LafargeHolcim Ltd · CORPORATES ISSUER IN-DEPTH 9 March 2018 RATINGS LafargeHolcim Ltd LT issuer...

8

CORPORATES ISSUER IN-DEPTH 9 March 2018 RATINGS LafargeHolcim Ltd LT issuer rating Baa2 ST issuer rating P-2 Senior Unsecured Baa2 Outlook Negative KEY METRICS: LafargeHolcim Ltd CHF in millions 2016 2017 Revenue 26,904 26,129 EBITDA 5,529 5,431 RCF/net debt 20.4% 17.4% Debt/EBITDA 4.1x 4.0x Contacts Stanislas Duquesnoy +49.69.7073.0781 VP-Sr Credit Officer [email protected] Matthias Hellstern +49.69.70730.745 MD-Corporate Finance [email protected] Taisiia Alieksieienko +49.69.7073.0707 Associate Analyst [email protected] CLIENT SERVICES Americas 1-212-553-1653 Asia Pacific 852-3551-3077 Japan 81-3-5408-4100 EMEA 44-20-7772-5454 LafargeHolcim Ltd New growth strategy should underpin credit quality » 'Building for Growth' strategy for 2018-2022 should support the current rating. We welcome global building materials producer LafargeHolcim Ltd 's (Baa2 negative) shift to a disciplined growth strategy after years of focusing on asset disposals to reduce leverage. The previous strategy was unsuccessful because it has not sufficiently delevered the company and was overly skewed towards shareholder returns. » Profitability of aggregates and ready-mix concrete businesses lags best-in-class peers. LafargeHolcim's public recognition of its profitability gap with competitors in aggregates and ready-mix, such as HeidelbergCement AG (Baa3 stable), CRH plc (Baa1 stable) or independent producers (not vertically integrated in cement), for the first time is an important first step to address the issue. » Plan to improve cash conversion should help fund growth. We welcome LafargeHolcim's target to improve cash conversion as measured by FCF/recurring EBITDA to around 40% by 2022 from 28% in 2017. Free cash flow generation has been historically weak. In 2017, LafargeHolcim had a Moody's-defined reported FCF (i.e. after dividends) of around CHF70 million for a Moody's defined reported EBITDA of around CHF5.7 billion. An improvement in FCF is needed to fund the company's organic growth programme. » Focus on Products and Solutions business to reduce capital intensity. Peers such as Compagnie de Saint-Gobain SA (Baa2 stable) have also set themselves the objective of reducing capital intensity to generate more return on invested capital in a low-return environment. Both Saint-Gobain and CRH have shown that a high level of vertical integration (both on the heavy and light side of the industry) can be a very successful business model. » LafargeHolcim should benefit from sound market conditions during the next 12 to 18 months. However we are cautious about the company's forecast revenue growth of 3% to 5% per annum and a recurring EBITDA growth of at least 5% per annum until 2022, which implies a benign macroeconomic environment for the next five years. That would be quite exceptional because we are already nine years into the recovery from the global financial crisis. We are concerned that LafargeHolcim, which is weakly positioned in its rating category, has not built more headroom ahead of a potential downturn.

Transcript of LafargeHolcim Ltd · CORPORATES ISSUER IN-DEPTH 9 March 2018 RATINGS LafargeHolcim Ltd LT issuer...

CORPORATES

ISSUER IN-DEPTH9 March 2018

RATINGS

LafargeHolcim LtdLT issuer rating Baa2

ST issuer rating P-2

Senior Unsecured Baa2

Outlook Negative

KEY METRICS:

LafargeHolcim LtdCHF in millions 2016 2017

Revenue 26,904 26,129

EBITDA 5,529 5,431

RCF/net debt 20.4% 17.4%

Debt/EBITDA 4.1x 4.0x

Contacts

Stanislas Duquesnoy +49.69.7073.0781VP-Sr Credit [email protected]

Matthias Hellstern +49.69.70730.745MD-Corporate [email protected]

Taisiia Alieksieienko +49.69.7073.0707Associate [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

LafargeHolcim LtdNew growth strategy should underpin credit quality

» 'Building for Growth' strategy for 2018-2022 should support the current rating.We welcome global building materials producer LafargeHolcim Ltd's (Baa2 negative)shift to a disciplined growth strategy after years of focusing on asset disposals to reduceleverage. The previous strategy was unsuccessful because it has not sufficiently deleveredthe company and was overly skewed towards shareholder returns.

» Profitability of aggregates and ready-mix concrete businesses lags best-in-classpeers. LafargeHolcim's public recognition of its profitability gap with competitors inaggregates and ready-mix, such as HeidelbergCement AG (Baa3 stable), CRH plc (Baa1stable) or independent producers (not vertically integrated in cement), for the first time isan important first step to address the issue.

» Plan to improve cash conversion should help fund growth. We welcomeLafargeHolcim's target to improve cash conversion as measured by FCF/recurringEBITDA to around 40% by 2022 from 28% in 2017. Free cash flow generation has beenhistorically weak. In 2017, LafargeHolcim had a Moody's-defined reported FCF (i.e. afterdividends) of around CHF70 million for a Moody's defined reported EBITDA of aroundCHF5.7 billion. An improvement in FCF is needed to fund the company's organic growthprogramme.

» Focus on Products and Solutions business to reduce capital intensity. Peers suchas Compagnie de Saint-Gobain SA (Baa2 stable) have also set themselves the objectiveof reducing capital intensity to generate more return on invested capital in a low-returnenvironment. Both Saint-Gobain and CRH have shown that a high level of verticalintegration (both on the heavy and light side of the industry) can be a very successfulbusiness model.

» LafargeHolcim should benefit from sound market conditions during the next 12to 18 months. However we are cautious about the company's forecast revenue growthof 3% to 5% per annum and a recurring EBITDA growth of at least 5% per annum until2022, which implies a benign macroeconomic environment for the next five years. Thatwould be quite exceptional because we are already nine years into the recovery from theglobal financial crisis. We are concerned that LafargeHolcim, which is weakly positioned inits rating category, has not built more headroom ahead of a potential downturn.

MOODY'S INVESTORS SERVICE CORPORATES

Return to disciplined growth after several years of asset salesLafargeHolcim Ltd (Baa2 negative), the world's largest building materials producer by volumes, presented its new five-year strategycalled 'Building for Growth' to investors on 2 March 2018. We welcome the company's return to disciplined organic and externalgrowth which, alongside its continued commitment to the investment-grade rating, should support credit quality. The strategy coversthe period 2018-2022.

LafargeHolcim's approach under new Group Chief Executive Jan Jenisch, who took the post in September 2017, follows several years ofshrinking the group's operations (both at Lafarge SA and LafargeHolcim Ltd, which was created by the merger of Lafarge and Holcim in2015). As illustrated in Exhibit 1, the pro forma revenue and EBITDA of LafargeHolcim has almost halved since 2010 while the pro formaEBITDA margin has not improved significantly. We believe that this strategy has not convincingly addressed the company's objectiveto restore a stronger balance sheet to sustain its solid investment-grade rating and to improve its return on invested capital (ROIC).The group's reported net debt/ recurring EBITDA has only marginally improved to 2.4x at the end of 2017 from 2.8x pro forma 2014.LafargeHolcim's ROIC was around 5.8% in 2017, below its weighted average cost of capital of 7%-7.5% which indicates that investedcapital is not being used effectively. ROIC is also well below the company's target of exceeding 8% presented as part of its strategicupdate to investors. LafargeHolcim's credit metrics have been below the requirements to maintain the current rating category since themerger of the two companies in July 2015.

Exhibit 1

LafargeHolcim has scaled back its operations substantially over time without a significant improvement in profitabilityComparison of LafargeHolcim/Lafarge pro forma revenue, EBITDA and EBITDA margin for 2010 and 2017 (revenue and EBITDA in CHF billions)

20%

21%

22%

23%

24%

0

5

10

15

20

25

30

35

40

45

50

Fiscal year 2010 Fiscal year 2017

Revenues EBITDA EBITDA margin

Sources: Lafarge SA, Holcim Ltd, LafargeHolcim Ltd

The high level of debt on the balance sheet (reported net debt of CHF14.3 billion at 31 December 2017) and high invested capital(around CHF46 billion) resulted from the primarily debt-funded acquisition of Egyptian cement producer Orascom, which was donein 2008 based on very high valuation multiples at the peak of the construction cycle. That forced Lafarge SA and LafargeHolcim intoa deleveraging strategy through shrinking the group's balance sheet rather than through addressing the numerator of the leverageequation, the earnings. While this strategy probably made sense in the aftermath of the global financial crisis due to very tough marketconditions, it is now time to capitalise on LafargeHolcim's forecast of a 2%-3% annual growth in cement consumption until 2030 toaddress the return side of the equation.

LafargeHolcim has four main levers for growth: more selective investments in markets with strong growth potential, a more aggressivestrategy in aggregates and ready-mix concrete, development of its downstream Products and Solutions business and bolt-onacquisitions.

While the company announced the divestment of another CHF2 billion of assets on 2 March, it has indicated that it will reinvest theproceeds in the business to support operations with the strongest growth prospects. We do not see the reinvestment of divestmentproceeds as credit negative per se, as long as they are used for organic projects or bolt-on acquisitions that add value and profits.

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 9 March 2018 LafargeHolcim Ltd: New growth strategy should underpin credit quality

MOODY'S INVESTORS SERVICE CORPORATES

We also welcome the group's continued commitment to its investment grade-rating, the discontinuation of the CHF1 billion sharebuyback programme after CHF581 million had been spent. The dividend at CHF2 per share remains very high compared to the FCFgeneration ability, but we take comfort from the fact that, for the time being, it is not going to be increased. We believe that investorsshould not read too much into LafargeHolcim's revised wording on its commitment to an investment-grade rating from a stronginvestment-grade rating previously. We believe that this change was driven by the weak rating positioning of LafargeHolcim ratherthan by a shift to more aggressive financial policies.

Acknowledgment of profitability gap in aggregates and ready-mix concrete is first step to fixing itAs part of its strategy presentation, LafargeHolcim also acknowledged that profitability in its aggregates and ready-mix concretebusinesses lags that of best-in-class peers such as HeidelbergCement AG (Baa3 stable), CRH plc (Baa1 stable) and independentproducers (not vertically integrated in cement) (see Exhibit 2). LafargeHolcim's aggregates and ready-mix concrete businesses togethercontributed 35% of group revenue in 2017.

It is the first time the company has talked about the profitability gap, which is a good sign in itself and an important first step inaddressing the problem. LafargeHolcim intends to close the gap by appointing dedicated management teams for these two activitieswith full profit and loss (P&L) responsibility and setting independent financial targets to avoid the activities serving only as by-productsof the group's cement business. The closing of this gap bears execution risk.

Exhibit 2

LafargeHolcim's aggregates activities are less profitable than HeidelbergCement's2017 EBITDA margin for aggregates business of LafargeHolcim and HeidelbergCement

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

LafargeHolcim HeidelbergCement

We have not included a comparison of RMC and other activities as we believe that the composition of the segments is very different for both companiesSources: LafargeHolcim, HeidelbergCement

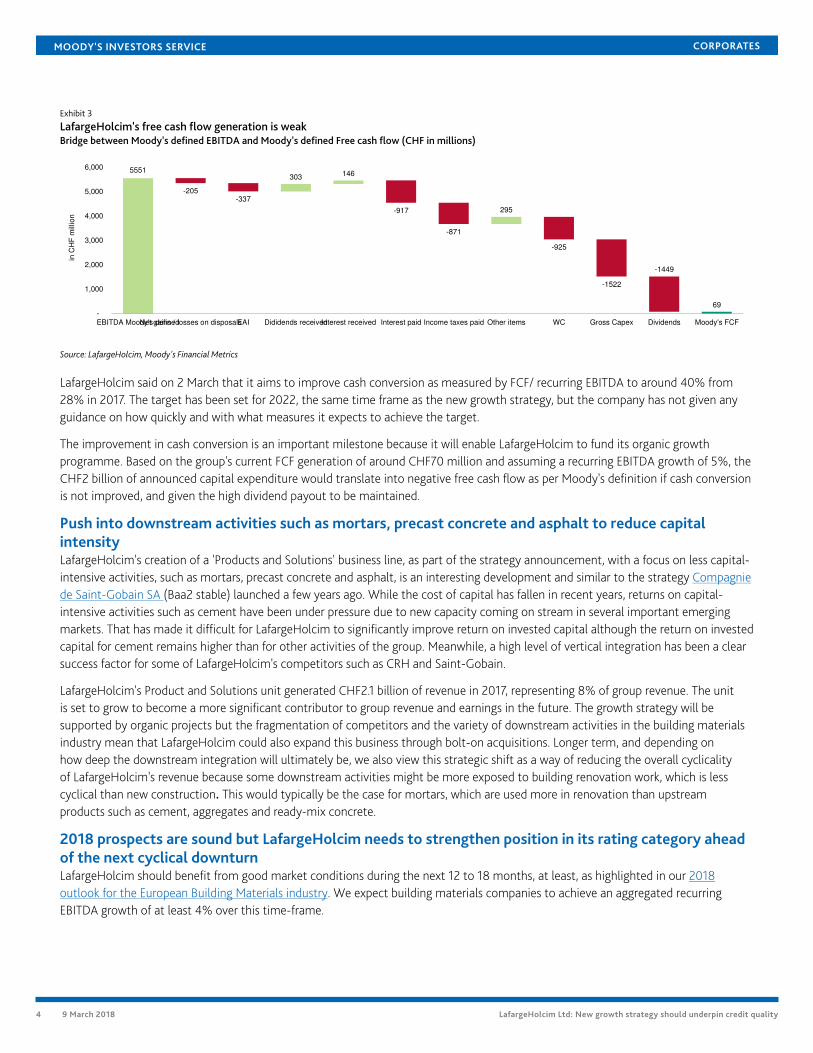

Plan to improve cash conversion should help fund growthLafargeHolcim's free cash flow (FCF) generation has been historically weak with a 2017 Moody's-defined reported FCF of only aroundCHF70 million for a Moody's-defined reported EBITDA of around CHF5.7 billion (see Exhibit 3). Arguably cement production is avery capital intensive business and several important markets are currently oversupplied, but that does not satisfactorily explainLafargeHolcim's weak FCF.

3 9 March 2018 LafargeHolcim Ltd: New growth strategy should underpin credit quality

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 3

LafargeHolcim's free cash flow generation is weakBridge between Moody's defined EBITDA and Moody's defined Free cash flow (CHF in millions)

5551

-205-337

303 146

-917

-871

295

-925

-1522

-1449

69 -

1,000

2,000

3,000

4,000

5,000

6,000

EBITDA Moody's definedNet gains / losses on disposalsEAI Dididends receivedInterest received Interest paid Income taxes paid Other items WC Gross Capex Dividends Moody's FCF

in C

HF

millio

n

Source: LafargeHolcim, Moody's Financial Metrics

LafargeHolcim said on 2 March that it aims to improve cash conversion as measured by FCF/ recurring EBITDA to around 40% from28% in 2017. The target has been set for 2022, the same time frame as the new growth strategy, but the company has not given anyguidance on how quickly and with what measures it expects to achieve the target.

The improvement in cash conversion is an important milestone because it will enable LafargeHolcim to fund its organic growthprogramme. Based on the group's current FCF generation of around CHF70 million and assuming a recurring EBITDA growth of 5%, theCHF2 billion of announced capital expenditure would translate into negative free cash flow as per Moody's definition if cash conversionis not improved, and given the high dividend payout to be maintained.

Push into downstream activities such as mortars, precast concrete and asphalt to reduce capitalintensityLafargeHolcim's creation of a 'Products and Solutions' business line, as part of the strategy announcement, with a focus on less capital-intensive activities, such as mortars, precast concrete and asphalt, is an interesting development and similar to the strategy Compagniede Saint-Gobain SA (Baa2 stable) launched a few years ago. While the cost of capital has fallen in recent years, returns on capital-intensive activities such as cement have been under pressure due to new capacity coming on stream in several important emergingmarkets. That has made it difficult for LafargeHolcim to significantly improve return on invested capital although the return on investedcapital for cement remains higher than for other activities of the group. Meanwhile, a high level of vertical integration has been a clearsuccess factor for some of LafargeHolcim's competitors such as CRH and Saint-Gobain.

LafargeHolcim's Product and Solutions unit generated CHF2.1 billion of revenue in 2017, representing 8% of group revenue. The unitis set to grow to become a more significant contributor to group revenue and earnings in the future. The growth strategy will besupported by organic projects but the fragmentation of competitors and the variety of downstream activities in the building materialsindustry mean that LafargeHolcim could also expand this business through bolt-on acquisitions. Longer term, and depending onhow deep the downstream integration will ultimately be, we also view this strategic shift as a way of reducing the overall cyclicalityof LafargeHolcim's revenue because some downstream activities might be more exposed to building renovation work, which is lesscyclical than new construction. This would typically be the case for mortars, which are used more in renovation than upstreamproducts such as cement, aggregates and ready-mix concrete.

2018 prospects are sound but LafargeHolcim needs to strengthen position in its rating category aheadof the next cyclical downturnLafargeHolcim should benefit from good market conditions during the next 12 to 18 months, at least, as highlighted in our 2018outlook for the European Building Materials industry. We expect building materials companies to achieve an aggregated recurringEBITDA growth of at least 4% over this time-frame.

4 9 March 2018 LafargeHolcim Ltd: New growth strategy should underpin credit quality

MOODY'S INVESTORS SERVICE CORPORATES

LafargeHolcim's guidance for recurring EBITDA growth of at least 5% for 2018 seems achievable and much more realistic thanguidance the company has given in the past. The group's strong geographical diversification should enable it to weather difficult marketconditions in some South East Asian or Middle Eastern markets. Rising prices for building materials in many developed markets and anexpected acceleration in volume growth are positive drivers for the company's operating performance.

However we are more cautious about the new management team's longer-term guidance. LafargeHolcim expects revenue growthof 3% to 5% per annum and a recurring EBITDA growth of 5% per annum until 2022, which implies a benign macroeconomicenvironment for the next five years. That would be quite exceptional in light of the fact that we are already nine years into arecovery from the global financial crisis and that building materials markets tend to be cyclical. In this respect, we are concerned thatLafargeHolcim has not built any headroom under its current rating category ahead of a potential downturn in the economy. We expectLafargeHolcim will touch the lower end of our rating guidance - RCF/net debt of 20% and debt/EBITDA of 3.5x - by the end of 2018 ifit achieves its target of at least 5% growth in recurring EBITDA. LafargeHolcim's credit metrics at the end of 2017 were just outside thelower end of our rating guidance with RCF/net debt of around 17-18% and debt/EBITDA of around 4.0x.

5 9 March 2018 LafargeHolcim Ltd: New growth strategy should underpin credit quality

MOODY'S INVESTORS SERVICE CORPORATES

Moody’s related publications

» Outlook: Building Materials - Europe: 2018 outlook positive on stronger volumes, prices (Slides), November 2017

» Issuer in-depth: Compagnie de Saint-Gobain : FAQ about planned Sika acquisition, strategy update, September 2017

» Issuer Comment: HeidelbergCement AG: Strong synergy delivery enables HC to achieve the lower end of its 2017 earningsguidance, February 2018

6 9 March 2018 LafargeHolcim Ltd: New growth strategy should underpin credit quality

MOODY'S INVESTORS SERVICE CORPORATES

© 2018 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGSDO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’SOPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVEMODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’SPUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOTPROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THESUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATIONAND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FORPURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSESAND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1114700

7 9 March 2018 LafargeHolcim Ltd: New growth strategy should underpin credit quality

MOODY'S INVESTORS SERVICE CORPORATES

Contacts

Erica K Billingham +44.20.7772.5655AVP-Research [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

8 9 March 2018 LafargeHolcim Ltd: New growth strategy should underpin credit quality