Launching of Thailand's First Inflation Linked Bond

23

1 Project Funding For Infrastructure Development in Bangkok Launching of Thailand’s First Inflation Linked Bond 20 th – 25 th June 2011 Thailand first’s ILB London – UK, SG, HK

description

Launching of Thailand's First Inflation Linked Bond

Transcript of Launching of Thailand's First Inflation Linked Bond

1

Project Funding For Infrastructure Developmentin Bangkok

Launching ofThailand’s First Inflation Linked Bond

20th – 25th June 2011

Thailand first’s ILB

London – UK, SG, HK

2

The information contained in this presentation is for informational purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to purchase or subscribe for THB inflation linked bonds (the “ Bonds”) issued by the Ministry of Finance of the Kingdom of Thailand in the United States, Thailand or any other jurisdiction nor should it or any part of it form the basis of, or be relied upon in any connection with, any contract or commitment whatsoever.

This presentation is confidential and is intended only for the exclusive use of the recipients thereof and may not be reproduced (in whole or in part), retransmitted, summarized or distributed by them to any other persons.

None of The Hongkong and Shanghai Banking Corporation Limited, Bangkok Branch Krung Thai Bank Public Company Limited, The Siam Commercial Bank Public Company Limited and Kasikornbank Public Company Limited (together, the “the Joint Lead Managers”) or the Issuer nor any of their holding companies, subsidiaries, affiliates, associated undertakings or controlling persons, nor any of their respective directors, officers, partners, employees, agents, representatives, advisers or legal advisers makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained in this document or otherwise madeavailable nor as to the reasonableness of any assumption contained herein or therein, and any liability therefore (including in respect of direct, indirect or consequential loss or damage) is expressly disclaimed. Nothing contained herein or therein is, or shall be relied upon as, a promise or representation, whether as to the past or the future and no reliance, in whole or in part, should be placed on, the fairness, accuracy, completeness or correctness of the information contained herein. None of the Joint Lead Managers, the Issuer or their subsidiaries or affiliates has independently verified, approved or endorsed the material herein, or undertakes to update or revise any information subsequent to the date hereof, whether as a result of new information, future events or otherwise.

This presentation may contain forward-looking statements that may be identified by their use of words like “plans”, “expects”, “will”, “anticipates”, “believes”, “intends”, “depends”, “projects”, “estimates” or other words of similar meaning and that involve risks and uncertainties. Forward-looking statements are based on certain assumptions and expectations of future events. None of the Joint Lead Managers or the Issuer can guarantee that these assumptions and expectations are accurate or will be realized. Actual future performance, outcomes and results may differ materially from those expressed in forward-looking statements as a result of a number of risks, uncertainties and assumptions. You are cautioned not to place undue reliance on these forward looking statements. None of the Joint Lead Managers or the Issuer assumes any responsibility to publicly amend, modify or revise any forward looking statements, on the basis of any subsequent developments, information or events, or otherwise.

These materials may not be taken or transmitted or distributed, directly or indirectly, to a U.S. person (as defined in Regulation S under the U.S. Securities Act of 1933, as amended (the “Securities Act”)) or to any officer, employee or affiliate of a U.S. person located in the United States or any of its territories. It may be unlawful to distribute these materials in certain jurisdictions.

DisclaimerPublic Debt Management Office, Ministry of Finance - Thailand

3

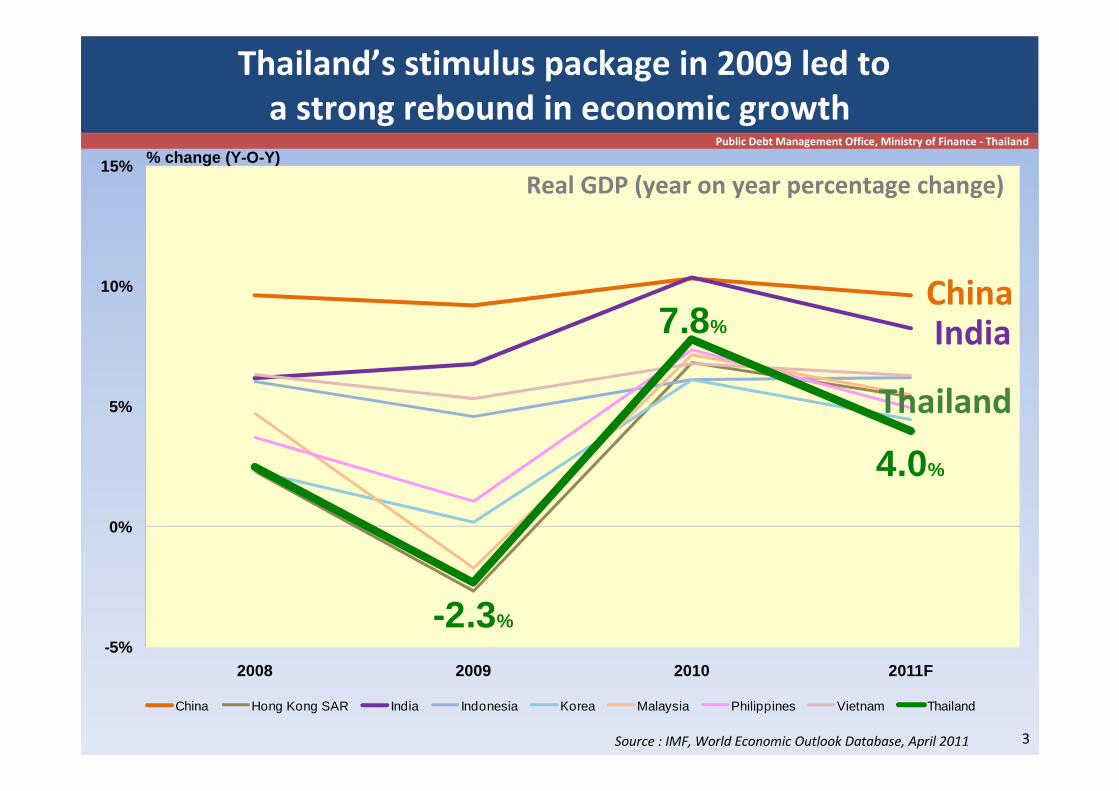

-2.3%

7.8%

4.0%

-5%

0%

5%

10%

15%

2008 2009 2010 2011F

China Hong Kong SAR India Indonesia Korea Malaysia Philippines Vietnam Thailand

Thailand’s stimulus package in 2009 led to

a strong rebound in economic growth

ChinaIndia

Real GDP (year on year percentage change)

Source : IMF, World Economic Outlook Database, April 2011

% change (Y-O-Y)Public Debt Management Office, Ministry of Finance - Thailand

Thailand

4

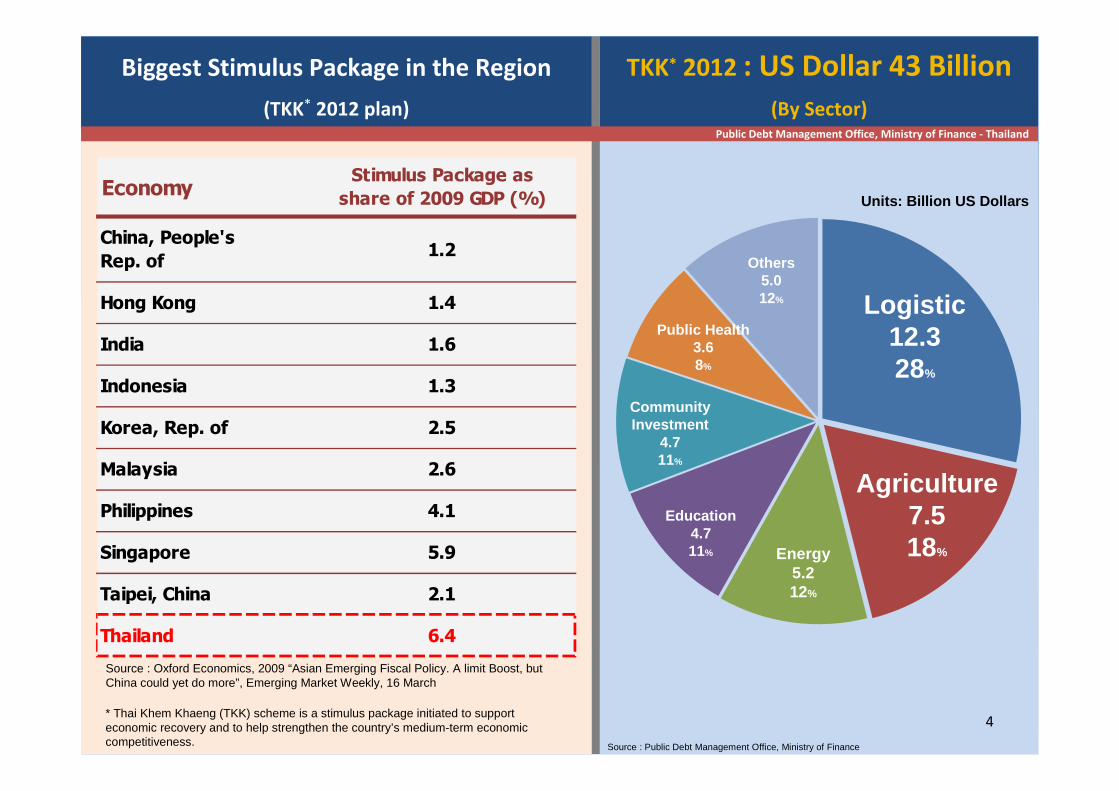

Biggest Stimulus Package in the Region

(TKK* 2012 plan)

TKK* 2012 : US Dollar 43 Billion

(By Sector)

Logistic12.328%

Agriculture7.518%Energy

5.212%

Education4.711%

CommunityInvestment

4.711%

Others5.012%

Public Health3.68%

Source : Public Debt Management Office, Ministry of Finance

EconomyStimulus Package as

share of 2009 GDP (%)

China, People's

Rep. of1.2

Hong Kong 1.4

India 1.6

Indonesia 1.3

Korea, Rep. of 2.5

Malaysia 2.6

Philippines 4.1

Singapore 5.9

Taipei, China 2.1

Thailand 6.4

Source : Oxford Economics, 2009 “Asian Emerging Fiscal Policy. A limit Boost, but China could yet do more”, Emerging Market Weekly, 16 March

Units: Billion US Dollars

Public Debt Management Office, Ministry of Finance - Thailand

* Thai Khem Khaeng (TKK) scheme is a stimulus package initiated to support economic recovery and to help strengthen the country’s medium-term economic competitiveness.

4

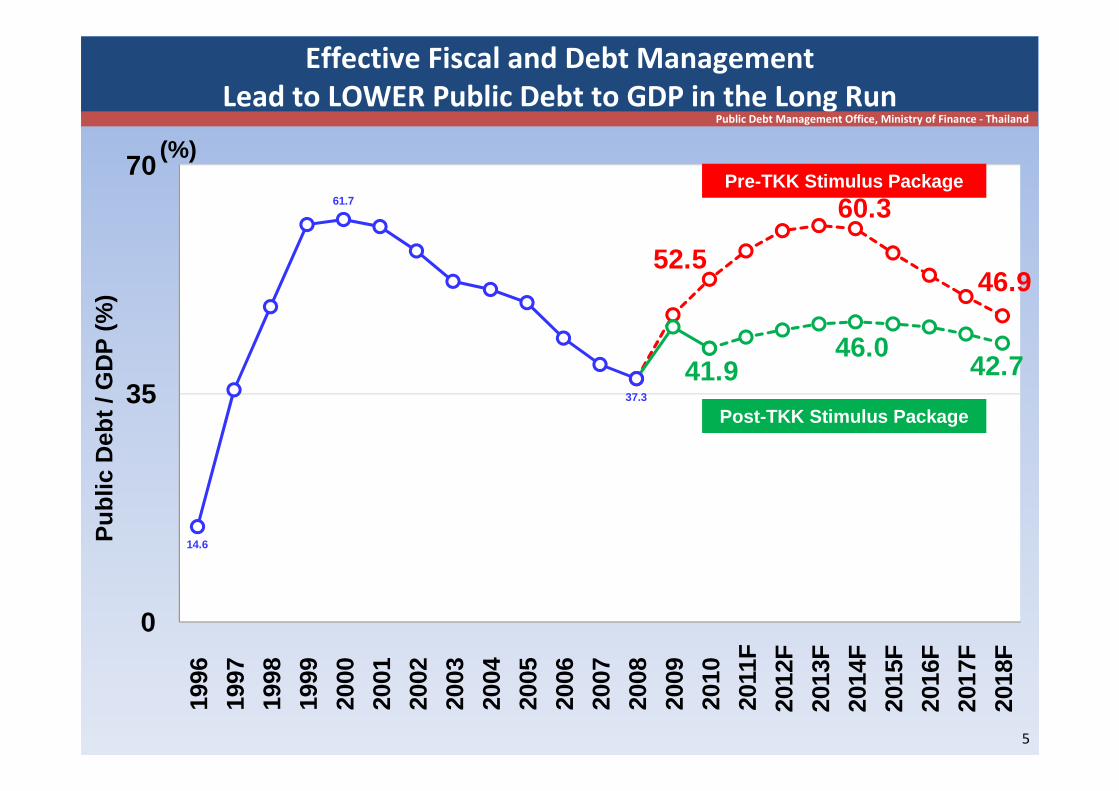

5

41.946.0

42.7

52.5

60.3

46.9

14.6

61.7

37.3

0

35

7019

96

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

F

2012

F

2013

F

2014

F

2015

F

2016

F

2017

F

2018

F

Effective Fiscal and Debt Management

Lead to LOWER Public Debt to GDP in the Long RunP

ublic

Deb

t / G

DP

(%

)

(%)Pre-TKK Stimulus Package

Post-TKK Stimulus Package

Public Debt Management Office, Ministry of Finance - Thailand

6

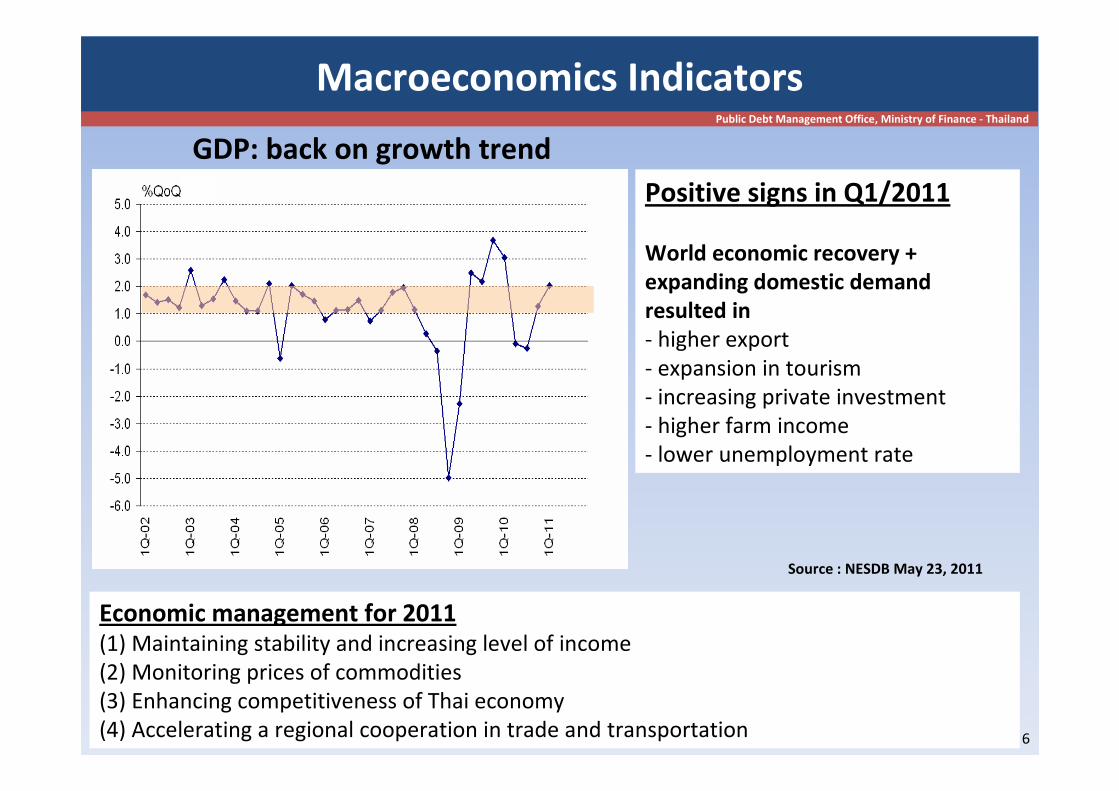

Macroeconomics Indicators Public Debt Management Office, Ministry of Finance - Thailand

Positive signs in Q1/2011

World economic recovery +

expanding domestic demand

resulted in

- higher export

- expansion in tourism

- increasing private investment

- higher farm income

- lower unemployment rate

Economic management for 2011(1) Maintaining stability and increasing level of income

(2) Monitoring prices of commodities

(3) Enhancing competitiveness of Thai economy

(4) Accelerating a regional cooperation in trade and transportation

Source : NESDB May 23, 2011

GDP: back on growth trend

7

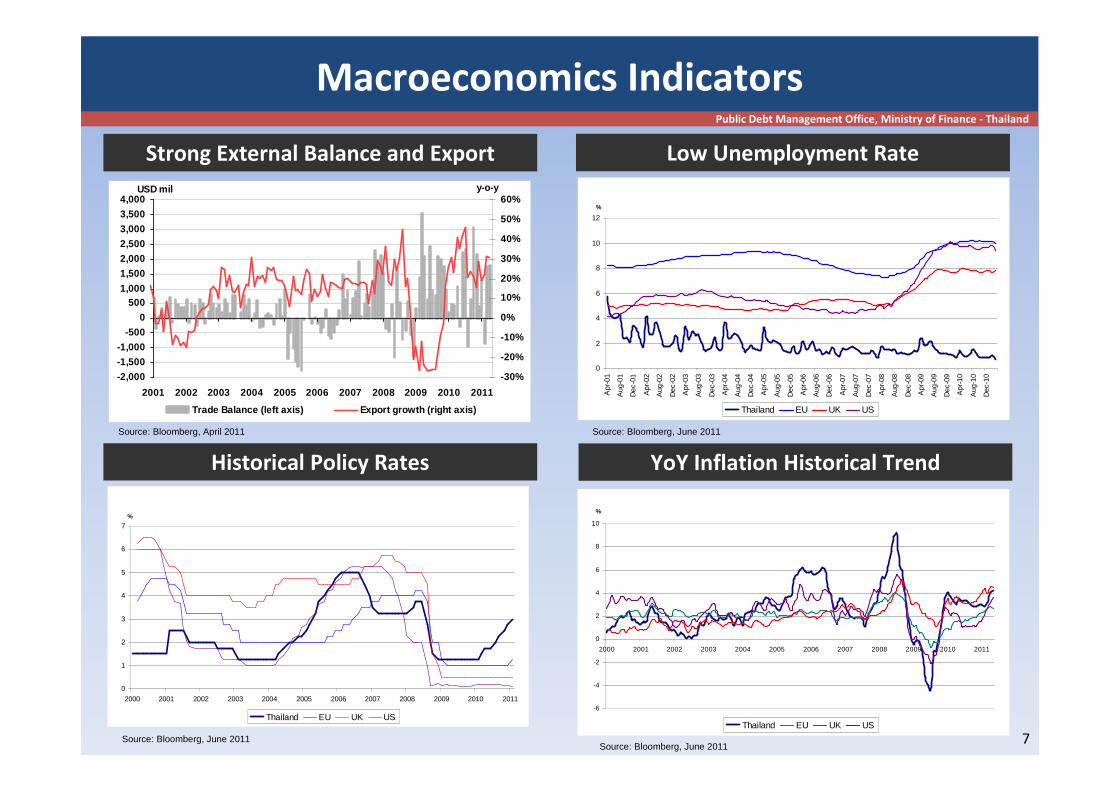

Macroeconomics Indicators

Low Unemployment Rate

Historical Policy Rates YoY Inflation Historical Trend

Public Debt Management Office, Ministry of Finance - Thailand

Source: Bloomberg, June 2011

0

2

4

6

8

10

12

Apr

-01

Aug

-01

Dec

-01

Apr

-02

Aug

-02

Dec

-02

Apr

-03

Aug

-03

Dec

-03

Apr

-04

Aug

-04

Dec

-04

Apr

-05

Aug

-05

Dec

-05

Apr

-06

Aug

-06

Dec

-06

Apr

-07

Aug

-07

Dec

-07

Apr

-08

Aug

-08

Dec

-08

Apr

-09

Aug

-09

Dec

-09

Apr

-10

Aug

-10

Dec

-10

%

Thailand EU UK US

0

1

2

3

4

5

6

7

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

%

Thailand EU UK US

Source: Bloomberg, June 2011Source: Bloomberg, June 2011

-6

-4

-2

0

2

4

6

8

10

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

%

Thailand EU UK US

Strong External Balance and Export

-2,000

-1,500

-1,000

-500

0

5001,000

1,500

2,000

2,500

3,000

3,500

4,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

USD mil

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Trade Balance (left axis) Export growth (right axis)

y-o-y

Source: Bloomberg, April 2011

8

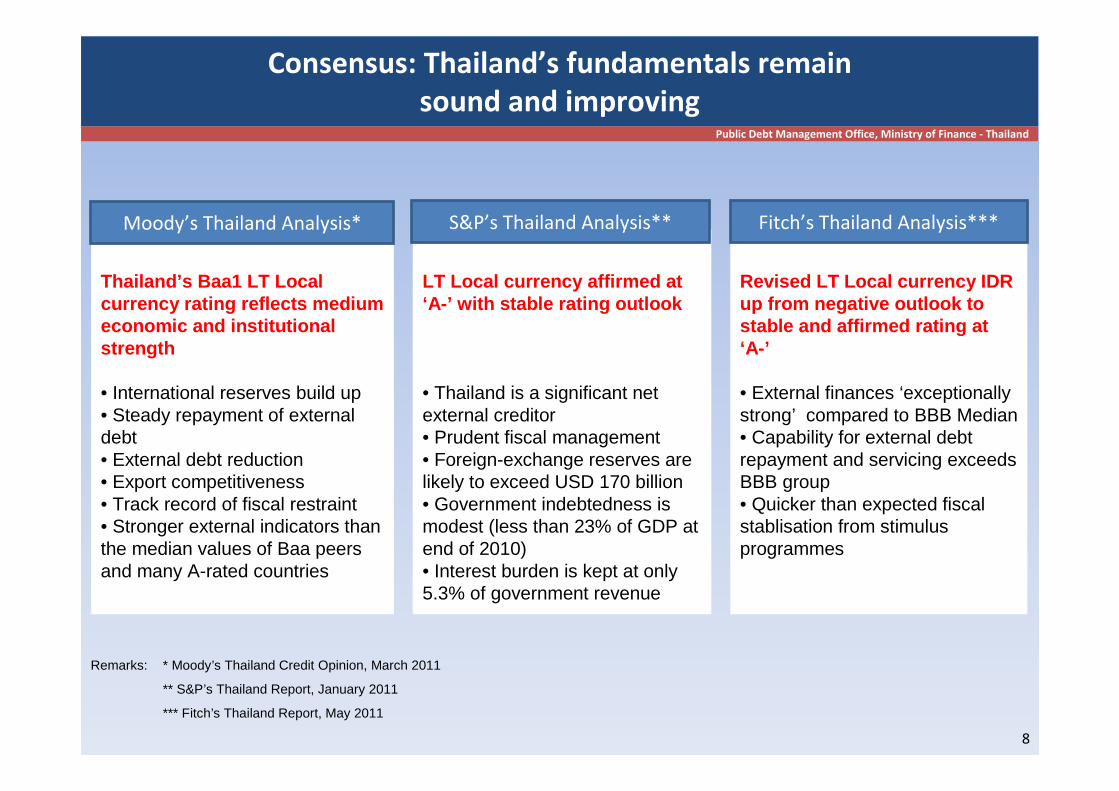

Consensus: Thailand’s fundamentals remain

sound and improving

Thailand’s Baa1 LT Local currency rating reflects medium economic and institutional strength

• International reserves build up• Steady repayment of external debt• External debt reduction• Export competitiveness• Track record of fiscal restraint• Stronger external indicators than the median values of Baa peers and many A-rated countries

Moody’s Thailand Analysis*

Remarks: * Moody’s Thailand Credit Opinion, March 2011

** S&P’s Thailand Report, January 2011

*** Fitch’s Thailand Report, May 2011

Public Debt Management Office, Ministry of Finance - Thailand

Revised LT Local currency IDR up from negative outlook to stable and affirmed rating at ‘A-’

• External finances ‘exceptionally strong’ compared to BBB Median• Capability for external debt repayment and servicing exceeds BBB group• Quicker than expected fiscal stablisation from stimulus programmes

Fitch’s Thailand Analysis***

LT Local currency affirmed at ‘A-’ with stable rating outlook

• Thailand is a significant net external creditor• Prudent fiscal management• Foreign-exchange reserves are likely to exceed USD 170 billion• Government indebtedness is modest (less than 23% of GDP at end of 2010)• Interest burden is kept at only 5.3% of government revenue

S&P’s Thailand Analysis**

9

Thai Bond Market

10

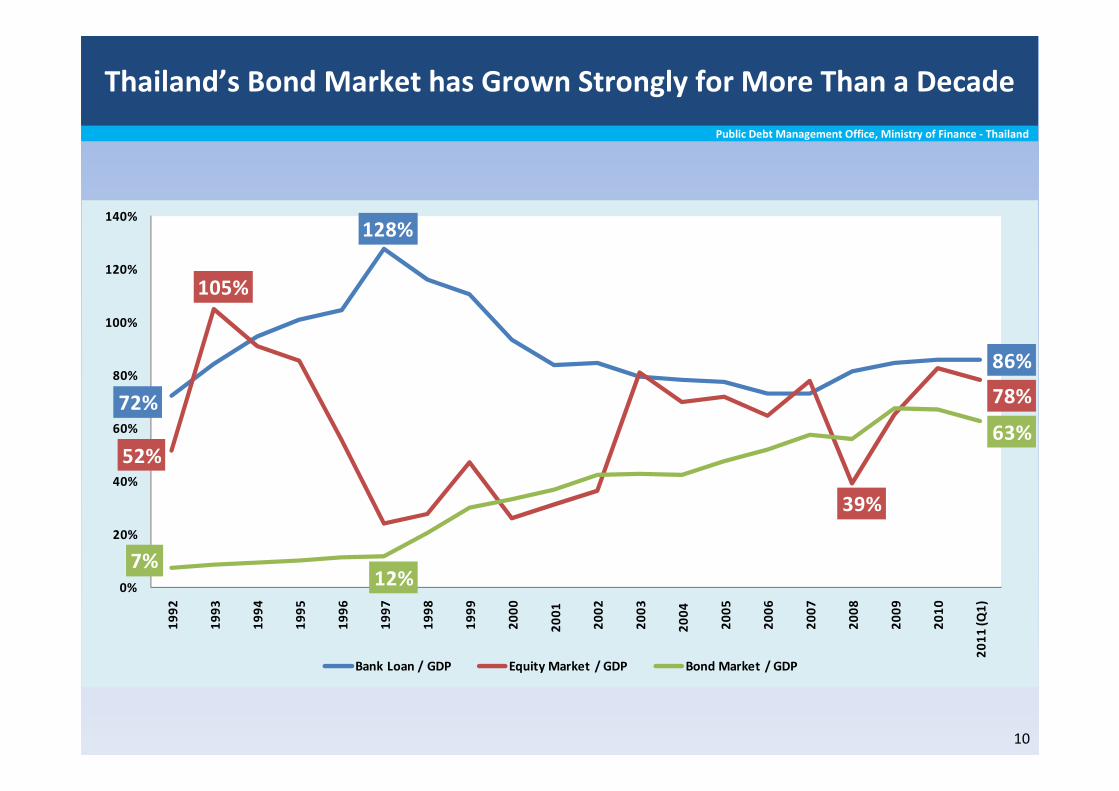

72%

128%

86%

52%

105%

39%

78%

7%12%

63%

0%

20%

40%

60%

80%

100%

120%

140%

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

(Q

1)

Bank Loan / GDP Equity Market / GDP Bond Market / GDP

Thailand’s Bond Market has Grown Strongly for More Than a Decade

Public Debt Management Office, Ministry of Finance - Thailand

11

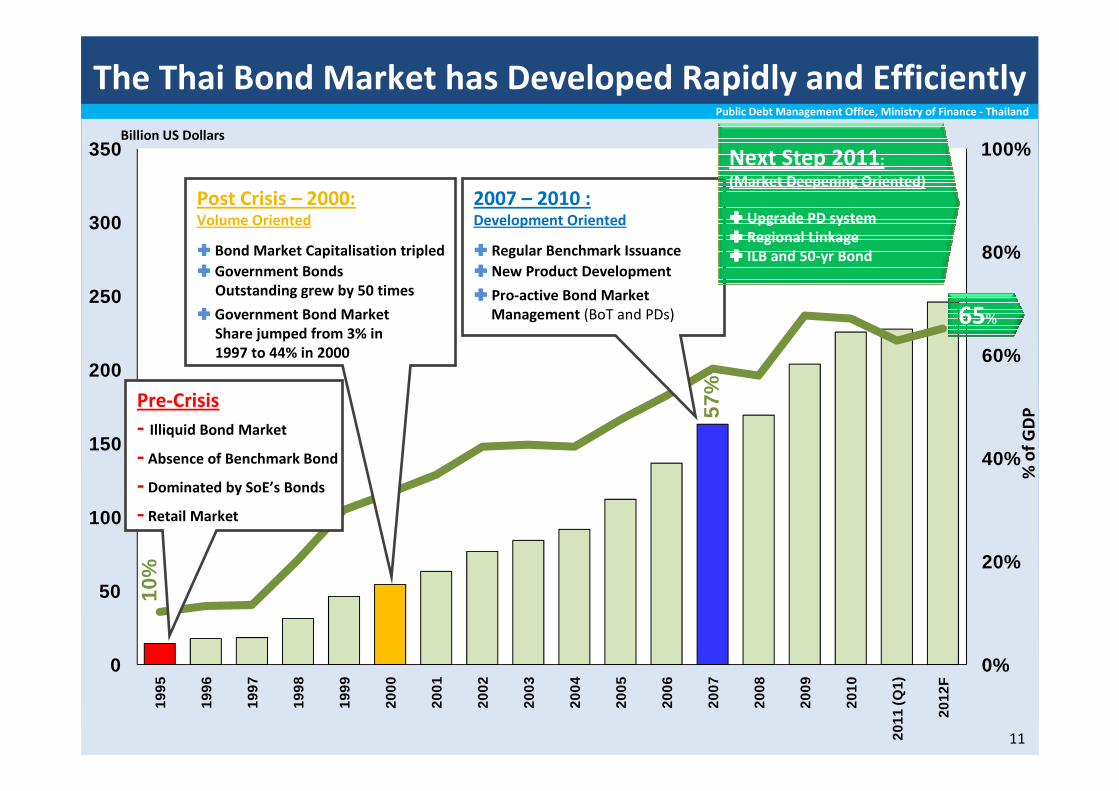

10%

57%

0%

20%

40%

60%

80%

100%

0

50

100

150

200

250

300

35019

95

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

(Q1)

2012

F

% o

f G

DP

Billion US Dollars

65%

Post Crisis – 2000: Volume Oriented

���� Bond Market Capitalisation tripled

���� Government Bonds

Outstanding grew by 50 times

���� Government Bond Market

Share jumped from 3% in

1997 to 44% in 2000

2007 – 2010 : Development Oriented

���� Regular Benchmark Issuance

���� New Product Development

���� Pro-active Bond Market

Management (BoT and PDs)

Pre-Crisis

- Illiquid Bond Market

- Absence of Benchmark Bond

- Dominated by SoE’s Bonds

- Retail Market

Next Step 2011:

(Market Deepening Oriented)

���� Upgrade PD system

���� Regional Linkage

���� ILB and 50-yr Bond

Public Debt Management Office, Ministry of Finance - Thailand

The Thai Bond Market has Developed Rapidly and Efficiently

11

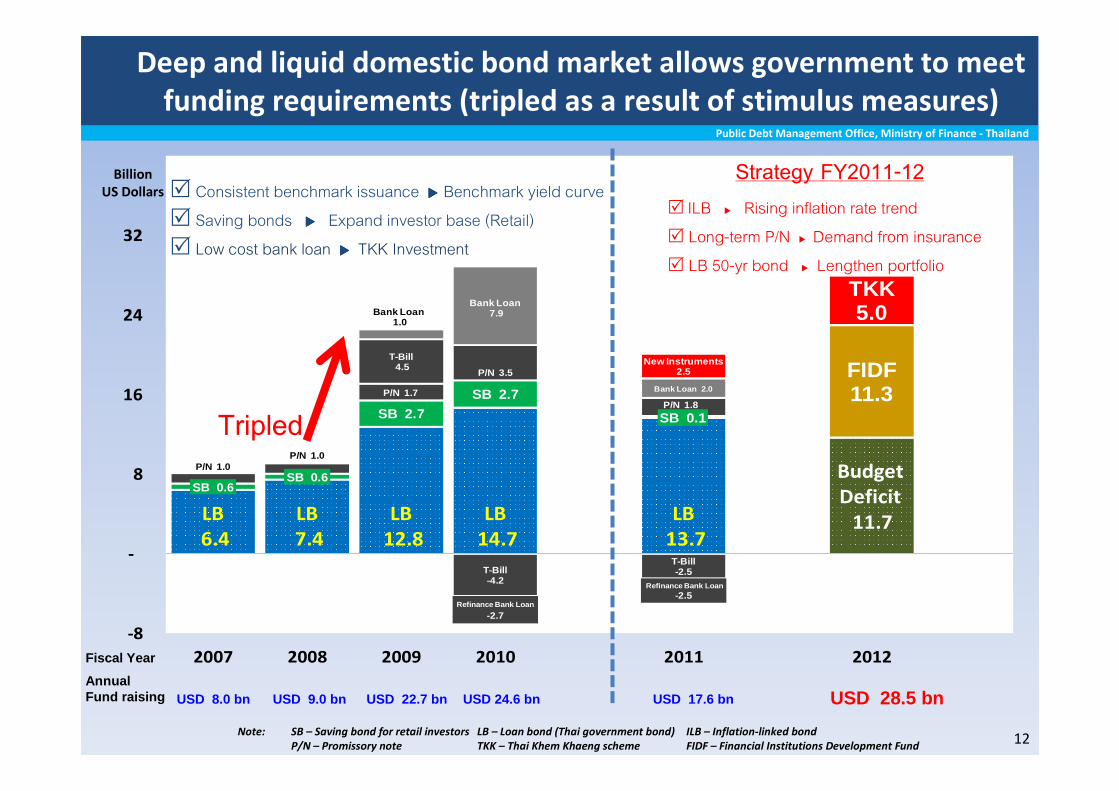

LB

6.4

LB

7.4

LB

12.8

LB

14.7

LB

13.7

Budget

Deficit

11.7

SB 0.6 SB 0.6

SB 2.7 SB 2.7

SB 0.1

FIDF11.3

P/N 1.0 P/N 1.0

P/N 1.7

P/N 3.5

P/N 1.8

T-Bill4.5

T-Bill-4.2

T-Bill-2.5

Bank Loan1.0

Bank Loan7.9

Bank Loan 2.0

New Instruments2.5

TKK5.0

-2.7

-2.5

-8

-

8

16

24

32

2007 2008 2009 2010 2011 2012

Refinance Bank Loan

Refinance Bank Loan

12

Deep and liquid domestic bond market allows government to meet

funding requirements (tripled as a result of stimulus measures)

Tripled

Billion

US Dollars

USD 28.5 bnUSD 17.6 bnUSD 8.0 bnAnnual Fund raising USD 9.0 bn USD 22.7 bn USD 24.6 bn

Fiscal Year

Public Debt Management Office, Ministry of Finance - Thailand

� Consistent benchmark issuance ���� Benchmark yield curve

� Saving bonds ���� Expand investor base (Retail)

� Low cost bank loan ���� TKK Investment

� ILB � Rising inflation rate trend

� Long-term P/N � Demand from insurance

� LB 50-yr bond � Lengthen portfolio

Strategy FY2011-12

Note: SB – Saving bond for retail investors LB – Loan bond (Thai government bond) ILB – Inflation-linked bond

P/N – Promissory note TKK – Thai Khem Khaeng scheme FIDF – Financial Institutions Development Fund

13

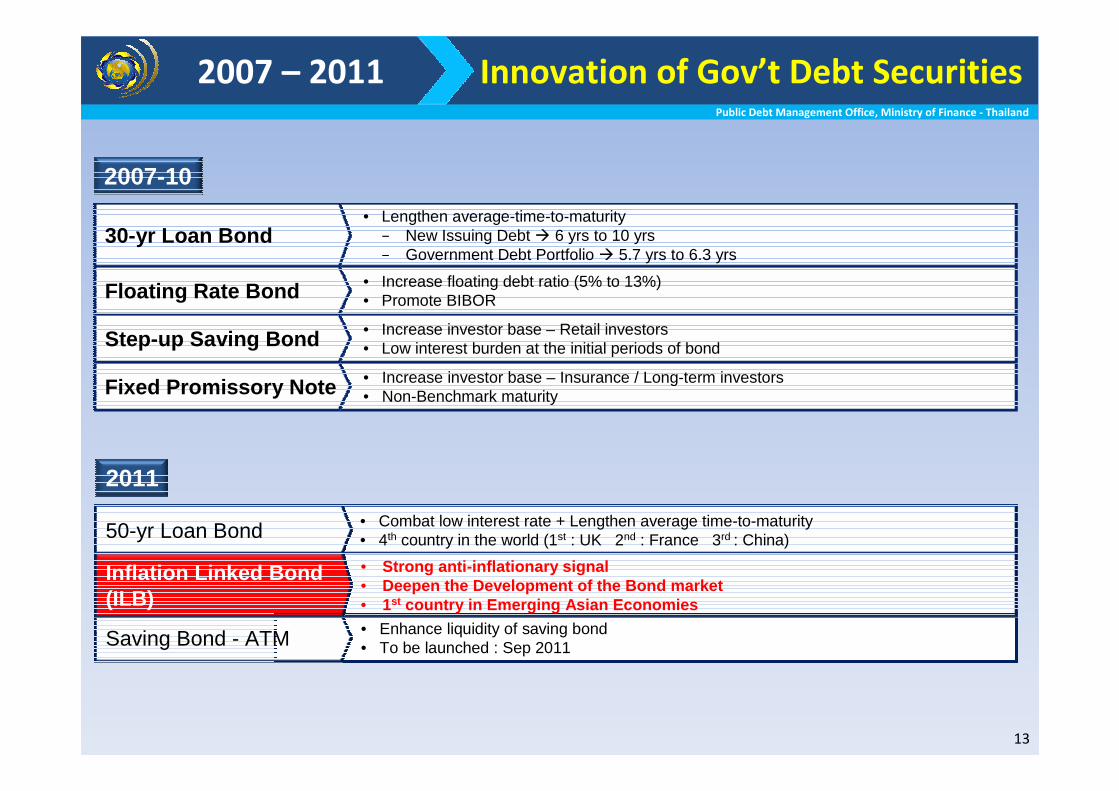

2007 – 2011 Innovation of Gov’t Debt Securities

• Combat low interest rate + Lengthen average time-to-maturity• 4th country in the world (1st : UK 2nd : France 3rd : China)50-yr Loan Bond

• Enhance liquidity of saving bond• To be launched : Sep 2011Saving Bond - ATM

2007-10

2011

• Strong anti-inflationary signal• Deepen the Development of the Bond market• 1st country in Emerging Asian Economies

Inflation Linked Bond (ILB)

• Increase investor base – Insurance / Long-term investors• Non-Benchmark maturityFixed Promissory Note

• Increase investor base – Retail investors• Low interest burden at the initial periods of bondStep-up Saving Bond

• Increase floating debt ratio (5% to 13%)• Promote BIBORFloating Rate Bond

• Lengthen average-time-to-maturity − New Issuing Debt � 6 yrs to 10 yrs− Government Debt Portfolio � 5.7 yrs to 6.3 yrs

30-yr Loan Bond

Public Debt Management Office, Ministry of Finance - Thailand

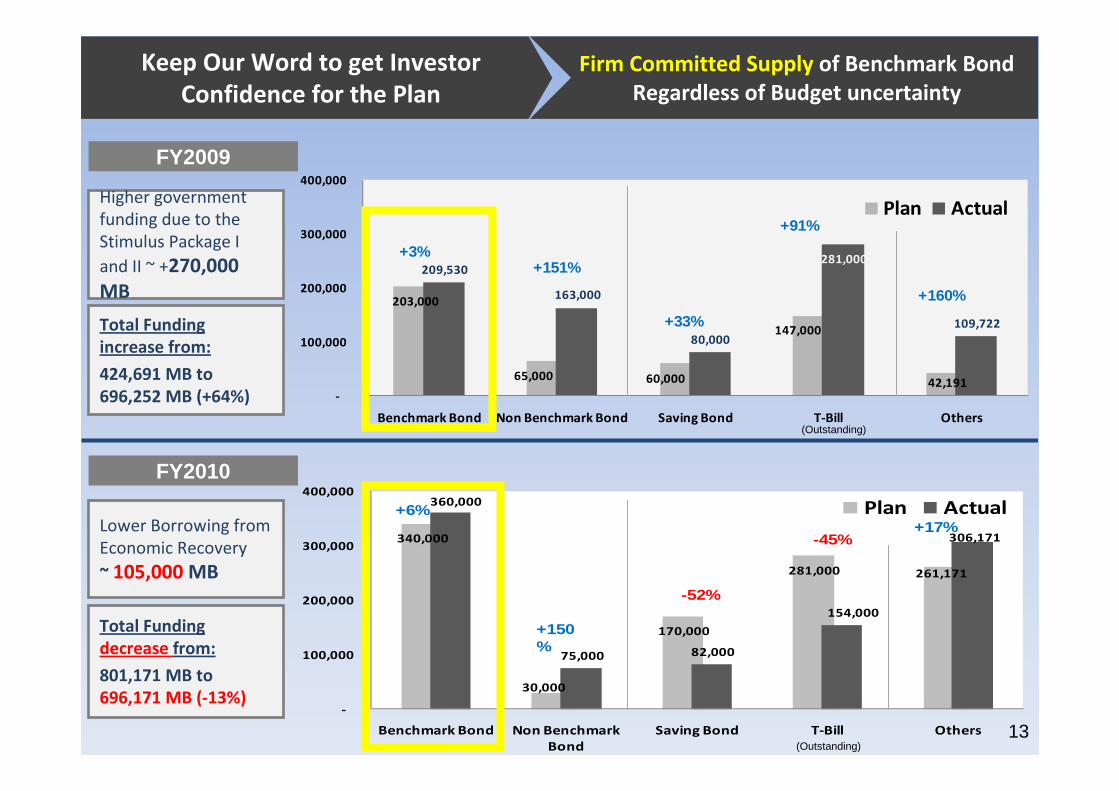

340,000

30,000

170,000

281,000 261,171

360,000

75,000 82,000

154,000

306,171

-

100,000

200,000

300,000

400,000

Benchmark Bond Non Benchmark

Bond

Saving Bond T-Bill Others

Plan Actual+6%

+150%

-52%

-45%+17%

203,000

65,000 60,000

147,000

42,191

209,530

163,000

80,000

281,000

109,722

-

100,000

200,000

300,000

400,000

Benchmark Bond Non Benchmark Bond Saving Bond T-Bill Others

Plan Actual

+3%+151%

+33%

+91%

+160%

Firm Committed Supply of Benchmark Bond

Regardless of Budget uncertainty

Keep Our Word to get Investor

Confidence for the Plan

Higher government

funding due to the

Stimulus Package I

and II ~ +270,000

MB

FY2009

Lower Borrowing from

Economic Recovery

~ 105,000 MB

FY2010

Total Funding

increase from:

424,691 MB to

696,252 MB (+64%)

Total Funding

decrease from:

801,171 MB to

696,171 MB (-13%)

(Outstanding)

(Outstanding)13

15

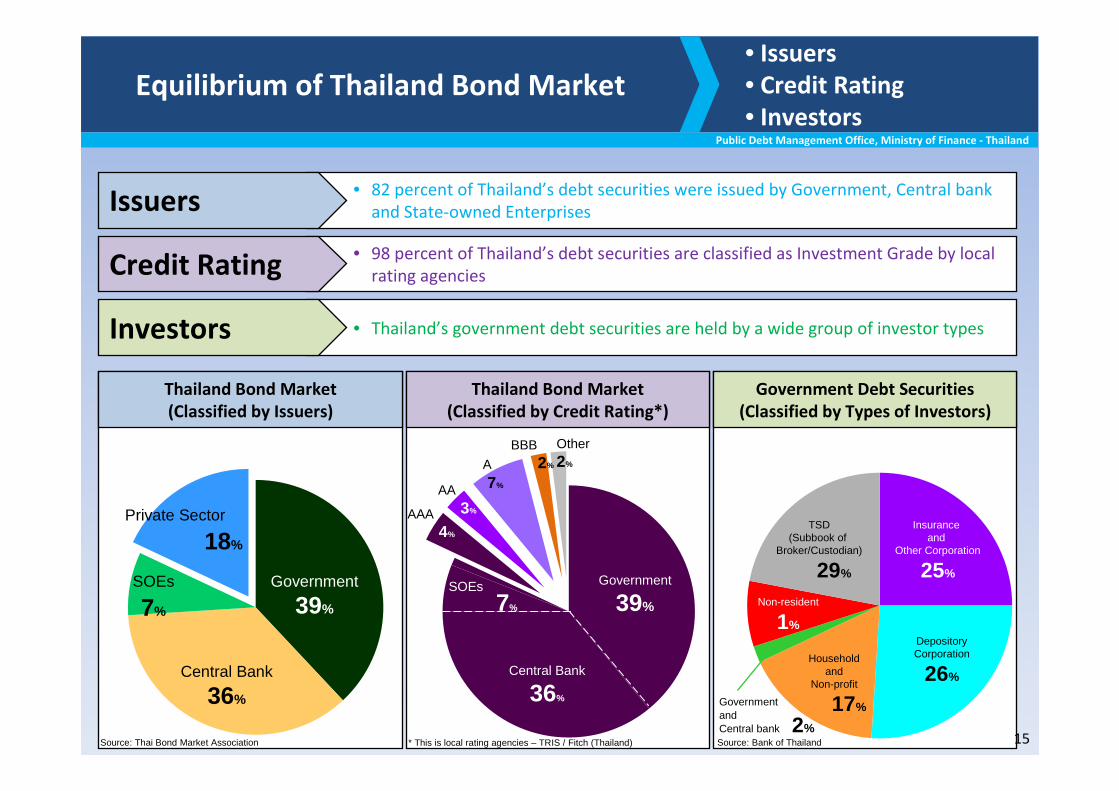

Equilibrium of Thailand Bond Market• Issuers

• Credit Rating

• Investors

• 82 percent of Thailand’s debt securities were issued by Government, Central bank

and State-owned EnterprisesIssuers

• 98 percent of Thailand’s debt securities are classified as Investment Grade by local

rating agenciesCredit Rating

• Thailand’s government debt securities are held by a wide group of investor typesInvestors

Thailand Bond Market

(Classified by Issuers)

Thailand Bond Market

(Classified by Credit Rating*)

Government Debt Securities

(Classified by Types of Investors)

Government

39%

Central Bank

36%

SOEs

7%

Private Sector

18%

Other2%

BBB2%A

7%AA3% AAA

4%

Government

39%

Central Bank

36%

SOEs

7%

Insurance and

Other Corporation

25%

DepositoryCorporation

26%

Householdand

Non-profit

17%

TSD(Subbook of

Broker/Custodian)

29%

Government and Central bank 2%

Non-resident

1%

Public Debt Management Office, Ministry of Finance - Thailand

Source: Thai Bond Market Association Source: Bank of Thailand* This is local rating agencies – TRIS / Fitch (Thailand)

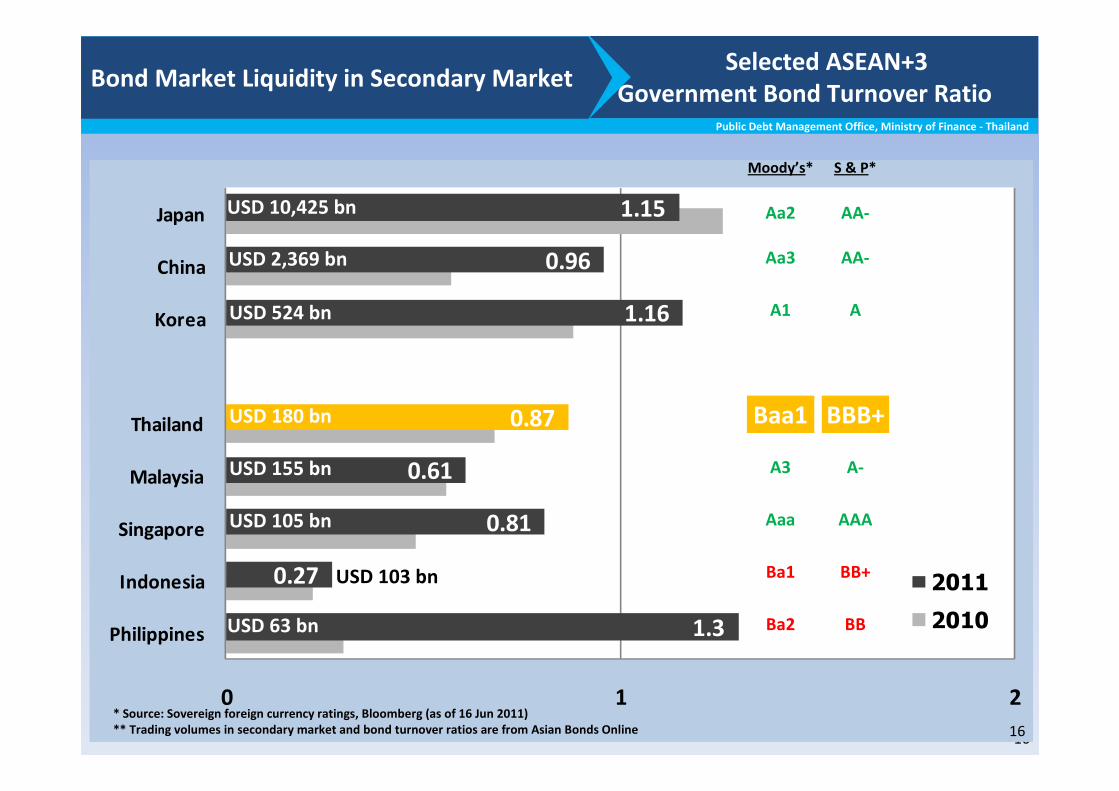

16

1.3

0.27

0.81

0.61

0.87

1.16

0.96

1.15

0 1 2

Philippines

Indonesia

Singapore

Malaysia

Thailand

Korea

China

Japan

2011

2010

49.6

Selected ASEAN+3

Government Bond Turnover RatioBond Market Liquidity in Secondary Market

USD 63 bn

USD 524 bn

USD 10,425 bn

USD 2,369 bn

USD 180 bn

USD 105 bn

USD 155 bn

USD 103 bn

Aa2

Aa3

A1

Baa1

A3

Aaa

Ba1

Ba2

AA-

AA-

A

BBB+

A-

AAA

BB+

BB

Moody’s* S & P*

* Source: Sovereign foreign currency ratings, Bloomberg (as of 16 Jun 2011)

** Trading volumes in secondary market and bond turnover ratios are from Asian Bonds Online

Public Debt Management Office, Ministry of Finance - Thailand

16

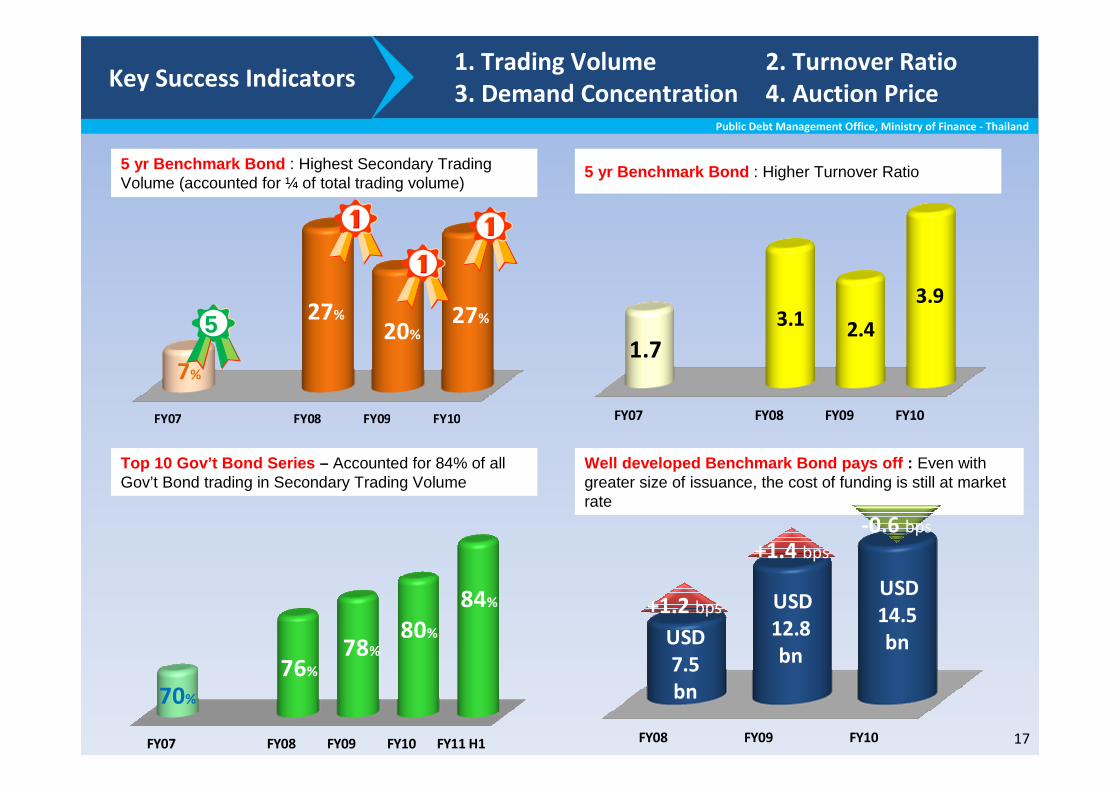

17

Public Debt Management Office, Ministry of Finance - Thailand

FY07 FY08 FY09 FY10

7%

27%

20%27%

FY07 FY08 FY09 FY10

1.7

3.12.4

3.9

FY07 FY08 FY09 FY10 FY11 H1

70%

76%

78%

80%

84%

FY08 FY09 FY10

USD

7.5

bn

USD

12.8

bn

USD

14.5

bn

1. Trading Volume 2. Turnover Ratio

3. Demand Concentration 4. Auction PriceKey Success Indicators

5 yr Benchmark Bond : Highest Secondary Trading Volume (accounted for ¼ of total trading volume)

5 yr Benchmark Bond : Higher Turnover Ratio

Top 10 Gov’t Bond Series – Accounted for 84% of all Gov’t Bond trading in Secondary Trading Volume

Well developed Benchmark Bond pays off : Even with greater size of issuance, the cost of funding is still at marketrate

+1.2 bps

+1.4 bps

-0.6 bps

5

18

ILB Features

19

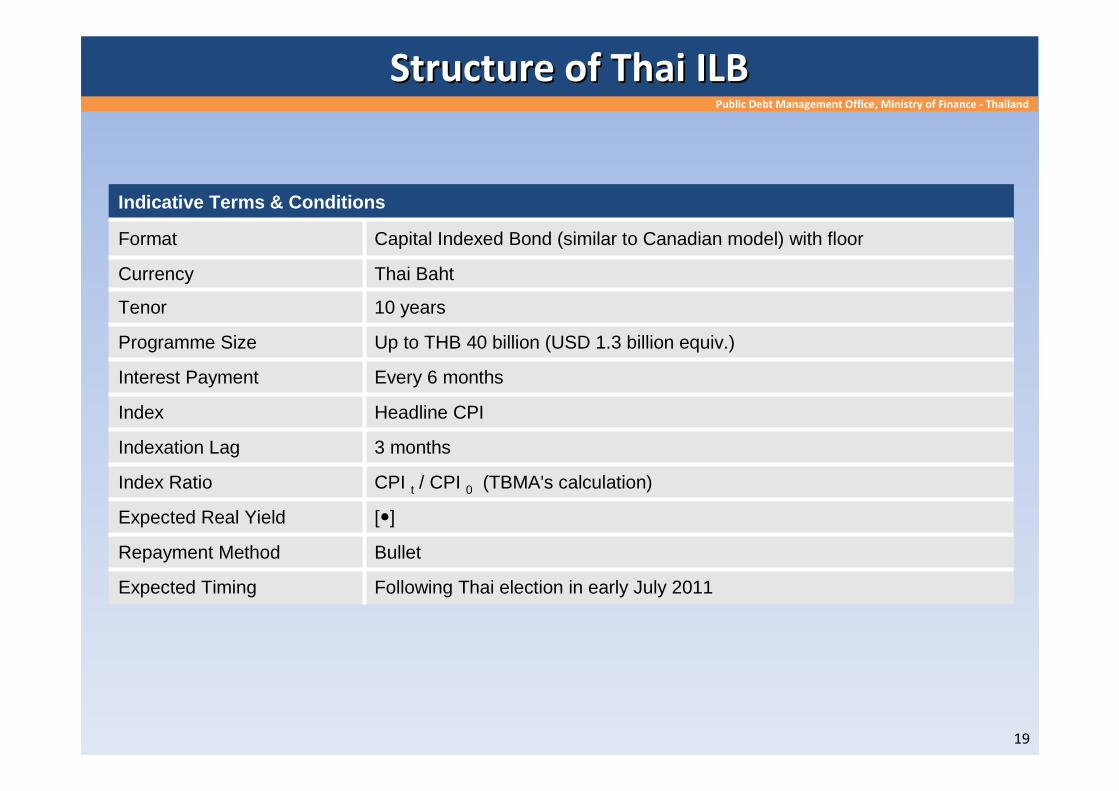

Structure of Thai ILBStructure of Thai ILB

Indicative Terms & Conditions

Format Capital Indexed Bond (similar to Canadian model) with floor

Currency Thai Baht

Tenor 10 years

Programme Size Up to THB 40 billion (USD 1.3 billion equiv.)

Interest Payment Every 6 months

Index Headline CPI

Indexation Lag 3 months

Index Ratio CPI t / CPI 0 (TBMA's calculation)

Expected Real Yield [�]

Repayment Method Bullet

Expected Timing Following Thai election in early July 2011

Public Debt Management Office, Ministry of Finance - Thailand

20

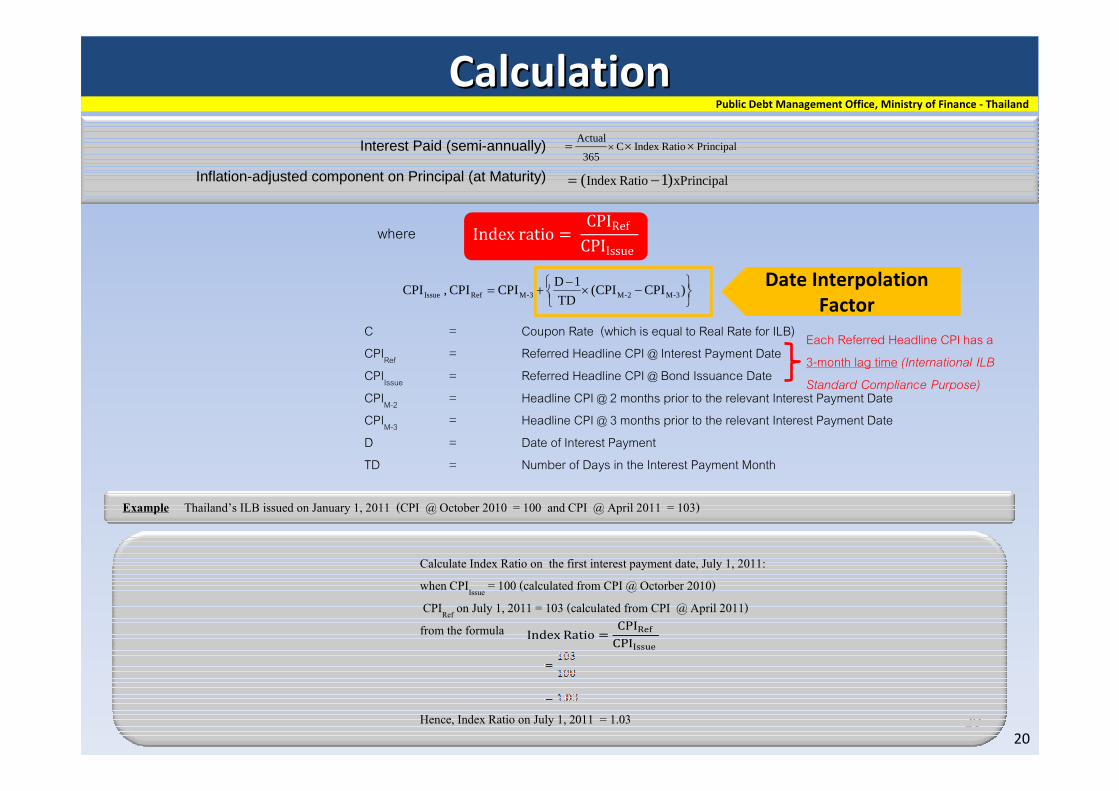

CalculationCalculation

PrincipalRatioIndex C365

Actual ××= ×

xPrincipalRatioIndex )1( −=

Interest Paid (semi-annually)

Inflation-adjusted component on Principal (at Maturity)

where

−×−

+= )CPICPI(TD

1DCPICPI , CPI 3-M2-M3-MRefIssue

C = Coupon Rate (which is equal to Real Rate for ILB)

CPIRef

= Referred Headline CPI @ Interest Payment Date

CPIIssue

= Referred Headline CPI @ Bond Issuance Date

CPIM-2

= Headline CPI @ 2 months prior to the relevant Interest Payment Date

CPIM-3

= Headline CPI @ 3 months prior to the relevant Interest Payment Date

D = Date of Interest Payment

TD = Number of Days in the Interest Payment Month

Calculate Index Ratio on the first interest payment date, July 1, 2011:

when CPIIssue

= 100 (calculated from CPI @ Octorber 2010)

CPIRef

on July 1, 2011 = 103 (calculated from CPI @ April 2011)

from the formula

Hence, Index Ratio on July 1, 2011 = 1.03

Index Ratio =CPIRef

CPIIssue

Index ratio = CPIRef

CPIIssue

Example Thailand*s ILB issued on January 1, 2011 (CPI @ October 2010 = 100 and CPI @ April 2011 = 103)

Date Interpolation

Factor

Each Referred Headline CPI has a

3-month lag time (International ILB

Standard Compliance Purpose)

Public Debt Management Office, Ministry of Finance - Thailand

20

21

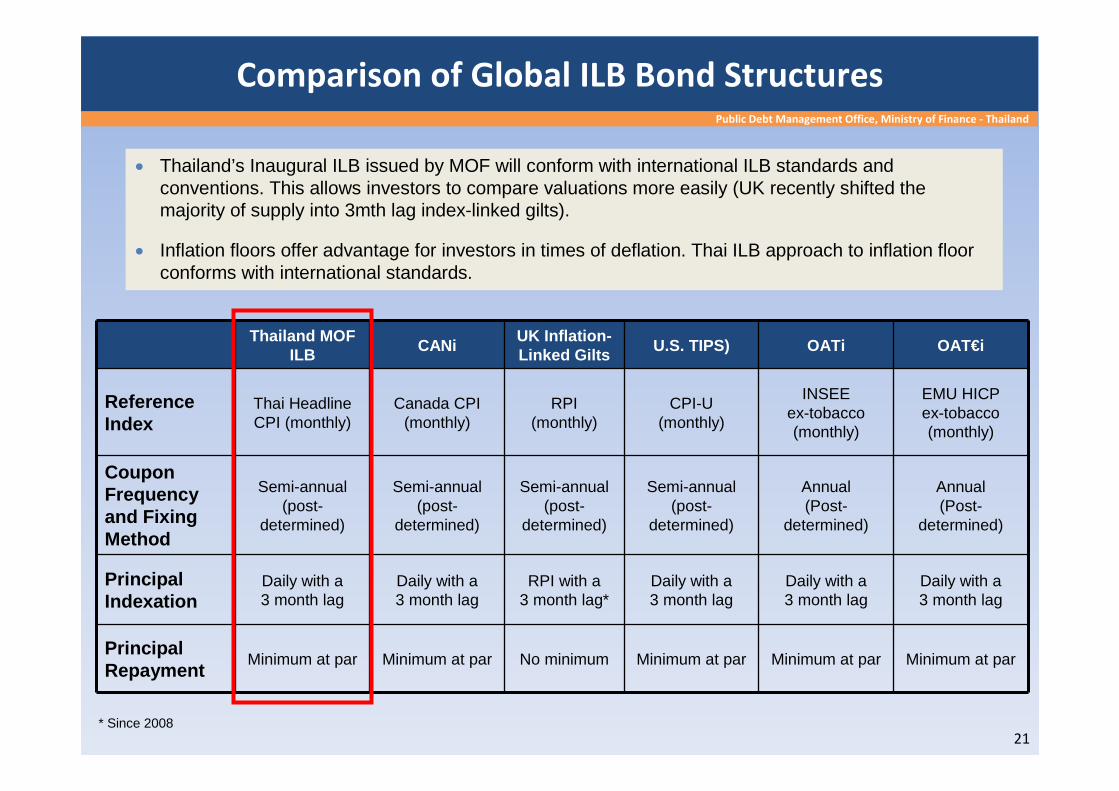

• Thailand’s Inaugural ILB issued by MOF will conform with international ILB standards and conventions. This allows investors to compare valuations more easily (UK recently shifted the majority of supply into 3mth lag index-linked gilts).

• Inflation floors offer advantage for investors in times of deflation. Thai ILB approach to inflation floor conforms with international standards.

Comparison of Global ILB Bond Structures

Thailand MOF ILB CANi

UK Inflation-Linked Gilts U.S. TIPS) OATi OAT€i

Reference Index

Thai Headline CPI (monthly)

Canada CPI (monthly)

RPI(monthly)

CPI-U(monthly)

INSEE ex-tobacco (monthly)

EMU HICP ex-tobacco (monthly)

Coupon Frequency and Fixing Method

Semi-annual (post-

determined)

Semi-annual (post-

determined)

Semi-annual (post-

determined)

Semi-annual (post-

determined)

Annual (Post-

determined)

Annual (Post-

determined)

Principal Indexation

Daily with a 3 month lag

Daily with a 3 month lag

RPI with a 3 month lag*

Daily with a 3 month lag

Daily with a 3 month lag

Daily with a 3 month lag

Principal Repayment

Minimum at par Minimum at par No minimum Minimum at par Minimum at par Minimum at par

* Since 2008

Public Debt Management Office, Ministry of Finance - Thailand

22

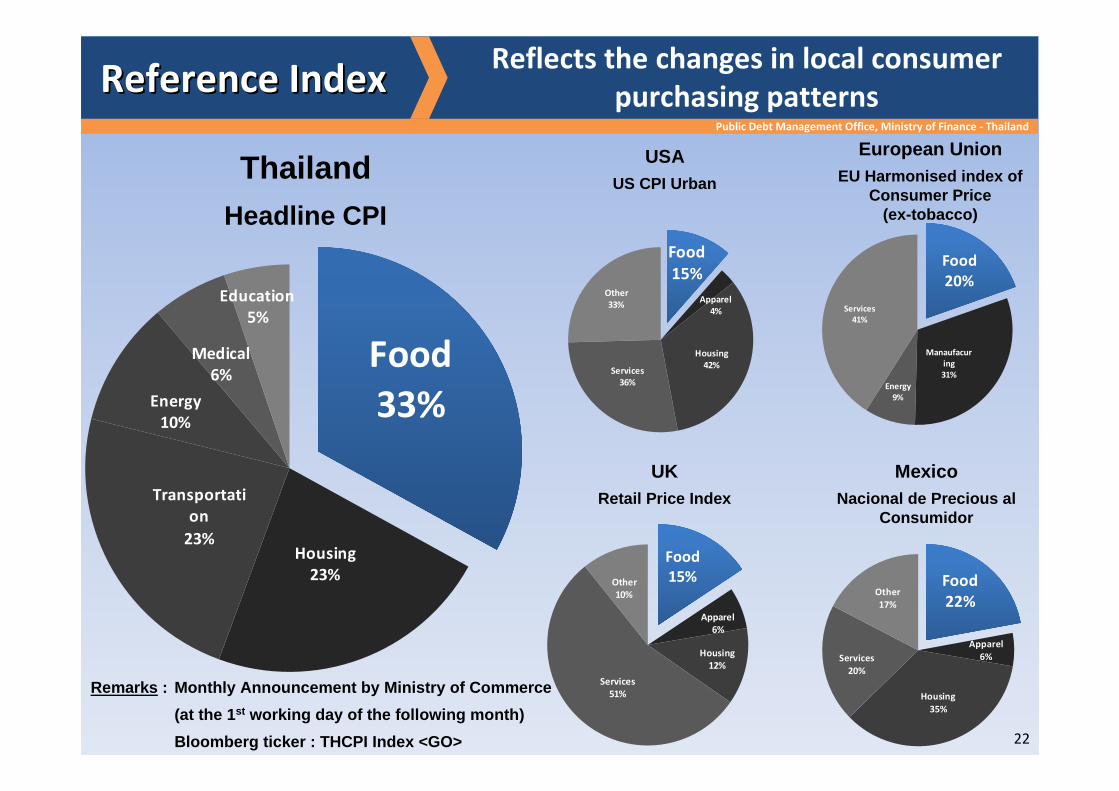

Reference IndexReference Index

Food

33%

Housing

23%

Transportati

on

23%

Energy

10%

Medical

6%

Education

5%

Food

15%

Apparel

4%

Housing

42%Services

36%

Other

33%

Food

20%

Manaufacur

ing

31%

Energy

9%

Services

41%

Food

15%

Apparel

6%

Housing

12%

Services

51%

Other

10%

Food

22%

Apparel

6%

Housing

35%

Services

20%

Other

17%

ThailandHeadline CPI

USAUS CPI Urban

European UnionEU Harmonised index of

Consumer Price(ex-tobacco)

UKRetail Price Index

MexicoNacional de Precious al

Consumidor

Reflects the changes in local consumer

purchasing patterns

Remarks : Monthly Announcement by Ministry of Commerce

(at the 1st working day of the following month)

Bloomberg ticker : THCPI Index <GO>

Public Debt Management Office, Ministry of Finance - Thailand

23

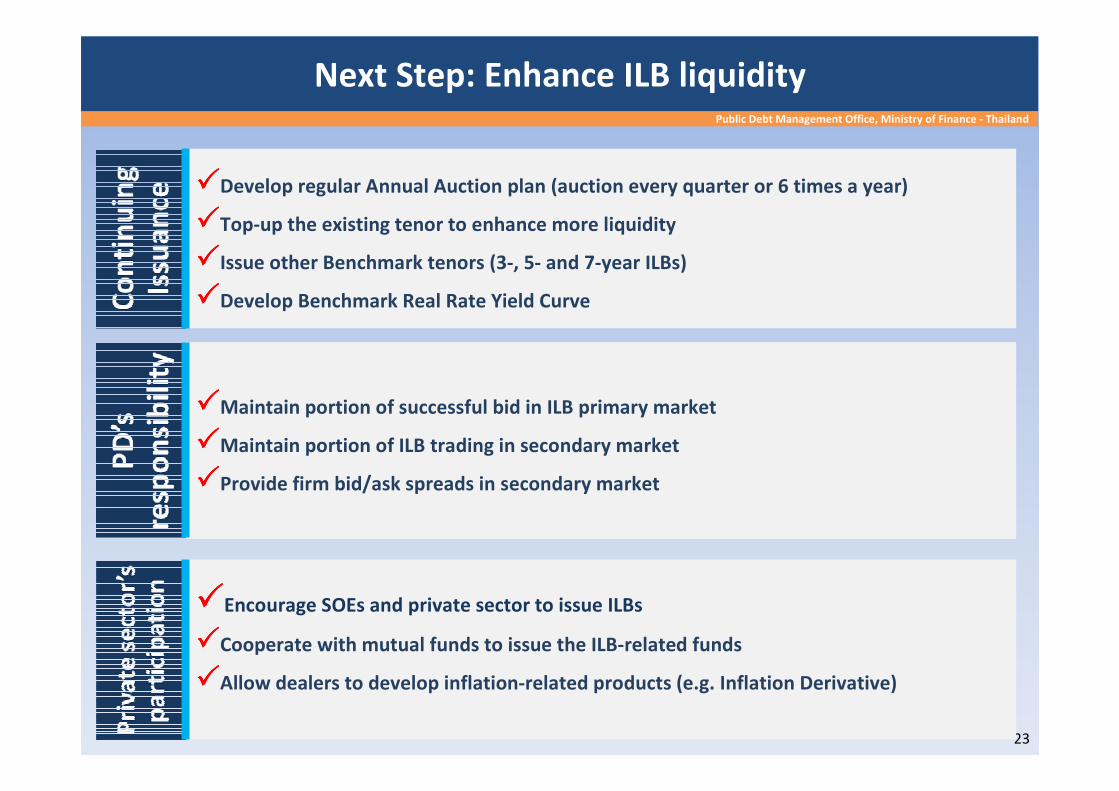

Next Step: Enhance ILB liquidity

����Develop regular Annual Auction plan (auction every quarter or 6 times a year)

����Top-up the existing tenor to enhance more liquidity

����Issue other Benchmark tenors (3-, 5- and 7-year ILBs)

����Develop Benchmark Real Rate Yield Curve

����Maintain portion of successful bid in ILB primary market

����Maintain portion of ILB trading in secondary market

����Provide firm bid/ask spreads in secondary market

����Encourage SOEs and private sector to issue ILBs

����Cooperate with mutual funds to issue the ILB-related funds

����Allow dealers to develop inflation-related products (e.g. Inflation Derivative)

Public Debt Management Office, Ministry of Finance - Thailand