L1 a Changing India

50

Changing India: A Consumer & Retail Perspective

Transcript of L1 a Changing India

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 1/50

Changing India:

A Consumer & Retail Perspective

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 2/50

K ey Points

Overview of the retail sector.

Current Retail Channel

Impact Areas

The New Indian Consumer

The Emerging Indian consumer

Winnable Practices

Conclusion

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 3/50

Overview Of Indian Retail

Opportunity

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 4/50

Size of the economy

Fiscal Year GDP at current prices (US$

Billion)

2005-6 804

2009-10 1133

2014-15 1721

Sources

2006 GDP :Central Statistical Organization (CS0)

Growth Rates :Goldman Sach¶s BRIC report

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 5/50

GDP US$ 804 Bn

PrivateConsumption

US $482 Bn (60%)

RetailUS $300 Bn (62%)

Non-RetailUS $182 Bn (38%)

UrbanUS $135 Bn (45%)

RuralUS $165 Bn (55%)

..With high Private Consumption

India is a consumption led economy : Private Final Consumption Expenditure(PFCE) is 60% of the economy (as against 42% of China and 55% of Japan)

Source :Central Statistical Organization (CS0) and Technopak Analysis

Public Spendingand Gross CapitalFormation 40%

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 6/50

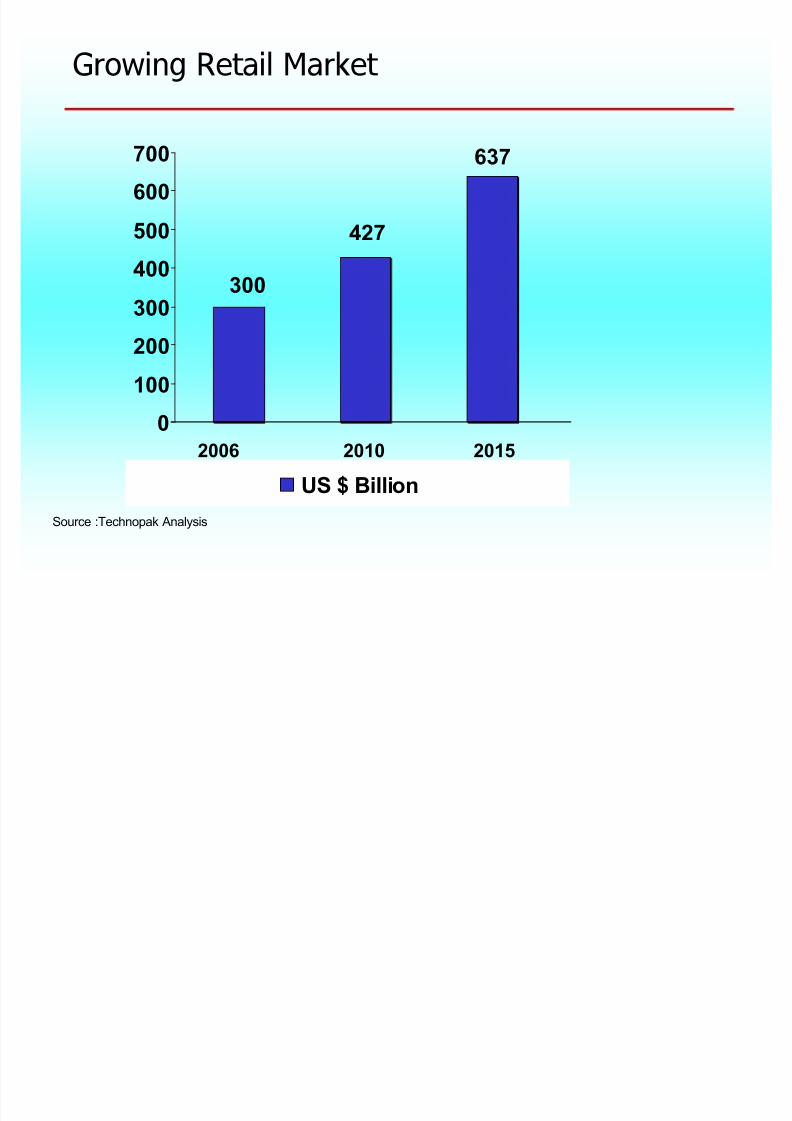

Growing Retail Market

300

427

637

0

100

200

300400

500

600

700

US $ Billion

2006 2010 2015

Source :Technopak Analysis

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 7/50

Retail Market : Rural/Urban Split

Almost half of retail market in 2006 is in ruralIndia; although share of urban market is

increasing by almost 5% every 8-10 years

Source :National Account Statistics; Monthly per capita Expenditure

and Technopak Analysis

% Split

Urban 45%

Rural 55%

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 8/50

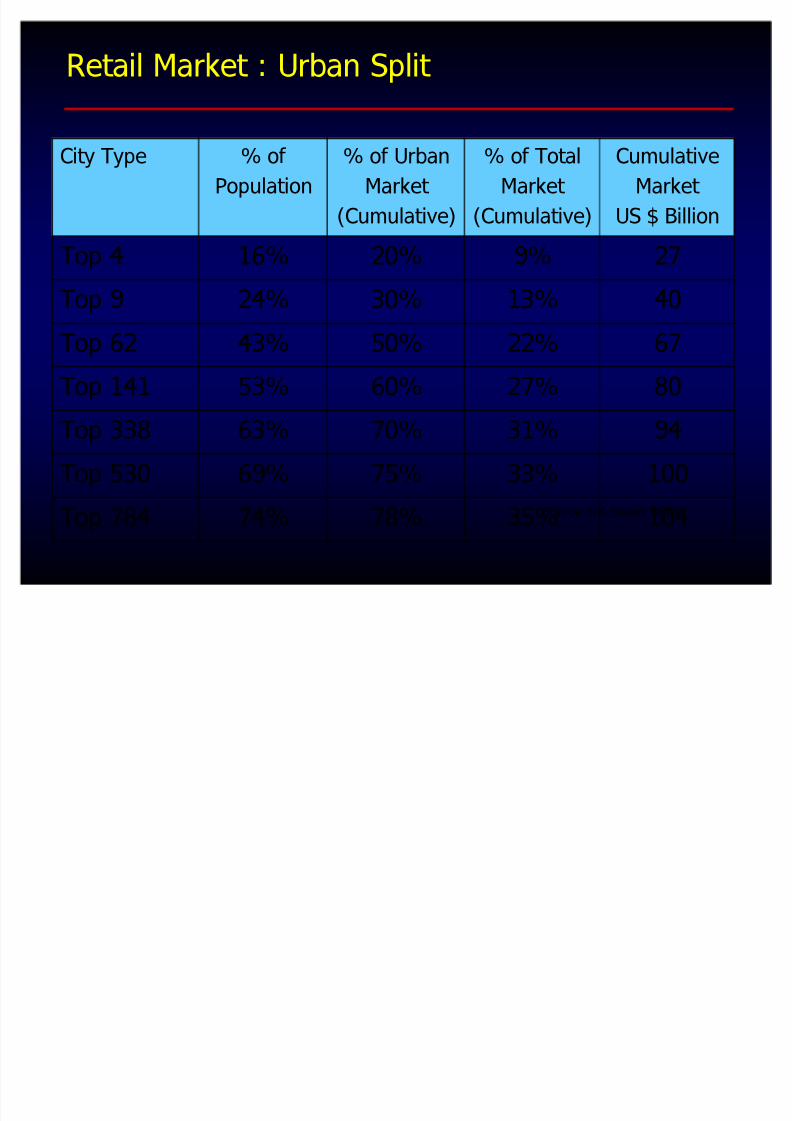

Retail Market : Urban Split

Source :RK Swami BBDO

City Type % of

Population

% of Urban

Market

(Cumulative)

% of Total

Market

(Cumulative)

Cumulative

Market

US $ Billion

Top 4 16% 20% 9% 27

Top 9 24% 30% 13% 40

Top 62 43% 50% 22% 67

Top 141 53% 60% 27% 80

Top 338 63% 70% 31% 94

Top 530 69% 75% 33% 100

Top 784 74% 78% 35% 104

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 9/50

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 10/50

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 11/50

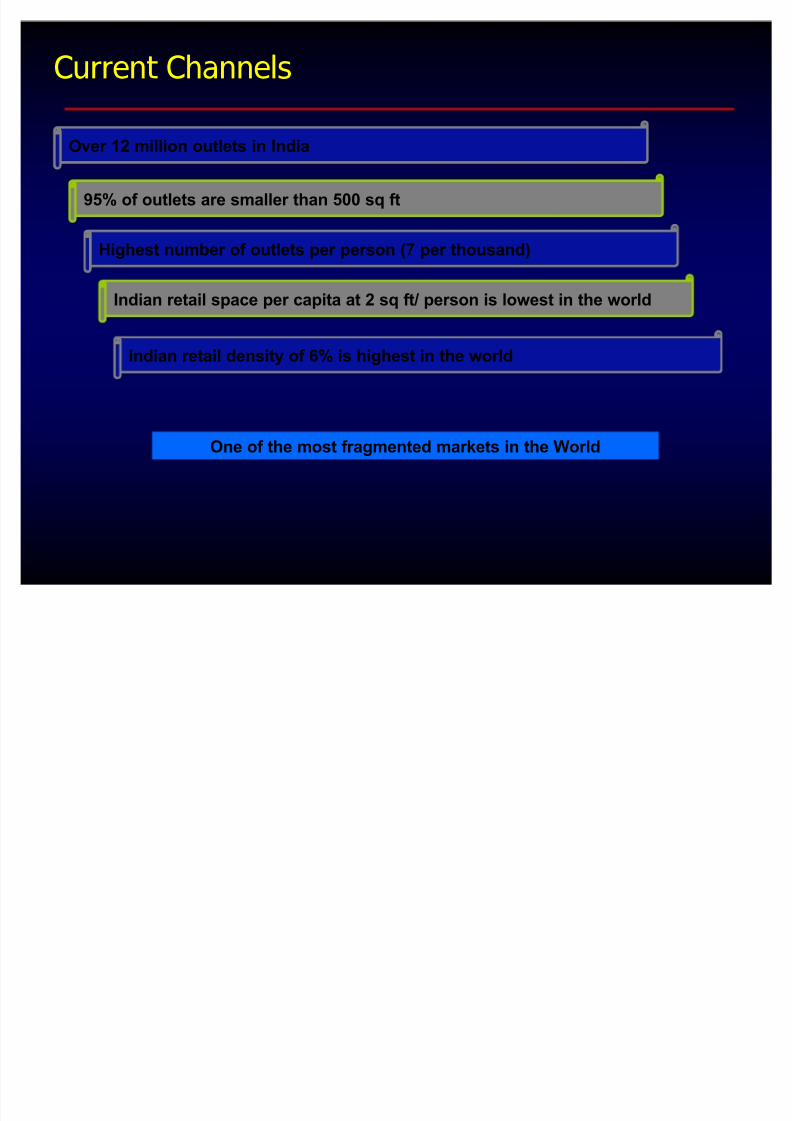

Current Channels

Over 12 million outlets in India

95% of outlets are smaller than 500 sq ft

Indian retail space per capita at 2 sq ft/ person is lowest in the world

Indian retail density of 6% is highest in the world

Highest number of outlets per person (7 per thousand)

One of the most fragmented markets in the World

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 12/50

The share of organized retail is less than 3% of the total retailmarket

The size of modern retail is about US$ 8 Billion and has grown by

35% CAGR in last five years

85% 81%

55%

40%36%

30%20% 20% 3%

0%

20%

40%

60%

80%

100%

US Taiwan Malaysia Thailand Brazil Indonesia Poland China India

Traditional Channel Modern Channel

Current Channels : Organized Retail

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 13/50

Market Size : US $ 8billion

Current Channels : Organized Retail

9%

17%

9%

3%5%1%7%7%

9%

20%

2%9%

2%

CD IT F&G Footwea r

Furn itu re Pha rmacy H ome improvement

Books a nd Music Jewe lle ry a nd W a tches Non store

R esta ura nt Appa re l E nterta inmen t

Misc Produ cts an d S ervices

Source: Technopak Analysis

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 14/50

Leading Players (Illustrative List) : Turnover

Name US $ Million

Future Group (Pantaloon) 444

Shoppers Stop 133

Landmark (Lifestyle) 80

Trent 53

Subhiksha 44

Vishal Mega Mart 25The above analysis does not include the specialty retailers like Bata, Titan and Tanishq

Source: myIRIS,Media and Technopak Analysis

The biggest players are small as yet !

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 15/50

Largest Retail Chains

Largest Retailers(number of stores)

Sector Retailer Number of stores

Public Distribution System 46300

Post offices 16000

Petrol Pump 1800

Defence Stores 3400

Footwear Bata 4700

Health and Beauty Care Shanaz 350

Apparel & Textiles Raymond 320

CafeCafé Coffee

Day200

Watches Titan 196

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 16/50

Rapid Transformation .

Investments in the range of US$ 20+ Billion expected in the next 5years in Retail & its Supply Chain alone

Size of modern retail likely to touch US$ 60+ Billion by 2011

At least 2.5 Million additional direct jobs likely to be created in the

next 5 years

Hyper-competition is expected to set in by 2008-9 as the footprint

of the top-5 players starts significant overlapping in top 20 30towns

Significant impact on other retailers and branded good players

creating new opportunities and threats

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 17/50

Impact Areas

Branded Consumer Goods Players

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 18/50

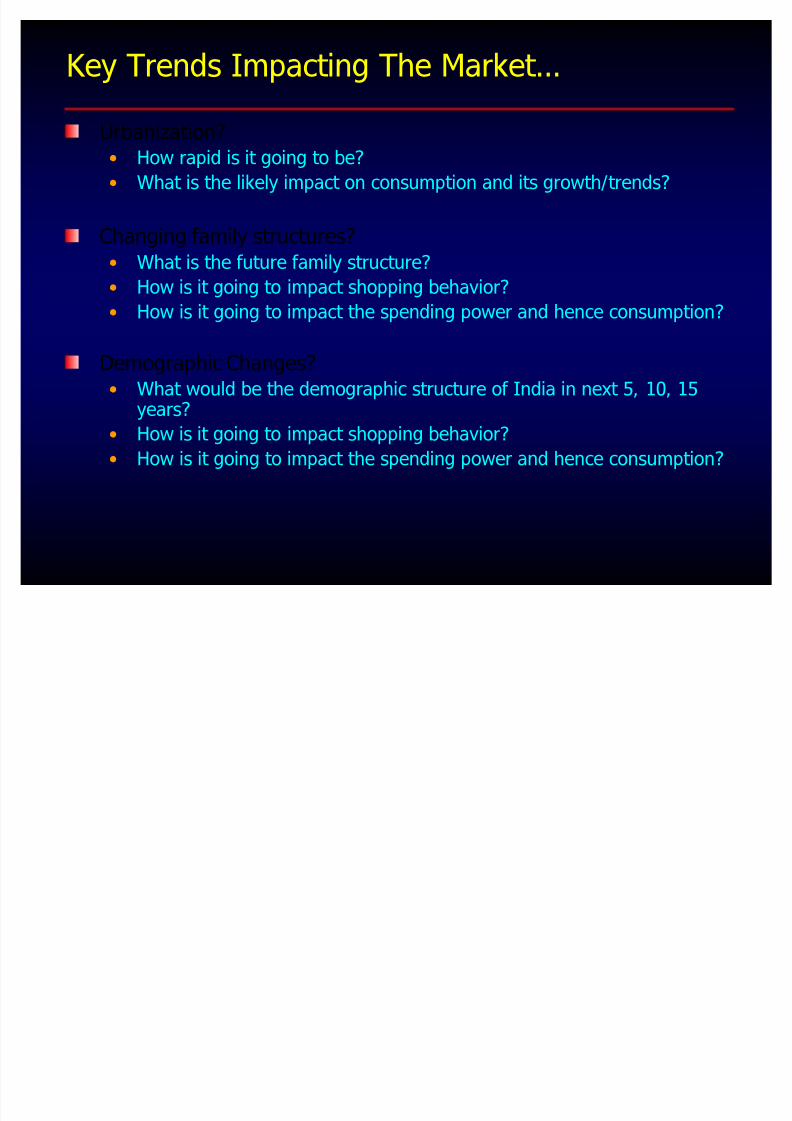

K ey Trends Impacting The Market

Urbanization? How rapid is it going to be?

What is the likely impact on consumption and its growth/trends?

Changing family structures? What is the future family structure?

How is it going to impact shopping behavior?

How is it going to impact the spending power and hence consumption?

Demographic Changes? What would be the demographic structure of India in next 5, 10, 15

years? How is it going to impact shopping behavior?

How is it going to impact the spending power and hence consumption?

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 19/50

The New Indian Consumer !

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 20/50

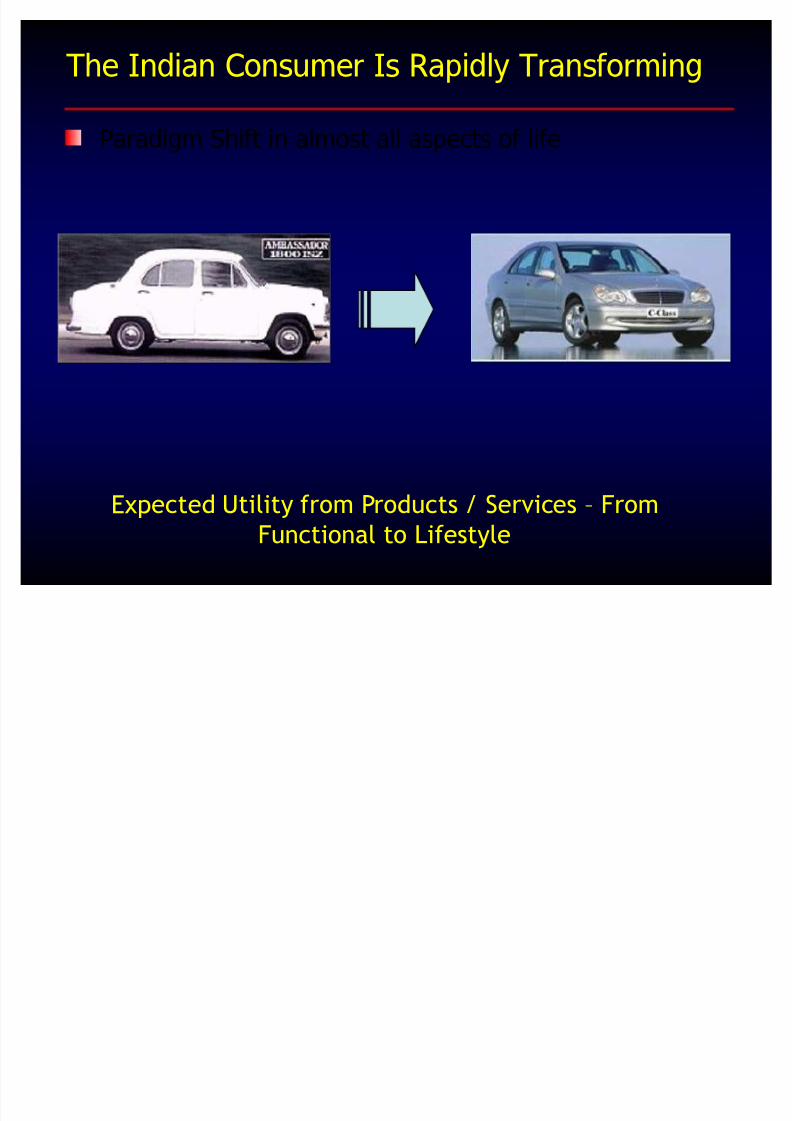

The Indian Consumer Is Rapidly Transforming

Outlook² From Traditional to Modernized Traditional

Paradigm Shift in almost all aspects of life

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 21/50

The Indian Consumer Is Rapidly Transforming

Expected Utility from Products / Services ² From

Functional to Lifestyle

Paradigm Shift in almost all aspects of life

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 22/50

The Indian Consumer Is Rapidly Transforming

Eating Habits ² From Traditional Meals to ´McAloo Tikkiµ

Paradigm Shift in almost all aspects of life

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 23/50

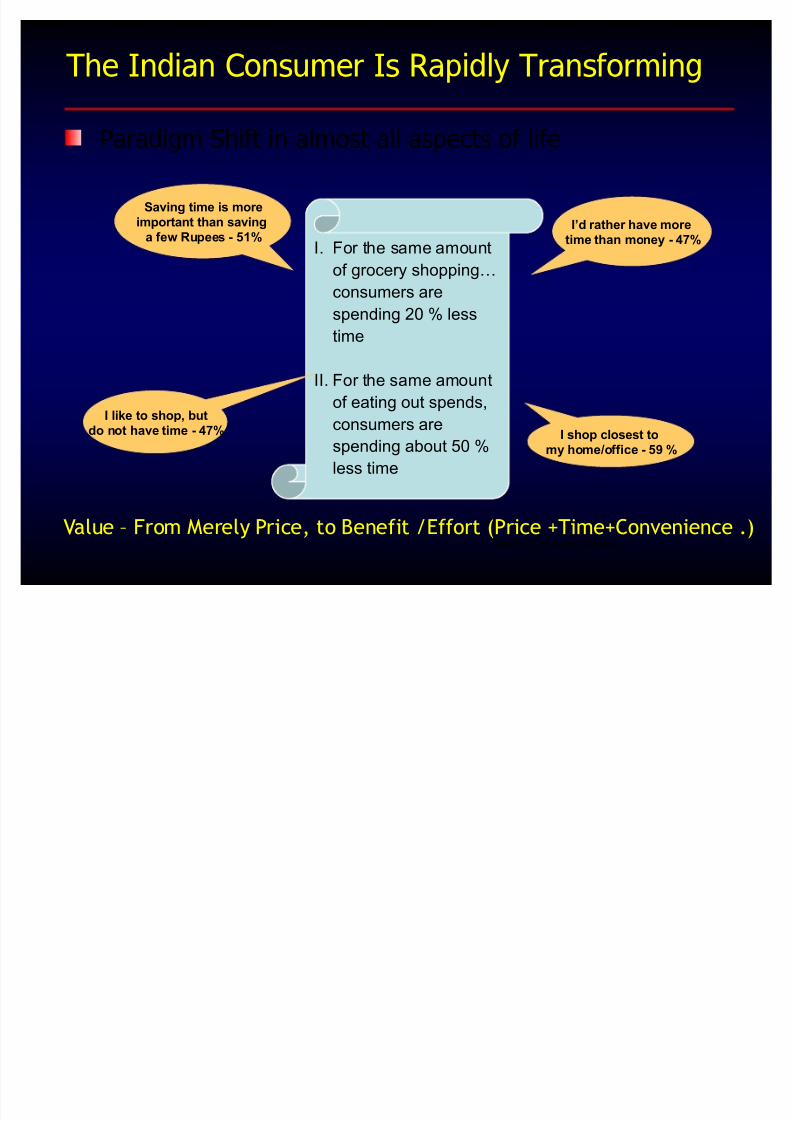

The Indian Consumer Is Rapidly Transforming

Value ² From Merely Price, to Benefit /Effort (Price +Time+Convenience .)

Paradigm Shift in almost all aspects of life

I. For the same amount

of grocery shopping«

consumers are

spending 20 % less

time

II. For the same amount

of eating out spends,

consumers are

spending about 50 %

less time

Saving time is moreimportant than saving

a few Rupees - 51%I¶d rather have more

time than money - 47%

I like to shop, butdo not have time - 47% I shop closest to

my home/office - 59 %

Sou

c¡

:¢

o£ ¤

um¡

Ou¥

look

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 24/50

The Indian Consumer Is Rapidly Transforming

Spending : From Denial to Indulgence

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 25/50

Spending On All Fronts: Herself, Her Family And Her Home..

MyselfApparel, footwear,accessories, books

& music

Entertainment,Movies and

theatre, eating out

My homeConsumer Durables,Appliances, home

textiles

My family

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 26/50

In View Of The Rapidly Expanding Spend Categories

1. Food and Grocery

2. Clothing

3. Footwear

4. Consumer durables

5. Home linen

6. Movies and theatre

7. Eating out

1991

1. Food and Grocery

2. Clothing

3. Footwear

4. Consumer durables

5. Expenditure on DVDs and VCDs

6. Home linen

7. Home accessories

8. Accessories9. Gifts

10. Take-away/ Pre cooked / RTE meals

11. Movies and theatre

12. Eating out

13. Entertainment parks

14. Mobile phones and service

15. Household help

16. Travel packages17. Club membership

18. Computer Peripheral & InternetUsage

2004 2010

1. Food and Grocery

2. Clothing

3. Footwear

4. Consumer durables

5. Expenditure on DVDs and VCDs

6. Home linen

7. Home accessories8. Accessories

9. Gifts

10. Take-away/ Pre cooked / RTE meals

11. Movies and theatre

12. Eating out

13. Entertainment parks

14. Mobile phones and service

15. Household help

16. Travel packages

17. Club membership

18. Computer Peripheral & Internet Usage

19. ???

20. ???

21. ???

22. ???Note: The above categories account for 80% of consumer spending

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 27/50

Two-faced Indian Consumers

Seeking upgradation in some categories & value in the others!

K ey issue for any retailer is to identify the upgrades and value-focused

product categories to rationalize the product mix and maintain healthy

margins

Consumer endsConsumer endsGrocery

Apparel

Eating Out

Upgrading

Mobile phones

Housing

Automobiles

Durables

Education

Seeking cheaper options

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 28/50

Implications

Profile of the Indian consumer is changing and so arethe aspirations and buying behavior

Consumer understanding and consumer orientation will

be one of the key drivers of future success

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 29/50

Transformation Driven ByMany Drivers .

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 30/50

Many Drivers

Demographics

Increased global exposure

Increased discretionary incomes across

wider spectrum of population, acrosswider geography

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 31/50

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 32/50

Global Exposure ..

Studying Abroad

Working Abroad

Traveling Abroad

Connected with Overseas

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 33/50

Increased Discretionary Spending ..

Multi-Income Households

Credit Friendly Households

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 34/50

.. However The Opportunities Are

Not Without The Challenges

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 35/50

Challenges

1. Growing movement towards Value Determining theRight Price Value Equation

2. Consumers looking for Solutions Developing

Consumer Centric Solutions

3. Rate of change shall be much faster than

beforeAdapting to the Changed World

4. Collision among the Channels, Categories & Variants

Retaining the Share of Wallet

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 36/50

Branded Consumer Goods Areas

At the mass market, most Indian consumers are brand-blankedthrough aspiring for brands (that can denote quality, trust, value)

Most major new entrants will start with heavy proportion of Private

Labels, and will probably use branded goods to demonstrate the

price value imbalance between such branded goods and their

private labels

Technopak believes that Branded good companies are in for some

surprises, and have to go back to the drawing board for strategy

learning from US and UK markets will not be of much use!

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 37/50

Impact Areas

Opportunities

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 38/50

Incredible Opportunities In The Supply Side

A new ecosystem of suppliers needed across diverseareas e.g.

Manufacturing

All categories of consumer goods

Store fit-outs and accessories e.g. shopping carts, packaging, etc.

Services

Entire gamut including IT, Logistics, Design (Store and Product),Communication, Promotions, HR recruitment and training et al

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 39/50

Fundamental Drivers Are In Place

Frenetic development of high quality retail space across India

Increased interest of Investors in funding Retail projects

Increased interest of International Brands & Retailers to

enter India

Exceptional response of Indian consumers to modern retail

options

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 40/50

Retailers Have Developed Profitable Businesses

Many strong regional and national players emerging acrossformats and product categories

Most have regained / improved profitability after going through

their respective learning curves indicating the viability of the

organized retailing across the formats

Most of these players are now geared to expand far more rapidly

than the initial years of starting up

With rapid roll out the Profitability shall further increase for

most of players as most of the central investments have

already been made

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 41/50

Where Are The Next Opportunities ?

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 42/50

Many Underexploited Opportunities

Specialty

Childrens Wear & Maternity (e.g. Mothercare)

Jewelry & Accessories (e.g. Tanishq)

Sari & Indian Ethnic Wear (e.g. Nalli) Intimate Wear (e.g. Victorias Secret )

Footwear ( Athletes Foot, Foot Locker)

Toys (e.g. Toys R Us)

Gifts and Artifacts ( e.g. K averi, Cottage Industries)

Nutrition / Health Maintenance (e.g. GNC)

Sports / Outdoor Lifestyle (e.g. REI, JJB Sports)

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 43/50

Opportunities In Indian Retailing

Food Services

Indian Fast Food

Family Diners (Indian style Plated or Combo meals)

Sandwich & Salad Parlors

Bread & Other Bakery Product Outlets

Multi-Cuisine Food Courts

Ice-cream & Juice / Beverage Parlors etc.

Indian Desserts & Snack Food Chains

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 44/50

Winnable Practices(In Indian Context)

Retailer Consumer Interface

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 45/50

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 46/50

Retail Consumer Interface

Availability

Right Product Right Size / Style / Color

Information

Signage

Speed of Service

Information

Check-Out

Return & Exchange Policy

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 47/50

Retail Operations

IT Enabled

Demand Forecasting

Merchandise Planning & Management

Replenishment Price Optimization

Efficiencies at POS

Dynamic Category / Brand Management

Private Label Strategy & Efficiencies

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 48/50

To Conclude .

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 49/50

Conclusion ..

Indian Consumer is changing

Changes offer opportunity

Many opportunities in Retail & Food Services

Enabling Conditions Exist for achieving Success

8/8/2019 L1 a Changing India

http://slidepdf.com/reader/full/l1-a-changing-india 50/50

THANK YOUFor Any Queries