Kick Start your 2021 Financial Year - Nexia

47

Kick Start your 2021 Financial Year 21 July 2020

Transcript of Kick Start your 2021 Financial Year - Nexia

Kick Start your 2021 Financial Year

21 July 2020

Presenters

Raoul StevensonSenior Manager, Business Advisory

Adelaide Office

Ian StoneDirector, Business Advisory

Sydney Office

David MontaniNational Tax Director

Nexia Australia

Introduction

Difficult and challenging period

Particularly affected industries:

Hospitality

Tourism

Retail

Wine industry embodies all of the above

Unique issues

3

Today’s session

Forward Tax Planning – Right Through to Business Sale

The New Normal

Wine Industry Matters

4

Forward Tax Planning

5

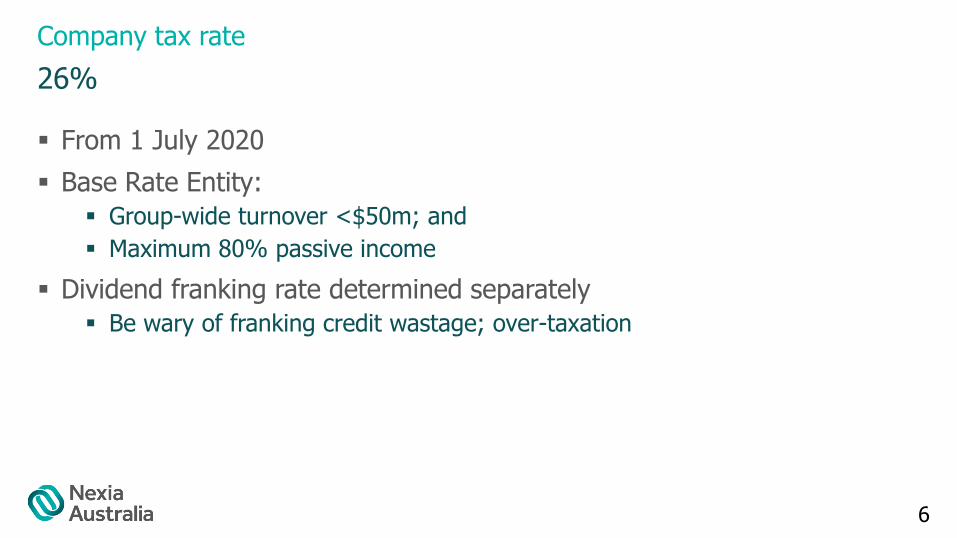

Company tax rate

From 1 July 2020

Base Rate Entity:

Group-wide turnover <$50m; and

Maximum 80% passive income

Dividend franking rate determined separately

Be wary of franking credit wastage; over-taxation

26%

6

Closing stock value

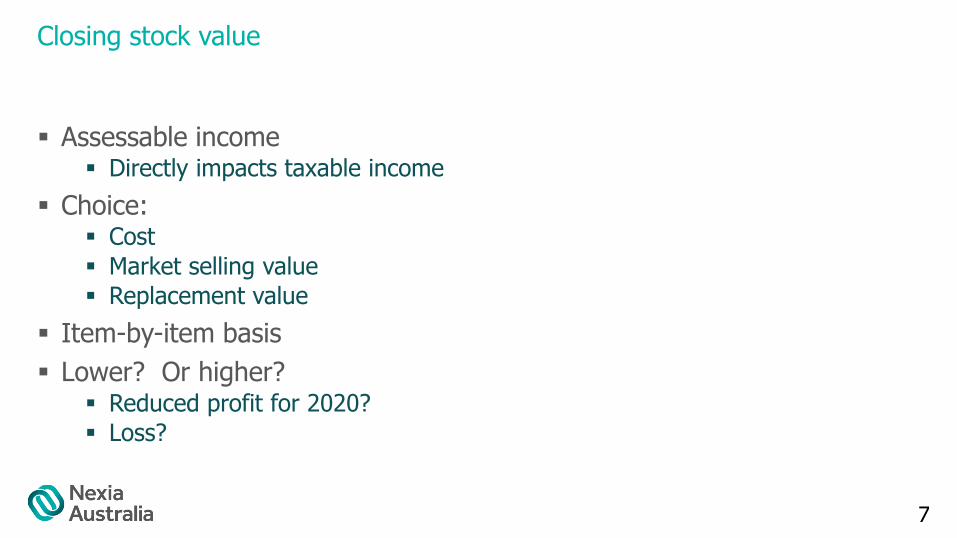

Assessable income Directly impacts taxable income

Choice: Cost

Market selling value

Replacement value

Item-by-item basis

Lower? Or higher? Reduced profit for 2020?

Loss?

7

Superannuation for employees

9.5% of OTE

Due 28th day after each quarter

eg, June 2020 quarter due 28 July 2020

Allow additional time if using a Clearing House

If miss 28th deadline – do not subsequently pay SG to super fund

Lodge SG statement, pay SG charge

Within one month of 28th

Deadline

8

Superannuation for employees

Unpaid super for 1 July 1992 to 31 March 2018

7 September 2020 deadline

Tax deductible; no penalties

If decline to take up amnesty:

Non-deductible

100% penalty

$20 per-employee, per-quarter administrative penalty

Amnesty

9

Bad debts

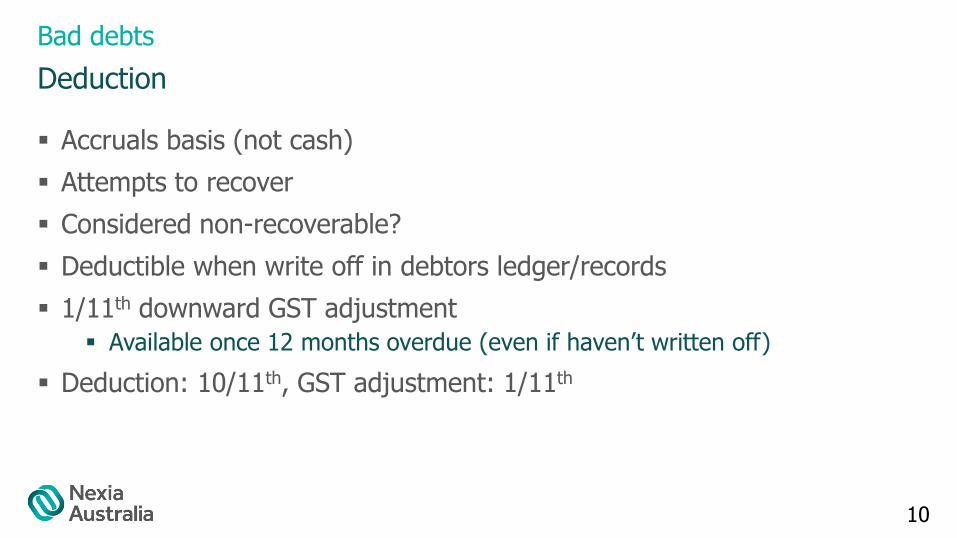

Accruals basis (not cash)

Attempts to recover

Considered non-recoverable?

Deductible when write off in debtors ledger/records

1/11th downward GST adjustment

Available once 12 months overdue (even if haven’t written off)

Deduction: 10/11th, GST adjustment: 1/11th

Deduction

10

Instant asset write-off

Increased from $30k to $150k, 12 March to 31 December 2020

Cost, net of GST credit, must be less than $150,000

Group-wide turnover <$500 million (up from $50m)

New or second-hand, internally constructed

Installed, ready for use by 31 December 2020

Car limit: $57,581

From 1 January 2021, reverts to: Small Business Entities only: <$10m group-wide turnover Must be using pooling <$1,000

11

Accelerated depreciation

New depreciable assets only

Group-wide turnover <$500 million

Used/installed between 12 March and 30 June 2021

50% up-front deduction for asset’s cost

Remainder depreciated in usual manner

No limit on asset cost

Except car limit: $57,581

12

Concessions for small business entities

$150k instant asset write-off

Depreciation pooling

Immediate deduction for start-up costs

Deduction for certain prepaid expenses

Simplified trading stock rules

Simplified PAYG tax instalment rules

Cash basis for GST, ATO-calculated GST instalments

FBT exemption for car parking, multiple devices

Capital gains tax roll-over

Group-wide turnover <$10 million

13

Business exit concessions

Conditions

Just before sale

Period of time

Integrity rules

Think about this: $4 million x 47% = $1.88 million

Tax impost: between 0% and 47%

You keep at least53%

Up for grabs:47%

14

Business Horizon Review

Identify currently present concession disqualifiers. eg:

Legal/equity structure

50% discount

Small business relief

Pre-CGT

Asset protection

Non-deal asset extractions

15

Ideal timing

Tax advice – before sale/transaction

Groom business for sale – 2 years minimum

Business Horizon Review – anytime

16

The New Normal –2021 and Beyond

17

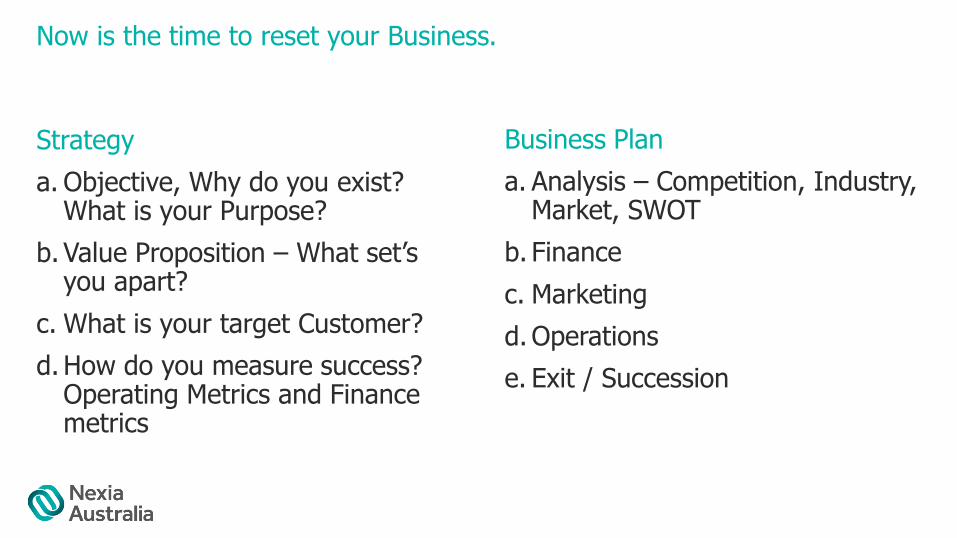

Now is the time to reset your Business.

Strategy

a. Objective, Why do you exist? What is your Purpose?

b. Value Proposition – What set’s you apart?

c. What is your target Customer?

d. How do you measure success? Operating Metrics and Finance metrics

Business Plan

a. Analysis – Competition, Industry, Market, SWOT

b. Finance

c. Marketing

d. Operations

e. Exit / Succession

Business Plan

Finance

• Review Operating Structure -risk

• Cash flow forecasts - Cash in not King it is Oxygen

• Budgets

• Review Pricing

• Review Banking Facilities / Working Capital Capacity

• Taxation Obligations

• Insurance review – bush fires ??

Marketing

• Review – what has gone well, what can we stop

• Distribution Model

• Mailing lists

• Web site

• Everyone in your team represents your Brand

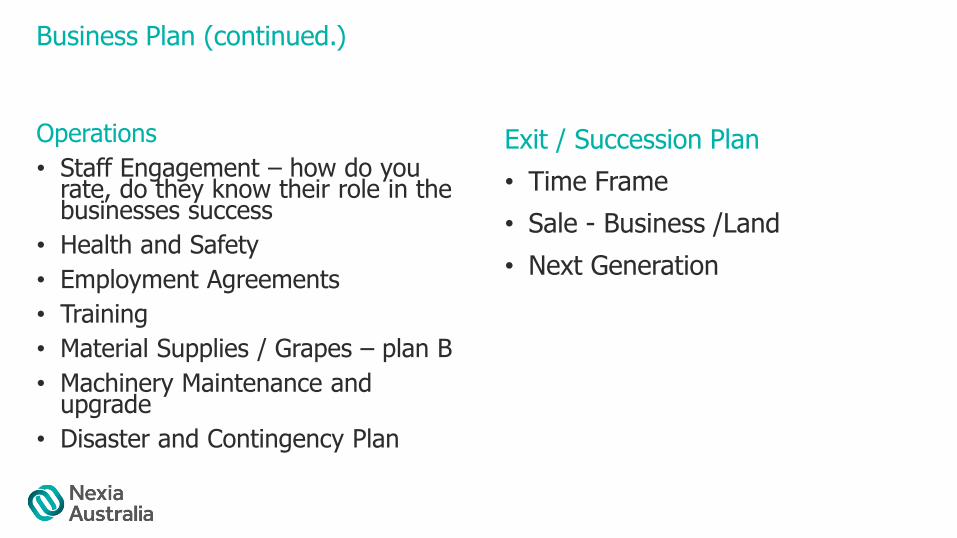

Business Plan (continued.)

Operations

• Staff Engagement – how do you rate, do they know their role in the businesses success

• Health and Safety

• Employment Agreements

• Training

• Material Supplies / Grapes – plan B

• Machinery Maintenance and upgrade

• Disaster and Contingency Plan

Exit / Succession Plan

• Time Frame

• Sale - Business /Land

• Next Generation

Monitoring Your Performance

Traffic Light System

Has not commenced or

Not achieved

Progressing/Changes Required

Completed

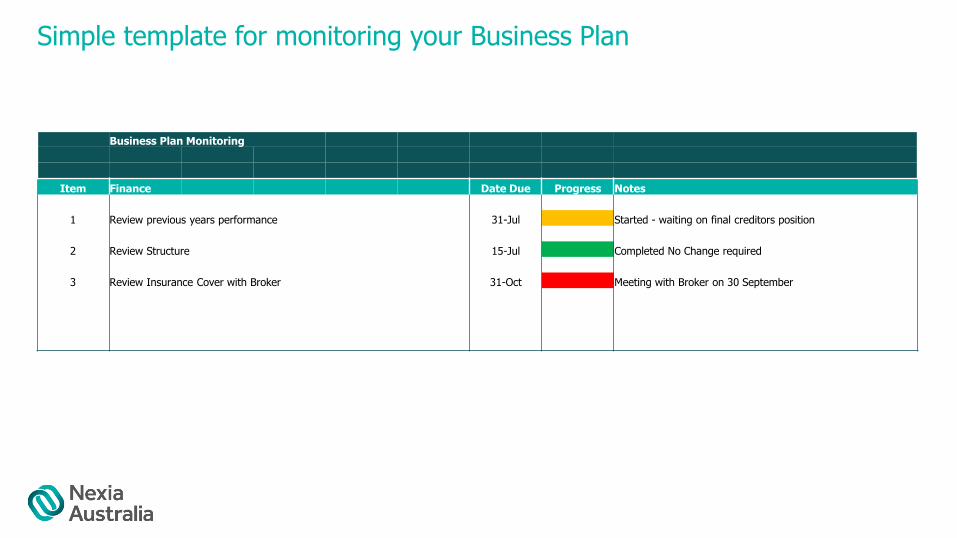

Simple template for monitoring your Business Plan

Business Plan Monitoring

Item Finance Date Due Progress Notes

1 Review previous years performance 31-Jul Started - waiting on final creditors position

2 Review Structure 15-Jul Completed No Change required

3 Review Insurance Cover with Broker 31-Oct Meeting with Broker on 30 September

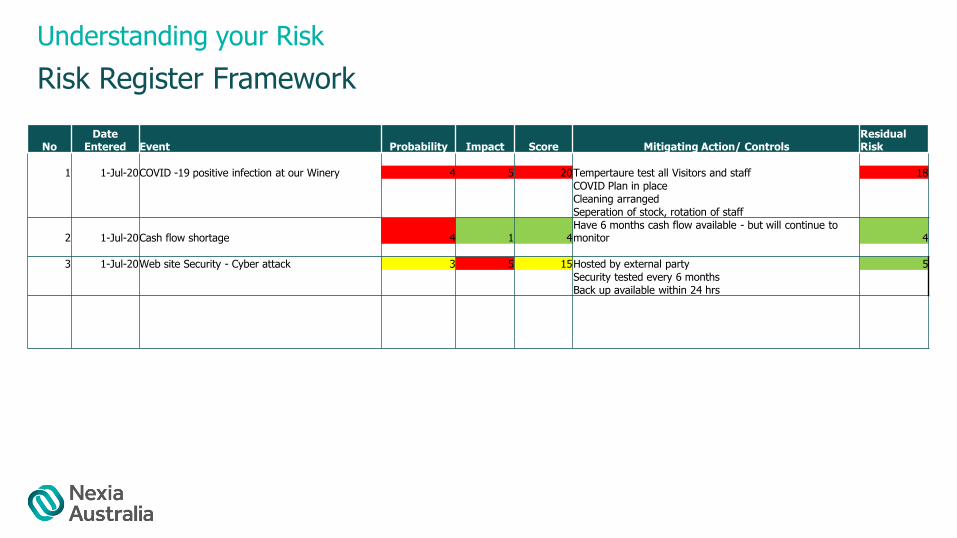

Understanding your Risk

NoDate

Entered Event Probability Impact Score Mitigating Action/ ControlsResidual Risk

1 1-Jul-20COVID -19 positive infection at our Winery 4 5 20Tempertaure test all Visitors and staff 18

COVID Plan in place

Cleaning arranged

Seperation of stock, rotation of staff

2 1-Jul-20Cash flow shortage 4 1 4Have 6 months cash flow available - but will continue to monitor 4

3 1-Jul-20Web site Security - Cyber attack 3 5 15Hosted by external party 5

Security tested every 6 months

Back up available within 24 hrs

Risk Register Framework

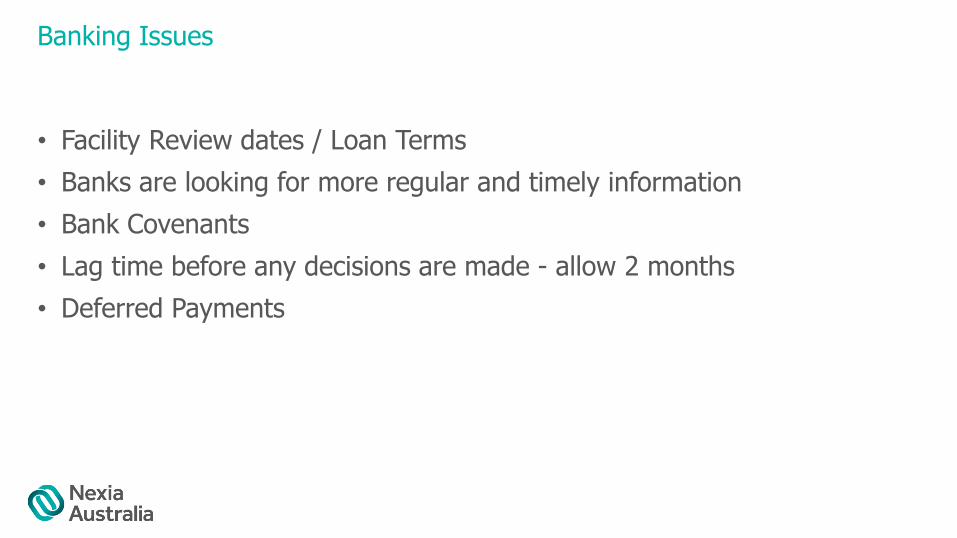

Banking Issues

• Facility Review dates / Loan Terms

• Banks are looking for more regular and timely information

• Bank Covenants

• Lag time before any decisions are made - allow 2 months

• Deferred Payments

Building working capital and additional capacity

• Normal Ratio is Current Assets / Current Liabilities 1 to 2 is good however if you cannot sell your stock?

• How many months cash or cash and stock which can be sold do you need? 3 – 6 months

• Cash Flow modeling - sensitivity , different scenarios

• Fixed Costs vs Variable Costs

• Contingency Costs

Building Capacity

• Converting short term debt to long term

• Extending Trading terms with Suppliers

• Debtors – personal approach

• Reduce discretionary spending

• Address slow moving stock quickly

Government SME Guarantee Scheme

Government Guarantee 50% of new loans

Turnovers up to $50m

Maximum loan originally $250k now $1m

Working capital or Investment

Loans up to 3 years and now 5 years – 6 monthly repayment holiday

Unsecured Finance

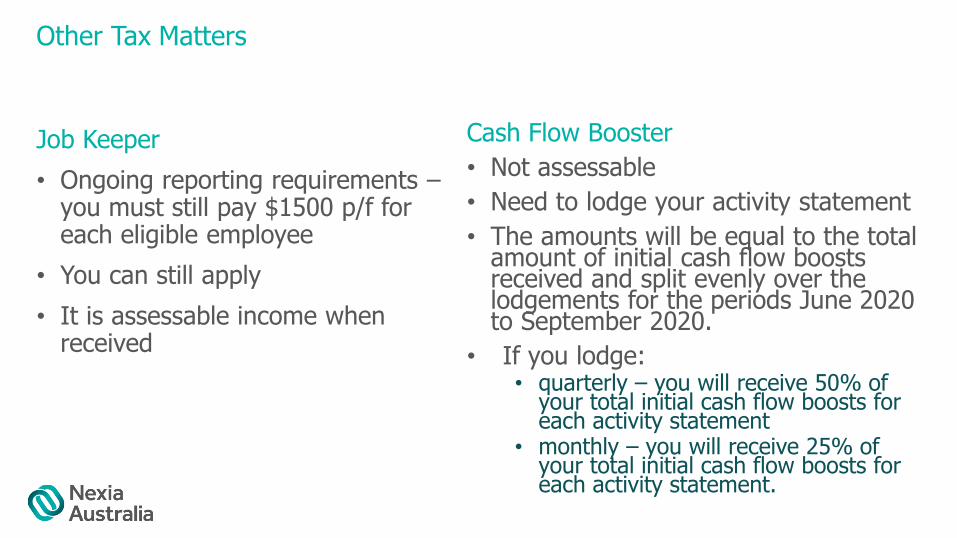

Other Tax Matters

Job Keeper

• Ongoing reporting requirements –you must still pay $1500 p/f for each eligible employee

• You can still apply

• It is assessable income when received

Cash Flow Booster

• Not assessable

• Need to lodge your activity statement

• The amounts will be equal to the total amount of initial cash flow boosts received and split evenly over the lodgements for the periods June 2020 to September 2020.

• If you lodge:• quarterly – you will receive 50% of

your total initial cash flow boosts for each activity statement

• monthly – you will receive 25% of your total initial cash flow boosts for each activity statement.

Wine Industry Matters

28

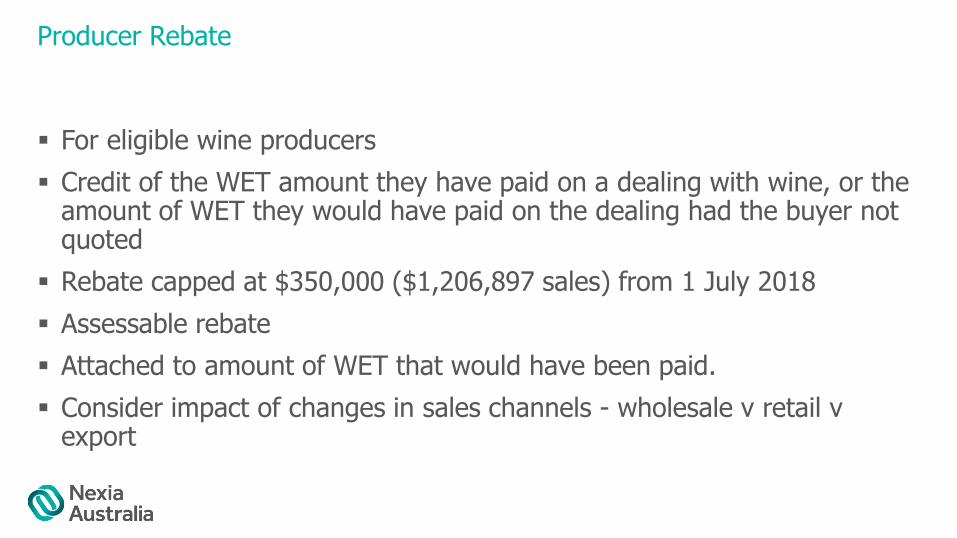

Producer Rebate

For eligible wine producers

Credit of the WET amount they have paid on a dealing with wine, or the amount of WET they would have paid on the dealing had the buyer not quoted

Rebate capped at $350,000 ($1,206,897 sales) from 1 July 2018

Assessable rebate

Attached to amount of WET that would have been paid.

Consider impact of changes in sales channels - wholesale v retail v export

Eligibility Criteria

From 1 July 2018 onwards, to qualify for WET rebates on assessable dealings in wine, a producer will need to satisfy the:

85% ownership of source product requirement

Packaging requirement

WET payment requirement

A producer is an entity that:

Manufactures wine, or

Supplies source product to another entity for that other entity to manufacture wine on its behalf

Still qualify as a producer if wine produced by contracted winemaker

85% Ownership Requirement

A producer will satisfy the 85% ownership requirement, for a parcel of wine, if:

At least 85% of that wine by volume in its final form, packaged for retail sale, was produced from source product owned by the producer before the winemaking process commenced, and

The producer maintained ownership of that source product and the resultant wine throughout the winemaking process

Producers need to keep evidence of ownership of the source products

Potential consequences for blending and pooling

Restructure warning Change in operating entity and owner of stock

Rebate at risk

Source Product

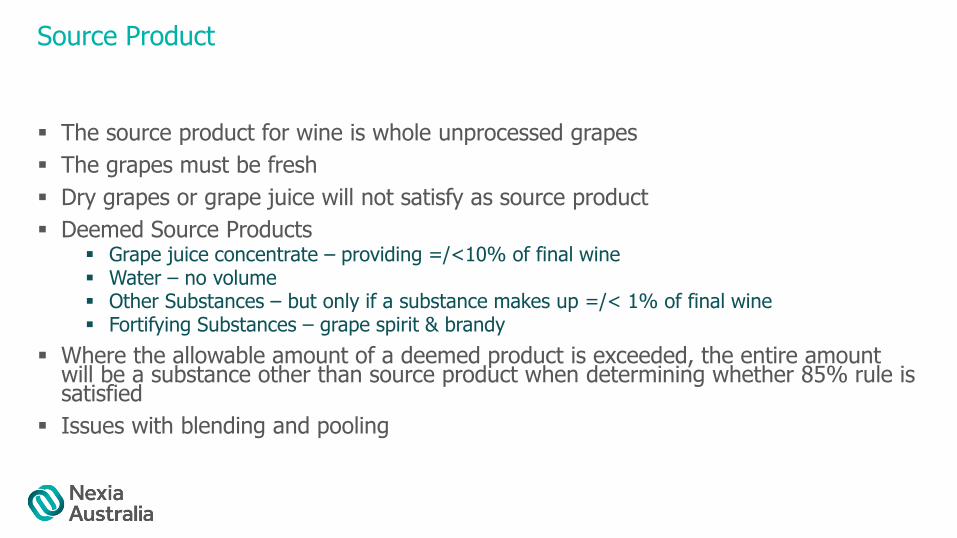

The source product for wine is whole unprocessed grapes

The grapes must be fresh

Dry grapes or grape juice will not satisfy as source product

Deemed Source Products Grape juice concentrate – providing =/<10% of final wine Water – no volume Other Substances – but only if a substance makes up =/< 1% of final wine Fortifying Substances – grape spirit & brandy

Where the allowable amount of a deemed product is exceeded, the entire amount will be a substance other than source product when determining whether 85% rule is satisfied

Issues with blending and pooling

Source Product

Must own all of the source product necessary to meet the 85% ownership requirement:

Before crushing & maintain ownership throughout wine-making process

Ownership = good title to source product

Need evidence of ownership

Grape purchase invoices

Weighbridge records

Production records

Grape supply contracts

Packaging Requirement

To satisfy the packaging requirement, wine must be:

Packaged in a container not exceeding 5 litres, suitable for retail sale

Branded with:

A registered trade mark

A trade mark for which registration is pending, or

A trade mark that has been used in the course of trade from 1 July 2015 to the time of an assessable dealing in the wine

The trade mark must be owned by the producer or an associate

WET Payment Requirement

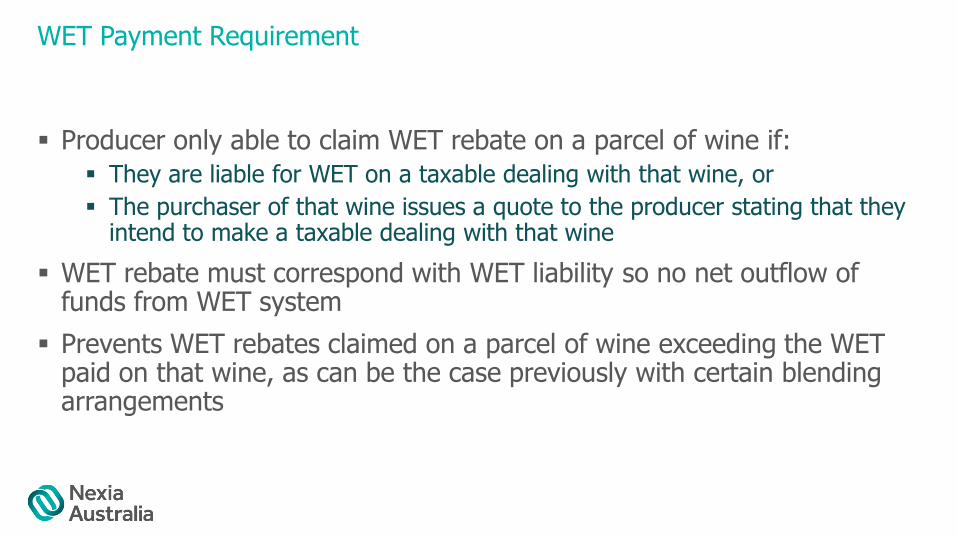

Producer only able to claim WET rebate on a parcel of wine if:

They are liable for WET on a taxable dealing with that wine, or

The purchaser of that wine issues a quote to the producer stating that they intend to make a taxable dealing with that wine

WET rebate must correspond with WET liability so no net outflow of funds from WET system

Prevents WET rebates claimed on a parcel of wine exceeding the WET paid on that wine, as can be the case previously with certain blending arrangements

2018 and Earlier Vintages

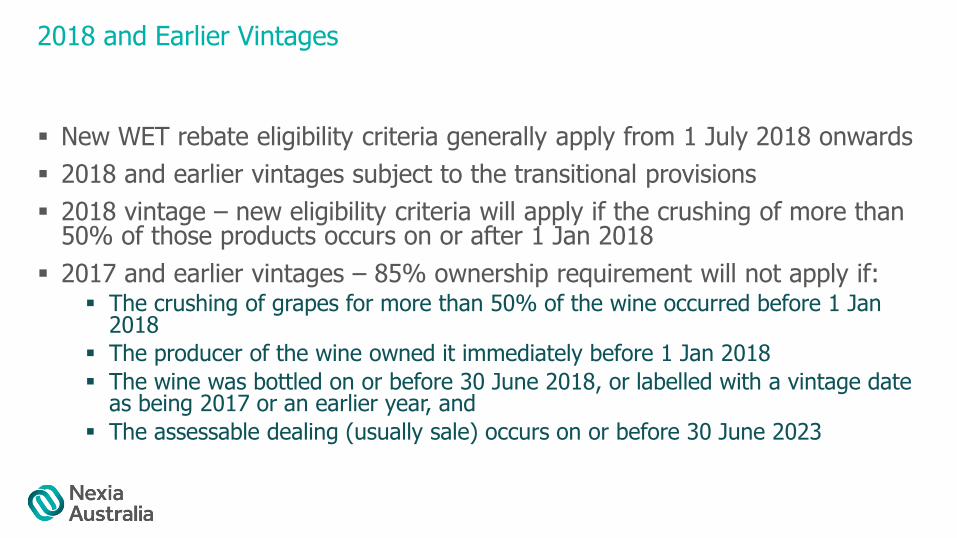

New WET rebate eligibility criteria generally apply from 1 July 2018 onwards

2018 and earlier vintages subject to the transitional provisions

2018 vintage – new eligibility criteria will apply if the crushing of more than 50% of those products occurs on or after 1 Jan 2018

2017 and earlier vintages – 85% ownership requirement will not apply if: The crushing of grapes for more than 50% of the wine occurred before 1 Jan

2018

The producer of the wine owned it immediately before 1 Jan 2018

The wine was bottled on or before 30 June 2018, or labelled with a vintage date as being 2017 or an earlier year, and

The assessable dealing (usually sale) occurs on or before 30 June 2023

Quoting

Buyer quotes ABN to seller in approved form – transaction become exempt from WET

Producers only able to claim WET rebate on sales made ‘under quote’ indicating that the purchaser intends to make a taxable dealing with the wine

Once WET is paid on wine, it can no longer be sold under quote

Quotes required to indicate if purchaser intends to: Make a GST-free supply of the wine

Sell the wine under quote (by making another wholesale sale of the wine)

Use the wine as an input in the manufacture of further wine or wine product

If purchaser quotes, absolutely liable to remit WET on that wine – no exemption of exclusion

Purchase liable for WET even if they make a GST-free supply for the wine, sell the wine under quote or use the win as an input in manufacture

Common Errors

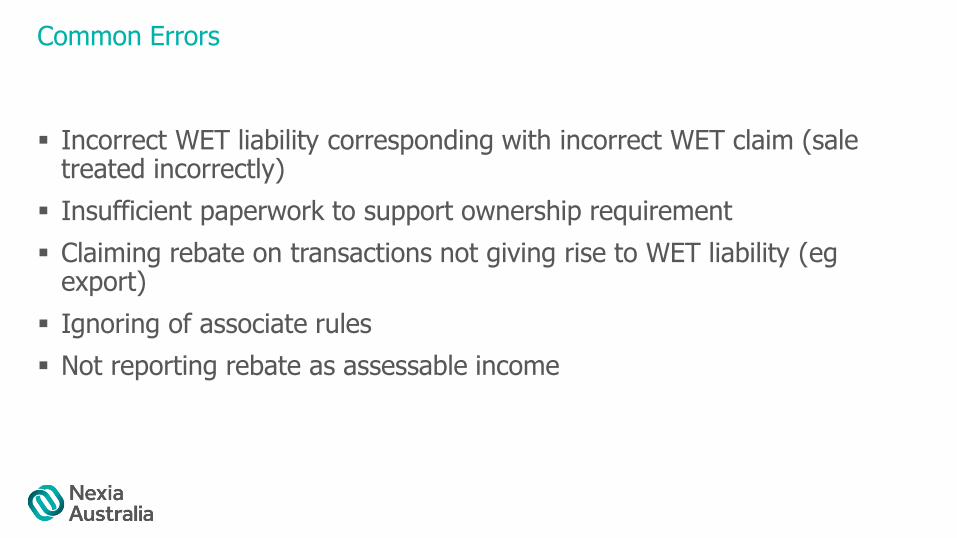

Incorrect WET liability corresponding with incorrect WET claim (sale treated incorrectly)

Insufficient paperwork to support ownership requirement

Claiming rebate on transactions not giving rise to WET liability (egexport)

Ignoring of associate rules

Not reporting rebate as assessable income

Grants for Wine Industry

Wine Tourism and Cellar Door Grant (round 2 applications open shortly)

Export Market Development Grants (EMDG)

National

Grants for Wine Industry

Small Business Support Grant – Bushfires (applications close 30 Sep 2020)

Small Business Bushfire Recovery Grant

PIRSA Financial Support after Bushfire

Smoke Taint Grants

Export Accelerator Grant

South Australia

Grants for Wine Industry

Small Business Support Grant - Bushfires

Small Business Recovery Grant – COVID19

Small Business Recovery Grant - Bushfires

Primary Producers Special Disaster Grant – Bushfires (Low interest loans are also available)

Bushfire Supply Chain Support Grant (closed 12 June 2020)

Smoke Taint Grants

New South Wales

Grant for Wine Industry

International Competitiveness Co-investment Fund

Western Australia

42

Conclusion

Wine industry issues, opportunities

Grants

Forward planning, manage outcomes

New normal

Nexia expertise

43

Nexia Australia Wine Industry Specialists

Adelaide

Raoul Stevenson [email protected]

Grantley Stevens [email protected]

Robert Prime [email protected]

Brisbane

Sarah Richmond [email protected]

Shaye Eyre [email protected]

Canberra

Mark O’Shaughnessy [email protected]

Melbourne

Perth

Dean Birch [email protected]

Sydney

Ian Stone [email protected]

Adam Boles [email protected]

44

Your feedback

You will soon receive an e-mail with a link to a short online feedback form

Please let us know what you think of this session

Important Disclaimer

The material contained in this presentation is in the nature of general comment only, and neither purports, nor is intended, to be advice on any particular matter. Readers should not act or rely upon any matter or information contained in or implied by this presentation without taking appropriate professional advice which relates specifically to their particular circumstances. The publishers, authors, consultants, editors and presenters expressly disclaim all and any liability to any person who acts or fails to act as a consequence of reliance upon the whole or any part of this presentation.

57

Thank you

If you would like to discuss anything further, please do not hesitate to contact us.