Kingboard Chemical (0148.HK) Phillip Securities...

17

Kingboard Chemical (0148.HK) -- Chemicals division with bright prospect Phillip Securities Research Pte. Ltd. January 05 2012 Market Stock Exchange Hong Kong Sector Chemicals Reuters 0148.HK Bloomberg 0148.HK HOLD Previous Closing Price: HK$23.70 Target Price: HK$25.50 (+7.6%) Phillip Research Team 65 65311240 FAX 65 63367607 [email protected] Web: www.poems.com.sg MICA (P) 004/01/2011 Ref No: HK2012_0002 What’s new The subsidiary of Kingboard Chemical Holdings (0148.HK), Kingboard Laminates (1888.HK), announced that its Singapore-listed subsidiary, Kingboard Copper Foil Holdings Limited, as of the end of September 2011, recorded a turnover of HK$ 719 million in three months, which reduced by 42.67% annually. The profit attributable to shareholders for the period was HK$ 5.072 million, dropped by 86.7% annually. Enhance the weighting of properties division Group's managements plan to raise the weighting of properties business to 10% - 15% in the next 3 - 5 years. However, developing properties business require inputting large amount of capital and time in order to build up land reserves, which create heavy pressure on Group’s working capital. Remarkable results from chemical division Regarding rapid industrial development in China, market demand for chemical products will continually increase, especially for the methanol business. Methanol and its derivatives have a lot of applications and there is a supply gap in China’s methanol market. Methanol business has a huge room for development and can boost the overall chemical business. Reiterate “HOLD” rating Our 12-month target price is HK$ 25.50 which is based on DCF valuation. The target price implies 2012 P/E of 5.4x and 0.675 PEG. Compared to HK$ 23.70 of current price, the potential upside for one year is 7.6%. Reiterate “HOLD” rating. (HK$ m) 2010A 2011E 2012E 2013E 3-Yr CARG Total revenue 33,892 37,906 41,318 47,928 12.2% YoY% 42% 12% 9% 16% -- Operating profit 5,470 5,581 6,027 6,961 8.4% YoY% 59% 2% 8% 15% -- EPS (in HK$) 4.278 4.364 4.713 5.467 8.5% YoY% 51% 2% 8% 16% -- Source: Company data; Phillip estimates

Transcript of Kingboard Chemical (0148.HK) Phillip Securities...

Kingboard Chemical (0148.HK) -- Chemicals division with bright prospect

Phillip Securities Research Pte. Ltd.

January 05 2012 Market Stock Exchange Hong Kong Sector Chemicals

Reuters 0148.HK

Bloomberg 0148.HK HOLD Previous Closing Price: HK$23.70

Target Price: HK$25.50 (+7.6%)

Phillip Research Team � 65 65311240 FAX 65 63367607 � [email protected] Web: www.poems.com.sg MICA (P) 004/01/2011 Ref No: HK2012_0002

What’s new The subsidiary of Kingboard Chemical Holdings (0148.HK), Kingboard Laminates (1888.HK), announced that its Singapore-listed subsidiary, Kingboard Copper Foil Holdings Limited, as of the end of September 2011, recorded a turnover of HK$ 719 million in three months, which reduced by 42.67% annually. The profit attributable to shareholders for the period was HK$ 5.072 million, dropped by 86.7% annually. Enhance the weighting of properties division Group's managements plan to raise the weighting of properties business to 10% - 15% in the next 3 - 5 years. However, developing properties business require inputting large amount of capital and time in order to build up land reserves, which create heavy pressure on Group’s working capital. Remarkable results from chemical division Regarding rapid industrial development in China, market demand for chemical products will continually increase, especially for the methanol business. Methanol and its derivatives have a lot of applications and there is a supply gap in China’s methanol market. Methanol business has a huge room for development and can boost the overall chemical business.

Reiterate “HOLD” rating Our 12-month target price is HK$ 25.50 which is based on DCF valuation. The target price implies 2012 P/E of 5.4x and 0.675 PEG. Compared to HK$ 23.70 of current price, the potential upside for one year is 7.6%. Reiterate “HOLD” rating.

(HK$ m) 2010A 2011E 2012E 2013E 3-Yr CARG

Total revenue 33,892 37,906 41,318 47,928 12.2%

YoY% 42% 12% 9% 16% --

Operating profit 5,470 5,581 6,027 6,961 8.4%

YoY% 59% 2% 8% 15% --

EPS (in HK$) 4.278 4.364 4.713 5.467 8.5%

YoY% 51% 2% 8% 16% --

Source: Company data; Phillip estimates

Kingboard Chemical (0148.HK) January 05, 2012

2

Various businesses weighting Group’s business coverage is comprehensive, including the production of laminates, printed circuit boards, chemical products and developing properties. Among them, the production of laminates and chemicals are the most profitable to the Group. In 2011 1H, two businesses accounted for more than 40% of overall profit respectively. Exhibit 1: The weighting of various division in 2011 1H

Source: Company data; Phillip Research Regarding the huge demand for chemicals products in China, we forecast the group will put more resources to develop the chemicals division in the future. The shipment and average selling price of chemicals products rose annually. Among the chemicals, the production of methanol has the greatest potential for development as there is a supply gap in China. On the other hand, laminates and printed circuit board businesses are still affected by the earthquake of Japan in March. The overall profit is mainly driven by the chemical division.

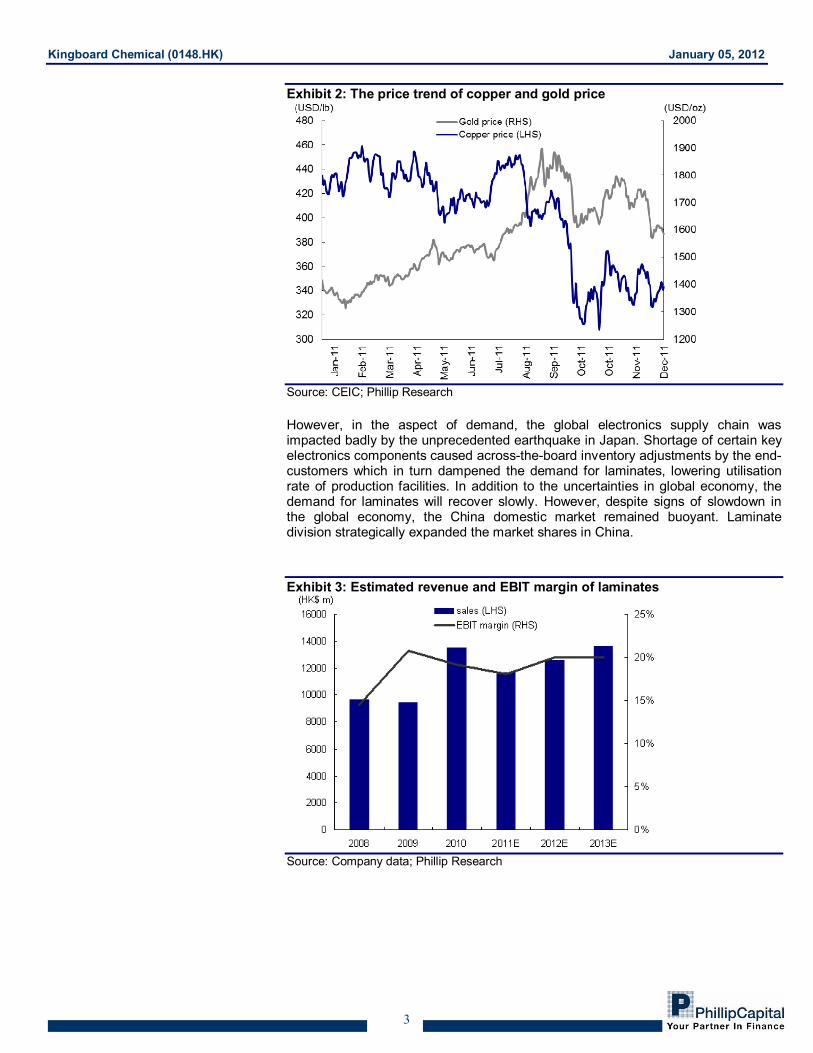

Laminates In 2011 1Q, the demand for laminates was stronger than 2010 4Q. However, the copper price increased, resulting in the increase in the production cost of laminates. The group passed the cost to the customers, causing the average selling price of laminates in 2011 1H increase. In the 2011 2H, the copper price trend fluctuated. Since the gold price exceeded US$ 1900 per oz in August, the gold prices dropped significantly. The decline in copper price was much more than that of gold price. The annual decline in copper price was 21%. Large fall in copper price can reduce the production cost of manufacturing laminates and there will be room for adjusting the average selling price of laminates downward.

Kingboard Chemical (0148.HK) January 05, 2012

3

Exhibit 2: The price trend of copper and gold price

Source: CEIC; Phillip Research

However, in the aspect of demand, the global electronics supply chain was impacted badly by the unprecedented earthquake in Japan. Shortage of certain key electronics components caused across-the-board inventory adjustments by the end-customers which in turn dampened the demand for laminates, lowering utilisation rate of production facilities. In addition to the uncertainties in global economy, the demand for laminates will recover slowly. However, despite signs of slowdown in the global economy, the China domestic market remained buoyant. Laminate division strategically expanded the market shares in China.

Exhibit 3: Estimated revenue and EBIT margin of laminates

Source: Company data; Phillip Research

Kingboard Chemical (0148.HK) January 05, 2012

4

Printed Circuit Board (PCB) PCBs products are also affected by the earthquake in Japan and there is a supply shortage in the supply chain of electronic products. Worse still, the demand for conventional PCBs is weak. Therefore, The Group focused on expanding high density interconnects “HDI” business. HDI is the fastest growing areas in the printed circuit board industry, which can be applied to the camera, data communications, automotive electronics and mobile phones. Mobile phone industry is one of the most widely used area. HDI business will benefit from the increase in the production of high-end electronic products like smart phones.

In 2011 1H, the revenue of PCB dropped by 11% yoy. We expect that the annual revenue of PCB in 2011 will be HK$8 billion only. But with the rapid development of smart phones, the demand for printed circuit boards increased and we expect the revenue from PCB division in 2012 will return to the level of 2010. Exhibit 4: Estimated revenue and EBIT margin of PCB

Source: Company data; Phillip Research

Chemicals Methanol Methanol is commonly converted to formalin, which is used in the manufacturing process of plastics, plywood, paints, explosives and permanent press textiles. Methanol is also blended in gasoline as methanol fuel for use by vehicles. Methanol and its derivatives like Dimethyl Ether, Acetic Acid and Methyl tert-butyl ether can be applied widely.

Kingboard Chemical (0148.HK) January 05, 2012

5

Table 1: The applications of methanol’s derivatives Derivatives Applications

Dimethyl Ether (DME) - Mixed with liquefied petroleum gas for heating - Used as a transportation fuel and as a substitute for diesel

Acetic acid - Production of a variety of compounds used in the manufacture of pesticides, chemicals and pharmaceutical products

Methyl tert-butyl ether - Used as a gasoline fuel components

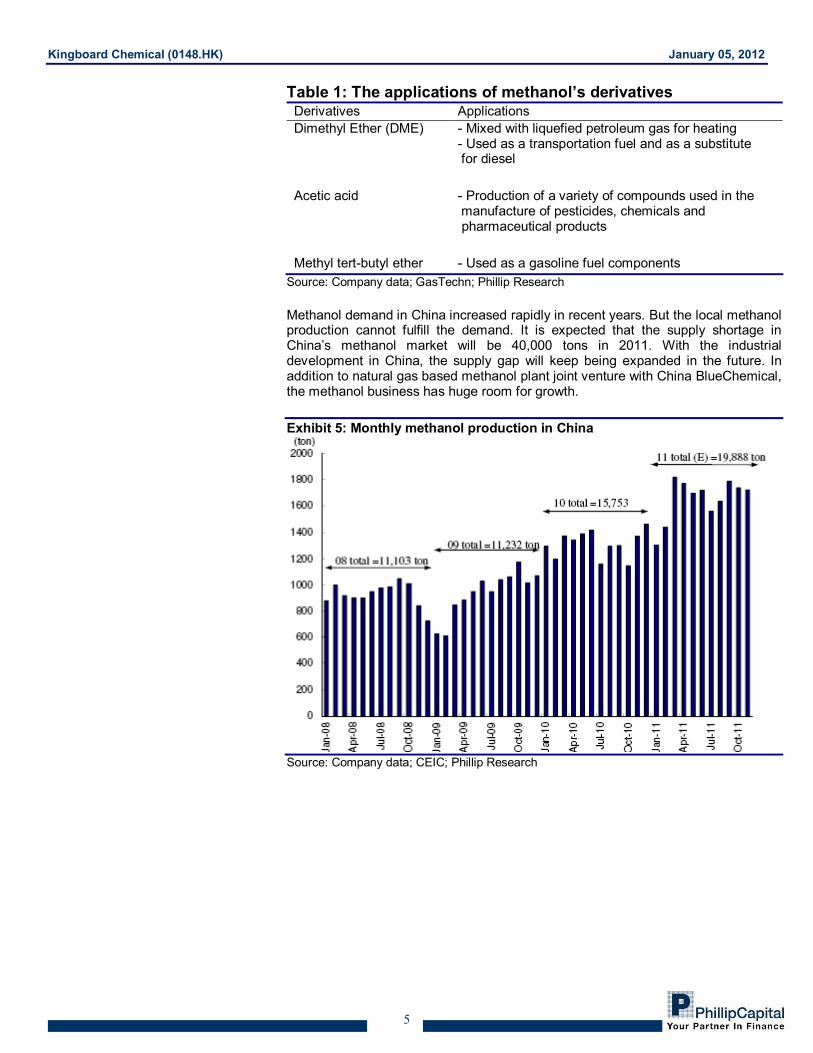

Source: Company data; GasTechn; Phillip Research Methanol demand in China increased rapidly in recent years. But the local methanol production cannot fulfill the demand. It is expected that the supply shortage in China’s methanol market will be 40,000 tons in 2011. With the industrial development in China, the supply gap will keep being expanded in the future. In addition to natural gas based methanol plant joint venture with China BlueChemical, the methanol business has huge room for growth.

Exhibit 5: Monthly methanol production in China

Source: Company data; CEIC; Phillip Research

Kingboard Chemical (0148.HK) January 05, 2012

6

Exhibit 6: Production and demand of methanol in China

Source: Company data; CEIC; allbusiness; asiachem; Phillip Research

Exhibit 7: Price trend of methanol

Source: CEIC; Phillip Research

Phenol/Acetone The Group allocates more resources to develop chemical division. In 2010, a new phenol/acetone plant with an annual capacity of 300,000 tons was developed. The capacity enhancement plan for the existing phenol/acetone plant in Huizhou expected to be completed in 2011, in order to catch up the huge demand for phenol and acetone in China.

Kingboard Chemical (0148.HK) January 05, 2012

7

Exhibit 8: Price trend and applications of phenol

Source: CEIC; Phillip Research

Exhibit 9: Price trend and applications of acetone

Source: CEIC; Phillip Research

Overall results of chemical division In 2011 1H, Group’s chemical division posted remarkable results. Chemical division revenue soared 38% to HK$9,078.4 million with EBITDA up 73% to HK$1,442.9 million in 1H 2011. Regarding rapid industrial development in China, market demand for chemical products will continually increase, especially for the methanol business. Methanol and its derivatives have wide applications and there is supply gap in China’s methanol market. Methanol business has huge room for development and can boost the overall chemical business. We expect the weighting of chemical division will keep rising to be over 50% in 2012. The chemical division will be the most profitable business to the Group.

Kingboard Chemical (0148.HK) January 05, 2012

8

Exhibit 10: Estimated revenue and EBIT margin of chemicals

Source: Company data; Phillip Research

Properties division The Group started to engage in properties business since 2008. The first residential development project is Shanghai Yu Garden in Kunshan and its earnings will be recognized in 2H 2011. In addition, pre-sale for another residential project, Kunshan Qiandeng Yu Garden, is also expected to commence in 2H 2011. The properties division is expected to generate stable and attractive returns for the Group. Apart from Shanghai, the Group’s key investment properties in eastern and southern China continued to generate stable rental income. Group's managements plan to raise the weighting of properties business to 10% - 15% in the next 3 - 5 years. However, developing properties require inputting large amount of capital and time in order to build up land reserves. The Group held a land bank of over 3 million square metres of gross floor area located at prime sites in major cities such as Guangzhou, Shanghai and Kunshan in China. And Rental income from the properties division jumped 72% to HK$100.3 million in 1H 2011. However, the rental income from properties division in 2011 1H accounted for less than 1% of overall turnover. The group had spent HK$ 2.6 billion on properties held for development. Developing properties creates heavy pressure on Group’s working capital.

Kingboard Chemical (0148.HK) January 05, 2012

9

SWOT Analysis Strengths � The Group has a natural gas based

methanol plant joint venture with China BlueChemical, which can increase the methanol production in order to fulfill the huge demand for methanol from China.

� The Group held a land bank of over 3 million square metres of gross floor area located at prime sites in major cities such as Guangzhou, Shanghai and Kunshan in China, which assist the Group to develop properties division.

Weaknesses � Laminates and PCB businesses are

greatly impacted by the earthquake in Japan happened in March. There is a supply shortage in the supply chain of electronic products. In addition to the uncertainties of global economy, the demand for the products from oversea declined.

� The rental income from properties division in 2011 1H accounted for less than 1% of overall turnover.

Opportunities � Benefited from the increase in the

production of high-end electronic products like smart phones, the demand for HDI increases. HDI is the fastest growing areas in the printed circuit board industry.

� With the industrial development in China, it is expected that the supply shortage in China’s methanol market will be 40,000 tons and the supply gap will keep being expanded.

Threats � Developing properties require inputting

large amount of capital and time in order to build up land reserves, which create heavy pressure on Group’s working capital.

� Raising labour cost and the appreciation of RMB reduce the international competitiveness of Group’s products.

Kingboard Chemical (0148.HK) January 05, 2012

10

Valuation We use DCF for valuation. According to Bloomberg data, the Group’s beta and equity risk premium are 1.2 and 13.8% respectively. Assume the risk-free rate (US 10-year Treasury yield) is 1.5%. The Group’s WACC is calculated as 13.6%. We forecast the free cash flow in the next 10 years and the free cash will grow at 2% of terminal growth rate after 2020.

Table 2: DCF

Source: Bloomberg; Company data; Phillip estimates

Table 3: Sensitivity analysis

Source: Phillip estimates

Kingboard Chemical (0148.HK) January 05, 2012

11

According to DCF valuation, the 12-month TP of Group is HK$ 25.50. We forecast the earning per share in 2011, 2012 and 2013 are HK$ 4.364, HK$ 4.713 and HK$ 5.467 respectively, with 8.5% of 3-year CARG. The target price implies 2012 P/E of 5.4x and 0.675 PEG. Compared to HK$ 23.70 of current price, the potential upside for one year is 7.6%. Reiterate “HOLD” rating.

Peer valuation table

Prices are as close of 04 January 2012; "na" entries are excluded from the calculation of averages Source: Bloomberg; Phillip Research

Kingboard Chemical (0148.HK) January 05, 2012

12

Exhibit 11: PE band Exhibit 12: PB band

Exhibit 13: ROE Exhibit 14: Dividend yield

Source: Company report; Bloomberg; Phillip Research

Latest Max. Median Min. +2 SD +1SD Average -1 SD -2 SD PE 5.5 25.43 10.10 2.48 18.94 14.45 9.96 5.47 0.98 PB 0.7 3.29 1.52 0.38 2.88 2.27 1.66 1.05 0.44 ROE 15.3% 58.40% 15.62% 5.55% na na na na na Dividend yield 4.2% 12.22% 5.20% 0% na na na na na Source: Bloomberg; Phillip Research

Kingboard Chemical (0148.HK) January 05, 2012

13

Financial statements

Source: Company data; Phillip estimates Source: Company data; Phillip estimates

Source: Company data; Phillip estimates

Kingboard Chemical (0148.HK) January 05, 2012

14

Ratings History

Rating Date Closing price (HK$) Fair value (HK$) Remarks

Buy 23-03-2007 32.90 35.60

Buy 14-11-2006 31.90 33.0

TRADING BUY Share price may exceed 10% on the upside over the next 3

months, however longer-term outlook remains uncertain

BUY >15% upside from the current price HOLD -10% to 15% from the current price SELL >10% downside from the current price

TRADING SELL Share price may exceed 10% on the downside over the next 3 months, however longer-term outlook remains uncertain

Phillip Research Stock Selection

Systems We do not base our recommendations entirely on the above quantitative return bands. We consider qualitative factors like (but not limited to) a stock's risk reward profile, market sentiment, recent rate of share price appreciation, presence or absence of stock price catalysts, and speculative undertones surrounding the stock, before making our final recommendation

15

Important Information

This publication is prepared by Phillip Securities Research Pte Ltd., 250 North Bridge Road, #06-00, Raffles City Tower, Singapore 179101 (Registration Number: 198803136N), which is regulated by the Monetary Authority of Singapore ( “Phillip Securities Research”). By receiving or reading this publication, you agree to be bound by the terms and limitations set out below. This publication has been provided to you for personal use only and shall not be reproduced distributed or published by you in whole or in part, for any purpose. If you have received this document by mistake, please delete or destroy it, and notify the sender immediately. Phillip Securities Research shall not be liable for any direct or consequential loss arising from any use of material contained in this publication. The information contained in this publication has been obtained from public sources which Phillip Securities Research has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this publication are based on such information and are expressions of belief of the individual author or the indicated source (as applicable) only. Phillip Securities Research has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete, appropriate or verified or should be relied upon as such. Any such information or Research contained in this publication is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, (i) be liable in any manner whatsoever for any consequences (including but not limited to any special, direct, indirect, incidental or consequential losses, loss of profits and damages) of any reliance or usage of this publication or (ii) accept any legal responsibility from any person who receives this publication, even if it has been advised of the possibility of such damages. You must make the final investment decision and accept all responsibility for your investment decision including but not limited to your reliance on the information, data and/or other materials presented in this publication. Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this material are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this publication is not indicative of future results. This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This publication should not be relied upon exclusively or as authoritative without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this publication has been made available constitutes neither a recommendation to enter into a particular transaction nor a representation that any product described in this material is suitable or appropriate for the recipient. Recipients should be aware that many of the products which may be described in this publication involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks. Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this research should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this publication, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have provided advice or investment services to such companies and investments or related investments as may be mentioned in this publication.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

16

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold a interest, whether material or not, in respect of companies and investments or related investments which may be mentioned in this publication. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, which is not reflected in this material, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this material. The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction. Section 27 of the Financial Advisers Act (Cap. 110) of Singapore and the MAS Notice on Recommendations on Investment Products (FAA-N01) do not apply in respect of this publication. This material is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this material may not be suitable for all investors and a person receiving or reading this material should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products. Please contact Phillip Securities Research at [65 65311240] in respect of any matters arising from, or in connection with, this document. This report is only for the purpose of distribution in Singapore.

Contact Information

Singapore Research Chan Wai Chee CEO, Research Special Opportunities +65 6531-1231 [email protected]

Lee Kok Joo, CFA Head of Research S-chips, Strategy +65 6531-1685 [email protected]

Joshua Tan Strategy & Macro Singapore, US, China +65 6531-1249 [email protected]

Magdalene Choong Investment Analyst SG & US Financials, Gaming +65 6531-1791 [email protected]

Go Choon Koay Bryan Investment Analyst Property +65 6531-1792 [email protected]

Derrick Heng Investment Analyst Transportation, Telecom +65 6531-1221 [email protected]

Nicholas Low, CFA Investment Analyst Commodities, Offshore & Marine +65 6531-1535 [email protected]

Travis Seah Investment Analyst REITS +65 6531 1229 [email protected]

Regional Member Companies

SINGAPORE Phillip Securities Pte Ltd Raffles City Tower 250, North Bridge Road #06-00 Singapore 179101 Tel : (65) 6533 6001 Fax : (65) 6535 6631 Website: www.poems.com.sg

MALAYSIA Phillip Capital Management Sdn Bhd B-3-6 Block B Level 3 Megan Avenue II, No. 12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel (603) 21628841 Fax (603) 21665099 Website: www.poems.com.my

HONG KONG Phillip Securities (HK) Ltd Exchange Participant of the Stock Exchange of Hong Kong 11/F United Centre 95 Queensway Hong Kong Tel (852) 22776600 Fax (852) 28685307 Websites: www.phillip.com.hk

JAPAN PhillipCapital Japan K.K. Nagata-cho Bldg., 8F, 2-4-3 Nagata-cho, Chiyoda-ku, Tokyo 100-0014 Tel (81-3) 35953631 Fax (81-3) 35953630 Website:www.phillip.co.jp

INDONESIA PT Phillip Securities Indonesia ANZ Tower Level 23B, Jl Jend Sudirman Kav 33A Jakarta 10220 – Indonesia Tel (62-21) 57900800 Fax (62-21) 57900809 Website: www.phillip.co.id

CHINA Phillip Financial Advisory (Shanghai) Co. Ltd No 550 Yan An East Road, Ocean Tower Unit 2318, Postal code 200001 Tel (86-21) 51699200 Fax (86-21) 63512940 Website: www.phillip.com.cn

THAILAND Phillip Securities (Thailand) Public Co. Ltd 15th Floor, Vorawat Building, 849 Silom Road, Silom, Bangrak, Bangkok 10500 Thailand Tel (66-2) 6351700 / 22680999 Fax (66-2) 22680921 Website www.phillip.co.th

FRANCE King & Shaxson Capital Limited 3rd Floor, 35 Rue de la Bienfaisance 75008 Paris France Tel (33-1) 45633100 Fax (33-1) 45636017 Website: www.kingandshaxson.com

UNITED KINGDOM King & Shaxson Capital Limited 6th Floor, Candlewick House, 120 Cannon Street, London, EC4N 6AS Tel (44-20) 7426 5950 Fax (44-20) 7626 1757 Website: www.kingandshaxson.com

UNITED STATES Phillip Futures Inc 141 W Jackson Blvd Ste 3050 The Chicago Board of Trade Building Chicago, IL 60604 USA Tel +1.312.356.9000 Fax +1.312.356.9005

AUSTRALIA PhillipCapital Australia Level 37, 530 Collins Street, Melbourne, Victoria 3000, Australia Tel (613) 96298380 Fax (613) 96148309 Website: www.phillipcapital.com.au