Ladies and gentlemen. - United Cities and Local Governments · Ladies and gentlemen. ... model, the...

38

UCLG World Council, 30 October - 1 November 2006 Meeting of the UCLG Committee on Local Finance and Development Wednesday, 1 st November Ladies and gentlemen. First of all I would like to thank the Committe on Finances for the invitation to give a presentation of the four Associations project on Finance of local public services. The four Associations is a grouping of Deutscher Staedtetag (the German Association of Cities), Vereniging van Nerderlandske Gemeenden (VNG) from the Netherlands, The Local Government Association for England and Wales (LGA) and Local Government Denmark. But before I give a presentation of the report, I would like to make reference to the broader tendencies in Europe. The issue of financing local and regionsl public services – and more generally, that of local and regional finances – is one of the primary concerns for the local and regional elected representatives in Europe. This being the case, on 4 July 2005, The Council of European Municipalities and Regions (CEMR) organised in Stuttgart a first seminar on local finances in Europe. One of the the first commomn conclusions to come out of this seminar was that without adequate financing, local self-government and the principle of subsidiarity are meaningless. Financial autonomy is a pre-requisite for local self- gernment. Following the seminar on Local Finances in Europe in Stuttgart, one of the major topics at CEMR’s General Assembly in Innsbruck from 10.-12. of May this year was “Adapting and financing public services”. Among others there were organised a Workshop of finances and a report on Local Finance in Europe was presented by the Centre for Public Administration Research in Austria. (My colleage from the Austrian Association, Mr. Erich Prambroeck) Today local and regional authorities in Europe are especially confronted with three developing phenomena at present: • The economic and budgetary context that drives Central Governments to reduce financing to local and regional authorities • The growing proportion of State allocations in local budgets, and • The often uncompensated transfer of competencies to local and regional authorities. On the other hand, our citizens demand more and more services and question the quality of the services delivered by the local authorities. And - as was emphasized in several speaches yesterday – it is the local level which play an crucial role as we meet the challenges og globalisation, migration, etc. But apart from these common challenges, it is interesting to note, that even within Europe, we can identify different directions and traditions for local finance – we often refer to them as the anglo saxon model, the nordic model and the continental model. Lately we can identify a mediteranian model. Local government revenue and its main elements: The local government revenue in percent of the Gross Domestic Product GDP varies widely • High quotas ranging from 20 to 32 percent are shown for Finland, Sweden and Denmark

Transcript of Ladies and gentlemen. - United Cities and Local Governments · Ladies and gentlemen. ... model, the...

UCLG World Council, 30 October - 1 November 2006 Meeting of the UCLG Committee on Local Finance and Development

Wednesday, 1st November

Ladies and gentlemen. First of all I would like to thank the Committe on Finances for the invitation to give a presentation of the four Associations project on Finance of local public services. The four Associations is a grouping of Deutscher Staedtetag (the German Association of Cities), Vereniging van Nerderlandske Gemeenden (VNG) from the Netherlands, The Local Government Association for England and Wales (LGA) and Local Government Denmark. But before I give a presentation of the report, I would like to make reference to the broader tendencies in Europe. The issue of financing local and regionsl public services – and more generally, that of local and regional finances – is one of the primary concerns for the local and regional elected representatives in Europe. This being the case, on 4 July 2005, The Council of European Municipalities and Regions (CEMR) organised in Stuttgart a first seminar on local finances in Europe. One of the the first commomn conclusions to come out of this seminar was that without adequate financing, local self-government and the principle of subsidiarity are meaningless. Financial autonomy is a pre-requisite for local self-gernment. Following the seminar on Local Finances in Europe in Stuttgart, one of the major topics at CEMR’s General Assembly in Innsbruck from 10.-12. of May this year was “Adapting and financing public services”. Among others there were organised a Workshop of finances and a report on Local Finance in Europe was presented by the Centre for Public Administration Research in Austria. (My colleage from the Austrian Association, Mr. Erich Prambroeck) Today local and regional authorities in Europe are especially confronted with three developing phenomena at present:

• The economic and budgetary context that drives Central Governments to reduce financing to local and regional authorities

• The growing proportion of State allocations in local budgets, and • The often uncompensated transfer of competencies to local and regional authorities.

On the other hand, our citizens demand more and more services and question the quality of the services delivered by the local authorities. And - as was emphasized in several speaches yesterday – it is the local level which play an crucial role as we meet the challenges og globalisation, migration, etc. But apart from these common challenges, it is interesting to note, that even within Europe, we can identify different directions and traditions for local finance – we often refer to them as the anglo saxon model, the nordic model and the continental model. Lately we can identify a mediteranian model. Local government revenue and its main elements: The local government revenue in percent of the Gross Domestic Product GDP varies widely

• High quotas ranging from 20 to 32 percent are shown for Finland, Sweden and Denmark

UCLG World Council, 30 October - 1 November 2006 Meeting of the UCLG Committee on Local Finance and Development

Wednesday, 1st November

• Shares above the European average of up to 18% af GDP are given for local government in numerous countries such as the Czech Republic, Italy, Hungary the Netherlands, Poland, UK, Norway and Iceland.

• Slightly below the European average share of local government of GDP we find France, • Whereas shares from 10 to 5 percent are shown for local government in Austria, Germany

and Spain, amoung several other European countries. Thus the local government revenue in percentage of GDP differs widely between the four countries, which have elaborated the 4 Association project. Out of the four countries the local government revenue has only increased in Denmark in the period from 2000-2005. Local government compared to General government: General government comprises central, state and local government as well as social security funds. Compared to General Government, shares of more than 28 percent show up for the Nordic countries, the Netherlands, UK, Italy and Poland, whilst countries like Germany, Spain, France and many other European countries have a share between 10 to 27 percent. There have been clear signs of growth in local government revenue over the last years (measured in % of General Government) in several European Countries – amoug then the Netherlands, the Nordic countries, Italy, Greece etc. On the other hand there has been steady or even declining shares for the local government sector in Germany, Austria, Spain, to mention some countries. Local revenue from direct and indirect taxes, revenue from social contributions, general grants versus specific or earmarked grants, other revenues and net lending/net borrowing. Generally speaking, the characteristics of local government tax revenues are similar to the facts for total local income, which I presented earlier. But it is important to emphasize, that tax revenues account for more than 50 percent of total local government revenue only in Austria, Denmark, Latvia, Slovakia and Spain. In several countries, like the UK and Denmark government is mainly financed by direct taxes, whilst in several other European countries like Germany, local government is financed mainly by indirect taxes.In the Netherlands – on the other hand – direct and indirect taxes are of more or less equivalent importance. Due to the competencies of local government in some countries (social insurance for civil servants) social contributions generate a certain share of local government revenue in a few countries, among them the Netherlands and Denmark. When it comes to transfers to local governments, transfers contribute to total local government revenue by more than 50 percent in one third of the countries, for instance the Netherlands on the UK, whilst the transfers account for a major share ranging from 30-50 percent of total local revenue in the main part of the countries, for instance in Germany and Denmark. So as can be seen from the above, the way Local Finance is organised in the 4 countries: the UK, the Netherlands, Germany and Denmark are different. This gives an excellent opportunity to exchange experiences and to bring forward at the national agendas.

UCLG World Council, 30 October - 1 November 2006 Meeting of the UCLG Committee on Local Finance and Development

Wednesday, 1st November

4 Associations Report As mentioned in the introduction the 4 Associations are the grouping of four Associations from the Netherlands, England and Wales, Germany and Denmark. The grouping har been active for a number of years and currently meets in one of the member countries each year at Chief Executive level. The associations share a common agenda in promoting the interests of their local authorities at a national and European agenda. In 2006 a report was elaborated for the meeting of the Chief Executive level on how we finance our local public services. The main intention is to provide a basis from which we can support each other in national campaigns to realise our shared ambition for long term, sustainable funding of local government. Reference to report: Contrywise. ................. As I mentioned in the introduction, we find this meetings at the Chief Executive level of major importance, since the meetings allows our for Chief Executives to discuss strategic issues of common interest, contribute to the formulation of a common agenda in promoting the interests of our local authorities on the European agenda and give inspiration and usefull examples of best practise from the four countries to bring forward at the national agendas. For the meeting next year to be celebrated in London, we will elaborate a report on Demographic Change, since the impact of demographic change is moving up the political agenda at the local, national and European level. Conclusions:

• Statistics: There are many pitpitfalls of public sector statistics, so – concentrate on a limited amount of data which allows general information. Anyhow, there will be a pionering challenge to statistical work about Local Finance, since there are no such comparisons of recent local finance data avaliable across the continents. Therefore, another suggestion from my side to the Committee on Local Finance would be to urge the member associations of UCLG to elaborate descriptions of “Municipal self-rule and local finance”. I have handed out a memorandum on “Municipal self-rule and municipal economy in Denmark” as an example. At this 2nd World Council meeting a draft version of a publication on profiles of the members of the Executive Bureau has been presented. Added value – our members.

• What is transferable? Exchange of approaches and best practises to use at the national level –

added value to our members at UCLG As one example of best practise, I have handed out a decription of the principle of compensation, which is part of the law concerning grants to the local authorities in Denmark. The principle assures, that local authorities are compensated, everytime when new tasks or competences are transferred to the local or regional level.

• Information about the local government reform in Denmark

UCLG World Council, 30 October - 1 November 2006 Meeting of the UCLG Committee on Local Finance and Development

Wednesday, 1st November

• Finally, in my opinion there is the question which role UCLG can play – in other words are there issues UCLG can put forward and advocate. But there, you the members of the Committee of Finance are the experts, and I look forward to follow the work of the Committee.

If you are interested in the full report of the 4 Associations report or have additional questions, please don’ t hesitate to contact me. Thank you very much for your attention. Thank you very much for your attention. Uwe Nikolai Lorenzen Director International Relations Local Government Denmark

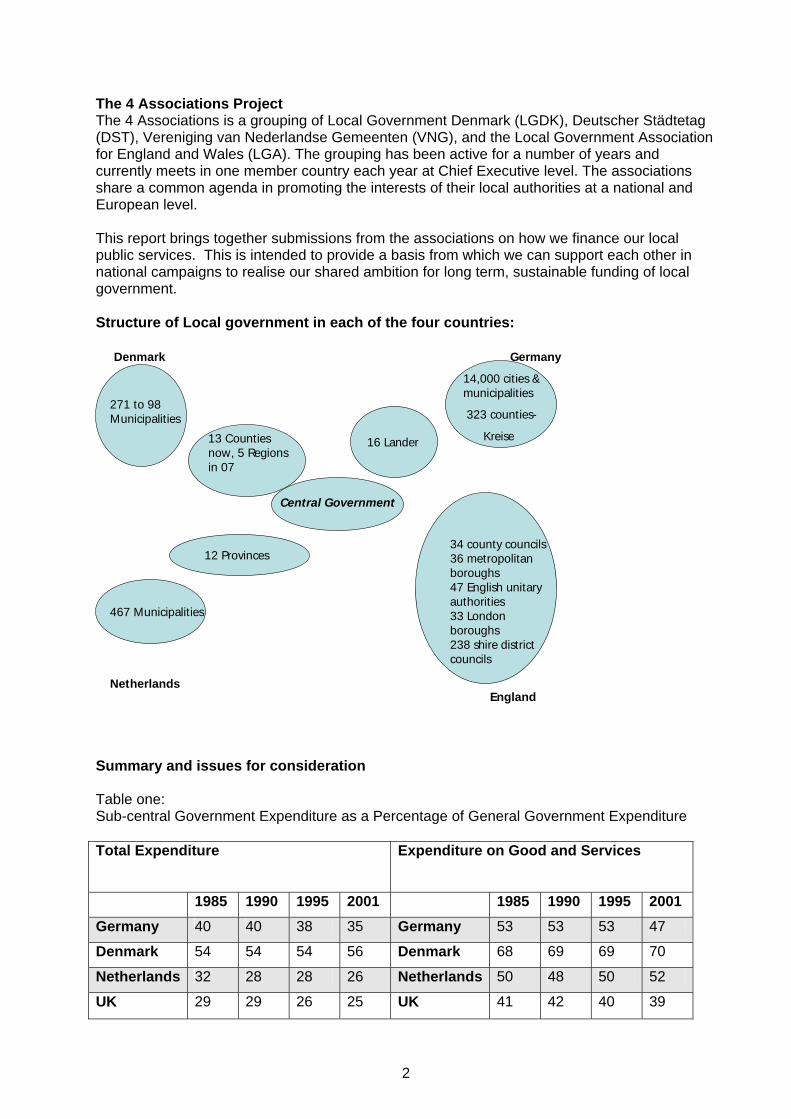

The 4 Associations Project

Local Government Denmark (LGDK), Deutscher Städtetag (DST), Vereniging van Nederlandse Gemeenten (VNG), and the Local Government Association for England and Wales (LGA) Contents:

The 4 Associations Project P 2 Summary and key issues P 2 Local Government Finance in England P 6 Local Government Finance in Germany P 13 Local Government Finance in the Netherlands P 22 Local Government Finance in Denmark P 26 Annex 1: The European Charter of Self Governance P 27 Annex 2: Exchange rates P 27

England

The Netherlands

Denmark

Germany

Learning from each other: A Four Associations Report “How we finance our local

2

The 4 Associations Project The 4 Associations is a grouping of Local Government Denmark (LGDK), Deutscher Städtetag (DST), Vereniging van Nederlandse Gemeenten (VNG), and the Local Government Association for England and Wales (LGA). The grouping has been active for a number of years and currently meets in one member country each year at Chief Executive level. The associations share a common agenda in promoting the interests of their local authorities at a national and European level. This report brings together submissions from the associations on how we finance our local public services. This is intended to provide a basis from which we can support each other in national campaigns to realise our shared ambition for long term, sustainable funding of local government. Structure of Local government in each of the four countries:

Central Government

Denmark

467 Municipalities

34 county councils36 metropolitan boroughs47 English unitary authorities33 London boroughs238 shire district councils

Germany

14,000 cities & municipalities

323 counties-

Kreise16 Lander

12 Provinces

Netherlands

13 Counties now, 5 Regions in 07

271 to 98 Municipalities

England Summary and issues for consideration Table one: Sub-central Government Expenditure as a Percentage of General Government Expenditure Total Expenditure Expenditure on Good and Services

1985 1990 1995 2001 1985 1990 1995 2001 Germany 40 40 38 35 Germany 53 53 53 47

Denmark 54 54 54 56 Denmark 68 69 69 70

Netherlands 32 28 28 26 Netherlands 50 48 50 52

UK 29 29 26 25 UK 41 42 40 39

3

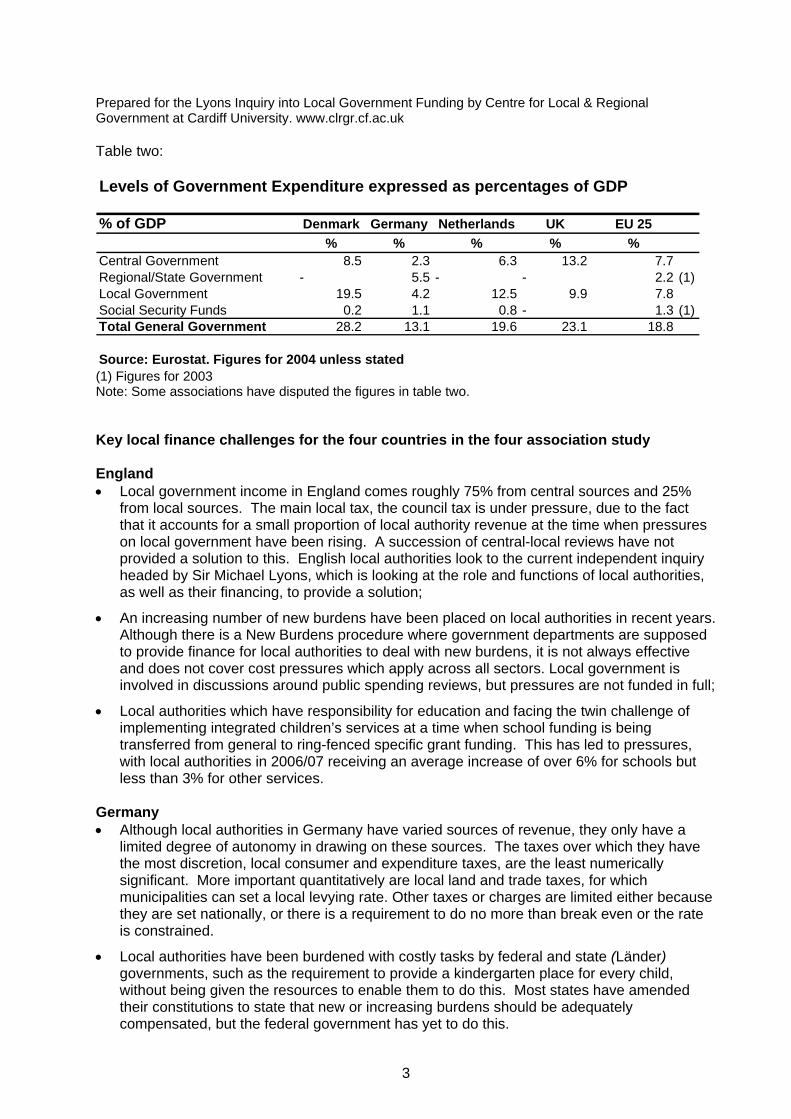

Prepared for the Lyons Inquiry into Local Government Funding by Centre for Local & Regional Government at Cardiff University. www.clrgr.cf.ac.uk Table two:

Levels of Government Expenditure expressed as percentages of GDP

% of GDP Denmark Germany Netherlands UK EU 25% % % % %

Central Government 8.5 2.3 6.3 13.2 7.7Regional/State Government - 5.5 - - 2.2 (1)Local Government 19.5 4.2 12.5 9.9 7.8Social Security Funds 0.2 1.1 0.8 - 1.3 (1)Total General Government 28.2 13.1 19.6 23.1 18.8

Source: Eurostat. Figures for 2004 unless stated (1) Figures for 2003 Note: Some associations have disputed the figures in table two. Key local finance challenges for the four countries in the four association study England • Local government income in England comes roughly 75% from central sources and 25%

from local sources. The main local tax, the council tax is under pressure, due to the fact that it accounts for a small proportion of local authority revenue at the time when pressures on local government have been rising. A succession of central-local reviews have not provided a solution to this. English local authorities look to the current independent inquiry headed by Sir Michael Lyons, which is looking at the role and functions of local authorities, as well as their financing, to provide a solution;

• An increasing number of new burdens have been placed on local authorities in recent years. Although there is a New Burdens procedure where government departments are supposed to provide finance for local authorities to deal with new burdens, it is not always effective and does not cover cost pressures which apply across all sectors. Local government is involved in discussions around public spending reviews, but pressures are not funded in full;

• Local authorities which have responsibility for education and facing the twin challenge of implementing integrated children’s services at a time when school funding is being transferred from general to ring-fenced specific grant funding. This has led to pressures, with local authorities in 2006/07 receiving an average increase of over 6% for schools but less than 3% for other services.

Germany • Although local authorities in Germany have varied sources of revenue, they only have a

limited degree of autonomy in drawing on these sources. The taxes over which they have the most discretion, local consumer and expenditure taxes, are the least numerically significant. More important quantitatively are local land and trade taxes, for which municipalities can set a local levying rate. Other taxes or charges are limited either because they are set nationally, or there is a requirement to do no more than break even or the rate is constrained.

• Local authorities have been burdened with costly tasks by federal and state (Länder) governments, such as the requirement to provide a kindergarten place for every child, without being given the resources to enable them to do this. Most states have amended their constitutions to state that new or increasing burdens should be adequately compensated, but the federal government has yet to do this.

4

• Faced with this situation, and with the rising costs of personnel and pensions, local authorities have been running short-term deficits for several years. In 2003 the level of short-term debt reached €15bn (£10bn). It is currently unclear how they will get out of this crisis. The level of capital investment, which is traditionally financed locally, has fallen under this pressure.

Netherlands • The main local tax up to 2006 has been the real estate (property tax) which is levied on

domestic property and businesses, with separate charges for ownership and occupancy. This accounted for 15% of municipal income and 83% of all local taxes in 2005. From 1 January 2006 local authorities have lost discretion over the right to set the rate for most of this income, which is now tied to the rate of inflation. They retain discretion over setting the rate for the element relating to domestic property ownership. This is the subject of a court challenge, claiming that this violates article 9 of the European Charter of Local Self-Government. Local authorities are pressing for a local income tax to replace the property taxes which they have lost.

• From 1 January 2007 local authorities take over responsibility for social support. This will be financed both through existing budgets and through transfers from central government through general grant.

• A central/local committee has recently examined specific grants to local authorities. The outcome of this review is that there will be fewer specific grants and more consolidation of accounting and auditing requirements for specific grants. This is in line with the wishes of local authorities, who contend that they give rise to more bureaucracy and less freedom for local authorities.

Denmark • Local Government in Denmark is in the middle of a major reorganisation. From a system

with 271 districts and 13 counties; they are moving to a system with 98 district municipalities and 5 regions. This will come fully into effect on 1 January 2007. The new structure was negotiated and agreed with local government.

• There has been much discussion on which tasks are appropriate to be performed by which tier. Overall, there is a movement of tasks from the old counties to the new districts. Functions of the new districts include community healthcare, social affairs, special education, environment and roads and public transport. Functions of the new regions include hospital services, regional development and public transport. Tax collection will become a central government responsibility.

• There are major issues concerned with compensation. Authorities are continuing to negotiate the compensation for these new arrangements and expect it to take 2-3 years to finalise the arrangements. Transition costs are an issue and there has been a large overspend

• The main local tax is local income tax. This is split 68% for the national government, 10% for the regions and 22% for the districts. There is also a local property tax.

• Since 2002 the government has imposed a tax freeze, which means that taxes cannot be increased. The tax freeze applies to both direct and indirect taxes.

• There has been extensive debate over the split of taxes and the equalisation system. LGDK’s role is to concentrate on guiding principles rather than to advocate any particular distribution.

• The new arrangements for health will aim at promoting treatment in community rather than specialist settings. Districts will commission services from regions, which will have responsibility for hospitals. The system is aimed at incentivising local government to reduce health costs by providing better community health care. 80% of health budgets are at

5

regional level with 20% at a district level. 10% of this 20% is provided through general grant.

• There is a relationship between the Danish Treasury and the KLDK whereby a compensation arrangement has to be reached before any new burdens on local authorities can be passed on.

Issues for the 4 association partners to consider: • This document provides information on the state of local government finance in the 4

countries. It is clear that we share common issues at the national level and there are a number of particular challenges that the associations may wish to consider for further discussion.

• Across three countries it seems to be the case that government is not fully funding new or increased burdens. This is true for the England but also for Germany (eg funding kindergartens), and for the Dutch. The Danes have a new burdens procedure and the it may be worth the other associations considering how well this is working and if it is a model that can be exported.

• There is a need for local government to have access to local sources of taxation where they can determine the rate. This is the key message from the Dutch challenge on loss of most their property tax, and from the German comment that most of their taxes are either determined nationally or give them little leeway. The LGA’s “combination option work” highlights this problem.

• The associations have a strong preference for general rather than specific grants. This comes out of the English experience with school funding and with the Dutch review of specific grants - which led to a reduction in the number of specific grants.

• We restate the importance of the principles set out in article 9 of the European Charter of Local Self-Government for local financial autonomy which in particular states:

o that “local authorities’ financial resources should be commensurate with the responsibilities provided for by constitutions and by law” in different countries.

o the importance of local authorities having diversified sources of income which are of a buoyant nature.

o that, as far as possible, funds should not be earmarked for specific projects. (full text of article 9 included in Annex 1)

6

Local Government Finance in England As Travers1 says; “Britain, and indeed, England, has a medium-scale system of local government; smaller than those in the Nordic countries, but rather larger than those in countries such as France, New Zealand or Japan”. Some reasons for this are:

The public sector is relatively small in terms of its importance within GDP; Local government represents about a quarter of public expenditure; in some countries, such

as Denmark it is around 60%; Many services are delivered locally through national agencies which are not locally

accountable. These include health services, further and higher education and vocational training. In many cases these were previously the responsibility of local government.

The context: Sources of local income and debate over reform In 2005/06 76%of all income for Local government in England came in the form of government grant and redistributed business rates, which is an assigned revenue. 24.4% came from local domestic taxation; the council tax. A substantial proportion of government grant to authorities is ring-fenced. From 2006/07 this proportion is over 50% due to ring-fencing of schools’ funding. The one local tax, Council Tax, is collected by local authorities. One local authority in each area, known as the billing authority, collects income on behalf of itself and others, which are known as preceptors. The Council Tax is a banded capital values tax; values are set according to estimated sale price in April 1991. A revaluation of property to April 2005 values, due to come into effect in April 2007, was recently cancelled by the Government. In recent years, the level of council tax rises has come under scrutiny. This follows a 12.9% increase in council taxes in the year 2003/042. In 2004/05 and 2005/06 the government has used its powers to limit the level of council tax increases for some authorities; 12 authorities had their budgets ‘capped’ in this way in 2004/5 and 9 in 2005/06. Before April 1990 business rates were set and collected locally but since then there has been a national non-domestic rate which is pegged to the general rate of inflation3. Business rates are collected by billing authorities, but the income is paid into a pool and redistributed as part of general grant, known as formula grant. This is distributed according to a formula which takes into differing needs and capacity to generate resources through the council tax. This is constrained by damping rules giving all authorities a minimum grant increase and scaling back the increase of other authorities in order to fund this. Public expenditure is governed by multi-year Spending Reviews covering three years each. Normally the last year of one round overlaps with the first year of the next; although the next spending round; in 2007, will follow on three years behind the last one. In theory there is no provision for discussion outside the Spending Review process. However, in practice there have been a series of discussions in recent years, following surveys by the

1 Tony Travers International Comparisons of Local Government Finance: Propositions and Analysis; research carried out for the Lyons Inquiry; obtainable at http://www.lyonsinquiry.org/ ; Office of the Deputy Prime Minister; Local Government Financial Statistics, England, No 16 2005; Chart K1a 2 Audit Commission (2003) Council Tax Increases 2003/04; Why were they so high ? 3 Specifically; to the increase in the Retail Price Index (RPI) measured from September to September.

7

LGA which indicated that spending pressures were greater than the likely grant increase, and that the effect might well be council tax increases. There is a New Burdens procedure in place whereby government departments are supposed to provide for local authorities finance for any new burdens imposed on local authorities due to any policy or initiative which increases the cost of local authority services. This can be either through a specific grant or through an addition to the general Formula Grant. It does not cover policies which apply across the private and public sectors (for example changes in National Insurance rates)4 This ‘vertical fiscal imbalance’; or Balance of Funding, as it is known in the English context, has been the subject of much comment and analysis, for example within the Balance of Funding Review, chaired by former Local Government Minister Nick Raynsford; which met from 2003 to 2004; and the current independent Inquiry led by Sir Michael Lyons. The view of local government is that the Balance of Funding is a major problem, which stands in the way of accountability to local people. The LGA has set out a way of tackling this, through a series of proposals known as the Combination Option; which include

A reformed a fairer property tax; The progressive return of business rates to local government; The use of a proportion of income tax to fund local government directly, either as a local

income tax or as an assigned share of national income tax; Local government to have access to other taxes and charges, such as tourist taxes; A reduction in grant income to local government consistent with this shift.5

Work for both the Balance of Funding and the Lyons Reviews has concluded that there is widespread ignorance among the public of how local government is funded. For example; most people think that local government services are paid for 75% from the council tax and 25% from government grant.6 Schools Local authorities which are education authorities have the responsibility for provision of universal free education from the age of 5 to the age of 16. This has recently been extended in order to provide a free education place for all three and four year olds. Increasingly over the last twenty years, more and more decisions have been devolved to school level. Most schools operate a system of devolved budgets. Local authorities are responsible for securing the provision of education and for driving up standards. They are also responsible for the upkeep of most school buildings. A minority of secondary schools own their own buildings; this number could increase under the Education and Inspection Bill currently before parliament. Councils support school improvement and challenge performance and provide services for schools such as legal and personnel advice.

There is a national curriculum to which all schools must keep. At the same time in recent years schools have been given more autonomy for budget decisions, with the local authority being obliged by law to put into place a scheme, known as “Fair Funding” for devolving budgets to schools according to a formula which is mainly based on pupil numbers, weighted by age and other factors such as deprivation.

From 1 April 2006/07 schools are funded through a ring-fenced Dedicated Schools Grant which is paid to authorities, which they then distribute to schools, This will be £26.7bn in 2006/07. It is distributed to local authorities on the basis of a formula based on an uplift on past spending

4 See http://www.local.odpm.gov.uk/finance/newburd05.pdf 5 Local Government Association A Combination Option 2004 obtainable from http://www.lga.gov.uk/ 6 Reference BoF and Lyons public opinion work

8

per pupil on schools, with top-ups allocated on the basis of specific DfES priorities, such as personalised learning.

The government has also put in place specific initiatives which are financed through specific grant. This includes the improvement of basic literacy and numeracy skills, money for behaviour related initiatives and improving school leadership capacity. These grants, under the umbrella of the Standards Fund, expanded significantly after 1997. Schools may welcome the additional resources, but there is, at the very least, an expectation that they be spent for the purposes for which they have been allocated. There are also issues about what happens when the grant comes to an end. Schools may expect the resources to continue and to become part of base budgets, thus leading to funding pressures. According to opinion survey work, the public regard schooling as a high priority service. For instance, Islington Council, during its consultation on budget increases for 2006/07, found that the top priority for residents was “improving education standards by investing in our schools”7. A few authorities have consulted on budget options, to the extent of holding local referendums. In Bristol in 2000 54% residents voted for 0% council tax increase in a referendum dominated by the issue of education spending. This was an example of the authority allowing the public to state its preference.8 Charges are levied for items which are not part of the national curriculum, such as school trips and some musical instrument tuition, as well as for school meals. With the government’s extended schools’ agenda, there is the assumption that there will be user charges for childcare provision outside basic school hours9. It remains to be seen the extent to which this is publicly acceptable. Schools are responsible for managing their own budgets. The local education authority verifies that they meet various financial standards. There is a forecasting process for the main demographic changes, for example pupil numbers and numbers with special educational needs both at national and local level. This is carried out both by DfES and by local authorities collectively under the umbrella of the Local Government Association. There is discussion between the two and results are fed into the Spending Review process, but the result is not transparent. For example for the 2004 Spending Review the LGA put in a bid for resources of some £5bn; in fact £3.7bn was allocated.

As far as pay is concerned; basic pay for teachers and other education staff are determined through review bodies or negotiation. Teachers can also receive additional payments for performance. There is some discretion for individual schools as to grading for individual teachers. This has led some commentators to conclude that there is not enough control of spending10; with schools budgets increasing. The DfES and authorities have put in place measures to improve the standards of financial management in schools. Schools are accountable to school governors, parents, nominees of the local authority and other partners, as well as to the local authority, which has the power to withdraw delegation of budgets. Local authorities are responsible to their council tax payers, who up to 2006/07 pay for a proportion of school funding. Local authorities agree delegated budgets to schools, in consultation with Schools Forums, local bodies consisting of heads and governors. Their Fair Funding scheme must be approved by the Government. Only the local authority is accountable through the ballot box.

7 Islington Council press release 6th February 2006 8 Office of the Deputy Prime Minister (2002) Council Tax Consultation – Guidelines for Local Authorities; chapter 6 9 Department for Education and Skills Five Year Strategy for Children and Learners chapter 2 10 Audit Commission (2004) Education Funding; the impact and effectiveness of measures to stabilise school funding, National Foundation for Educational Research/ LGA (2005) School Funding: Where Next (p33)

9

Children’s Services This includes provision of childcare, nursery facilities, children's social services, play and recreation facilities, social work support and day care services for children, young people and their families, services to support children in need, adoption services; placements in foster care and children's homes; respite residential care for children with disabilities. They cover the range between detailed social services interventions with children in need and more universal services and families and other, more intensive, services. In 2005/06 total revenue provision is estimated at around £7.7bn, of which £7.1bn was Formula Grant and £511m were specific grants, in some cases ringfenced. In 2006/07 authorities responsible for Children’s Services had an average grant increase of 2.7%, compared with 6.4% increase in Dedicated Schools Grant. Children’s Services are currently going through a period of reorganisation following some high profile cases where the different agencies failed children. The Government’s policy was set out in a 2003 policy paper, “Every Child Matters” and subsequently brought into law by the Children’s Act 2004. Under this, local authorities are required by 2008 to have in place arrangements for all children’s services, including education, to have common lead officer and member arrangements.11 This replaces arrangements where schools and children’s social care where dealt with separately in authorities. All local authorities which have educational responsibilities are also Children’s Services authorities. They are required to publish a plan which considers specifically their activities as regards: (a) physical and mental health and emotional well being; (b) protection from harm and neglect; (c) education, training and recreation;(d) the contribution made by them to society; and(e) social and economic well-being. These are the 5 'key outcomes' in the 2004 Children's Act. Authorities have local discretion in how they implement these aims, with local partners, through Children’s Trust arrangements which involve the local authority and other local partners, such as the health service. The challenge for local arrangements is the extent to which they can meet national goals and still be responsive to local circumstances.12 Local authorities, through a series of measures put in place by the government, following discussions with the Local Government Association, are encouraged to sign Local Public Service Agreements which include specific targets based on performing to higher than a national standard. For example, Kent’s agreement for the period 2006/07 includes targets related to support children with emotional and behavioural difficulties13. If they meet these targets, they will get extra grant in the form of a performance reward grant. More recently, a system of local area agreements has been developed, where local authorities agree with local partners the best way forward for key service areas, including children’s services. As part of this, authorities have been given relaxation from grant giving regimes. In some cases requests for exemption from quite detailed prescriptions have been refused; for example the staffing of Children’s Centres. The issue of charging for services is covered in authorities’ children’s services plans. For example the London Borough of Merton consulted on charging for some fostering or residential

11 Every Child Matters http://www.everychildmatters.gov.uk/publications/ 12 Improvement and Development Agency for Local Government (IDeA) – articles by Paul Roberts on IDeA website 13 Local Public Service Agreement; Kent and the Office of the Deputy Prime Minister – on ODPM website at http://www.odpm.gov.uk

10

care; parents may contribute towards this from child tax credits.14 As noted above, the government expect some of the provision for childcare out of school hours to be met from user charges. Pressures are discussed between the LGA and DfES in the spending review process and in regular meetings between civil servants, the LGA and advisers from authorities. Providing support for looked-after children has been increasing recently by about 10% per year as a result of demographic changes, with increasing number of children with severe and complex needs, a shift from residential to foster care. There are also significant costs from implementing the commitments on extended early years education and higher level skills in the child care workforce. 15 In practice the responsibility for managing pressures is that of the local authority, which has to meet a variety of targets and performance measures, for example the Performance Assessment Framework Ring-fenced grants account for a minority of finance. These are not automatically renewed from year to year. For instance, in 2004/05 and 2005/06 the Government paid a Safeguarding Children grant to assist in the implementation of new integrated Children’s Services arrangements. This grant was discontinued in 2006/07, leading to pressures at local level, particularly in implementing the new integrated children’s arrangements. With the new integrated children’s services arrangements, authorities work with a variety of local partners, including the health service and voluntary organisations. Other bodies, such as the health service, do not have the same degree of accountability to local people through the ballot box as do local authorities. Health Services Most public sector health care in Britain is delivered through the National Health Service, which is not a local government responsibility. This is financed by central government through general taxation and National Insurance contributions. In 2005/06 94% of the funding of the NHS (over £76bn in total) comes from this source. The remainder comes from charges and receipts, including land sales and proceeds from income generation schemes16 . Individual institutions within the NHS, such as hospital trusts, have increasingly acquired more financial autonomy, and a number have run up deficits, for which the government is refusing to provide additional resources beyond the £6bn increase already announced over the next two years17 Local authorities are closely involved with local NHS bodies in both adults and children’s social services. For example in children’s social services, children’s trust arrangements are being put in place involving both the local authority and the health service. These are funded by pooled budgets. Local authorities work closely with hospital trusts in planning for social services support for people discharged from hospital, thus freeing up NHS resources for other patients. They receive a specific ‘delayed discharge’ grant to help them in this Local authorities are concerned that any reductions in expenditure locally as trusts balance their budgets could have an effect on these joint arrangements, leading to increased demands on local authority resources.18 14 See http://www.merton.gov.uk/merton_charging_policy_2005_for_children_s_social_care_services_-_core_doc_.pdf 15 Local Government Association (2005) Beyond the Black Hole; a time of opportunity and challenge; pre-budget submission 16 Department of Health summary report 2005; section 3.9 – at http://www.dh.gov.uk/assetRoot/04/11/70/74/04117074.pdf 17 ‘Thousands of jobs go in NHS cash crisis’ Guardian 24.03.06 18 See LGA Social Services Finances Survey 2005/06; at http://www.lga.gov.uk/Documents/Publication/socialservicesfinance0506.pdf

11

Local Environmental Services This covers a range of local environmental services such as waste collection and disposal, environmental health, consumer protection, licensing, crime reduction, safety services, flood defence and coast protection. In recent years European directives had resulted in a number of legislative changes and national targets, leading to a change in the proportions of type of waste and marked a move towards more expensive, yet sustainable, forms of waste management19 In 2005/06 total expenditure is estimated at £4.4bn. Some services, for example waste, are subject to national service standards and to EU regulation. Others, such as the provision of consumer advice or local streetscape facilities, are discretionary. Environmental services have been included within local public service agreements. For example, Sheffield City Council includes a target on time taken to clear abandoned vehicles.20 Within its Local Area Agreement Suffolk County Council includes detailed targets on increasing the amount of waste recycled and composted and increasing green space. These have been negotiated with local partners, including district and parish councils, the local police and fire services, local training agencies and voluntary associations.21 Residents identify local environmental services are a priority, whilst still wanting to see council tax rises kept to a minimum. The Islington consultation referred to above identified “cleaner streets” as second priority to “Improving education standards”. However at the same time, residents supported reducing the levels of some services in order to keep council tax levels down. There is discretion to charge for some services, for example collection of commercial waste, and licenses. The 2003 Local Government Act gave authorities power to charge for a range of services, but this power is limited to cost recovery. Many recent debates on pressures between local authorities and the government have concerned environmental services issues. Among them are new licensing arrangements and the implementation of the EU Waste Electrical Emissions Directive (WEEE). A specific sum for the latter was put into the formula grant settlement for 2006/07. Evidence for the Lyons Review tends to suggest that people are more likely to hold local government responsible for local environmental services. Conclusion This brief survey of finance for local government services points to the following key conclusions

National rather than local priorities are imposed on local authorities in many ways; o Detailed legislative provisions and codes of practice; o A prescriptive method of target-setting and monitoring; o The involvement by government departments in micro-management,

The development of partnership arrangements, through local area agreements and bodies

such as children’s trusts is a positive development. But it should be noted that other partners at a local level may be from local agencies of national organisations, such as the

19 Ibid. p.11 20 Local Public Service Agreement; Sheffield and the Office of the Deputy Prime Minister – on ODPM website at http://www.odpm.gov.uk 21 See http://www.onesuffolk.co.uk/laa/overview

12

local health service, or probation service, without clear arrangements for local accountability.

Recently, increases in grant have come in the form of ring-fenced grants. This may produce

a distortion of local priorities and give an expectation that the initiative will continue to be funded once the programme has come to an end, leading to additional pressures.

There is a process for forecasting pressures, which feeds into Spending Reviews.

However, in recent years this has not prevented the need for campaigns for additional resources in order to head off unacceptable council tax rises or service reductions.

13

Local Government Finance in Germany I. The context: Sources of local income and debate over reform

A. Sources of Income – Quantitative Dimensions Local authorities in Germany have several sources of revenues. They can be systematized according to different criteria. Overall, Local Authorities had revenues of 141,35 Billion € in 2003 (unless otherwise noted, all numbers refer to the year 2003). This amounts to about 30 % of the combined revenues of all federal, state and local public budgets. Taxes (Steuern) are the largest source of income at 46,76 Billion €. The local trade tax (Gewerbesteuer; 18,5 Billion €) and the local authorities’ portion of the federal income tax (Einkommensteuer; 18,76 Billion €) are the most important taxes. The local land tax (Grundsteuer; 7,46 Billion €) and the local authorities’ portion of the federal value-added tax (Umsatzsteuer; 2,20 Billion €) are also key sources of funding. Both are dependable sources of revenue, but the Germany land tax is relatively low in international comparison. The remaining tax income, from local consumer and expenditure taxes, amounts to just over 1% of total tax revenues (0,54 Billion €). State Grants (Zuweisungen) are the second largest source of income, amounting to 45,95 Billion €. Grants specifically earmarked for local investment are 7,99 Billion €. Fees and contributions (Gebühren, Beiträge) account for 16,22 Billion €, whereas other sources of income (Sonstige Einnahmen) are 32,42 Billion €. Other scources of income are mainly rents and leases, licence fees, sales proceeds and borrowing. It must be noted that even today, fifteen years after German reunification, significant differences between East and West German states and municipalities exist, which should not be overlooked. In East Germany, State grants are still by far the most important source of income, whereas tax revenues only account for about 20 % of income, compared to almost 42 % in West German municipalities. These numbers are a reflection of the still existing large differences in economic strength between West Germany and East Germany.

B. Sources of Income – Degrees of Autonomy As described above, local authorities in Germany have various sources of income. However, they have only a limited degree of autonomy in drawing from these sources. The highest degree of autonomy is realized in the field of local consumer and expenditure taxes, which is also the least important source from a quantitative perspective. In most German states, local authorities are legally entitled to introduce and levy such taxes on the basis of local by-laws. However, these taxes may not be equivalent to taxes already existent according to federal or state law. Typical examples of these taxes are: entertainment tax (gambling machines, film showing, dance events, etc.), second residence tax, dog ownership tax. Although such taxes are not a major source of income, they also have the function of giving local authorities a financial instrument to control certain aspects of public order. Fees and contributions in theory also allow a relatively high degree of local autonomy. They are compensation for creating or extending particular public facilities or for administrative activities by a local authority. The legal basis for local fees and contributions are the relevant laws of the state to which a local authority belongs. Sometimes additional details are contained in local by-laws. An overriding legal principle for fees and contributions, however, is that they may not amount to more than 100 % of the actual cost incurred by the local authorities. This has in recent years – in spite of cash-strapped budgets -restrained local authorities from raising fees and contributions, because in many cases they are already at that threshold. Fees and

14

contributions which can not be expected to cover actual costs, on the other hand, are typically for services with a public purpose, such as libraries, children’s care, sports facilities and cultural institutions and events. For example, a typical library contributes less than 10% to its costs through user fees. Local land and trade taxes are regulated by national law, but set and levied by the local authorities on the basis of an assessment notice set by the fiscal administration. For these taxes the municipalities have the right to set the local levying rate (Hebesatz) under their own responsibility. It should be noted that municipalities keep all of the local land tax, but are required to transfer an apportionment of local trade tax to the federal and state governments. This apportionment was introduced in 1969, to compensate for the newly introduced local authorities’s share of the income tax. The trade tax levying rate typically increases with the size of the municipality. Small towns’ rates may be lower than 300, whereas the cities above 500.000 inhabitants average a levying rate of 458. Beginning in 2004, municipalities are now required by national law to have a levying rate of at least 200 to prevent a number of very small communities from becoming “trade taxe havens” with a levying rate of zero, thereby drawing away needed trade tax revenue from cities and towns. The rest of the local sources of income – with the exception of the various sources of “other income”, give the municipalities little or no autonomy. The local authorities’ share of the federal income tax revenue and value-added tax revenue is simply distributed to them on the basis of key criteria. In effect, these are taxes neither raised locally nor influenced locally. The key criteria for distributing these tax revenues among the individual municipalities are the subject of perennial political debate. Generally, the cities and towns feel that the distribution does not adequately take into account the need for larger municipalities to fulfill central functions within there area or region. Federal and state grants are also mostly immune to local decision-making. Municipalities receive different types of grants. The most important grants are those provided within each State according to the municipal financial equalisation system, which will be discussed below. But municipalities can also receive certain federal grants. Grants are either general (without purpose linkage), investment grants (in general, sometimes only for specific investments) or grants on demand (in cases of special financial hardships or bottlenecks in the administrative budget). Sometimes grants are conditioned by financial participation of local authorities, especially in the case of investment grants. A typical such example are waste water treatment projects.

C. Problems of Municipal Finances – Current Situation German municipalities have been in a very serious financial crisis now for several years. Simple indicators for the depth of this crisis are the annual deficits in local administrative budgets, the unprecedented amount of short-term debt and the decline of local investment activity. When making generalizations, one must of course keep in mind that an individual municipality’s situation may be different from the overall situation, which I am outlining. Local budgets have been running up large deficits over several years now. There has been a negative gap between overall local revenues and overall spending almost every year since the early 1990s. Under local budgeting law, municipalities are in principle required to balance their budget every year (see below in more detail). Short-term debt (Kassenkredite) is meant to only provide temporary liquidity.

15

In spite of these rules of local budgeting law, local authorities’ administrative budgets (excluding investment-related revenues and spendings) have been running annual and increasing deficits in every year since 1992. These deficits are reflect in the cumulated growth of short-term debt, which has skyrocketed to over 15 Billion € in 2003 and risen several billions since. Presently, it is unclear how and when it will be possible to balance annual administrative budgets again and begin paying back the short-term debts, which are not supposed to exist, except for short term liquidity, but not for paying the running cost of a local administration. A further indicator of the current financial crisis is the falling levels of local investment activity (see in more detail below). The reasons for this financial crisis are manifold. Of course, partially it reflects the weak development of the German economy since the early 1990s with a corresponding low growth in tax revenues on the one hand and rising costs of social security payments on the other hand. In this respect, the local level shares the fiscal problems of the state and federal level, as one would expect in a federal system. However, the degree to which local finances are part of a centralistic system of public finance has become higher over time. As explained above, municipal autonomy with regard to revenues is basically limited to the relatively unimportant local consumer and expenditure taxes and to the setting of levying rates for the local land and commerce taxes. There is another large reason why the local authorities have not been able to cope better with these difficult general economic conditions. To put it bluntly, there has been a dramatic process of redistribution of financial means between the federal, state and local level. The federal and state governments have claimed larger parts of local financial ressources while burdening municipalities with increased costly tasks, a phenomen which will be discussed more below. One indicator for this process is the local level’s share of tax revenues in Germany. Whereas that level stood at around 14 % in the 1980s, it had fallen to 11,7 % in 2003. Had it remained the same, the municipalities’ tax revenues would have been about 10 billion € higher in 2003.

D. Problems of Municipal Finances – Possible Reactions As mentioned above, the last decade has been marked by a serious budget crisis of the local level in Germany. Revenues have not matched expenditures in many municipalities. This problem is partially caused by structural problems of local financing, but partially also caused by the rules governing municipalities’ expenditures. Many local expenditures are predetermined by laws, most directly when municipalities are required to fulfill certain tasks. For example, a few years ago a federal law was passed which requires all municipalities to guarantee the availability of kindergarten capacities for every child. Other laws granting individual social welfare benefits to specific groups of people have also been recently passed. Moreover, as mentioned above, a large and growing number of legal standards for carrying out tasks have forced higher expenditures over which municipalities had no influence. Generally, the expenditures for social welfare entitlements have risen strongly in recent years. General low-income aid for adults and children now account for over a quarter of regular expenditures, whereas that percentage was as low as 15 % in the 1970s. The local reaction to the resulting budgetary squeeze has been to cut back on investment and on personnel. Personnel costs (Personalausgaben) have been practically stagnant since 1992. This means that local authorities had to continually lower the number of employees to cover the rising labour costs from annual raises and pension benefits. Investments, on the other hand, have fallen even in nominal terms. In Germany, the local level traditionally finances the largest part of overall public investment. Because of the local financial crisis, local investment in 2003 was about one third lower than in 1992, even in nominal terms.

16

In recent years the search for solutions regarding the permanent rise in forced expenditures has centered on the so-called connexity principle. As mentioned, many problems result from the fact that state laws and federal laws can simply force municipalities to carry out new tasks without providing corresponding financial means. One solution to this problem is the introduction of a so-called connexity principle in the federal and state constitution. Simply stated, such a constitutional rule requires to provide adequate financial means whenever task are newly created or made more expensive by new laws. Most German state constitutions now have such rules, and they seem to be having the deterring effect which was hoped for. However, the federal constitution has not been amended yet, so federal laws can still cause uncompensated financial burdens on local authorities. II. Service issues A. Health

Balance between national standards and local variation; The health care field in Germany consists of three separate fields: public health service, ambulant health care by resident doctors (niedergelassene Ärzte) and stationary health care in hospitals. The field of public health service is regulated by Federal laws (example: federal law on epidemic prevention; Bundesseuchengesetz) and State laws (State health care laws; Gesundheitsgesetze der Länder). The execution, especially of the State health care laws, is mostly a municipal task (local health authority, Gesundheitsamt). Because of Germany’s federal system, the public health service is regulated differently within the States. In some States, public health is a State responsibility, but in most States it is delegated to the rural districts and non-district (larger) cities. With respect to sovereign functions of public health service, municipalities are subject to legal supervision by the State. Ambulant health care by resident doctors is regulated by Federal law (Sozialgesetzbuch V). This task is carried out on the basis of a joint self-administration by the Associations of Panel Doctors (Kassenärztliche Vereinigungen) and the health insurance companies. They are jointly responsible for ensuring ambulant health care. The scope of the required services is defined in SGB V. There is no State supervision of this self-administration. Municipalities have almost no role in this field; they are only entitled to a hearing regarding the demand-planning by the self-administration bodies. Stationary health care in hospitals is also regulated by federal law (Krankenhausfinanzierungsgesetz, Bundespflegesatzverordnung, Krankenhausentgeltgesetz, Verordnung zum Fallpauschalensystem für Krankenhäuser, SGB V, etc.). The States and municipalities (rural district and non-district cities) are responsible for ensuring these services. Investment costs are provided by the State, whereas the running costs of hospitals are financed by the health insurance companies (Krankenkassen). The main tasks in this field have also been delegated during the past few years to self-administration institutions (Deutsche Krankenhausgesellschaft, Landeskrankenhausgesellschaften und Krankenkassen). However, in most cases disputes within the self-administration are to be settled by the State (Federal level or State level). Legal supervision of self-administration is a State task. Of 2166 hospitals in Germany (in 2004), 780 (36 %) were publicly governed, many of them by a municipality. These publicly governed hospitals had 280,770 beds, which equals 52.8 % of all hospital beds in Germany.

Balance what the public want and what they are willing to pay for

17

The public health services are tax-funded (State and local taxes). They only amount to a rather small share of the total costs of all health services in Germany. The ‘lion’s share’ of health-related costs are caused by ambulant health care and stationary health care. These costs are funded by social-security health insurance contributions of employers and employees (typically ½ each). Because the cost of health services in Germany has ballooned in recent years, there is a discussion how It can be financed without cutting back on services. 90 % of the population is insured through the mandatory (social-security) health insurance (Gesetzliche Krankenversicherung; GKV) just mentioned. The rest is either insured through private insurance companies or not insured (self-payin patients). The reform health insurance is a permanent issue. Recently, mandatory patients’ own contributions to the costs of ambulant health care have been introduced. In addition, the employers’ share of health-insurance contributions will be frozen in small steps at the current levels in order to improve the competitiveness of German firms. Because of an aging population and technical progress in medicine, further cost increases in the health services are expected. Because of high unemployment in Germany, social security-based health insurance is suffering from reduced contributions. The federal government has already announced a new reform of health service financing for this year. Currently, different reform models are being evaluated (especially mandatory social security for the whole populations; Bürgerversicherung; alternatively lump-sum contributions per person; Kopfpauschale). Since there is a grand coalition in federal government at the moment, a compromise between both reform models is most likely. This would entail a combination of tax funding and employers’ and employees’ contribution. Because health insurance contributions are already quite high in Germany, the public willingness to pay for health services can probably not be extended further. Therefore, all reform initiatives aim to reduce the average contribution level significantly, which has, however, never successfully been done through previous reforms. Such reforms were mainly focused on cost-cutting measures in recent years. Currently, the aim is to enhance efficiency by introducing more elements of competion, both in ambulant and stationary health care.

Managing pressures effectively Them main spending pressures are caused by an aging population and the continuous technical progress in medicine, which makes it possible, to give just one example, to still operate patients at a very high age. In the context of a globalised economy, it will be necessary to adjust employers’ social security burdens to levels, which are comparable to those in other countries.

Accountability In the field of public health service, the States or municipalities are accountable for service quality, depending on who is responsible for a specific service. In the field of ambulant health care, service quality is monitored and regulated by the self-administration of the Associations of Panel Doctors (Kassenärztliche Vereinigungen) and the health insurance companies. In the hospital sector, accountability has been recently changed. Now federal committees are responsible, which are a form self-administration by the hospitals and health insurance companies. B. Schools

Balance between national standards and local variation;

18

The division of responsibility for schools is in Germany traditionally divided between each State (Land) and its municipalities. Municipalities provide the necessary facilities (in particular school buildings) and also conduct the local organisation and administration of schools (so-called ‘outer’ school affairs). The State is responsible for all educational issues (including curricula, degrees, school supervision) and provides the necessary staff. The ‘governing body’ (Schulträger) for around 94 % of all public schools in Germany are municipalities. The financing of schools is in accordance with this division of responsibility: The State almost fully provides the teacher salaries, whereas municipalities are responsible for facility investments and the running costs of schools. In most German States, this includes the cost of learning aids (books, etc.) and pupil transport. Through each State’s financial equalisation structure, municipalities receive earmarked funds for school purposes (such as building facilities). The traditional division of responsibility between the State and the municipalities is nowadays in many cases not in accordance with reality and the current challenges in the school sector. For many cities, being the governing body (Schulträger) in reality entails much more than just providing the facilities for schools. On the basis of an expanded interpretation of what it means the be the governing body for local schools, many municipalities voluntarily provide additional staff, for example to integrate handicapped children, for supervision and care outside of classroom hours or for social work within schools. In addition, they initiate the cooperation between schools and social services, promote the cooperation between school sports and club sports or assist in the vocational preparation especially of disadvantaged pupils. The governing bodies thus contribute in many ways to the pedagogical advancement within schools, much beyond their duty to provide the facility basis for schools. The independence of schools has been significantly strengthened in the past few years. This not only concerns pedagogical issues, but also responsibility for organisational issues and application of funds. Since the mid-1990s, many cities have introduced budgeting of materials costs. In several States, efforts are being made to extend a school’s budget responsibilities to personnel costs.

Balance what the public want and what they are willing to pay for; The general obligation to attend school requires 12 years of school in most States, in a few the requirement is 13 years. The obligation ends with the high school diploma, which allows entry into colleges and universities (Abitur), alternatively the conclusion of vocational training (Berufsausbildung). Attending school is generally free in Germany. The freedom from school fees is explicitly guranteed in the State constitutions (e.g. Art. 9 of the State Constitution of Nordrhein-Westfalen). In most States, parents are required to pay a share of the cost of learning aids and pupil transportation. Special rules for needy parts of the population exist, which exempt them from paying any such charges. A recent debate concerning the introduction of a “school book fee” (Büchergeld) in Bavaria shows that parental contributions to the material costs of schooling are controversial. Many parents are of the opinion that all school-related costs should be born by the public authorities (that is: the State or the municipality). On the other hand, there is a growing acceptance to pay for additional school services related to the introduction of all-day schooling (specific care and tutoring). For example, in Nordrhein-Westfalen, a parental contribution of up to 150 Euro per month and pupil could be required.

Managing pressures effectively In line with the described shared financing of schools, there are financial pressures on different levels:

19

Since all State budgets are in deficit, the States are attempting to reduce personnel costs. All States are either increasing working hours, reducing supplementary wages or reducing pension entitlements. On the other hand, some States are currently increasing the number of teachers for reasons of educational policy. At the local level, the financial crisis is also leading to cost reduction measures. This pertain especially to facility investments (school buildings, equipment), but also entails a reduction in supplementary school services such as psychological care or in the field of social pedagogy. At the school level, it means reduced budgets. Consequently, schools have less room for manoeuvre, which in many cases they try compensate through generating supplementary funds (through sponsoring, for example).

Accountability The public regards the system of school financing as intransparent. In many cases, the system of divided State and municipal responsibility is not understood. Municipalities often receive complaints about issues which they are not responsible for (such as cancelled classes). A school has responsibilities towards the State, municipality and parents. The States have in recent years, based on the results of the international PISA research studies, developed unified quality standards (such as centralized final exams or standardized tests to measure learning progress) and procedures of securing quality levels (evaluations, school inspections). Towards the municipality, a school is accountable for the use of the school budgets and with respect to a demand-oriented provision of school services. Legally, each head of school is a trustee of municipal funds. Within each school, through a system of participation accountability towards parents and pupils is warranted. C. Children’s Services In Germany, municipalities as the governing bodies for Child and Youth Services are required by law to offer (and pay for) such services. This obligation includes Kindergarten care as well as municipal youth work offerings (offene Jugendangebote) and socio-educational provision (Erziehungshilfen) for children with problems. Overall, around 20 billion Euros are spent in Germany each year,. About half of that sum is spent for care in day care institutions for children, the rest for the other services. The German States partially support municipal funding by way of earmarked grants. In many cases, Child and Youth Services institutions are governed by churches and specific charity institutions (Wohlfahrtsverbände). Such institutions are mainly funded by municipalities; they only support public funding by a small own share raised through church taxes, member fees or donations. Additional background information (in English) about Child and Youth Services in Germany can be found on the homepage of the Federal Ministry of Youth: http://kinder-jugendhilfe.org/e_kjhg/ Child and Youth Services in Germany are currently mainly discussed against the background of demographic developments and the results of the international PISA and IGLU research studies, in which German pupils did not have satisfactory results. The statutory mandate in the elementary field (0 to 6 year old children) is in the German Child and Youth Services Act (German abbreviation KJGH) defined by the terms upbringing (Erziehung), education (Bildung) and care (Betreuung). As the governing bodies (öffentliche Träger) of Child and Youth Services in Germany, the rural districts (Landkreise) and the larger, non-district cities (kreisfreie Städte) are responsible for the day-care facilities for children. There is no obligation in Germany for children to attend any such facilities before school age. There is a discussion going on concerning the improved availability of day-care facilities for children. Through binding demand criteria in the KJHG the municipal obligation to provide such services has been increased. For defined individual constellations, beginning at the latest in

20

2010 municipalities must make access to a day-care facility possible for children even under the age of 3. The political goal is to have places in such facilities in all German States for 20 % of all children under the age of 3. Children from the age of 3 years on already have a legal entitlement for a place in a Kindergarten, which is, however, only half-day care. In the States comprising former West Germany, places in day-care facilities, which are open the whole day, are available for about 20 to 25 % of all children between the ages of 3 and 6. In the States of former East Germany, there are enough such spaces available to fulfil the demand. At the federal level, there is also a discussion about the qualitative improvement of children’s day care. Discussed means for such an improvement include a better child-personnel-ratio in the facilities and a required college (Fachhochschule) degree for the employees of such facilities. Against the background of the PISA and other comparative studies, the educational function of the Kindergarten are emphasized and the importance of early advancement of children’s skills are emphasized, not limited to language capabilities. In Germany, school enrolment begins rather late at an average age of 6.7 years, so the advancement of skills within Kindergarten is especially important. In addition to the improved available of day-care facilities, two other changes of the current system are currently being discussed: The first proposal is to eliminate any fees for attending Kindergarten, at least during the last year before school enrolment. Some States have already done so, others are still deliberating. At the moment, about 20 % of the costs of Kindergarten are covered by parental fees. Since these charges vary according to parental incomes, low-income families only pay for a small share of the cost, whereas high-income families pay for most of the cost. The existence of a fee for attending Kindergarten is nonetheless viewed by some as a restraining factor, which limits the Kindergarten attendance especially of children from low-income families. The second proposal is to reduce the age of school enrolment by one year, creating an obligation for children to attend school from the age of 5 on. This could also help the advancement of education at an early age.

Managing pressures effectively The existing schemes of mixed funding of day care facilities (municipal funds, third-sector institutions acting as governing bodies, especially the churches, parental fees, earmarked State grants) have created a situation, in which the long-term financing of services is influenced by various different parameters. The discussion concerning the elimination of parental fees is coinciding with the reduction of State grants in some States and also with the withdrawal of third-sector institutions from co-financing the facilities. Churches in particular experience difficulties in keeping up their current level of involvement, given their own losses in church membership and corresponding reductions in income. At the same time, the expectations of employers, politicians and the general public are increasing with regard to a demand-oriented supply of day-care facilities, which operate all day. The municipalities will under these circumstances hardly be able to finance the necessary facility investments and running costs of operating facilities of high qualitative standards. D. Local Waste Services The legal framework for waste collection services in German cities consists of EU, Federal and State Regulations. The Refinancing of these services by the cities is governed by State law. On the basis of a city council decision, local by-laws are enacted for waste services and waste service fees. The setting of waste service fees by the municipalities can be subjected to legal review by the administrative courts. Each land owner receiving a fee assessment is entitled to challenge it in court.

21

The cities are legally obligated to ensure waste collection services. However, they can conduct the task themselves, in cooperation with other municipalities or through private firms. To fulfill their tasks, the cities as the legally designated disposal agents (öffentlich-rechtliche Entsorgungsträger; ÖRE) have various competencies for planning, organizing and enacting of local bye-laws. This includes a certain scope for variations to adequately take into account specific local circumstances. The technical and organizational standards of waste collection services are - partially proscribed by EU, the Federal Government, the State, - partially developed by technical associations or groups, - partially enacted by the cities based on their competencies in the field of waste collection planning and management. The fees themselves for waste collection are governed by the principle of cost-recovery. Only costs necessary for the fulfillment of such services may be included in the calculation of fees. Although the services of different local disposal agents (ÖRE) vary and are refinanced though different fee structures, there is an increasing tendency to conduct fee and cost comparisons on the basis of standardized services and types of households.

22