Kimmel Fin 5e Ch03 - Westmont HOhomepage.westmont.edu/charmon/Westmont/003slides3a.pdf · Chapter...

50

Chapter 3-1

Transcript of Kimmel Fin 5e Ch03 - Westmont HOhomepage.westmont.edu/charmon/Westmont/003slides3a.pdf · Chapter...

Chapter 3-1

Chapter 3-2

The AccountingThe AccountingInformation SystemInformation System

Financial Accounting, Fifth Edition

Chapter 3-3

1. Analyze the effect of business transactions on the basic accounting equation.

2. Explain what an account is and how it helps in the recording process.

3. Define debits and credits and explain how they are used to record business transactions.

4. Identify the basic steps in the recording process.5. Explain what a journal is and how it helps in the recording process.6. Explain what a ledger is and how it helps in the recording process.7. Explain what posting is and how it helps in the recording process.8. Explain the purposes of a trial balance. 9. Classify cash activities as operating, investing, or financing.

Study ObjectivesStudy ObjectivesStudy Objectives

Chapter 3-4

Transactions are economic events that require recording in the financial statements.

May be external or internal.

Not all activities represent transactions.

Each transaction has a dual effect on the accounting equation.

Accounting TransactionsAccounting TransactionsAccounting Transactions

Chapter 3-5

Question:Question: Are the following events recorded in the accounting records?

EventPurchased a computer.

Criterion Is the financial position (assets, liabilities, or stockholders’ equity) of the company changed?

Pay rent.

Record/ Don’t Record

Accounting TransactionsAccounting TransactionsAccounting Transactions

Discuss product

design with potential customer.

Chapter 3-6

AssetsAssetsAssets LiabilitiesLiabilitiesLiabilities Stockholders’Equity

StockholdersStockholders’’EquityEquity= +

Transaction AnalysisThe process of identifying the specific effects of economic events on the accounting equation.

SO 1 SO 1 Analyze the effect of business transactions on the basic accounting equation.

Basic Accounting Equation

Accounting TransactionsAccounting TransactionsAccounting Transactions

Chapter 3-7

Transaction Analysis

SO 1 SO 1 Analyze the effect of business transactions on the basic accounting equation.

Accounting TransactionsAccounting TransactionsAccounting Transactions

Illustration 3-2 Expanded accounting equation

Chapter 3-8

Illustration:Illustration: 1. On October 1, cash of $10,000 is invested in Sierra Corporation by investors in exchange for $10,000 of common stock.

Accounting TransactionsAccounting TransactionsAccounting Transactions

SO 1 SO 1 Analyze the effect of business transactions on the basic accounting equation.

Chapter 3-9

2. On October 1, Sierra borrowed $5,000 from Castle Bank by signing a 3-month, 12%, $5,000 note payable.

Accounting TransactionsAccounting TransactionsAccounting Transactions

SO 1 SO 1 Analyze the effect of business transactions on the basic accounting equation.

Chapter 3-10

3. On October 2, Sierra purchased office equipment by paying $5,000 cash to Superior Equipment Sales Co.

Accounting TransactionsAccounting TransactionsAccounting Transactions

SO 1 SO 1 Analyze the effect of business transactions on the basic accounting equation.

Chapter 3-11

4. On October 2, Sierra received a $1,200 cash advance from R. Knox, a client.

Accounting TransactionsAccounting TransactionsAccounting Transactions

SO 1 SO 1 Analyze the effect of business transactions on the basic accounting equation.

Chapter 3-12

5. On October 3, Sierra received $10,000 in cash from Copa Company for advertising services performed.

Accounting TransactionsAccounting TransactionsAccounting Transactions

SO 1 SO 1 Analyze the effect of business transactions on the basic accounting equation.

Chapter 3-13

6. On October 3, Sierra Corporation paid its office rent for the month of October in cash, $900.

Accounting TransactionsAccounting TransactionsAccounting Transactions

SO 1 SO 1 Analyze the effect of business transactions on the basic accounting equation.

Chapter 3-14

7. On October 4, Sierra paid $600 for a one-year insurance policy that will expire next year on September 30.

Accounting TransactionsAccounting TransactionsAccounting Transactions

SO 1 SO 1 Analyze the effect of business transactions on the basic accounting equation.

Chapter 3-15

8. On October 5, Sierra purchased a three-month supply of advertising materials on account from Aero Supply for $2,500.

Accounting TransactionsAccounting TransactionsAccounting Transactions

SO 1 SO 1 Analyze the effect of business transactions on the basic accounting equation.

Chapter 3-16

10. On October 20, Sierra paid a $500 dividend.

Accounting TransactionsAccounting TransactionsAccounting Transactions

SO 1 SO 1 Analyze the effect of business transactions on the basic accounting equation.

Chapter 3-17

11. Employees have worked two weeks, earning $4,000 in salaries, which were paid on October 26.

Accounting TransactionsAccounting TransactionsAccounting Transactions

Chapter 3-18

Account NameDebit / Dr. Credit / Cr.

Record of increases and decreases in a specific asset, liability, equity, revenue, or expense item.Debit = “Left”Credit = “Right”

AccountAccount

An Account can An Account can be illustrated in a be illustrated in a TT--Account form.Account form.

SO 2 Explain what an account is and how it helps in the recordiSO 2 Explain what an account is and how it helps in the recording process.ng process.

The AccountThe AccountThe Account

Chapter 3-19

DoubleDouble--entry entry accounting systemEach transaction must affect two or more accounts to keep the basic accounting equation in balance.

Recording done by debiting at least one account and crediting another.

DEBITS must equalmust equal CREDITS.

SO 3 Define debits and credits and explain their use in recordiSO 3 Define debits and credits and explain their use in recording business transactions.ng business transactions.

Debit and Credit ProceduresDebit and Credit ProceduresDebit and Credit Procedures

Chapter 3-20

Account NameDebit / Dr. Credit / Cr.

If Debits are greater thangreater than Credits, the account will have a debit balance.

$10,000 Transaction #2$3,000

$15,000$15,000

8,000Transaction #3

Balance

Transaction #1

SO 3 Define debits and credits and explain their use in recordiSO 3 Define debits and credits and explain their use in recording business transactions.ng business transactions.

Debit and Credit ProceduresDebit and Credit ProceduresDebit and Credit Procedures

Chapter 3-21

Account NameDebit / Dr. Credit / Cr.

If Credits are greater thangreater than Debits, the account will have a credit balance.

$10,000 Transaction #2$3,000

Balance

Transaction #1

$1,000$1,000

8,000 Transaction #3

SO 3 Define debits and credits and explain their use in recordiSO 3 Define debits and credits and explain their use in recording business transactions.ng business transactions.

Debit and Credit ProceduresDebit and Credit ProceduresDebit and Credit Procedures

Chapter 3-22

Chapter 3-23

AssetsAssetsDebit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Chapter 3-27

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

ExpenseExpense

Chapter 3-24

LiabilitiesLiabilitiesDebit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

StockholdersStockholders’’ EquityEquity

Chapter 3-26

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

RevenueRevenue

Normal Balance Credit

Normal Balance Credit

Normal Balance Debit

Normal Balance Debit

Debits and Credits SummaryDebits and Credits SummaryDebits and Credits Summary

SO 3 Define debits and credits and explain their use in recordiSO 3 Define debits and credits and explain their use in recording business transactions.ng business transactions.

Chapter 3-23

Owner’s investments and revenues increase stockholder’s equity (credit).

Dividends and expenses decrease stockholder’s equity (debit).

Dr./Cr. Procedures for Stockholders’ EquityDr./Cr. Procedures for StockholdersDr./Cr. Procedures for Stockholders’’ EquityEquity

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Common StockCommon Stock

Chapter 3-23

DividendsDividendsDebit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

StockholdersStockholders’’ EquityEquity

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Retained EarningsRetained Earnings

SO 3 Define debits and credits and explain their use in recordiSO 3 Define debits and credits and explain their use in recording business transactions.ng business transactions.

Chapter 3-24

Balance Sheet Balance Sheet Income StatementIncome Statement

= + =-Asset Liability Equity Revenue Expense

Debit

Credit

Debits and Credits SummaryDebits and Credits SummaryDebits and Credits Summary

SO 3 Define debits and credits and explain their use in recordiSO 3 Define debits and credits and explain their use in recording business transactions.ng business transactions.

Chapter 3-25

Debits:a. increase both assets and liabilities.b. decrease both assets and liabilities.c. increase assets and decrease liabilities.d. decrease assets and increase liabilities.

Review QuestionReview Question

Debits and Credits SummaryDebits and Credits SummaryDebits and Credits Summary

SO 3 Define debits and credits and explain their use in recordiSO 3 Define debits and credits and explain their use in recording business transactions.ng business transactions.

Chapter 3-26

Accounts that normally have debit balances are:a. assets, expenses, and revenues.b. assets, expenses, and equity.c. assets, liabilities, and dividends.d. assets, dividends, and expenses.

Review QuestionReview Question

Debits and Credits SummaryDebits and Credits SummaryDebits and Credits Summary

SO 3 Define debits and credits and explain their use in recordiSO 3 Define debits and credits and explain their use in recording business transactions.ng business transactions.

Chapter 3-27

Summary of Debit/Credit RulesSummary of Debit/Credit RulesSummary of Debit/Credit Rules

Relationship among the assets, liabilities and Relationship among the assets, liabilities and stockholdersstockholders’’ equity of a business: equity of a business:

The equation must be in balance after every The equation must be in balance after every transaction. transaction. For every For every DebitDebit there must be a there must be a CreditCredit..

Illustration 3-16

Assets Liabilities= Stockholders’ EquityBasic Equation

Expanded Basic Equation

+

SO 3 Define debits and credits and explain their use in recordiSO 3 Define debits and credits and explain their use in recording business transactions.ng business transactions.

Chapter 3-28

Journalizing - Entering transaction data in the journal.

Illustration: Presented below is information related to Sierra Corporation.

SO 4 Explain what a journal is and how it helps in the recordinSO 4 Explain what a journal is and how it helps in the recording process.g process.

Sierra issued common stock in exchange for $10,000 cash.

Oct. 1

Sierra borrowed $5,000 by signing a note.1Sierra purchased office equipment for $5,000.2

Instructions - Journalize these transactions.

The JournalThe JournalThe Journal

Chapter 3-29

Account Title Ref. Debit Credit

Oct. 1

Date

JournalizingJournalizingJournalizing

General Journal

SO 4 Explain what a journal is and how it helps in the recordinSO 4 Explain what a journal is and how it helps in the recording process.g process.

Sierra issued common stock in exchange for $10,000 cash.

Oct. 1

Chapter 3-30

Account Title Ref. Debit Credit

Oct. 1

Date

JournalizingJournalizingJournalizing

General Journal

SO 4 Explain what a journal is and how it helps in the recordinSO 4 Explain what a journal is and how it helps in the recording process.g process.

Sierra borrowed $5,000 by signing a note.Oct. 1

Chapter 3-31

Account Title Ref. Debit Credit

Oct. 2

Date

JournalizingJournalizingJournalizing

General Journal

SO 4 Explain what a journal is and how it helps in the recordinSO 4 Explain what a journal is and how it helps in the recording process.g process.

Sierra purchased office equipment for $5,000.Oct. 2

Chapter 3-32

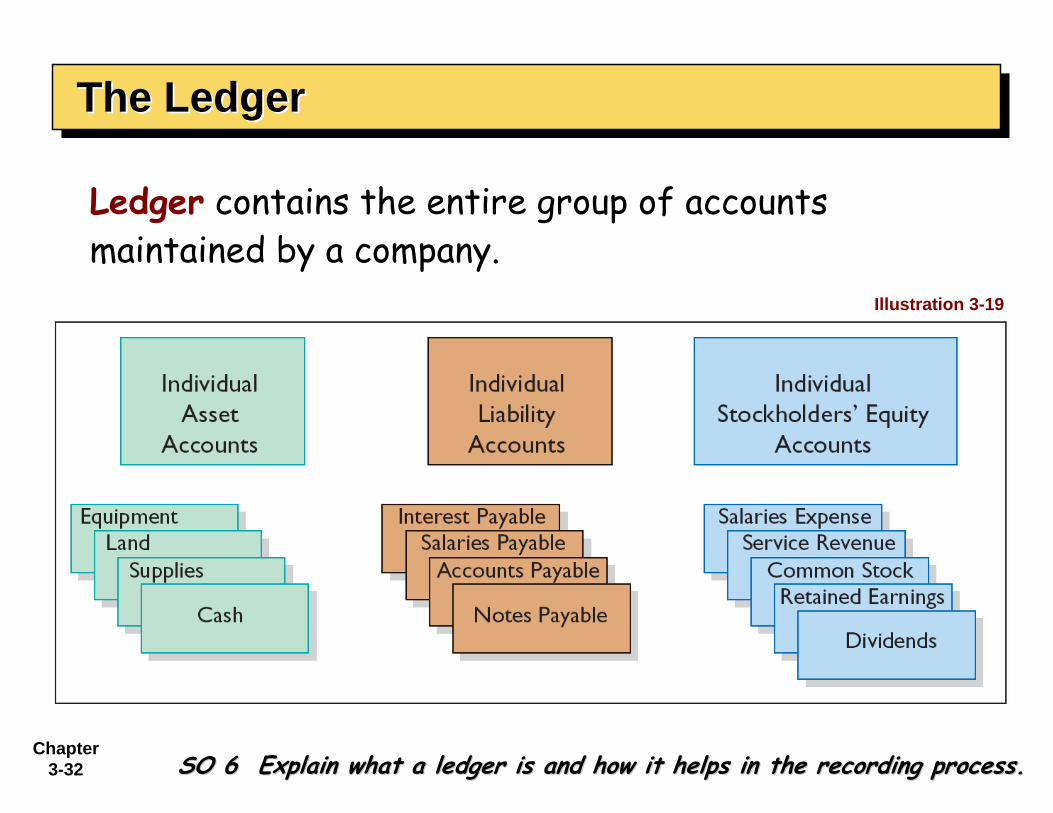

Ledger contains the entire group of accounts maintained by a company.

The LedgerThe LedgerThe Ledger

SO 6 Explain what a ledger is and how it helps in the recordingSO 6 Explain what a ledger is and how it helps in the recording process.process.

Illustration 3-19

Chapter 3-33

Accounts arranged in sequence in which they are presented in the financial statements.

Chart of AccountsChart of AccountsChart of Accounts

SO 6 Explain what a ledger is and how it helps in the recordingSO 6 Explain what a ledger is and how it helps in the recording process.process.

Chapter 3-34

Posting Posting – the process of transferring amounts from the journal to the ledger accounts.

Cash Acct. No. 101Date Explanation Ref. Debit Credit Balance

General Ledger

Date Account Title Ref. Debit Credit

Oct. 1 Cash 10,000 Common stock 10,000

General Journal

Oct. 1 Owner investment J1 10,000 10,000

101

J1

PostingPostingPosting

SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Chapter 3-35

The Recording Process IllustratedThe Recording Process IllustratedThe Recording Process Illustrated

SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Follow these steps:

1. Determine what type of account is involved.

2. Determine what items increased or decreased and by how much.

3. Translate the increases and decreases into debits and credits.

Illustration 3-21

Chapter 3-36

The Recording Process IllustratedThe Recording Process IllustratedThe Recording Process Illustrated

SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Follow these steps:

1. Determine what type of account is involved.

2. Determine what items increased or decreased and by how much.

3. Translate the increases and decreases into debits and credits.

Illustration 3-22

Chapter 3-37

The Recording Process IllustratedThe Recording Process IllustratedThe Recording Process Illustrated

SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Follow these steps:

1. Determine what type of account is involved.

2. Determine what items increased or decreased and by how much.

3. Translate the increases and decreases into debits and credits.

Illustration 3-23

Chapter 3-38 SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Illustration 3-24

Additional Transactions

The Recording Process Illustrated

The The Recording Recording Process Process IllustratedIllustrated

Chapter 3-39 SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Illustration 3-25

Additional Transactions

The Recording Process Illustrated

The The Recording Recording Process Process IllustratedIllustrated

Chapter 3-40 SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Illustration 3-26

Additional Transactions

The Recording Process Illustrated

The The Recording Recording Process Process IllustratedIllustrated

Chapter 3-41 SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Illustration 3-27

Additional Transactions

The Recording Process Illustrated

The The Recording Recording Process Process IllustratedIllustrated

,

Chapter 3-42 SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Illustration 3-28

Additional Transactions

The Recording Process Illustrated

The The Recording Recording Process Process IllustratedIllustrated

Chapter 3-43 SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

The Recording Process IllustratedThe Recording Process IllustratedThe Recording Process Illustrated

Additional Transactions

Illustration 3-29

Chapter 3-44 SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Illustration 3-30

Additional Transactions

The Recording Process Illustrated

The The Recording Recording Process Process IllustratedIllustrated

Chapter 3-45 SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Illustration 3-31

Additional Transactions

The Recording Process Illustrated

The The Recording Recording Process Process IllustratedIllustrated

Chapter 3-46

Summary Illustration of JournalizingSummary Illustration of JournalizingSummary Illustration of Journalizing

SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Illustration 3-32

Chapter 3-47

Summary Illustration of JournalizingSummary Illustration of JournalizingSummary Illustration of Journalizing

SO 7 Explain what posting is and how it helps in the recording SO 7 Explain what posting is and how it helps in the recording process.process.

Illustration 3-32

Chapter 3-48

Summary Illustration of Posting

Summary Summary Illustration Illustration of Postingof Posting

Illustration 3-33

Chapter 3-49

A list of accounts and their balances at a given time.

Purpose is to prove that debits equal credits.

The Trial BalanceThe Trial BalanceThe Trial Balance

Illustration 3-34

Chapter 3-50

Copyright © 2009 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

CopyrightCopyrightCopyright