LDT Program 2007 Master’s Project Vic Vuchic Greg Warman.

33

LDT Program 2007 Master’s Project Vic Vuchic Greg Warman

-

Upload

simon-rich -

Category

Documents

-

view

219 -

download

0

Transcript of LDT Program 2007 Master’s Project Vic Vuchic Greg Warman.

LDT Program 2007 Master’s Project

Vic VuchicGreg Warman

Have you ever been asked for advice?

responsibility

responsibility

• sociology• social exchange theory

• evolutionary biology• altruism as adaptive

trait

• psychology• diffusion• reciprocity• liking

• religion• prescribed value

system as identity

• philosophy• Hume’s ’generous

action’

• political theory• marxism

• education• student as teacher

design

personal finances

a fiscal crisis is looming

2005 was the first year since the Great Depression with a personal negative

savings rate.

a fiscal crisis is looming• About 43% of American families spend more than they earn

each year.• 2003 Federal Reserve

• As of 2004, of households that have at least one credit card, average households debt is over $9,000.

• CardTrack.com

• Personal bankruptcies have doubled in the past decade.• The Fragile Middle Class: Americans in Debt

• Average household debt excluding mortgages was $18,654/household!

• Federal Reserve Board, 2003 survey

• Formal “financial literacy” tests among youth reveal a significant decrease in financial knowledge.

• 2006 Jumpstart Survey, the mean was score of 52% (a passing grade was 60%)

learning problem

• People with an understanding of financial concepts have better financial habits than others who do not understand basic personal finances.

• Given that financial literacy is not mandatory in most school curriculums, people educated in the U.S. are mostly left to fend for themselves.

Something significant has to be done to teach financial literacy in a manner that impacts behavior.

Our educational environment is not effectively teaching financial concepts to its citizens and this is reflected in people’s financial habits.

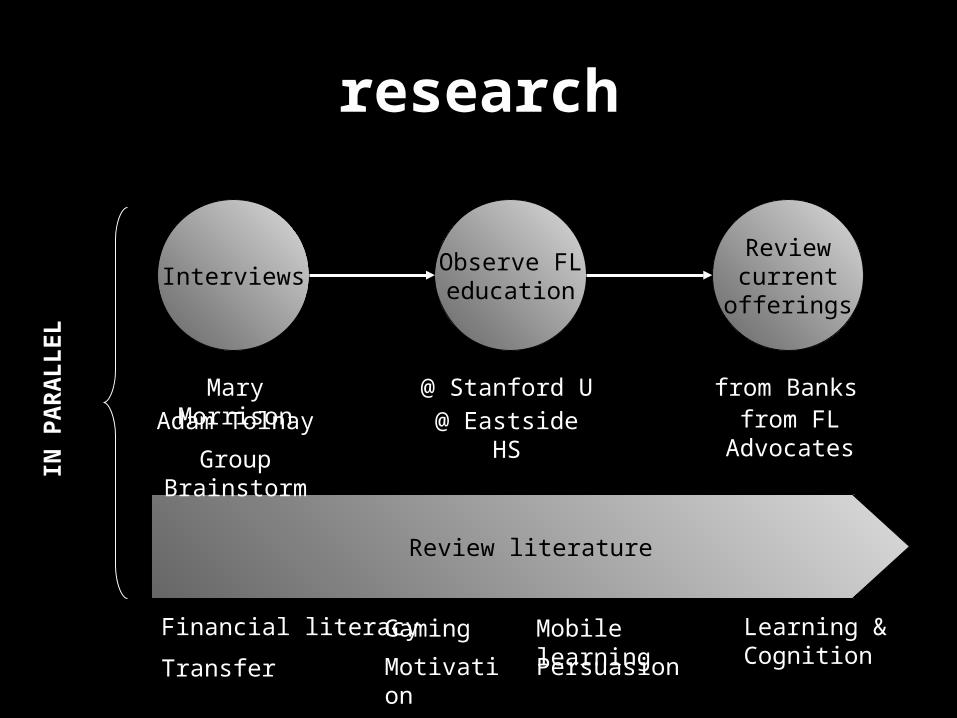

our process

1. Research2. Synthesize findings3. Design Solution4. Test Prototype 1: Internal5. Test Prototype 2: External6. Launch Beta (today!)7. Conduct Assessment

research

InterviewsObserve FLeducation

Reviewcurrent

offerings

Review literature

Financial literacy

Transfer

Gaming

Motivation

Mobile learning

Persuasion

Learning & Cognition

Mary Morrison

Adam Tolnay

@ Stanford U

@ Eastside HS

from Banksfrom FL Advocates

IN P

AR

ALLEL

Group Brainstorm

1. It’s critical to get information to individuals at a time in their life when they’re most receptive to learning and applying it (Prochaska and Velicer, 1997)

synthesis & design

Target LearnerStudents, High School or College, on the verge

of graduating and entering the workforce.

2. Rudimentary financial knowledge is lacking among youth (OECD Report, 2003).

synthesis & design

Learning GoalsBasic, sequential building blocks regarding Cash

Flow, Credit Management, and Savings.

3. Challenges vary from person-to-person and it is counter-productive to “hit people over the head with what they’re not doing.” (Gurney, 1988; NEFE Conference Proceedings, 2004)

synthesis & design

Pre-AssessmentDetermine the learner’s financial habits and then

match him / her with a similar protégé. The resulting game scenario is relevant for the

learner.

4. For financial literacy, experience is cited as the best teacher, followed by learning from friends & family (Hilgert et al, 2003)

synthesis & design

Model ExperienceLearner navigates scenarios and witnesses (and

hears about!) the direct impact on his/her protégé

5. Behavioral economics demonstrates that people will make decisions counter to their best interest because of ‘loss aversion’ in today’s marketing saturated culture. (NEFE Conference Proceedings, 2005; Tversky and Kahneman, 1991)

synthesis & design

MetricsPoor financial decisions are shown to be a loss

of happiness and future freedom

6. There is an asymmetry between the financial literacy concepts taught in most financial literacy interventions and how they manifest in practice. The mismatch of elements impedes transfer, (Thorndike and Woodsworth, 1901).

synthesis & design

Context of DecisionsColloquial language and the ‘money map’ bridge

concept and practice. Through the mobile interaction the timing of financial decisions more

closely resembles reality.

7. Financial matters are emotionally charged. Cultural taboos, fear of being duped, and frustration with financial jargon impede financial literacy education.

synthesis & design

Framing & Structure of FS!FS! is a single-user experience and positioned as an opportunity to learn how to “stick it to the

man!”. And yes, gameplay is fun!

8. Conflict in the brain (emotional vs. analytical) makes it challenging to maintain a patient, long-term view to finances. (Laibson, 1997; NEFE Conference Proceedings, 2005)

synthesis & design

ImplementationFS! will include a “mechanism for action” to help

the learner start practicing good financial behaviors immediately.

prototyping

Evolving the concept:1) Internal

– Technology: Excel, Word, and “SneakerNet”

2) External– Technology: Flash and SMS

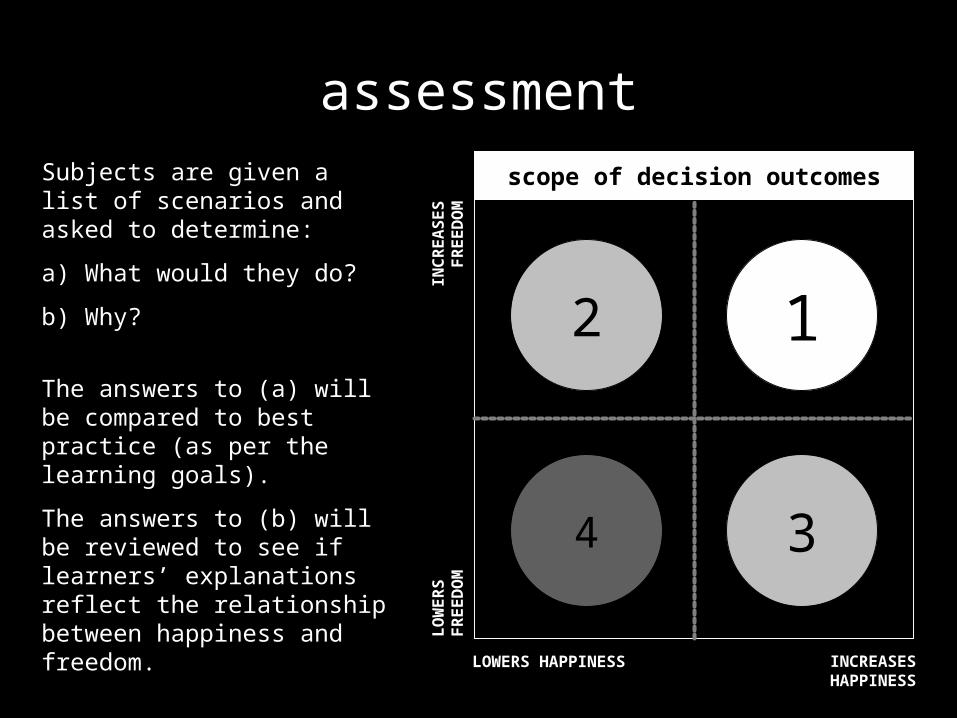

assessment

4

1

LOWERS HAPPINESS

INCREASES HAPPINESS

LO

WE

RS

FR

EE

DO

MIN

CR

EA

SE

SF

RE

ED

OM

2

3

scope of decision outcomesSubjects are given a list of scenarios and asked to determine:

a) What would they do?

b) Why?

The answers to (a) will be compared to best practice (as per the learning goals).

The answers to (b) will be reviewed to see if learners’ explanations reflect the relationship between happiness and freedom.

questions?

appendices

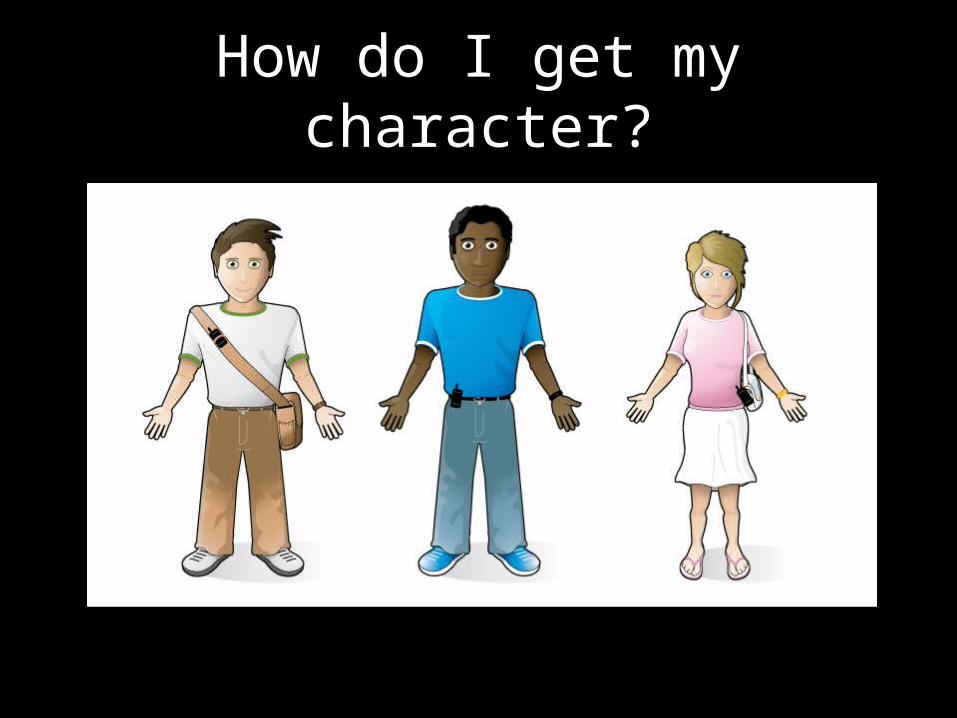

How do I get my character?

How do I get my character?

1. Complete the pre-assessment answering questions like “If I were to receive an unexpected gift of money I would…”

Based on your determined “money personality”, you receive a circumscribed list of possible characters.

These characters’ scenarios reflect the type of money challenges appropriate for one’s “money personality”.

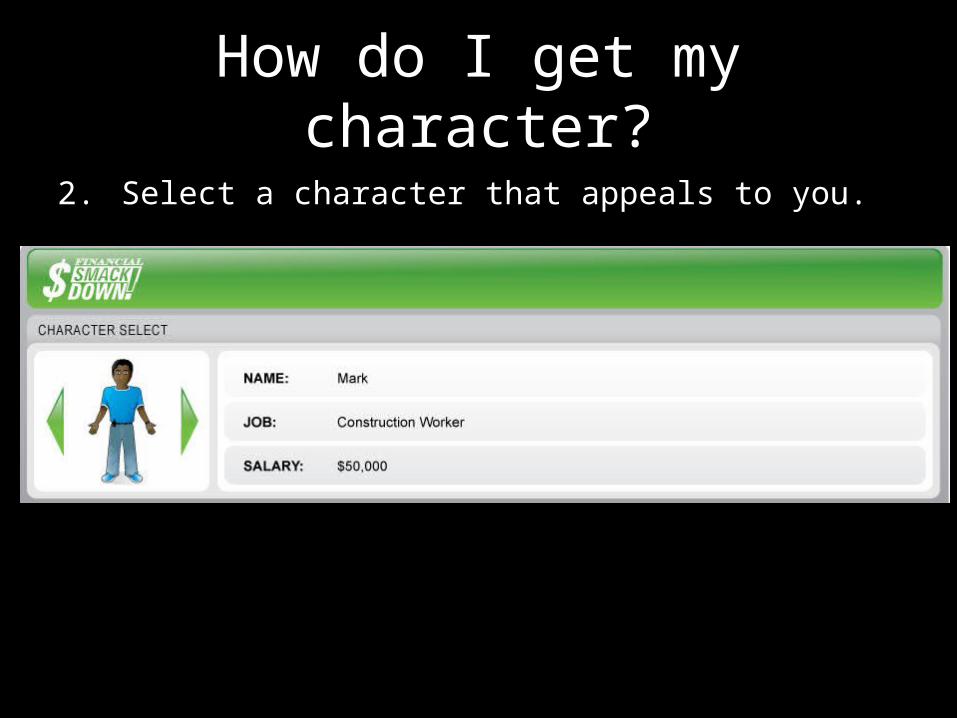

How do I get my character?

2. Select a character that appeals to you.

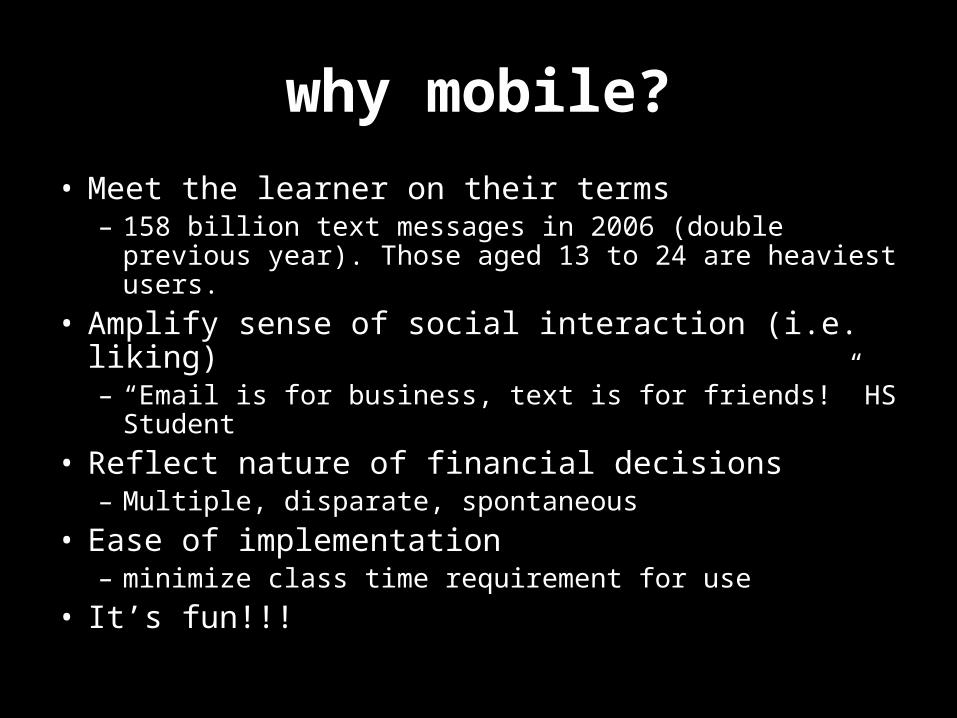

why mobile?

• Meet the learner on their terms– 158 billion text messages in 2006 (double previous

year). Those aged 13 to 24 are heaviest users.

• Amplify sense of social interaction (i.e. liking)– “Email is for business, text is for friends!” HS Student

• Reflect nature of financial decisions– Multiple, disparate, spontaneous

• Ease of implementation– minimize class time requirement for use

• It’s fun!!!

responsibility

• kinship• Identification – select character• Liking – social responses from character

• reciprocity• Exchange – framing of game as opportunity to learn

• reputation• Reciprocity, Dominance – high scores list

• ownership• Singular onus – 1:1 match between character & learner

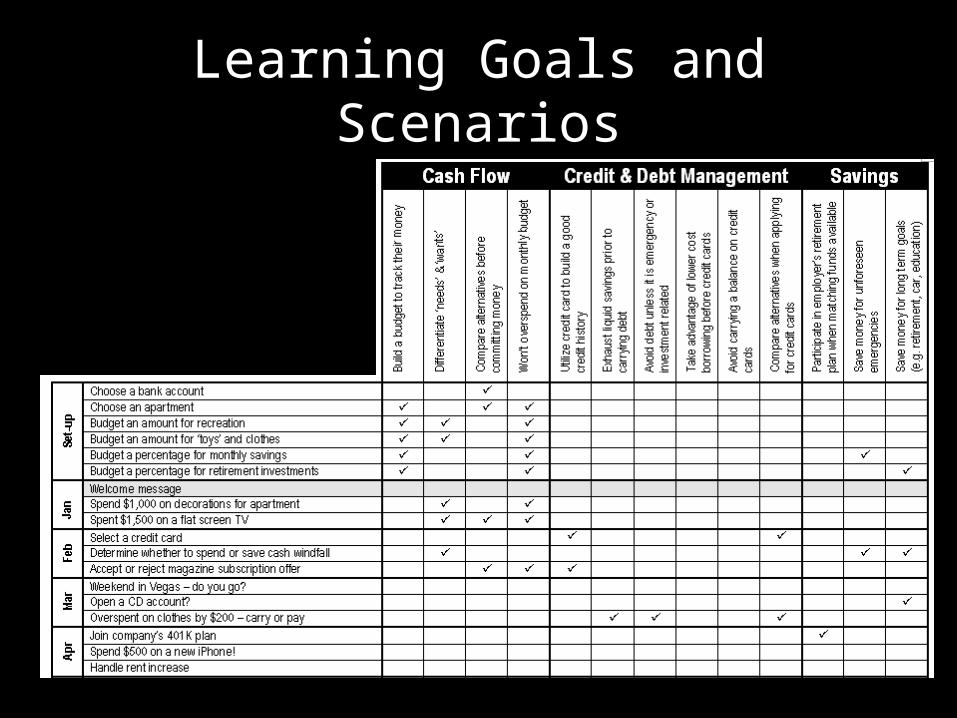

Learning Goals and Scenarios

• Cash Flow– Build a budget to track their money– Differentiate between ‘needs’ and ‘wants’– Compare alternatives before committing money– Won’t overspend on monthly budget

• Credit Management– Utilize credit card to build a good credit history– Exhaust liquid (low-interest) savings prior to carrying debt– Avoid debt unless it is an emergency or investment related– Take advantage of lower cost borrowing before carrying a balance on credit

cards– Compare alternatives when applying for credit cards

• Savings– Participate in employer’s retirement plan when matching funds available– Save money for unforeseen emergencies (3x monthly ‘needs’ expenses)– Save money for long term goals (e.g. further education, car, retirement)

Learning Goals and Scenarios

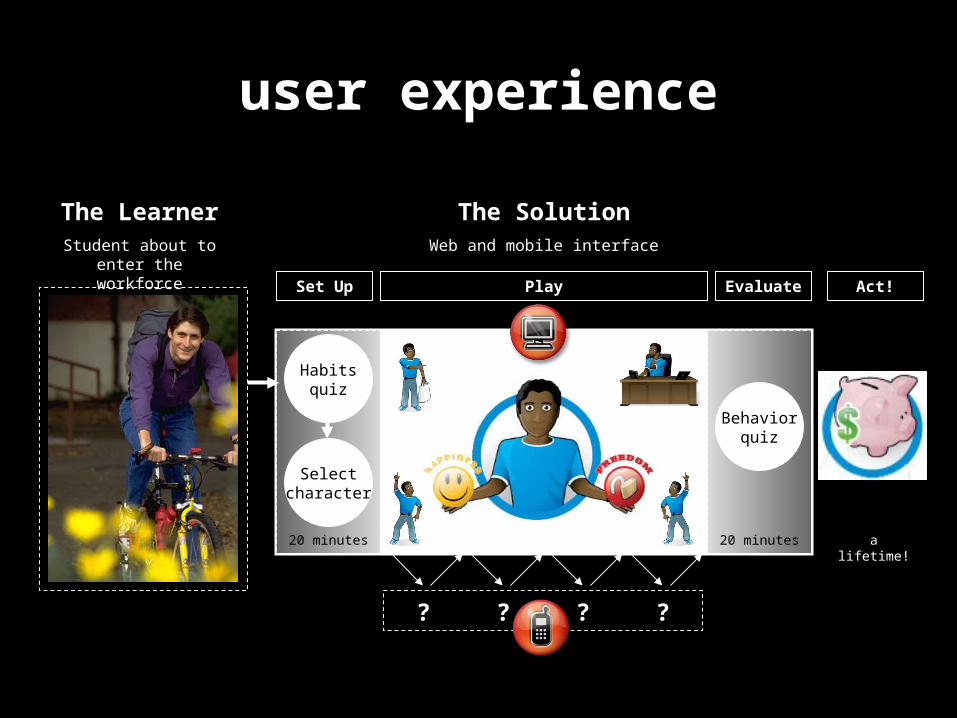

user experience

The LearnerStudent about to enter

the workforce

Habitsquiz

Selectcharacter

Behaviorquiz

Set Up Play Evaluate

The SolutionWeb and mobile interface

20 minutes 12 days 20 minutes

Act!

? ? ? ?

a lifetime!