KPMG's 6th annual insurance industry opportunities & risks ...€¦ · financial services in KPMG...

36

6th annual Canadian insurance industry opportunities & risks report December 2018 kpmg.ca/insurance

Transcript of KPMG's 6th annual insurance industry opportunities & risks ...€¦ · financial services in KPMG...

6th annual Canadian insurance industry opportunities & risks report

December 2018

kpmg.ca/insurance

Cyber security specialists

Canadian insurance industry opportunities & risks overview

view technological disruption as more of an opportunity than a threat63%

The insurance industry is at one of the most transformative times in its history. The impacts of new technologies overwriting traditions and regulation spurring back-office transformation are just a few of the factors that are combining to bridge the gaps between insurers and their customers. KPMG's 6th annual Canadian insurance industry opportunities & risks report builds on our previous surveys, capturing insights and perspectives from industry stakeholders about the accelerators and disruptors impacting both their individual organizations and the industry as a whole.

Most valued skills

Digital transformation

managersData scientists

54%

46%

39%

37%

Emerging technology specialists

of Canadian insurers expect major technological disruption in their sector over the next three years68%agree disruption will weaken and/or eliminate some of the traditional leaders68%

are taking steps to actively disrupt the sector49%

believe organic growth will be most important for achieving organizational growth over the next three years (63% strategic alliances with third parties | 24% M&A)

85%

2 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Top 2018 Canadian industry opportunities

Top 2018 Canadian industry risks

Data analytics to enhance product design, marketing, and pricing

Regulatory and compliance burden | Natural catastrophes

Changing customer needs and expectations

Low interest rates and equity market risks

Enhanced operational processes and use of technology

Cyber security risks

2018 Survey respondent overview

54% P&C

27% Life

5% Intermediary

14% Other

Sector profile

55% Ontario

17% Saskatchewan

10% Quebec

7% New Brunswick

5% Alberta

2% British Columbia

2% Manitoba

2% Other

Headquarter locations

Executive management 27%

External board member 20%

Finance/Accounting 17%

Risk and compliance 12%

Other 12%

Actuarial 5%

Sales & Marketing 5%

Information Technology (IT) 2%

Role

68%

41%

54%

39%

49%

32%

6th annual Canadian insurance industry opportunities & risks report 3

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

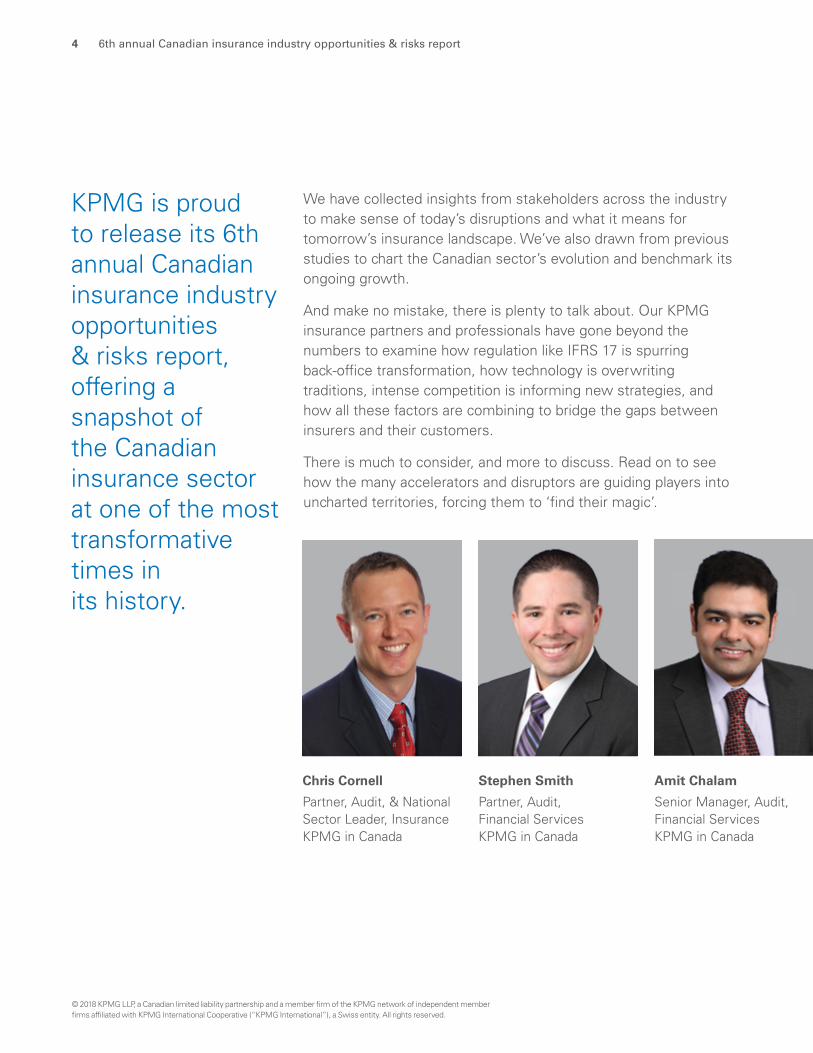

KPMG is proud to release its 6thannual Canadian insurance industry opportunities & risks report, offering a snapshot of the Canadian insurance sector at one of the most transformative times in its history.

We have collected insights from stakeholders across the industry to make sense of today’s disruptions and what it means for tomorrow’s insurance landscape. We’ve also drawn from previous studies to chart the Canadian sector’s evolution and benchmark its ongoing growth.

And make no mistake, there is plenty to talk about. Our KPMG insurance partners and professionals have gone beyond the numbers to examine how regulation like IFRS 17 is spurring back-office transformation, how technology is overwriting traditions, intense competition is informing new strategies, and how all these factors are combining to bridge the gaps between insurers and their customers.

There is much to consider, and more to discuss. Read on to see how the many accelerators and disruptors are guiding players into uncharted territories, forcing them to ‘find their magic’.

Chris Cornell

Partner, Audit, & National Sector Leader, InsuranceKPMG in Canada

Stephen Smith

Partner, Audit, Financial ServicesKPMG in Canada

Amit Chalam

Senior Manager, Audit, Financial Services KPMG in Canada

4 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Let’s do this.

6th annual Canadian insurance industry opportunities & risks report 5

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Tempered ambitionsIt wasn’t long ago when digital advances and mobile technologies were the most visible hurdles in the insurance industry’s path. Now, amidst ground-shifting regulations, demographic shifts, monolithic competition, and game-changing technologies, those days seem quaint by comparison.

Change is nothing new for the industry, and neither does it appear to be cause for alarm. The outlook among Canadian insurers remains relatively unchanged since our previous study. Two-thirds of Canadian insurers outright anticipate major disruption in their sector over the next three years and half intend on being the disruptors.

And while heightened compliance and technological mandates present elements of risk, they are also being viewed as motivation for back-office transformations, cost-saving initiatives, and investments in the people, capabilities, and tools that will forge stronger ties with their customers.

“In the past, it was about ‘go big or go home’. Now, for many insurers, it’s about go small and find your home.”

Amit ChalamSenior Manager, Audit, Financial Services, KPMG in Canada

Canadian insurers recognize these opportunities come with both sizable costs and strategic risks. While they can see the opportunities ahead of them, their view is obscured by regulatory challenges, competitive issues, and transformative hurdles. It’s unsurprising, then, that many remain cautiously optimistic – if not slightly more anxious – over their odds of ongoing success.

“It’s not surprising to see Canadian insurers in the same place as they were in previous years,” says John Armstrong, Partner and National Industry Leader, Financial Services, KPMG in Canada. “There’s a sense of optimism in the fact that many are getting comfortable with their strategy and ability to face the disruptions ahead, but that confidence is tempered by the challenges of meeting the need for stronger digital skills, more advanced technologies, and a greater demand for an enhanced customer experience.”

The question for many moving forward, he continues, is: “What are we doing to move into this new world, and can we do it better than our competitors?”

6 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Find your magicThe opportunities to grow via market share are fading. New online entrants, niche-competitors, and direct-to-consumer alternatives are all vying for customers in an increasingly cramped space. Rather than stay the course and hope for the best, many insurers are pursuing growth through alternate means. For some, that means forming strategic alliances (63%), while for others it’s seeking M&A opportunities (24%). For a majority of this year’s respondents, it’s chasing organic growth by looking inwards for ways to cut costs, increase sales among existing customers, and pursue innovative ways to differentiating themselves in the market.

“It used to be simple,” says Pierre Lepage, Partner and Business Leader, Property and Casualty Actuarial, KPMG in Canada.

“You were either a generalist or a niche player. Then, everyone was doing the analytics, distribution,

“One of the only ways I see growth coming for Canadian insurers in the future is if they change the way they interact with customers; that is, if they create a direct relationship with customers in ways that haven’t been done before.”

Gavin LubbePartner, Management Consulting, KPMG in Canada

underwriting, and managing the capital. Now, everything is more fluid, which means you may not be good at all these areas but you can narrow in on one thing that makes you stand out and still be successful.”

The desire to stand out is a dominant theme in this year’s survey. Insurers are leveraging their strengths, size, and the latest tools and technology to hone in on what their customers really want and to become known as the brand that can make it happen.

“More people are starting to ask ‘What’s our magic? What do we bring to this marketplace? What makes us stand out?’” Lepage adds.

Now is the time to find that “magic,” especially as industry juggernauts (e.g., Google, Amazon, or Facebook) threaten to enter the space using their own wealth of data, influence, and resources to dominate more traditional insurance functions.

6th annual Canadian insurance industry opportunities & risks report 7

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Trends to watch in insuranceThis report looks at several trends within insurance. Among them are seismic shifts in how life and P&C insurance is viewed and delivered.

1Insurance as a platformBusiness models are changing. Whereas insurance has traditionally been provided through a closed commercial eco-system, providers are moving outside this box to offer platforms upon which other services (e.g., InsurTech, health apps, P&C software) can operate.

2“Insurance on my terms” With the evolution to predominantly algorithm-driven models, InsurTech companies are moving customers rapidly toward micro insurance models, in which a provider insures by the moment. “It’s about being insured the way I, as a customer, want to be insured,” explains Roman Ryzer, Executive Director, KPMG in Canada. “Maybe I don’t want to insure the whole house, but only pay the premium for what I insure. Maybe I want to turn off insurance for my belongings when I’m home or have different types of coverage depending on how, when, and where I’m using my vehicle. That’s where insurance is going; it’s a movement from macro to micro insurance that’s driven by customer preferences.”

3Prevention over protectionThe advance of smart devices, telematics, and Internet of Things (IoT) technologies are giving insurers the means to track customer activity and offer actionable insights, supportive resources, and services to prevent claims before they happen. “Prevention over protection is quickly becoming the new norm,” says Ryzer. “Instead of giving someone a policy and saying ‘I’m going to pay you money if something happens’, insurers are starting to look at how they can spend a little bit of money to protect those people from risk events occurring in the first place. Maybe it is sending health advice, equipping them with a flood detection device, or feeding them tips on healthy living.”

4The sharing economy In the P&C realm, how do you insure a car that is both a family vehicle, business necessity and – on occasion – a ride-sharing asset? How do you insure a house that may double as an Airbnb? The sharing economy presents both unique opportunities and fundamental challenges for insurers, demanding the right combination of innovative risk models and tailored products.

Read what industry leaders are saying about the future of all financial services in KPMG International’s 30 Voices on 2030.

8 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Top 5 opportunities

Organization Canadian insurers

61% Enhanced operations processes and use of technology

68% Data analytics to enhance product design, marketing, and pricing

59% Data analytics to enhance product design, marketing, and pricing

54% Changing customer needs and expectations

51% Offering better customer experience | Changing customer needs and expectations

49% Enhanced operational use of technology

34% Customer preferences for direct and digital channels

46% Customer preferences for direct and digital channels

29% Cost reduction initiatives 44% Offering better customer experience

“The industry is evolving faster and faster, so you can’t take technology decisions as slowly as you may be used to. You have to be agile. You may have to experiment, assume the risks of innovation, or try some short-term tactical situations to achieve that organic growth that everyone appears to be after. Yes, that means larger investments, but that’s where having the proper governance and change management strategies will help you become more nimble.”

Pierre LepagePartner and Business Leader, Property and Casualty Actuarial, KPMG in Canada

6th annual Canadian insurance industry opportunities & risks report 9

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

A segment of one

Once again, all roads lead to the customer. Whether using data analytics to fine-tune client offerings (68%), new technologies to enhance the customer experience (44%), or wielding data-driven insights to keep pace with changing customer needs and expectations (54%), the message is clear: it’s the customer that is calling the shots.

“In speaking with many of our major clients and looking at where the focus is among this year’s respondents, it’s all about knowing the customer,” says Chris Cornell, Partner, Audit, and National Sector Leader, Insurance, KPMG in Canada. “Organizations want – and need – to deal with the customer in the way the customer wants to be dealt with, whether that’s through a digital experience, directly with the company, or through the broker channel.”

Catering to the customer is not a new industry mandate. Now, however, advances in AI and data analytics have made it easier to code new customer touch-points and approach each individual as a

“segment of one”.

Even still, becoming more customer focused can be difficult in an industry where consumer interactions have traditionally been few and far between, and typically saved for onboarding or claims scenarios. Moreover, insurers have largely stayed at arm’s length from their customers, relying on brokers to make those connections.

“For many, what’s standing in the way of creating a direct-to-consumer channel is the past. A lot of insurers have roots in broker-based models, and they can’t simply be tossed out because it’s in transition,” explains Cornell. “Therefore, the balancing act they need to perform is managing a broker-based business model, while also building out a direct to consumer channel that will be distinguishable in the market and surviving that transition phase.”

Certainly, as customer preferences move towards on-demand platforms, point-and-click services, and simplified service delivery, the need to pursue direct-to-consumer strategies is more apparent than ever.

“The customer is going to be core to everything; but in order to make that a core focus, you need re-think how you connect, interact, and understand those customers, and you need to modernize across the board to do that properly.”

Gavin LubbePartner, Management Consulting, KPMG in Canada

10 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The brokersWith insurers exploring direct-to-consumer services, the fate of the broker is in question. Given Canada’s historical reliance on brokers, the good news is that these industry intermediaries aren’t likely to retire overnight (at least, not all of them). Nevertheless, many are beginning to see the writing on the wall and taking measures to find their own niche within the supply chain.

“For the most part, brokers have accepted direct distribution as a fact of life and are adapting,” says Georges Pigeon, Partner, Deal Advisory, KPMG in Canada. “Many are increasing the customization of client service by, for example, supporting products that are less susceptible to digital disruptions to demonstrate their value to manufacturers.”

Walter Rondina, Partner, Management Consulting, KPMG in Canada, agrees that the role of the broker is evolving. Digital channels and direct-to-consumer tools aren’t a means to their extinction, but an opportunity to take the broker function to the next level: “A lot of brokers have jumped on that direct-to-consumer trend. In fact, many of the new digital companies we’re seeing are essentially digital brokers who are often backed by a reinsurance company.”

The Millennial factor

Changing demographics is one of the most influential headwinds facing the insurance industry. Millennials (and to a degree, their younger Gen Z cohorts) are delaying life events, ignoring traditional triggers for insurance purchases, and growing accustomed to one-click, on-demand service from every service provider in their network.

It’s little wonder that 86% of Insurance CEOs surveyed are concerned about how Millennials and their differing habits will change their business.

“Insurers need to prepare for demographic changes happening in Canada,” says Gavin Lubbe, Partner, Management Consulting, KPMG in Canada. “Wealth is a good play. Many of the Millennials and Gen Xers are in the saving phase of life, with some set to inherit significant wealth from their parents. At the same time, some Baby Boomers have accumulated wealth and are looking to both deploy it for maximum value, while ensuring they won’t be left short of cash in their golden years.”

“A number of companies have created separate teams or even separate units to look at things like a better digital customer experience or direct sales. The separation is key to giving those teams license to think differently.”

Doron MelnickPartner, Management Consulting, KPMG in Canada

Source: Me, My Life, My Wallet, KPMG International, 2018

6th annual Canadian insurance industry opportunities & risks report 11

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

For simplicity sakeInsurance customers are growing tired of fine print. They are leery of the claims processes, less willing to fill out volumes of paperwork, and growing less patient in dealing with what is often perceived as a complex industry. Therefore, in their pursuit to meet changing customer needs and expectations (the top third and second opportunity for organizations and industries, respectively), many insurers are looking to differentiate themselves by offering a more customer-friendly and focused service offering.

This is a particularly timely strategy as more and more customers become accustomed to one-click, on-demand, same-day services – experiences that are rarely replicated in the insurance world. Herein, making underwriting processes less burdensome in regards to testing and paperwork may go a long way towards standing out among customers.

The drive for simplicity can be tricky, especially for an industry beholden to increasingly complex rules and regulations. Nevertheless, says Peter Hughes, Canadian Digital Services Leader, KPMG in Canada, “Winning organizations will make regulation their friend.

They’ll be the ones who can differentiate their experience by giving clients the confidence that they’re adhering to data privacy laws and industry regulations, but the comfort in knowing their client experience isn’t going to be any more complicated as a result.” He adds, “When you’re talking about making insurance simple, one of the best plays is to leverage design, digital, and technology to cut through the paperwork, the claims processes, and compliance exercises so that it doesn’t create an onerous experience.”

Reducing costsOver a quarter of Canadian insurers believe cost-saving initiatives will be one of the largest opportunities ahead for their organizations. And with avenues for market growth in short supply, it makes sense to seek out ways in which to align business functions, enhance operations, or leverage technology to grow the bottom line and reduce claim payouts.

According to the Insurance Bureau of Canada, more than half of every dollar received is paid out in claims. Together, claim payouts and operating expenses account for approximately 75% of all insurance premiums.

“The whole experience needs to be simple. That means more accessible, more data-driven, and more automatic. As a customer, you shouldn’t have to fill out fields of information and jump through multiple hoops for the privilege of getting a quote. The industry should be looking into their data to know about my car and my home already.”

Peter HughesCanadian Digital Services Leader, KPMG in Canada

12 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Averaged over seven years, from 2011 to 2017 Source: IBC 2018 Facts

8.7%

Profit margin

13.5%

Taxes and levies

21.5%

Operating expenses, including employee compensation

56.3%

Claims paid out to policyholders

“Claims is one area where automation, operational analytics and deeper customer insights should be leveraged to improve both the process and the outcomes,” suggests Roman Ryzer, Executive Director, KPMG in Canada. “To be successful, insurers need to be able to embed analytical models directly into their core insurance applications. The goal is to be able to leverage these models in real time in order to guide and automate the claim processes. This will help allow the insurers to get the most benefits from the investments made in expensive core insurance applications, reduce claims payouts through better decisions and reduced cycle time, and allow the employees to spend more time on value-added tasks that will result in improved customer experience.”

Digital imperativeThe definition of “going digital” has changed. In years past, taking the digital journey meant trading pen and paper for processors and screens. Now, it means using advanced analytics, cloud computing, mobile networks, artificial intelligence, or even blockchain to collect, analyze, and leverage data in an increasing number of ways.

6th annual Canadian insurance industry opportunities & risks report 13

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

“It can be particularly difficult for organizations to take the next digital step because they’re so entrenched in the current way of doing things and it can be a challenge to take a step back and a fresh look,” says Doron Melnick, Partner, Management Consulting, KPMG in Canada. “The leaders of the future industry will be the ones who can successfully figure out how to leverage all these innovations around them and bring them into their main product offerings. That will likely involve a series of challenging conversations with their executive teams, employees, and dealers around how everybody needs to do things differently.”

Canadian insurers recognize that data analytics is a bridge to many of the perceived opportunities ahead. Over half of respondents in this year’s survey (59%) said building data analytics (DA) capabilities will provide opportunities for their organization, and over a third (68%) believe the industry as a whole can stand to benefit from DA technologies.

As Canadian insurers gain more comfort around data analytics, it’s likely we will see greater investments in related technologies (e.g., cloud, blockchain, AI, automation), more legacy system upgrades, and more efforts to remove digital silos to support data-sharing between all parts of the organization.

“The insurance sector is not unlike the rest of the financial services industry when it comes to recognizing the power of data and the desire to use data analytics to understand their customers and get a better handle on risk management.”

John ArmstrongPartner and National Industry Leader, Financial Services, KPMG in Canada

Indeed, one of the biggest transformative pieces going forward is going to be how organizations bring that data together, make it accessible to all company functions, and keep it safe and secure.

Tech in front- and back-officeData analytics is only one piece of the technological puzzle. As capabilities evolve, attentions are also turning to robotic process automation (RPA), artificial intelligence, distributed ledgers (i.e. blockchain), and other disruptors, which have shown potential for delivering both front- and back-office enhancements.

“What we’re seeing is the use of technology throughout the insurance value chain,” notes Walter Rondina, Partner, Management Consulting, KPMG in Canada. “That includes a fair amount of large IT transformation programs that focus on the business or the core insurance operations, such as policy administration, underwriting, HR, billing, and claims.”

At the front-office, technology is being used as a bridge to new and innovative business models (e.g., “Insurance on my terms,” adaptive policies, Internet of

14 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Meanwhile in the back-office, insurers are also undergoing a migration from legacy systems towards newer commercial solutions or build-outs of in-house developed solutions for critical business elements, such as policy administration, actuarial functions, and compliance processes (especially in light of incoming IFRS 17 changes). What’s more, a growing number are experimenting with distributed ledger technology (commonly known as blockchain) as a means to eliminate manual processes and drive operational efficiency. Mass adoption of blockchain may still be some years away, but given the growing awareness, capabilities, and confidence building around distributed ledger technology, it won’t be long before it becomes the rule, rather than the exception.

Taking it further with InsurTech

It’s a brave new world for the insurance industry. And while talk of back-end tools like automation, AI, and data analytics may be dominating conversations today, it’s likely those discussions will turn to more consumer-centric technologies down the road.

Things synergies). Organizations are leveraging on-demand platforms, AI services (e.g., robo-advisors and virtual assistants), and mobile technologies to improve the customer experience, make it more accessible, and integrate multiple service lines.

To that end, many insurers are attempting to figure out how to break down their internal barriers to provide more than just insurance to their clients. That includes wealth management, banking, estate planning, or other services that make sense given their strengths and resources.

John Armstrong, Partner and National Industry Leader, Financial Services, KPMG in Canada, anticipates that the rate of tech adoption will only increase as insurers draw inspiration from other industries, saying, “We’re starting to see doctors conduct virtual appointments over Skype or service providers provide live consultations over mobile applications, and there’s potential for insurers to learn from those models. And why not? Instead of making customers send pictures for a claim after the fact, why not set up a system whereby clients can Skype or FaceTime with an insurance representative and do a walkthrough of their home or car.”

KPMG Lighthouse

KPMG Lighthouse is our Advanced Analytics & Intelligent Automation Centre of Excellence that offers a broad range of services to help solve our clients’ most pressing challenges. We perform hands-on, deep analytics of the data to solve business problems effectively. We understand the importance of establishing a process for D&A and artificial intelligence that is repeatable, efficient, and insight driven.

Advanced analytics create powerful information for companies, which we have seen used in the areas of customer segmentation optimization, financial reporting automation, and predictive analytics to derive business insights that lead to better decision making. For example, a model for disability claims that is able to identify high risk injury claims with over 95% confidence can be used to reduce time off work, map the claimant journey at a macro and micro view, and help to identify risks and issues associated with the reoccurrence of injury. The main benefits include the potential to reduce costs on the organization, improve current processes leading to better customer experience, and optimize resource allocation.

6th annual Canadian insurance industry opportunities & risks report 15

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Failure to adopt

Failure to adopt new technologies successfully is the third-most identified risk by survey respondents both when it comes to their organization (39%) and the Canadian insurance industry as a whole (29%).

“Many insurers are struggling to figure out how to incorporate digital throughout the value chain. There’s a lot of hype with respect to digital elements like AI, intelligent process automation, or robotic process automation, but they’re trying to come up with concrete use cases and making those innovation investments in a cost-effective way that adds value to the organization,” explains Walter Rondina, Partner, Management Consulting, KPMG in Canada. “The challenge for insurers is trying to put the pieces of digital together to add the most value to clients, as well as improve operations as much as possible, and that’s where we can help.”

This burgeoning field, dubbed InsurTech, includes tools that are designed to personalize insurance products using telematic

“wearables” that wield real-time telematics to assess customer activity at an individual level. This is opening the doors to usage-based insurance, wherein customers can be rated as per their day-to-day activities and exposure to risk (i.e., “insurance on my terms”).

Customers who are more active, for example, may receive lower health and life insurance rates than those who are not. Meanwhile, customers who use their car for multiple purposes may migrate to different policies depending on their locations and activities.

Furthermore, Alison Rose, Senior Manager, Life Actuarial Practice, KPMG in Canada, suggests InsurTech may also soon allow insurers to build customer communities wherein benefits are shared among groups of like-minded customers: “For example, I could see someone offering a group insurance product policy where joining this player would give you points and help reduce the cost of the program. I think innovative ideas like this are happening, but it does take some investment.”

“Insurers are leveraging technology to deliver their product to customers in a more efficient way. They’re applying tools to price the product more accurately, to help clients file claims faster and more conveniently, and to make their front- and back-office processes run more seamlessly.”

Georges PigeonPartner, Deal Advisory, KPMG in Canada

16 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Several major players are already leveraging InsurTech solutions to offer more tailored, data-driven coverage to their customers. Amazon, for example, recently partnered with a major US insurance company to sell “smart home kits” containing security cameras, water sensors, and other safety devices to insurance customers, who then receive discounts on their home insurance policy for integrating them into their lives. Closer to home, a Canadian insurer has also started testing the InsurTech waters by tracking clients’ driving behaviours via a mobile app and rewarding them with insurance discounts based on favourable driving habits.

Elsewhere, InsurTech players are using “smart” devices, such as digital wristbands and sensors to collect and analyze customer activity and adjust their coverage accordingly. For others, it’s incorporating data driven tools to provide risk prevention tools and resources.

Trading security for service

Findings from KPMG International’s 2018 Me, My Life, My Wallet report lend credence the fact that some Canadian consumers may be willing to trade data security and privacy guarantees for better online service. That is, while nearly one-in-three (31%) respondents wouldn’t trade their data for any benefit, a majority would be open to the idea in exchange for financial compensation (21% Canadian/13% Global), better value/prices (17% Canadian/11% Global), better security (11% Canadian/18% Global), better products and services (7% Canadian/15% Global), or better customer experience and personalization (5% Canadian/15% global).

By extension, insurers must ascertain their customers’ comfort levels around giving up expectations around data privacy and protection for the benefits that InsurTech innovations and more digitally-inclined services provide.

Source: Me, My Life, My Wallet, KPMG International, 2018

“A lot is happening in the InsurTech space,” notes Georges Pigeon, Partner, Deal Advisory, KPMG in Canada. “Of course, visible examples are sensor-enabled wearables and telematics, but it’s moving into the back-office as well with connected tools that can help make carriers operate more efficiently.”

The move towards wielding customer data for usage-based insurance has also given rise to security concerns. And yet, considerations for data privacy don’t appear to be slowing down the adoption or interest in InsurTech products. In fact, it appears Canadians are willing to forego some degree of security for the ability to be serviced in this way.

It may be several years until InsurTech devices and related services become really mainstream. In the meantime, it is promising to see the rise of an industry that will bring insurers closer to their goals of becoming more data-driven and customer-centric.

6th annual Canadian insurance industry opportunities & risks report 17

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Emerging InsurTech segmentsKPMG International’s 2018: InsurTech hits its stride report explores the rise of InsurTech products and companies, as well as several segments that are becoming increasingly attractive for investment and development.

1Autonomous vehiclesSelf-driving cars have already seen a significant increase in investment in recent months. Regulators and governments are keen to develop this area (such as through incentives like those seen in the UK Budget in November), and the biggest insurance companies want to position themselves as the insurers of choice.

2Cyber insurance Products in the cyber security space have also come to the fore, with a plethora of cyber insurance InsurTechs spawning out of Israel and other markets. There is, however, plenty of room for improvement. Many current products in the market are inadequate, poorly priced, and not offering the coverage or service that companies need.

3Aviation and drone insuranceWhile a more niche market, aviation and drone insurance is nonetheless an important area for future growth. Drones themselves are of increasing interest for insurers, such as for the remote inspection of claim sites and areas affected by natural disasters, and a few drone-related InsurTechs are already attracting interest.

Source: 2018: InsurTech hits its stride, Murray Raisbeck, Global Co-leader, Fintech, and Partner, Financial Services, KPMG in UK & Paul Merrey, Partner, Global Strategy Group, KPMG in the UK

18 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Come togetherAlthough M&A activity did not make the top list of opportunities, the fact that one-quarter (24%) of Canadians cite M&A as a growth strategy is revealing. As larger organizations look to become more agile, and as start-ups seek footholds into the industry, it is unsurprising to see this activity persist.

“M&A activity still exists, but we see a movement toward strategic alliances that aren’t necessarily about the exchange of cash or shares for an ownership interest, but more so an alignment of common goals,” observes Georges Pigeon, Partner, Deal Advisory, KPMG in Canada.

US firms may also be looking to unload the risk of IFRS 17 to Canadian firms as well, thereby driving cross-border M&A activity.

Whatever the motives, however, it’s evident that M&A is still on the planning table.

Yet with competitors coming at the Canadian market from different angles, Pigeon says it pays to be cautious about signing agreements: “You want to make sure you are seeing eye-to-eye

with that third party, that you understand the repercussions of whatever alliance you’re striking and you’re performing an appropriate level of due diligence. You need to ask yourself: Is it the right party? Is the contract properly drafted? Are your financials well measured and projected, and will they be well measured going forward to really see the benefits of this alliance?”

It all comes back to peopleTalk of automation, smart machines, and sophisticated algorithms may spell doom for human workers at first, and yet the reality is the industry will lean even heavier on talent as it moves into the digital future.

In this year’s survey, we asked insurers what skills they deemed important in their organization. Of those rated somewhat or highly important were data scientists (83%), emerging technology specialists (90%), digital transformation managers (95%), and cyber security specialists (98%) – high-tech talent that is critical for not only guiding digital agendas, but reshaping them and maintaining them as the industry continues to evolve.

The future- proof CEO

The insurance companies of tomorrow will not simply be in the business of providing insurance; they will be in the business of solving their customers’ problems. Similarly, the CEO of the future won’t simply be the head of an insurance company, but someone who can foster partnerships between the services and product providers across all industries to provide the most comprehensive solution.

6th annual Canadian insurance industry opportunities & risks report 19

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

“The ability to mine data and make sense of all the information is crucial to envisioning the future,” says Soula Courlas, Partner and National Leader, People & Change Services, KPMG in Canada.

“Organizations need people who go beyond that data to find where it is most applicable and how it can be used to reach clients in new and innovative ways.”

It’s not just about filling ranks with tech-related skills. To steer their ships effectively, companies are building growth-oriented workforces with people who are comfortable with disruption. That means recruiting those who are adept at change, can foster a culture of innovation, understand their competitors, and help larger organizations pivot faster as conditions change.

As Courlas foretells: “The companies of the future will need leaders who can influence how the business is going to be reshaped. Fortunately, employers have so much more knowledge and data at their fingertips to draw from in matching people with the skills it will need down the road, but it is still a bit of an art with the science to find out how to draw the right correlations to the business.”

Competing for those capabilities can be a challenge for a sector that has traditionally not been seen as being progressive or

innovative. Therefore, she adds, “The key is going to become how to differentiate themselves as a brand for attracting and retaining the talent to sustain the level of innovation that is required to remain relevant and competitive.”

Staffing for tomorrow

What will the workforce of tomorrow look like? This is a question all industries are working to solve as industry veterans prepare to make their exit and Gen Xers, Millennials, and even younger Gen Zers move into their former roles… or maybe even a robot?

“What’s really important for human resource (HR) leaders is to understand the demographics of their talent – and that’s across any organization, insurance or otherwise,” stresses Courlas.

“You have to understand what proportion of people are entering the workforce, who is occupying the middle- and back-end of your organization, and where your most knowledgeable and experienced people are going.”

This understanding is central to building a future-ready office. For one, as more established talents prepare to retire, HR professionals must ensure their experiences, skills, and intellectual capital are not going out the door with them. At the same time, HR must help

20 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Rise of the humans

If the fate of human workers in an AI, automated, digital world seems bleak, think again. While it is true that automation alone is set to change every job category by 25%, KPMG International’s two-part report, Rise of the Humans: The integration of digital and human labor, argues that digital disruption will likely open opportunities for new human skills, while transforming others. As such, it is beneficial for employers to keep several considerations in view:

Now is the time to develop transition strategies to manage the disruption to the workforce. Leaders need to be aware of their role and develop the skills required to ensure success.

Traditional supply and demand forecasting must be replaced with agile workforce shaping. This is a structured yet agile approach to determine the appropriate shape and size of the workforce incorporating all elements (e.g., employed vs. contingent, human vs. digital, career ladder vs. career lattice, etc.).

Early movers are already learning lessons about the best way to deploy intelligent automation. One lesson is the importance of preparing the workforce and enabling them to re-skill themselves for new roles.

them respectfully wind down their careers with the recognition that many of these same employees may become consumers of the organizations they once served.

Then there are those who occupy “the middle”; the up-and-coming Gen X and Millennials who will be influential in how the organization responds to the changes and disruptions around it. Herein, insurance organizations would do well to learn what they value most within their careers and wield an array of incentives and strategies to keep them loyal.

“It’s not always about money either,” says Courlas. “If employees feel that they have a connection – that they have a path forward, the organization cares, and that they are doing meaningful work – they will stay and continue to evolve with the organization along with the leadership.”

Succession planning

Succession planning is set to take focus in the coming years as veterans of the industry prepare to exit and a mix of demographics rise to fill the gaps. This is on the minds of insurance companies as well, as leadership begins to consider what skills it will need to acquire and which it will want to transfer from those in the final years of their career.

6th annual Canadian insurance industry opportunities & risks report 21

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

“Succession planning needs to have a pulse on how the business is changing,” says Courlas. “You need to marry that to what kind of succession is required to keep in line with the way the business is evolving. This is not a point in time activity,” she adds. Succession needs to continue to be top of mind as the business evolves. That means considering how one’s talent capability needs will evolve in relation to where the business sees itself differentiating itself in the market, and what tools and technologies it is likely to adopt.

As Courlas explains: “It’s very scenario-based and modelling based, and how the organization is going to evolve is going to determine what capability you need. Those scenarios, and the thinking behind that exercise, will help influence who your successors will be and what kind of skills and opportunities they’ll need to be ready for. There are some potential scenarios that might happen in the business given the market trends, socio-economic dynamics, and any number of factors.”

Outsourcing talent

In the hunt for talent, one alternative is to outsource critical functions. This can be an opportunity, says Courlas, but one that carries third-party risk: “You have organizations that specialize in data mining, customer acquisitions, and other specialized skills, which can take on some of the functions that are key to a core business, but ultimately the decisions to outsource for those functions comes down to an organization’s appetite for risk and ability to get the kind of skills to do what they need done.”

“Data scientists and AI experts emerged as some of the most highly valued talent in the insurance space, and that lines up well with insurers’ priorities for using data to enhance the customer experience and product design. Now, the challenge will be to actually find those candidates, which is only going to get harder moving forward.”

Amit ChalamSenior Manager, Audit, Financial Services, KPMG in Canada

22 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

236th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Top 5 risks

Organization Canadian insurers

46% Failure to adapt to changing customer preferences and insurance needs

41% Regulatory and compliance burden | Natural catastrophes

44% Regulatory and compliance burden 39% Low interest rates and equity market risks

39% Failure to adopt new technologies successfully

32% Cyber security risks

34% Cyber security risks | Cost and risks of IT investment

29% Failure to adopt new technologies successfully

29% Slow to adopt data analytics 27% Failure to adapt to changing customer preferences and insurance needs

Bracing for IFRS 17

It’s difficult to discuss the future of Canadian insurers without mentioning IFRS 17. Currently effective January 1, 2021, but tentatively delayed to 2022, the new accounting requirements will have an effect on players large and small, including multi-national insurers who have a footprint in the Canadian market.

“It is a big disruptor, in particular for life insurers,” insists Zaid Hoosain, Partner, Advisory Services, Management Consulting, KPMG in Canada. “It is going to change the underpinning of the organizations – the data

flows and models that allow for the production of the financial results.”

Moreover, Dana Chaput, Partner and Insurance Accounting Change Leader, KPMG in Canada, says the accounting changes introduced by IFRS 17 will have knock-on implications with respect to regulations, capital, and taxes: “Regulatory and tax authorities are trying their best to signpost where they’re going to head, but they’ve yet to come out with updated

24 6th annual Canadian insurance industry opportunities & risks report24 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

In it to win it

How is the world preparing for IFRS 17? In KPMG International’s 2018 Report: In it to win it – IFRS, we collected feedback from 160 insurers both within Canada and globally. Top insights include:

– Large insurers are further along than smaller insurers, having entered the design and implementation of IFRS 17 (67% to 9%).

– Twenty-four percent of respondents had not started their IFRS 17 project yet or were still following developments as of May 2018.

– The majority of respondents were targeting one year of parallel running before the IASB tentatively agreed to defer the effective date to January 1, 2022.

– Nine out of ten respondents foresee difficulties in securing sufficiently skilled people to do the job.

“IFRS 17 is a massive challenge and Canada is one of the few jurisdictions in which all insurers, large and small, must comply,” says Dana Chaput, Partner and Accounting Change Leader, KPMG in Canada. She adds that,

“Ambitious insurers are using this change as a catalyst for process improvements within Finance or Actuarial, increases in automation, and to develop future leaders.”

requirements. This creates a ‘chicken and egg’ scenario where insurers are moving forward on IFRS 17 implementation, but questions about capital and tax implications remain outstanding.”

In recent years, insurers have been focused on identifying and assessing gaps, while those further ahead have started designing and implementing solutions, including preparing and enhancing their data.

“Complying with IFRS 17 is going to stretch current processes and tools to their breaking point, so many life companies now have to invest in the modernization of their valuation functions,” notes Hoosain. “That’s a big change because the valuation functions are often quite complex and there are a lot of inter-dependencies and interactions.”

Trying to change everything all at once while staying in operation is understandably tricky, he adds:

“It’s like trying to change a plane’s engines while it’s in mid-air.”

Indeed, the cost of bare minimum compliance may be high in some instances, depending on a company’s products, level of technological maturity, and how long it’s been working towards IFRS 17 implementation. Herein, it pays to have financial discipline over incremental spend and

be clear about what benefits the organization hopes to derive from that spend.

Opportunity in change

Few disruptors loom heavier over the industry than the arrival of IFRS 17. Like all disruption, however, the resulting transformation is rife with opportunity.

In KPMG International’s In it to win it – IFRS report, 97% of the world’s largest companies are using the opportunity to optimize systems and processes at the same time in order to reap longer-term, enterprise-wide benefits such as process optimization, actuarial process, and system modernization.

“Operational process improvements are a massive deal, yet insurers aren’t always effective at funding them,” says Hoosain. “IFRS 17 is making them look at that entire reporting process and giving them an opportunity to act on opportunities to automate processes that are today wholly manual, create reports that are more fit for purpose, or rationalize their valuation models.”

Regulatory burden IFRS 17 may be the primary reason why regulatory and compliance burden ranks as

6th annual Canadian insurance industry opportunities & risks report 25

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Supporting IFRS 17 transformation

Since its release, KPMG has been working with clients to apply a distinctive top-down and business-focused approach to IFRS 17 – one that is designed to accelerate progress towards an organization’s goals surely and securely. Central to this tailored approach are:

A hypothesis-driven approach, starting top down rather than bottom up with a gap analysis, allowing for design decisions to be taken earlier, reducing demands on scarce resources.

Deep market insights from advising many leading insurers on IFRS 17.

Custom strategies, understanding that one size does not fit all, with a tailored approach to client needs and aspirations – whether it’s quick wins, cost savings, high quality and efficient financial and regulatory reporting, improved teamwork and other benefits.

Proprietary tools and accelerators to fast-track impact assessments and solution designs.

Highly qualified teams that bring insights every step of the way, actively promoting knowledge transfer to your people from the outset.

“As insurance CEOs begin managing broad alliances across various industries to solve their customers’ problems, regulators won’t be far behind. They will have to realign themselves to regulate activities rather than industries.”

Amit ChalamSenior Manager, Audit, Financial Services, KPMG in Canada

the highest risk for the Canadian insurance industry (41%) and the second highest among Canadian organizations (44%). Still, it is far from the only regulatory and compliance consideration.

Another is FASB’s Targeted Improvements to the US GAAP Long-Duration Contract Accounting, which would result in significant changes to how insurers required to report under US GAAP measure the liability for certain insurance contracts and amortize deferred acquisition costs.

“In conversations with clients, one of the biggest questions that comes up is how many synergies can be achieved between these changes. That’s because if you are going to have two sets of accounting change to go through, you want to align your policies and processes wherever possible,” says Chaput.

Combined with new Know Your Customer (KYC) and Know Your Product (KYP) expectations, and revised Life Insurance Capital Adequacy Test (LICAT) calculations, keeping pace with compliance can be overwhelming. Nevertheless, adjusting to new rules is a common hurdle in the insurance industry, and it’s one that isn’t expected to become easier any time soon.

26 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Disruptors at the doorEvery year brings new market entrants to the fore; some with new direct-to-consumer offerings, tech-savvy services, and more appealing value propositions that can give even the most established players cause for concern.

Disruption isn’t catching Canadian insurers off guard. Sixty-eight percent of Canadian insurers expect major disruption in their sector over the coming years, while the same amount believes it will eliminate or reposition existing leaders in the space.

Attitudes around new competitors appear focused on the potential arrival of major new entrants like Google, Amazon, Apple, and Facebook who are already helping start-ups enter the space. A decade ago, companies would need to build all their own infrastructure, whereas modern start-ups like Uber or Airbnb can use platforms built by Facebook, Google, Amazon, and Apple for server space, processing power, marketing, and distribution.

Beyond opening doors for more players, these big names have also shown signs of preparing to enter the insurance space themselves. Google, for example,

has had a head of insurance for some time, while Amazon is well poised to become an online aggregator of insurance products (a “super broker”), thereby forcing manufacturers, new and old, to jockey for representation on its platform.

Data-rich players, like Facebook and Apple, are also well positioned to enter the space given their wealth of consumer data, access to consumer devices, and proven affinity for data analytics – the foundations of a solid insurance offering. Players like these also have the stability and financial resources to weather the inherent risks of entering the business.

As Doron Melnick, Partner, Management Consulting, KPMG in Canada, predicts, “I wouldn’t be surprised to see these technology giants make progress on that front in the next five years. And yet, the biggest question for them will not be whether or not they are able to compete – because they are – but whether it makes sense for them to do so. Is it the most profitable venture for them to invest in? Is insurance a better value proposition than another line of business?”

It’s understandable that Canadian insurers are losing some sleep over pervasive competition. Moreover, it makes sense that these anxieties are now driving

those same players to provide customers with the same level of service and innovation as these potential competitors before they hit the market.

Cyber security and fraud The industry may be gaining more confidence around cyber security and fraud, but that doesn’t make it any less of a concern. In 2018, cyber security continues to be one of the top five risks for both organizations and industries. Granted, numbers are down, but with digital technologies and systems transforming the industry, it remains as relevant as ever.

“Cyber is a big thing for almost any board in any industry, and getting a handle on that requires comfort on the board level that there’s a robust cyber plan in place and an organizational culture that places data privacy and security first,” says John Armstrong, Partner and National Industry Leader, Financial Services, KPMG in Canada.

Enterprises of scale need to have a thorough, ruggedized cyber security strategy, he continues. This is especially true in Canada, where current and incoming data privacy and breach reporting

6th annual Canadian insurance industry opportunities & risks report 27

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

laws hold all data-holders to higher standards than most other countries.

Fraud is an equally critical topic for insurers. While not among this year’s top five risks, Roman Ryzer, Executive Director, KPMG in Canada, believes it must remain top of mind regardless. “Fraud is extremely important, particularly on the claims side. If you can apply strong fraud governance and controls to claims, that’s where you’ll stand to receive the biggest operational savings,” he says.

Natural catastrophesIt may not dominate boardroom agendas as much as other risks, but natural catastrophes are a growing challenge for Canadian insurers all the same.

P&C insurers, for example, are growing increasingly concerned with the frequency and severity of those catastrophes, and their inability to re-price those risks or move that risk around like other re-insurers.

“Companies like Google and Amazon have the resources to play in this sector. The question is whether or not it makes sense for them to do so, and if they want to handle the regulatory framework around solvency whilst providing the returns stakeholders have become accustomed to.”

Georges PigeonPartner, Deal Advisory, KPMG in Canada

28 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

And with record-setting wildfires, floods, and droughts becoming more commonplace, we expect consideration for natural disasters to grow among all insurance manufacturers.

“It’s something companies have to deal with,” adds Pierre Lepage, Partner and Business Leader, Property and Casualty Actuarial, KPMG in Canada. “This is an opportunity for insurers because it is a chance to modify products to be more valuable to customers exposed to natural catastrophe risks. Before, insurers might have excluded certain events from their contracts to keep them profitable, but now they are realizing they can keep more customers by offering policies with fewer related exemptions. Natural catastrophes also make insurance more important, by increasing demand for products that can adequately address these risks.”

By being more valuable to clients in their time of need is truly when insurers need to embrace their time to shine.

Low interest rates and equity marketsWhile interest rates nudging higher has benefited the industry, it has increased concern around the global economic environment in regards to trade uncertainty and things of that nature. Perhaps this is the cause behind 39% of this year’s respondents noting low interest rates and equity markets as the second-most concern; although we suspect this is also residual from other years. There was also a shift away from an organizational level, which does indicate insurers see the low interest rates as the new norm, but are still keeping an eye on the risk from an industry perspective.

The slight increase in reinvestment returns is welcome by the industry, however the rising rates may put a strain on an individual’s ability to make mortgage payments and poses a possible risk to the Canadian housing markets. The impact on customers could far outweigh the marginal increase in investment returns.

6th annual Canadian insurance industry opportunities & risks report 29

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Board takeawaysKeep competition on the radar. Most insurance companies will be thinking about the fact of Amazon or Google entering the space, how it will affect them, and what they can do in advance. Herein, boards must decide how concerned they are about new competition, how (or if) they plan to respond, and how their organizations can differentiate themselves in their respective markets.

Make peace with technology. Boards would do well to track technological trends, review what some of the bigger tech companies are doing, assess the risks of adoptions, and collaborate with management to determine where new technologies would make the best fit.

Find your magic. What makes your organization unique? How good is it at executing on its specialties? How can new technologies, alliances, talent, or

models align with that “magic”, and what’s being done to invest in those elements? Moreover, are any competitors doing what you do? How can you be better?

Are you covered? The industry may be anything but traditional, but that doesn’t mean taking an eye off conventional risks. Boards must work with all business units and leadership to assess coverage of risks related to regulatory compliance, cyber, natural catastrophes, and other fundamentals.

Consider your allies. Boards must remain diligent in their search for M&A opportunities that align with their goals and will generate real growth down the road.

Strength in numbers. Transformation doesn’t have to be a solo journey. More than ever, organizations have access to the proven strategies, industry-tested methodologies, and third-party support to make good on their transformation initiatives.

30 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Top 5 opportunities for organizations in 2017/18

Frequency Response

63% Data analytics to enhance product design, marketing and pricing

60% Offering better customer experience

54% Enhanced operational processes and use of technology

46% Changing customer needs and expectations

42% Focusing on brokers and their needs

Top 5 opportunities for organizations in 2018/19

Frequency Response

61% Enhanced operational processes and use of technology

59% Data analytics to enhance product design, marketing and pricing

51% Offering better customer experience | Changing customer needs and expectations

34% Customer preferences for direct and digital channels

29% Cost reduction initiatives

Appendix: Opportunities & risks

6th annual Canadian insurance industry opportunities & risks report 31

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Top 5 opportunities for Canadian insurers in 2018/19

Frequency Response

68% Data analytics to enhance product design, marketing and pricing

54% Changing customer needs and expectations

49% Enhanced operational processes and use of technology

46% Customer preferences for direct and digital channels

44% Offering better customer experience

Top 5 opportunities for Canadian insurers in 2017/18

Frequency Response

65% Changing customer needs and expectations

62% Data analytics to enhance product design, marketing and pricing

58% Enhanced operational processes and use of technology

56% Offering better customer experience

44% Customer preferences for direct and digital channels

32 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Top 5 risks for organizations in 2018/19

Frequency Response

46% Failure to adapt to changing customer preferences and insurance needs

44% Regulatory and compliance burden

39% Failure to adopt new technologies successfully

34% Cyber-security risks | Cost and risks of IT investment

29% Slow to adopt data analytics

Top 5 risks for organizations in 2017/18

Frequency Response

50% Low interest rates and equity market risks | Regulatory and compliance burden

40% Legacy systems constrain ability to adapt to change

35% Cost and risks of IT investment

33% Cyber-security risks | Failure to adopt new technologies successfully

25% Natural catastrophes

6th annual Canadian insurance industry opportunities & risks report 33

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Top 5 risks for Canadian insurers in 2018/19

Frequency Response

41% Regulatory and compliance burden | Natural catastrophes

39% Low interest rates and equity market risks

32% Cyber-security risks

29% Failure to adopt new technologies successfully

27% Failure to adapt to changing customer preferences and insurance needs

Top 5 risks for Canadian insurers in 2017/18

Frequency Response

56% Low interest rates and equity market risks

44% Regulatory and compliance burden

33% Failure to adapt to changing customer preferences and insurance needs | Natural catastrophes | Legacy systems constrain ability to adapt to change

25% Canadian economic downturn | Cyber-security risks | Customer preferences for direct and digital channels

23% Increased regulation of market conduct | Failure to adopt new technologies successfully

34 6th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

356th annual Canadian insurance industry opportunities & risks report

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

kpmg.ca/insurance

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2018 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 19981 The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Contact usJohn ArmstrongNational Industry Leader, Financial ServicesKPMG in [email protected]

Amit Chalam Senior Manager, Audit, Financial Services KPMG in [email protected]

Dana Chaput Partner and Accounting Change Leader KPMG in [email protected]

Chris Cornell Partner, Audit & National Sector Leader, InsuranceKPMG in [email protected]

Soula CourlasPartner and National Leader, People & Change ServicesKPMG in [email protected]

Zaid Hoosain Partner, Advisory Services, Management Consulting KPMG in [email protected]

Peter Hughes Canadian Digital Services Leader KPMG in [email protected]

Pierre Lepage Partner and Business Leader, Property & Casualty ActuarialKPMG in [email protected]

Gavin LubbePartner, Management ConsultingKPMG in [email protected]

Doron Melnick Partner, Advisory, Management Consulting KPMG in [email protected]

Georges Pigeon Partner, Deal Advisory KPMG in [email protected]

Walter Rondina Partner, Management ConsultingKPMG in [email protected]

Alison RoseSenior Manager, Life Actuarial Practice416 777 [email protected]

Roman Ryzer Executive Director KPMG in [email protected]

Stephen SmithPartner, Audit, Financial ServicesKPMG in [email protected]