance

(see Risk and indemnity below).

Indemnity also applies to contractual obligations. For example, you incorporate a consultant's work

into a report that you are preparing for a client. The consultant's work is inaccurate and you carry

that mistake through into your own work product. You get sued by your client for breach of contract.

If you have an indemnity clause, you have a means to seek reimbursement from your consultant for

the damages you might have to pay to your client as a result of the error in your consultant's report.

The following is an abstract from the article “Indemnity: A Clause Worth Reading” published in the

Good Company Newsletter on 25 October 2007. In this article, J.H. Perten explains the importance of

the language of the indemnity clause and that one should take note what is stated.

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 9

For example, when does the obligation arise? Does it cover legal fees or just damages? What

happens if more than one party is at fault? There is no exact formula to answer these questions.

You need to look at the language itself. For example, a typical broad indemnity clause might say:

Contractor agrees to indemnify and hold harmless Owner of and from any and all claims,

demands, losses, causes of action, damage, lawsuits, judgments, including attorneys' fees and

costs, arising out of or relating to the work of Contractor.

The above seems to cover every possible type of potential loss, and is applied even in the demand

stage. It also covers attorneys' fees and makes no accommodation for the possibility that someone

else might also be responsible.

A narrower version of this clause might say:

Contractor agrees to indemnify and hold harmless Owner of and from any and all claims,

demands, losses, causes of action, damage, lawsuits, judgments, including attorneys' fees and

costs, but only to the extent caused by, arising out of, or relating to the work of Contractor.

This additional language suggests an apportionment of relative fault.

Maybe you want to cap your exposure. The indemnity might read:

Contractor agrees to indemnify and hold harmless Owner of and from any and all claims,

demands, losses, causes of action, damage, lawsuits, judgments, including attorneys' fees and

costs, to the extent caused by or arising out of or relating to the work of Contractor. In no event

shall the maximum liability hereunder exceed the sum of R _________. or

"In no event shall the maximum liability hereunder exceed the amount actually paid to

Contractor under this contract."

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 10

Indemnity form

This is a legal agreement by which the tour operator/service provider clarifies liability if something

goes wrong with an activity or service offered. The agreement is used to protect the company

against any future claims or other losses (see Customer Protection Framework for more

information). The wording of an Indemnity Clause is very important and must be accurate and

inclusive as possible. Signed indemnities are subjected to the same legal requirements as for

contracts and may be rendered invalid if it does not comply for example if signed by a minor or

under pressure. Even though clients transfer risks from the company by signing an indemnity

form, there might be financial expenses in defending claims brought against a company.

Indemnifying oneself against one’s own negligence

More controversial is the tendency to indemnify oneself against one's own negligence. This

tendency finds its roots in Durban Water Wonderland vs. Botha & Another (1999) where the

Supreme Court of Appeals upheld an appeal that an indemnity, which absolved the appellant from

any liability even if it were to be found to have acted negligently, was valid and enforceable.

This case was however, restricted to the so-called Ticket Purchasing' cases and is yet to be

universally endorsed. It is interesting to note that in a challenge to an indemnity clause in a very

recent river rafting case the courts did not comment negatively on an indemnity which read as

follows: "not to claim from and undertake not to take legal action against and to indemnify, hold

harmless and absolve Storms River Adventures, its owners, members, guides, organisers, servants,

helpers and agents from any or all claims and or liability in connection with loss or damage to any

property or injury to myself or even my death arising from negligence of the above parties or from

any cause whatsoever in the course of any tours and/or transport organised by Storms River

Adventures in which I partake ".

Adapted from Press release from SATIB Risk Management Consultants (No.5 in an series of

articles previously published in SATASA’s Tourism Tattler Journal).

Declining an indemnity insurance

The tour operator should ensure that clients sign an indemnity form prior to departure when they

refuse to take out travel insurance releasing the agency from any claims that may arise usually

covered by it. It is important that all passengers or participants in a tour/ activity sign indemnity

forms individually since a person cannot voluntarily assume risk on behalf of other persons. See

Africancape Travel Indemnity example on the next page.

Travel insurance for travellers

Travelling involves a number of risks and travellers never know what unforeseen events might

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 11

impact on their journey. These may include terrorist attacks, natural disasters (floods,

earthquakes, volcanic eruptions, tsunami’s, etc.), accidents, and personal injuries or falling ill, and

should be taken injuries are all real dangers that exist in our world, and need to be taken into

account when planning a trip to a foreign country.

Travel insurance is insurance that is intended to cover the traveller’s medical expenses, trip

cancellation, lost luggage, flight accident and other losses incurred while traveling, either

internationally or within one's own country.

The insurance broker will take care of the traveller in the event of loss, and personal injury, or death.

AFRICAPE TRAVEL INDEMNITY FORMS TRAVEL INSURANCE

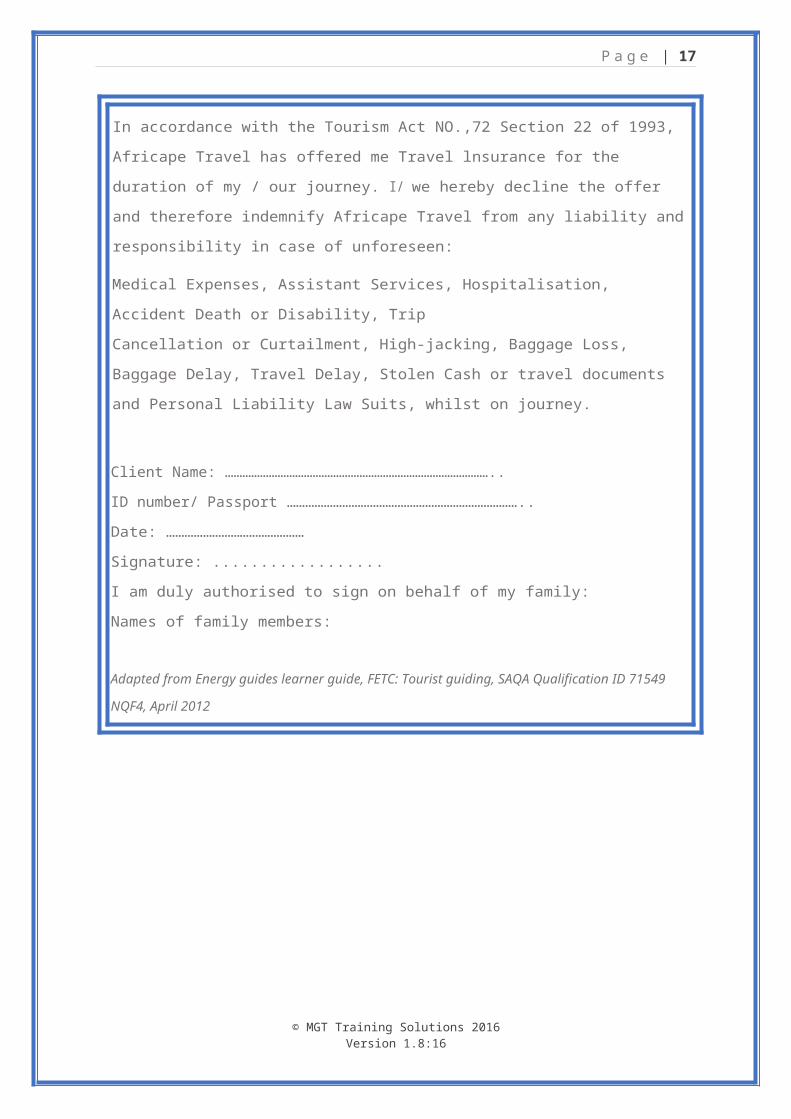

In accordance with the Tourism Act NO.,72 Section 22 of 1993, Africape Travel has offered me Travel lnsurance for the duration of my / our journey. I/ we hereby decline the offer and therefore indemnify Africape Travel from any liability and responsibility in case of unforeseen:

Medical Expenses, Assistant Services, Hospitalisation, Accident Death or Disability, Trip Cancellation or Curtailment, High-jacking, Baggage Loss, Baggage Delay, Travel Delay, Stolen Cash or travel documents and Personal Liability Law Suits, whilst on journey.

Client Name: ………………………………………………………………………………..ID number/ Passport ………………………………………………………………….. Date: ………………………………………Signature: ..................................... I am duly authorised to sign on behalf of my family: Names of family members:

Adapted from Energy guides learner guide, FETC: Tourist guiding, SAQA Qualification ID 71549 NQF4, April

2012

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 12

Registration of South Africans Citizens (ROSA)

The Department of International Relations and Cooperation (DIRCO) offers a voluntary registration

service for South African citizens that are travelling or living abroad. This service is provided in the

event there is a need to contact you to offer urgent advice on a natural disaster or civil unrest or a

family emergency.

Adapted from http://www.gov.za/services/travel-outside-sa/register-south-africans-abroad

viewed on 15 August 2016.

Insurance against risks for tour operator businesses

A tour operator is by law obliged to offer a client insurance (a form of indemnity) to cover any

unforeseen circumstances that may cause the cancellation of a trip or excursion. This could include

accidents, Acts of God, or bankruptcy of the tour operator or travel agency.

Businesses that are registered with SATSA or ASATA are covered by the associations bond for

contingencies.

Bonding provides clients and members assurance that your company is in a position to guarantee

a refund on pre-tour deposits should you or another member be placed under involuntary

insolvency. This is subject to the terms and conditions of the SATSA Lost Advances Fund.

http://www.satsa.com/member-benefits/ viewed on 15 August 2016.

Adapted from http://southafrica.smetoolkit.org/sa/en/content/en/5441/Insurance-for-the-tourism-business viewed on 29 July 2016.

There are various insurance brokers that specialise in insuring tourism businesses e.g. the South

African Insurance Brokers (SATIB). Failing to take out sufficient cover may mean the end of your

business in the event of a claim. It is not worthwhile not planning for risks, or trying to save

money by not taking out insurance.

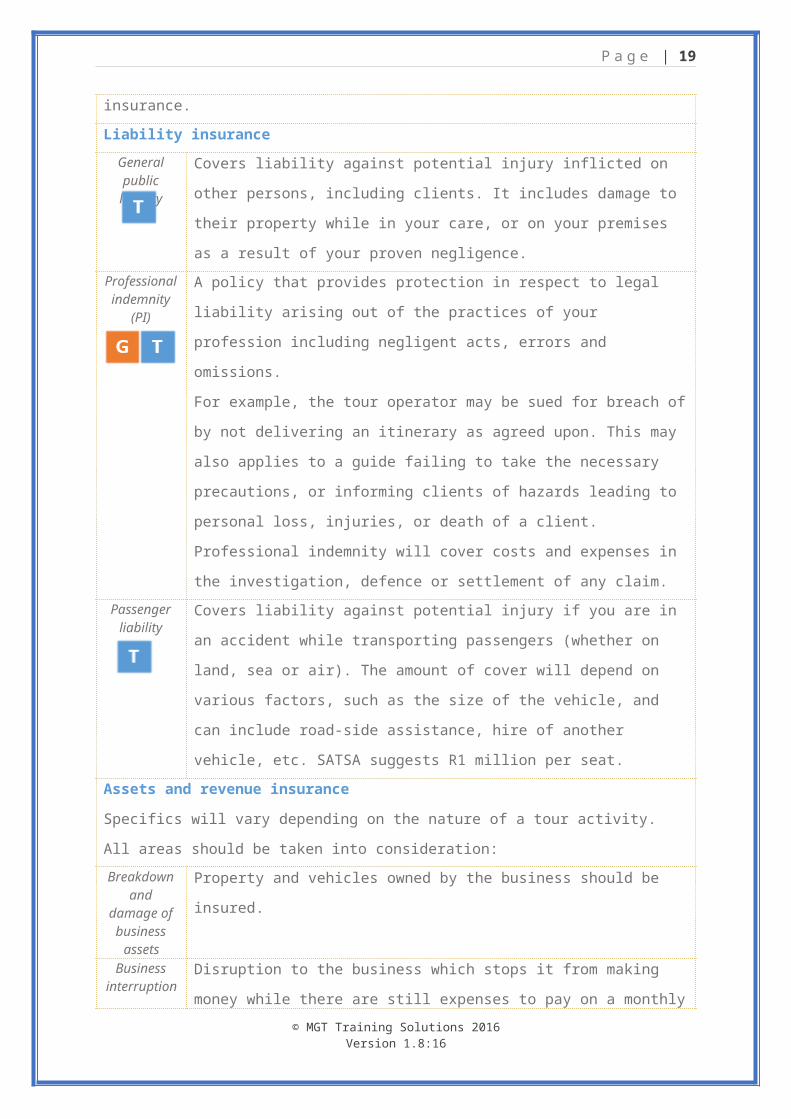

Liability insurance

General public liability

Covers liability against potential injury inflicted on other persons, including clients.

It includes damage to their property while in your care, or on your premises as a

result of your proven negligence.

Professional indemnity

(PI)

A policy that provides protection in respect to legal liability arising out of the

practices of your profession including negligent acts, errors and omissions.

For example, the tour operator may be sued for breach of by not delivering an

itinerary as agreed upon. This may also applies to a guide failing to take the

necessary precautions, or informing clients of hazards leading to personal loss,

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 13

injuries, or death of a client. Professional indemnity will cover costs and expenses

in the investigation, defence or settlement of any claim.

Passenger liability

Covers liability against potential injury if you are in an accident while transporting

passengers (whether on land, sea or air). The amount of cover will depend on

various factors, such as the size of the vehicle, and can include road-side

assistance, hire of another vehicle, etc. SATSA suggests R1 million per seat. Assets and revenue insurance

Specifics will vary depending on the nature of a tour activity. All areas should be taken into

consideration:

Breakdown and damage of business

assets

Property and vehicles owned by the business should be insured.

Business interruption

Disruption to the business which stops it from making money while there are still

expenses to pay on a monthly bases. Interruptions can be caused by bad weather

or any other occurrence that prevents a tour/s to take place. For example, a

company offering adventure activities, loses all the equipment in a fire and cannot

continue all has been replaced. Insurance will pay for the expenses of the business

during the time

Employees

Workers compensatio

n

Protect the business against workplace accident or illness. It does not cover the

owner of the business. Personal income protection insurance and medical aid are

required.

Guidelines for managing risks during tour operations

Risk assessment

Risk is the chance, high or low, that somebody could be harmed by hazards (physical, human

error, etc.) or property loss/damage, together with an indication of how serious the harm or loss

can be. It is the tour operators responsibility to

It is completed prior to a tour, or other service offered to a client by

Identifying hazards

Hazards have the potential to cause harm, injury, loss, and damage.

Slips, trips, theft, cancellations, etc. The group size, culture, attitude, etc. can

play a role in different outcomes.

Who could be affected?

Can include the clients (adults and/children), staff, and business. \

Likelihood Determining the probability of a hazard to cause injury or harm (Options

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 14

include unlikely/possible/likely).

Severity Deciding what the impact of the outcome if a hazard is released (minor or

serious injuries / slight or major financial loss for the company).

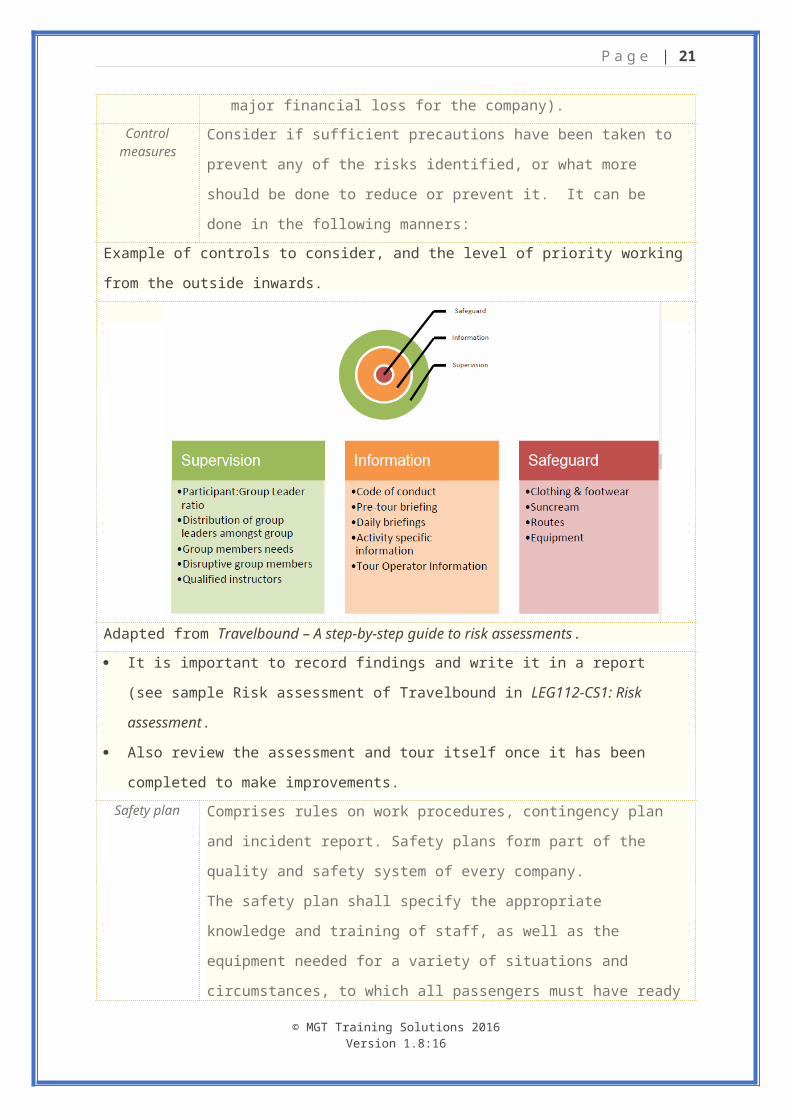

Control measures

Consider if sufficient precautions have been taken to prevent any of the risks

identified, or what more should be done to reduce or prevent it. It can be done

in the following manners:

Example of controls to consider, and the level of priority working from the outside inwards.

Adapted from Travelbound – A step-by-step guide to risk assessments.

It is important to record findings and write it in a report (see sample Risk assessment of

Travelbound in LEG112-CS1: Risk assessment.

Also review the assessment and tour itself once it has been completed to make

improvements.

Safety plan Comprises rules on work procedures, contingency plan and incident report.

Safety plans form part of the quality and safety system of every company.

The safety plan shall specify the appropriate knowledge and training of staff, as

well as the equipment needed for a variety of situations and circumstances, to

which all passengers must have ready access. Passengers must be informed of

relevant safety matters and consequently the operator has to ensure that a staff

member who speaks a foreign language understood by all passengers is present

on all tours and excursions. The safety plan shall stipulate that all tours and

excursions are equipped with reliable telecommunications devices.

The operator must ensure that the number of tourists per staff member who

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 15

serves as a guide on each tour never reaches such a level as to threaten

passengers’ safety and guidelines must be established for this purpose. Staff

members must be thoroughly familiar with the company’s safety plan.

Organised travel

Defined as tours and excursions which travel agencies and tour operators create,

offer and sell, on their own initiative or upon a customer’s request, tourism

related services or leisure activities for professional purposes

Risk assessment A written risk assessment must be compiled for each excursion. This involves

identifying and analysing the dangers which threaten the work environment and

might cause accidents. The risk assessment shall weigh and compare the

seriousness of the risk and the likelihood of a dangerous situation occurring.

Participants and buyers of tours and excursions must be informed of the main

risk factors it involves. There must exist within companies a knowledge of areas

and routes travelled and a familiarity with services on offer. A risk assessment

must contain the following items:

All products and services should be provided in compliance with the safety regulations

applicable to the area of operation so as to ensure the safety of clients/customers.

The legal compliance during the execution of the service should be monitor by a control plan .

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 16

LEARNING UNIT 3: National and international customer protection framework

Consumer Protection Act April 2011 (CPA)

(http://www.westerncape.gov.za/general-publication/national-consumer-protection-act)

The National Consumer Protection Act

Office of the Consumer Protector

Summary

The South African National Consumer Protection Act (CPA) came into effect on 1 April 2011. The

Act is aimed at promoting fairness, openness and good business practice between the suppliers

of goods or services and consumers of such goods and services. The Act only applies to

contracts signed after 1 April, and won't affect anything signed before then. All suppliers of

goods and services need to comply with the Act.

What is covered by the CPA?

The CPA covers a wide range of factors aimed at protecting consumers. Below are some of the

key aspects covered by the Act:

Cooling-off periods

Section 16 of the Act provides for a cooling-off period of five business days in instances where

transactions came from direct marketing - in other words, transactions which were not initiated

by the consumer. The five business day period will commence five days after the day on which

the transaction or agreement was concluded, or the day on which the goods or services were

delivered to the consumer.

Contracts

The Act regulates the term, renewal and cancellation of fixed-term contracts. In terms of

section 14 of the Act, there can be no automatic renewal of a fixed term contract.

Language

The Act does not contain a provision for information to be in an official language. However,

section 22 requires that all information should be in plain language. The Act also requires that

the language used should be appropriate to the group that the goods or services are aimed at.

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 17

Overselling and overbooking

The Act provides for the "reasonableness" test for overselling and overbooking. In terms of this

test a supplier may not accept payment for goods or services where it has no reasonable

intention to supply the goods or services, or where it intends to supply goods or services that

are materially different to the goods or services for which the consumer has paid.

Implied warranty of quality

The Act provides for an implied warranty of quality. In terms of this warranty the

producer/importer, distributor and retailer each warrant that the goods comply with the

requirements and standards outlined in the Act.

Prepaid certificates, credits and vouchers

The Act states that gift or similar vouchers expire either upon redemption or after three years.

Rights of consumers

The Consumer Protection Act gives eight rights to consumers:

1. The right to consumer education

Consumers must be able to access the knowledge and skills needed to make informed and

confident choices about goods and services, while being aware of basic consumer rights and

responsibilities and how to act on them.

2. The right to disclosure and information

Consumers must be provided with the facts needed to make informed choices and ensure their

protection against dishonest or misleading advertising and labelling.

3. The right to choice

Consumers should be able to choose from a range of products and services, offered at

competitive prices, with the assurance of satisfactory quality.

4. The right to representation

Consumer interests should be represented in the making and execution of government policy,

and development of products and services.

5. The right to redress

Consumers must receive a fair settlement of just claims, including compensation for

misrepresentation, or shabby goods or services.

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 18

6. The right to safety

From a trade and industry perspective, consumers should be protected against production

processes, and products and services that are dangerous to health or life.

7. The right to a healthy environment

Consumers should be able to live and work in an environment that is not threatening to the

well-being of present and future generations.

8. The right to access basic needs and service

Consumers should have access to basic goods and services, such as adequate food, clothing,

housing, health care, education, clean water and sanitation.

Adapted from http://www. abta.com/

Most visitors to South Africa arrive from countries with a Consumer Protection Framework in place.

However, the tourism industry has its own unique requirements to address specific issues.

The tour operator organises the services provided by others. Most tour operators do not own the

carrier or the hotel used in the package holiday. The tourist relies upon the skill and judgment of the

tour operator in selecting suitable service providers and guides.

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 19

The question arises as to whether the tour operator is liable for a breach of contract or negligence

by a third party. Two views are generally expressed according to Downes (2003):

1. That the tour operator is only liable when a claim arises from failure to provide the services

indicated in the brochure. They are not liable for the acts or omissions of third parties (e.g.

the carrier/the hotelier) over which they have no control unless the client has established

that the tour operator failed to exercise due skill and care to select a competent

carrier/hotelier etc.

2. That the contract is between the client and the tour operator and the tour operator is liable

whenever there has been a defective performance of any part of the contract.

(http://www.ln.edu.hk/econ/staff/plin/HK.pdf)

EU States

The EU Package Travel Directive endorses the second view. This means that where the tour operator

has contracted with the hotel to provide accommodation to his clients, the tour operator must

accept liability for the hotel’s negligent provision of accommodation, e.g. where the client is injured

due to the lack of safety of the premises.

The EU states have also sought to address the consumer’s vulnerability when engaging in travel

transactions. Here follows some of the issues:

MGTMGT The roles of tour operator and travel agent, the relationship between them and the rights

and obligations which each one of them has with regards to the consumer, are not always

clear. MGTMGT Travel agents and tour operators may become insolvent, leaving tourists stranded at holiday

destinations or evicted from their hotel.MGTMGT The tourist relies on advertisements, brochures, websites etc. and cannot see what he/she is

actually buying.MGTMGT Tour operators may make errors with bookings and confirmations. They may also reserve

the right to make changes and provide “suitable alternatives”.

It has not only been the EU states that have sought to address the need for greater legal protection.

Japan, Australia, Israel, Ontario (Canada), Russian Federation, etc. have also sought to impose a

higher standard of care on the part of travel agents and tour operators than generally required by

Commercial Law. Most western states have also introduced legislation governing unfair contract

terms controlling exclusion and limitation of liability clauses.

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 20

Australia

The Tourist Consumer Protection Working Group (the Group) in Australia was established to

enhance consumer protection of visitors to Australia and to improve compliance in the inbound

tourism market with Australia's laws and regulations.

United States

According to the Customer Protection policy and framework of the US the Government is committed

to protecting the legitimate interests of consumers. The Economic Services Bureau has, since 1 July

2000, taken up the overall policy responsibility for consumer protection. The primary objective of

the consumer protection policy is to ensure that the products (and services) procured by consumers

are safe, the quality is up to their expectation, and the contract terms are fair. It also ensures that

aggrieved consumers have access to conciliation or relevant legal remedies and are given adequate

consumer education and information. The Consumer Council assumes the front-line role in handling

complaints, mediating in consumer disputes and conducting tests and surveys on products and

services.

Americans are known for their demand of high levels of service and numerous claims have been

lodged against tour operators in foreign countries for lack of it. The Federal Trade Commission is

one of the organisations that protects America’s consumers and they post practical information on

their website on a variety of topics to avoid rip-offs and aid in exercising consumer rights (even for

overseas trips).

There are legal advisers offering tourists assistance with claims against tour operators for various

reasons. Tourists can easily find assistance online. Below is an example of such a service offered and

what tourists are advised to claim back for. It is important for both the tour operator and tourist

guide to take note of the various aspects of possible claims.

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 21

Comparison of the functions and powers of organisations with Consumer Protection

responsibilities adapted from Consumer Protection in Hong Kong

http://www.ln.edu.hk/econ/staff/plin/HK.pdf accessed on 23 August 2010

*Non-government organisations

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 22

Holiday accident compensation

If you have suffered an injury or illness whilst on holiday or business abroad, then you may be

entitled to make a claim for compensation.

Your tour operator, airline and hotel staff all have a duty of care to ensure your safety and

provide a safe and hygienic environment.

If your holiday was booked through a travel agent as part of a package holiday then it is likely that

you will be able to bring a claim in the UK against the travel company rather than, for example,

having to bring a claim directly against a hotel owner in a foreign country. If you are involved in a

car accident abroad then you can still claim in your home country, even if the foreign driver is not

insured.

Some of the most common types of accidents abroad include:

MGTMGT Tripping over a defective path or slipping on a wet floor in the hotel. MGTMGT Road traffic accident whilst driving a rental car, motorcycle, minibus or as a pedestrian. MGTMGT Accident as a passenger whilst travelling in a car, coach or taxi. MGTMGT Food poisoning from the hotel restaurant. MGTMGT Sports accident due to poorly maintained or faulty equipment, e.g. skiing accident. MGTMGT Injured whilst on an arranged day excursion.

The claim for your accident abroad will include compensation for the injuries and illness suffered,

loss of enjoyment for you and your family, loss of income due to time off work and costs to help

with medication and rehabilitation.

Our solicitors have many years of experience in helping clients claim compensation for accident or

illness suffered whilst on holiday in Europe, Africa, America, Asia and Australia. As the law in

different countries can make claiming a complex process, our expert solicitors can help you get the

maximum amount of compensation.

If you believe you may be entitled to compensation for an accident or illness whilst on holiday or

require further information, please call our specialist holiday compensation advisors on 0800 567

7866 or fill out a claim form.

Adapted from www.first4lawyers.com (2010)

© LIN SMITH 2016 Version 1.8:16

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 23

Tourists are also advised on the following

Key facts about the law...

For a claim to succeed it is not enough that it was not enjoyed. There may be many reasons for

this, e.g. bad weather or simply a wrong choice of holiday, and things beyond the tour operator’s

control.

You have a legal duty to prove that the tour operator has broken the terms of the holiday

contract. These are known as ‘expressed’ or ‘implied’ terms. Ensure what was promised in the

package is delivered other than outside the tour operator’s control.

To qualify for compensation a loss suffered must be as a direct result of a breach of the holiday

contract. This is not always a straightforward process. How much compensation can be

reasonably expected (if any), depends on the extent to which the holiday was not enjoyed.

A claim may not succeed if not dealt with immediately and the tour operator not given

reasonable opportunity to put things right.

Compensation claims can have three components:

a) Loss of value: the difference between the value of the holiday paid for and the one

actually experienced.

b) Out-of-pocket expenses: refund of any reasonable expenses incurred as a result of the

breach of contract

c) Loss of enjoyment: something to compensate for the disappointment and distress

caused by things going wrong

Where ‘disappointment’ and ‘distress’ form part of the claim, there is little guidance for arbitrators

or judges to help them work compensation levels.

The following is a guide to tourists as to the manner a judge or arbitrator will deal with a claim for

compensation. (www.abta.com).

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 24

Resources and further reading

Philippides, M. (March 1, 2007). Disclaimers, exemption clauses & indemnities. What do these mean

to insurers? (www.deneysreitz.co.za viewed on 14 June 2010).

Kruger, M.L. (2007) Advanced Guiding. www.culturalguiding.com.

Kruger, M.L. (2010). Basics of Guiding. www.culturalguiding.com.

Murray, J. Are Verbal Contracts Legal? Jean’s Business Law. (http://biztaxlaw.about.com viewed on

14 June 2010).

Perten, J.H. Good Company Newsletter - Indemnity: A Clause Worth Reading. Thursday, October 25,

2007. (www.sheehan.com/publications/good-company-newsletter/Indemnity--A-Claus viewed on 12

June 2011).

Vrancken et al. (2002). Tourism and the Law in South Africa. Butterworths.

3 Types of Insurance All Tour Operators Need. https://www.rezdy.com/blog/3-types-of-insurance-

all-tour-operators-need/ 9 MAY 2014

Rob Brindley. Generic risk assessments - visits and

activitieshttps://www.dorsetforyou.gov.uk/article/394858/Generic-risk-assessments---visits-and-

activities

Website

http://wiki.answers.com – legality of object viewed on 14 June 2010.

http://wordnetweb.princeton.edu/perl/webwn?s=agreement viewed on 14 June 2010.

www.adventureescapades.co.za viewed on 14 June 2010.

www.bcb.uwc.ac.za

(Jean's Business Law / Taxes: U.S. Blog by Jean Murray, US Business Law) – Are Verbal contracts

legal? viewed on 14 June 2010.

www.businessdictionary.com viewed on 14 June 2010.

www.cipro.co.za – registration of a business viewed on 14 June 2010.

www.ftc.gov viewed on 14 June 2010.

www.indemnityforms.com viewed on 14 June 2010.

© MGT Training Solutions 2016 Version 1.8:16

P a g e | 25

www.investorglossary.com – disclaimer viewed on 14 June 2010.

www.iss.co.za INSTITUTE FOR SECURITY STUDIES viewed on 14 June 2010.

www.labour.gov.za on 8 June 2011.

www.netlawman.co.uk – Terms and conditions of contracts viewed on 14 June 2010.

www.wikipedia.com viewed on 14 June 2010.

www.wisegeek.com – liability and negligence viewed on 14 June 2010.

© MGT Training Solutions 2016 Version 1.8:16