Keyera PowerPoint Presentation · • 1,290 undeveloped acres in Alberta’s industrial heartland....

40

Keyera Corp. December 2019 Corporate Profile March 2020 Issued March 15

Transcript of Keyera PowerPoint Presentation · • 1,290 undeveloped acres in Alberta’s industrial heartland....

Keyera

Corp

. D

ecem

ber

2019

Corporate Profile

March 2020 Issued March 15

Forward-Looking Information & Non-GAAP Measures

2

In the interests of providing Keyera Corp. (“Keyera” or the “Company”) shareholders and potential investors with information regarding Keyera, including

Management’s assessment of future plans and operations relating to the Company, this document contains certain statements and information that are forward-

looking statements or information within the meaning of applicable securities legislation, and which are collectively referred to herein as “forward-looking

statements". Forward-looking statements in this document include, but are not limited to statements and tables with respect to: capital projects and

expenditures; strategic initiatives; anticipated producer activity and industry trends; and anticipated performance. Readers are cautioned not to place undue

reliance on forward-looking statements, as there can be no assurance that the plans, intentions or expectations upon which they are based will occur. By their

nature, forward looking statements involve numerous assumptions, as well as known and unknown risks and uncertainties, both general and specific, that

contribute to the possibility that the predictions, forecasts, projections and other forward-looking statements will not occur and which may cause Keyera’s actual

performance and financial results in future periods to differ materially from any estimates or projections of future performance or results expressed or implied by

the forward-looking statements. These assumptions, risks and uncertainties include, among other things: Keyera’s ability to successfully implement strategic

initiatives and whether such initiatives yield the expected benefits; future operating results; fluctuations in the supply and demand for natural gas, NGLs, crude

oil and iso-octane; assumptions regarding commodity prices; activities of producers, competitors and others; the weather; assumptions around construction

schedules and costs, including the availability and cost of materials and service providers; fluctuations in currency and interest rates; credit risks; marketing

margins; potential disruption or unexpected technical difficulties in developing new facilities or projects; unexpected cost increases or technical difficulties in

constructing or modifying processing facilities; Keyera’s ability to generate sufficient cash flow from operations to meet its current and future obligations; its

ability to access external sources of debt and equity capital; changes in laws or regulations or the interpretations of such laws or regulations; political and

economic conditions; and other risks and uncertainties described from time to time in the reports and filings made with securities regulatory authorities by

Keyera. Readers are cautioned that the foregoing list of important factors is not exhaustive. The forward-looking statements contained in this document are

made as of the date of this document or the dates specifically referenced herein. All forward-looking statements contained in this document are expressly

qualified by this cautionary statement. This document also includes financial measures that are not determined in accordance with Generally Accepted

Accounting Principles (“GAAP”). For additional information on non-GAAP measures and forward-looking statements, refer to Keyera’s public filings available on

SEDAR at www.sedar.com and available on the Keyera website at www.keyera.com.

A Leading Canadian Based Midstream Company

3

COMPANY OVERVIEW

Responsible & reliable midstream service provider• decades of operating complex facilities safely

• focused on customer service

• strong track record of financial performance & dividend growth

Highly integrated, difficult to replicate business• provide customers full range of essential midstream services

Core infrastructure strategically located in WCSB• key producing areas in liquids-rich Montney & Duvernay

• liquids infrastructure at Edmonton/Ft. Sask major liquids hub

Predominately fee-for-service cash flows• virtually no direct commodity price exposure for Gathering &

Processing and Liquids Infrastructure businesses

Low leverage provides financial flexibility • supports BBB/Stable5 credit rating enabling future growth

Meaningful ongoing growth capital investments• history of strong returns on capital

KAPS a new strategic asset providing a platform for growth

KEYERA NUMBERS AT A GLANCE1

$7.0 billion2

Market capitalization

$9.8 billion2

Enterprise value

$944 million3

2019 Adjusted EBITDA

6.0%4

Dividend yield

$700 – 800 million2020 Growth capital program

67%3

2019 payout ratio

2.7x6

Net debt/EBITDA ratio

1. All information as at December 31, 2019, unless otherwise stated. 2. As at February 28, 2020. 3. Adjusted EBITDA, Payout Ratio, return on capital, and EBITDA are not standard measures under GAAP.

See “non-GAAP Financial Measures” in Keyera’s 2019 Year End MD&A for further details. 4. Calculated using Keyera’s share price as at February 28, 2020 and annual dividend of $1.92 per common share. 5. DBRS and S&P. 6. Net Debt + 50% of hybrid subordinated debt divided by trailing Adjusted EBITDA.

Committed to Responsible Growth

4

Prioritizing our people & safety • Targeting zero safety incidents

• Recognized as a Top Employer in Canada & Alberta

Committed to corporate governance• ESG board and committee oversight

• Independent and diverse Board (>30% female directors)

Improving our environmental performance• Initiatives to reduce green house gas & methane emissions

Engaged with our communities• Volunteered >7,000 hours to community causes in 2019

• Strong relationships & partnerships with local residents &

Indigenous communities

Our Recent ESG Ratings

5

SUSTAINALYTICS

“OUTPERFORMER” RATING

MSCI

“A” RATING

Peer Benchmarking

LARGEST 5 INDUSTRY PEERS

(OIL & GAS REFINING, MARKETING,

TRANSPORTATION & STORAGE) Rating Trends

Keyera Corp. A ▲

Enbridge Inc. A ◄►

PHILLIPS 66 BBB ◄►

TC Energy BBB ◄►

Reliance Industries Limited BB ▲

Kinder Morgan, INC. BB ◄►

RATING TREND KEY: Maintain ◄► Upgrade ▲

Refiners & Pipelines (Industry Group)

6

Business is Highly Integrated & Difficult to Replicate

Raw

Gas

Gathering

Compression

Sweetening

NGL extraction

EX

TR

AC

TIO

N

CO

NS

UM

PT

IO

N

GATHERING & PROCESSING

Marketing

Ethane

Propane

Butane

Condensate

Iso-octane

Margin

En

d M

ark

ets

Oil

Sands

LIQUIDS BUSINESS UNIT

Fractionation

Storage

Transportation

~64%1 Fee for Service

1. Percentage of total realized margin for the last twelve months ended December 31, 2019. Realized margin is defined as operating margin excluding unrealized gains and losses from commodity-

related risk management contracts. Realized margin is not a standard measure under GAAP.

Gathering & Processing

Liquids Infrastructure

Under Construction

FORT

ST.JOHN

DAWSON

CREEK

FORT McMURRAY

CALGARY

EDMONTON

Simonette

South Cheecham

Terminal

Rimbey Pipeline

Fort Saskatchewan

PipelinesEdson

Ricinus

Rimbey

Strachan

Nordegg River

Brazeau River

West Pembina

Zeta Creek

Pembina

North

Alder

Flats

Minnehik

Buck Lake

Bigoray

Cynthia

Brazeau North

Josephburg Terminal

Dow Fort Saskatchewan

Keyera Fort Saskatchewan

Alberta Crude Terminal

Alberta Diluent Terminal

Edmonton Terminal

Alberta EnviroFuels

Base Line Terminal

A L B E R T AB.C.

GRANDE PRAIRIE

Pipestone

Wapiti

Infrastructure is Strategically Located

7

Full suite of services in liquids-rich Montney• Growing production in the area, driven by strong returns

• Keyera’s 3 gas plants will provide a meaningful position

• KAPS will be 1 of 2 pipelines providing liquids egress

Liquids infrastructure assets in high demand • Fractionation capacity fully utilized; storage highly utilized

• Industry-leading condensate handling system

• Keyera’s assets and connectivity are difficult to replicate

Positioned for future growth• Current capital program provides secured growth to 2022

• KAPS provides platform for next phase of growth

• 1,290 undeveloped acres in Alberta’s industrial heartland

Our Strategy & Capital Investment Considerations

8

Deliver steady

DISCIPLINED GROWTHto create long-term value for shareholders

by investing in projects that are

Complementary to our capabilities & competitive advantages

Backed by contracts that provide secure long-term cash flow

Supportive of corporate annual return on capital* of 10% - 15%

9

Capital Structure Provides Capacity & Flexibility

ISSUER CREDIT RATINGS

DBRS Limited: BBB with a Stable trend

S&P Global: BBB/Stable

2.7x NET DEBT1 TO EBITDAMidstream Peer Group3 Average >4.6x4

1. Calculated as of December 31, 2019 - Keyera methodology assumes Net Debt includes 50% of hybrid subordinated debt. For further information regarding covenant calculations, please see

Keyera’s 2019 Annual Report MD&A or copies of the note purchase agreements, all of which are filed on SEDAR. 2. All US dollar denominated debt is translated into Canadian dollars at its swap rate.3. Midstream Peer Group includes ENB, GEI, IPL, PPL, and TRP. 4. Source Peters & Co. as of February 18, 2020. 5.$600MM Hybrid Note issuance is callable after 10 years in June 2029.

LONG-TERM DEBT MATURITIES2

(excludes drawings under revolver)

$700

$600

$500

$400

$300

$200

$100

$0

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029

$109$60 $30

$143 $264 $230 $400 $267

$75

Hybrid Note

Public Debt

Private Notes

C$

MM

$400 $6005

Financial Priorities

Financial Priorities Target 2019 2018 2017

Continue disciplined

capital allocation

Fee-for-Service

contribution of

Realized Margin> 75% 64% 66% 80%

Annual Return

on Capital program1 10% - 15% n/a n/a n/a

Preserve

financial flexibility

Credit ratings BBB BBB BBB BBB

Net Debt / Adjusted

EBITDA1,2 2.5x - 3.0x 2.7x 2.7x 2.4x

Long-term

dividend Payout Ratio 50% - 70% 67% 56% 61%

Grow dividend steadily

10

1. Not standard measures under GAAP. See “Forward-Looking Information & Non-GAAP Financial Measures” slide. 2. Net Senior Debt + 50% of hybrid subordinated debt divided by trailing Adjusted EBITDA.

Growing Fee-for-Service Realized Margin

11

Fee-for-Service Realized Margin*

Non Fee-for-Service Realized Margin*

61%67%

80%

64%

76%

2015 2016 2017 2018

Using mid-point of base marketing

guidance

66%78%

* Non Fee-for-Service & Fee-for-Service Realized Margin are rolling LTM. With the adoption of IFRS 16, Lease Expenses are excluded from Realized Margin as of 01/01/2019. Historical

Realized Margin has not been adjusted. Non-Fee-for Service & Fee-for-Service Realized Margin are not standard measures under GAAP. See “Forward-Looking Information & Non-

GAAP Financial Measures” slide.

2019

$612

$1,054

million

million

$407million

$670million

4%

4% 11%

22%59%

5%

23%

32%

29%

11%

13%

13%

18%34%

22% Secured

AA- to AA+

A- to A+

BBB- to BBB+

Non-IG

Keyera's Credit Worthy Customer Base

12

Gathering & Processing Liquids Infrastructure Marketing

Consolidated*

* Based on 2019 revenues to December 31, 2019. Counterparty credit ratings at March 12, 2020. Secured category includes, counterparties who have prepay terms or a posted letter of credit. Parent's

credit rating used when parental guarantees exist.

15%

14%

18%37%

16%

Creditworthy counterparties

• Majority of revenue from investment grade/secured and

split rated counterparties

Mitigating credit risk

• Letters of credit, netting agreements, pre-payments

Broad domestic & international customer base

• Over 125 different fee-for-service customers

GATHERING &

Processing

Providing a Full Suite of Services in the Montney

14

Handle all products produced• condensate stabilization

• sour gas processing

• liquids extraction

• acid gas disposal

• water handling capacity

Integrate NGL egress via KAPS

Interconnect our plants to

enhance reliability & flexibility

Grande Prairie

Pipestone

Wapiti

Simonette

A L B E R T A

Wapiti Pipeline

North Cabin Pipeline

North Wapiti Pipeline

System

MONTNEY

DUVERNAY

Gas plant

Gas pipeline

NGL pipeline

NGL pipeline under construction

Source: Scotiabank 2019 Playbook. IRR reflects mid-cycle returns.

Source: RBC Capital Markets. Alberta Fairway is the Montney liquids-rich area

where Keyera’s Simonette, Wapiti, & Pipestone gas plants and KAPS assets are

located.

MONTNEY

PRODUCTION GROWTH

Alberta

Fairway

2.4 bcfe/d

0.6 bcfe/d

Q3 20192014

Producers Investing in the Montney

15

+1.8 bcfe/d

Karr /

Pipestone

Montney

0%

10%

20%

30%

60%

70%

Kaybob

Duvernay

Elmworth

Montney

Bigstone /

Placid

Montney

50%

40%

US$65/bbl WTI

US$55/bbl WTI

US$45/bbl WTI

MONTNEY REGION

RETURNS

Are

a I

nte

rnal

Rate

of

Retu

rn (

%)

Optimizing our Portfolio in West Central Alberta

16

Objective

Increase competitiveness &

profitability

Reduce costs & increase utilization• reduce redundant costs

• attract volumes to most efficient facilities

• increase liquids recoveries

• preserve capacity for recovery

DEEP BASIN

A L B E R T A

MONTNEY

DUVERNAY

Rimbey

14 gas plants

2.1 bcf/d capacity

49% utilization*

Edmonton

Calgary

Fort Saskatchewan

Gas plant

Gas pipeline

NGL pipeline

NGL pipeline under construction

* Based on licensed capacity and includes the Gilby plant, where operations have been suspended.

LIQUIDS

Infrastructure

18

KFS – Integrated Fractionation & Storage Assets

ASSETS & CONNECTIVITY DIFFICULT TO REPLICATE

KFS FRACTIONATION CAPACITY FULLY UTILIZED

One of four fractionation service providers in Fort Saskatchewan

65,200 bbls/d C3+ capacity & 30,000 bbls/d C2+ capacity

LARGEST UNDERGROUND STORAGE POSITION IN WCSB

~15 million barrels of storage capacity in high demand

expansion program underway to add new caverns over the next few years

COMPETITIVE ADVANTAGES

Connectivity provides customers with flexibility

Storage provides customers with reliability

Integration provides customers competitive services difficult to replicate

FUTURE GROWTH OPPORTUNITIES

Fractionation and Storage

~1,300 acres of undeveloped land nearby for future development

Keyera Fort Saskatchewan (KFS)

19

Our Industry-Leading Condensate System

KAPS

PEMBINA

NEXUS

COLD

LAKE

SUNCOR

REFINERY

SOUTH GRAND RAPIDS PIPELINE

CANADIAN

DILUENT HUB

CRW

ACCESS

PIPELINE

COCHIN

ADT

KFS

KET

PEMBINA

PLAINS

CRW, GIBSON,

TRANSMOUNTAIN

FORT

SASKATCHEWAN

PIPELINE

DOW

RIMBEY

JOSEPHBURG

SOUTHERN LIGHTS

IPL POLARIS

PIPELINE

FORT SASKATCHEWAN

CONDENSATE SYSTEM MANIFOLD NORLITE

NORTHWEST

REDWATER

20 Source: Keyera internal estimates & company reports. Wood Mackenzie for oil sands demand and forecast.

Keyera has significant

condensate storage capacity

65-70%Keyera

Peers

Keyera transports > 50%

of oil sands demand

2017

bb

ls/d

Perc

en

tag

e o

f T

ota

l D

em

an

d

0%

Oil sands demand

Oil sands forecast

60%

40%

2018 2019 2020 2021 2022

Volume % transported

on Keyera’s system

Leading Condensate Service Provider

0

200,000

400,000

600,000

800,000

80%

100%

20%

Strong Fundamentals Support Continued Growth

Source: CAPP 2019 Bitumen Forecast21

BITUMEN

PRODUCTION GROWING

CONDENSATE

SUPPLY vs DEMAND

2010

0

mb

bl/d

1,000

2,000

3,000

4,000

2015 2020 2025 2030

Oil Sands Mining

Oil Sands In-Situ

2020

0

mb

bl/d

200

400

600

800

1,200

WCSB Supply Forecast

Demand Forecast1,000

2025 2030 2035 2040

Condensate

Imports

WCSB

Condensate

Production

Source: Condensate forecast Wood Mackenzie

22

KAPS will Provide NGL Connectivity From Montney

A L B E R T A

Edmonton

Fort

Saskatchewan

Grande Prairie

Pipestone

Wapiti

KFS

OIL SANDS

MONTNEY

DEEP BASIN

DUVERNAY

SimonetteKAPS

Keyera

SemCAMS

KAPS – Key Attributes

Secure, long-term cash flow with 75% take-or-pay

Strong return on capital* of 10% - 15%, starting in 2024

Highly desired by industry

Direct connection to oil sands diluent demand

Easily integrated with owners’ gas plants

Upstream & downstream benefits

Creates a new platform for growth

23 * See “Forward-Looking Information & Non-GAAP Measures” slide.

MARKETING

MARKETING CREATES VALUE

25

Knowledge, Relationships and Infrastructure

C3 C2C4C5+iC8

$180M - $220MANNUAL BASE GUIDANCE*

WHAT WE DOBuy and Sell NGLs

Lock in sales margins and supply costs

Protect the value of our inventory

Upgrade low value products, incl C4 to iC8

Use our infrastructure to take advantage of

opportunities

WHAT WE DON’T DOSpeculative trading

Financial trading without physical product

Take frac spread exposure

* Refer to Keyera’s 2019 Year End MD&A for the assumptions. See “Forward-Looking Information & Non-GAAP Measures” slide.

STRATEGIES

GOALS

HOW WE MANAGE RISK

26

Intense Focus on Risk Management

INVENTORY RISKStored inventory is exposed to market

price fluctuations from when it is

purchased to when it is ultimately

sold, consumed, or blended

BASIS RISKCommodity purchases and

sales can be priced on different

price indexes

Protect the value of our inventory from market price fluctuations

Use physical and financial contracts to protect a high proportion of stored inventory

Reduce basis risk by aligning purchases and sales transactions on the same index

Use basis spreads to convert exposure from one index to another; match the purchases and sales indexes

27

Marketing Utilizes our Infrastructure to Create Value

C5+ CONDENSATE• Keyera’s C5+ hub creates industry liquidity

• Consumed in Alberta as diluent for bitumen

• Significant imports required to meet demand

C2 ETHANE• Sold under long-term agreements to

petrochemical producers in Alberta

• Limited spot market in western Canada

• Produced at three Keyera facilities

C3 PROPANE• Demand and pricing vary seasonally

• Keyera uses its storage and logistics to

access markets

• Majority sold into U.S. markets

• Supply exceeds demand in North America

C4 BUTANE• Sourced and consumed in Alberta

• Feedstock for iso-octane production at

Alberta EnviroFuels

iC8 Iso-octane• High quality gasoline additive

• Produced from butane at Keyera’s Alberta

EnviroFuels facility

• Majority of sales in the U.S.

28

Upgrading Butane into High Value Iso-octane

WTI

RBOB premium

Iso-octane premium

upgraded

value

STRONG CONTRIBUTORTO MARKETING*

ISO-OCTANE DEMANDIS STRONG

Superior gasoline blend stock pricing

• Lower RVP & higher octane than alternatives

• Clean burning additive with virtually no sulfur,

aromatics or benzene

Strong demand for iso-octane

• Iso-octane <1% of gasoline blend stock demand

• AEF only merchant facility in North America

• Refineries producing lower octane gasolines

• Qualities to meet changing gasoline specs

* Bar chart for illustrative purposes only; components of upgraded value do not represent actual size; cost of Butane assumed to range between 25% - 50% of WTI.

Butane

Feedstock Cost

(% of WTI)

WTI

RBOB premium

Iso-octane premium

Feedstock

29

Leveraging Our Infrastructure to Create Value

KEYERA’S

NORTH AMERICAN

VALUE CHAIN

GULF COAST MARKET

BAKKEN

CONWAY MARKET

C3C4iC8

C4C3

C3

C5

FINAL

Word

8%dividend/share

CAGR1,3

10%distributable cash

flow/share CAGR2,3

19%total annual

shareholder return2,4

31

Delivering Impressive Returns

1. Compound annual growth rate from 7/15/2003 to 12/31/2019. 2. Compound annual growth rate from 5/30/2003 to 12/31/2019. 3. Not standard measures under GAAP. See “Forward-Looking

Information & Non-GAAP Measures” slide. 4. Includes reinvestment of dividends.

What to Expect From Keyera

32

AN INCREASE IN BASE GUIDANCE2

Wildhorse completed and generating strong returns

New Galena Park investment generating strong returns

Opportunities associated with KAPS

Selectively pursue new high value niche opportunities

STEADY, DISCIPLINED GROWTH

Success with KAPS

Additional fractionation & storage capacity

Increased utilization of our condensate system

Integrated, complementary growth

Marketing

2020 2022

Pipestone

Gas Plant

Wildhorse

Terminal

Wapiti

Phase 2

Wapiti

Phase 1

Simonette

Expansion

20212019 2022 - 2024

retu

rn o

n c

ap

ital1

10% - 15%

INCREASED PROFITABILITY

Success with Montney build-out

Increase utilization of West Central Alberta portfolio to > 60%

Selectively pursue growth opportunities

Gathering & Processing

Liquids Infrastructure

1. Not a standard measure under GAAP. See “Forward-Looking Information” & “None-GAAP Financial Measures” slide. 2. Base guidance is $180 million to $220 million annually. Refer to Keyera’s 2019 Year End Report MD&A for the assumptions.

Contact Information

33

www.keyera.com

Lavonne Zdunich, CPA, CA

Director, Investor Relations

Calvin Locke, P.Eng, MBA

Manager, Investor Relations

Beata Graham, CPA, CMA

Senior Analyst, Investor Relations

888-699-4853

Keyera Corp.

Sun Life Plaza West Tower

200, 144 4 Avenue SW

Calgary, Alberta

T2P 3N4

APPENDIXOur Assets

35

Growth Projects Currently Under Development

Approved Projects Capital Cost (Net, in $ Millions)1

2020 2021 2022

Wapiti Gas Plant Complex 1,000

Wapiti Phase I (including Water Disposal System) and NWPS Phase I COMPLETE

Wapiti Phase II and Compressor & Gathering System Expansion

Simonette Acid Gas Injection & Inlet Enhancements 80 COMPLETE

Simonette Plant Expansion 71 COMPLETE

Pipestone Plant (Phase I) 600

Wildhorse Terminal US197

Storage Cavern Development Program at Keyera Fort Saskatchewan2 125

KAPS2 650

Sulphur Handling Project2 58

TOTAL ~$2.9 Billion $1.7 Billion Invested as of December 31, 2019

1. Keyera’s share of estimated capital cost. See Keyera’s 2019 Year End Report MD&A for capital investment risks and assumptions. 2. Projects expected to be completed in 2022 subject to timely receipt of regulatory approvals and construction schedule variables.

36

Simonette Gas Plant – Supporting Montney & Duvernay

INFRASTRUCTURE INCLUDES450 mmcf/d of gas processing capacity

27,000 bbls/d of condensate handling facilities

Backed by gas handling agreements, including take-or-pay

commitments and facility dedications

GAS PLANT EXPANSIONIncreased processing capacity by 150 mmcf/d

Project completed 3Q19

ACID GAS INJECTION & OTHER ENHANCEMENTSAcid gas injection is the most reliable and environmentally

responsible method to dispose of acid gas, virtually eliminating

emissions

Project became operational in July 2019

GROWTH OPPORTUNITIESAbility to connect to Keyera’s Wapiti gas plant

GRANDE

PRAIRIE

Pipestone

Simonette

Wapiti Pipeline

North Cabin

Pipeline

North

Wapiti

Pipeline

System

Wapiti

Capture Area

Producers active in

Wapiti Area:

• CNRL

• NuVista

• Paramount

• Pipestone Energy

• Seven Generations

• Shell

• Sinopec

37

Wapiti Gas Plant Complex – Phase I Operating

INFRASTRUCTURE INCLUDES300 mmcf/d of sour gas processing capacity

25,000 bbls/d of condensate handling capacity

30,000 bbls/d water disposal system

A raw gas gathering and field compression system

Acid gas injection, the most reliable and environmentally

responsible method to dispose of acid gas, virtually eliminating

emissions

PHASE I 150 mmcf/d - FULLY CONTRACTEDLong-term gas handling agreement with Paramount

Includes area of dedication and take-or-pay commitments

PHASE II TO BE COMPLETED MID-20201

Incremental 150 mmcf/d of sour gas processing capacity

Compressor and gas gathering system expansion

Long-term gas handling agreements with Pipestone Energy

Includes take-or-pay commitments

GROWTH OPPORTUNITIESAbility to connect to Keyera’s Simonette & Pipestone gas plants

1. Project timing subject to timely receipt of remaining regulatory approvals and construction schedule variables.

38

Pipestone Gas Plant – On Schedule & Fully Contracted

STRATEGIC PARTNERSHIP WITH OVINTIV

Major gas producer focused on developing the liquids-rich Montney;

contracted 85% of the available capacity

Keyera will own the facilities with the option to operate after five years of

plant start up

Expected to be completed in early 2021 at a cost of $600 million1

NEW INFRASTRUCTURE INCLUDES

200 mmcf/d of sour gas processing capacity

24,000 bbls/d of condensate processing facilities

Liquids hub with an additional 14,000 bbls/d of condensate processing

capacity (completed in 2018)

Acid gas injection, the most reliable and environmentally responsible

method to dispose of acid gas, virtually eliminating emissions

PHASE I 100% CONTRACTED & BACKED BY LONG-TERM AGREEMENTS

Includes an area dedication and revenue guarantee from Ovintiv

In May, 2019 new customer contracted available capacity with long-term

take-or-pay commitment

GROWTH OPPORTUNITIES

Ability to expand gas plant by 200 mmcf/d

Ability to connect to Keyera’s Wapiti gas plant

1. Project timing and cost subject to timely receipt of regulatory approvals, completing engineering & cost estimates, and construction schedule variables. Estimate excludes the cost of the Liquids Hub.

Source: Peters & Co.

Pipestone Liquids Hub & Plant

39

Wildhorse – Strategic Crude Oil & Blending Terminal

STRATEGIC CRUDE OIL STORAGE AND BLENDING TERMINAL1

Located at the major crude oil hub in the US

Backed by fee-for-service take-or-pay storage contracts ranging

from 2 - 6 years in length

Provides significant commercial opportunities by blending lower

value products into higher value product streams

Leverages Keyera’s liquids handling expertise

NEW INFRASTRUCTURE INCLUDES12 crude oil storage tanks with 4.5 million barrels of working

storage capacity under construction

Terminal will initially be pipeline connected to two existing storage

terminals in Cushing, OK

EXPECTED TO BE IN SERVICE IN 2H20, NET CAPITAL COST OF US$197 MILLION2

GROWTH OPPORTUNITIESComplemented by acquisition of Oklahoma Liquids Terminal, a

nearby logistics and diluent blending facility

Subject to customer demand, site allows for additional tanks

Cushing, OKUnparalleled connectivity

with 90 mmbls of storage

Wildhorse

Terminal1. 90/10 joint venture with an affiliate of Lama Energy Group.2. Cost and timing subject to construction and schedule variables.

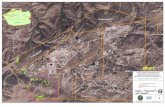

40

Positioned for Future Development

1,290undeveloped acres

in Alberta’s Industrial

Heartland

KFSJosephburg

Rail Terminal