Lacey Buyers Guide

18

Lacey’s Personalized Marketing Strategy Buyer’s Guide

-

Upload

abby-mcclain -

Category

Documents

-

view

76 -

download

0

Transcript of Lacey Buyers Guide

Lacey’s Personalized Marketing Strategy

Buyer’s Guide

B u y e r ’s Gu id e

Get Serious about Buying

Hire a Realtor®

Get Your Finances In Order

Get Pre-Qualified for a loan

Find your Dream Home & Make an Offer

Welcome to Your New Home!

Welcome

home!

4 REASONS TO BUY YOUR HOME NOW!

Here are four great reasons to consider buying a home today instead of waiting.

1. Prices Will Continue to Rise The Home Price Expectation Survey polls a distinguished panel of over 100 economists, investment

strategists, and housing market analysts. Their most recent report projects appreciation in home values

over the next five years to be between 10.5% (most pessimistic) and 25.5% (most optimistic).

The bottom in home prices has come and gone. Home values will continue to appreciate for years.

Waiting no longer makes sense.

2. Mortgage Interest Rates Are Projected to Increase Freddie Mac’s Primary Mortgage Market Survey shows that interest rates for a 30-year mortgage

have started to inch up, most experts predict that they will begin to rise even more over the next

12 months. The Mortgage Bankers Association, Fannie Mae, Freddie Mac & the National Association of

Realtors are in unison projecting that rates will be up almost a full percentage point by this time next

year.

An increase in rates will impact YOUR monthly mortgage payment. Your housing expense will be

more a year from now if a mortgage is necessary to purchase your next home.

3. Either Way You are Paying a Mortgage As a paper from the Joint Center for Housing Studies at Harvard University explains:

“Households must consume housing whether they own or rent. Not even accounting for more favorable tax

treatment of owning, homeowners pay debt service to pay down their own principal while households that

rent pay down the principal of a landlord plus a rate of return. That’s yet another reason owning often

does—as Americans intuit—end up making more financial sense than renting.”

4. It’s Time to Move On with Your Life The ‘cost’ of a home is determined by two major components: the price of the home and the current

mortgage rate. It appears that both are on the rise.

But, what if they weren’t? Would you wait?

Look at the actual reason you are buying and decide whether it is worth waiting. Whether you want to

have a great place for your children to grow up, you want your family to be safer or you just want to

have control over renovations, maybe it is time to buy.

If the right thing for you and your family is to purchase a home this year, buying sooner rather

than later could lead to substantial savings.

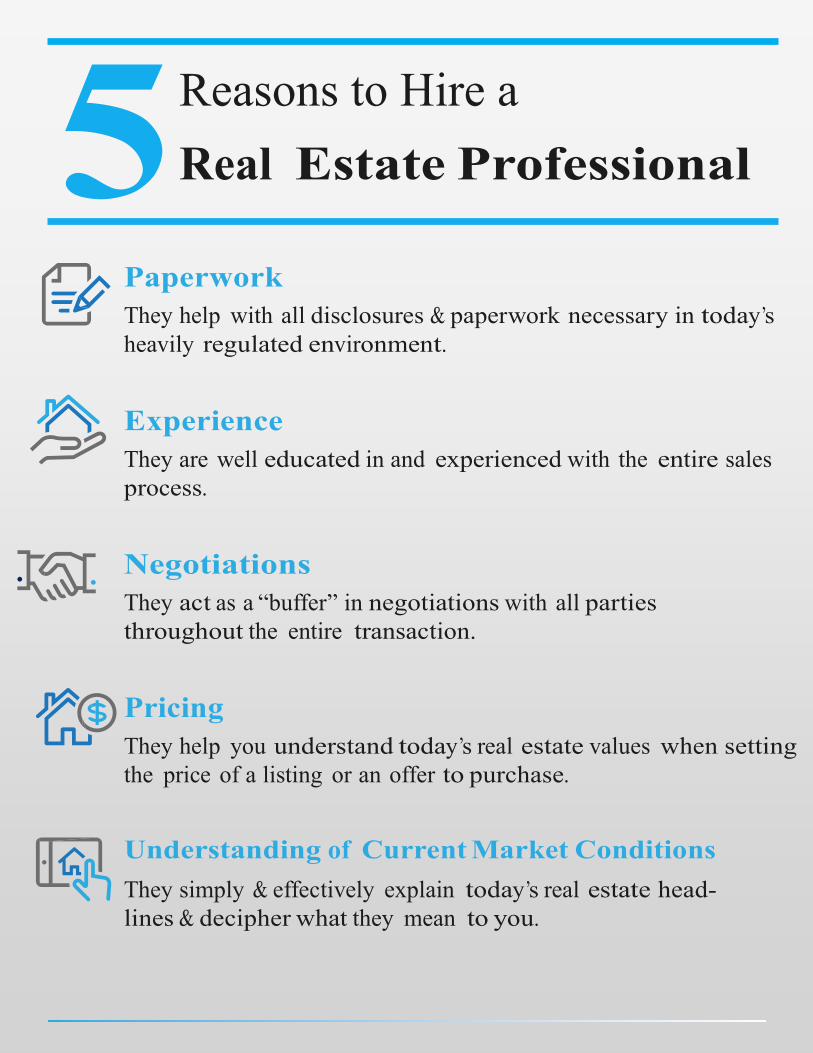

Reasons to Hire a

Real Estate Professional

Paperwork

They help with all disclosures & paperwork necessary in today’s

heavily regulated environment.

Experience

They are well educated in and experienced with the entire sales

process.

Negotiations

They act as a “buffer” in negotiations with all parties

throughout the entire transaction.

Pricing

They help you understand today’s real estate values when setting

the price of a listing or an offer to purchase.

Understanding of Current Market Conditions

They simply & effectively explain today’s real estate head-

lines & decipher what they mean to you.

5

Wh y u se a S t r a t t o n R e a l Es t a t e a ge n t

w h e n b u y in g a h o m e ?

Our agents: Are full-time professionals Are licensed by the Wyoming Real Estate Commission Are members of the National Association of Realtors & must adhere to NAR’s code of ethics & conduct Will listen closely to your wants & needs Won’t pressure you into making a decision to buy Will explain each step of the home buying process so that you always understand what’s happening. Our agents will: Prescreen homes on the market & select those that match your criteria. Educate you about the home buying process and the local real estate market. Make appointments with the sellers & show you the homes you have selected. Provide you with enough information so you can make an informed decision about making an offer Work with you to create an offer & present the offer to the seller’s agent. Negotiate the deal-this is one of the most important parts of an agent’s job! Schedule & attend all inspections that you have selected for the property Keep in contact with all concerned parties to make sure things are running smoothly Perform a walk-through of the property with you prior to closing to make sure that the condition of the home hasn’t changed, that everything the seller agreed to leave is actually there & in good shape. Attend the closing with you

Ab o u t La c e y Wilso n ,

L ic e n se d R e a l t o r

Bachelors in Business

10 years in the Human Resource field

Human Resource skills enhanced and supported my real estate career

Efficiently handles difficult situations

Enjoys helping others meet their goals

Will offer options on the best approach

Real estate has always been a passion of mine.

High interest in architecture

Degree in architectural drafting and design

Continuous real estate market research

Member of National Association of Realtors

Member of Casper Board of Realtors

Member of Wyoming Association of Realtors

My P r o m ise t o Yo u

Professionalism

Constant Communication

Educate you on each process

Assistance through each step

Complete Transaction

Dedicated to YOUR success in buying or selling

Your personal advocate in the buying or selling process

It is my goal, desire, and passion to help others through the entire real estate

transaction process, working to ensure the process runs smoothly and to

personally ensure that my clients feel supported each step of the way.

My passion is people and finding that ideal home that each client has

envisioned.

Ensure that each client has their questions answered and is supported

throughout the process.

Ge t Yo u r F in a n c e s

in Or d e r

So you want to buy a house, now what?

Get your finances in order, how?

Check your credit score!

AnnualCreditReport.com offers you a free credit report annually. Check for

any errors on your report and dispute them!

Do not make any large purchases.

Do not apply for loans or credit cards during the buying process

Start saving

Home purchases require money for loan fees, closing costs, a down payment,

and home inspections and repairs.

Tips to save:

Limit vacations and trips or take shorter trips to a nearby area

Start using coupons and limit name brand purchases

Limit eating out

Stash change and loose bills

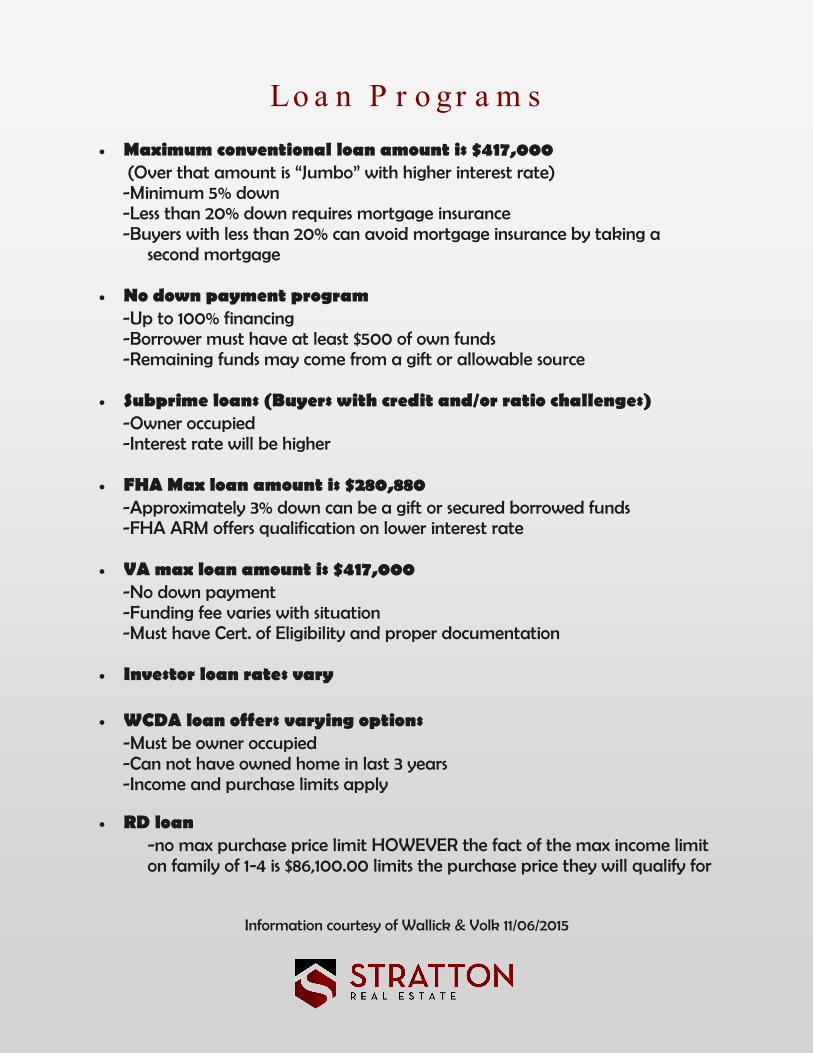

Lo a n P r o gr a m s

Maximum conventional loan amount is $417,000 (Over that amount is “Jumbo” with higher interest rate) -Minimum 5% down -Less than 20% down requires mortgage insurance -Buyers with less than 20% can avoid mortgage insurance by taking a second mortgage No down payment program -Up to 100% financing -Borrower must have at least $500 of own funds -Remaining funds may come from a gift or allowable source Subprime loans (Buyers with credit and/or ratio challenges) -Owner occupied -Interest rate will be higher FHA Max loan amount is $280,880 -Approximately 3% down can be a gift or secured borrowed funds -FHA ARM offers qualification on lower interest rate VA max loan amount is $417,000 -No down payment -Funding fee varies with situation -Must have Cert. of Eligibility and proper documentation Investor loan rates vary WCDA loan offers varying options -Must be owner occupied -Can not have owned home in last 3 years -Income and purchase limits apply RD loan -no max purchase price limit HOWEVER the fact of the max income limit on family of 1-4 is $86,100.00 limits the purchase price they will qualify for

Information courtesy of Wallick & Volk 11/06/2015

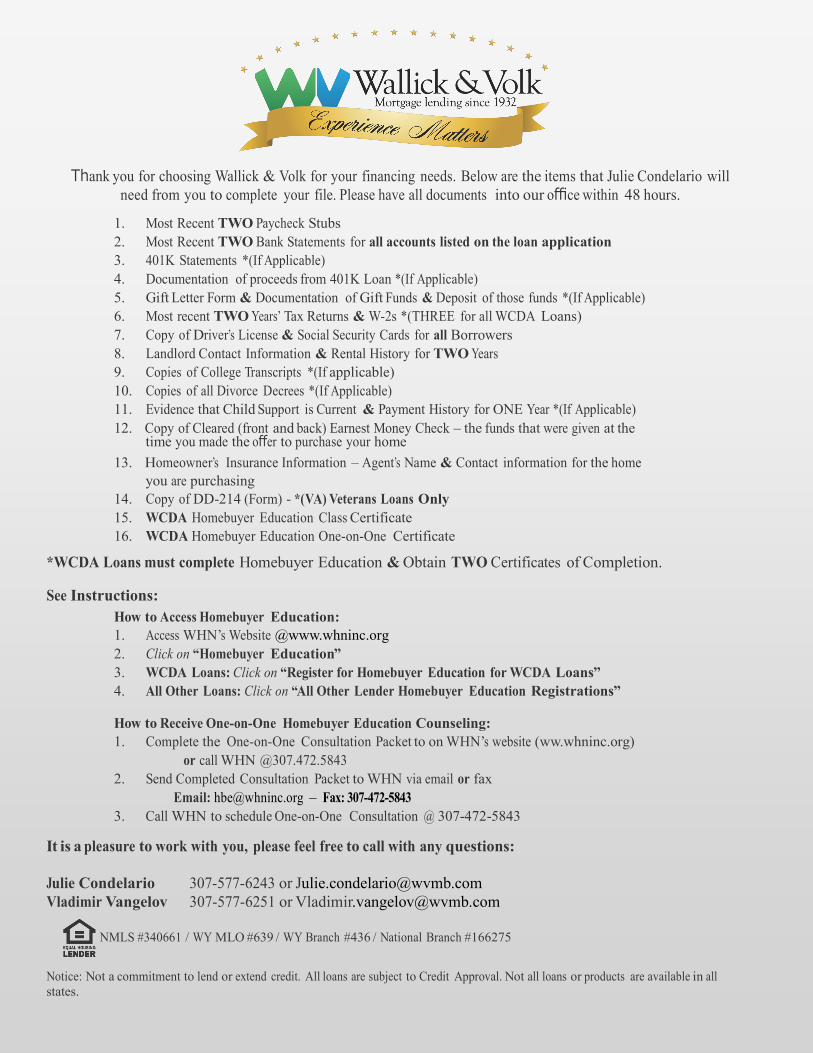

Thank you for choosing Wallick & Volk for your financing needs. Below are the items that Julie Condelario will

need from you to complete your file. Please have all documents into our office within 48 hours.

1. Most Recent TWO Paycheck Stubs

2. Most Recent TWO Bank Statements for all accounts listed on the loan application

3. 401K Statements *(If Applicable)

4. Documentation of proceeds from 401K Loan *(If Applicable)

5. Gift Letter Form & Documentation of Gift Funds & Deposit of those funds *(If Applicable)

6. Most recent TWO Years’ Tax Returns & W-2s *(THREE for all WCDA Loans)

7. Copy of Driver’s License & Social Security Cards for all Borrowers

8. Landlord Contact Information & Rental History for TWO Years

9. Copies of College Transcripts *(If applicable)

10. Copies of all Divorce Decrees *(If Applicable)

11. Evidence that Child Support is Current & Payment History for ONE Year *(If Applicable)

12. Copy of Cleared (front and back) Earnest Money Check – the funds that were given at the time you made the offer to purchase your home

13. Homeowner’s Insurance Information – Agent’s Name & Contact information for the home

you are purchasing

14. Copy of DD-214 (Form) - *(VA) Veterans Loans Only

15. WCDA Homebuyer Education Class Certificate

16. WCDA Homebuyer Education One-on-One Certificate

*WCDA Loans must complete Homebuyer Education & Obtain TWO Certificates of Completion.

See Instructions:

How to Access Homebuyer Education:

1. Access WHN’s Website @www.whninc.org

2. Click on “Homebuyer Education”

3. WCDA Loans: Click on “Register for Homebuyer Education for WCDA Loans”

4. All Other Loans: Click on “All Other Lender Homebuyer Education Registrations”

How to Receive One-on-One Homebuyer Education Counseling:

1. Complete the One-on-One Consultation Packet to on WHN’s website (ww.whninc.org)

or call WHN @307.472.5843

2. Send Completed Consultation Packet to WHN via email or fax

Email: [email protected] – Fax: 307-472-5843

3. Call WHN to schedule One-on-One Consultation @ 307-472-5843

It is a pleasure to work with you, please feel free to call with any questions:

Julie Condelario 307-577-6243 or [email protected]

Vladimir Vangelov 307-577-6251 or [email protected]

NMLS #340661 / WY MLO #639 / WY Branch #436 / National Branch #166275

Notice: Not a commitment to lend or extend credit. All loans are subject to Credit Approval. Not all loans or products are available in all

states.

What You Need to Know About The

MORTGAGE PROCESS

2

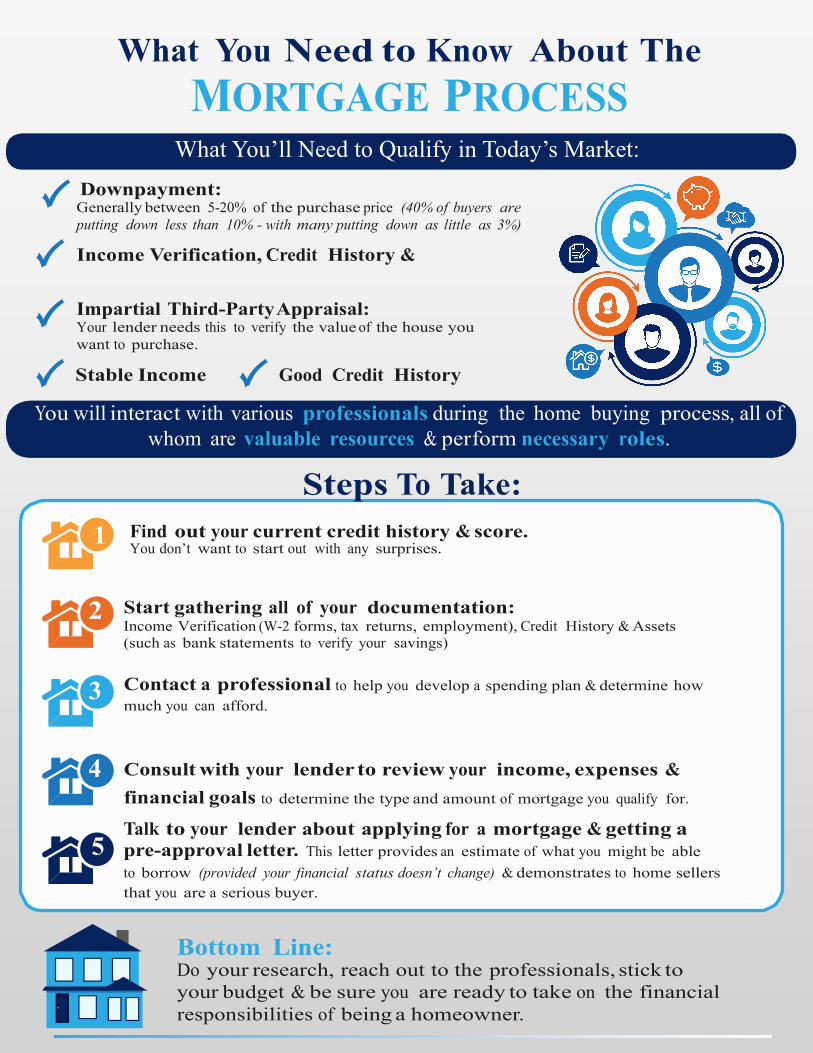

What You’ll Need to Qualify in Today’s Market:

Downpayment: Generally between 5-20% of the purchase price (40% of buyers are

putting down less than 10% - with many putting down as little as 3%)

Income Verification, Credit History &

Impartial Third-Party Appraisal: Your lender needs this to verify the value of the house you

want to purchase.

Stable Income Good Credit History

You will interact with various professionals during the home buying process, all of

whom are valuable resources & perform necessary roles.

Steps To Take:

1

3

4

5

Find out your current credit history & score. You don’t want to start out with any surprises.

Start gathering all of your documentation: Income Verification (W-2 forms, tax returns, employment), Credit History & Assets

(such as bank statements to verify your savings)

Contact a professional to help you develop a spending plan & determine how

much you can afford.

Consult with your lender to review your income, expenses &

financial goals to determine the type and amount of mortgage you qualify for.

Talk to your lender about applying for a mortgage & getting a

pre-approval letter. This letter provides an estimate of what you might be able

to borrow (provided your financial status doesn’t change) & demonstrates to home sellers

that you are a serious buyer.

Bottom Line: Do your research, reach out to the professionals, stick to

your budget & be sure you are ready to take on the financial

responsibilities of being a homeowner.

WHAT DO YOU REALLY NEED TO QUALIFY FOR A MORTGAGE?

A recent survey by Ipsos found that the American public is still somewhat confused about what

is actually necessary to qualify for a home mortgage loan in today’s housing market. The study

pointed out two major misconceptions that we want to address today.

1. Down Payment The survey revealed that consumers

overestimate the down payment funds

needed to qualify for a home loan.

According to the report, 36% think a

20% down payment is always required.

In actuality, there are many loans written with a

down payment of 5% or less.

On the right are the results of a Digital Risk survey

done on Millennials who recently purchased a home.

2. FICO Scores The Ipsos survey also reported that two-

thirds of the respondents believe they

need a very good credit score to buy a home, with

45 percent thinking a “good

credit score” is over 780. In actuality,

the average FICO scores of approved conven-

tional and FHA mortgages are much lower.

On the right are the numbers from a recent

Ellie Mae report.

Bottom Line If you are a prospective purchaser who is ‘ready’ and ‘willing’ to buy but not sure if you are also ‘able’,

sit down with someone who can help you understand your true options.

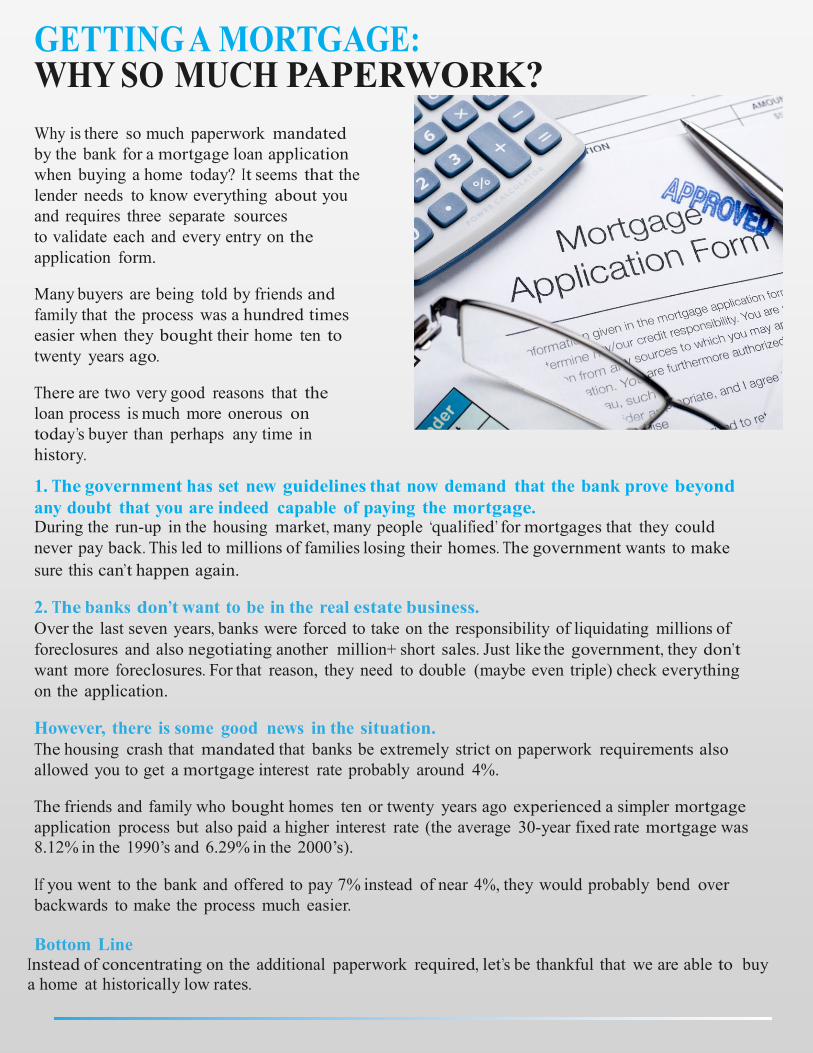

GETTING A MORTGAGE: WHY SO MUCH PAPERWORK?

Why is there so much paperwork mandated

by the bank for a mortgage loan application

when buying a home today? It seems that the

lender needs to know everything about you

and requires three separate sources

to validate each and every entry on the

application form.

Many buyers are being told by friends and

family that the process was a hundred times

easier when they bought their home ten to

twenty years ago.

There are two very good reasons that the

loan process is much more onerous on

today’s buyer than perhaps any time in

history.

1. The government has set new guidelines that now demand that the bank prove beyond

any doubt that you are indeed capable of paying the mortgage. During the run-up in the housing market, many people ‘qualified’ for mortgages that they could

never pay back. This led to millions of families losing their homes. The government wants to make

sure this can’t happen again.

2. The banks don’t want to be in the real estate business.

Over the last seven years, banks were forced to take on the responsibility of liquidating millions of

foreclosures and also negotiating another million+ short sales. Just like the government, they don’t

want more foreclosures. For that reason, they need to double (maybe even triple) check everything

on the application.

However, there is some good news in the situation.

The housing crash that mandated that banks be extremely strict on paperwork requirements also

allowed you to get a mortgage interest rate probably around 4%.

The friends and family who bought homes ten or twenty years ago experienced a simpler mortgage

application process but also paid a higher interest rate (the average 30-year fixed rate mortgage was

8.12% in the 1990’s and 6.29% in the 2000’s).

If you went to the bank and offered to pay 7% instead of near 4%, they would probably bend over

backwards to make the process much easier.

Bottom Line Instead of concentrating on the additional paperwork required, let’s be thankful that we are able to buy

a home at historically low rates.

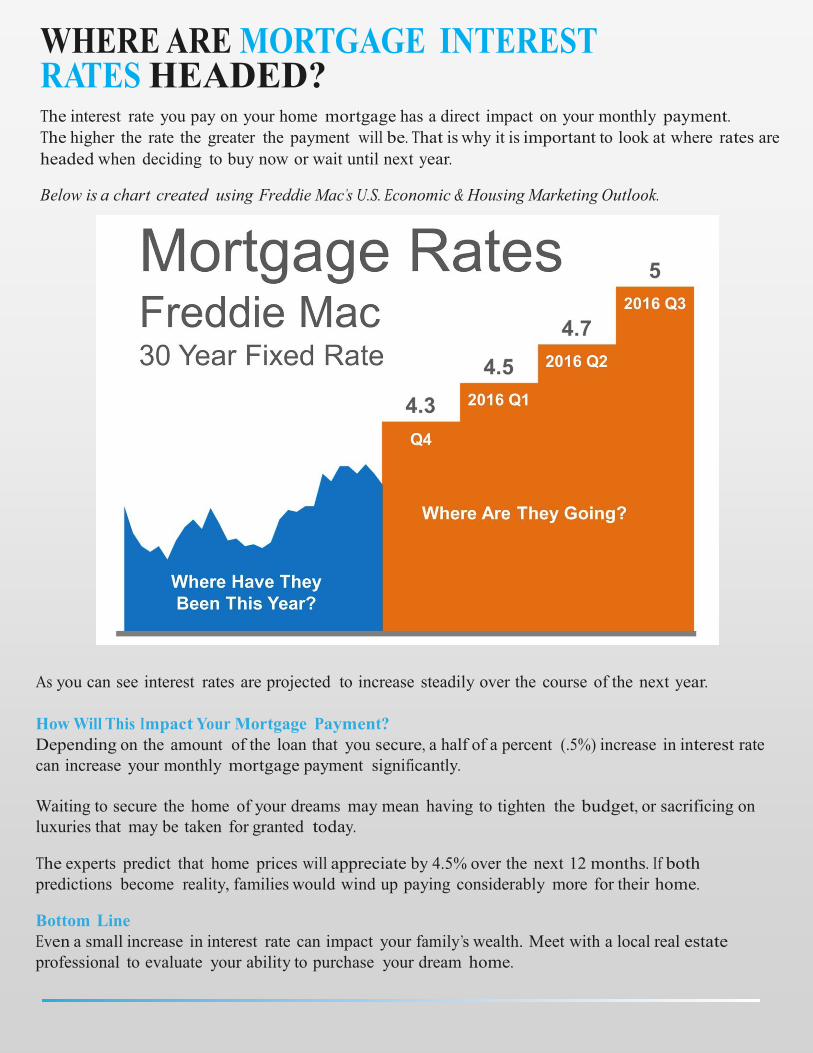

WHERE ARE MORTGAGE INTEREST RATES HEADED?

The interest rate you pay on your home mortgage has a direct impact on your monthly payment.

The higher the rate the greater the payment will be. That is why it is important to look at where rates are

headed when deciding to buy now or wait until next year.

Below is a chart created using Freddie Mac’s U.S. Economic & Housing Marketing Outlook.

As you can see interest rates are projected to increase steadily over the course of the next year.

How Will This Impact Your Mortgage Payment?

Depending on the amount of the loan that you secure, a half of a percent (.5%) increase in interest rate

can increase your monthly mortgage payment significantly.

Waiting to secure the home of your dreams may mean having to tighten the budget, or sacrificing on

luxuries that may be taken for granted today.

The experts predict that home prices will appreciate by 4.5% over the next 12 months. If both

predictions become reality, families would wind up paying considerably more for their home.

Bottom Line

Even a small increase in interest rate can impact your family’s wealth. Meet with a local real estate

professional to evaluate your ability to purchase your dream home.

H o w m u c h h o u se c a n y o u a ffo r d ?

Prequalification The first step in the home buying process is getting prequalified. Your lender will let you know how much you can afford to pay during the prequalification process. You tell your lender how much you earn & what debts you have. The lender uses a formula & comes up with an actual mortgage amount that you can afford. A prequalification carries no commitment from the lender, but you have an idea of what you can afford.

So , y o u ’v e fo u n d y o u r d r e a m h o m e !

Wh a t n e x t ?

How do I make an offer? The basic elements of a Contract to Purchase include: the assurance of good title, the deed, conveyance (that is, transfer to your ownership) of personal property (appliances, etc.), notification of the method of paying for the property, the selling price & where & when the closing will take place. The following must also be addressed: Your offer should contain extremely important escape clauses known as contingencies, which you build into the contract to protect yourself. A contingency is some specific future event that must be satisfied in order for the sale to go through. It gives you the right to pull out of the deal if that event fails to happen. The following contingencies appear in nearly every offer Financing– You can pull out of the deal if the loan specified in your contract isn’t approved Property inspections-You can pull out of the deal if you don’t approve

the inspection reports or can’t reach an agreement with the sellers about how to handle any necessary repairs.

Earnest money must be included with your offer. The buyers put up earnest money to show they are serious about buying the property. The amount varies. A prequalification letter from your bank should be included with your offer.

Yo u h a v e a s ign e d c o n t r a c t ,

w h a t n o w ?

Your Stratton agent will forward copies of the contract to the lender & the title company. The title company will research the title to determine who legally owns the property that you want to buy & find out whether there are any unpaid tax liens or judgments recorded against it. They will then issue a title insurance pol-icy that assures homeowners & mortgage lenders that the property has a valid title. Title insurance also indemnifies homeowners against title claims after the close of escrow. Inspections The buyers select the inspections they want. A full house inspection includes ra-don & termite inspections. If the buyers choose, instead of a full house inspection, they can select individual inspections such as plumbing, electrical, roof, furnace or termite inspections. Your Stratton Real Estate agent can supply you with names of licensed inspectors. Your agent will schedule & attend all inspections. You may also attend the inspections along with your agent. If repairs are needed, repair requests must now be negotiated with the sellers.

I t ’s c lo s in g d a y !

The closing agent is a representative from the title company & will oversee the closing. The closing generally consists of: Reviewing & signing the loan documents provided by the lender. Exchange of documents among the buyer, seller & the title company. Disbursement of funds. After the closing you gain possession of your new home!

Congratulations!