KPMG’S PRIVATE EQUITY GROUP Key …...Of 114 deals rated by Fitch in 1H06, 43% were rated B-vs....

44

KPMG’S PRIVATE EQUITY GROUP Key developments & trends in the LBO market Breakfast Meeting for PE Leaders Zurich, 20 November 2006

Transcript of KPMG’S PRIVATE EQUITY GROUP Key …...Of 114 deals rated by Fitch in 1H06, 43% were rated B-vs....

KPMG’S PRIVATE EQUITY GROUP

Key developments & trends in the LBO marketBreakfast Meeting for PE Leaders

Zurich, 20 November 2006

Der Private Equity Lebenszyklus –Unterstützung durch KPMG

Beteiligungsmöglichkeiten lokalisieren und prüfen:

KPMG denkt und handelt interdisziplinär und hat Zugriff

auf ein aktives globales Netzwerk

Wertsteigerungspotenziale erkennen und freisetzen:

KPMG unterstützt Portfoliounternehmen in jeder

unternehmerischen Entwicklungsphase praxiserfahren und

umsetzungsorientiert

KPMG‘s PE Gruppe bietet mit einem umfassenden Dienstleistungsangebot Unterstützung

ThePrivate Equity

House

Investments& Deals

Fundraising

RealisingValue Portfolio

Management

Ausstieg planen und durchführen:

KPMG erfasst die Industrielogik von Portfoliounternehmen ganzheitlich, was ergebnis-orientierten Lösungen begünstigt

Mittelbeschaffung und Aufsetzen eines neuen Fond:

KPMG unterstützt PE Häuser beim Set-up neuer Vehikel –von der Definition der Investment Strategie, zum Fundraising bis zur Fund-Strukturierung

Der Private Equity Lebenszyklus –Investments & Deals

KPMG bietet ein interdisziplinär und international agierendes Netzwerk –eine nachhaltige Deal-Quelle

Beteiligungsmöglichkeiten lokalisieren und prüfen

ThePrivate Equity

House

Investments& Deals

Fundraising

RealisingValue Portfolio

Management

MARKTVERSTÄNDNIS

DIENSTLEISTUNGEN

MEHRWERT

Die Globalisierung und die Liberalisierung der Realgüter- als auch der Kapitalmärkte sowie die Beschleunigung des Innovationszyklus in den einzelnen Industriesegmenten wirken sich auf alle Unternehmen aus. Die Unternehmen sehen sich gezwungen, das Supply Chain Management zu optimieren, interne Abläufe zu straffen, neue innovative Produkte zu lancieren, Produktions- und Forschungskapazitäten sowie Vertriebskanäle und Marketingaktivitäten kontinuierlich den Erfordernissen der Märkte anzupassen.

KPMG kennt die Herausforderungen, denen Unternehmen in dynamischen Märkten täglich begegnen müssen. Das antizipieren der sich daraus ergebenden Industrielogik gehört zu unseren Kernkompetenzen. Diesem Ansatz folgend, nutzt KPMG das Potenzial, über ihr international agierendes Berater-Netzwerk, um Unternehmen frühzeitig in Bezug auf Nachfolgeregelungen, Unternehmensabspaltungen, Zusammenschlüssen und auf die Umsetzung sowie Finanzierung von Expansionsvorhaben zu sensibilisieren.

KPMG ist Berater von interessanten Unternehmen, deren Aktivitäten die kritische Unternehmensgrösse aufweisen und sich im geographischen sowie industriellen Fokus ihrer Beteiligungsgesellschaft bewegen. KPMG kann ihrer Beteiligungsgesellschaft als Quelle für Beteiligungsnahmen dienen. Darüber hinaus sind die Berater-Teams von KPMG international vernetzt und können sie bei der Strukturierung und Durchführung von grenzüberschreitenden DueDilgences unterstützen.

Private Equity Lebenszyklus –Realizing Value

KPMG bietet Expertise bei der Erarbeitung von Exit-Optionen und unterstützt in der konkreten Umsetzung

ThePrivate Equity

House

Investments& Deals

Fundraising

RealisingValue Portfolio

ManagementAusstieg planen und durchführen

• Klärung von Exit-Optionen (IPO, Trade Sale, Secondary, etc.)

• Industrielogik im Rahmen des Trade Sales

• Einbezug länderübergreifender Netzwerke

• Vernetzung zu institutionellen Investoren

STRATEGIE

• Vendor Due Dilligence

• Unternehmen für Beauty Contest vorbereiten

• Koordination der Buyer Due Dilligence

• Rechtliche und steuerliche Strukturierung

• Transaktionsmanagement-Unterstützung

TRANSAKTION

Key developments & trends in the LBO market- by Michael DanceKey developments & trends in the LBO market- by Michael Dance

Where Do We Come From, What Are We, Where Do We Go (Gauguin 1897)

AgendaAgenda

Cyclical trendsCyclical trendsSecular trendsSecular trendsRisk and reward Risk and reward -- phantom menace?phantom menace?The next big thing?The next big thing?

Is the balloon about to pop?Is the balloon about to pop?

‘‘Given current leverage levels and recent developments in the Given current leverage levels and recent developments in the economic/credit cycle, the default of a large privateeconomic/credit cycle, the default of a large private--equity equity backed backed …… seems inevitableseems inevitable’’ (FSA Report, Nov 06)(FSA Report, Nov 06)

Governments & regulators are hot on the trail Governments & regulators are hot on the trail …… EU and US EU and US ((DoJDoJ) launch enquiries into Private Equity) launch enquiries into Private EquityCredit ratings for LBO loans are fallingCredit ratings for LBO loans are fallingThe balloon is about to pop The balloon is about to pop ……

The evidence seems compellingThe evidence seems compelling

4.3 4.2 4.65.4 5.7

2.7 2.52.8

2.9 2.9

0x

1x

2x

3x

4x

5x

6x

7x

8x

9x

10x

2002 2003 2004 2005 1H06

Total debt / ebitda Equity / ebitda

LBO purchase & debt multiples

Source: S&P, Alcentra

Rocketing debt multiples fund acquisition premia …

Average EV multiples rocket Average EV multiples rocket to new peak of 8.6x from to new peak of 8.6x from historic lows of 6.7x in 2003 historic lows of 6.7x in 2003 Total leverage also ratchets Total leverage also ratchets up to new high of 5.7x from up to new high of 5.7x from 4.2x in 2003 4.2x in 2003 Average equity fall from to Average equity fall from to 37% in 2003 to new low of 37% in 2003 to new low of 33%33%

The longThe long--term trendsterm trends

The big picture is more positiveThe big picture is more positive

These are cyclical trends These are cyclical trends …… which will lead to defaults which will lead to defaults and bankruptcies and bankruptcies …… but will be healthy for the PE but will be healthy for the PE industry industry The key are the secular trends The key are the secular trends …… where the picture is where the picture is much brighter much brighter

AgendaAgenda

Cyclical trendsCyclical trends

Trend 1 - waves of equityTrend 1 - waves of equity

PE funds have raised $800bn in the last 5 years ($200bn in PE funds have raised $800bn in the last 5 years ($200bn in 2006) and funds are getting larger 2006) and funds are getting larger -- Blackstone up to $20bnBlackstone up to $20bnHedge funds are expanding rapidly and are becoming more Hedge funds are expanding rapidly and are becoming more active in private equity (Perry, active in private equity (Perry, OchOch Ziff, Cerberus, Ziff, Cerberus, OaktreeOaktree))Infrastructure funds (Macquarie, Babcock) are crossingInfrastructure funds (Macquarie, Babcock) are crossing--over to PE type deals over to PE type deals (e.g. (e.g. BAA, LSE, Thames Water)BAA, LSE, Thames Water)IInstitutional investors are increasing their exposure nstitutional investors are increasing their exposure to PEto PE

Blackstone’s $20 billion fund sets the pace …

Trend 2 - oceans of debtTrend 2 - oceans of debt

CDOsCDOs have raised $62 billion by have raised $62 billion by Oct 06 with forward calendar Oct 06 with forward calendar shows further $14 billion shows further $14 billion (IFR (IFR Magazine)Magazine)Hedge funds manage $1.2 Hedge funds manage $1.2 trillion with increasing amounts trillion with increasing amounts allocated to PE debtallocated to PE debtInstitutional investors are Institutional investors are increasingly committed increasingly committed ((CalpersCalpers))PE funds (Carlyle, Blackstone, PE funds (Carlyle, Blackstone, EQT) have raised debt fundsEQT) have raised debt fundsTraditional banks remain activeTraditional banks remain activeOctober record issuance October record issuance €€18.6bn 18.6bn

€0bn

€20bn

€40bn

€60bn

€80bn

€100bn

€120bn

2002 2003 2004 2005 20060

50

100

150

200

250

Q1 Q2 Q3 Q4 Deals (rhs)

EU Loan volumes

Source: S&P / LCD

EU Loan volume

Institutional investors rush in …pushing loan volumes to new peaks

Trend 3 - pricing compression in LBOsTrend 3 - pricing compression in LBOs

255

242

257

246

254

243

225

250

275

300

Q1 05 Q2 05 Q3 05 Q4 05 Q1 06 Q2 063x

4x

5x

6x

7x

8x

9xAv. Senior pricing (bps)

Tot. Leverage (rhs)

Linear (Tot. Leverage (rhs))

Increasing number of allIncreasing number of all--senior senior structures structures -- AVR, AVR, PicardPicard, , ParquesParques ReunidosReunidos, MTU, , MTU, RhiagRhiag, , GrupoGrupo LevantinaLevantina, , OrklaOrkla Media, Media, Phones4U and Phones4U and NycomedNycomed

Margin ratchets bite earlier Margin ratchets bite earlier …… at at 2.5x2.5x--3.5x 3.5x ebitdaebitda vsvs 1.5x 1.5x historicallyhistorically to achieve the lowest to achieve the lowest margins (still about 125 bpsmargins (still about 125 bps--150 150 bps)bps)

Weighted average senior pricing Weighted average senior pricing trends down despite declining trends down despite declining proportion of cheaper TLA and proportion of cheaper TLA and higher overall leveragehigher overall leverage

Pricing trends downPricing trends down

Source: Fitch Ratings

Weighted average senior pricing

Margin ratchets bite earlier … making headline margin “cosmetic”

Trend 3 - pricing compression in LBOs …contTrend 3 - pricing compression in LBOs …cont

8 8 -- 15%15%16 16 -- 18%18%Total cost of fundsTotal cost of funds

returnreturn

spreadspread

spreadspread

marginmarginmarginmargin

marginmargin

c. 18%c. 18%c. 22%c. 22%PIK LoansPIK Loans

700 700 -- 900900N/AN/APIK NotesPIK Notes

c. 500 (8%)c. 500 (8%)c. 1000 (12%)c. 1000 (12%)High YieldHigh Yield

400 Cash pay400 Cash pay400 PIK400 PIK

No WarrantsNo Warrants

500 Cash pay500 Cash pay500 PIK500 PIK

300 Warrants300 Warrants

MezzanineMezzanine375 375 -- 600600N/AN/A2nd Lien2nd Lien

200 / 250 / 300200 / 250 / 300225 / 275 / 325225 / 275 / 325SeniorSenior

2006200620032003DebtDebt

Lower pricing across the capital structure …makes debt more affordable

Trend 4 - rising leverage … across the boardTrend 4 - rising leverage … across the board

4.6 4.74.9

5.9 6.0

4.1 4.0

4.9

5.3

3.63.8

4.2

4.64.9

5.9

3x

4x

5x

6x

7x

2002 2003 2004 2005 H1 2006

> €500m €250 - 499m < €250m

Source: Fitch Ratings

Tot. EBITDA leverage (transaction size)

Total leverage rockets for all deal sizes … as junior debt takes more strain

4.4

4.85.1

5.5

5.9

3.53.8 3.9

4.44.6

3x

4x

5x

6x

7x

2002 2003 2004 2005 H1 2006

Tot. Leverage Senior Leverage

Average EBITDA multiples

Source: S&P

Trend 4 - rising leverage … contTrend 4 - rising leverage … cont

4x

5x

5x

6x

6x

7x

7x

8x

2004 2005 Q106 Q206 Q306RLCP TMTIndustrials Total Market

Source: Fitch Ratings

Total EBITDA leverage

Industrials dip below market average …but other sectors race ahead

Source: Fitch Ratings

Pricing begins to diverge in Pricing begins to diverge in 2006 reflecting cyclical risks2006 reflecting cyclical risksBut some mediocre credits But some mediocre credits getting 7x getting 7x ebitdaebitda leverage leverage with better names attracting with better names attracting more (more (PhadiaPhadia at 8.5x total at 8.5x total debt, debt, FerrettiFerretti at 7.5x plus), at 7.5x plus),

Pricing diverges in 2006Pricing diverges in 2006

Trend 5 - signs of stress emerge... deteriorating creditTrend 5 - signs of stress emerge... deteriorating credit

Of 114 deals rated by Fitch in Of 114 deals rated by Fitch in 1H06, 43% were rated 1H06, 43% were rated BB-- vs. vs. 33% (FY05) and 19% (FY04)33% (FY05) and 19% (FY04)In the same period Fitch In the same period Fitch downgraded 47 credits downgraded 47 credits vsvs 17 17 in 1H05in 1H05Fitch also noted upswing in Fitch also noted upswing in covenant waivers requestedcovenant waivers requested

Shadow Shadow IDRsIDRs trend lowertrend lower

Source: Fitch Ratings

0%

20%

40%

60%

80%

100%

2003 2004 2005 H1 06

CCC & below B- B B+ BB- & above

Issuer IDRs

Defaults remain historically low …but for how long?

NumericableNumericable, , InforInfor Global Solutions, Global Solutions, VersatelVersateland and TravalonTravalon, VNU flexed twice, VNU flexed twice

Flexed deals on Flexed deals on the increasethe increase

5 deals struggle in October 5 deals struggle in October TravalonTravalon flexed up, whilst House of Fraser, flexed up, whilst House of Fraser, Phones4U, Tommy Hilfiger and Lucite also Phones4U, Tommy Hilfiger and Lucite also struggledstruggled

Negative mNegative market arket sentiment sentiment

Lender declines Lender declines increasingincreasing

SymptomSymptom EffectEffect

Banks and mature Banks and mature CDOsCDOs declining 3 in 4 declining 3 in 4 dealsdealsTraditional banks scale back as budgets are Traditional banks scale back as budgets are done and year end loomsdone and year end looms

Trend 5 - signs of stress emerge ….contTrend 5 - signs of stress emerge ….cont

Lender declines, tricky syndications, flexes increase …is the cycle turning?

Source: S&P

AgendaAgenda

Secular trends Secular trends -- the big picturethe big picture

Trend 1 - Institutionalisation of the EU debt marketTrend 1 - Institutionalisation of the EU debt market

0%

25%

50%

75%

1999 2000 2001 2002 2003 2004 2005 1H06

EU Banks Inst. Investors Non EU Banks Securities Firms

Source: S&P / LCD

Investors in EU LBO Loans

Institutional investors overtake banks … as Europe mimics the US model

70%

6%22%

2%

CDO Managers Finance CoCredit Funds Insurance Cos.

Institutional Investors (2005)

CDOs fall from 90% to 70% … as hedge funds expand the market

Trend 2 - Geographic convergenceTrend 2 - Geographic convergence

150

200

250

300

350

400

1996 1999 2Q01 1Q02 4Q02 3Q03 2Q04 1Q05 4Q05 3Q06

Europe US (LIBOR +)

Source: Standard & Poors

Weighted average spread for LBOs

23%

3%

32%62%

18%11%

12% 25%10%

6%

EU USA

Other

RCF

2nd Lien

TLC

TLB

TLA

EU vs USA - Bank loan structure

US pricing converges on Europe EU loan structures mimic US

Trend 2 - Geographic convergence … contTrend 2 - Geographic convergence … cont

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2003 2004 2005 3Q06

RCF TLA TLB TLC 2nd Lien

European Bank loan structures

Source: Standard & Poors

Cheap 2nd Lien plus declining TLA … ease debt service

Growing number of allGrowing number of all--bullet bullet structures structures -- IMO Carwash, IMO Carwash, EutelsatEutelsat, KDG, , KDG, EliorElior, PHS, , PHS, Paragon Healthcare, Travelodge Paragon Healthcare, Travelodge & Kettle Foods& Kettle Foods

2nd2nd Lien imported from US Lien imported from US NNow accounts for 5% of capital ow accounts for 5% of capital structure whilst tstructure whilst total issuance otal issuance hit $5.7bn in 2005hit $5.7bn in 2005

TLA declines from 48% in TLA declines from 48% in ‘‘03 to 03 to under 25% by under 25% by 3Q3Q06 06 Institutional Institutional tranchestranches (TLB & (TLB & TLC) up to 50% (32% & 18%)TLC) up to 50% (32% & 18%)

2nd Lien & shrinking TLA2nd Lien & shrinking TLA

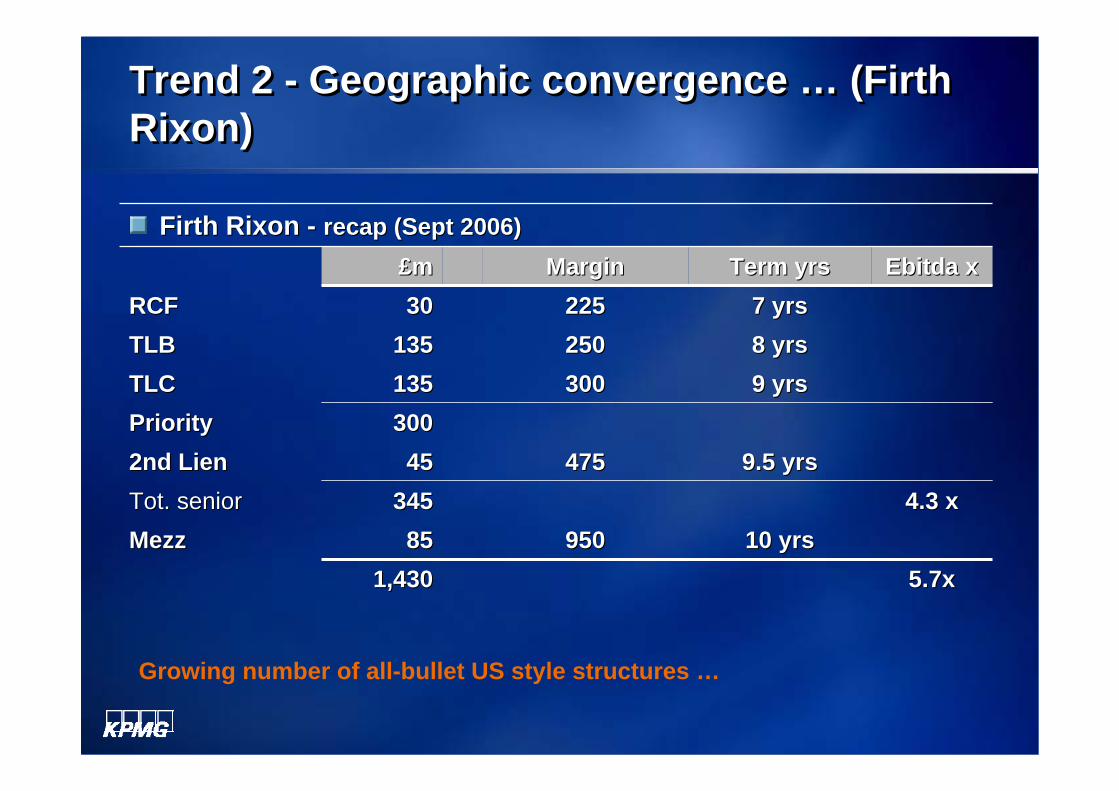

Trend 2 - Geographic convergence … (Firth Rixon)Trend 2 - Geographic convergence … (Firth Rixon)

Firth Firth RixonRixon -- recap (Sept 2006)recap (Sept 2006)

5.7x5.7x1,4301,43010 yrs10 yrs9509508585MezzMezz

4.3 x4.3 x345345Tot. seniorTot. senior9.5 yrs9.5 yrs47547545452nd Lien2nd Lien

300300PriorityPriority9 yrs 9 yrs 300300135135TLCTLC8 yrs8 yrs250250135135TLBTLB7 yrs7 yrs2252253030RCFRCF

EbitdaEbitda xxTerm yrsTerm yrsMarginMargin££mm

Growing number of all-bullet US style structures …

Hybrid Hybrid

Senior High Yield Mezzanine

Senior High Yield MezzanineNew

Model

OldModel

HY HY -- FRNsFRNs with reduced callwith reduced callPIK Notes / LoansPIK Notes / LoansMezzanine Notes (Mezzanine Notes (BaxiBaxi))2nd Lien Notes (2nd Lien Notes (CognisCognis))

1st Lien 1st Lien FRNsFRNs (NSX)(NSX)2nd Lien L2nd Lien LoansoansStretched senior Stretched senior (TLD)(TLD)

Trend 3 - Product convergenceTrend 3 - Product convergence

Trend 3 - Product convergence … part 2 (NXP)Trend 3 - Product convergence … part 2 (NXP)

The The €€6.4bn acquisition of Royal Philips Electronics6.4bn acquisition of Royal Philips Electronics ssemiconductor unit by KKR, emiconductor unit by KKR, SilverlakeSilverlake and and AlpInvestAlpInvest ((OOct 2006)ct 2006)

€€ 4.54.5Total equiv.Total equiv.

n/cn/c 5 (104.3, 102.9, 100)5 (104.3, 102.9, 100)998.625%8.625%€€0.5250.525HY Notes Fix.HY Notes Fix.

Senior rated BB+ and high yield unsecured B+Senior rated BB+ and high yield unsecured B+Senior fixed priced at 330 over the benchmarkSenior fixed priced at 330 over the benchmarkJunior Junior €€ priced at 497 spread over benchmark whilst $ at 493 spreadpriced at 497 spread over benchmark whilst $ at 493 spread

n/cn/c 5 (104.7, 103.2, 101.6,100)5 (104.7, 103.2, 101.6,100)999.5%9.5%$1.250$1.250HY Notes Fix.HY Notes Fix.

n/cn/c 1 (102, 101, 100)1 (102, 101, 100)77E+275E+275€€1.0001.0001st Lien FRN 1st Lien FRN

n/cn/c 4 (103.9, 101.9, 100)4 (103.9, 101.9, 100)887.875%7.875%$1.026$1.0261st Lien Fixed1st Lien Fixed

n/cn/c 2 (102, 101, 100)2 (102, 101, 100)77E+275E+275$1.535$1.5351st Lien FRN 1st Lien FRN

Call protectionCall protectionyryrPricePriceBnBnTrancheTranche

1st Lien FRNs tap wide investors base achieving competitive pricing, greater operational flexibility (fewer covenants & less disclosure) … while bullets relieve debt service & match operational cash flows

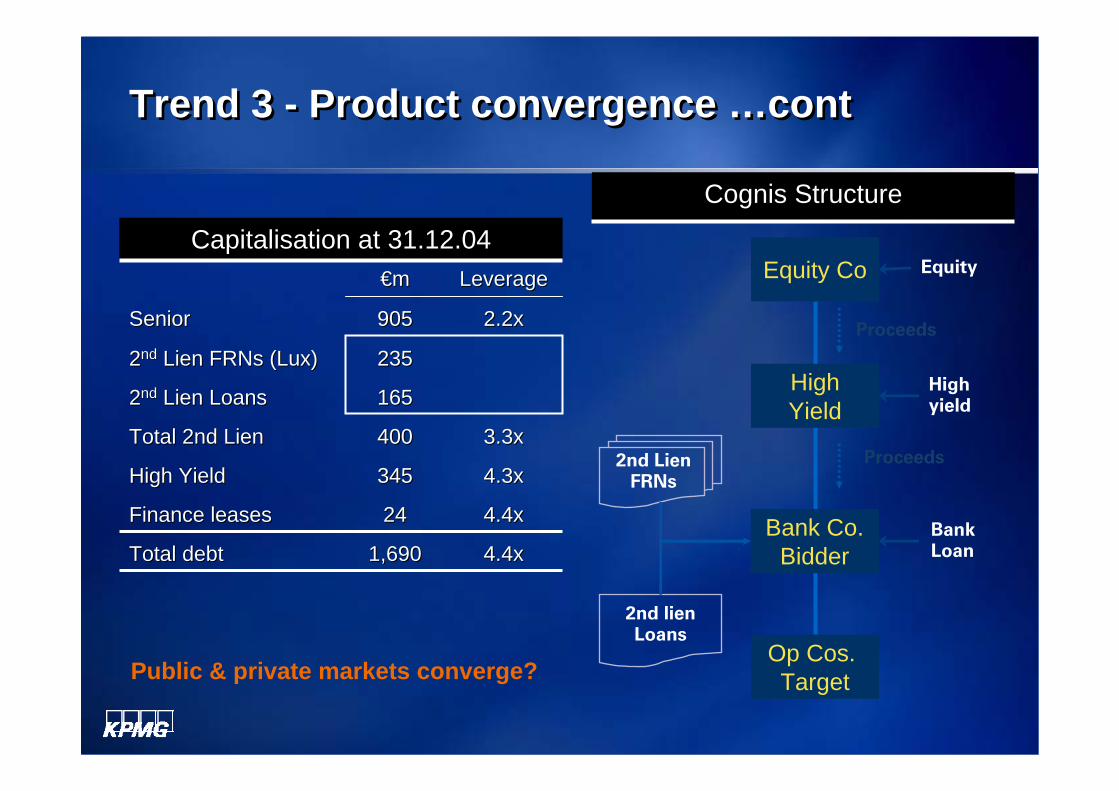

Trend 3 - Product convergence …contTrend 3 - Product convergence …cont

Capitalisation at 31.12.04Capitalisation at 31.12.04

4.4x4.4x1,6901,690Total debtTotal debt

3.3x3.3x400400Total 2nd LienTotal 2nd Lien

4.4x4.4x2424Finance leasesFinance leases

16516522ndnd Lien LoansLien Loans

4.3x4.3x345345High YieldHigh Yield

23523522ndnd Lien FRNs (Lux)Lien FRNs (Lux)

2.2x2.2x905905SeniorSenior

€€mm LeverageLeverage

Op Cos. Target

Bank Co.Bidder

Equity Co Equity

Bank Loan

2nd LienFRNs

HighYield

High yield

Proceeds

Proceeds

2nd lienLoans

Cognis StructureCognis Structure

Public & private markets converge?

Jumbo deals Jumbo deals such as such as HCA, HCA, VivendiVivendiNew segmentsNew segments

Pipelines (Kinder Morgan), Power (Texas Pipelines (Kinder Morgan), Power (Texas GencoGenco), Utilities (Water), Airports (BAA) ), Utilities (Water), Airports (BAA)

Other asset classes Other asset classes --InfrastructureInfrastructure

Australasia Australasia India, China, Asia, South AmericaIndia, China, Asia, South America

New regions and New regions and emerging marketsemerging markets

Sectors previously off Sectors previously off limitslimits

New targets What are they?

CyclicalsCyclicals such as NSX, such as NSX, FreescaleFreescaleReal estateReal estate

Trend 4 - PE firms target new sectorsTrend 4 - PE firms target new sectors

Firms refocus to generate super-returns ... Jumbo deals offer rich pickings

• 3i, Innisfree• KKR, MD (Power & Pipelines)• Macquarie (LSE, BAA, Thames)• Terra Firma (Tank & Rast)• Goldmans ($3bn fund)• Carlyle ($1bn fund)

• Perry, Och Ziff (Peacock) • Cerberus (Alamo, Warner)• Boxclever (Perry, Cerberus)• Texas Genco (KKR vs Cerberus)

• Drax - Power (Perry)• Kaltima Coal

Trend 4 - Sector convergence or collision…contTrend 4 - Sector convergence or collision…cont

InfrastructureProject Finance

Hedge Funds PE Funds

Texas Genco (power) pitted private equity firms against hedge funds ….

6.6x6.6x

5.9x5.9x0.7x0.7x

100%100%461461CapitalisationCapitalisation

89%89%4114115.9x5.9x3.7x3.7x3.2x3.2x2.4x2.4x

Leverage (approx)Leverage (approx)

P2P of Peacock in Nov 2005 by various Hedge Funds which took P2P of Peacock in Nov 2005 by various Hedge Funds which took significant minority stake and provided significant minority stake and provided mezzmezz and PIK and PIK tranchestranches

11%11%5050EquityEquity

18% plus?18% plus?151151PIKPIK950 + warrants950 + warrants3030Junior Junior mezzmezz

9009005555Senior Senior mezzmezz225 225 -- 325325175175SeniorSenior

MarginMargin££mmLoanLoan

Trend 4 - Sector convergence … contTrend 4 - Sector convergence … cont

Six hedge funds team up … to complete a P2P

Trend 5 - Mega dealsTrend 5 - Mega deals

Note: Mezzanine & high yield are mutually exclusive in EuropeNote: Mezzanine & high yield are mutually exclusive in Europe

CasemaCasema covered 2x?covered 2x?1.51.5MezzMezz

c. 20 plusc. 20 plusTotalTotal

HertzHertz6.06.0ABLABLCablecomCablecom €€550m, 550m, RexelRexel €€1bn 1bn rumourrumour??1.01.0PIK NotesPIK NotesIneos issues 2.37bnIneos issues 2.37bn2.5 2.5 High YieldHigh Yield

Wind raised Wind raised €€700m700m1.01.02nd Lien2nd LienTDC raised TDC raised €€8.5bn8.5bn10.010.0SeniorSenior

CommentComment€’€’bnbn equiv.equiv.TrancheTranche

KKRsKKRs $51bn bid for $51bn bid for VivendiVivendi implies debt capacity of c. $40bn at 80% leverageimplies debt capacity of c. $40bn at 80% leverage

A number of mega funds have raised over $10 billion each KKR, A number of mega funds have raised over $10 billion each KKR, PermiraPermira, TPG , TPG ……while Blackstone reopens fund in push to reach $20bnwhile Blackstone reopens fund in push to reach $20bn

AgendaAgenda

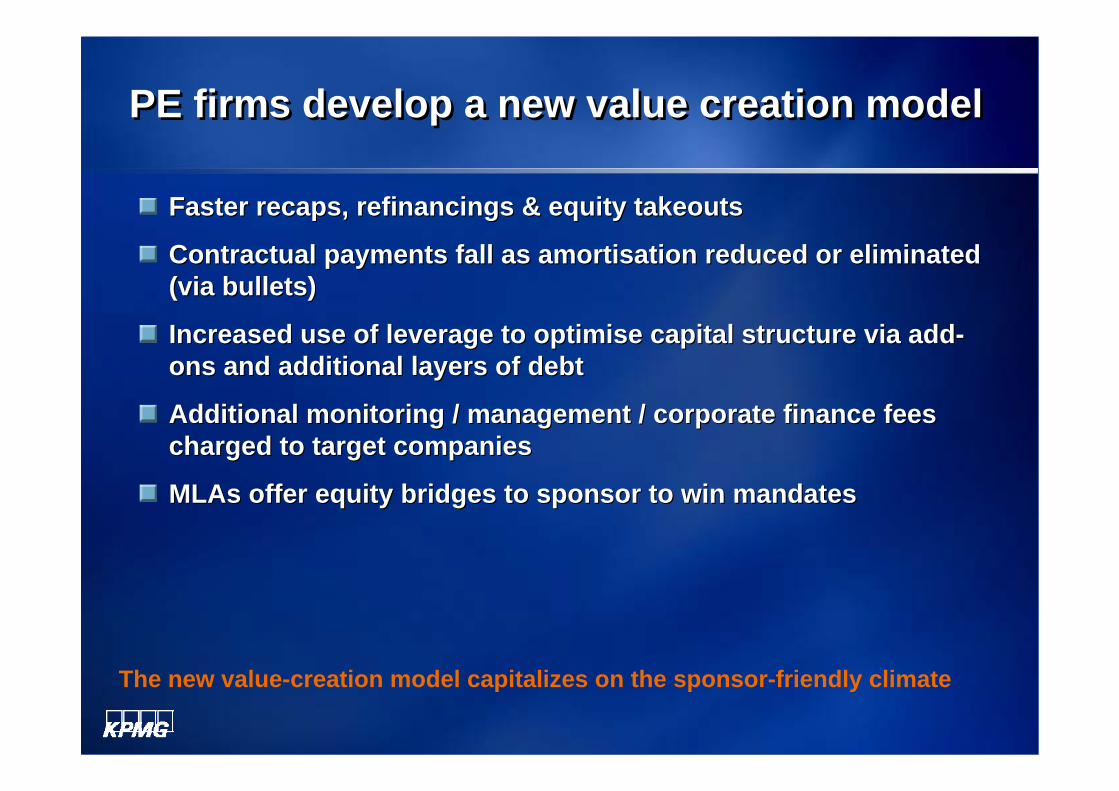

The new value creation modelThe new value creation model

Faster recaps, Faster recaps, refinancingsrefinancings & equity takeouts & equity takeouts

Contractual payments fall as Contractual payments fall as amortisationamortisation reduced or eliminated reduced or eliminated (via bullets)(via bullets)

Increased use of leverage to Increased use of leverage to optimiseoptimise capital structure via addcapital structure via add--ons and additional layers of debtons and additional layers of debt

Additional monitoring / management / corporate finance fees Additional monitoring / management / corporate finance fees charged to target companiescharged to target companies

MLAsMLAs offer equity bridges to sponsor to win mandatesoffer equity bridges to sponsor to win mandates

PE firms develop a new value creation modelPE firms develop a new value creation model

The new value-creation model capitalizes on the sponsor-friendly climate

Step 1 - Faster recapsStep 1 - Faster recaps

24

20

29

18%

29%

37%

64%

77%

86%

10

15

20

25

30

35

40

2004 2005 1H0610%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Months to recycling (lhs)Annualised IRR (rhs)Equity repaid (rhs)

Months to recap falls from high Months to recap falls from high of 29 months in 2004 to 20 and of 29 months in 2004 to 20 and 24 months in 2005 and 1H06 24 months in 2005 and 1H06 respectivelyrespectively

Original equity repaid climbs Original equity repaid climbs from 66% in 2004 to 77% (05) from 66% in 2004 to 77% (05) and 86% in 1H06 as leverage and 86% in 1H06 as leverage rises in recapsrises in recaps

Recaps boost Recaps boost IRIRRsRs

Source: Fitch Ratings

European Bank loan structures

Faster recaps with higher leverage boost IRR

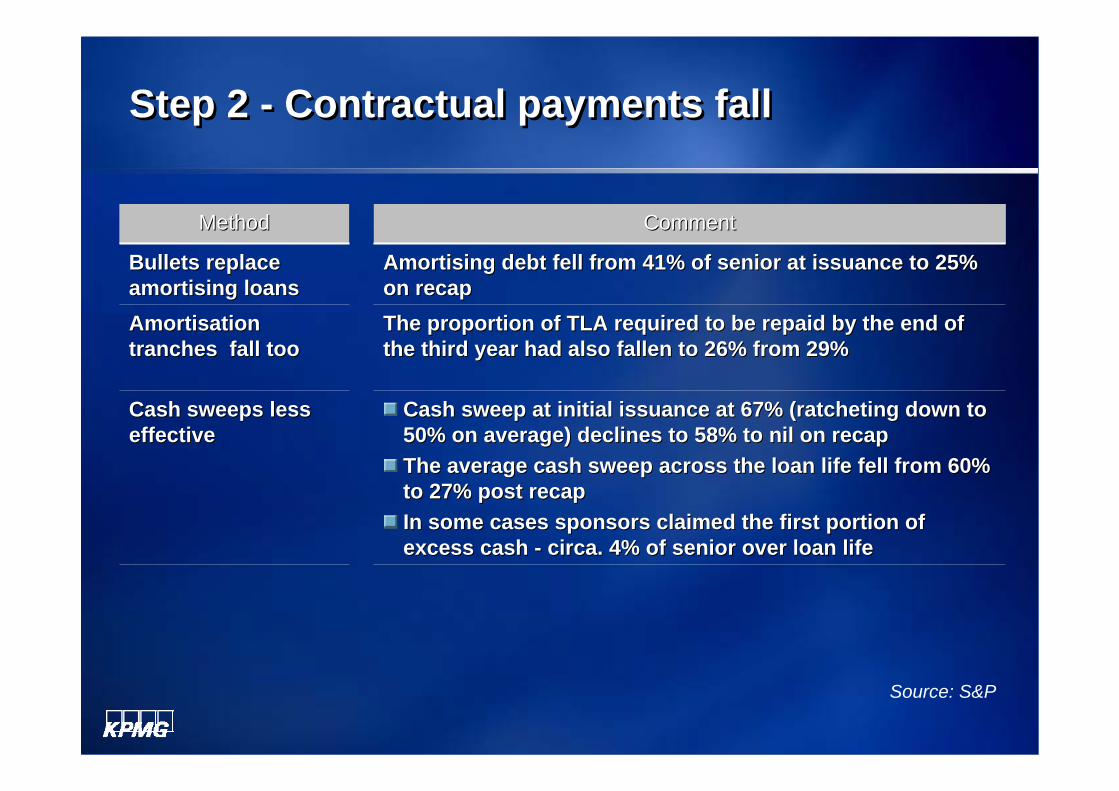

Step 2 - Contractual payments fall Step 2 - Contractual payments fall

The proportion of TLA required to be repaid by the end of The proportion of TLA required to be repaid by the end of the third year had also fallen to 26% from 29%the third year had also fallen to 26% from 29%

Amortisation Amortisation tranchestranches fall toofall too

AmortisingAmortising debt fell from 41% of senior at issuance to 25% debt fell from 41% of senior at issuance to 25% on recapon recap

Bullets replace Bullets replace amortisingamortising loansloans

Cash sweep at initial issuance at 67% (ratcheting down to Cash sweep at initial issuance at 67% (ratcheting down to 50% on average) declines to 58% to nil on recap50% on average) declines to 58% to nil on recapThe average cash sweep across the loan life fell from 60% The average cash sweep across the loan life fell from 60% to 27% post recapto 27% post recapIn some cases sponsors claimed the first portion of In some cases sponsors claimed the first portion of excess cash excess cash -- circa. 4% of senior over loan lifecirca. 4% of senior over loan life

Cash sweeps Cash sweeps less less effectiveeffective

CommentCommentMethod Method

Source: S&P

Step 3 - New instruments & more bullets Step 3 - New instruments & more bullets

850/900 ?850/900 ?350.0350.0PIKPIK

450/550450/55055.055.0100100MezzMezz

22522550.050.050.050.0RCFRCF

325325189.25189.2583.7583.75TLCTLC

22522530.030.0AcquisitionAcquisition

New Look New Look Recap in June 2005 released Recap in June 2005 released ££100m dividend & further with100m dividend & further with££350m 350m PIK added May 06 in place of IPO PIK added May 06 in place of IPO

50050080.080.02nd Lien2nd Lien

620.2620.2385.0385.0Tot. seniorTot. senior

275275189.25189.2583.7583.75TLBTLB

225225161.7161.7167.5167.5TLATLA

MarginMarginMay 06May 06Jun 05Jun 05April 04April 04££mm

Equity released in 2005 with TLB/C and 2nd Lien … & in 2006 with PIK loan

Step 4 - Additional fees & equity bridges increasingStep 4 - Additional fees & equity bridges increasing

Blackstone charged Celanese $45m Blackstone charged Celanese $45m for advisory work done on for advisory work done on the 2004 acquisition the 2004 acquisition -- double the $18m Celanese paid Goldmandouble the $18m Celanese paid Goldman

Warner MusicWarner Music paid its owners, Bain Capital, Thomas H. Lee, and paid its owners, Bain Capital, Thomas H. Lee, and Providence Equity Partners, a $75 million advisory feeProvidence Equity Partners, a $75 million advisory fee

Warner Warner ChilcottChilcott four sponsors (Bain, DLJ, J P Morgan & Tfour sponsors (Bain, DLJ, J P Morgan & Thomas homas H. Lee) charged $27.4 million as compensation for terminating H. Lee) charged $27.4 million as compensation for terminating their advisory arrangements when the company went publictheir advisory arrangements when the company went public

MLAsMLAs expected to bridge sponsor equity post completionexpected to bridge sponsor equity post completion

Fees and equity bridges boost IRR further …

AgendaAgenda

Risk Risk –– phantom menace?phantom menace?

Cyclical risks - a soft landing in prospect?Cyclical risks - a soft landing in prospect?

The main cyclical risks are high leverage and increasing use of The main cyclical risks are high leverage and increasing use of nonnon--amortisingamortising / bullet structures/ bullet structuresHowever this has been mitigated by falling debt service through However this has been mitigated by falling debt service through lower pricinglower pricing and falling amortization and falling amortization When defaults occur When defaults occur …… Lenders seem willing to grant waivers and Lenders seem willing to grant waivers and extensions to retain the goodwill of sponsorsextensions to retain the goodwill of sponsorsAggressive Aggressive lenders have been emasculated by lenders have been emasculated by ““covenantcovenant--litelite””documentation which allow sponsors to documentation which allow sponsors to ““divide and ruledivide and rule””

Lower debt service mitigates the effects of rising leverage … Lenders have far fewer rights now & are reluctant to “rock the boat”

Covenant-lite documentationCovenant-lite documentation

Requirement for unanimous consent is being eroded Requirement for unanimous consent is being eroded --Supermajorities (75 Supermajorities (75 --80%) can now carry decisions with 80%) can now carry decisions with dissenters being dissenters being ““yyankedanked”” at parat par

VotingVoting

Sponsors seek to control syndicates by limiting transfer Sponsors seek to control syndicates by limiting transfer before & after defaultbefore & after default

TransferabilityTransferability

Borrower can Borrower can ““curecure”” by paying in to overcome cashby paying in to overcome cash--flow or flow or EBITDA shortfallEBITDA shortfall

Equity cureEquity cure

Borrower can call loans of any dissenting minoritiesBorrower can call loans of any dissenting minoritiesYank the bankYank the bank

NonNon--voting / attendance means lenders excluded from voting / attendance means lenders excluded from quorum & ignored quorum & ignored

Snooze and Snooze and loselose

Financial covenant breach Financial covenant breach disdis--applied 1st timeapplied 1st timeMulliganMulligan

Covenant-lite loans allow sponsors to call the shots

Government interference is the main concernGovernment interference is the main concern

Bullets and recaps have shifted risks from sponsors to lenders Bullets and recaps have shifted risks from sponsors to lenders …… so refinancing risk is a growing issue ... for lendersso refinancing risk is a growing issue ... for lendersGovernments interference (negative public sentiment)Governments interference (negative public sentiment)

Protectionism Protectionism ……. protect the national champion. protect the national championRegulators Regulators -- DoJDoJ enquiry into Clubs, SEC, FSA etcenquiry into Clubs, SEC, FSA etcTaxTax

…… But continued overBut continued over--regulation of public markets will continue regulation of public markets will continue to boost private equity activity (Sarbanes Oxley) to boost private equity activity (Sarbanes Oxley)

Governments (driven by negative public sentiment) are a real risk …… making the case for private equity is key

The next big thing - will this restore the balance?The next big thing - will this restore the balance?

Infrastructure opportunities Infrastructure opportunities -- Governments donGovernments don’’t have the t have the financial resources to meet increasing demands for (expensive) financial resources to meet increasing demands for (expensive) public services or meet liabilities (e.g. unfunded pensions)public services or meet liabilities (e.g. unfunded pensions)Traditional public procurement is typically inefficient Traditional public procurement is typically inefficient -- over over budget and late (e.g. Scottish Parliament budget and late (e.g. Scottish Parliament -- 10x over budget)10x over budget)The TransThe Trans--Texan Highway project is worth $187 billionTexan Highway project is worth $187 billionEurope, Asia, Rest of World?Europe, Asia, Rest of World?

The demand is vast …. the issue will be how to provide the human/intellectual and financial capital to feed the demand.”Source: KPMG Report “PFI - over the next 10 years”

The global market potential The global market potential …… trillionstrillions

In summary - a cautious opinionIn summary - a cautious opinion

Although cyclical trends are at their peak defaults will Although cyclical trends are at their peak defaults will be confined to cyclical sectors and some overbe confined to cyclical sectors and some over--

leveraged dealsleveraged dealsConsensual restructurings will dominate as lenders Consensual restructurings will dominate as lenders

appease sponsors and lack teeth to bite appease sponsors and lack teeth to bite TThe longhe long--term outlook for private equity is very term outlook for private equity is very

positive positive …… unless Governments interfereunless Governments interfere

Michael DanceMichael Dance

Michael Dance is the Managing Director of MBO Training InternatiMichael Dance is the Managing Director of MBO Training International, a company providing training and onal, a company providing training and consultancy services on acquisition finance, leveraged and managconsultancy services on acquisition finance, leveraged and management buyouts and project finance to ement buyouts and project finance to clients in the Europe, The Middle East, North America and Africaclients in the Europe, The Middle East, North America and Africa. . His clients embrace a wide selection of professionals involved iHis clients embrace a wide selection of professionals involved in those industries. Over the past few n those industries. Over the past few years he has presented inyears he has presented in--house programmes to KPMG Corporate Finance, KPMG Transaction Serhouse programmes to KPMG Corporate Finance, KPMG Transaction Services, vices, PWC, E&Y, Close Brothers, AIB, Morgan Stanley, Barclays Capital,PWC, E&Y, Close Brothers, AIB, Morgan Stanley, Barclays Capital, Mizuho, CIBC, Deutsche Bank, Mizuho, CIBC, Deutsche Bank, CinvenCinven, SJ Berwin, , SJ Berwin, MacfarlanesMacfarlanes, Bingham McCutchen, Berwin Leighton , Bingham McCutchen, Berwin Leighton PaisnerPaisner, , OgierOgier, White & Case, , White & Case, National Australia Group (Europe), Lloyds TSB, Rand Merchant BanNational Australia Group (Europe), Lloyds TSB, Rand Merchant Bank, Bank of China. He is on the k, Bank of China. He is on the transaction panel for Royal Bank of Scotland via a venture with transaction panel for Royal Bank of Scotland via a venture with SJ Berwin. Over the past few years he SJ Berwin. Over the past few years he has been a visiting lecturer on Infrastructure Finance at the CAhas been a visiting lecturer on Infrastructure Finance at the CASS Business School for the Master SS Business School for the Master Science programme in Business Administration and Finance. Science programme in Business Administration and Finance. He has a number of clients whom he has advised on mezzanine and He has a number of clients whom he has advised on mezzanine and other forms acquisition finance and other forms acquisition finance and is a member of is a member of IIRIIR’’ss advisory panel for their Mezzanine Conference. He was involved advisory panel for their Mezzanine Conference. He was involved in the EU in the EU PharePhareprogramme during which advised the Estonian Government on its prprogramme during which advised the Estonian Government on its privatisation programme. ivatisation programme. Prior to founding MBO Training International, Michael was head oPrior to founding MBO Training International, Michael was head of cross border M&A at f cross border M&A at MiesPiersonMiesPierson in in London, an Assistant Director at Hoare London, an Assistant Director at Hoare GovettGovett and an executive at and an executive at LazardLazard Brothers. He qualified as a Brothers. He qualified as a lawyer in South Africa and as a Chartered Accountant with Deloitlawyer in South Africa and as a Chartered Accountant with Deloitte. He holds various degrees including te. He holds various degrees including BA, LLB, B BA, LLB, B ComptCompt ((HonsHons), Diploma in Taxation and is a CA (SA).), Diploma in Taxation and is a CA (SA).

44

Claudio SteffenoniClaudio SteffenoniPartner, Partner, HeadHead of PE Groupof PE Group

KPMGKPMGBadenerstrasse 172Badenerstrasse 172PostfachPostfach8026 Z8026 Züürichrich

TelefonTelefon +41 44+41 44 249 31 08249 31 [email protected]@kpmg.com

ContactContact