La compliance in un’azienda multinazionale: innovare .... Installation and configuration 1. SoD...

48

Milano, 3 Ottobre 2013 Matteo E. Corsi Group IT Compliance & Security Officer La compliance in un’azienda multinazionale: innovare nonostante i controlli

Transcript of La compliance in un’azienda multinazionale: innovare .... Installation and configuration 1. SoD...

Milano, 3 Ottobre 2013

Matteo E. Corsi Group IT Compliance & Security Officer

La compliance in un’azienda multinazionale: innovare nonostante i controlli

L’implementazione di

sistemi di controllo:

3 progetti

3 storie di Profit & Loss

Sarbanes-Oxley attestation

(SOX)

Progetto A

4

DI CHE SI TRATTA?

SOX What: cos’è il Sarbanes Oxley Act

COSA COMPORTA?

A CHI SI APPLICA?

Il Sarbanes Oxley Act (SOX) è una normativa emessa nel Luglio 2002

negli USA a seguito degli scandali finanziari di alcune grandi

corporation come ENRON e WORLDCOM.

La normativa introduce la responsabilità penale e societaria in materia di

frodi oltre che un inasprimento delle pene per il Top Management delle

società che si rendono colpevoli di non fornire una rappresentazione

veritiera e corretta del bilancio.

Si applica a tutte le società americane e alle società di diritto estero quotate al NYSE (New York

Stock Exchange).

In particolare, le società quotate al NYSE come Luxottica sono interessate principalmente dalle

sezioni della normativa sulla:

Responsabilità Societaria (Corporate Responsability) – Section 302

Miglioramenti dell’informativa finanziaria – Section 404

5

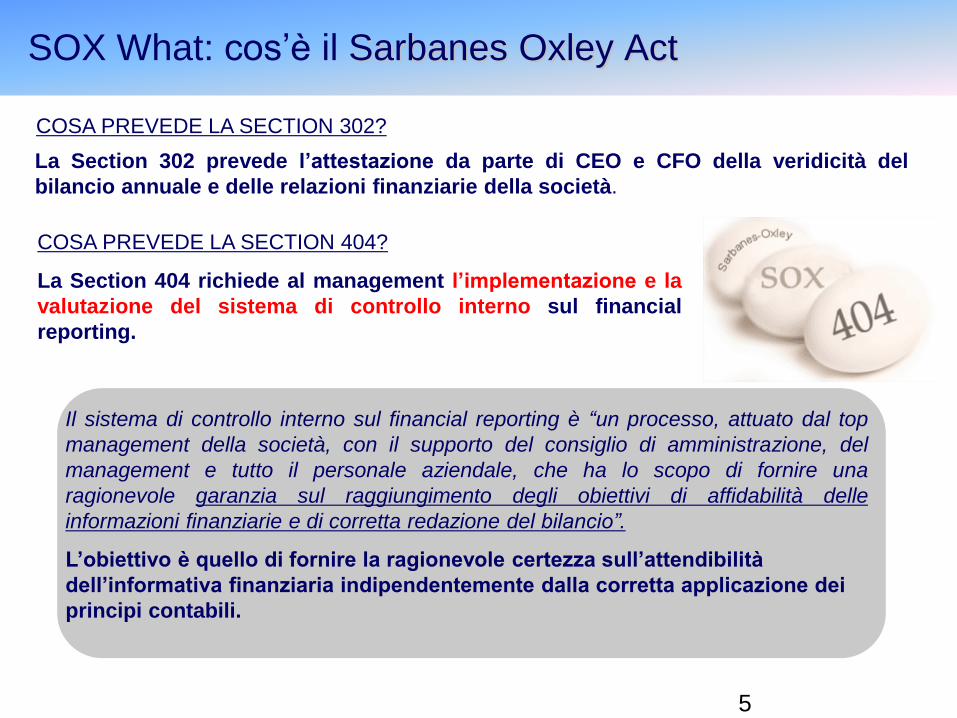

COSA PREVEDE LA SECTION 302?

COSA PREVEDE LA SECTION 404?

La Section 302 prevede l’attestazione da parte di CEO e CFO della veridicità del

bilancio annuale e delle relazioni finanziarie della società.

La Section 404 richiede al management l’implementazione e la

valutazione del sistema di controllo interno sul financial

reporting.

SOX What: cos’è il Sarbanes Oxley Act

Il sistema di controllo interno sul financial reporting è “un processo, attuato dal top

management della società, con il supporto del consiglio di amministrazione, del

management e tutto il personale aziendale, che ha lo scopo di fornire una

ragionevole garanzia sul raggiungimento degli obiettivi di affidabilità delle

informazioni finanziarie e di corretta redazione del bilancio”.

L’obiettivo è quello di fornire la ragionevole certezza sull’attendibilità

dell’informativa finanziaria indipendentemente dalla corretta applicazione dei

principi contabili.

6

1. Scoping : identificazione delle società e dei processi materiali ai fini SOX Rivisto

semestralmente

Marzo – Aprile 2012

Luglio2012-Marzo

2013

Luglio2012-Marzo

2013

2. Analisi del design dei controlli – WALK-THROUGH e

RAZIONALIZZAZIONE

4. Analisi del funzionamento dei controlli - TESTING

5. Identificazione “gap” e implementazione delle azioni correttive

7. Attestazione da parte del management

8. Attestazione da parte della società di revisione

Aprile 2013

Ottobre 2012 -

Aprile 2013 6. Condivisione dei risultati di test con la società di revisione e con l’Audit

Committee

Maggio - Giugno

2012 3. Analisi del design dei controlli con la società di revisione

SOX Profit: processo continuo

7

Con riferimento all’anno 2011, la metodologia ha individuato 16 società del Gruppo incluse nel

perimetro dell’analisi relativa al sistema di controllo interno sul financial reporting.

SOX Profit: progressione dei controlli

MCU (Material Control Unit) Valutazione del sistema di controllo a livello di processo tramite le RCM

(risk control matrix) e a livello entity tramite un questionario “Entity Level”.

SR (Specific Risk) Valutazione del sistema di controllo a livello di processo attraverso le RCM sui

processi rappresentativi del rischio della società in oggetto e a livello entity tramite un questionario “Entity

Level” con focus sui processi “risk”..

MWA (Material When Aggregated) Valutazione del sistema di controllo a livello di processo e a livello

entity attraverso un questionario “Entity Level” con focus sui processi rilevanti.

La valutazione del sistema di controllo interno è diversa a seconda di come è stata qualificata la società in

scope:

MCU - Material Control Units SR - Specific Risk Entities MWA - Material When Aggregated Entities

Luxottica Retail North America - Retail & dDistribution

Luxottica S.r.l.

Luxottica Italia S.r.l.

Luxottica Group SpA

Oakley Inc.

OPSM Group

Luxottica US Holdings Corp

Managed Vision Care

Luxottica USA LLC

Luxottica Iberica

Luxottica France

Luxottica Extra Limited

Luxottica Brasil

Luxottica Fashion Brillen

Luxottica Tristar Optical

Luxottica Trading and Finance Limited

8

No Material weakness (FY 06: > € 21.2 milioni).

5 Significant deficiency (FY 06: tra € 4.2 e € 21.2 milioni):

1. Income taxes Corporate – North America

2. Ciclo passivo – Corporate – Operation Italia

3. Segregation of duties – Corporate – Operations Italia

4. Non routines transactions – Corporate

5. Revenues recognition. –Retail North America

132 Control deficiencies (FY 06: < € 4.2 milioni) di cui 45 per Luxottica Srl e Group.

Il primo anno di compliance - 2006 - si concluse con la certificazione dell’adeguatezza del sistema di

controllo sul financial reporting secondo quanto previsto dalla SOX.

Sono però emerse le seguenti deficiencies:

SOX Profit: razionalizzazione & miglioramento

9

Nel corso di 6 anni l’Internal Audit insieme alle unità di business hanno proceduto ad una revisione del

sistema di controllo interno sui processi relativi alle SOCIETÀ ITALIANE DEL GRUPPO, razionalizzando i

controlli esistenti con l’obiettivo di renderli sempre più efficaci in linea con i cambiamenti organizzativi,

societari, di sistemi informativi e diminuire il peso di tutte le attività di controllo “a basso valore aggiunto”.

Tale attività ha portato a una riduzione del numero di controlli manuali e automatici di più del 43% (da

592 inseriti nelle matrici del 2006 a soli 338 del 2011).

Financial Closing 43 14 -29 -67%

Expenditure 52 25 -27 -52%

Fixed Asset 42 15 -27 -64%

Inventory 96 57 -39 -41%

Sales & Revenues 90 28 -62 -69%

Sales Commission 22 8 -14 -64%

Royalties 7 10 3 43%

Consolidated Financial closing* 37 57 20 54%

HR & Payroll 21 11 -10 -48%

Finance and Treasury 74 30 -44 -59%

Tax & Legal** 33 35 2 6%

IT OPERATIONS&NETWORK - CB 26 19 -7 -27%

IT COMPANY LEVEL CONTROLS - CA 19 14 -5 -26%

IT PROGRAM DEVELOPMENT - CC 30 15 -15 -50%

Totale complessivo 592 338 -254 -43%

* comprende Consolidated Financial Closing, Stock Option, Goodwill& Intangible

**comprende Tax&Legal, Consolidated Tax, Transfer Price

PROCESSO 20112006

Totale Controlli Delta

n° controlli %

SOX Profit: razionalizzazione & miglioramento

10

La valutazione del sistema di controllo interno sul financial reporting per il 2011 è la seguente:

0 MATERIAL WEAKNESS !!!!

L’assenza di MW comporta l’adeguatezza del sistema di controllo di LUXOTTICA sul financial reporting

secondo quanto previsto dal SARBANES OXLEY ACT – Section 404.

Ricordiamoci che se NON si implementano delle azioni migliorative una Control Deficiency può diventare

una Significant Deficiency e allo stesso modo una Significant Deficiency può diventare una Material

Weakness !

È necessario proseguire nel MIGLIORAMENTO CONTINUO

del nostro sistema di controllo!

Soglie di Materialità FY 2011:

Material Weakness > € 34,8 milioni

Significant Deficiency tra € 7 e € 34,8 milioni

Control Deficiencies < € 7 milioni

SOX Profit: misurabile

11

SOX Profit: automatizzabile

12

Gli ITAC (Automated Controls) sono stati divisi in 3 tipologie di controlli:

SOX Loss: automatico vs transitorio

13

SOX Profit: dettaglio informazioni

Presentazione Powerpoint 14

SOX Loss: maggiori risorse

Improved alignement with business needs via formally defined

communication channels (Authorisation workflow, keyusers

acceptance, scheduled meetings, interfunctional project teams)

Strenghtened software development procedure

Priority management (system differentiation & scalable procedure)

Risk management responsabilities may be properly assigned

(instead of rolling onto IT functions)

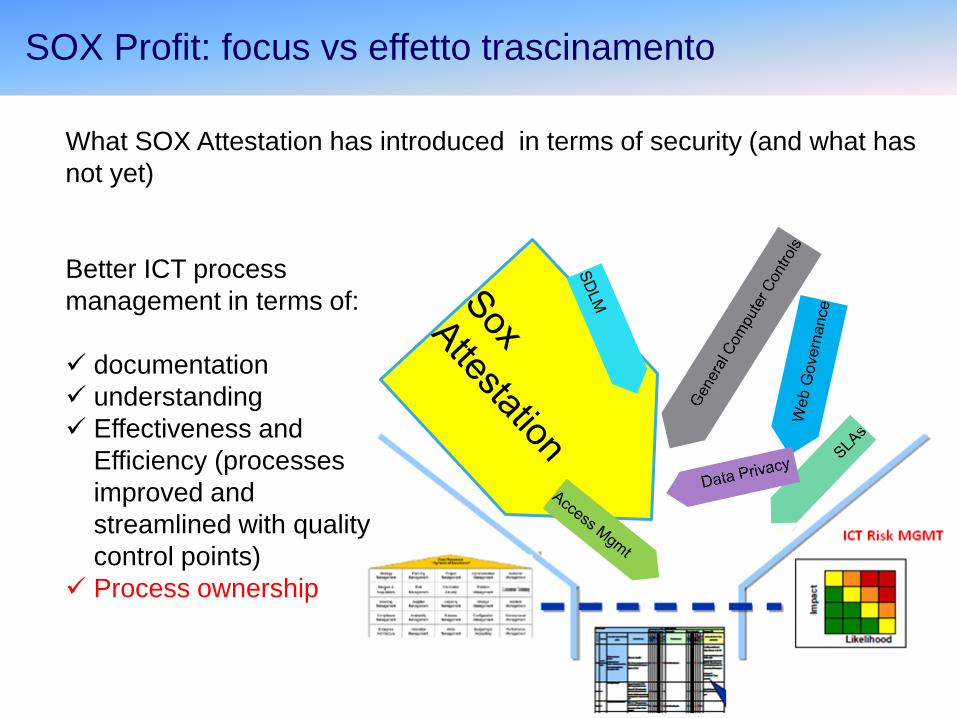

SOX P/L: trascinamento

What SOX Attestation has introduced in terms of security (and what has

not yet)

Better ICT process

management in terms of:

documentation

understanding

Effectiveness and

Efficiency (processes

improved and

streamlined with quality

control points)

Process ownership

SOX Profit: focus vs effetto trascinamento

What may be improved:

Process elements (Data, Risk, documentation mgmt) ownership

low frequency risks detection & management

Risk monitoring tools adoption ( to support risk mgmt

ownership)

Requirements surveying and monitoring (HIPPA, PCI-DSS, CT-

PAT, AEO...)

inclusion of not-financial objectives

SOX Loss: trascinamento

Gruppo CED Audit – lessons learned

Lack of a clear objectives: poorly defined and conflicting and changing

Management test (audit) requires detachment

Implement controls & procedures documentation deep involvement

Controls & procedures evangelization loneliness

Access to Production control (ChaRM) urgency/critical

SoD decisions in place of Business Process Owners Audit goal, not IT!

He’s becoming IT Help Desk’s Help desk (IT sprue) leading to quality

unbalances

Audit activities needs careful planning: overlapping and urgent/critical

tasks disrupt audit activities (Transport, ChaRM, User HelpDesk

Support, unplanned projects such Scissofusione)

Poor Standing

SOX Loss: dispersione delle risorse

Presentazione Powerpoint 19

A.Filling gaps:

SOX Profit: proporzionalità

Segregation of Duties

SoD

Progetto B

Agenda

• Structure of SAP user authorizations

• The project of role and user definitions in SAP

• Subsidiaries Roll-in and SSC

SoD What: implementing SAP and User Profiling

Transformation Program

2008-2011

SoD Profit: lo strumento SAP GRC

SoD Profit: lo strumento SAP GRC

2. Installation and configuration

1. SoD Matrix definition

3. Defining role and profiles

4. Training and Test

5. Training and Go-Live 6. Support & Follow up

Finalizzazione e approvazione SoD Matrix standard

Completamento configurazione Suite

Completamento definizione ruoli e profili per test

Test

Training

Go Live

1

2

3

4

Milestones:

5

6

Piano originale

Piano effettivo

Milestone

Forecast

Activities substantially completed

Stage of Assistance and training completed

%

di avanzamento

Consuntivo Pianificato

90%

90%

100%

90%

100%

0%

100%

100%

95%

100%

0%

100%

Milestone effettiva

2008

MAR APR MAG GIU LUG AGO SET OTT NOV DEC JAN FEB MAR

2009

1

2

4 5

6

Profilazione e Implementazione SAP GRC

3

Oggi: 24/03/2009

2

1

SoD Profit: lo strumento SAP GRC

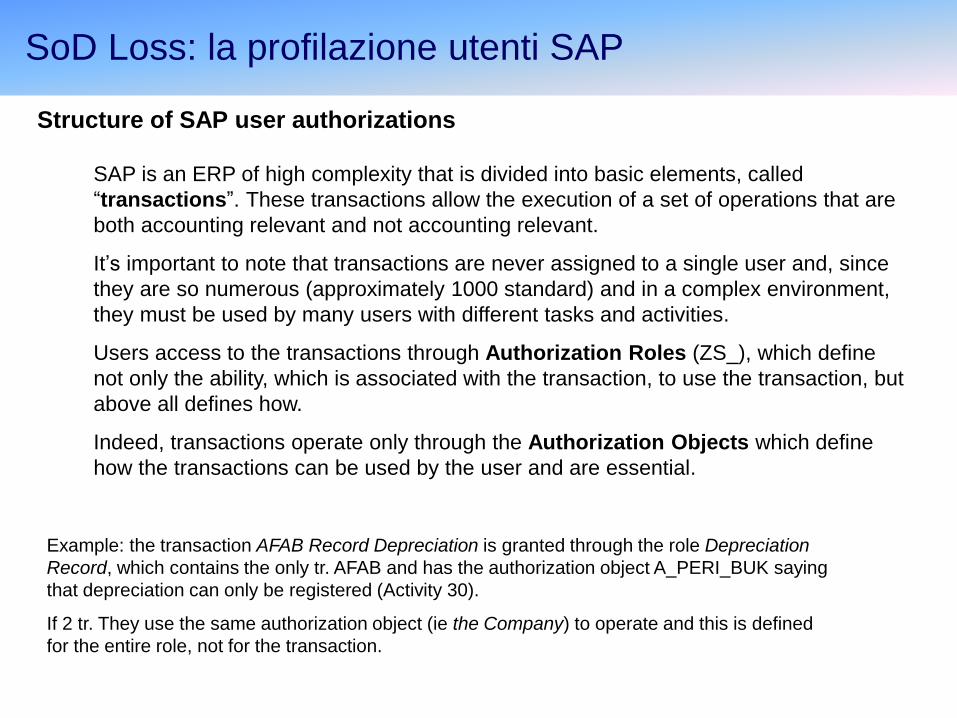

SAP is an ERP of high complexity that is divided into basic elements, called

“transactions”. These transactions allow the execution of a set of operations that are

both accounting relevant and not accounting relevant.

It’s important to note that transactions are never assigned to a single user and, since

they are so numerous (approximately 1000 standard) and in a complex environment,

they must be used by many users with different tasks and activities.

Users access to the transactions through Authorization Roles (ZS_), which define

not only the ability, which is associated with the transaction, to use the transaction, but

above all defines how.

Indeed, transactions operate only through the Authorization Objects which define

how the transactions can be used by the user and are essential.

SoD Loss: la profilazione utenti SAP

Example: the transaction AFAB Record Depreciation is granted through the role Depreciation

Record, which contains the only tr. AFAB and has the authorization object A_PERI_BUK saying

that depreciation can only be registered (Activity 30).

If 2 tr. They use the same authorization object (ie the Company) to operate and this is defined

for the entire role, not for the transaction.

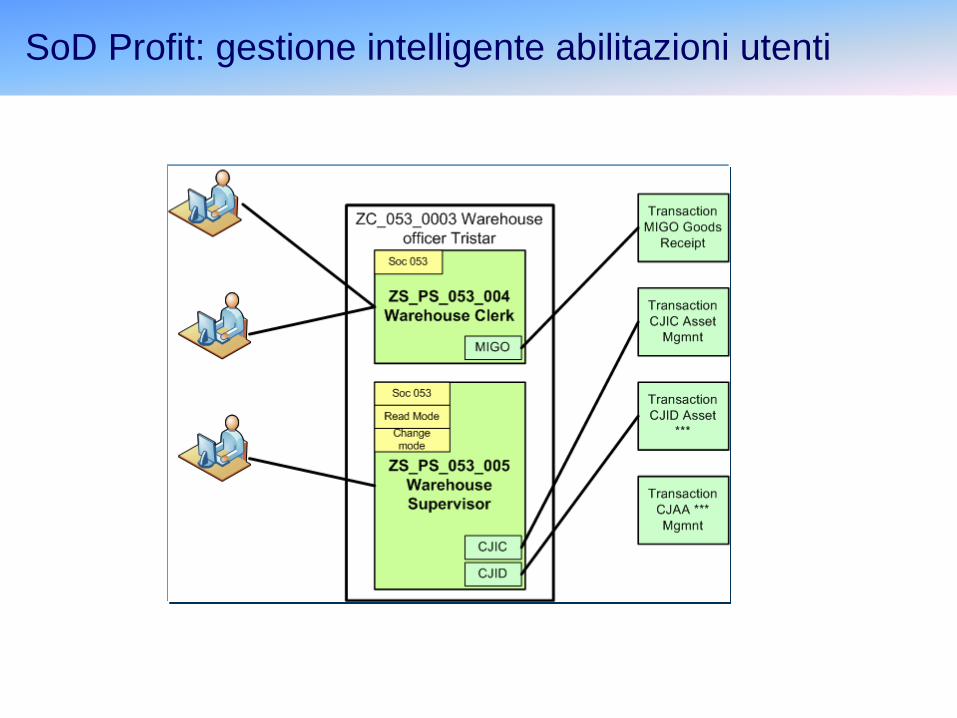

Structure of SAP user authorizations

SoD Profit: gestione intelligente abilitazioni utenti

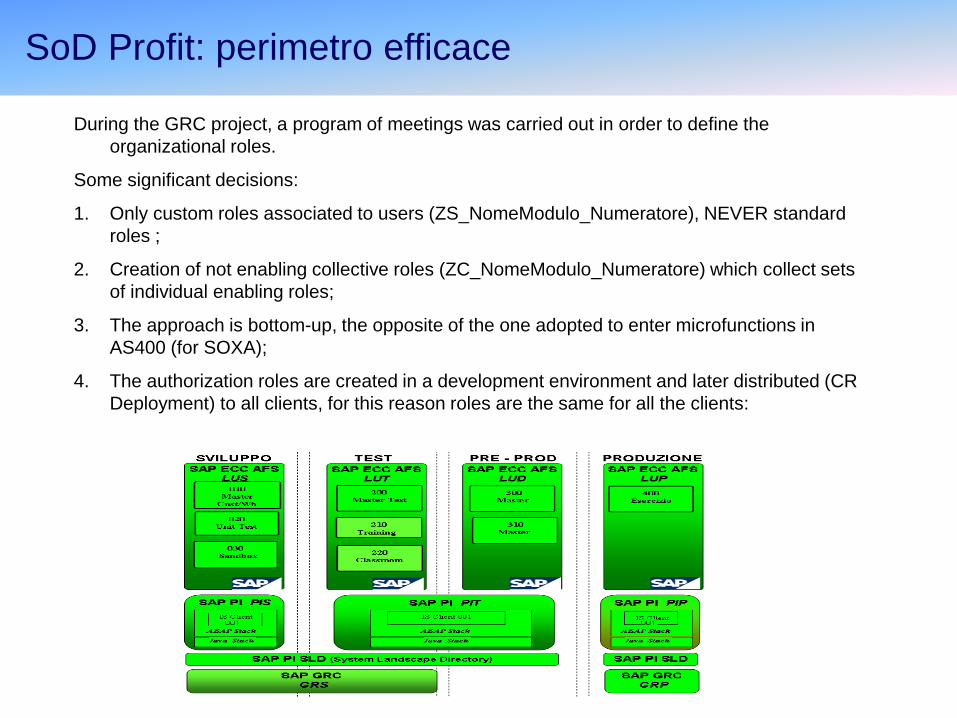

During the GRC project, a program of meetings was carried out in order to define the

organizational roles.

Some significant decisions:

1. Only custom roles associated to users (ZS_NomeModulo_Numeratore), NEVER standard

roles ;

2. Creation of not enabling collective roles (ZC_NomeModulo_Numeratore) which collect sets

of individual enabling roles;

3. The approach is bottom-up, the opposite of the one adopted to enter microfunctions in

AS400 (for SOXA);

4. The authorization roles are created in a development environment and later distributed (CR

Deployment) to all clients, for this reason roles are the same for all the clients:

SoD Profit: perimetro efficace

SAP GRC Compliance User Provisioning introduction

LUXOTTICA – Creazione nuovo ruolo in SAP – Overview Processo

TB

DT

BD

IT C

ompl

ianc

eIT

Com

plia

nce

Hel

p D

esk

Hel

p D

esk

Res

pons

abile

auto

rizza

to

Res

pons

abile

auto

rizza

to

No

SI

SI

NO

Implementazione

nuovo ruolo su

SAP (ambiente di

sviluppo) da ERM

Modifica autorizzata?

Controllo impatti

SoD in Enterprise

Role Management

Analisi conflitti e

individuazione

possibili soluzioni

Esistono conflitti?

End

Start

Invio richiesta

attraverso HDA

Chiusura ticket e

invio mail al

richiedente

Analisi richiesta e

individuazione

modifiche da

eseguire

Approvazione

nuovo ruolo su

Enterprise Role

Management

Rifiuto della

richiesta su

Enterprise Role

Management

Inserimento dati in

Enterprise Role

Management

Trasporto in

ambiente di test e

produzione

MS Excel con

Ruoli e Profili

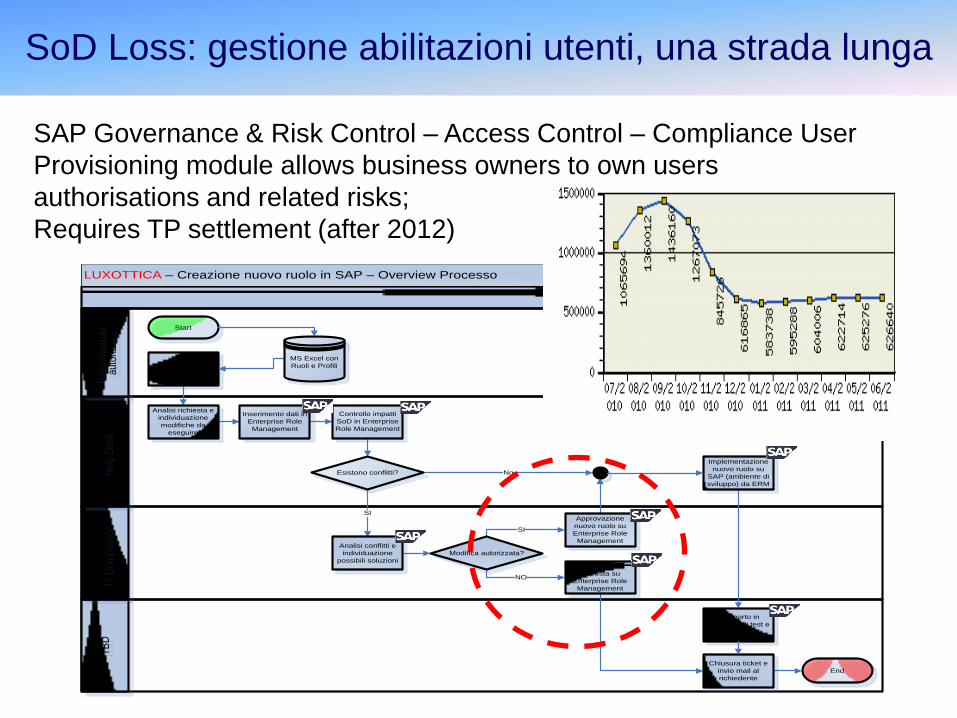

SAP Governance & Risk Control – Access Control – Compliance User

Provisioning module allows business owners to own users

authorisations and related risks;

Requires TP settlement (after 2012)

SoD Loss: gestione abilitazioni utenti, una strada lunga

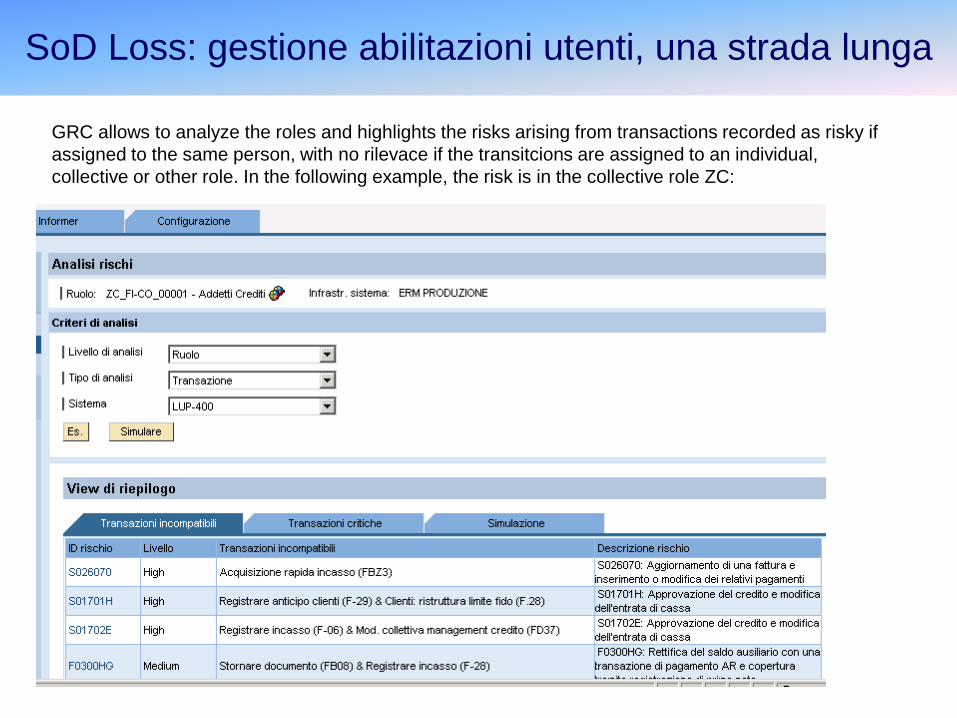

GRC allows to analyze the roles and highlights the risks arising from transactions recorded as risky if

assigned to the same person, with no rilevace if the transitcions are assigned to an individual,

collective or other role. In the following example, the risk is in the collective role ZC:

SoD Loss: gestione abilitazioni utenti, una strada lunga

SAP GRC (formerly Virsa) is an additional module that supports the process of managing access and

authorizations, and it consists of 4 modules:

SoD Loss: gestione abilitazioni utenti, una strada lunga

The definition of authorization roles (ZS) has been realized taking into account

conflicting requirements:

On the one hand:

1. Ensuring users with the necessary authorizations to perform their work , primarily to

grant authorizations according to SOXA assessment (i.e. Control Model ); secondarily

refining progressively the authorizations

2. Reducing as much as possible the sheer number of authorization roles to manage

On the other hand:

1. Implementing the Segregation of Duties to support controls (automatic) previously

defined in the Risk Control Matrix (SOXA) in order to reduce the control risks

2. Reducing control risks using Automatic Controls in palce of Manuals ones (leaner and

more reliable)

3. Implementing management requirements ( "vertical segregation”): for example, each

controller manages only its own cost center, and not the others.

SoD Loss: processi integrati

Luxottica User Management has been integrated with SAP User Management.

› The Authorization Management of entitlements is assigned to the Information Systems, which

require for the implementation of the Internal Control Model informations and settlements from

Process Owners (which can be neither IA or IT)

› The Control Owners test periodically the controls. The Process Owners define the Control and

ensure compliance, effectiveness and efficiency.

SoD Loss: accountability & ownership

LUXOTTICA – Creazione nuovo ruolo in SAP – Overview Processo

TB

DT

BD

IT C

om

plia

nce

IT C

om

plia

nce

He

lp D

esk

He

lp D

esk

Re

sp

on

sa

bile

au

torizza

to

Re

sp

on

sa

bile

au

torizza

to

No

SI

SI

NO

Implementazione

nuovo ruolo su

SAP (ambiente di

sviluppo) da ERM

Modifica autorizzata?

Controllo impatti

SoD in Enterprise

Role Management

Analisi conflitti e

individuazione

possibili soluzioni

Esistono conflitti?

End

Start

Invio richiesta

attraverso HDA

Chiusura ticket e

invio mail al

richiedente

Analisi richiesta e

individuazione

modifiche da

eseguire

Approvazione

nuovo ruolo su

Enterprise Role

Management

Rifiuto della

richiesta su

Enterprise Role

Management

Inserimento dati in

Enterprise Role

Management

Trasporto in

ambiente di test e

produzione

MS Excel con

Ruoli e Profili

SoD Loss: accountability & ownership

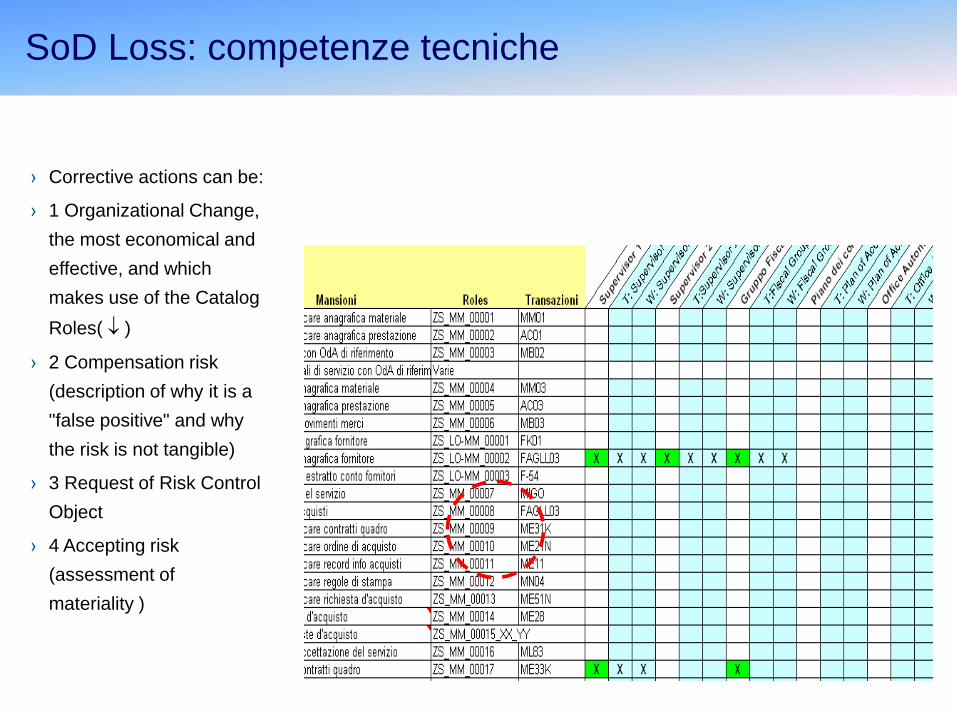

› Corrective actions can be:

› 1 Organizational Change,

the most economical and

effective, and which

makes use of the Catalog

Roles( )

› 2 Compensation risk

(description of why it is a

"false positive" and why

the risk is not tangible)

› 3 Request of Risk Control

Object

› 4 Accepting risk

(assessment of

materiality )

SoD Loss: competenze tecniche

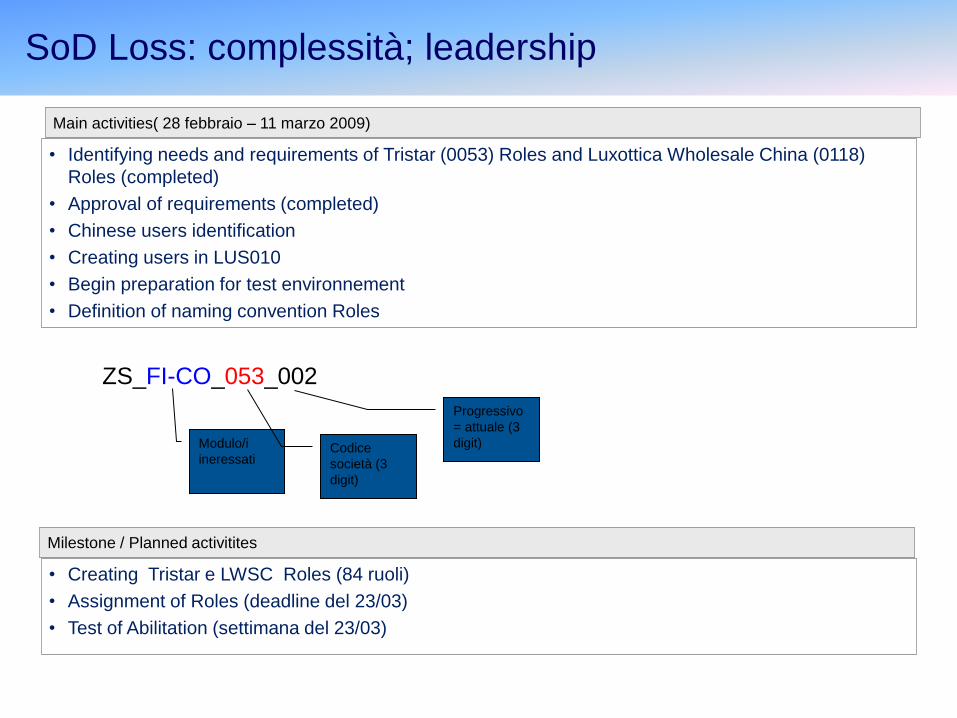

SoD Loss: competenze tecniche

• Identifying needs and requirements of Tristar (0053) Roles and Luxottica Wholesale China (0118)

Roles (completed)

• Approval of requirements (completed)

• Chinese users identification

• Creating users in LUS010

• Begin preparation for test environnement

• Definition of naming convention Roles

Main activities( 28 febbraio – 11 marzo 2009)

• Creating Tristar e LWSC Roles (84 ruoli)

• Assignment of Roles (deadline del 23/03)

• Test of Abilitation (settimana del 23/03)

Milestone / Planned activitites

ZS_FI-CO_053_002

Modulo/i

ineressati

Codice

società (3

digit)

Progressivo

= attuale (3

digit)

SoD Loss: complessità; leadership

SoD Loss: complessità: raccolta informazioni

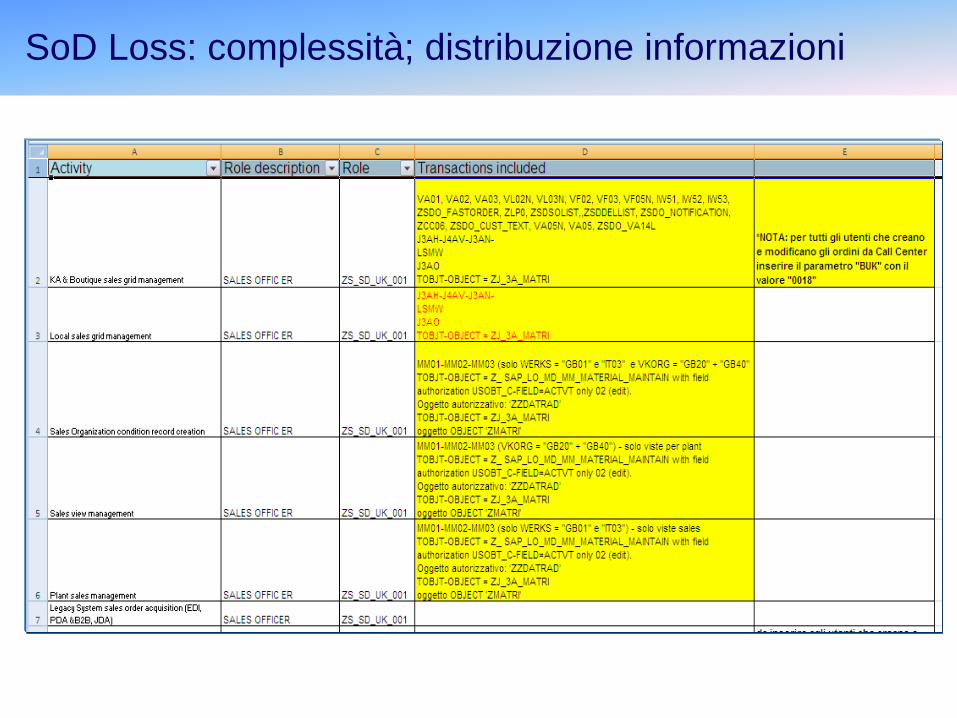

SoD Loss: complessità; distribuzione informazioni

Presentazione Powerpoint 39

PUNTO

APERTO

Gestione utenti SAP ruoli e

responsabilità

Pro (O) Contro (T)

Descrizione

Chi gestirà gli utenti SAP (creazione

utenti e assegnazione ruoli

autorizzativi)

Va

nta

gg

i (S

)

Abbiamo le risorse

Difficoltà di

comunicaizone lingua e

ritardo (time zone)

Soluzione 1 Lo staff cinese (Zanardo)

Co

sti

(W

)

I ticket devono essere

“indirizzati” completati

tradotti: chi lo fa e per

quanto?

Soluzione 2

Quando? <Q4/12

Showstoppe

rs

Zanardo è d’accordo?

Soluzione

Adottata

SoD Loss: complessità; distribuzione informazioni

40

Il Gruppo CED Audit svolgerà le seguenti funzioni:

Audit sui controlli IT

Creazione e manutenzione Ruoli Autorizzativi SAP (area azzurra) comprese l’avvio

nuove filia

La creazione utenti e l’associazione RA (area verde) sarà svolta da gdl in Cina + BMA

SOD Profit: cambiamenti organizzativi

Data Leakage Prevention

DLP

Progetto C

Presentazione Powerpoint 42

SAP GRC Compliance User Provisioning introduction SAP GRC Compliance User Provisioning introduction

Current status:

• Assessment of pilot department (Product

Development)

• Define Security Policies for Deployment

Print/Fax Copy/Paste Mobile Networks

Product Diagrams Confidential Data

Laptop Theft Wrongly Stored Data Removable Media

Social Security or Credit Card Numbers Price Lists

Customer List

Customer List

Project Objective Luxottica is developing a solution that can protect the data owned by Luxottica from threats as:

• Unlawful removal;

• Improper use;

• Illegal distribution

SOD What: Progetto Data Loss Prevention

Engineering

Dpt

SOD Loss: complessità

Kick-off 1 month 2 months 6 months

PILOT SCOPE

Definition, for the countries in scope (Italy, US and UK in this first part of project), of the supports to be used by country

DEVELOPMENT

Development of the training material and identification, if necessary, of specific e-learning IT tools

VIDEO

Recording of the video-presentation in order to give a worldwide overview of the Privacy Data Management project

COACHING

Identification, for the countries in scope, of the coaching needs. Planning and executing of the coaching sessions

NEWSLETTER

Development of a standard newsletter in order to give updates and spread news about privacy and data management

TRAINING/E-LEARNING

Training delivery (both online and live) for the countries in scope and eventual roll-out / go live of the e-learning platform

WORKSHOP

Organization of specific workshop (both online and live) with Legal Depts in order to aware the key people

Communication

/ Awareness

TIMELINE Protiviti offering

SOD Loss: comunicazione

Deployment in corso nell’Area Corporate Financial Reporting:

• Aggiornamento piattaforma

DLP 11.6.2

• Integrazione policy con

Prototyping

• Endpoint deployment

DLP Loss: perimetro flessibile

Conclusioni

Presentazione Powerpoint 47

Chiarezza obiettivi ma flessibilità nei mezzi

Grazie.