Klöckner & Co - 1st Klöckner & Co Analysts' and Investors' Meeting September 19, 2007

15

Klckner & Co AG 1st Klckner & Co Analysts and Investors Meeting Switzerland, September 19, 2007 Ueli Hartmann, CEO Switzerland

-

Upload

kloeckner-co-se -

Category

Investor Relations

-

view

39 -

download

1

Transcript of Klöckner & Co - 1st Klöckner & Co Analysts' and Investors' Meeting September 19, 2007

Klöckner & Co AG1st Klöckner & CoAnalysts� and Investors� Meeting

Switzerland, September 19, 2007

Ueli Hartmann, CEO Switzerland

2

Introduction

Facts & Key Figures

Activities & Markets

Locations

Additional Division

Structure & Organisation

Business Key Drivers

Potentials & Outlook

3

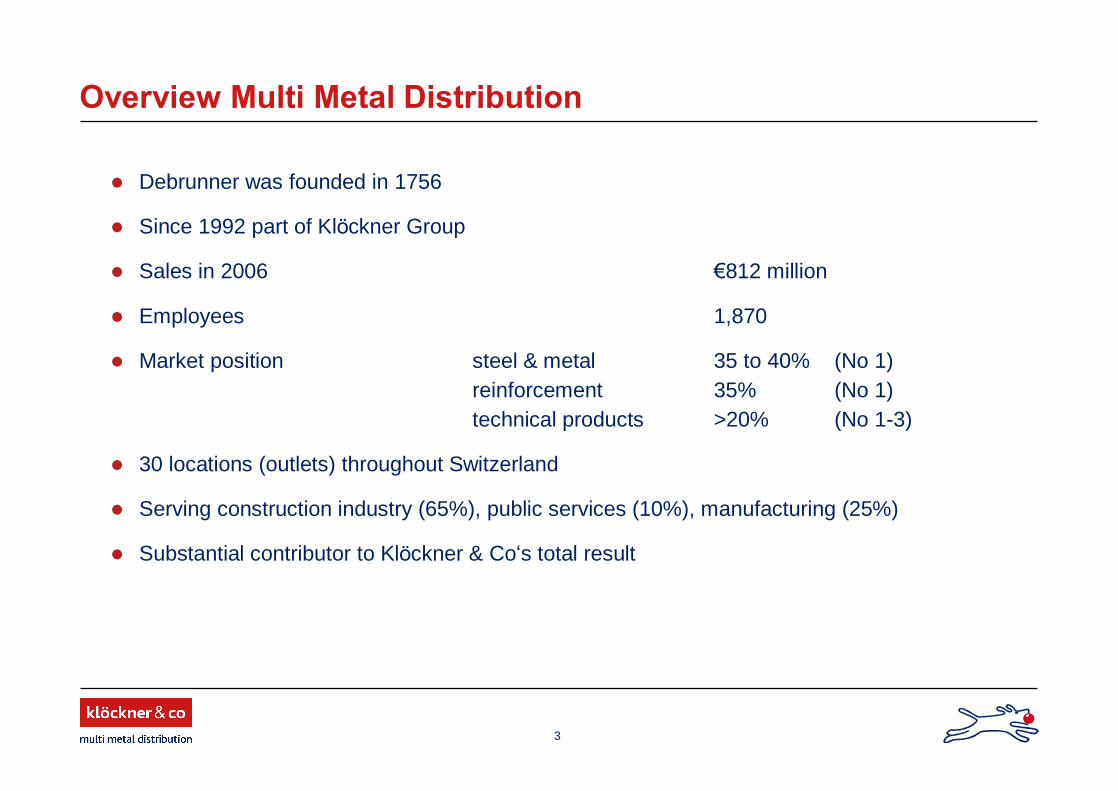

Overview Multi Metal Distribution

Debrunner was founded in 1756

Since 1992 part of Klöckner Group

Sales in 2006 �812 million

Employees 1,870

Market position steel & metal 35 to 40% (No 1)reinforcement 35% (No 1)technical products >20% (No 1-3)

30 locations (outlets) throughout Switzerland

Serving construction industry (65%), public services (10%), manufacturing (25%)

Substantial contributor to Klöckner & Co�s total result

4

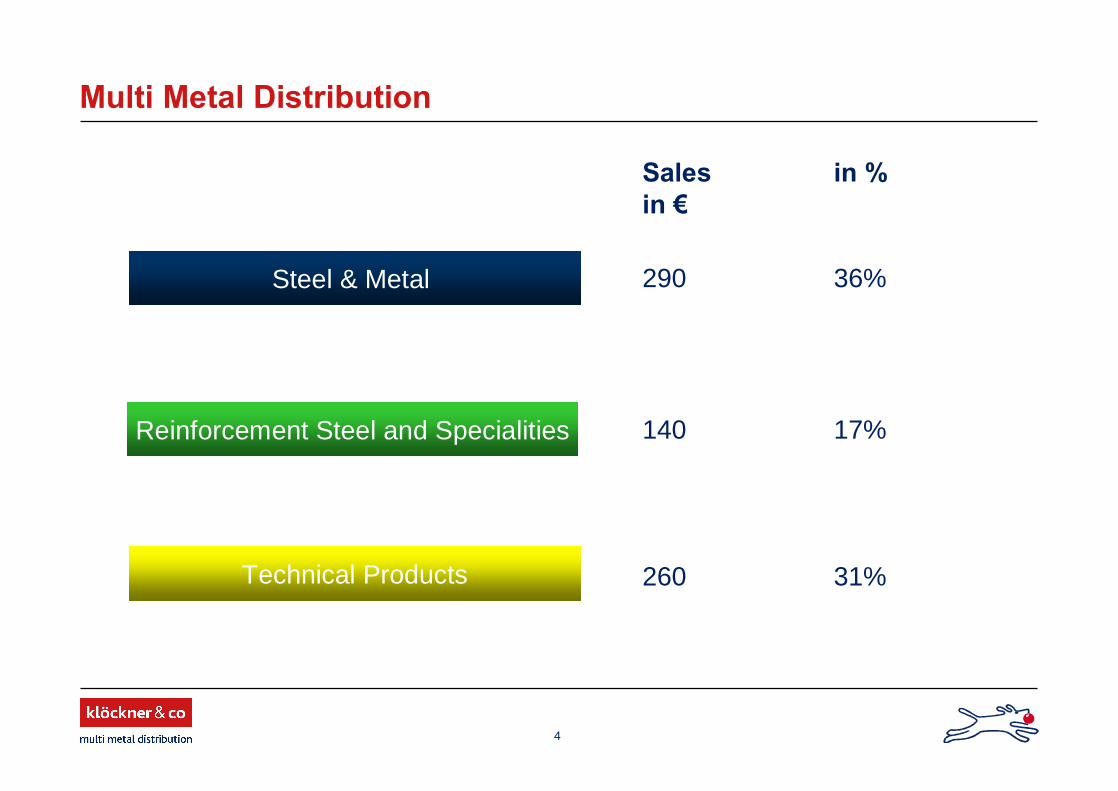

Multi Metal Distribution

Sales in %in �

290 36%

140 17%

260 31%

Steel & Metal

Reinforcement Steel and Specialities

Technical Products

5

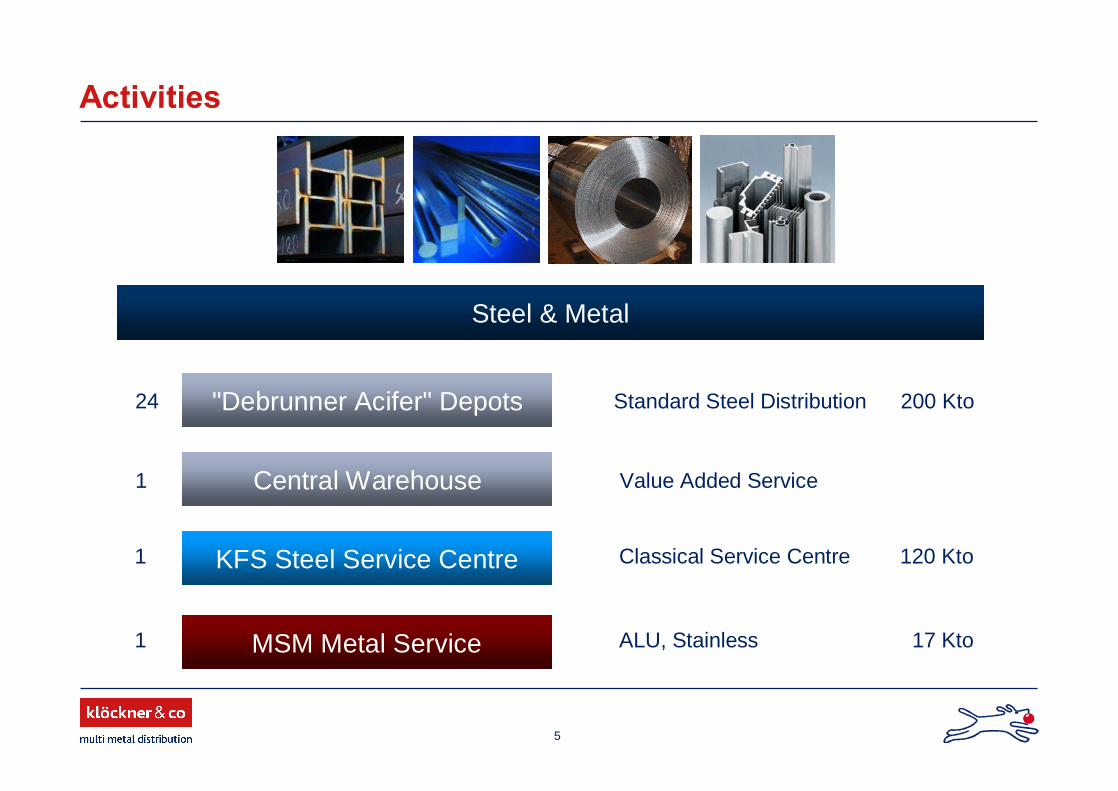

Activities

1 ALU, Stainless 17 Kto

24 Standard Steel Distribution 200 Kto

1 Value Added Service

1 Classical Service Centre 120 Kto

Steel & Metal

"Debrunner Acifer" Depots

Central Warehouse

KFS Steel Service Centre

MSM Metal Service

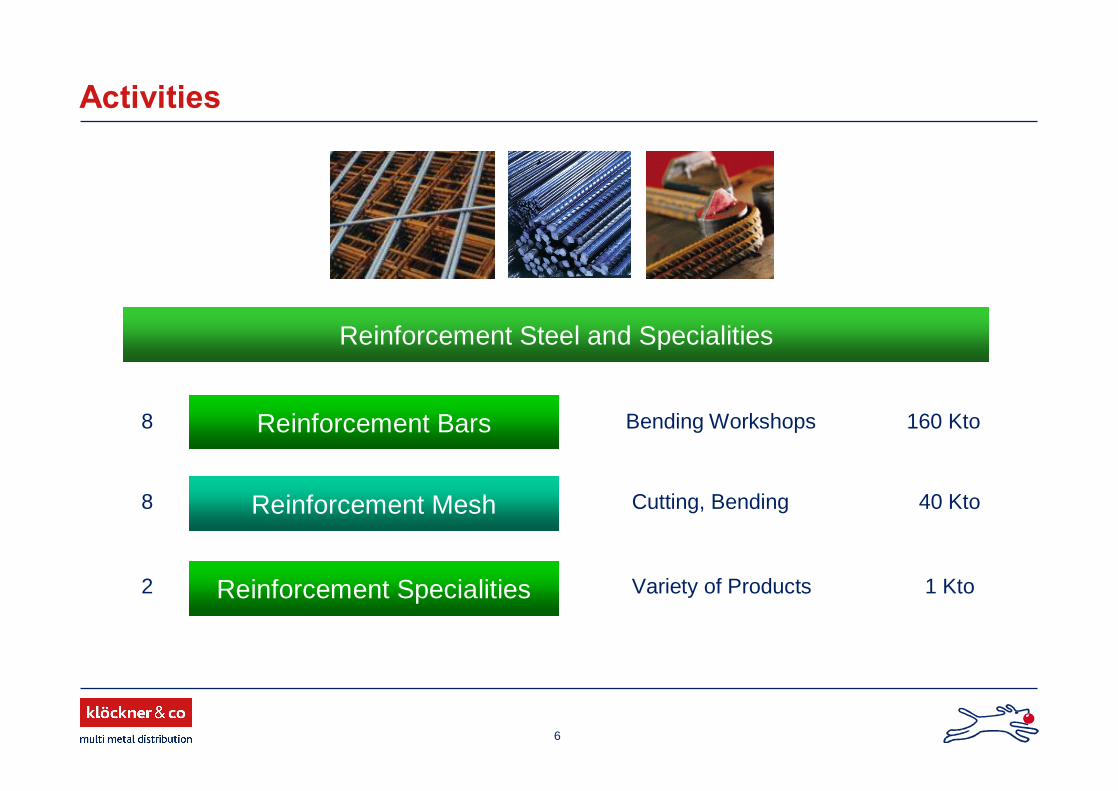

6

Activities

2 Variety of Products 1 Kto

8 Cutting, Bending 40 Kto

Reinforcement Steel and Specialities

8 Bending Workshops 160 KtoReinforcement Bars

Reinforcement Mesh

Reinforcement Specialities

7

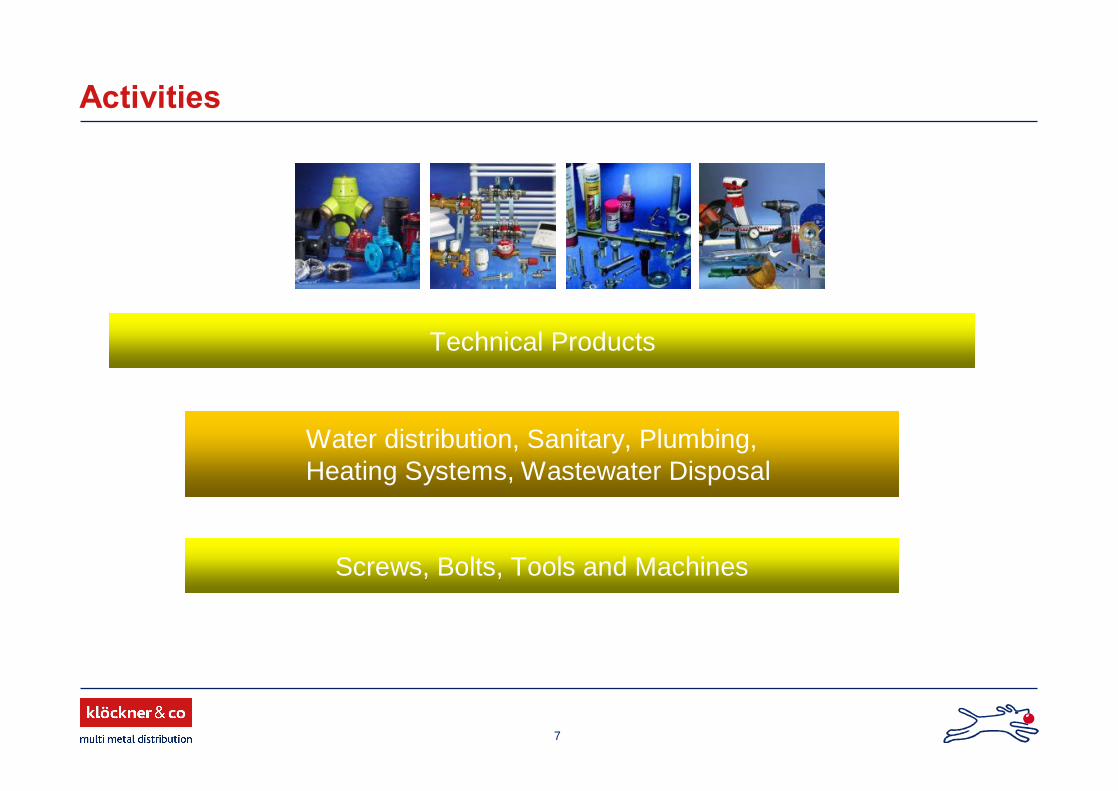

Activities

Technical Products

Water distribution, Sanitary, Plumbing, Heating Systems, Wastewater Disposal

Screws, Bolts, Tools and Machines

8

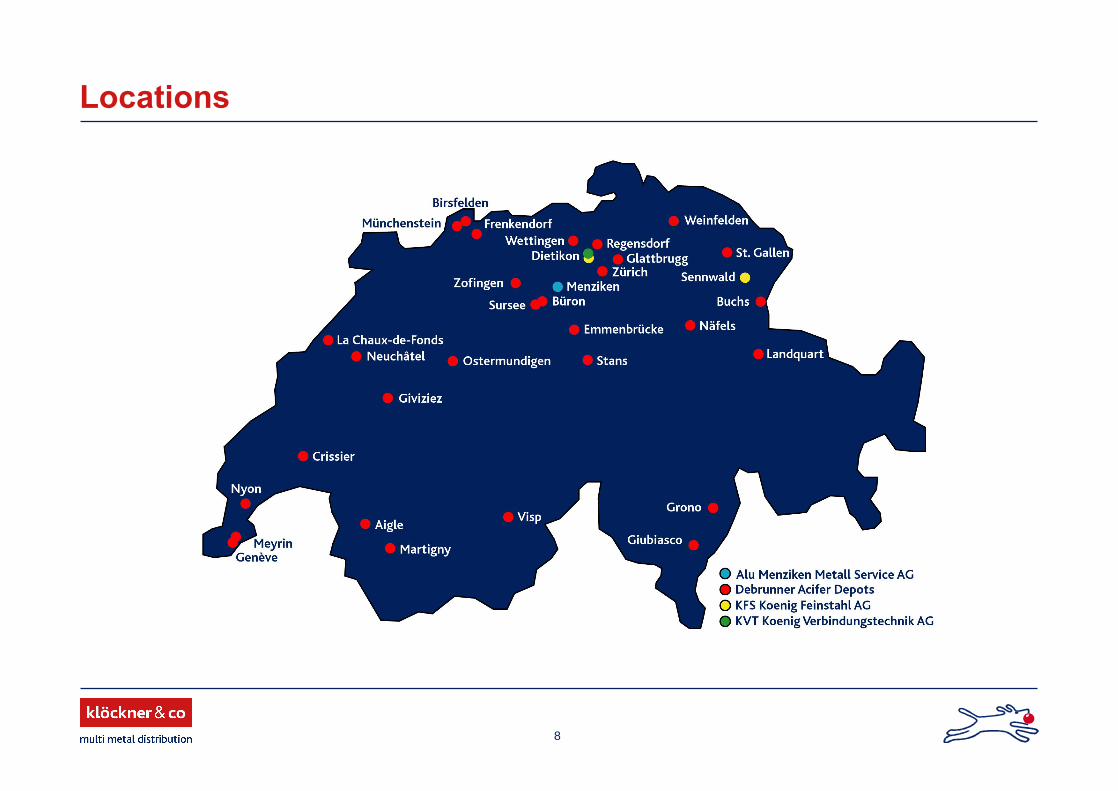

Locations

9

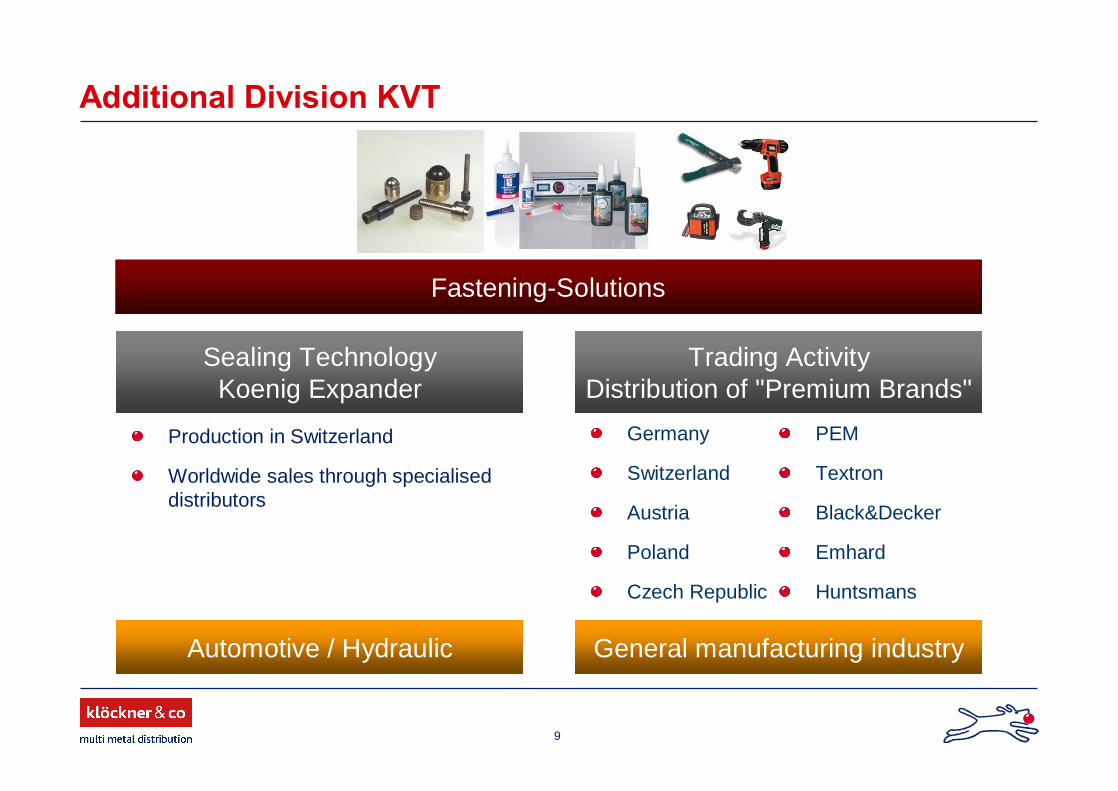

Additional Division KVT

Fastening-Solutions

Sealing TechnologyKoenig Expander

Trading ActivityDistribution of "Premium Brands"

Germany

Switzerland

Austria

Poland

Czech Republic

PEM

Textron

Black&Decker

Emhard

Huntsmans

General manufacturing industryAutomotive / Hydraulic

Production in Switzerland

Worldwide sales through specialised distributors

10

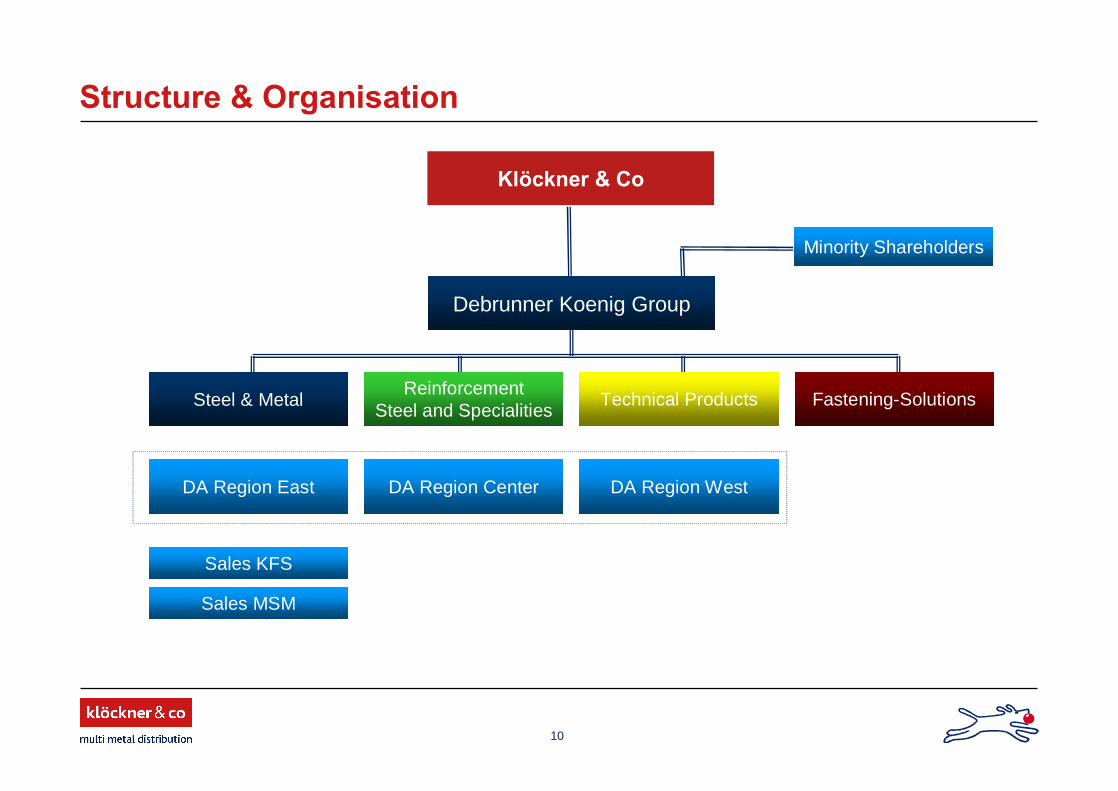

Structure & Organisation

Steel & MetalReinforcement

Steel and SpecialitiesTechnical Products Fastening-Solutions

Debrunner Koenig Group

DA Region East DA Region Center DA Region West

Klöckner & Co

Minority Shareholders

Sales KFS

Sales MSM

11

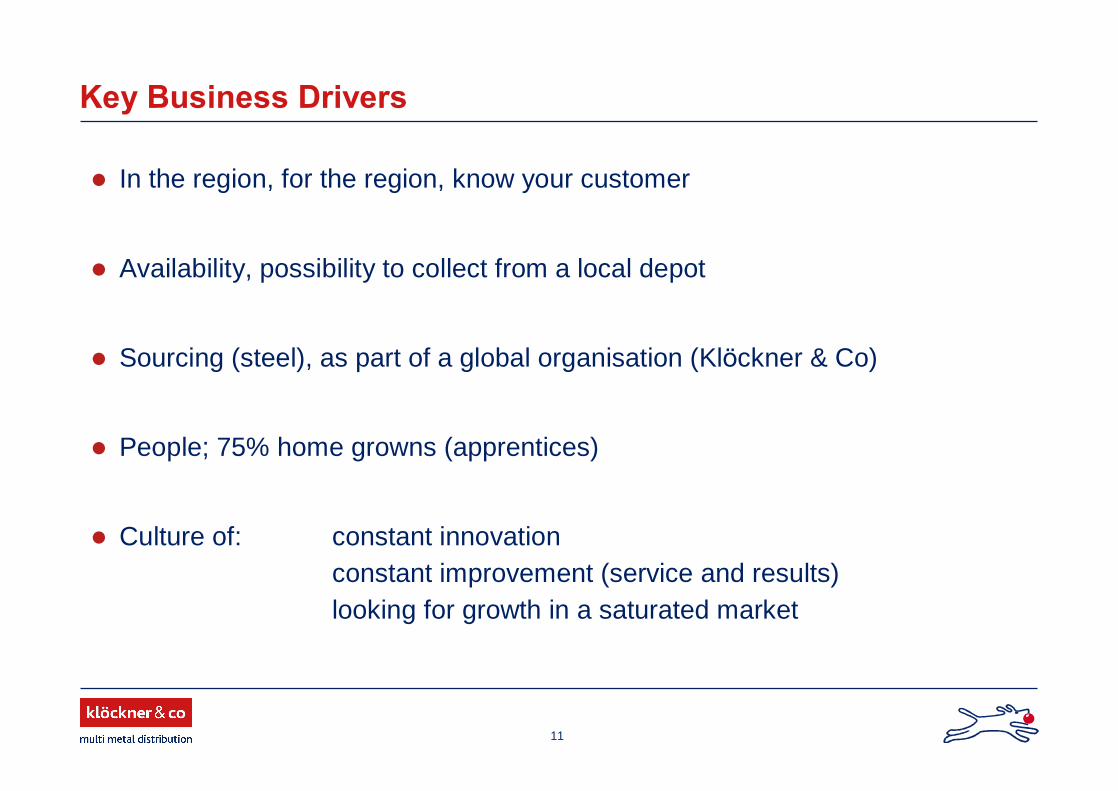

Key Business Drivers

In the region, for the region, know your customer

Availability, possibility to collect from a local depot

Sourcing (steel), as part of a global organisation (Klöckner & Co)

People; 75% home growns (apprentices)

Culture of: constant innovationconstant improvement (service and results)looking for growth in a saturated market

12

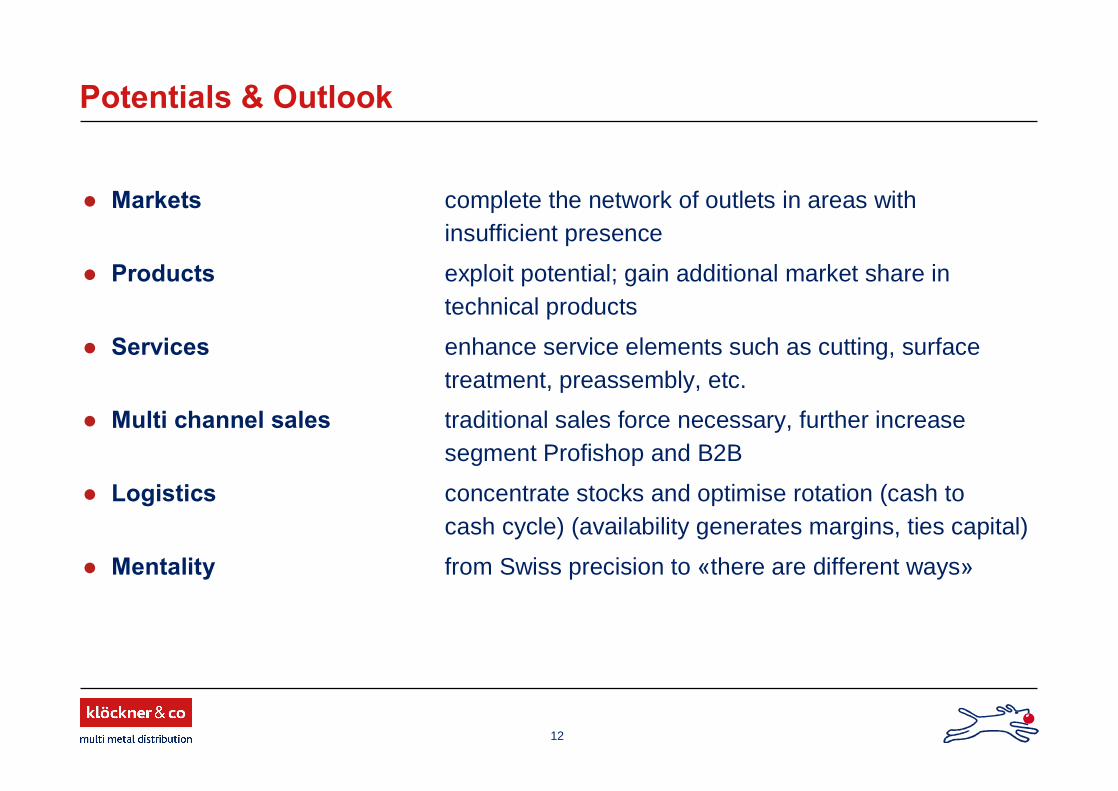

Potentials & Outlook

Markets complete the network of outlets in areas with insufficient presence

Products exploit potential; gain additional market share in technical products

Services enhance service elements such as cutting, surface treatment, preassembly, etc.

Multi channel sales traditional sales force necessary, further increase segment Profishop and B2B

Logistics concentrate stocks and optimise rotation (cash to cash cycle) (availability generates margins, ties capital)

Mentality from Swiss precision to «there are different ways»

13

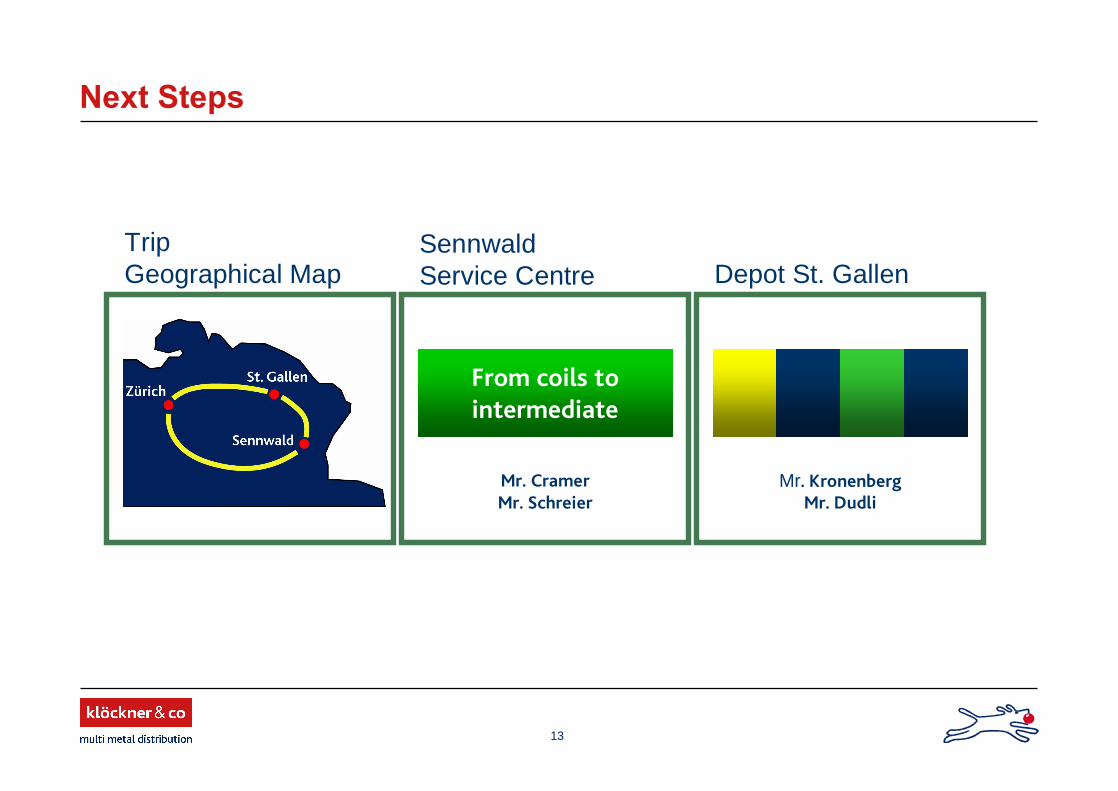

Next Steps

SennwaldService Centre

TripGeographical Map Depot St. Gallen

Mr. CramerMr. Schreier

Mr. KronenbergMr. Dudli

From coils tointermediate

14

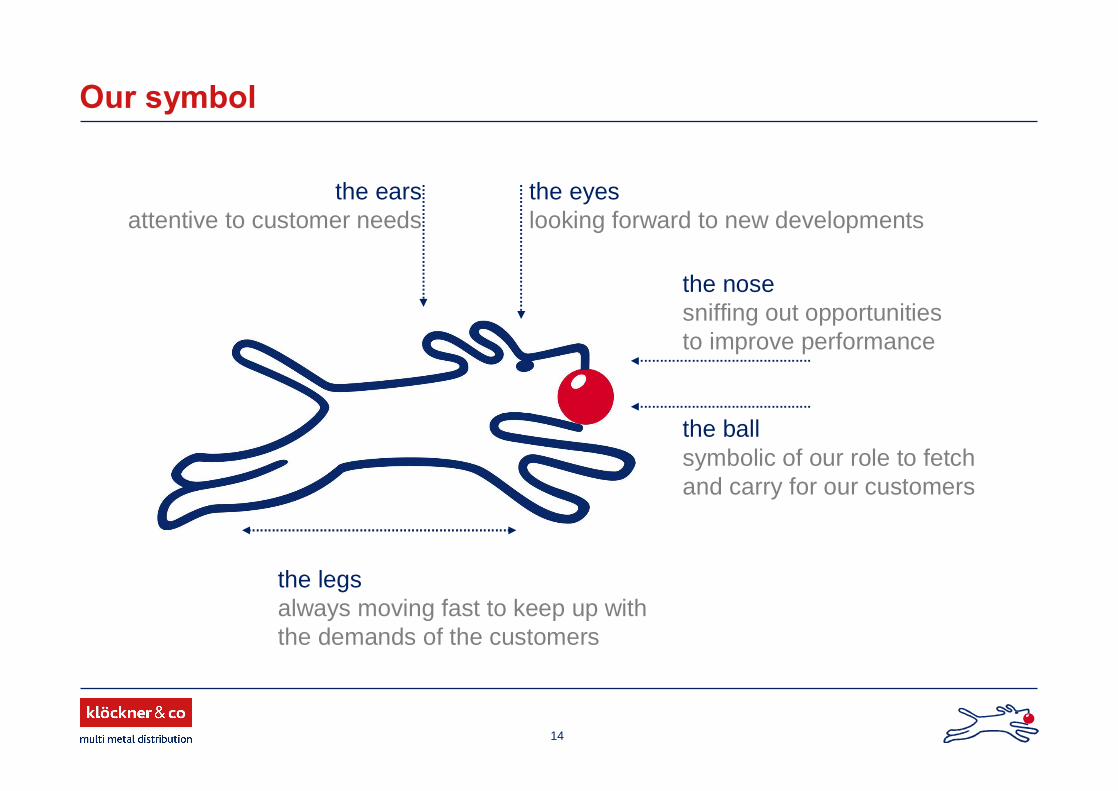

Our symbol

the earsattentive to customer needs

the eyeslooking forward to new developments

the nosesniffing out opportunitiesto improve performance

the ballsymbolic of our role to fetchand carry for our customers

the legsalways moving fast to keep up withthe demands of the customers

15

Disclaimer

This presentation contains forward-looking statements. These statements use words like "believes, "assumes," "expects" or similar formulations. Various known and unknown risks, uncertainties and other factors could lead to material differences between the actual future results, financial situation, development or performance of our company and those either expressed or implied by these statements. These factors include, among other things:

Downturns in the business cycle of the industries in which we compete; Increases in the prices of our raw materials, especially if we are unable to pass these costs

along to customers; Fluctuation in international currency exchange rates as well as changes in the general

economic climateand other factors identified in this presentation.In view of these uncertainties, we caution you not to place undue reliance on these forward-looking statements. We assume no liability whatsoever to update these forward-looking statements or to conform them to future events or developments.