Kirkpatrick Service Description and Manual

12

Kirkpatrick & Company, Inc. 1 www.charleskirkpatrick.com Kirkpatrick’s Market Strategist Description of Service Purpose of Service The Market Strategist subscription service provides market timing and stock selection based on a long series of studies by Charles D. Kirkpatrick II, CMT (co-author of Technical Analysis: The Complete Resource for Financial Market Technicians, 3 rd ed., Pearson Education as FT Press, New York, 2015.) The weekly and monthly reports offer investment managers timing signals for market trends, designed for the formulation of long-term investment strategies and short-term trading tactics. The reports also provide stock selection using relative price strength analysis, one of the only methods to statistically refute both the efficient markets hypothesis and random walk hypothesis in stock prices. The reports fully disclose the methods, formulas, variables, and parameters included in the timing and selection models. All models are derived through rigorous walk-forward optimizing analysis. Format of Service Weekly: The Weekly Market Strategist is sent to subscribers each weekend, and uses daily market price data to time trends in the U.S stock market, the U.S. long-term bond market, gold, crude oil, and emerging foreign stock markets. The report includes updated intermediate- term charts and a detailed analysis of those charts to derive market-timing signals. It also includes the Bargain List of stocks that have met proscribed relative strength purchase requirements, and a list of additions and deletions to and from the list for that week. The list includes ranks in relative price strength, relative earnings growth, the relative price-to-sales ratio, date and price when added to the list, profit or loss, and a suggested protective stop level for each security. Stock charts include a legend that describes the abbreviated symbols on each chart, and a table describes the Bargain List rules. Monthly: The Monthly Overview is a 9 to 12 page report that provides charts and analysis of intermediate- and long-term trends in the U.S. stock market, U.S bond market, gold, crude oil, industrial raw materials, agricultural product prices, foreign stock markets in aggregate and the Japanese stock market. It occasionally includes the timing results of three economic models that were the subject of the studies reported in my book (Time the Markets: Using Technical Analysis to Interpret Economic Data, Pearson Education as FT Press, 2012) and reports the annual performance of the Bargain List over the past three years. Investment Philosophy Disputing the concept of using diversification as a means of decreasing risk in stock portfolios, my investment philosophy encompasses two principle concepts: market timing and relative strength stock selection.

-

Upload

kirkpatrick-company-inc -

Category

Documents

-

view

244 -

download

4

description

Kirkpatrick & Company, Inc. publishes a weekly and monthly technical letter on trading markets. This publication describes the content, methods used, and performance.

Transcript of Kirkpatrick Service Description and Manual

Kirkpatrick & Company, Inc.

1

www.charleskirkpatrick.com

Kirkpatrick’s Market Strategist

Description of Service

Purpose of Service

The Market Strategist subscription service provides market timing and stock selection

based on a long series of studies by Charles D. Kirkpatrick II, CMT (co-author of Technical

Analysis: The Complete Resource for Financial Market Technicians, 3rd ed., Pearson

Education as FT Press, New York, 2015.) The weekly and monthly reports offer investment

managers timing signals for market trends, designed for the formulation of long-term investment

strategies and short-term trading tactics. The reports also provide stock selection using relative

price strength analysis, one of the only methods to statistically refute both the efficient markets

hypothesis and random walk hypothesis in stock prices. The reports fully disclose the methods,

formulas, variables, and parameters included in the timing and selection models. All models are

derived through rigorous walk-forward optimizing analysis.

Format of Service

Weekly: The Weekly Market Strategist is sent to subscribers each weekend, and uses

daily market price data to time trends in the U.S stock market, the U.S. long-term bond market,

gold, crude oil, and emerging foreign stock markets. The report includes updated intermediate-

term charts and a detailed analysis of those charts to derive market-timing signals. It also

includes the Bargain List of stocks that have met proscribed relative strength purchase

requirements, and a list of additions and deletions to and from the list for that week. The list

includes ranks in relative price strength, relative earnings growth, the relative price-to-sales ratio,

date and price when added to the list, profit or loss, and a suggested protective stop level for each

security. Stock charts include a legend that describes the abbreviated symbols on each chart, and

a table describes the Bargain List rules.

Monthly: The Monthly Overview is a 9 to 12 page report that provides charts and

analysis of intermediate- and long-term trends in the U.S. stock market, U.S bond market, gold,

crude oil, industrial raw materials, agricultural product prices, foreign stock markets in aggregate

and the Japanese stock market. It occasionally includes the timing results of three economic

models that were the subject of the studies reported in my book (Time the Markets: Using

Technical Analysis to Interpret Economic Data, Pearson Education as FT Press, 2012) and

reports the annual performance of the Bargain List over the past three years.

Investment Philosophy

Disputing the concept of using diversification as a means of decreasing risk in stock

portfolios, my investment philosophy encompasses two principle concepts: market timing and

relative strength stock selection.

Kirkpatrick & Company, Inc.

2

www.charleskirkpatrick.com

Market-timing is a controversial subject, rejected by many investment professionals for

its lack of preciseness. Assuming that precision is a hopeless task in any aspect of investment

management, I still can show successful models with simple formulas that manage to reduce

systemic risk through timing the major and minor waves in stock market prices. These models

use either 1) dual, filtered, moving-average crossovers, or 2) models based on Wilder’s DMI and

ADX. These models have all been derived and tested using walk-forward optimization analysis.

Once the market direction has been resolved, relative price strength is the basis for

selection of individual issues. Relative strength has been rigorously studied in academia and

elsewhere and is universally accepted by those who have investigated it as the best means of

selecting stocks. Different calculations of relative strength have been proposed and proven

useful, but I believe the Levy method using a ratio of the closing price to a simple moving

average of the price is the best. It is the basis for my studies and calculations and is one of the

subjects of my book on investment strategy (Kirkpatrick’s Investment and Trading Strategies,

Pearson Education as FT Press, 2014). A decade long track record of this selection method is

reported in the weekly report (see Figure 1).

Investment

Portfolio management requires two sets of decisions. The first decision is concerned with

the risk of capital loss to a general market decline when, regardless of selection method, most

investments lose value. The second decision is what and when to buy and what and when to sell

when the market or stock trend turns favorable. The purpose in all portfolio management should

be to make profits by reducing the risk of loss, not just to “beat the averages.” Beating the

averages during a decline by not losing as quickly as the averages is a ridiculous method of

investing. Protecting capital against loss is the most important aspect of any portfolio

management system. It not only reduces loss but also enhances performance when cash assets

are reinvested, especially at periods of minimum systemic risk.

Portfolio Management

Selection

After 50 years of studying and trading markets, especially the stock market, I’m

convinced that the most reliable method of selecting stocks for investment is the concept of

relative price strength. It is one of the only methods extensively and successfully tested, not only

by myself and other practitioners but also by finance professors in academia. One can make

money in the markets using other methods, some fundamental and some technical, but the best

method, in my opinion, is the use of relative price strength.

The principle selection criterion in my system is the relative price strength ratio. Other

screens having to do with price-to-sales ratios and earnings growth have been included at times

but neither is a profitable as using relative price strength. The stocks selected by this method are

reported weekly in the Bargain list (Blue line in Figure 1) in the Market Strategist letter. Other

Kirkpatrick & Company, Inc.

3

www.charleskirkpatrick.com

vendors calculate the proper ratios, the most reliable being HGSI, a web-based data provider that

can be reached for a free trial at www.highgrowthstock.com

The Bargain List

The Bargain List is the list of those stocks that meet the current ownership criteria. The

specific method by which stocks are added to or deleted from the Bargain list is described in

each weekly letter.

Two sets of performance of the list are graphed. One is the performance of the list itself

without market timing. The other is the list adjusted for market timing based on either a dual,

filtered, moving-average crossover system or the ADX/DMI trading method described below as

it is applied to a longer period. The second list is called the Bargain Portfolio. When the market

direction is bearish, the bargain portfolio liquidates all holdings and awaits a positive turn in the

timing system. Because moving averages lag behind prices, the timing system is always late at

tops and bottoms. It is used to confirm signals generated by the trading method described below

when applied to market averages over longer periods.

Selection Criteria

The universe of stocks that is used to find new additions to the Bargain List begins with

all NYSE, AMEX, and NASDAQ listed stocks. The total list varies but after discarding penny

stocks and very lightly traded stocks, it includes about 8,500 stocks. This list is further filtered

by eliminating stocks with a price below $5 and stocks with a 50-day moving average of dollar-

volume below $50,000,000. This leaves about a universe of about 4,500 stocks to choose from.

I use two kinds of relative strength methods to find new stocks for the Bargain List. Both

methods use a ratio of the weekly closing price to a moving average of past weekly prices. The

“Relative” screen uses a ratio of the weekly closing price to 30-week moving average. This ratio

is calculated for each stock in the universe and then ranked with the highest ratio at the top. The

ranked list is then divided into percentiles such that each percentile includes about 45 stocks.

The top percentile is 99 and the bottom is 0. Only stocks with a percentile of 97 or better are

considered for inclusion in the Bargain List.

The second relative strength method uses a similar ratio but doesn’t rank the results and

is called the “Absolute” method. It looks only for those stocks with ratios above a predetermined

threshold gained from experiment. Currently the ratio is the closing price to its 61-week moving

average, and the buy threshold is 1.47. Thus any stock with both a ratio above 1.47 using this

method and a relative rank in the first method of 97 or better is likely to be included in the list.

On the sell side, I have found that a relative rank below percentile 58, or 1.04 in the

absolute method, is the statistically best time to eliminate a stock from the list using relative

strength.

Selecting what stocks to sell and when to sell them is an easy problem for the investor to

solve if a tested, discipline system is used. Stocks are deleted from the list when they either

Kirkpatrick & Company, Inc.

4

www.charleskirkpatrick.com

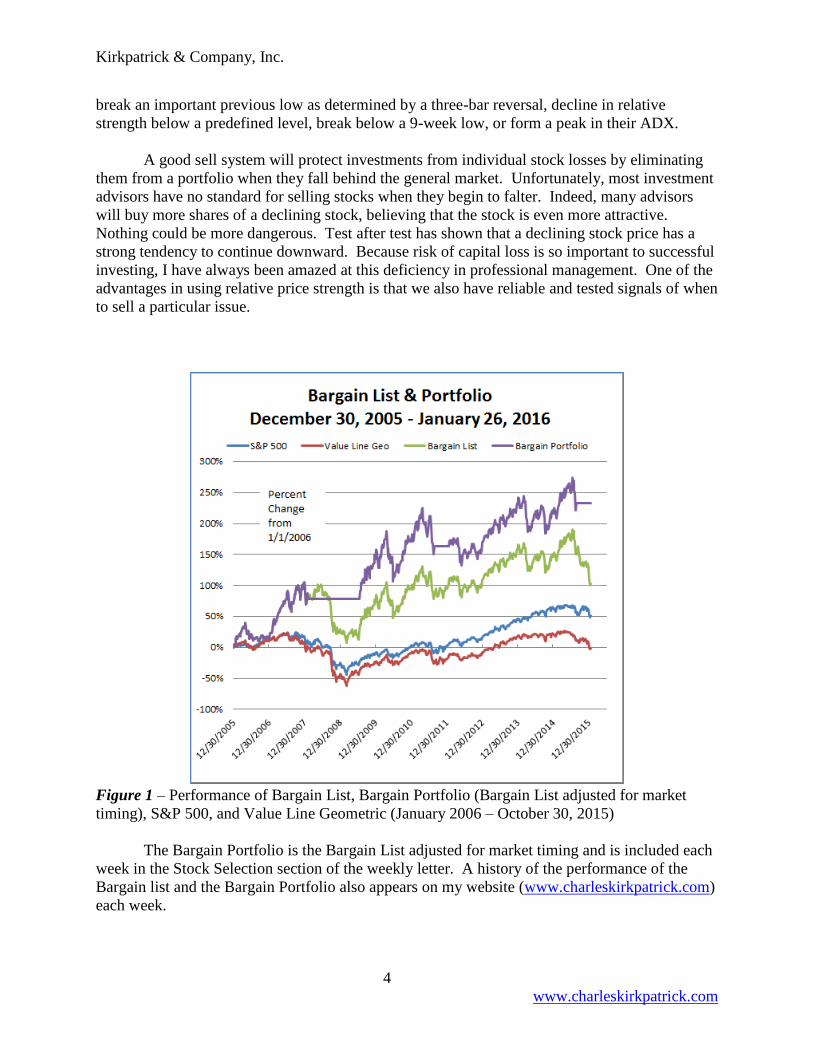

break an important previous low as determined by a three-bar reversal, decline in relative

strength below a predefined level, break below a 9-week low, or form a peak in their ADX.

A good sell system will protect investments from individual stock losses by eliminating

them from a portfolio when they fall behind the general market. Unfortunately, most investment

advisors have no standard for selling stocks when they begin to falter. Indeed, many advisors

will buy more shares of a declining stock, believing that the stock is even more attractive.

Nothing could be more dangerous. Test after test has shown that a declining stock price has a

strong tendency to continue downward. Because risk of capital loss is so important to successful

investing, I have always been amazed at this deficiency in professional management. One of the

advantages in using relative price strength is that we also have reliable and tested signals of when

to sell a particular issue.

Figure 1 – Performance of Bargain List, Bargain Portfolio (Bargain List adjusted for market

timing), S&P 500, and Value Line Geometric (January 2006 – October 30, 2015)

The Bargain Portfolio is the Bargain List adjusted for market timing and is included each

week in the Stock Selection section of the weekly letter. A history of the performance of the

Bargain list and the Bargain Portfolio also appears on my website (www.charleskirkpatrick.com)

each week.

Kirkpatrick & Company, Inc.

5

www.charleskirkpatrick.com

Market Timing

The two principle methods I employ for market timing are the filtered, dual, moving-

average, crossover system, and the ADX/DMI system devised through experimenting and

testing.

Dual, filtered, moving-average, crossover system

In terms of a portfolio (not individual issues which can be protected from capital loss

through sell stops) one method of reducing systemic risk is the use of market timing. Market

timing is a concept believed by many to be impossible to accomplish. Again, however, the

concept of market timing can be simple. The easiest and best methods I have found so far,

without becoming intensely mathematical, is the use of simple moving averages (SMA) and

Wilder’s DMI and ADX. I have experimented with various combinations of moving averages

and have found that a dual, filtered, moving-average, crossover system is the best. Dual means

that because market tops and bottoms have different configurations, a separate crossover system

is needed for each. Filtered means that each signal must make a crossover by a predetermined

distance before registering as “active”. This lowers the number of whipsaws often seen with

moving average crossovers. Finally, because no system is perfect, each signal must be protected

by stop orders to minimize capital risk even further. The timing signals reduce risk and increase

the likelihood of continuous profit, and the stops add additional safety. The specific parameters

for the crossover systems are described in the Monthly Overview.

Below (Figure 2) is a chart of the signals generated by the dual, moving-average system.

The system is longer-term in nature and suffers from almost no whipsaws. A chart showing the

moving averages is occasionally shown in the Weekly Market Strategist and always in the

Monthly Overview.

Figure 2 – Dual, filtered, moving-average, crossover signals of S&P 500 (weekly: June 2010

through January 2016)

Kirkpatrick & Company, Inc.

6

www.charleskirkpatrick.com

DMI and ADX Timing System

Trading encompasses both long and short positions over short periods, usually just days

or weeks. The Weekly Market Strategist covers shorter-term trends for several commodities, the

long-term interest rate, and stock markets. Directional decisions are based on the behavior of the

DMI, the ADX, (see Indicators below) and a percentage protective stop exit. The principle rules

have now been coded in TradeStation, and walk-forward optimized. All parameters for each

market are disclosed.

Upward Trend - In an upward trend, the DMI is positive (buying pressure is greater than

selling pressure), and the ADX is climbing (the trend is accelerating). Anything less is

suspicious. The first sell signal usually occurs at a peak in the ADX, which tends to peak at the

end of any trend regardless of direction. A sell may also occur when prices decline below a

protective stop. The DMI and ADX use a period of half the dominant cycle in the price data.

This period may change but is always reported. The forward line is a moving average of the

cycle length moved forward by half the cycle length (see “Forward Line Analysis” on page 7).

For example, a 20-day cycle is represented by a 20-day simple moving average plotted 10 days

ahead of the price. The forward line has predictive abilities as well as the DMI and ADX but is

no longer used in the trading system (see Indicators below).

The trading model is based on a crossover in the two DMI lines, positive and negative.

This crossover requires an additional price move beyond the bar (in a bar chart) that caused the

crossover. For example, the positive DMI line (usually shown in blue) crosses above the

negative DMI line (usually shown in red). This is called a positive crossover. The price bar that

occurs at the time of the crossover is called the crossover bar. In a positive crossover, the high

of the crossover bar must be exceeded by a proscribed amount in a following bar for a buy signal

to occur. The amount by which the bar high has to be exceeded is a parameter in the model.

Once that level is broken, unless canceled by a negative crossover, the crossover is considered

confirmed, a buy signal is generated, and the position is assumed to be long. That long position

can be sold either on a peak in the ADX that must reverse direction by a certain parameter

percentage, a confirmed negative crossover, a protective stop or a trailing stop.

Downward Trend - The same rules apply in a downward trend as for an upward trend

only in reverse. However, as in an upward trend, the ADX peaks at the end of the trend.

Kirkpatrick & Company, Inc.

7

www.charleskirkpatrick.com

Figure 3 – Short-term DMI/ADX trading signals on Dow Jones Industrial (daily: January 20,

2015 to December 14, 2015)

Figure 4 – Short-term DMI/ADX trading signals on Dow Jones Industrial (daily: September

1983 to January 2016)

Figures 3 and 4 show how the DMI/ADX method gives timely signals when walk-

forward optimized. Figure 3 is a daily bar chart of the Dow Jones Industrial Average for the year

2015 with the many signals that occurred. When I use monthly bar charts of the Dow Jones

Industrial Average in Figure 4, the signals become less common but just as important. It is these

signals that determine when the Bargain portfolio goes into cash.

Indicators Used in Commentary

Forward Line Analysis

Please refer to the attached chart of the daily S&P 500 (Figure 5).

The forward line is calculated as the dominant cycle’s moving average (from optimizing

the DMI/ADX model) moved one half the cycle length forward. This configuration has many

interesting consequences and shows several aspects of a security’s price behavior.

Notice that the forward line reaches tops when it is rounding over at approximately the

same time as a price low. In Figure 5, for example, the forward line has made a peak, suggesting

that a low is near.

Kirkpatrick & Company, Inc.

8

www.charleskirkpatrick.com

Notice that the price sometimes crosses the forward line and sometimes doesn't. When it

does cross the forward line, it gives a price projection of the distance from the prior peak or

trough from the forward line. When this happens and the price projections are met, the

underlying trend is flat. When the price doesn't cross the forward line, it suggests the underlying

trend is strong. If it does cross and the projection is over run, it suggests a trend reversal, and if

the projection is not met, it suggests the earlier trend is still in effect. There are many other rules,

but these are the basic ones:

A. A cycle low that did not appreciably decline below the forward line indicates the earlier

trend is still in force.

B. A cycle low that did not break the forward line indicates the trend is strongly in the

original direction.

C. The price breaks below the forward line price to the expected cycle low, indicating a

price target at XC, the distance from the peak to the crossover subtracted from the

crossover price.

D. The target XC was exceeded at the cycle low, indicating that the market is becoming

weaker and that the underlying trend is either flattening or reversing.

E. The price breaks above the forward line indicates a price target of 1372.

F. Cycle low occurs above the forward line, and the target from the earlier crossover was

met. The low occurring above the forward line is an indication of trend strength, and

reaching the target is a sign of a flat underlying trend.

G. Price breaks below the forward line early in the cycle period (after only 7 days in a 40-

day cycle), indicating trend weakness and a new target of GX (1295).

H. Price far exceeded the GX projection at 1258. Indicates underlying trend is likely

reversing downward.

I. Price crosses above the forward line. Indicates projected target (IX) of 1348.

J. Price reaches target and indicates the trend is flat to downward - downward slightly

because the high at J fails to exceed the earlier high.

K. Forward line is broken late in cycle and indicates the trend may still be flat. It projects a

target of 1249.

L. L? Target exceeded indicating that the underlying trend is likely downward and that

price will rally back to declining forward line.

Kirkpatrick & Company, Inc.

9

www.charleskirkpatrick.com

Figure 5 – Example of the use of a Forward Line (S&P 500 daily: October 15, 2011 – August

10, 2012)

Average True Range (ATR)

The Standard Range calculation used on bar and candlestick charts is the difference

between the high and low of that bar. An average range therefore is an average of those

individual ranges. This average is often used as a measure of volatility.

The Welles Wilder range is called the True Range and is calculated as below using the

high, low, and previous close of the last two bars.

Standard Price Range = High – Low

Wilder Price Range = the largest of

o Today’s high to low

o Today’s high to yesterday’s close

o Today’s low to yesterday’s close

The graphic in Figure 6 is Wilder’s drawing of the average true range calculation.

Kirkpatrick & Company, Inc.

10

www.charleskirkpatrick.com

Figure 6 – Diagram of Wilder True Range. Source: Wilder, J. Welles. New Concepts in Technical Trading Systems. Greensboro, SC: Trend Research, 1978.

The Average True Range (ATR) uses a special method of averaging concocted by

Wilder that in the example of a 14-bar average, takes yesterday’s ATR multiplied by 13 +

today’s TR, and the whole result then divided by 14.

ATR = [(N-1)*ATR-1 + TR] / N where N is the period.

This measure of price range calculates pure price volatility that is missed in the standard

method, especially in 24-hour markets, because it accounts for all trading activity over a

continuous time rather than that included only in active trading. Unlike standard deviation, it

does not include the trend. It is similar to an exponential moving average because it doesn’t

suffer the drop-off effect that occurs in a simple moving average. It is used in the calculation of

Wilder indicators such as the DMI, ADX & RSI and as a filter for protective stops. It is usually

referred to by its acronym ATR.

Directional Movement (DMI)

As defined by Wilder, directional movement is a measure of trend strength taking into

consideration the net of upward and downward trading pressure. It is calculated as follows:

1) The bar raw figure is the absolute amount by which the 2nd bar trading range

exceeds the 1st bar range, and is measured specifically as whichever is larger

of:

2) The 2nd bar high to the 1st bar high (+DM) or

3) The 2nd bar low to the 1st bar low (-DM).

4) In an “outside” bar, for example, the larger of the two outside ranges is the

directional movement, and in an “inside” bar, no figure is used.

5) All DM’s are positive numbers.

The period (number of bars) is picked, over which the movement is to be measured. The

standard is 14 bars, but can be any length, usually determined through optimization. The

Positive Directional Indicator and Negative Directional Indicator are calculated by averaging,

using Wilder’s method, +DMs and –DMs over the past period and dividing each by the ATR

over the same period. For 14 bars, the formula would look like:

Kirkpatrick & Company, Inc.

11

www.charleskirkpatrick.com

14-bar Positive Directional Indicator (+DI14) = +DM14 / ATR14

14-bar Negative Directional Indicator (-DI14) = -DM14 / ATR14

Figure 7 – Directional Movement of 1000-tick bars showing +DI in blue and –DI in red (S&P E-

mini futures (ES): January 22, 2016)

Notice in Figure 7 that the DI’s often cross each other and give signals as to the next

trend direction. The crossovers are usually late, depending on the length of the DI moving

averages, but similar to any moving average crossover, are useful in signaling the beginning of

longer trends. The earlier “whipsaws” have to be filtered out using price filters.

ADX

If we subtract the –DI from +DI, we get the DX, the directional index. To neutralize the

difference, we divide it by the sum of –DI and +DI, the total of all directional bars, and Wilder

average this figure over some period, say 14 bars. This is called the ADX, and it measures the

intensity of the trend but is independent of trend direction. It tends to peak at the end of trends

and turn upward when a trend increases momentum. It is thus a valuable indicator of when to

close a position and sometimes an indicator of when to add to a position in an existing trend.

Kirkpatrick & Company, Inc.

12

www.charleskirkpatrick.com

Figure 7 – ADX for same period as Figure 6 showing peaks correlated to price position. Blue

arrows designate price troughs, and red arrows designate price peaks. The ADX peaks

thus occur at market turning points, when the earlier trend, up or down, has ended. (S&P

E-mini futures (ES): January 22, 2016)

In Figure 7 notice the ADX peaks at trend completions, up or down, and the ADX

troughs turn upward just as a trend is beginning to increase in momentum, up or down. Likewise,

though not shown with lines, ADX troughs tend to suggest acceleration in the existing price

direction and end with an ADX peak.

Subscription Information

Cost: $195/year.

Delivery: Email notification with link to letter on a specific website address – currently use

ISSUU.com – from which the issue can be downloaded, read, and printed.

Ordering:

1) Mail check to Kirkpatrick & Company, Inc., 1 Bowen Road, Kittery, ME, 03904-

1355.

2) Go to website: www.charleskirkpatrick.com and click on “Market Strategist” tab at

top of the page. On “Market Strategist” page click on the yellow button at lower right

marked “BUY NOW.” This will send you to PayPal where you can either use PayPal

or a private credit card. Just follow the instructions.

Questions, Comments, Suggestions or Complaints: email: [email protected]