Key Success Factors for a Mining Project in a Time of Market Volatility

31

March 20, 2012

-

Upload

mines-and-money -

Category

Business

-

view

741 -

download

0

Transcript of Key Success Factors for a Mining Project in a Time of Market Volatility

March 20, 2012

Our Cover Photos

Red Dog Mine, located in Alaska, is one of the world’s largest zinc mines. Zinc is an essential nutrient for brain development and growth in children. Tragically, up to one-third of the world’s population does not get enough zinc in their diets. That’s why Teck and the zinc industry are working with UNICEF on the Zinc Saves Kids program to provide zinc supplements to children in need in developing countries.

Bob Hamaguchi and W.E. Stanley cast their lines in quest of rainbow trout on Trojan Pond, a former tailings pond at our Highland Valley Copper mine. Trojan Pond is the site of an annual fly fishing tournament that raises funds for Royal InlandHospital in Kamloops, BC., and is a living example of a successful reclamation program.

Our Cover Photos

People like Gene Veilette, a haul truck driver at our Highland Valley Copper Mine, are Teck’s most important asset. We strive to create a company that is a special place to work for our employees, where a “safety first” approach permeates our culture.

This small frog can tell a big story. A frog living downstream from a mine is a sign of an ecologically sound, well-managed operation. It means we are doing our job, using environmentally sensitive techniques to extract the metals that all of us use in our everyday lives.

Both these slides and the accompanying oral presentation contain certain forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995 and forward-looking information within the meaning of the Securities Act (Ontario) and comparable legislation in other provinces.

Forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variation of such words and phrases or state that certain actions, events or results “may”, “could”, “should”, “would”, “might” or “will” be taken, occur or be achieved. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Teck to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. These forward-looking statements include statements relating to our future production, sales, earnings and cash flow, and our statements as to management’s expectations with respect to, among other things, business and financial prospects, the size and quality of Teck’s copper development projects and the timing of those projects, proposed expansions at existing operations, our production growth profile in copper, coal and oil, mine lives and mineral and oil and gas reserves and resources, progress in development of mineral and oil sands properties, future production, capital and mine production costs, demand and market outlook for commodities, future commodity prices and the financial results, cash flows and operations of Teck.

These forward-looking statements involve numerous assumptions, risks and uncertainties and actual results may vary materially. These statements are based on a number of assumptions, including, but not limited to, assumptions regarding general business andeconomic conditions, interest rates, the supply and demand for, inventories of, and the level and volatility of prices of coal, zinc, copper and gold and other primary metals and minerals produced by Teck as well as oil, natural gas and petroleum, the outcome ofengineering studies currently underway in connection with Teck’s development projects, the timing of receipt of regulatory and governmental approvals for Teck’s development projects and other operations, Teck’s costs of production and production and productivity levels, as well as those of its competitors, power prices, market competition, the accuracy of Teck’s reserve and resource estimates (including with respect to size, grade and recoverability) and the geological, operational and price assumptions on which these are based, the resolution of environmental and other proceedings, our ongoing relations with our employees and partners and joint venturers, the availability of financing for development projects and the future operational and financial performance of the company generally. The foregoing list of assumptions is not exhaustive.

Forward Looking Information

2

Events or circumstances could cause actual results to differ materially. Factors that may cause actual results to vary include, but are not limited to: unanticipated developments in business and economic conditions in the principal markets for Teck’s products or in the supply, demand, and prices for metals and other commodities to be produced, changes in power prices, changes in interest or currency exchange rates, inaccurate geological or metallurgical assumptions (including with respect to the size, grade and recoverability of mineral or oil and gas reserves and resources), changes in taxation laws or tax authority assessing practices, legal disputes or unanticipated outcomes of legal proceedings, unanticipated operational difficulties (including failure of plant, equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of materials and equipment, government action or delays in the receipt of permits or government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), decisions made by our partners or co-venturers, political risk, social unrest, lack of available financing for Teck or its partners or co-venturers, and changes in general economic conditions or conditions in the financial markets.

Certain of these risks are described in more detail in Teck’s annual information form available at www.sedar.com and in public filings with the SEC. Teck does not assume the obligation to revise or update these forward-looking statements after the date of this document or to revise them to reflect the occurrence of future unanticipated events, except as may be required under applicable securities laws.

Forward Looking Information

3

Ranking

Producer of metallurgical coal in N. America #1

Exporter of metallurgical coal in world #2

Zinc miner in world(1) Top 3

Copper growth potential over next 5-7 years 2x

Building a Leading Diversified Mining Company

Note 1: Brook Hunt, 2009

4

TECK RESOURCES–DIVERSIFIED PORTFOLIO

‘Stay the Course’ Strategy

LowLow--cost cost

Incremental GrowthIncremental GrowthCoalCoal

Building Building

ResourcesResourcesEnergyEnergy

Converting Resources to Cash Flow

Brownfield Brownfield

ExpansionExpansionCopperCopper

5

CAGR Trend ~20%*

CAGR Trend ~23%*

$ millions

TECK RESOURCES

Strong and Growing Cash Flow

*Note: cash flows before asset sales, tax deferrals etc.

Record Record

resultsresults

6

December 2011December 2011

Net Debt to Net Debt + Equity 13%

Debt / EBITDA 1.3x

EBITDA / Interest 11.3x

Strong Financial Position

Mid Triple-B Ratings from All Major AgenciesMid Triple-B Ratings from All Major Agencies

Weighted average term to maturity: 15.2 Years

Weighted average coupon rate: 6.0%

Overall Debt Maturity Profile

Year

($millions)

7

TECK RESOURCES

Growing Global Middle Class*

Source: OECD, Jan 2010

3 Billion increase by 2030• 700 million increase

1980 to 2009

• 3 billion increase 2010 to 2030

• Most resource intensive period of economic growth

*Daily per capita spending $10 to $100 in PPP terms

(million)

8

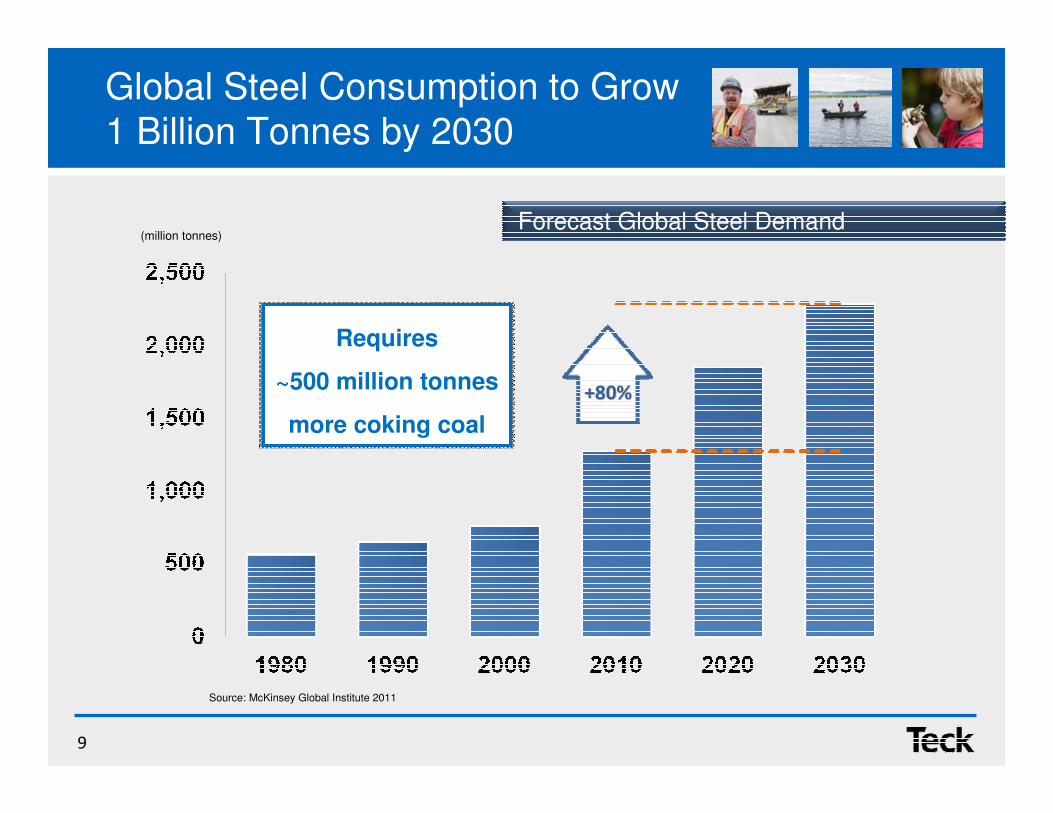

Global Steel Consumption to Grow 1 Billion Tonnes by 2030

+80%+80%

Source: McKinsey Global Institute 2011

Requires

~500 million tonnes

more coking coal

Forecast Global Steel Demand(million tonnes)

9

Neither: Managed Growth (at a lower trajectory)

GDP

FY: 9.2% Q4: 8.9%

GDPGDP

FY: 9.2% Q4: 8.9%FY: 9.2% Q4: 8.9%

Fixed Asset Investment

FY: 23.8%

Fixed Asset InvestmentFixed Asset Investment

FY: 23.8%FY: 23.8%

Retail Sales

FY: 17.1%

Retail SalesRetail Sales

FY: 17.1%FY: 17.1%

Industrial Production

FY: 13.9% Q4: 12.8%

Industrial ProductionIndustrial Production

FY: 13.9% Q4: 12.8%FY: 13.9% Q4: 12.8%

TECK RESOURCES

China: Hard Landing or Soft Landing?

10

Coal

Copper

Zinc

Energy

AGENDA

Delivering Results and Future Growth

11

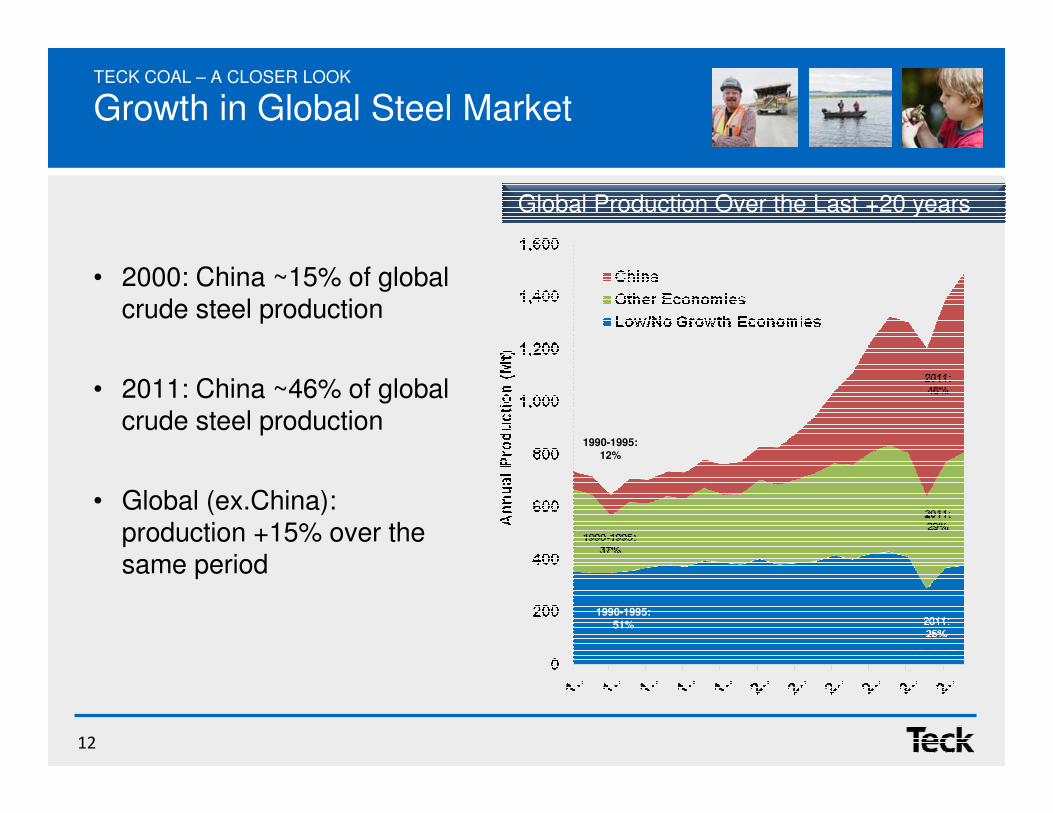

TECK COAL – A CLOSER LOOK

Growth in Global Steel Market

Source: WSA

Global Production Over the Last +20 years

• 2000: China ~15% of global crude steel production

• 2011: China ~46% of global crude steel production

• Global (ex.China): production +15% over the same period

1990-1995:51%

1990-1995:12%

12

TECK COAL – A CLOSER LOOK

China’s Changing Steel Industry

• 12th 5-year plan announced Nov 2011

• North east & central coastal regions: complete existing projects

• Central region: industry-wide upgrade and restructuring

• South-East Coast: New capacity in Guangdong (Zhanjiang), Guangxi (Fangcheng) and Fujian (Ningde)

CentralCentral

SouthSouth--East C

oast

East Coast

Domestic Steel Domestic Steel

ConsumptionConsumption

*Source: MIIT forecast

(Mt)

13

TECK COAL – A CLOSER LOOK

China’s Move Toward Larger Furnaces

Source: Wuhan Iron and Steel Corporation, Wuhan, China

Capacity byBlast Furnace Size

Mt

Measure 10001000mm33 30003000mm33 50005000mm33 Teck Teck HCCHCC

Ash (%) ≤≤≤≤13.0 ≤≤≤≤12.5 ≤≤≤≤12.0 <10

S (%) ≤≤≤≤0.7 ≤≤≤≤0.65 ≤≤≤≤0.6 <0.55

CSR (%) ≥≥≥≥58 ≥≥≥≥63 ≥≥≥≥66 70-74

Coke Quality Requirement by

Blast Furnace Size

14

• Production ‘12e vs. ‘11: +10%

• Increasing fleet size

• Modernizing plant

• Adding people

• Stabilizing strip ratio

TECK COAL – A CLOSER LOOK

Increasing Production from Existing Six Operations

Source: Teck Resources, 2012 guidance 24.5 to 25.5mt

Annual Coal ProductionMt

Targeting 28Mtpa 2013

15

• Trucks, shovels, drills have been ordered

• Permitting & stakeholder consultation proceeding

• Residential units acquired in Tumbler Ridge

• $340M capex for 2012

TECK COAL – A CLOSER LOOK

Quintette Re-start

Existing plant at Quintette

Targeting 3 Mtpa, 2013 start-up

16

Coal

Copper

Zinc

Energy

AGENDA

Delivering Results and Future Growth

17

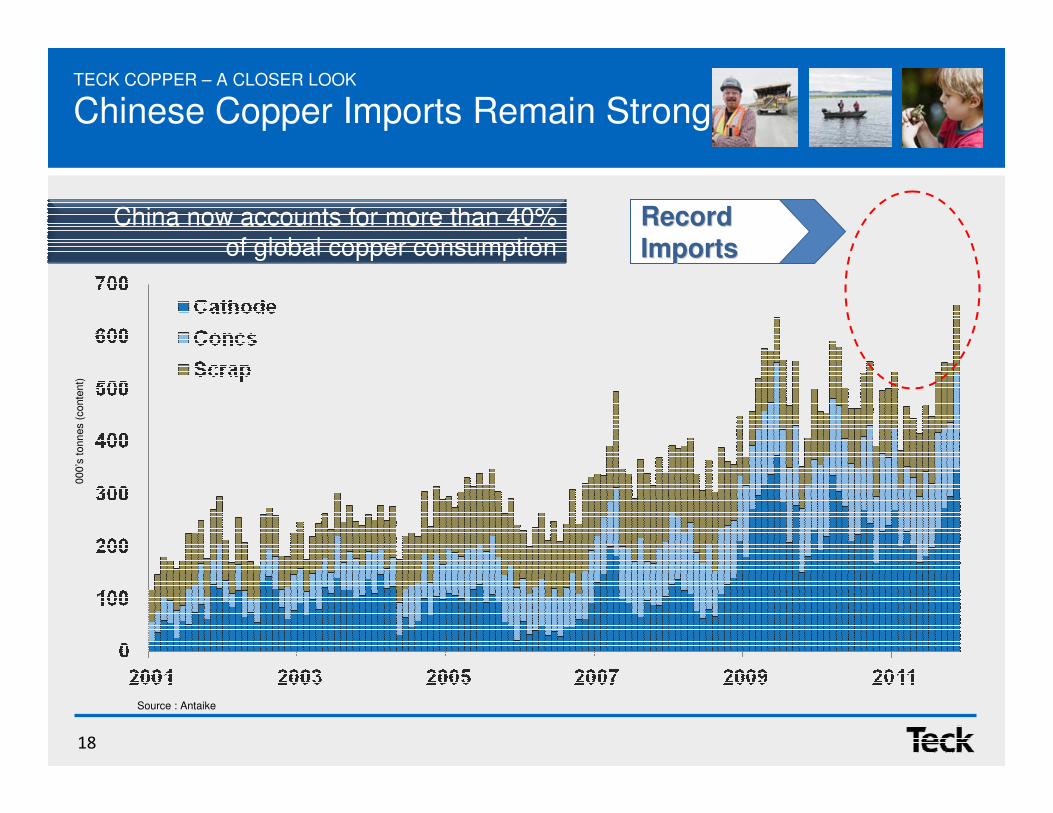

Source : Antaike

000’s

tonn

es (

conte

nt)

TECK COPPER – A CLOSER LOOK

Chinese Copper Imports Remain Strong

Record Record

ImportsImportsChina now accounts for more than 40%

of global copper consumption

18

TECK COPPER – A CLOSER LOOK

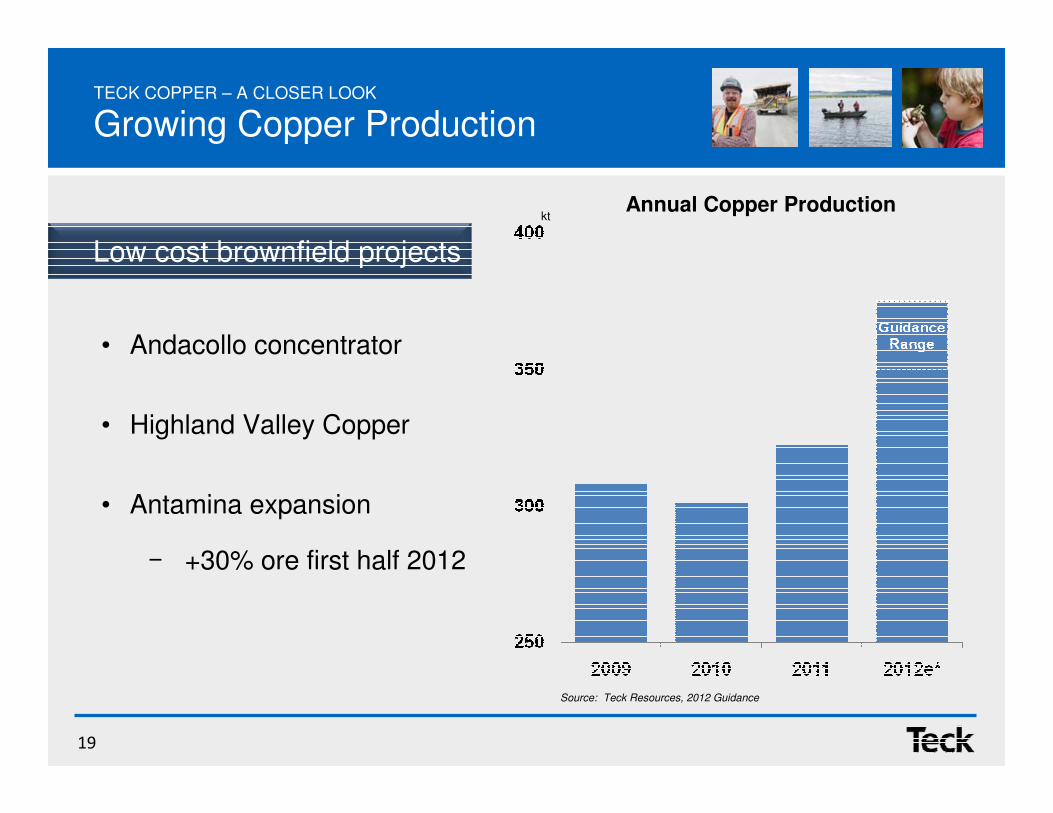

Growing Copper Production

Source: Teck Resources, 2012 Guidance

kt

• Andacollo concentrator

• Highland Valley Copper

• Antamina expansion

‒ +30% ore first half 2012

Low cost brownfield projects

Annual Copper Production

19

• Finalizing feasibility study

• Safe geo-political jurisdiction; low permitting risk

• Large resource: 200ktpa copper + 5ktpa molybdenum over 39 year mine life

• Low strip ratio

• No technology challenges – clean concentrate

• Recent concentrator construction experience (Andacollo)

TECK COPPER – A CLOSER LOOK

Quebrada Blanca Phase II200 kt Copper Production

South America

20

TECK COPPER – A CLOSER LOOK

Relincho Project (100% Teck)180kt Copper Production

• Central Chile, low altitude, access to infrastructure, and local workforce

• Pre-feasibility completed Q3 2011: US$3.9b capex, 180ktpa contained copper, 6ktpa contained moly, 22-yr mine life, cash costs ~US$1.30/lb

• 3.0Mt contained copper resource; upside potential

• Full feasibility expected Q1 2013

South America

21

Coal

Copper

Zinc

Energy

AGENDA

Delivering Results and Future Growth

22

Red Dog (100%)

• Exceptional zinc grades

• One of the largest zinc mines in the world

• 572,000 tonnes produced in 2011

• Outstanding exploration potential

Antamina (22.5%)

• Low cost, long life copper/zinc mine

• One of the world’s largest zinc producers – 53,000 tonnes produced in 2011

(Teck’s share)

• Expansion proceeding

Trail (100%)

• 1st quartile operating margin

• Fully integrated zinc and lead operations

• Captive hydro-electric power

TECK ZINC – A CLOSER LOOK

World Class Assets

Red Dog

23

Coal

Copper

Zinc

Energy

AGENDA

Delivering Results and Future Growth

24

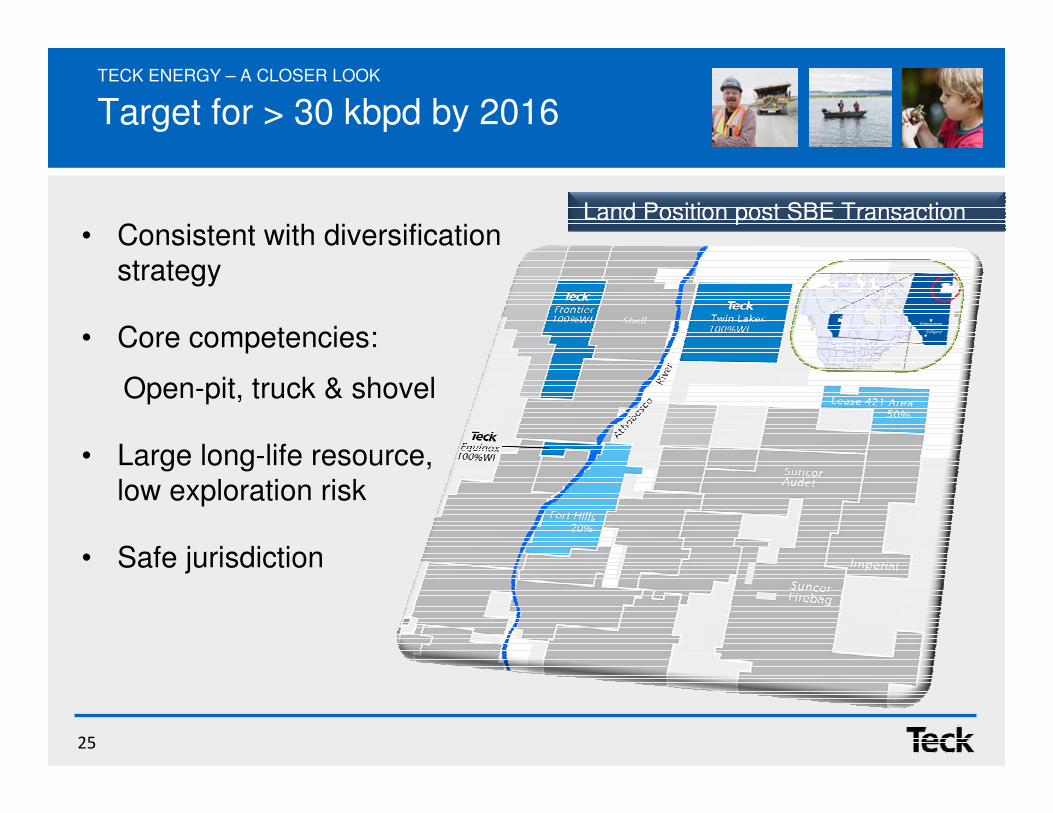

• Consistent with diversification strategy

• Core competencies:

Open-pit, truck & shovel

• Large long-life resource, low exploration risk

• Safe jurisdiction

TECK ENERGY – A CLOSER LOOK

Target for > 30 kbpd by 2016

Land Position post SBE Transaction

25

TECK ENERGY – A CLOSER LOOK

Growing our Resource Base

Contingent Bitumen Resource

billion bbls

Today:

•Teck’s share: ~2.1 billion barrels of bitumen resource

•20% interest in Fort Hills & 50% interest in Frontier/Equinox

Post-SBE transaction:

•100% interest in Frontier/Equinox

•Resources: over 3.5 billion bbls

•Lease 421 still to come

26

Source: Bloomberg, Teck estimates assuming Frontier at 50%, Lease 421 at 50%

Thousand B

arr

els

per

Day

TECK ENERGY – A CLOSER LOOK

Building a Substantial Energy Business

Teck’s Potential Oil Sands Production vs.Top 10 Canadian Oil Sands Producers (2010)

MarketCap:

$56bn $41bn $11bn $42bn

Market cap as at Feb 22, 2012

27

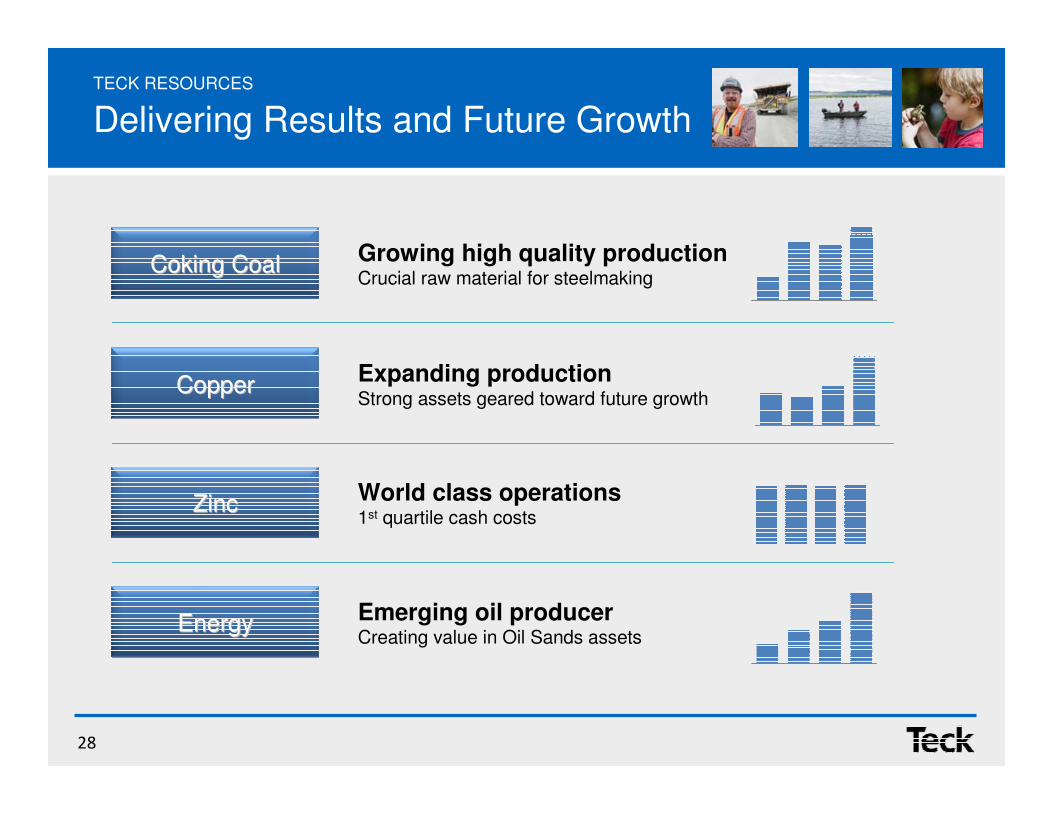

TECK RESOURCES

Delivering Results and Future Growth

Emerging oil producerCreating value in Oil Sands assets

EnergyEnergy

Growing high quality productionCrucial raw material for steelmaking

Coking CoalCoking Coal

Expanding production Strong assets geared toward future growth

CopperCopper

World class operations1st quartile cash costs

ZincZinc

28

March 20, 2012