Labor Market & Salary Report 2019 | 2020 · 2019-11-05 · 3 In partnership with Labor Market 2019...

56

In partnership with Labor Market & Salary Report 2019 | 2020 Brief Edition

Transcript of Labor Market & Salary Report 2019 | 2020 · 2019-11-05 · 3 In partnership with Labor Market 2019...

In partnership with

Labor Market & Salary Report

2019 | 2020Brief Edition

GERMAN CHAMBER OF COMMERCE IN CHINA

www.china.ahk.de/chamber

2019 | 2020

Labor Market & Salary Report

© 2019 by the German Chamber of Commerce in China. Thank you for not reproducing this report either in part or in full

without prior consent of the German Chamber of Commerce in China.

While every effort has been made to provide accurate information in the preparation of this report no responsibility or

liability is accepted for errors or omissions of fact or for any opinions expressed herein. Opinions, projections and estimates

are subject to change without notice. This report is for information purposes only. In no event shall the German Chamber of

Commerce in China, Direct HR Group or their employees be liable for any losses or other consequential, incidental,

exemplary or special damages relating in whole or part to the use of information contained in this report.

Cover picture by Kimi Lee on Unsplash

Brief Edition

3

In partnership with

Labor Market

2019 | 2020& Salary Report

BR

IEF

▪ After last year’s mild uptick, the expected wage increase

returns to a descending path that has been a trademark

feature since measurements started in 2012. German

companies anticipate a 5.53 percent increase in 2020.

▪ At the regional level, the slowdown is more pronounced in

East China. In North China, Beijing and Tianjin will put

forward increases above their 2019 expectation.

Shenzhen and Guangzhou in South China present the

highest expected increases.

▪ The automotive industry projects an increase of 5.26

percent in 2020, 1.37 percentage points (p.p.) below the

2019 forecast. In contrast, machinery / industrial

equipment presents a 5.84 percent expected wage

increase in 2020, 0.05 p.p. below that of 2019.

▪ The 5.87 percent effective increase reported in 2019

does not fall far from the 5.99 percent expected increase

reported last year.

▪ Beijing, Tianjin, Shenzhen, and Guangzhou report effective

wage increases in 2019 above their respective expected

increases as measured last year. Shanghai delivers an

effective 5.65 percent increase, 0.41 p.p. lower than

initially anticipated.

▪ The median total cost per employee for the 483

companies contributing to the survey this edition is RMB

15,000 / month. That is 2.2 times higher than the latest

official national average compensation in China, reported

by the NBS.

Productivity and HR Developments

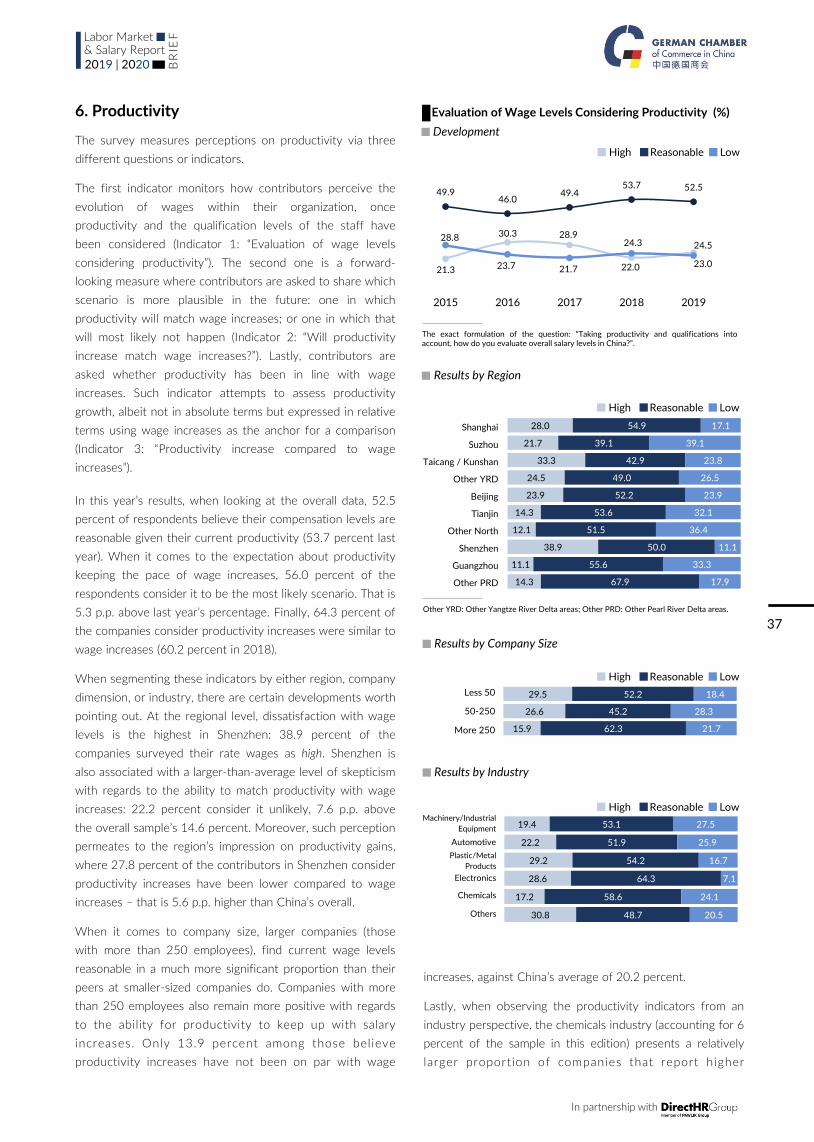

▪ 52.5 percent of German companies consider wage levels

as reasonable given productivity and staff qualifications.

▪ 60.1 percent of the companies have no strategic changes

planned due to increasing labor costs. Relocation to lower

labor cost areas, either within China or abroad, is

considered by ten percent of contributors.

▪ Data management and analysis, creativity and innovation,

and critical thinking represent the set of skills from local

staff with the highest margin for improvement.

KEY DEVELOPMENTS

Economic Environment

▪ China’s GDP in the first half of 2019 registered a 6.3

percent growth, compared to the same period last year.

▪ Although the GDP is growing at its slowest pace since

1992, the outcome is still considerable given the global

context, where protectionism is on the rise, and there are

concerns on the U.S. economy slowing down in 2020.

▪ Despite all the narrative around trade disputes, the

underpinnings of China’s economy remain within its

domestic market. Imports, an internal demand-driven

metric, continued to plunge 5.6 percent in July year-on-

year (YoY). Inflation was at 2.8 percent in July, the second

highest since January 2016.

Labor Market and Wage Developments

▪ The annual wage in China averaged RMB 82,461 in 2018,

an 11 percent increase in comparison to 2017, according

to data from the National Bureau of Statistics in China

(NBS).

▪ For the first time since 2015, there has been a decrease

of 0.2 percent in the migrant population of China’s eastern

regions.

▪ The country will relax its hukou residency rules in small

and mid-size cities in 2019. Cities with a population under

three million are required to completely lift all restrictions

on household registrations. Cities with a population

between three and five million are required to relax or

comprehensively lift household restrictions. Super cities

(population between five and ten million) and megacities

(population over ten million) will be exempt from the

reform.

▪ In 2018, for the first time, the number of migrant workers

employed in the secondary sector (49.1 percent) was

lower than in the service sector (50.5 percent).

Wage Developments at German Companies

5.99 5.87

Expected Effective

Expected and Effective Wage Increases in China

(in 2019, in %)

Expected Wage Growth Development at

German Companies in China (%)

20

12

20

13

20

14

20

15

20

16

20

17

20

19

20

20

10.20

7.10

8.80

8.10

6.235.99

5.53

20

18

8.90

5.90

In partnership with

4

Labor Market

2019 | 2020& Salary Report

BR

IEF

Content

I Labor Market Environment

1. Growth Developments

2. Business Sentiment & Price Developments

3. Labor Market Structure

4. Labor Market Developments

5. Notes

II Wage Developments in China

1. National Wage Developments

2. Provincial Wage Developments

3. Minimum Wages and Wage Guidelines

4. Wages by Industry and Ownership

5. Productivity

6. Notes

III General Survey Results

1. Expected Wage Developments at German Chamber Companies

2. Regional Wage Developments

3. Effective Wage Developments

4. Wage Levels

5. Compensation Levels: Perception

6. Productivity

7. Wage Determination

8. HR Challenges

9. Gender Wage Equality

10. Additional HR Data

11. Foreigners

12. General Results Overview

13. About the Survey

14. Profile of Contributors

15. Notes

IV Appendix: Definitions

V Compensation Data

1. Introduction

2. Wages and Wage Increases

3. Segmentation Variables

4. Region

5. East

6. North

7. South & Southwest

8. Industry

9. Company Size

10. City Tier

11. Total Cost per Employee: Median and Percentiles

5

5

8

10

14

15

17

17

18

19

21

23

25

26

26

28

30

33

35

37

41

42

45

46

46

48

50

50

52

53

53

54

54

55

61

67

73

79

85

91

97

To access specific compensation data, please contact:

Ms. Philippa Hungar

Project Manager Communications

German Chamber of Commerce in China | Shanghai

Tel.: +86 21 5081 2266 Ext. 1846

CONTACT

5

In partnership with

Labor Market

2019 | 2020& Salary Report

BR

IEF

Source: NBS. Data is cumulative: the contribution to GDP from a sector in a quarter for any given year includes the previous quarter/s within that year.

Tertiary52.8 (7.0)

Secondary41.1 (5.6)

Primary6.1 (3.3)

(6.2) 2019Q2

China’s GDP Second Quarter and First Half 2019 (%)

Contribution to GDP by Sector. (Year-on-Year Growth rate)

I Labor Market Environment

1. Growth Developments

At 6.2 percent, the second quarter of 2019 remained within

the stated GDP growth target for the year (between 6.0 to

6.5 percent).

China’s GDP in Q2 2019 showed an economy that is growing

at its slowest pace since quarterly readings started almost

three decades ago in 1992.1 Despite consensus that a

slowing trajectory is laying ahead, a 6.2 percent growth is still

a considerable figure, especially in a global context where

protectionism is on the rise, and where one given concern is

the U.S. economy slowing down in 2020.2 Monthly indicators

also signaled a slow down: in July retail sales went up 7.6

percent YoY, 2.2 p.p. below June; industrial output grew 4.8

percent YoY, 1.5 p.p. down the growth rate from June; and

cumulative fixed-asset investment rose 5.7 percent YoY, 0.1

p.p. below June.

The most dynamic sector continues to be services: the

tertiary sector did not only contribute to nearly 55 percent of

the GDP in the first half of the year but grew seven percent

YoY. The secondary sector (mining, manufacturing,

construction) makes up for 39.9 percent of the GDP in the

first six months of 2019 and presents slower growth (5.8

percent YoY).

At a more granular level, if there is one area of the economy

that shows impressive growth that is information, software

and information technology services (information and

communication technology (ICT)). In the first half of the year,

it grew by 20.6 percent. As of today, it only contributes a

share of 4.1 percent of China’s economy. However, since

technology is an essential strategic asset at the center of any

economy that strives for innovation and enhanced

productivity, it is worth to highlight China’s growth in this

area. ICT combines, following the OECD definition, both

manufacturing and services industries: manufacturing of

computer, communication equipment and other electronic

equipment (both production of and investment in), software

programming and information services, publishing,

broadcasting, or telecommunications.3 The ICT industry,

according to the accounting from NBS refers only to services

and no further details are provided about the specific types

of services that have fueled the industry’s growth.

Other industries exceeding China's first half year's average of

6.3 percent were business services (7.8 percent YoY) and

finance (7.3 percent YoY).

The two largest contributors to GDP remain, on one side,

GDP Growth China (%)

Quarterly Data, 2012-2019

Source: National Bureau of Statistics China (NBS). Preliminary accounting results.

Source: NBS. Preliminary accounting results.

4%

5%

6%

7%

8%

9%

2012 2013 2014 2015 2016 2017 2018 2019

6.2

2019 Q1

2019 Q2

20

17

Q4

20

14

Q4

7.9

20

12

Q4

6.47.3

6.9

54

.6

52

.4

51

.3

50

.2

56

.5

54

.0

52

.8

51

.6

56

.3

54

.0

52

.8

51

.6

56

.6

54

.3

53

.4

52

.2

57

.3

54

.9

40

.2

41

.3

41

.0

40

.9 38

.0

39

.5

39

.6

39

.9 38

.9

40

.2

40

.2

40

.5 39

.0

40

.4

40

.5

40

.7 38

.6

39

.9

PrimarySecondaryTertiary

50

%

Contribution to GDP by Sector (%)

Quarterly Data, 2015-2019

Tertiary54.9 (7.0)

Secondary39.9 (5.8)

Primary5.1 (3.0)

(6.3) 2019H1

Q1 Q2 Q3 Q4

2015 2016 2017 2018

Q1 Q2

2019

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

5.4

29.5

6.19.5

4.5 1.8 8.4 6.9 4.1 2.8

16.63.2

5.8

6.05.9

7.36.2

7.3

2.5

20.6

7.8

5.4

Contribution to GDP and Growth by Industry (%)

First Semester 2019

Source: NBS.

Year-on-year GrowthContribution to GDP

Ag

ricu

ltu

re

Man

ufa

ctu

rin

g

Co

nst

ruct

ion

Wh

ole

sale

&

Re

tail

Tra

nsp

ort

atio

n

Ho

spit

alit

y

Fin

ance

Re

al E

stat

e

ICT

Bu

sin

ess

S

erv

ice

s

Oth

er

Se

rvic

es

In partnership with

6

Labor Market

2019 | 2020& Salary Report

BR

IEF

manufacturing (29.5 percent of China’s economy in the first

semester), and other services (16.6 percent). Other services

are miscellaneous and combines scientific research, services

to households, healthcare, education, and others: no further

breakdown is available to get individual information for each

of sector.

When looking at fixed asset investment (long-term use of

assets, such as land, buildings, and equipment), the total

investment reached RMB 34,889.2 billion during the first

seven months of 2019. At the time of this writing (August

2019), a breakdown of how investment trickles down for

specific industries has not been provided. The only

information available is the variation experienced on a YoY

basis. The industries that presented a higher increase in

investment were: mining, in the secondary sector, with a 27.4

percent increase YoY; education, 18.5 percent; culture,

sports, entertainment (equipment and infrastructure) 15.8

percent; railway transportation infrastructure, 12.7 percent;

and investments in the manufacturing of telecommunications

and computer equipment, 10.5 percent. The most significant

declines in fixed-asset investment came from the following

activities: investment in the manufacturing of railways,

shipbuilding, and aerospace, declined by 10.4 percent in

comparison to the first seven months of 2018; investment in

food processing, 7.6 percent YoY decline; and manufacturing

of electrical machinery and equipment, decreased by 7.5

percent YoY.4

Retail sales of consumer goods reached RMB 22,828.3 billion

in the first seven months of 2019, which marks an 8.3

percent YoY increase. Online sales of physical products

totaled RMB 4,423.3 billion, about 20 percent of all retail

sales and grew 20.9 percent YoY.

Retail data for specific sectors is available in absolute values

(sales volume). One of the most important contributors to

retail sales is automotive sales, which accounts to almost ten

percent of the total retail sales in the first seven months of

the year.

From January to July, according to data provided by the NBS,

automobile sales went up by just 0.6 percent, in stark

contrast to the 8.3 percent YoY increase in retail sales in the

same period. In July 2019, automobile sales declined by 2.6

percent YoY.5

During the first seven months of 2019, fixed-asset

investment in the automotive industry increased 1.8 percent

YoY, compared to 5.7 percent for all manufacturing; the

number of automobile units produced decreased 12.8

percent YoY, amid an overall 5.8 percent YoY increase of the

overall industrial output.

On its first seven months of the year review, China’s

Growth of Retail Sales, Production and Fixed-asset

Investment. Monthly (%)

Fixed-asset investment YoY (monthly)

Industrial production YoY (monthly)

Retail sales YoY (monthly)

Source: NBS. Retail sales and value-added in industrial production growth rates compared to the same period last year. Data is cumulative for fixed-asset investment (total amount of money invested in the in construction and purchase of fixed assets).

4%

6%

8%

10%

12%

14%

2019JulMarDecMar Jun SepMar Jun Sep DecMar Jun Sep DecMar Jun Sep Dec

2015 2016 2017 2018

7.6

5.7

4.8

Retail Sales of Consumer Goods, January - July 2019

Absolute value (RMB 100 million) and Year-on-Year Growth

Rate (%)

Grain, Oil, Food 1,107 9.9 8,064 10.3

Beverages 180 9.7 1,173 9.9

Tobacco and Liquor 287 10.9 2,199 6.6

Garment, Footwear, Knitwear 934 2.9 7,499 3.0

Cosmetics 202 9.4 1,666 12.7

God, Silver, Jewelry 175 -1.6 1,529 2.9

Commodities 462 13.0 3,294 13.9

Household appliances and AV Equipment 713 3.0 5,113 6.2

Traditional Chinese , Western Medicines 485 11.6 3,424 11.0

Cultural and Office Appliances 258 14.5 1,739 5.6

Furniture 163 6.3 1,062 5.8

Communication Appliances 338 1.0 2,581 6.5

Petroleum and Related Products 1,641 -1.1 11,288 2.5

Automobile 3,056 -2.6 22,147 0.6

Building and Decoration Materials 173 0.4 1,083 3.1

July

Value YoY

January to July

Value YoY

Source: NBS.

7

In partnership with

Labor Market

2019 | 2020& Salary Report

BR

IEF

Association of Automobile Manufacturers (CAAM) reported

similar results. The 13.9 million units produced in the first

seven months of 2019 represent a 12.1 percent decrease

YoY; the 14.1million units sold in the first seven months of

2019, a 11.4 percent decline YoY. In July alone, vehicle sales

totaled 1.8 million units, a decline of 4.3 percent YoY.6 In

2019, the main cause for such reduction seems to be the

decision, urged by the central government, by 15 cities and

provinces (which account for more than 60 percent of the

total auto sales in China) to fast-track the adoption of a new

regulatory framework imposing cars built under the so-called

China stage-6 emission standards, ahead of the original 1 July

2020 deadline. Such a move created a vacuum in the market:

consumers were uncertain about whether to buy stage-5 cars

fearing to be unable to resell them. Such uncertainties lead to

a prompting decline of demand and thus a decline of the

number of units sold.7 In addition, as such standard was not

due to apply until 2020, manufacturers and retailers were not

able to provide the market with enough stage-6 certified cars

due to lack of stock.8

The headwinds faced by the automotive industry predate

2019. The total number of cars produced in China had

already decreased by 4.1 percent in 2018 compared to 2017.

It was the first time since 2009 that car production went

down on a yearly basis. Such decline was due to a decrease

in output of passenger cars (5.2 percent decline), whereas

commercial vehicles stood up 1.7 percent.9

Readings on China’s macroeconomic data depends very much

on the vantage point of the observer. The fact that retail

sales have gone up by 8.3 percent in the first seven months

of 2019 does not affect actors invested in the automotive

sector, who have reasons for concern based on the recent

domestic market developments.

The case for the automotive sector shows that the

underpinnings of China’s economy remain within its domestic

market, despite all the focus on trade frictions might suggest.

In July, exports rose unexpectedly 3.3 percent YoY, after a

fall in June by 1.3 percent YoY. Imports, an internal demand-

driven metric, continued to plunge 5.6 percent in July,

following a 7.3 decrease in June.10 China’s exposure to the

world has fallen in relative terms, whereas the world’s

exposure to China has increased.11

However, the role of trade frictions should not be

underestimated. Apart from the effects of these tensions on

trade volumes, the impact on security and confidence is

severe in any well-functioning economy.

Manufacturing in China, January – July 2019 (%)

Fixed-asset Investment and Industrial Output. Evolution

Year-on-Year Growth Rate

ALL Manufacturing 3.3 6.1

Of Chemical Raw Material & Chemical Products 9.4 4.6

Of Medicines 6.9 6.7

Of Fabricated Metal Products -5.2 7.3

Of General-Purpose Machinery 2.1 4.5

Of Special Purpose Machinery 7.2 7.7

Of Automobile 1.8 -12.8

Of Railways, Shipbuilding, Aerospace, Other Transportation Equipment

-10.4 11.4

Of Electrical Machinery & Equipment -7.5 9.7

Of Telecommunications Equipment, Computers and Other Electronic Equipment

10.5 9.1

Fixed-asset investment. Increase Rate (YoY)

Industrial production. Increase Rate (YoY)

Source: NBS.

In partnership with

8

Labor Market

2019 | 2020& Salary Report

BR

IEF

4.3

1.8 1.91.1

-1.1

2.5 2.6

Price Level Development 2015-2018

Variation over the Same Month in the Previous Year (%)

Breakdown of Consumer Price Developments

Average Variations from January to June 2019 (%)

2. Business Sentiment & Price Developments

The unfolding of trade tensions between the U.S. and China,

which have been going on for more than a year, reached new

peaks in August.12 In addition, on 24 May 2019, the China

Banking and Insurance Regulatory Commission (CBIRC) took

over Inner Mongolia’s based Baoshang Bank alleging “severe

credit risk”.13 Despite being a minor player, the move rattled

Chinese markets, with fears that Baoshang Bank could be the

first of many. This prompted the People’s Bank of China

(PBOC) to announce that no further moves were planned to

intervene in other banks, and that it would inject additional

cash reserves into the banking system.14

Both events are taking their toll on the business sentiment.

China’s Caixin / Markit Purchasing Managers’ Index (PMI)

shrank considerably in June, although it attenuated its fall in

July. June’s mark at 49.4 was its lowest reading since January

when the indicator came in at 48.3. In July it bounced to

49.9. Caixin / Markit’s index monitors private companies and

smaller firms than the official PMI from NBS. The latter

focuses on big businesses and state-owned enterprises and

presented a similar trend: remaining at 49.7 in July, an

increase from 49.4 in June. Both manufacturing PMIs

indicate the manufacturing sector contracted (in both indexes

the 50-point mark separates growth from contraction).15

The deterioration in the PMI sentiment data was expected,

after the trade tension escalated in May 2019. From 11 May,

tariff increased to 25 percent from the earlier ten percent

rate – applied to USD 250 billion worth of Chinese imports

to the United States. The U.S. was also putting together a

tariff of up to 25 percent on a further USD 300 billion of

Chinese goods, turning up the pressure on the Chinese

economy. China reacted by placing variable tariffs on USD 60

billion of U.S. imports. Industrial profits stood at RMB 515.39

billion in April (only a month before the escalation of the

trade tensions), decreasing by 3.7 percent compared to a

year earlier. This was the largest percentage decline since

December 2015. With further tariffs about to kick in on

Chinese exports, there is a great possibility for the downward

trend to continue.16

The PMI is an important economic indicator globally watched

by investors to anticipate economic trends. The fall in the

headline index was mostly driven by weaker new orders

(weak demand).17 Export orders dropped sharply, suggesting

the U.S. latest tariff hike may already be undermining foreign

demand. While the official NBS and Caixin non-

manufacturing PMIs remained above contraction levels in

July, 53.7 and 51.6 respectively, their stagnation and decline

point to continued skepticism and challenges for China’s

economy.18

Business Sentiment 2019

Purchasing Managers’ Index (PMI)

Source: Caixin / Markit. PMI values >50 indicate expanding business; values <50 indicate contraction.

Source: NBS.

ManufacturingServices

Source: NBS.T

ran

spo

rtat

ion

&

Co

mm

un

icat

ion

Fo

od

, To

bac

co

&L

iqu

or C

loth

ing

Ho

usi

ng

Ho

use

ho

ld

arti

cle

s &

se

rvic

es

Ed

uca

tio

n

& L

eis

ure

He

alth

care

The only signal of détente came in the weeks leading to and

during the G20 Summit, held in Osaka (Japan) at the end of

June, where Presidents Xi and Trump agreed to resume trade

talks. However, such respite was short lived: on 1 August, the

Trump administration said U.S. would impose ten percent

tariffs on another USD 300 billion of Chinese goods, starting

1 September; on 5 August, the U.S. Department of Treasury

declared China in a press release to be a "currency

manipulator".19

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

JAN

MA

R

MA

Y

JUL

SE

P

NO

V

JAN

MA

R

MA

Y

JUL

SE

P

NO

V

JAN

MA

R

MA

Y

JUL

SE

P

NO

V

JAN

MA

R

MA

Y

JUL

Producer Price Index (PPI)Consumer Price Index (CPI)

-0.3

2.8

53.6

51.1

54.4 54.5

52.752

51.6

48.349.9

50.850.2 50.2

49.4 49.9

JAN FEB MAR APR MAY JUN JULY

9

In partnership with

Labor Market

2019 | 2020& Salary Report

BR

IEF

Weaker demand caused a slowdown in manufacturing

activity which decreased producer prices (0.3 percent decline

YoY). Particularly weak was the evolution of prices for oil and

natural gas extraction, and paper and paper product

manufacturing, which decreased by 8.3 percent and 7.1

percent, respectively, compared to the same period last

year.20

July’s consumer prices grew in annual terms (2.8 percent)

driven by higher food prices: fruit prices increased by 39.1

percent compared to a year earlier, while pork prices went up

27 percent. This increase was caused by extreme weather

conditions and an outbreak of African swine fever that has

reportedly cut the pig population in China by about a third

from 360 million.21 The 2.8 percent inflation in July 2019 is

the second highest since January 2016 (the highest being 2.9

percent, in February 2018).

In partnership with

10

Labor Market

2019 | 2020& Salary Report

BR

IEF

Secondary PrimaryTertiary

Distribution of Workforce Across Sectors (%)

China’s Age Demographic Composition of Population (%)

Source: NBS; *2025: Forecast from World Bank.

Source: NBS.

22.9 20.3 16.6 16.5 16.9 16.6

70.1 72.0 74.5 73.0 71.2 69.2

7.0 7.7 8.9 10.5 11.9 14.2

Aged 0 to 14 yearsAged 15 to 64 years>65 years

2000 2005 2010 2016 2025*

34.1 34.6 35.7 36.1 38.5 40.6 42.4 43.5 44.9 46.3

27.8 28.7 29.5 30.3 30.1 29.9 29.3 28.8 28.1 27.6

38.1 36.7 34.8 33.6 31.4 29.5 28.3 27.7 27.0 26.1

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Distribution of Urban & Rural Population in China (%)

Source: NBS.

49.9 51.3 52.6 53.7 54.8 56.1 57.3 58.5 59.6

50.1 48.7 47.4 46.3 45.2 43.9 42.7 41.5 40.4

2010 2011 2012 2013 2014 2015 2016 2017 2018

RuralUrban

expectancy is 76.4 years, according to 2017 data from the

World Bank.27 Retirement age varies: 60 years for males, 55

for females in civil service jobs, 50 years otherwise. Increasing

the retirement age has been the subject of discussion for

several years now, as it could positively impact China's labor

force supply and pension system (in the short term).

However, there has not been any concrete policy

implementation.

China's working population decreased from its peak in 2011

of 925 million to 897 million in 2018. Back then, the ratio

worker to pensioner was 3.1-to-1. By 2050, a third of China’s

population will be over the age of 60. The Ministry of Human

3. Labor Market Structure

China’s decades-old household registration system, the

hukou, underwent a significant shift in 2019. The hukou

system designates a resident’s status as being either rural or

urban based on the resident’s registered birthplace. It

establishes a worker from the countryside not being entitled

to public services in a city, despite working and living there.

In yet another move to foster urbanization, the country will

relax its hukou residency rules in small and mid-size cities.

The announcement came on April 2019, via the National

Development and Reform Commission (NDRC).22 Under the

2019 Urban Development Plan, China aims to increase its

urbanization rate by one p.p. this year, to stay on the course

of its 60 percent urbanization target established at the 13th

Five Year Plan (FYP). China is well poised to achieve it: by the

end of 2018, the urban resident population in China totaled

831.4 million, 59.6 percent of the country’s total.23 At the

current pace, urban population could reach 61 percent by

2020.

The 2019 Urban Development Plan states that all cities with

a population under three million to “completely lift” all

restrictions, and cities between three and five million

“comprehensively lift or relax” restrictions on household

registration.24 Outside the scope of the reform are left

China’s super cities, between five and ten million (Chongqing,

Tianjin, Wuhan, Chengdu, Nanjing, Zhengzhou, Hangzhou,

Shenyang, Changsha), and megacities with populations over

ten million (Beijing, Shanghai, Shenzhen, Guangzhou).25

Therefore, the announcement aims mostly to tier-3 and tier-

4 cities, adding pressure to municipal governments to invest

in improving their public services offerings. The largest tier-1

and some tier-2 cities, often the most attractive to migrant

workers in terms of job expectations but not in living costs,

will continue to have more restrictive hukou policies.26

With the relaxation on household registration conditions, in

the context of a slowing economy and a rapidly aging

population, the government expectation is to reboot migrant

flows, by removing obstacles when relocating to small or mid-

size cities (more on migrant workers later in this section).

Under the new regulations, migration pressure should be

released of tier-1 cities – where labor and resources are

converging disproportionately – and redirect migrant worker

flows into tier-2, tier-3 and tier-4 cities, which are in higher

need of a boost in their urbanization, housing prices,

consumption, and productivity.

A further lever the Chinese government could implement to

alleviate the pressing issue of a shrinking labor force is an

increase in the age of retirement. China’s average life

2018

11

In partnership with

Labor Market

2019 | 2020& Salary Report

BR

IEF

Resources and Social Security (MOHRSS) estimates the ratio

worker to pensioner will decrease to only 1.3-to-1.28 In

mainland China, the number of citizens older than 60 hit 249

million in 2018, which amounts to about 18 percent of the

total population.29 According to an analysis by sociology Prof.

Wang Feng, University of California, if China was to maintain

the current welfare benefits at the current aging pace,

spending on education, healthcare, and pensions could go up

from ten percent of the GDP to 23 percent by 2050. 23

percent of the GDP equals the share of the total government

spending today.30

In 2016, China raised the limit of how many children all

families could have to two children, hoping to foster a baby

boom. Though 2016 saw a brief uptick, birth rates have fallen

in 2017 and 2018.31 There were 15.2 million births in 2018,

a decline of more than eleven percent from 2017.32 The

slowing rates of new births paired with an increase of life

expectancy creates challenges for the government. First, a

smaller working population in the future could cause

difficulties in paying pensions for an increasing retired

population; second, a shrinking labor force could reduce

consumer spending and have an impact on the economy in

China, reinforcing, in a negative loop, the difficulties to pay

pensions.33

According to a report from the World Social Security Center

at the Chinese Academy of Social Sciences, the urban worker

pension fund will reach its peak at RMB seven trillion in

2027. Following that, it will drop steadily reaching zero by

2035. Social security contribution rates are mandatory

(composed by up to 20 percent of the employees’ salaries by

the employer, and another eight percent by the employees).

To add further stress to the pension system, China’s State

Council announced in March 2019 the employer pension

contribution rate would be cut to 16 percent, as part of a

package of measures designed to support businesses.34

Despite China’s pension funds being critical to the country’s

social security system, the fund would run on a deficit

without subsidies from the central government: RMB 528.5

billion have been budgeted to support social security

payments in 2019, a 9.4 percent increase from the previous

year.35 Were those subsidies to be put on hold,

approximately half of China’s provinces would be geared

towards pension fund deficit by 2022, compared to just six

provinces in 2015.36 The central government created a

special fund in July 2018 to shift pension funds from

provinces with large working populations, like Guangdong, to

more impoverished regions where the number of retirees is

large, like Liaoning.37

Besides initiatives, like the 996 working hour system (working

from 9 am to 9 pm, six days a week),38 more sustainable

proposals have not been put forward to tackle the

fundamental imbalances currently present in China’s labor

market structure.

In partnership with

12

Labor Market

2019 | 2020& Salary Report

BR

IEF

5.44.4

3.9

2.4

1.91.3 1.5 1.7

0.6

5.5

3.43.0

1.71.3

0.4 0.31.5

0.5

5.2

5.95.4

3.6

2.8 2.73.4

2.0

0.9

2010 2011 2012 2013 2014 2015 2016 2017 2018

Source: NBS. Migrant workers outside inter province: Working in a province other than that of their household registration; Migrant workers outside inner province: Working in the same province of their household registration.

Local migrant workers

Migrant workers outside (inner+inter)

Total migrant workers

West27.5

East36.1

Central33.1

Northeast3.4

Source: NBS.

-0.2

0.9

1.3 1.3

2018 Growth over 2017 (in %)

Migrant Workers Distribution of Employment by Sector

of Economy 2015 - 2018 (%)

Migrant Worker Distribution and Evolution (%)

By Region in 2018 and Evolution Versus 2017

Source: NBS. Starting from 2016 the Northeast region was added into the official reporting.

Secondary PrimaryTertiary

44.5 46.7 48.0 50.5

55.1 52.9 51.5 49.1

0.4 0.4 0.5 0.4

2015 2016 2017 2018

Migrant Workers

Migrant workers have been contributing to China’s economic

success for the past three decades. As the country bet its

economic development to its eastern coast, millions migrated

to cities there. Workers settled around the three main

industrial regions: the Bohai Bay Economic Ring, the Yangtze

River Delta, and the Pearl River Delta.

Migrant workers amount to 20.6 percent of China’s total

population. As of 2018, the number of migrant workers

totaled 288.4 million, according to data from the NBS.39 That

is a 0.6 percent increase in comparison with 2017, the lowest

increase during the period from 2010 to 2018, putting an

end to two consecutive years of accelerated growth.

Among migrant workers, local migrant workers (those working

within the villages and towns where their hukou is) grew by

0.9 percent YoY, 1.1 p.p. below 2017. Migrant workers going

out (to work outside of the villages and towns where their

hukou is) grew at 0.5 percent YoY, one p.p. slower than in

2017.40 Migrant workers going out to seek jobs inside their

province increased by 1.7 percent (96.7 million in 2018, 95.1

million the year prior), whereas the number of migrant

workers going out seeking jobs across provinces experienced

a 1.2 percent decrease (75.9 million in 2018, 76.8 million in

2017).

Migrant workers concentrate mostly in China’s eastern and

central regions, accounting together for 69.2 percent of the

overall migrant working population.41 For the first time since

2015, there has been a slight decrease in the migrant

population in eastern regions (down 0.2 percent). In the other

areas, despite the growth, its pace has been reduced in some

instances by nearly a third. The migrant working population in

China’s central region grew 0.9 percent YoY, half the

increase in 2017; in Western China, the growth rate was 1.3

percent YoY in 2018, two p.p. below 2017; Northeast China,

which accounts only for 3.4 percent of the migrant working

population, saw a 1.3 percent YoY increase in 2018, 1.8 p.p.

below 2017’s growth.

As pointed out in previous editions of this report, the number

of migrant workers employed in the secondary industry

(manufacturing, mining, construction) has been steadily

declining. For the first time, in 2018 the number of migrant

workers employed in the secondary sector was lower than in

the services sector: 49.1 percent in the secondary sector,

50.5 in the services sector.

At the specific industry level, the largest number of migrant

workers are employed in manufacturing & mining (27.9

percent of all migrant workers) and construction (18.6

percent). Manufacturing & mining saw a decrease of two p.p.

Growth Rate of Migrant Workers (%)

Migrant Workers Distribution: 2017 & 2018

In millions: 2018, (2017)

Source: NBS.

288.4 Total

Local migrant workers

Migrant workers going outside: Inter-province

115.7

Migrant workers going outside: Inner-province

96.7

75.9

(114.7)

(76.8)

(95.1)(286.5)

13

In partnership with

Labor Market

2019 | 2020& Salary Report

BR

IEF

0.1

1.5

-3.9

-0.3

2.6

Migrant Workers Distribution of Employment by

Industry. 2017 and 2018 (%)

Source: NBS. No data provided for “Other services”.

3,4

44

3,9

18

3,0

48

4,0

48

3,0

19

3,0

22

3,4

85

3,7

32

4,2

09

3,2

63

4,3

45

3,1

48

3,2

02

3,7

21

8.47.4 7.0 7.3

4.3

6.06.8

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2000

4000

Manufacturing & Mining

Construction Retail Transportation Hospitality Real estate ALL

in the total number of migrant workers in comparison with

2017. In 2018 construction experienced a decrease of 0.3

p.p. over its 2017 employment contribution.

In the tertiary sector the migrant worker percentage

increased for the following industries: real estate (residential

services, repairs, and other services), with 12.2 percent of the

total migrant worker employment; wholesale and retail, 12.1

percent; and other services, 12 percent.

According to official data, the monthly income of a migrant

worker averaged RMB 3,721 in 2018, a 6.8 percent YoY

increase. The highest industry-specific YoY increase is for

manufacturing and mining migrant workers, with an 8.4

percent jump and an average monthly income of RMB 3,732.

Construction and transportation present a 7.4 and 7.3

percent YoY increase, respectively. The current average

monthly income for migrant workers in construction

moderately rose to RMB 4,209, and in transportation RMB

4,345. The lowest income levels are for real estate,

hospitality, and retail workers.

The average age of a migrant worker is 40.2 years, 0.5 years

older than last year. China’s migrant working population is

aging rapidly: those older than 40 represent 47.9 percent of

the total as of 2018, whereas in 2011 they made up for 38.3

percent. The youngest cohort, aged 16 to 30 years, accounts

for 27.6 percent in 2018, as opposed to 39 percent in 2011.

Growth year-on-year (%)Income 2018Income 2017

Age Composition of Migrant Workers, 2015 - 2018 (%)

Source: NBS.

32.9 31.9 29.9 27.6

49.2 49 48.8 50

17.9 19.1 21.3 22.4

2015 2016 2017 2018

Aged 16 to 30 yearsAged 31 to 50 years>50 years

Tertiary10.9

No Schooling1.2

Elementary School15.5

Junior High School55.8

Senior Middle School16.6

Migrant Workers Distribution by Education in 2018 (%)

and Comparison with 2015 (p.p.)

Variation over 2015 (in p.p.)

Source: NBS.

No Schooling

Tertiary

29.9

18.9

12.3

6.6 6.2

11.3 11.6

27.9

18.6

12.1

6.6 6.7

12.2 12.0

Manufacturing & Mining

Construction Retail Transportation Hospitality Real estate

Other services

2017 2018

Migrant Workers Monthly Income (in RMB)

Source: NBS. Agriculture (0.4%) and other secondary industries (3.5%) not included in the graphic.

Secondary Sector

Tertiary Sector

Elementary

Jr. High School

Sr. Middle School

In partnership with

14

Labor Market

2019 | 2020& Salary Report

BR

IEF

42.138.0

31.9 32.0

47.3

2018 Q1 2018 Q2 2018 Q3 2018 Q4 2019 Q1

Zhaopin Ratio of Job Applications by Job Vacancies

Source: Competitive index by Zhaopin.com. * Number of resume applications divided by the number of job vacancies: How many applicants on average per job vacancy published.

4. Labor Market Developments

China’s urban unemployment rate, provided by the MOHRSS,

amounted to 3.67 percent in the first quarter of 2019.42 The

rate is below the surveyed unemployment rate of five percent

in June, provided by the NBS, which it is based on a monthly

31-city survey.43 Data from the NBS is considered to be more

reliable than that of the MOHRSS, as the former is elaborated

following the international standards by the International

Labor Organization (ILO). Additionally, quarterly

unemployment rates from the MOHRSS refers to urban

registered jobless rate: the rate of unemployment leaves out

those in search for a job in urban areas who do not have an

urban registration.44

Since 2014, the MOHRSS publishes quarterly ratios of job

vacancies to job seekers, to gauge labor shortages or labor

oversupply.45 Following on MOHRSS data, in Q1 2019, there

were 5.9 million job vacancies (3.3 percent increase over Q1

2018) and 4.6 million job seekers (0.3 percent decrease over

the same period last year). This results in a ratio of job

vacancies to job seekers of 1.28, signaling labor shortage.

Over the years, the ratio presents a steady upward trend. This

indicates that the labor market is unable to efficiently allocate

the required amount of human resources to cover all the job

openings. With every passing year this gap increases. The

pace has hastened from Q4 2017, with the ratio remaining

above the 1.20 level. At the regional level, MOHRSS data for

East, Central China reproduces similar labor shortages as seen

for China overall. In Western China, the ratio increases to

1.40. Although the number of job seekers went up there by

14.1 percent over the same period last year, job demand

increased by 21.4 percent.46

Private online recruitment platform Zhaopin tracks job

vacancies and job applications from white collar professionals

across 37 major cities. In contrast with MOHRSS trends, from

Zhaopin’s research in Q1 2019, there was an average of 47.3

job applicants per job vacancy, a 10.5 percent increase over

the first quarter of 2019.47 These percentages point directly

to oversupply, and not labor shortages as per the official data.

Two very different snapshots from two different sources of

the country’s job market, amid concerns of whether the

economic slowdown seen in 2019 will take its toll in job

losses.

In the first half of 2019, a total of 7.4 million people were

newly employed (67 percent of the annual target), according

to the NBS. By the end of the year, it is expected that 8.3

million new graduates will enter the labor market.

Summary of Labor Market Developments

Metrics Last Previous Reference Frequency

Employed Population(Tens of thousands)

77,586 77,640 Dec. 2018 Yearly

Unemployment Rate(%)

3.67 3.80 March 2019 Quarterly

Unemployed Population(Tens of thousands)

974 975 Dec. 2018 Quarterly

Wages(RMB/month)

6,872 6,343 Dec. 2018 Yearly

Minimum Wages*(RMB/month)

2,480 2,420 Dec. 2018 Yearly

Population(Million)

1,395 1,390 Dec. 2018 Yearly

Source: Tradingeconomics.com China Indicators, from NBS and China Ministry of Human Resources (MOHRSS) data. * Minimum wage in Shanghai (the highest minimum wage in China).

1.23 1.22 1.231.271.28

1.26 1.26

1.4

China East Central Western

2019Q12018Q1

MOHRSS Ratio of Job Vacancies to Job Seekers

Overall China and by Region 2018 Q1 vs. 2019 Q1

Source: MOHRSS based on the tracking of 90 cities. *A value > 1 indicates labor shortages (demand greater than supply); a value < 1 means oversupply.

Source: MOHRSS based on the tracking of 90 cities. * A value > 1 indicates labor shortages (demand greater than supply); a value < 1 means oversupply.

1.071.05

1.11.13 1.13

1.11

1.16

1.22 1.23 1.231.25

1.27 1.28

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2016 2017 2018 2019

MOHRSS Ratio of Job Vacancies to Job Seekers

Overall China 2016 Q1 to 2019 Q1

15

In partnership with

Labor Market

2019 | 2020& Salary Report

BR

IEF

5. Notes

1. Miao Han et al., “China Economy Slips to Record Low Growth",

Bloomberg.com, 15 July 2019.

2. Neil Irwin, “How the Recession of 2020 Could Happen”, The New

York Times, 17 August 2019. “China and the world. Inside the

dynamics of a changing relationship”, McKinsey Global Institute,

July 2019.

3. Information and communication technology (ICT). OECD Library.

https://www.oecd-ilibrary.org/science-and-technology/

information-and-communication-technology-ict/indicator-

group/english_04df17c2-en, accessed 27 August 2019.

4. “Investment on Fixed Assets for the First Seven Months of 2019”,

National Bureau of Statistics (NBS) Press Release, 16 August

2019.

5. “Total Retail Sales of Consumer Goods up by 7.6 percent in July

2019”, NBS Press Release, 18 August 2019.

6. “China Flash Report, Sales Volume 2019”, Marklines.com, 5

September 2019. https://www.marklines.com/en/statistics/

flash_sales/salesfig_china_2019, accessed 6 September 2019.

7. In June 2019 authorities clarified that stage-5 cars could be

resold.

8. Yilei Sun, Norihiko Shirouzu, “Behind the plunge in China auto

sales”, Reuters.com, 1 July 2019.

9. “Production of cars in China from 2009 to 2019 (in 1,000 units)”,

Statista.com, https://www.statista.com/statistics/281133/car-

production-in-china/, accessed 27 August 2019.

10. Sidney Leng, “China’s exports and imports both fell in June, as

higher US trade war tariffs blitz Chinese economy”, SCMP, 12

July 2019.

11. “China and the world. Inside the dynamics of a changing

relationship”,McKinsey Global Institute, July 2019.

12. 29 June, trade talks to restart after presidents Xi and Trump

reached a tentative truce days before the G20 Summit. 9 July,

U.S. exempts 110 Chinese products from 25 percent tariffs. 16

July, Trumps threatens tariffs on USD 325 billion of Chinese

goods. 31 July, Shanghai trade talks end with little progress

being made. 1 August, Trump says U.S. will impose 10 percent

tariffs on another USD 300 billion of Chinese goods, starting 1

September. 5 August, the U.S. Department of Treasury declares

China to be a “currency manipulator”. That same day, Chinese

companies suspend new U.S. agricultural product purchases. 13

August, U.S. delays tariffs on certain products and removes

items from the list; U.S. and China agree to talk again in two

weeks. For a detailed timeline, see https://www.china-

briefing.com/news/the-us-china-trade-war-a-timeline/, accessed

27 August 2019.

13. “China's Baoshang Bank taken over for one year due to 'serious

credit risks’”, China Daily, 24 May 2019.

14. Andrew Galbraith, “China central bank urges calm after

Baoshang takeover”, Reuters.com, 3 June 2019.

15. Karen Yeung, “China factory activity contracted in June as US

trade war tariff increase in May starts to bite”, SCMP, 1 July

2019.

16. Finbarr Bermingham, John Carter, “China’s manufacturing index

drops into negative territory in May as economic pressures

mount”, SCMP, 31 May 2019.

17. The Caixin China PMI is compiled from surveys to business

owners and supply chain managers on a range of topics,

including new orders, employment trends or delivery times. The

answers are then boiled down into one number, in a scale

between 0 and 100. A mark above 50 indicates the economy is

expanding. Below 50 suggests it is contracting.

18. See Note 16.

19. “Treasury Designates China as a Currency Manipulator”, U.S.

Department of Treasury Press Release, 5 August 2019.

20. Yawen Chen, Ryan Woo, “China producer prices fall for first

time in three years, deflation worries resurface”, Reuters.com, 9

August 2019.

21. Huileng Tan, “China’s food prices jump 9.1% in July as the

country battles African swine fever”, CNBC, 9 August 2019.

Tom Hancock, “China swine fever hits small farmers and rural

communities hard”, Financial Times, 10 July 2019.

22. “China's comprehensive relaxation of settlement restrictions”,

BBC China, 11 April 2019. In Chinese.

23. NBS Database. http://data.stats.gov.cn/english/easyquery.htm

?cn=C01, accessed 27 August 2019.

24. Zheng Yangpeng,“What does China’s move to relax hukou

residency curbs mean for the property sector?”, SCMP, 11 April

2019.

25. Zoey Ye Zhang, “China is Relaxing Hukou Restrictions in Small

and Medium-Sized Cities”, China-Briefing.com, 17 April 2019.

26. See Note 25.

27. Life expectancy at birth, total (1960-2017). The World Bank.

https://data.worldbank.org/indicator/SP.DYN.LE00.IN?locations

=CN, accessed 26 August 2019.

28. Viola Rothschild, “China’s pension system is not aging well”, The

Diplomat, 6 March 2019.

29. Frank Tang, “China’s state pension fund to run dry by 2035”,

SCMP, 12 April 2019.

30. Wang Feng, Yong Cai, “China Isn’t Having Enough Babies”, The

New York Times, 26 February 2019.

31. Steven Lee Myers, “China’s Looming Crisis: A Shrinking

Population”, The New York Times, 21 January 2019.

In partnership with

16

Labor Market

2019 | 2020& Salary Report

BR

IEF

32. See Note 29.

33. See Note 31.

34. See Note 29.

35. See Note 29.

36. See Note 28.

37. See Note 29.

38. The 996 working hour system gained traction both in social

media and news outlets in China (and abroad) when, in April

2019, Jack Ma - founder of Alibaba Group - said in an internal

company post in Weibo: “996 is not a problem (…) doing

overtime is bliss”. Later, JD.com’s founder Richard Liu chimed in

to endorse Jack Ma words. The 996 working hour system is an

extremely polarizing subject: it is against China’s Labor Contract

Law to demand employees to work overtime without

compensation; additionally such working schedule imposes

serious hurdles on employees willing to balance personal with

professional life, an already daunting endeavor even in the

traditional 8:00 to 17:00 working schedule, given the pervasive

use of technology (email, wechat); finally, it does not take into

account health related issues (stress, fatigue, insufficient

reparatory sleep) that such working schedule induces, ultimately

impacting performance and productivity within the same

organizations that encourage it.

39. China has two types of hukou: agricultural and non-agricultural.

Migrant workers (农民工, nóng mín gōng) are workers whose

hukou remains in the country side but who have been working in

a non-agriculture activity for more than 6 months.

40. The NBS distinguishes between “Local Migrant Workers” (本地

农民工, běn dì nóng mín gōng) and “Migrant Workers who go

out” (外出农民工 , wài chū nóng mín gōng). Local migrant

workers are working within the villages and towns where their

hukou is; migrant workers who go out work outside of the

villages and towns where their hukou is in, either inside or

outside the province of their hukou.

41. The direct translation of 农民工 is “peasant workers”, referring

to people who have agriculture hukou but work in secondary or

tertiary related activities. However, since rural areas seldom

provide non-agricultural jobs, Chinese media uses 农民工 to

specifically refer to ‘peasant workers’ who ‘migrate’ to city areas

and do non-agricultural work.

42. A local migrant worker 本地农民工 indeed does not migrate.

Consider a Shanghainese holding a Shanghainese hukou that

happens to be an agricultural hukou (even Shanghai has rural

areas). He/she will be considered as a local migrant worker if

he/she is doing non-agricultural work in Shanghai (i.e., driving a

cab).

41. According to the NBS, Eastern region includes Beijing, Tianjin,

Hebei, Shanghai, Jiangsu, Zhejian, Fujian, Shandong, Guandong

and Hainan; Central: Shanxi, Anhui, Jianxi, Henan, Hubei;

Western: Inner Mongolia, Guangxi, Chongqing, Sichuan, Guizhou,

41. Yunnan, Tibet, Shaanxi, Gansu, Qinghai, Ningxia and Xinjiang;

Northeast: Liaoning, Jilin, and Heilongjiang.

42. China Economic Indicators 2019. Tradingecononics.com.

https://tradingeconomics.com/china/indicators, accessed 27

August 2019.

43. “China urban unemployment rate”, NBS Press Release, 15 July

2019.

44. Martin Hart-Landsberg, “China has an unemployment problem”,

Monthly Review Online, 14 March 2019.

45. The MOHRSS samples data from around 200 public

employment and talent service organizations. Each quarter

covers a varying number of cities (usually between 90 and 110).

The latest data available, by the time of this writing, was from

the first quarter of 2019 and the number of cities sampled was

90.

46. “Analysis Market Supply and Demand. First Quarter 2019”,

MOHRSS, 24 April 2019. http://www.cjob.gov.cn/rdzx/

100062.jhtml, accessed 27 August 2019. In Chinese.

47. “2019 Spring recruits. How much is the white collar salary?”,

Sina.com, 17 April 2019. In Chinese.

17

In partnership with

Labor Market

2019 | 2020& Salary Report

BR

IEF

Wage Growth Indicators China (%)

2012-2018. Nominal Growth

9.410.6

9.57.9 7.8 7.3 6.9 6.7 6.9 6.6 6.3

11.613.3

14.4

11.9 10.1 9.5 10.18.9

10.011.0

9.9

09 10 11 12 13 14 15 16 17 18 2019*

GDP and Wage Growth (%)

2009-2019

Wage growth (nominal)GDP growth

Source: NBS & German Chamber of Commerce in China analysis. *National wage growth estimate. The number of provinces issuing adjustments for wage guidelines & minimum wages varies every year.

Source: NBS & German Chamber of Commerce in China analysis. *2019 GDP growth until June. 2019 Wage growth: Estimates from the Chamber’s own analysis.

Minimum wageNational wageWage guidelines

Average Wage and Wage Growth

2009-2019

Wage growth, nominal (in %) Average wage RMB

32

,24

4

46

,76

9

82

,46

1

90

,61

3

0%

4%

8%

12%

16%

20%

24%

0

15,000

30,000

45,000

60,000

75,000

90,000

105,000

09 10 11 12 13 14 15 16 17 18 2019*

Source: NBS & German Chamber of Commerce in China analysis. * Average wage and wage growth: Estimates from the Chamber’s own analysis. Note: Annual wages based on 12 months; all wages are pre-tax.

II Wage Developments in China

1. National Wage Developments

The annual wage in China averaged RMB 82,461 in 2018 -

an increase of 11 percent in comparison to 2017 – according

to data from the NBS. The increase has been one p.p. above

the 10 percent forecasted by the German Chamber of

Commerce in China.1

According to online recruitment platform Zhaopin.com, the

annual salary in China averaged RMB 96,000 in the first

quarter of 2019: a 5.5 percent increase in comparison with a

year ago, but a drop of 0.6 percent from the last quarter of

2018.2

The German Chamber of Commerce in China estimates for

2019 project a wage increase of 9.9 percent and an average

annual compensation of RMB 90,613. Projections are based

on the current context of slower domestic growth and

inflationary pressures.

China’s per capita disposable income averaged RMB 15,294

year in the first six months of 2019, an increase of 8.8

percent YoY in nominal terms, according to preliminary

accounting results published by the NBS in July 2019.3 Since

inflation in China was at 2.7 percent YoY in June 2019, the

increase in real terms on per capita disposable income was

6.1 percent. The per capita disposable income of urban

households (RMB 21,342) represented 2.7 times that of rural

households (RMB 7,778).

11.9

10.1 9.5 10.1

8.910.0 11.0

9.9

14.0

13.6

11.610.2

8.57.8 7.6 6.4

20.2

17.0

13.112.4 12.8

10.7 11.2

8.6

2012 2013 2014 2015 2016 2017 2018 2019*

In partnership with

18

Labor Market

2019 | 2020& Salary Report

BR

IEF

Source: NBS & German Chamber of Commerce in China analysis.* 2019 Regional wage developments estimates.

2. Provincial Wage Developments

The most significant wage increases took place in Central

China regions (Shanxi, Anhui, Jiangxi, Henan, Hubei, and

Hunan). According to the latest official data available, the

overall increase for Central China regions was 12.7 percent in

2018. In 2017, Central China also claimed the highest wage

increase (10.7 percent). Contrary to what it might look based

on the developments for 2017 and 2018, the average salary

increase in Central China during the six years from 2013 to

2018 (9.5 percent) is lower than that of West (10.4 percent)

and East (9.7 percent) China regions.4

For the third consecutive year, Northeast China (Liaoning,

Jilin, and Heilongjiang) register the lowest wage increase: 8.9

percent, in 2018. It remains the region with the lowest

annual salaries (RMB 65,411). This is 0.70 times the average

compensation in East China, which is the highest paying

region (annual salary of RMB 93,253 in 2018, and an

estimated RMB 102,324 for 2019).

Since 2011, using East China as the baseline, only West

regions have produced salary increases closing the relative

gap in compensation: from West China salaries being 0.77

times those of the East in 2011, to be 0.81 in 2018. Central

China compensation in 2011 was 0.74 times that of East

China, the same proportion as in 2018. Northeast regions

have seen an increase in their compensation gap towards

East China during 2011 to 2018: the average compensation

in Northeast was 0.72 times that of the East in 2011,

whereas it was 0.70 times by 2018.

For an assessment of wage increases at the province level, an

overview is provided in the graph Average Wage Developments

by Province, which combines official data increases from 2014

to 2017 with projected increases for 2018 and 2019. Apart

the average increase for Tibet (addressed in detail in the 11th

Edition of the Salary Report),5 from the eleven provinces with

increases above China’s average, six are from Western China

(Yunnan, Guangxi, Guizhou, Gansu, Qinghai, and Tibet). The

other provinces are Hainan, Hebei, and Guangdong (which

includes Shenzhen and Guangzhou) in the East, and Hubei

and Hunan in Central China.

Wage Growth by Region (%)

2011-2019. Nominal Growth

Central, North East and West China Compensation

As Factor of East China’s Compensation 2011-2018

Source: NBS & German Chamber of Commerce in China analysis.

Average Wage Developments by Province (%)

2014-2019

West Central East =1Northeast

0.7

7

0.7

9

0.8

0

0.8

0

0.8

1

0.8

1

0.8

1

0.8

1

0.7

4

0.7

5

0.7

3

0.7

3

0.7

2

0.7

2

0.7

2

0.7

4

0.7

2

0.7

3

0.7

4

0.7

2

0.7

2

0.7

1

0.7

0

0.7

0

2011 2012 2013 2014 2015 2016 2017 2018

Source: NBS & German Chamber of Commerce in China analysis. According to data from the NBS

salary growth in Tibet in 2015 was 59.8%, due to a one-time transference of RMB 132.09 billion on

the 50th anniversary of the establishment of Tibet Autonomous Region, resulting in the region topping

the ranking of regional wage developments.

13.0

11.6

11.1

10.9

10.9

10.7

10.5

10.4

10.2

10.2

9.9

9.8

9.8

9.7

9.6

9.5

9.4

9.4

9.3

9.1

8.7

8.6

8.6

8.5

8.4

8.4

8.3

8.0

7.7

7.2

6.6

Tibet

Yunnan

Guangxi

Guizhou

Hainan

Hebei

Hubei

Hunan

Gansu

Guangdong

Qinghai

CHINA

Sichuan

Shandong

Jiangxi

Shanghai

Jilin

Zhejiang

Henan

Chongqing

Beijing

Tianjin

Fujian

Xinjiang

Ningxia

Heilongjiang

Jiangsu

Shaanxi

Anhui

Liaoning

Inner Mongolia

Shanxi

18.9

14.4

11.9

10.1 9.5 10.18.9

10.011.0

9.9

0%

4%

8%

12%

16%

2011 2012 2013 2014 2015 2016 2017 2018 2019*

West Central East ChinaNortheast

19

In partnership with

Labor Market

2019 | 2020& Salary Report

BR

IEF

3. Minimum Wages and Wage Guidelines

Wage guidelines are issued by provincial and local

governments, based on the economic development of the

regions they administer. They are not mandatory but meant

to provide a reference for wage increases by percentage over

base salary levels.6 Although the guidelines are supposed to

be published annually before the end of March, the reality is

that few local governments do. Publishing dates, when

guidelines are formulated, are usually pushed to the second

half of the year. For instance, 21 out of 31 provinces issued

wage guidelines in 2018. Of those, 14 were published in the

second half of the year.

At the time of this writing, only five provinces have issued

wage guidelines in 2019: Shanghai, and Shandong in East

China; Inner Mongolia, Shaanxi, and Xinjiang in West China.

For the first time, Shanghai issued recommended ranges and

not specific percentages, for the lower (minimum) guideline

and the reference (average) baseline: two percent to three

percent for the minimum tranche, and five to six percent for

the average. On March 2019, Shandong province issued its

guideline of seven percent for the average reference

(identical to that of 2018) but did not release guidelines for

the lower and upper tranches. Shaanxi kept the upper wage

guideline at 12 percent (same as last year) and reduced one

p.p. its minimum guideline (from three percent to two

percent), and 0.5 p.p. its average guideline (from 7.5 percent

to seven percent).

Additionally, China has a minimum wage system. In

opposition to wage guidelines, minimum wages are

mandatory. Although the system has been running since

1994, it was not enforced until 2004.

Like the wage guidelines, local governments issue minimum

wages. Those should be revised once every two years and

should stay between 40 to 60 percent of the region’s

average monthly salaries. In reality, minimum wages fall far

behind that. In 2019, in Shanghai and Beijing, the two areas

with the highest minimums, the minimum wages amount to

18.9 percent and 16.8 percent of the average salary

respectively. The closest provinces to meet such criteria were

Henan, where minimum wages were 34.7 percent of the

average compensation in 2019; and Heilongjiang where

minimum wages were 30.4 percent of the average salary. All

provinces considered, minimum wages represent 28 percent

of the minimum wage.7

In 2018, 15 provinces increased their minimum wages. By

August 2019, only four regions have issued minimum wage

rates this year: Beijing, Shanghai, Chongqing, and Shaanxi.

Other regions that are likely to put forward minimum wage

Wage Levels by Province

2017-2019. Average Monthly Wages, in RMB

Province 2017 2018* 2019* Factor**

Shanghai 10,816 11,959 13,102 1.74

Beijing 10,975 11,987 13,080 1.73

Tibet 9,068 10,672 12,686 1.68

Tianjin 7,878 8,585 9,336 1.24

Zhejiang 6,729 7,401 8,100 1.07

Guangdong 6,599 7,227 7,966 1.05

Jiangsu 6,522 7,117 7,712 1.02

Qinghai 6,308 6,956 7,666 1.02

Guizhou 5,983 6,689 7,433 0.98

Yunnan 5,759 6,505 7,349 0.97

Chongqing 5,907 6,485 7,085 0.94

Sichuan 5,785 6,387 7,015 0.93

Hainan 5,644 6,289 6,978 0.92

Ningxia 5,858 6,338 6,880 0.91

Shandong 5,673 6,252 6,865 0.91

Hubei 5,493 6,075 6,724 0.89

Xinjiang 5,661 6,160 6,688 0.89

Guangxi 5,318 5,953 6,641 0.88

Fujian 5,618 6,105 6,629 0.88

Gansu 5,281 5,861 6,472 0.86

Hunan 5,308 5,856 6,468 0.86

Hebei 5,253 5,794 6,425 0.85

Inner Mongolia

5,557 5,971 6,398 0.85

Shaanxi 5,432 5,901 6,394 0.85

Anhui 5,429 5,857 6,327 0.84

Jiangxi 5,119 5,620 6,165 0.82

Jilin 5,121 5,626 6,162 0.82

Liaoning 5,096 5,498 5,922 0.78

Shanxi 5,005 5,323 5,676 0.75

Heilongjiang 4,672 5,095 5,524 0.73

Henan 4,625 5,008 5,481 0.73

Source: German Chamber of Commerce in China analysis based on 2017 NBS data. *2018 and 2019 are

estimates considering GDP growth, inflation and wage increases in the past. ** Factor represents the

ratio of regional wage to national average for 2019. Monthly wages, based on 12-months year basis; all

wages are pre-tax.

Regional Wage Increase Guidelines 2019 (%)

Province Minimum Average Maximum

Shanghai 1 2.0 - 3.0 5.0 - 6.0 -

Inner Mongolia 2 - 7.5 11.0

Shandong 3 - 7.0 -

Shaanxi 2.0 7.0 12.0

Xinjiang 2.0 5.0 8.0

Average 2.2 6.4 10.3

Average 2018 4 3.2 7.6 11.8

Average 2017 3.0 7.8 12.2

Source: German Chamber of Commerce in China research and analysis. Annual averages for each tranche

are calculated based on regional adjustments identified during the year. Data as of 13 August 2019. 1.No

maximum increase guideline issued for Shanghai; 2.No minimum increase guideline issued for Inner

Mongolia; 3. No maximum and minimum increase guidelines issued for Shandong; 4.The 2018 average

includes all 17 provinces that issued new guidelines that year: five of them updated after the publication of

the last year’s Labor Market and Salary Report 2018/19. Therefore, data in the table for 2018 differs slightly

from the averages presented in last year’s report.

In partnership with

20

Labor Market

2019 | 2020& Salary Report

BR

IEF

Region ClassLast

Increase*

A B C D E F (%) Valid since

Beijing 2,200 - - - - - 3.8 Jul 2019

Tianjin 2,050 - - - - - 4.9 Jul 2017

Hebei 1,650 1,590 1,480 1,380 - - 12.5 Jul 2016

Shanxi 1,700 1,600 1,500 1,400 - - 5.4 Oct 2017

Inner Mongolia 1,760 1,660 1,560 1,460 - - 8.1 Aug 2017

Liaoning 1,620 1,420 1,300 1,120 - - 7.6 Jan 2018

Jilin 1,780 1,680 1,580 1,480 - - 18.1 Oct 2017

Heilongjiang 1,680 1,450 1,270 - - - 15.5 Oct 2017

Shanghai 2,480 - - - - - 2.5 Apr 2019

Jiangsu 2,020 1,830 1,620 - - - 14.7 Aug 2018

Zhejiang 2,010 1,800 1,660 1,500 - - 8.4 Dec 2017

Anhui 1,550 1,380 1,280 1,180 - - 2.3 Nov 2018

Fujian 1,700 1,650 1,500 1,380 1,280 - 19.9 Jul 2017

Jiangxi 1,680 1,580 1,470 - - 10.1 Jan 2018

Shandong 1,910 1,730 1,550 - - - 5.5 Jun 2018

Henan 1,900 1,700 1,500 - - - 17.1 Oct 2018

Hubei 1,750 1,500 1,380 1,250 - - 13.2 Nov 2017

Hunan 1,580 1,430 1,280 1,130 - - 12.9 Jul 2017

Guangdong 2,150 1,720 1,550 1,410 - - 6.2 Jul 2018

Guangxi 1,680 1,450 1,300 - - - 19.8 Feb 2018

Hainan 1,670 1,570 1,520 - - - 17.8 Dec 2018

Chongqing 1,800 1,700 - - - - 20.7 Jan 2019

Sichuan 1,780 1,650 1,550 - - - 20.4 Jul 2018

Guizhou 1,680 1,570 1,470 - - - 4.9 Jul 2017

Yunnan 1,670 1,500 1,350 - - - 9.0 May 2018

Tibet 1,650 - - - - - 17.9 Jan 2018

Shaanxi 1,800 1,700 1,600 - - - 7.6 May 2019

Gansu 1,620 1,570 1,520 1,470 - - 10.8 Jun 2017

Qinghai 1,500 - - - - - 19.1 Jun 2017

Ningxia 1,660 1,560 1,480 - - - 12.2 Oct 2017

Xinjiang 1,820 1,620 1,540 1,460 - - 10.4 Jan 2018

Shenzhen 2,200 - - - - - 3.3 Jul 2018

Minimum Wage Rates in China 2018

Source: Provincial Human Resources and Social Security Bureaus and German Chamber of Commerce in China analysis. “Class” refers to different wage districts or jurisdictions within a province. Local governments are responsible for setting minimum wages. *Increases are calculated as the average increases of adjustments for all categories in the region. With the exception of Shenzhen, only provinces and province-level municipalities set minimum wage levels.

increases, since they have not done so in the past two years:

Fujian, Hunan, Gansu, Guizhou, Tianjin, Qinghai,

and Zhejiang.8

Among the regions that have introduced minimum wage

increases this year, Chongqing presents the highest increase:

20.7 percent. Minimum wages had not been updated in

Chongqing since 2016. Minimum wages in Chongqing are

established for two different groups of districts: districts in

class A have seen minimum wage increasing from RMB 1,500

/ month to RMB 1,800 / month; districts in class B have gone

from RMB 1,400 / month to RMB 1,700 / month.9

Shanghai rose its minimum wage 2.5 percent in April, from

RMB 2,420 / month to RMB 2,480 / month; Beijing

increased it by 3.8 percent, from RMB 2,120 / month to

RMB 2,200 month. As opposed to Chongqing, minimum

wages in Shanghai and Beijing were updated just a year ago.

21

In partnership with

Labor Market

2019 | 2020& Salary Report

BR

IEF

Source: NBS. * Factor represents the ratio of INDUSTRY-specific average wage to national average wage for 2018. Monthly wages, based on 12-months year basis; all wages are pre-tax.

4. Wages by Industry and Ownership

In 2016, IT overtook finance services as the highest paying

industry in China and has remained at the top spot since

then. With an average monthly compensation of RMB

12,307 last year, IT grew 10.9 percent compared to 2017

and also put an additional distance with finance services’

compensation. Upward pressure on IT salaries remains as

China rises in becoming a global hub for technology which

leads to an increasing demand for IT professionals.

The mining industry registered with 17.2 percent the most

substantial wage increase in 2018. That is 2.4 p.p. above the

growth experienced by the industry the previous year, and

6.2 p.p. above the overall average increase in China in 2018

(eleven percent). As a consequence, wages in the industry

(RMB 6,786 / month) have practically caught up with China’s

average (RMB 6,872 / month).

The significant increases in the past two years in mining show

the industry is gaining momentum. Industrial profits increased

by 4.2 percent YoY during the first six months of 2019,

against a backdrop of a 2.4 percent decrease in overall

industry profits.10 Investment in fixed assets for the mining

industry grew 22.3 percent during the same period.11 China

approved more than RMB 45 billion worth of new coal

mining projects in 2018 after closing old coal mines to clean

up the environment. Furthermore, it produced 320.4 million

tons of coal in December 2018, the largest volume since

2015.11 China is also increasing mining efforts of rare earth

elements, for which it is already responsible for 71 percent of

the world’s production.13

Other relevant wage developments come from technical

services / R&D (14.4 percent increase), and retail &

wholesale (13.1 percent increase). The technical services /

R&D wage development is especially remarkable since it is

the third largest average compensation by industry in China:

RMB 10,279 / month in 2018. Despite being one of the

highest paying industries in China, wages are still growing at a

considerable pace at the technical services / R&D industry.

Similar to IT professionals, scientific researchers and technical

specialists are at the center of China’s advances in innovation

and subject to several tax exemptions. Since 2017, China

provides enterprises with a 75 percent bonus deduction for

qualifying R&D expenses, which applies as well to staff

costs.14

The most modest increases have been for transport &

logistics (4.6 percent, and average compensation of RMB

7,096 / month), hospitality services (5.5 percent, RMB 4,022

/ month), and finance services (5.7 percent, RMB 10,820 /

month – the second highest paying industry in China, after

IT). Additionally, wages in agriculture stagnated with a slight

Wage Developments by Industry 2018

Ranked Based on 2018 Wages

Industry 2017 2018Growth

(%)Factor*

IT 11,096 12,307 10.9 1.79

Finance Services 10,238 10,820 5.7 1.57

Technical Services, R&D 8,985 10,279 14.4 1.50

Utilities 7,529 8,347 10.9 1.21

Culture 7,317 8,218 12.3 1.20

Healthcare 7,471 8,177 9.4 1.19

Education 6,951 7,699 10.8 1.12

Transport & Logistics 6,685 7,448 11.4 1.08