Leadership in life insurance - Prudential plc/media/Files/P/Prudential...ICICI Prudential Bajaj...

40

Leadership in life insurance April 2008

Transcript of Leadership in life insurance - Prudential plc/media/Files/P/Prudential...ICICI Prudential Bajaj...

Leadership in life insurance

April 2008

2

Agenda

Indian life insurance opportunity

Organisational overview

Performance highlights

3

Agenda

Indian life insurance opportunity

Organisational overview

Performance highlights

4

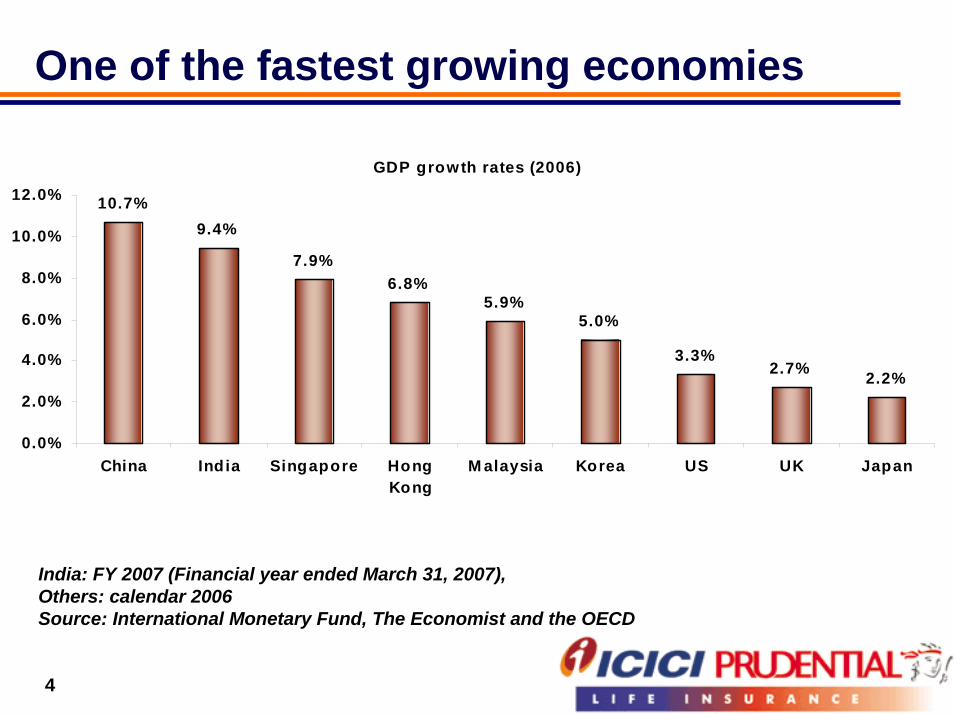

One of the fastest growing economies

GDP growth rates (2006)

10.7%9.4%

7.9%6.8%

5.9%5.0%

3.3%2.7% 2.2%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

China India Singapore HongKong

M alaysia Korea US UK Japan

India: FY 2007 (Financial year ended March 31, 2007), Others: calendar 2006Source: International Monetary Fund, The Economist and the OECD

5

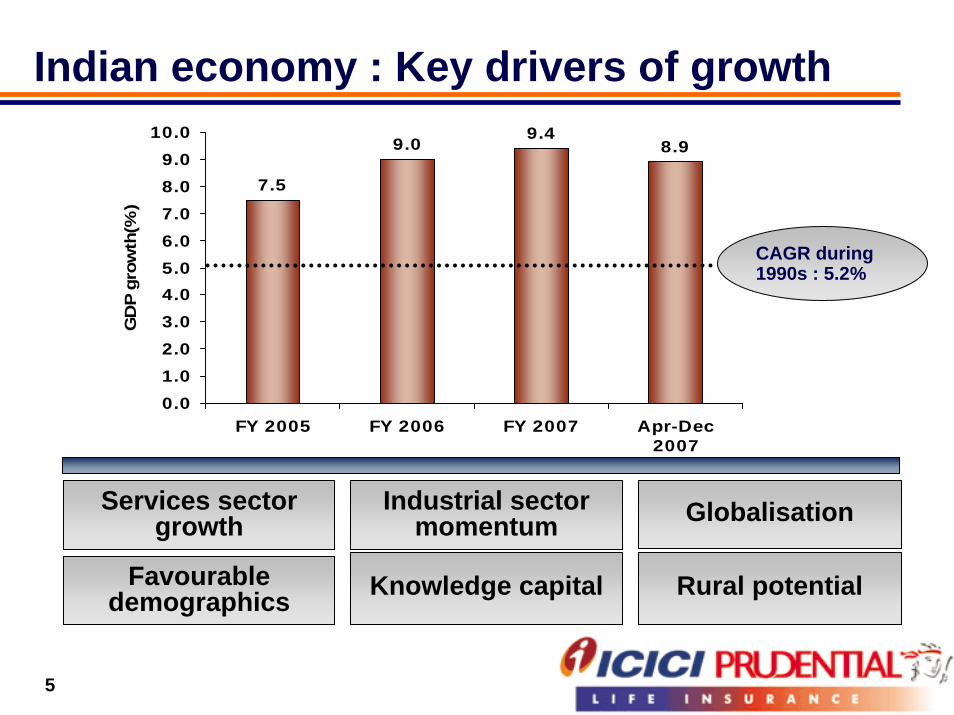

7.5

9.0 9.48.9

0.01.02.03.04.05.06.07.08.09.0

10.0

FY 2005 FY 2006 FY 2007 Apr-Dec2007

GD

P gr

owth

(%)

CAGR during 1990s : 5.2%

Indian economy : Key drivers of growth

Services sector growth

Industrial sector momentum Globalisation

Favourabledemographics Knowledge capital Rural potential

6

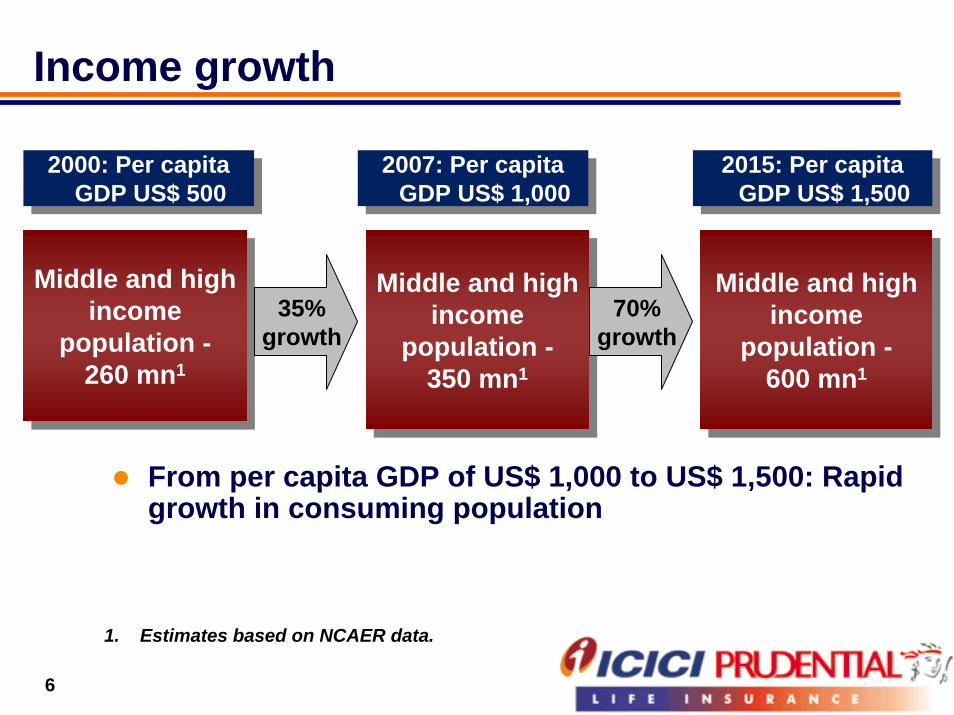

Income growth

2000: Per capita GDP US$ 500

2000: Per capita GDP US$ 500

2007: Per capita GDP US$ 1,000

2007: Per capita GDP US$ 1,000

2015: Per capita GDP US$ 1,500

2015: Per capita GDP US$ 1,500

Middle and high income

population -260 mn1

Middle and high income

population -260 mn1

Middle and high income

population -350 mn1

Middle and high income

population -350 mn1

Middle and high income

population -600 mn1

35% growth

70% growth

Middle and high income

population -600 mn1

From per capita GDP of US$ 1,000 to US$ 1,500: Rapid growth in consuming population

1. Estimates based on NCAER data.

7

Increasing proportion of working population

2006 2026(Age group)

To further fuel India’s growth and rising disposable income levels

Shift towards nuclear families

Increased savings and protection needs

(percentage of population)

5

32

8

23

6963

65+

15-64

0-14

Source: Census of India

8

India life insurance opportunity

Only a third of the target population is insured

Life insurance penetration & per capita (2006)

33

1,617

34189

1,480

1,790

2,4562,829

5,140

13.1%

4.1%

8.3%

4.0%

9.2%7.9%

3.2%1.7%

5.4%

0

1000

2000

3000

4000

5000

6000

UK Japan Hong Kong US Singapore Korea M alaysia China India

Insu

ranc

e pe

r ca

pita

(U

SD

)

0 .0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Insu

ranc

e pe

netr

atio

n

Source: Swiss Re

9

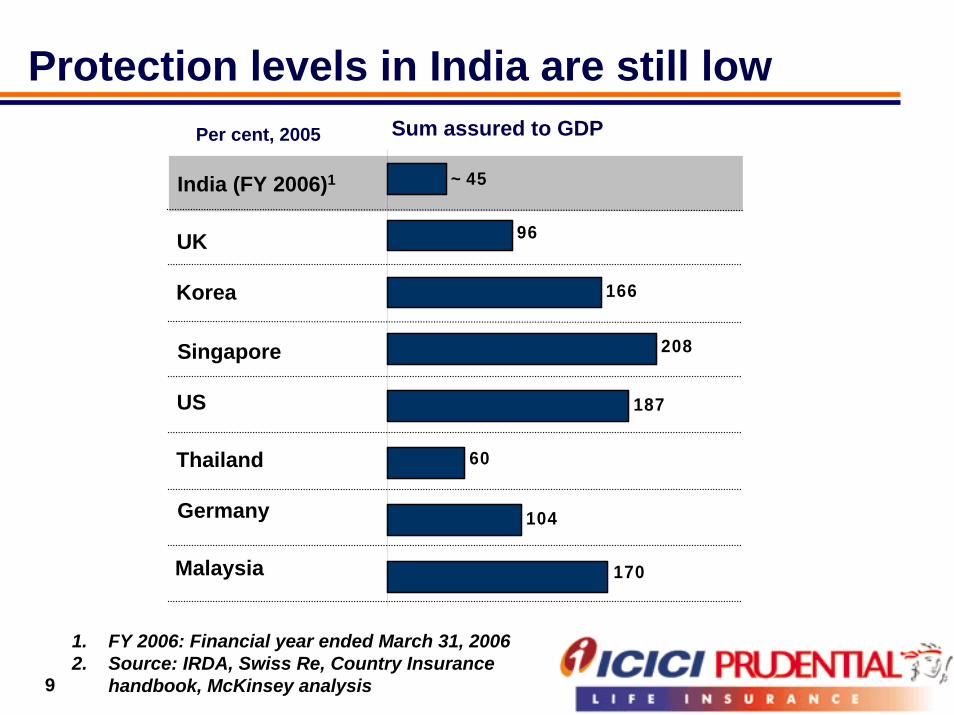

Protection levels in India are still low Sum assured to GDPPer cent, 2005

~ 45

166

96

208

187

60

104

170

India (FY 2006)1

UK

Korea

Singapore

US

Thailand

Germany

Malaysia

1. FY 2006: Financial year ended March 31, 20062. Source: IRDA, Swiss Re, Country Insurance

handbook, McKinsey analysis

10

Evolution of industry: Growth

1. FY 2007: Financial year ended March 31, 20072. Source: IRDA, Swiss Re

Penetration (as a% of GDP)

Insurance premiumper capita (Rs )

Number of players

1.2%

~280

1

FY 2000

NB premium (Rs bn) 64.00

270.00

CAGR of 42%

CAGR of 30%

4.1%

16

FY 20071

754.00

~1,510

1,696.00Total premium (Rs bn)

11

Evolution of industry: Changing landscapeTraditional products

Linked products: 79% of the overall market

Life productsEmergence of Health & Pensions: 16% of overall market

Agency channel

Multi channel distribution

Service delivery through branches only

Technology driven service delivery: Call centres, E-mail

12

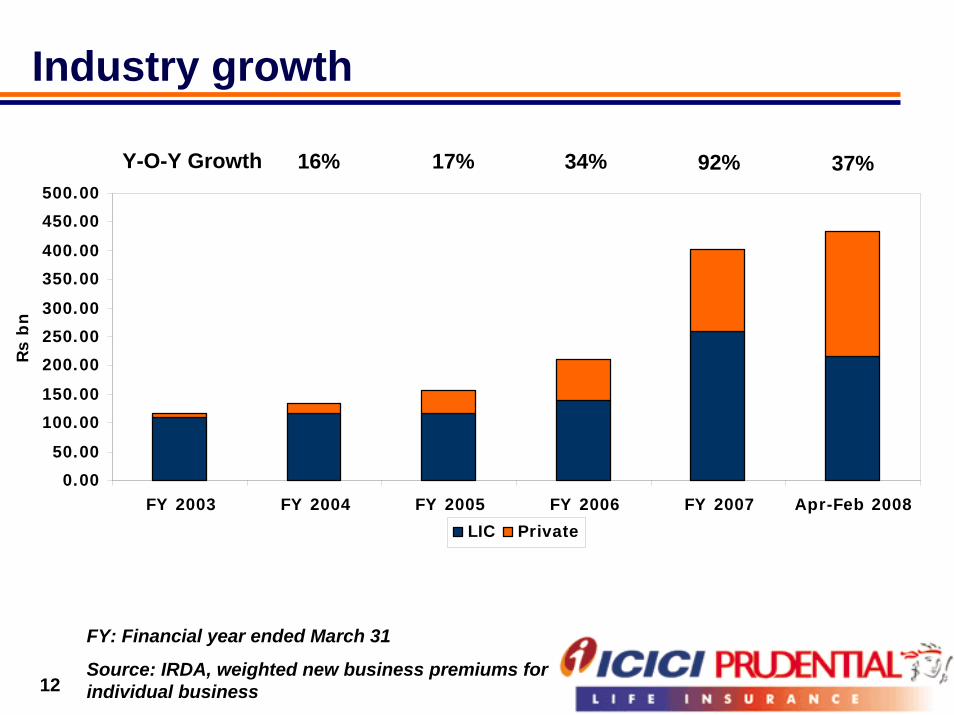

Industry growth

Y-O-Y Growth 16% 17% 34% 92% 37%

0.0050.00

100.00150.00

200.00250.00300.00

350.00400.00

450.00500.00

FY 2003 FY 2004 FY 2005 FY 2006 FY 2007 Apr-Feb 2008

Rs b

n

LIC Private

FY: Financial year ended March 31

Source: IRDA, weighted new business premiums for individual business

13

Agenda

Indian life insurance opportunity

Organisational overview

Performance highlights

14

Key strategic elements

ProductNeed-based innovative and flexible products

Scalable delivery architecture

DistributionBuild-up of agencyPioneering alternate distribution

High brand salience

Service

PeopleTalent from diverse industriesCapability development across functions

Aggregate capital infusion of Rs 37.72 bn (USD 945 mn)

15

Sustained private market leadership

FY 2007

Apr-Feb 2008

FY 2003

FY 2004

FY 2005

FY 2006

1

2

3

4

5

FY: Financial year ended March 31

Based on weighted new business premiums for individual business

16

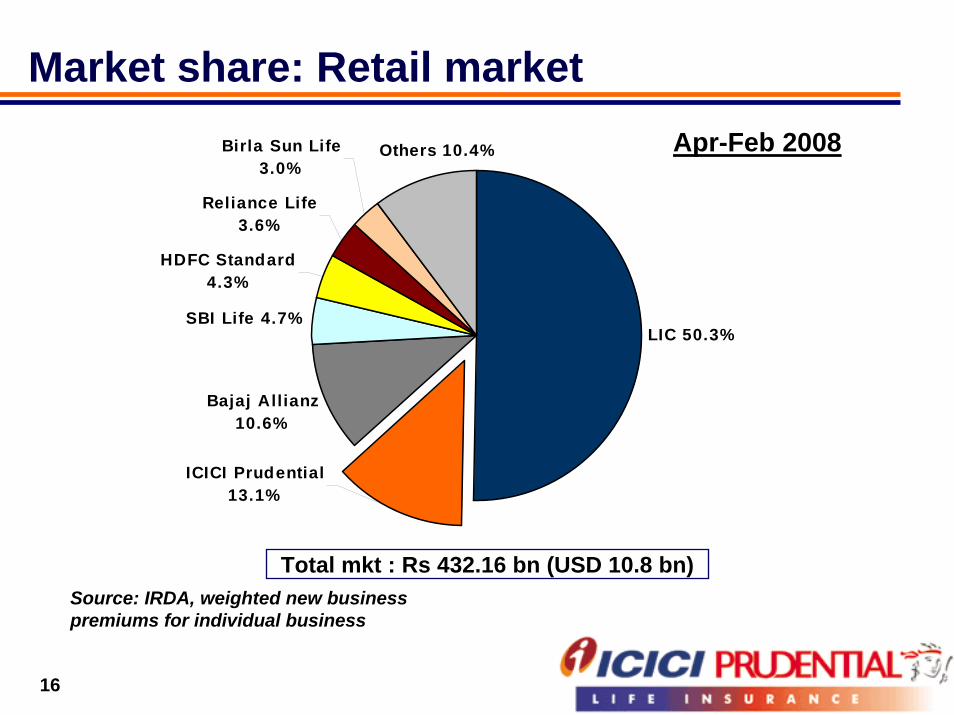

Market share: Retail market

LIC 50.3%

Bajaj Allianz 10.6%

SBI Life 4.7%

HDFC Standard 4.3%

Reliance Life 3.6%

Birla Sun Life 3.0%

ICICI Prudential 13.1%

Others 10.4% Apr-Feb 2008

Total mkt : Rs 432.16 bn (USD 10.8 bn)Source: IRDA, weighted new business premiums for individual business

17

Leadership on other parameters

0.0010.0020.0030.0040.0050.0060.0070.0080.0090.00

ICICI Prudential

BajajAllianz

SBI Life

HDFCStandard

Reliance Life

Rs

bn

Single Initial Renewal

Source: Life Insurance Council website

Assets held

40%

28%

14% 45%

Total premium

Apr-Dec 2007

Apr-Dec 2007284.09

125.79

88.59 86.01

30.50

0.00

50.00

100.00

150.00

200.00

250.00

300.00

ICICI Prudential

BajajAllianz

SBI Life

HDFCStandard

Reliance Life

Rs

bn

14%

18

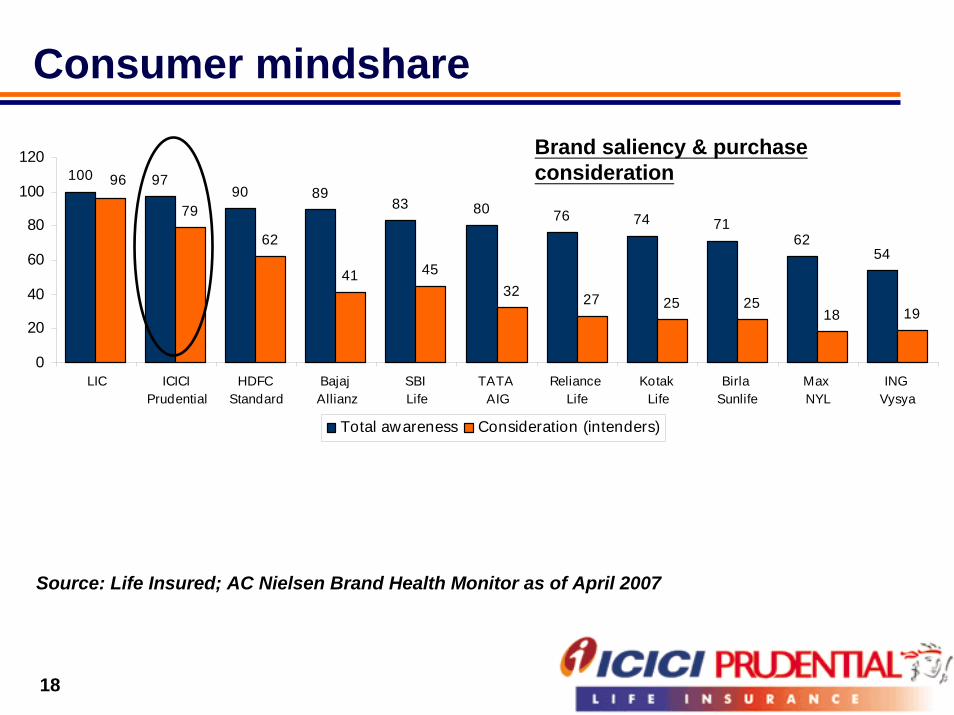

Consumer mindshare

100 9790 89

83 80 76 74 7162

54

79

62

41 4532 27 25 25

18 19

96

0

20

40

60

80

100

120

LIC ICICI Prudential

HDFC Standard

Bajaj Allianz

SBI Life

TATA AIG

Reliance Life

Kotak Life

Birla Sunlife

Max NYL

ING Vysya

Total awareness Consideration (intenders)

Brand saliency & purchase consideration

Source: Life Insured; AC Nielsen Brand Health Monitor as of April 2007

19

Rapid expansion in policy base …

01

2

3

4

5

6

7

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Mn

December2000

October2004

February2006

October2006

M arch2007

August2007

January2008

M arch2008

16 months

8 months

44 months

5 months

5 months

5 months

2 months

20

… backed by market innovationContinued development of the market with new products and

services

Leading the evolution of unit linked productsIntroduction of LifeStage RP: Automatic asset allocation and increased protection

Focus on emerging segmentsHealth: Introduction of 9 health products, including innovative health product for diabeticsPensions: Emphasis on retirement planning backed by a comprehensive product suite

Health Link

Pensions Link

Health Link

21

Health opportunity

Over 85% of the population without health cover

Low health penetration

Only 1.6% of private healthcare expenses1 covered through insurance

High out of pocket

expenditure

Around 75% of population in informal sector without employer-provided coverage

Large informal sector

15.9% CAGR of private health expenses in last five years

Increase in health spends

1. Estimated at Rs 1400.00 bn

22

Health business: Building capabilitiesHealth Link

Dedicated direct distribution channel extended to 53 cities

Pharmacy channel launched

Innovative products

Crisis Cover: A comprehensive policy covering 35 critical illnesses, disability & death

Hospital Care: A fixed benefit hospital plan with cashless facility

23

… backed by market innovationContinued development of the market with new products and

services

Leading the evolution of unit linked productsIntroduction of LifeStage RP: Automatic asset allocation and increased protection

Focus on emerging segmentsHealth: Introduction of 9 health products, including innovative health product for diabeticsPensions: Emphasis on retirement planning backed by a comprehensive product suite

Health Link

Pensions Link

Pensions Link

24

Retirement opportunity

0200400600800

100012001400

2000 2005 2010 2015 2020 2025

Year

No.

of p

eopl

e (M

n)

Population Below 20 yrs Population between 20-59 yrs Population above 60 yrs

7688 99 115 135 159

Age group of 60+ is the fastest growing and will almost double in the next 20 years

Source: Oasis Committee Report

Pensions Link

25

Comprehensive product offeringProducts for the accumulation phase

Advanced ULIP products with automatic asset allocationDifferent premium paying optionsRange of funds offered

Products for the payout phaseRange of annuity options

Life annuity, joint life annuity, annuity with return of purchase priceAnnuity guaranteed for 5, 10, 15 years

Launch of Annuity Card First of its kind debit card in Asia for annuitants

Philosophy: Different customers, different needs

Pensions Link

26

Retirement solutions campaignRetirement solutions: Key focus area of the company in brand communication

Commenced with ‘Retire from work, not life’ campaign

Retirement planning weaved into the recent corporate campaign ‘Jeetey Raho’

New campaign: ‘Plan your NUMBER with us’To enhance action orientation of consumers in planning for retirement

27

Distribution strategyContinue to expand to take advantage of market size and increased affluence

New branch roll out @ ~2 per day in the last 8 quartersIncrease in direct and partnership distribution

Pan India coverage through 3,300 touch pointsContinued strengthening of partnership distribution Dedicated direct distribution channel extended to 53 citiesLaunched pharmacy channel

Widening international reachOffices in Dubai & Bahrain

28

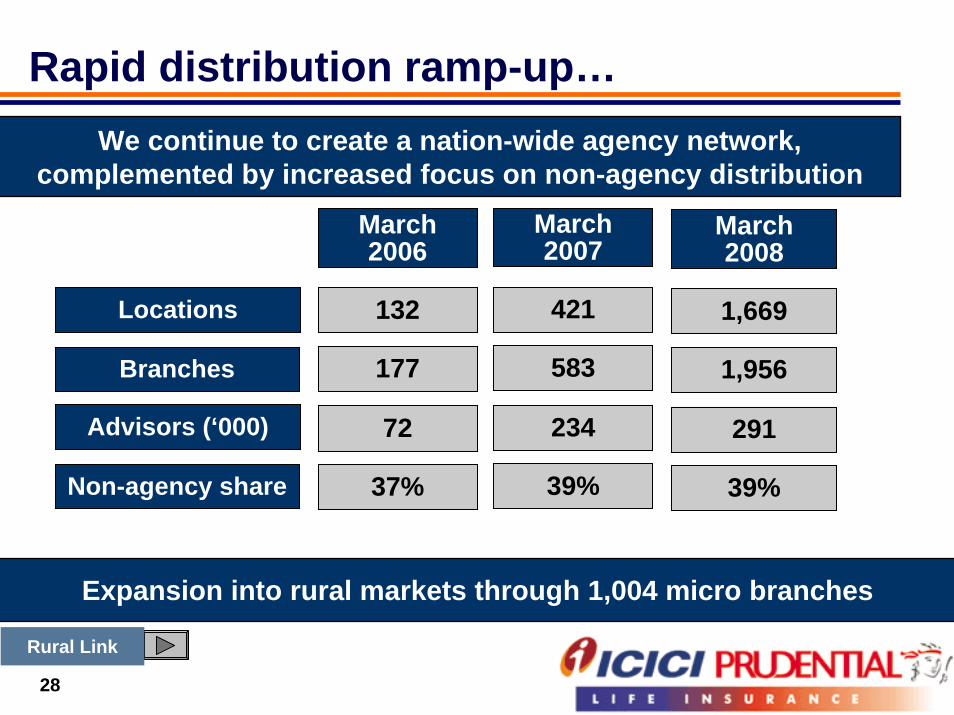

Rapid distribution ramp-up…We continue to create a nation-wide agency network,

complemented by increased focus on non-agency distribution

March 2007

March 2006

March 2008

421Locations 132 1,669

583177Branches 1,956

Advisors (‘000) 23472 291

39%37%Non-agency share 39%

Expansion into rural markets through 1,004 micro branches

Rural Link

Rural Link

29

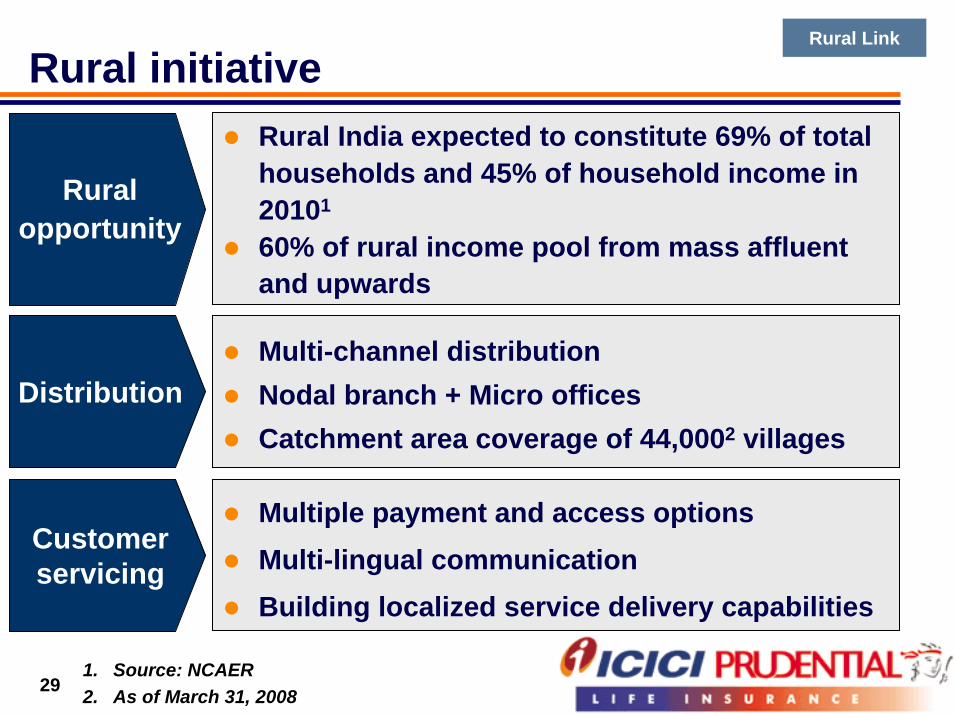

Rural initiativeRural India expected to constitute 69% of total households and 45% of household income in 20101

60% of rural income pool from mass affluent and upwards

Ruralopportunity

Multi-channel distributionNodal branch + Micro officesCatchment area coverage of 44,0002 villages

Distribution

Multiple payment and access options Multi-lingual communicationBuilding localized service delivery capabilities

Customer servicing

1. Source: NCAER2. As of March 31, 2008

30

Rural Link

31

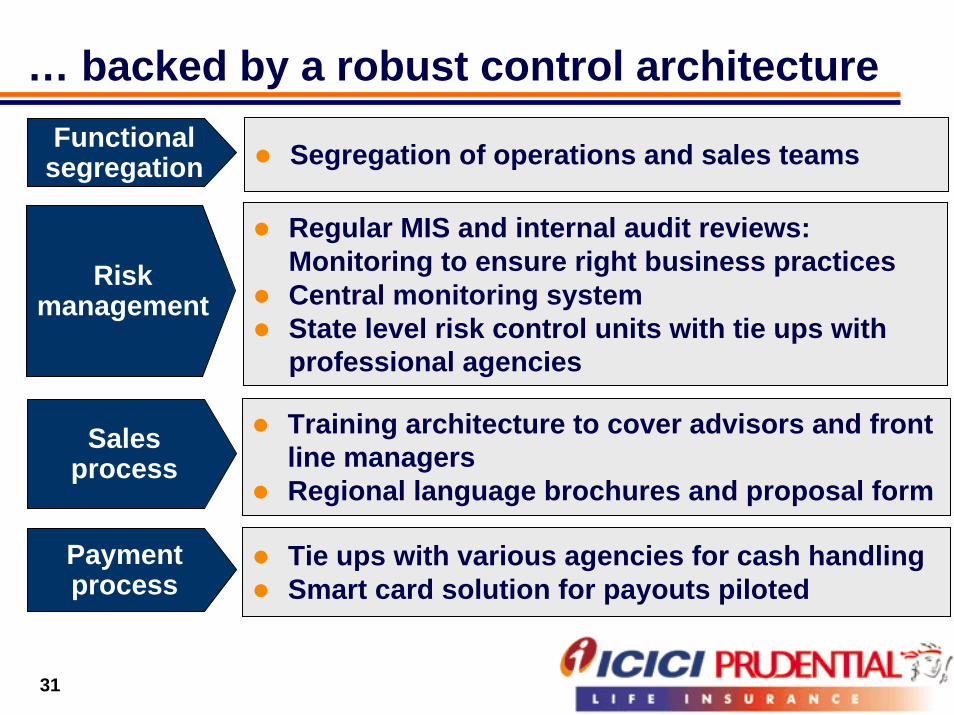

… backed by a robust control architecture

Segregation of operations and sales teamsFunctional segregation

Regular MIS and internal audit reviews: Monitoring to ensure right business practicesCentral monitoring systemState level risk control units with tie ups with professional agencies

Risk management

Training architecture to cover advisors and front line managersRegional language brochures and proposal form

Sales process

Tie ups with various agencies for cash handlingSmart card solution for payouts piloted

Payment process

32

Our service promise…

Vision Statement

“To be the dominant

Life, Health & Pensions player

built on trust

by world class people & service”

Customer First Value

Own the customer; deliver the

promise

Keep customer interest at the center of all

decisions

Promise what you can, deliver it to the

end

Proactively seek voice of customer and

act on it

Customer Experience StatementAfter each experience, we want our customers to feel confident about having made the right choice

We will do this by ensuring all our dealings are based on the “F.A.C.T.” principle.The result will be that we are their first choicefor financial security so that they will stay with us, buy more from us & recommend us to others”

The PromiseFAIR AccurateConsistentTransparent

33

…delivering consistent results

RecognitionAvaya GlobalConnect customer Responsiveness Award 2008Web 18 and Frost & Sullivan Genius of the Web Award

Customer satisfaction

Tracking of key satisfaction metrics:Satisfaction with sales experienceSatisfaction with service experienceComplaint ratioRepeat complaint ratio

Process efficiencies

Identify key customer facing processesRegular monitoring of sigmas

34

Agenda

Indian life insurance opportunity

Organisational overview

Performance highlights

35

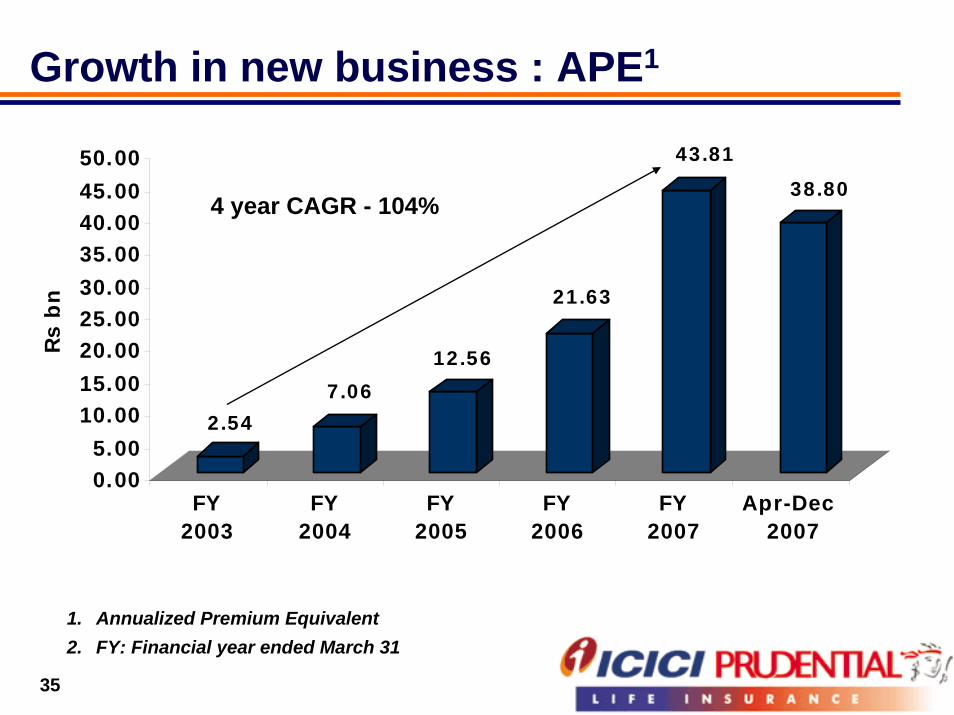

Growth in new business : APE1

2.547.06

12.56

21.63

43.81

38.80

0.005.00

10.0015.0020.0025.0030.0035.0040.0045.0050.00

Rs b

n

FY2003

FY2004

FY2005

FY2006

FY2007

Apr-Dec 2007

4 year CAGR - 104%

1. Annualized Premium Equivalent2. FY: Financial year ended March 31

36

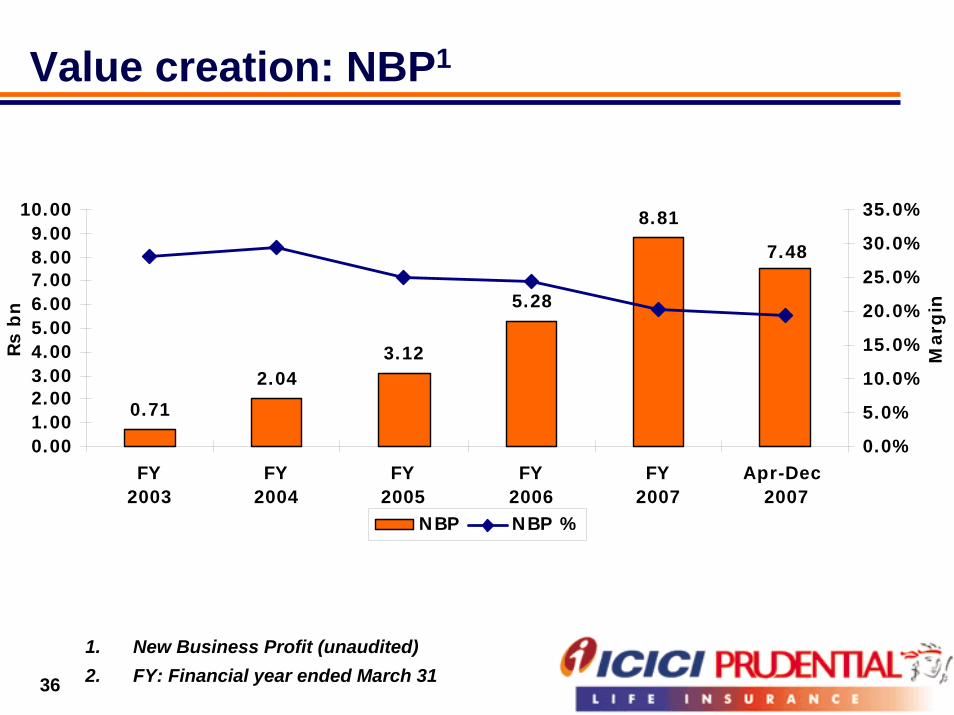

Value creation: NBP1

0.712.04

3.12

5.28

8.81

7.48

0.001.002.003.004.005.006.007.008.009.00

10.00

FY2003

FY2004

FY2005

FY2006

FY2007

Apr-Dec 2007

Rs b

n

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Mar

gin

NBP NBP %

1. New Business Profit (unaudited)2. FY: Financial year ended March 31

37

Robust growth in assets held

6.100.56 13.28

3.35 27.83

10.48

42.52

45.69

63.10

95.09

87.49

197.69

0.00

50.00

100.00

150.00

200.00

250.00

300.00

Rs

bn

M arch 2003

M arch 2004

M arch 2005

M arch 2006

M arch 2007

February 2008

Debt Equity

Linked funds constitute 87% of total assets held

6.66 16.6338.31

88.21

158.18

285.18

38

Expense ratio trend

Expense ratio: Operating expenses / (Total premium less 90% of single premium & 50% of limited pay products)

74%

54%

14%14%

26%

17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

FY 2002 FY 2003 FY 2004 FY 2005 FY 2006 FY 2007

FY: Financial year ended March 31

39

Summary of key achievements

Sustained private market leadership: 7 years in a row

More than 7 million policies sold

Over Rs 280.00 bn (USD 7.0 bn) of assets held

Awarded most respected private life insurer

Fitch rating of ‘AAA (Ind)’

NBP of Rs 7.48 bn (USD 189.9 mn) in Apr-Dec 2007

Total premiums of Rs 77.58 bn (USD 2.0 bn) in Apr-Dec 2007

40

Safe harbourExcept for the historical information contained herein, statements in this release which contain words or phrases such as 'will', 'would', ‘indicating’, ‘expected to’ etc., and similar expressions or variations of such expressions may constitute 'forward-looking statements'. These forward-looking statements involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those suggested by the forward-looking statements. These risks and uncertainties include, but are not limited to our ability to successfully implement our strategy, our growth and expansion in business, the impact of any acquisitions, technological implementation and changes, the actual growth in demand for insurance products and services, investment income, cash flow projections, our exposure to market risks, policies and actions of regulatory authorities; impact of competition; experience with regard to mortality and morbidity trends, lapse rates and policy renewal rates; the impact of changes in capital , solvency or accounting standards , tax and other legislations and regulations in the jurisdictions as well as other risks detailed in the reports filed by ICICI Bank Limited, our holding company, with the United States Securities and Exchange Commission. ICICI Bank and we undertake no obligation to update forward-looking statements to reflect events or circumstances after the date thereof.