KEY MILESTONES OF THE FIRST ISLAMIC BANK IN MALAYSIA · KEY MILESTONES OF THE FIRST ISLAMIC BANK IN...

68

KEY MILESTONES OF THE FIRST ISLAMIC BANK IN MALAYSIA Hizamuddin Jamalluddin 25 Sept 2014 Strictly Private & Confidential

Transcript of KEY MILESTONES OF THE FIRST ISLAMIC BANK IN MALAYSIA · KEY MILESTONES OF THE FIRST ISLAMIC BANK IN...

KEY MILESTONES OF THE FIRST ISLAMIC BANK IN MALAYSIA

Hizamuddin Jamalluddin25 Sept 2014

Strictly Private & Confidential

TABLE OF CONTENTS

Managing Director’s Office Page 2

Birth of Islamic Financial Institutions

History – Establishment of Bank Islam

Islamic Finance in Malaysia

Islamic Finance – Development Phase

Our Journey

Bank Islam Today

Key Financial Highlights

Conclusion – Evolution of Islamic Financial Landscape

Sec 1

Sec 2

Sec 3

Sec 4

Sec 5

Sec 6

Sec 7

Sec 8

ISLAMIC BANKS TODAY

Managing Director’s Office Page 3

“…the total global financial assets of the Islamic financial industry is now estimated to be more than US$2 trillion” – GIFF2014

BIRTH OF MODERN ISLAMIC FINANCE INSTITUTIONS

Managing Director’s Office Page 4

1963

1983

1975

1. Mit Ghamr Savings Bank – 19632. Perbadanan Wang Simpanan Bakal-

Bakal Haji (Now – Tabung Haji)– 19633. Nasser Social Bank -19724. Philippine Amanah Bank - 19735. Dubai Islamic Bank – 19756. Islamic Development Bank – 19757. Faisal Islamic Bank Sudan – 19778. Faisal Islamic Bank Egypt – 19779. Kuwait Finance House –197710. Bahrain Islamic Bank - 197911. Bank Islam Malaysia Berhad - 1983

1975

1977

1977

HISTORY - ESTABLISHMENT OF THE FIRST ISLAMIC BANK IN MALAYSIA Bumiputera Economic Congress 1980 - proposed the establishment of an Islamic bank for

the purpose of moving and investing funds of the Malays and Muslims based on the Shariah principles

“Seminar Kebangsaan Tentang Konsep Pembangunan Dalam Islam” (National Seminar on the Concept of Development in Islam) took place at Universiti Kebangsaan Malaysia in March 1981 had approved of a resolution asking the government to take urgent steps in drafting a banking act that operates based on Islamic principles

“Jawatankuasa Pemandu Kebangsaan Bank Islam” (National Steering Committee for Islamic Bank) was formed in September 1981 to conduct a research on the possibility of an Islamic Bank in Malaysia. The Steering Committee comprised of 14 members was chaired by Y.M Raja Tan Sri Mohar bin Raja Badiozzaman with Lembaga Urusan & Tabung Hajiappointed as its secretariat

On July 5, 1982, the Steering Committee proposed the establishment of an Islamic bank in Malaysia. The Parliament and the Senate approved the Islamic Bank Act at the end of 1982, which was then gazetted in 1983.

Bank Islam Malaysia Berhad was incorporated as a limited company on 1st March 1983. It began its operation four months later; on July 1, 1983 with its temporary headquarters at Tingkat 1, Kompleks Jemaah Haji, Jalan 5C/1A, Subang, Selangor with 30 pioneer staff

Managing Director’s Office Page 5

ISLAMIC FINANCE IN MALAYSIA

Managing Director’s Office Page 6

19831963 1984

The first Islamic financial institution

& Islamic fund management entity

in the region The pioneer

Islamic Commercial Bank

in Malaysia & South East Asia

The first Islamic Takaful operator in

the region

1997

Formed to replace Bank Islam as the first listed Islamic

financial institution in the Kuala Lumpur Stock Exchange

The first full-pledged Shariah-compliant stock

broking

1994

ISLAMIC FINANCE - DEVELOPMENT PHASE

Managing Director’s Office Page 7

Instituting Foundation •1970 – 1992 (Establishment of Enabling Infrastructure)• Islamic Banking Act 1983 – Establishment of Bank Islam Malaysia Berhad•Merely as an alternative to conventional banking

Institutional Building, Activity Generation & Market Vibrancy•1993-2005 (Deepening, Creating Critical Mass & Liberalisation)•Ensuring greater access to Islamic finance

Strategic Positioning & International Integration with Global Financial System. •2006 -2013•Becoming hub of international Islamic finance

Advancing in Islamic Financing – Well Developed Marketplace•2013 onwards • Islamic Financial Services Act 2013 - Robust Shariah Framework•Marketplace for Global Linkages

OUR JOURNEY – THE FIRST ISLAMIC BANK IN MALAYSIA

Managing Director’s Office Page 8

1983 1993

Stand-alone bank Focus on product and market development Creation of awareness – Customers' education Development of technical competencies (30 pioneer staff) Building key infrastructure – branch network Attract customers with strong conviction

10 years - Exclusivity

Key Challenges Limited capital for expansion Limited distribution channel & branches Absence on inter-bank money market Basic banking products Product differentiation Learning process

Instituting Foundation • Founding Shareholders – Ministry of Finance (RM30 mil), Lembaga Urusan & Tabung Haji (RM10 mil),

Pertubuhan Kebajikan Islam Malaysia – PERKIM (RM5 mil), Majlis-Majlis Agama Negeri (RM20 mil), Foundation of Religious Affairs (RM3 mil) and Federal Corporations (RM12 mil)

Initial paid up capital of

RM79.9 mil

Banking And Financial Institution Act 1989

OUR JOURNEY – REGULATORY ENVIRONMENT

Managing Director’s Office Page 9

19981983 1984 1993 1994 1997

Islamic Banking Scheme

December 1998

Government Investment Act

1983

Institution Act 1989

Interest Free Banking Scheme

1993

BNM National Shariah Advisory

Council May 1997

Islamic Banking Act 1983

Islamic Money Market 1994

Takaful Act 1984

Legal Redress Framework

Islamic Financial Service Act 2013

2013

The Central Bank of Malaysia Act

2009

2009

The Securities Commission

1993

OUR JOURNEY – MARKET DEVELOPMENT

Managing Director’s Office Page 10

1983 19991993 2004 2005

The Parliament and the Senate approved the

Islamic Bank Act (IBA) at the end of 1982, which was gazetted in 1983

(IBA) at the end of

Introduced interest-free

banking scheme on March 4, 1993

and Islamic banking window

banking scheme on March 4, 1993

Birth of second full fledged

Islamic bank, Bank Muamalat

Berhad

Establishment of Islamic banking

subsidiary

Entrance of foreign Islamic

banks

Issuance of international

Islamic banking license

2008 2010

Further liberalization –

entrance of foreign banks

OUR JOURNEY – CORPORATE DEVELOPMENT

Managing Director’s Office Page 11

2003July 1983 1992 1997 2000 20011995

Official commencement of Bank Islam’s

operation

1992 - The first Islamic

financial institution to be listed on

Bursa Malaysia

1997 - Launched its corporate website.

Transfer of listing status to BIMB

Holdings Berhad

Incorporated Bank Islam Labuan Ltd

2001 – Rated “A” by

Malaysia Rating

Corporation

2000-Received ISO

9001:2000 certification by

SIRIM for trade

financing and bills operation

1984 –Incorporated Al-WakalahNominees Sdn Bhd

1993 -Established

the first Islamic Unit Trust Company

2003 -Incorporated its offshore

trust company

1995 - Bank Islam Institute for Research & Training Sdn

Bhd, commenced its

operation.

1984 1993

The first Islamic

financial

1997 - Launched its

OUR JOURNEY – CORPORATE DEVELOPMENT…CONT

Managing Director’s Office Page 12

2003 2009

2007 –Embarked on corporate rebranding –“Banking for All” and branch remodeling

2003 -Launched its internet banking

2004 - First bank in Malaysia to offer SMS banking service (bankislam.sms)

2008 –Opened its first bureau de change at Low Cost Carrier Terminal (LCCT), KLIA

2009 – Sole Islamic bank and only commercial bank that was approved by the Securities Commission under its list of Principal Advisers

2010 –Acquired FarihanCorporation Sdn Bhd for Ar Rahnubusiness

2011 –Established Amana Bank Ltd, the first Islamic bank in Sri Lanka

2004 2007 2008 2010 20132010 2013

2004 - First bank

OUR JOURNEY – BRANCH EXPANSION

Managing Director’s Office Page 13

… commenced its first year of operations with 4 branches (Kuala Lumpur, Kuala Trengganu, Kota Baharu & Alor Setar), to-date Bank Islam has more than 130 branches nation-wide and targeted to expand to 150 branches by 2015.

Year No. of Branches

1983 4

1988 21

1993 32

1998 80

2003 84

2008 89

2013 133

Year No.

OUR JOURNEY – RETAIL MARKETPLACE

Managing Director’s Office Page 14

20121998

2003 – First bank to offer zakat payment via ATM & credit card

2003 2008 2009 2010

2008 –Launched the first Islamic structured and capital protected funds – An NajahNID-i.

First to introduce “Payment Holiday” feature in home financing

First to introduce “No Payment During Construction” feature for house financing

Introduced house financing based on floating rate

Launched Housing Credit Guarantee Scheme

2009 – First bank to join effort with LembagaTabung Haji in launching UnitellerService which enables TH transactions and Hajragistration to be performed at any Bank Islam branches

Launched Al-Awfar, the first of its kind account that offers cash prizes

2010 –Launched the first mobile banking service without internet access known as TAP Mobile Banking-i ,where account owners can perform banking transaction anywhere and anytime.

2012 – First bank to launch floating rates for personal financing

Launched the Bank’s first 7-Day Banking Services at shopping malls with full range of services

2013 – First implementation of low cost electric payment facility (mPOS)in collaboration with VISA Malaysia as part of its financial inclusion agenda

1998 – Collaborated with YayasanPembangunan EkonomiIslam to introduce its first Ar Rahnu business (Islamic Pawn-broking)

2013

1998 – Collaborated

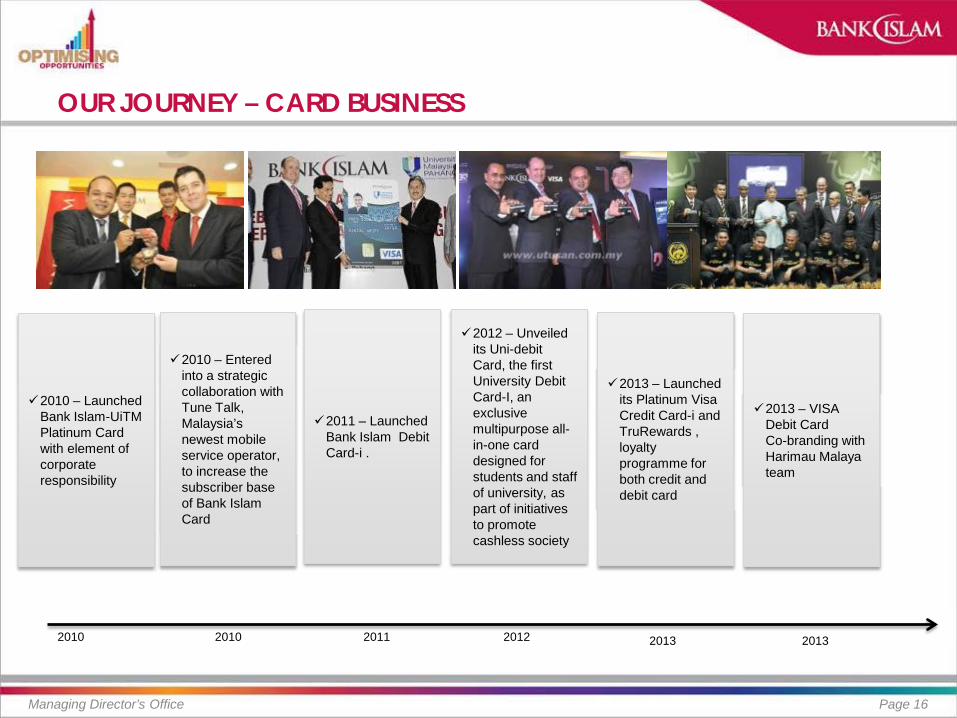

OUR JOURNEY – CARD BUSINESS

Managing Director’s Office Page 15

2009

1992 – First bank in Malaysia to introduce chip-based ATM

1992 – Introduced the first Islamic credit card

First card issuer to implement global clearing management system

1992 2002 2005 2006

2002 – First bank in Asia Pacific to introduce EMV2000 compliant credit cards with chip-based system following the launch of Bank Islam MasterCard

2005 - First card issuer and acquirer in Southeast Asia to implement MasterCard SecureCode

2006 – First bank in Southeast Asia to introduce an Islamic PatinumMasterCard

2009 – The first Islamic World MasterCard-iIssuer

2002 2003 – First Islamic Visa Smart chip Credit Card in Asia Pacific

2007 – Strategic partnership with MEPS and ArtaJasa of Indonesia to enables cossborder automated teller machines

2003 2007

OUR JOURNEY – CARD BUSINESS

Managing Director’s Office Page 16

20132010 2010 2011 2012 2013

2012 – Unveiled its Uni-debit Card, the first University Debit Card-I, an exclusive multipurpose all-in-one card designed for students and staff of university, as part of initiatives to promote cashless society

2013 – Launched its Platinum Visa Credit Card-i andTruRewards ,loyalty programme for both credit and debit card

2010 – Entered into a strategic collaboration with Tune Talk, Malaysia’s newest mobile service operator, to increase the subscriber base of Bank Islam Card

2011 – Launched Bank Islam Debit Card-i .

2010 – Launched Bank Islam-UiTMPlatinum Card with element of corporate responsibility

2013 – VISA Debit Card Co-branding with Harimau Malaya team

OUR JOURNEY – TREASURY SERVICES

Managing Director’s Office Page 17

2006 20132007

2006 –Introduced Wiqa’ Forward Rate, a Shariah-based financial hedging tool

2007 –Entered into the first Islamic cross currency swap agreement

2009 2010

2010 –Launched Waheed-I, the first Malaysian Ringgit fixed term deposit based on Wakalahcontract that meets international Shariahstandards

Signed a collaboration agreement with Barclays Capital Market for customization of Islamic hedging solution

2011

2009 –Appointed as a Principal Dealer by Bank Negara Malaysia

Transacted the first Islamic equity option.

Introduced Bulk Payment Foreign Exchange transaction

Launched ZiyadNID-i , a 5-year investment product in the form of Islamic Negotiable Instruments

2013 –Appointed as a Main Banker for the Government of Malaysia to facilitates payment of foreign telegraphic transfers to countries across the globe.

2011 –Enhanced the ForexTelegraphic Transfer which allow customers to remit more than 100 currencies globally

2012 –launched Islamic Dual Currency Investment-i ,using Wakalah-lil-Istithmar

2008 –Launched “Commodity Undertaking-i” , an Islamic option based product to be used for asset liability management purpose

2012

product to be

2007

used for asset liability management purpose

2008Launched “Commodity Undertakingan Islamic option based product to be product to be used for asset

OUR JOURNEY – SUKUK MARKETPLACE

Managing Director’s Office Page 18

1990 2003

1990 – LeadArranger for the world’s first bai’bithaman ajilIslamic debt securities by Shell MDS SdnBhd (RM125 mil)

2001 – LeadArranger for the world’s first global sukukbased on ijarahcontract by Kumpulan GutrieBerhad – First Global Sukuk Inc (USD150 mil)

2002 – Co-manager for the first sovereign sukuk ijarahby the Government of Malaysia (USD600 mil)

2003 – Joint Lead Arrangers for the first tradable sukukistisna’ by SKS Power Sdn Bhd (RM2.5 bil)

2001 2002 2013

OUR JOURNEY – CORPORATE FINANCE

Managing Director’s Office Page 19

2009 2011

2009 – Sole Islamic bank and only commercial bank that was approved by the Securities Commission under its list of Principal Advisers

2009 – The first Commercial Bank as Adviser for equity-linked transaction –YSP Southeast Asia Holdings Bhd

2011 – The first Islamic bank to advise al listing and initial public offering exercise, on the Main Board of Bursa Malaysia APFT Berhad,Malaysia’s leading flight education & training provider

OUR JOURNEY – IT INFRASTRUCTURE

Managing Director’s Office Page 20

20031983 July 2009 to June 2003 May 2010 June 2010 2012

2009-13 Upgraded Core Banking System

2009-10 Financing Collection System

2010 Risk Management System

20 12 Financing Origination System

20 12 Asset-Liability Management System

2014 New Internet Banking System

20 14 AMLA System

2009-13 Upgraded Core Banking System

Developed its Total Islamic Banking IT Platform

1997

Platform

OUR JOURNEY – RISK MANAGEMENT

Managing Director’s Office Page 21

OUR JOURNEY – RISK MANAGEMENT

MaximiseEarningsPotential

EarningsStability

ProtectionAgainstUnforeseenLosses

Increased Risk Management Sophistication

Risk Identification Risk Management/Assessment Risk Reporting Processes & Procedures RMS(datamart, credit risk, Basel II)

Loss Minimization/Risk Control Framework

Risk-based product pricing Linking risks and returns Measuring risk adjusted

performance Integration of market, credit

and operational risks RMS(market, operational)

Economic capital RAROC Bank-wide VaR Incremental VaR IRB Full compliance with Pillar 2

Prior to 2009 2010 2012

RAPM Framework

Active Portfolio ManagementFramework

Reactive

Active

Proactive

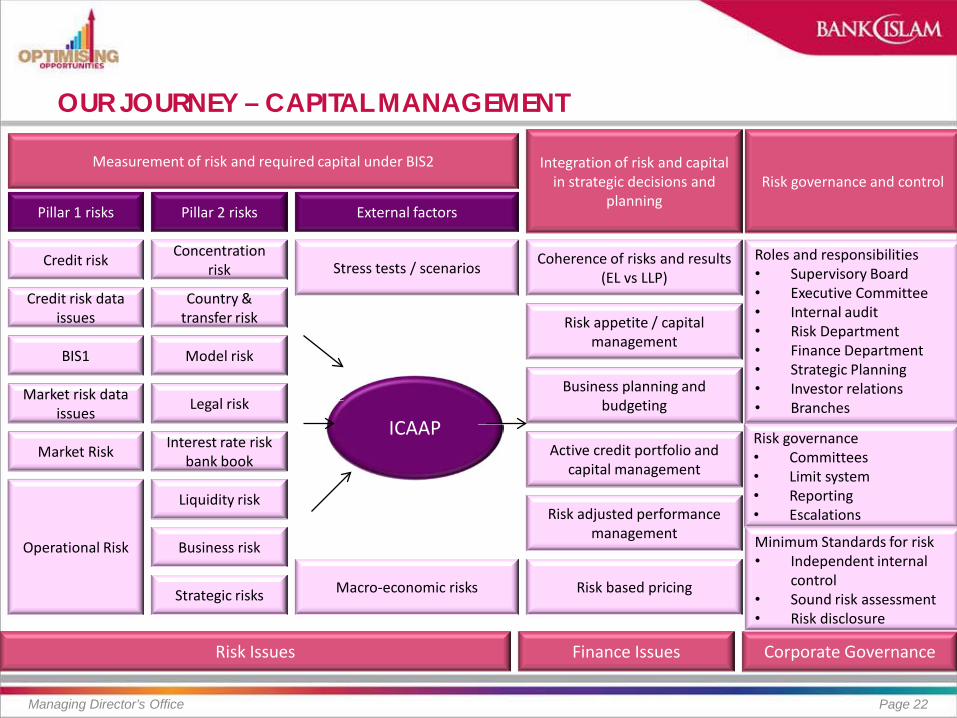

OUR JOURNEY – CAPITAL MANAGEMENT

Managing Director’s Office Page 22

Measurement of risk and required capital under BIS2 Integration of risk and capital in strategic decisions and

planningPillar 1 risks Pillar 2 risks External factors

Risk governance and control

Credit risk data issues

Market Risk

Market risk data issues

BIS1

Credit risk

Model risk

Legal risk

Interest rate risk bank book

Liquidity risk

Business risk

Strategic risks

Country & transfer risk

Concentration risk

Operational Risk

Stress tests / scenarios

Macro-economic risks Risk based pricing

Risk adjusted performance management

Active credit portfolio and capital management

Business planning and budgeting

Risk appetite / capital management

Coherence of risks and results (EL vs LLP)

Roles and responsibilities• Supervisory Board• Executive Committee• Internal audit• Risk Department• Finance Department• Strategic Planning• Investor relations• Branches

Risk governance• Committees• Limit system• Reporting• Escalations

Minimum Standards for risk• Independent internal

control• Sound risk assessment• Risk disclosure

Risk Issues Finance Issues Corporate Governance

ICAAP

OUR JOURNEY – INTERNAL AUDIT FRAMEWORK

Managing Director’s Office Page 23

Source : PwC

OUR JOURNEY - SHARIAH GOVERNANCE FRAMEWORK

Managing Director’s Office Page 24

1983 2004 20062000

Shariah Coordinator

20042000

Establishment of Shariah

Department(dedicated resources)

Establishment of Shariah Risk Management

Establishment of dedicated Shariah Audit Department

BNM introduced

Shariah Governance Framework

2010

ISLAMIC BANKING JOURNEY …CONT

Managing Director’s Office Page 25

1983 - 1990 1991 - 2000 2001 - 2005 2006 - 2008 2009 Onwards

Wadiah Current a/c Wadiah Savings a/c Mudharabah

Investment a/c Mudharabah

Financing Ijarah Financing BBA Financing Murabahah LC Musharakah LC Wakalah LC Bai’ Dayn Trade

Finance Murabahah

Working Capital Financing

Sarf Forex Mudharabah

Interbank Investment

MusharakahFinancing

Bai Inah Credit Card Ar Rahn

Bai Dayn, Musharakah , Mudharabah ICDO

Wadiah Debit Card Bai Inah Overdraft Bai Inah

Commercial Credit Card

Bai Inah Personal Financing

Bai Inah Negotiable Instrument of Deposit (NID)

Commodity Murabahah Profit Rate Swap

Commodity Murabahah Forward Rate Agreement

Ijarah Rental Swaps-I BBA Floating Rate Murabahah Floating

Rate Istisna’ Floating Rate Mudharabah Capital

Protected Structured Investment

Bai Inah Floating Rate NID

Mudharabah Savings Multiplier Deposit

Tawarruq Commodity Undertaking

Tawarruq Business Financing

Tawarruq Personal Financing

Murabahah with Novation Agreement

Istisna’ convertible to Ijarah

Bai and Ijarah (Sale & Lease Back)

Musharakah Mutanaqisah

Istisna’ with Parallel Istisna’

Wakalah Deposit Waqf Tawarruq Revolving

Credit-i Etc

Note – This listing is non exhaustive. Although they have been developed and/or approved,

some products have yet to be rolled out at the time this presentation was drafted.

Simple structure to cater for basic needsSimple structure to cater for basic needs Customer-driven structure/products Cost effective structure to compete in the competitive marketplace

OUR JOURNEY – ORGANIC GROWTHFinancial Performance

Managing Director’s Office Page 26

325.53 1,153.73 1,890.62 5,018.55

13,717.16

23,559.42

42,836.53

1984* 1988 1993 1998 2003 2008 2013^

Total Assets (RM'mil)

* Since date of incorporation 1 March 1983 to 30 June 1984 hence 16 months financial period. ^ Financial period of 12 months ending 31 December 2013.All financial years ended as of 30 June, with the exception of financial years 2010 onwards ending as at 31 December of respective financial years.

161.11 609.37 996.47 3,061.23

6,890.77 9,061.32

23,740.95

1984* 1988 1993 1998 2003 2008 2013^

Net financing (RM'mil)

(1.29)

6.19 26.85 11.53

130.33

308.27

683.02

1984* 1988 1993 1998 2003 2008 2013^

Profit Before Zakat & Taxation (RM'mil)

78.13 85.75 196.32

927.88 1,113.13 1,308.95

3,329.37

1984* 1988 1993 1998 2003 2008 2013^

Shareholders’ Funds (RM'mil)

OUR JOURNEY – BUILDING CAPABILITY

Managing Director’s Office Page 27

.

.

‘

Bank Islam Institute for Research & Training Sdn Bhd (BIRT)

OUR JOURNEY – ENABLING INSTITUTIONS

Managing Director’s Office Page 28

.

.

‘

BANK ISLAM TODAY

Originating Department Page 29

Malaysia’s 1st

Islamic bankIncorporated on 1 March 1983

>135 branchesnationwide with more than 1,200 self-service terminals

Universal licenceable to offer commercial and investment banking activities all under one roof

>4,000 staffTop 50 Malaysia’s Most Preferred Employers

Primarily a

retail bankwith more than 70% financing driven by Consumer banking

Voted

Islamic Bank of the Year by The Banker in 2013

UNIVERSAL LICENSE

Managing Director’s Office Page 30

CPORPORATE STRUCTURE AS AT MARCH 2014

Managing Director’s Office Page 31

54.4% 9.98%5.11% 5.05%

100%

14.4%

60.4%

GOVERNANCE STRUCTURE

Managing Director’s Office Page 32

BOARD OF DIRECTORS

Managing Director’s Office Page 33

SENIOR MANAGEMENT

Managing Director’s Office Page 34

VISION

Managing Director’s Office Page 35

Value-Based Organization

TO BE A GLOBAL LEADER IN ISLAMIC BANKING

“Global Leader” is defined as being the ultimate guidance and source of reference for innovative Shariah-based products and services

NEW BUILDING BLOCKS

Managing Director’s Office Page 36

TURNAROUND PLAN

SUSTAINABLE GROWTH

PLANOCT 2006 – JUNE 2009 JULY 2009 – DEC 2012

…in our pursuit to be a “Global Leader in Islamic Banking”

JAN 2013 – DEC 2015

TURNAROUND PLAN

Managing Director’s Office Page 37

Recapitalization & Balance Sheet Restructuring

Transformation Programme

IT Infrastructure

RevampCost

RationalizationHuman Capital Development

Recapitalization & Recapitalization & Recapitalization & Balance Sheet Balance Sheet Balance Sheet

SUSTAINABLE GROWTH PLAN

Managing Director’s Office Page 38

Business Innovation

Robust Risk Management

Strengthening Enabling

Infrastructure

Building Capability & Capacity

Franchise Develop-

ment

In-organic

Growth & Corporate Expansion

Management Infrastructure

Page 38

InIn

HIJRAH TO EXCELLENCE PLAN

Managing Director’s Office Page 39

Robust Organic Growth

Service Excellence

Shariah-led Innovation

Resource Optimisation

Employer of Choice

Regional-isation

KEY DRIVERS TO CUSTOMER SATISFACTION

Managing Director’s Office Page 40

People Basic Shariah knowledge, Ethics, Islamic values, Courtesy and etc

Place/Presentation Ambiance, Accessibility, Branding, Signage, Marketing etc

Product Value Proposition, Transparency, Innovative, Differentiation and etc

Process

Paper-work, waiting time, hassle free, etc

Price Value, Price Option

SERVICE DELIVERY/DISTRIBUTION CHANNELS

Managing Director’s Office Page 41

BRANCH NETWORKSBRANCH NETWORKSINTERNET BANKING

CONSUMER BANKING CENTERS

AR RAHNU OUTLETS

BUREAU DE CHANGESMS BANKING

CORPORATE DESKTOP BANKING

INTERNET BANKING

ELECTRONIC BANKING CENTERS

BRANCH NETWORKS

Managing Director’s Office Page 42

Perlis - 1

Kedah - 11

Kelantan - 13Pulau Pinang - 5

Perak - 9

Pahang - 9

Terengganu - 5

Selangor – 26Kuala Lumpur - 0

NegeriSembilan -7

Melaka - 4Johor - 15

Sarawak - 6

Sabah - 5Labuan- 1

Selangor Kuala Lumpur

Melaka

- 13

Terengganu 5

Region Total

Central 46

Northern 26

Eastern 27

Southern 26

East Malaysia 12

Total @ 31 Dec 2013 134

SELF SERVICE TERMINALS

Managing Director’s Office Page 43

ATM – 8 CDM – 4

CQM – 1 SP - 1

ATM – 36 CDM – 14

CQM – 7 SP -1

ATM – 30 CDM – 16

CQM – 7 SP -3

ATM – 2 CDM – 1

CQM – 1 SP - 1

ATM – 58 CDM – 27

CQM – 14 SP -4

ATM – 56 CDM –31

CQM – 11 SP - 4

ATM – 32 CDM – 13

CQM – 3 SP - 1

ATM – 39 CDM – 22

CQM – 7 SP - 2

ATM – 55 CDM – 20

CQM – 12 SP - 7

COIN - 1

ATM -158 CDM – 57

CQM – 28 SP - 10

ATM – 31 CDM – 14

CQM – 6 SP -2

ATM – 78 CDM - 36

CQM – 14 SP – 7

ATM – 33 CDM – 16

CQM – 6 SP - 4

ATM – Automated Teller MachineCDM – Cash Deposit MachineCQM – Cheque Deposit MachineSP – Statement PrinterCOIN – Coin Deposit Machine

ATM – 39 CDM – 17

CQM – 5 SP - 0

COIN - 1

ATM – 67 CDM – 36

CQM – 11 SP - 4

COIN - 1

Location type ATM CDM CQM SP Coin TotalBranches 291 211 116 43 3 664IPTA/IPTS 119 19 4 4 0 146Shopping Centres 92 9 1 2 0 104Corporate Offices 67 23 7 1 0 98TH Branches 40 29 0 0 0 69Petrol Stations 34 2 0 0 0 36Hospitals 21 0 1 0 0 22Mosques 15 10 0 0 0 25Others 43 21 4 1 0 69Total 722 324 133 51 3 1,233

AR RAHNU OUTLETS

Managing Director’s Office Page 44

Kota Bharu Outlet

Pasir Puteh Outlet

Pasir Mas Outlet

Tanah Merah Outlet

No. Location State Day 11 Kota Bahru KLN 10 Jun 20102 Pasir Puteh KLN 15 Jul 20103 Pasir Mas KLN 29 Jul 20114 Tanah Merah KLN 28 Jun 20125 Kubang Kerian KLN 11 Jul 20136 Kuantan PHG 24 Aug 20137 Sungai Petani KDH 10 Jun 20138 Kuala Treengganu TGN 21 Aug 20139 Alor Setar KDH

Kubang Kerian Outlet

BUREAU DE CHANGE

Managing Director’s Office Page 45

Kota Kinabalu International Airport

Contact Pier, Kuala Lumpur International Airport

Gateway @ KLIA 2

BUREAU DE CHANGE

Penang International Airport*

Bukit Bintang BDC

KL Sentral . Location State Day 1 1 Contact Pier International,

KLIASGR 01 Oct 2010

2 Bukit Bintang KL 03 Dec 2010

3 Kota Kinabalu International Airport SBH 26 Jul 2012

4 Penang International Airport PNG 1 Feb 2013

5 KL Sentral KL 13 Sept 2013

6 Setiawalk, Pusat Bandar Puchong SEL 21 Nov 2013

7 Swiss Inn, Jalan Sultan KL 22 April 2014

8 Taman Sri Muda, Shah Alam SEL 12 May 2014

9 Gateway@KLIA 2 SEL 26 May 2014

BUSINESS INNOVATION

Managing Director’s Office Page 46

2009 2010 2011 2012 2013 2009 2010 2011 2012 2013 2009 2010 2011 2012 2013

ACHIEVEMENTS

Managing Director’s Office Page 47

2010 2011 2012 2013

FINANCIAL HIGHLIGHTS

Managing Director’s Office Page 48

^ Annualised # Bank Negara Malaysia Monthly Statistical Bulletin @ June 2014* Bank Negara Malaysia Annual Report 2013 1 Include foreign individuals

Key Indicators ActualJune 14

FYEDec 13

Islamic BankingSystem

BankingSystem

Return on equity (%) - PBT 19.0% ^ 21.2% 17.3% * 15.9% *

Return on equity (%) - PAT 13.7% ^ 15.3% NA NA

Return on assets (%) - PBT 1.6% ^ 1.7% 1.2% * 1.5% *

Return on assets (%) - PAT 1.1% ^ 1.2% NA NA

Non-fund based income (%) 12.0% 12.6% 8.1% * 19.2% *

Gross impaired financing (%) 1.1% 1.2% 1.3% # 1.8% #

Net impaired financing (%)

(Less IA) 0.6% 0.6% 1.0% # 1.3% #

(Less IA & CA) -0.9% -0.9% -0.3% # -0.1% #

CASA growth (RM billion) -RM0.7 billion RM1.1 billion RM4.0 billion # RM3.7 billion #

Individual deposits growth (RM billion) RM0.3 billion -RM0.0 billion RM6.1 billion # RM20.6 billion #

Individual Deposits1 to Total Deposits (%) 14.6% 14.1% 18.9% # 36.4 % #

FINANCIAL HIGHLIGHTS…CONT

Managing Director’s Office Page 49

Key Indicators ActualJune 14

FYEDec 13

Islamic BankingSystem

BankingSystem

PROFITABILITY

Cost Income Ratio (%) 52.5% 54.1% 47.4% * 45.6% *

EFFICIENCY

Financing to Deposits (%) 70.2% 65.0% 83.1% # 81.9% #

CASA to Total Deposits (%) 36.4% 39.1% 25.7% # 26.3% #

ASSET QUALITY

Financing Loss Coverage Ratio (%) 179.5% 175.8% 126.6% # 104.4% #

CAPITALISATION

RWCR (%) 13.8% 14.0% 15.7% # 14.8% #

PRODUCTIVITY

Profit before tax over average employee (RM‘000) 159.3 ^ 163.9 164.2 *+ 235.5 *

Profit before allowance for impairment over average employee (RM‘000) 174.6 ^ 161.2 176.5 *+ 254.4 *

Personnel cost per employee (RM‘000) 106.6 ^ 103.2 57.3 *+ 107.5 *

Assets per employee (RM’000) 10,110.4 10,072.1 14,285.7 *+ 16,192.0 *

Gross financing per employee (RM’000) 6,312.6 5,700.1 9,356.2 *+ 9,712.3 *

Deposits per employee (RM’000) 8,987.9 8,763.8 11,497.6 *+ 12,103.2 *^ Annualised* Bank Negara Malaysia Annual Report 2013+ Number of employees is estimated based on the percentage of institution’s Islamic assets# Bank Negara Malaysia Monthly Statistical Bulletin @ June 2014

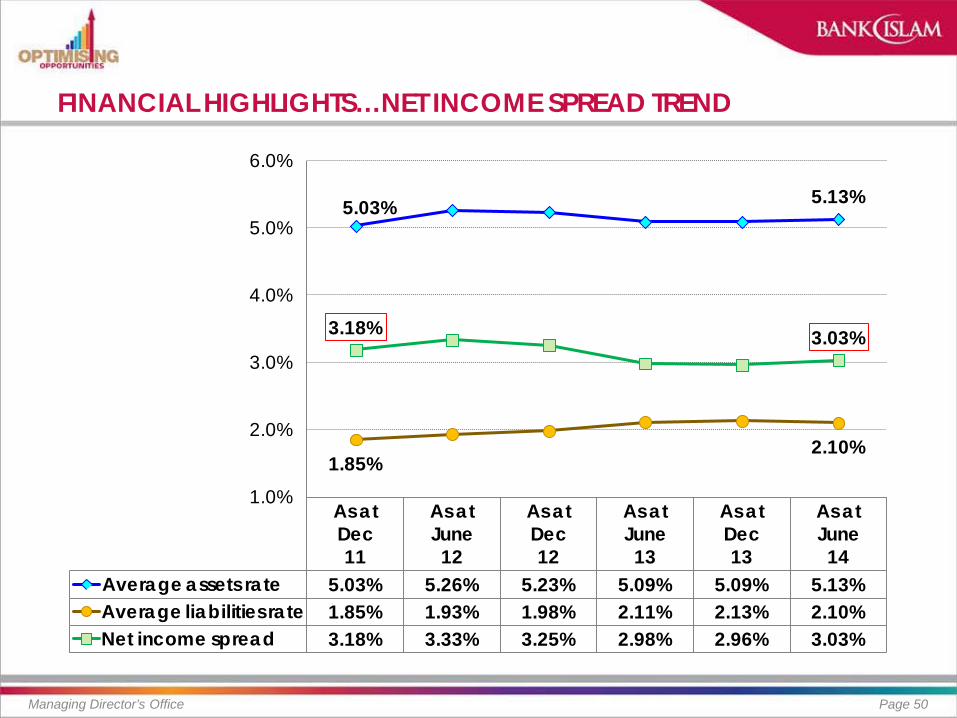

FINANCIAL HIGHLIGHTS…NET INCOME SPREAD TREND

Managing Director’s Office Page 50

As at Dec 11

As at June 12

As at Dec 12

As at June 13

As at Dec 13

As at June 14

Average assets rate 5.03% 5.26% 5.23% 5.09% 5.09% 5.13%Average liabilities rate 1.85% 1.93% 1.98% 2.11% 2.13% 2.10%Net income spread 3.18% 3.33% 3.25% 2.98% 2.96% 3.03%

5.03% 5.13%

1.85%2.10%

3.18% 3.03%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

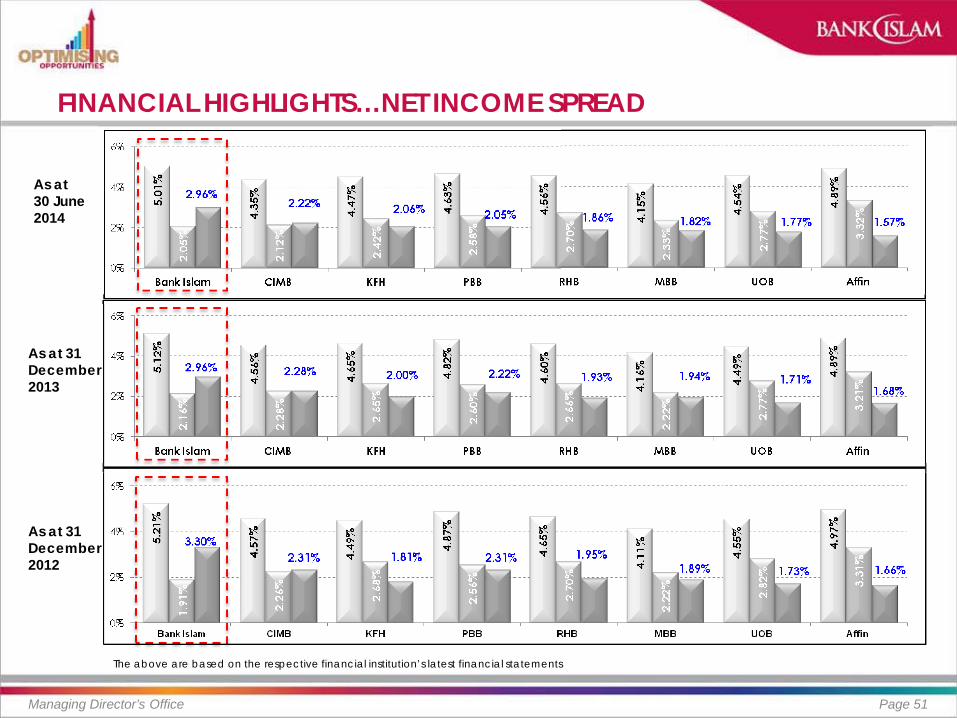

FINANCIAL HIGHLIGHTS…NET INCOME SPREAD

Managing Director’s Office Page 51

As at 31 December 2012

As at 31 December2013

As at 30 June2014

The above are based on the respective financial institution’s latest financial statements

FINANCIAL HIGHLIGHTS - MARKET SHARE OF TOTAL ASSETS

Managing Director’s Office Page 52

RM BillionBanking System^

Selected Banking Group #

Total assets 2,125.2 42.9 583.9 323.7 315.7 116.7

6 monthsgrowth 66.9 0.1 23.5 17.9 12.3 (4.4)

% growth 3.3% 0.2% 4.2% 5.9% 4.1% -3.6%

Marketshare

June 14 2.0% 27.5% 15.2% 14.9% 5.5%

Dec 13 2.1% 27.2% 14.9% 14.7% 5.9%

RM Billion

Islamic Banking System^

Selected Islamic Banks #

Total assets 453.0 42.9 132.3 49.5 36.8 33.4

6 monthsgrowth 19.5 0.1 7.3 0.0 2.3 0.4

% growth 4.5% 0.2% 5.8% 0.1% 6.6% 1.1%

Marketshare

June 14 9.5% 29.2% 10.9% 8.1% 7.4%

Dec 13 9.9% 28.8% 11.4% 8.0% 7.6%

MBB27.5%

PBB15.2%

CIMB 14.9%

AmBank5.5%

Bank Islam2.0%

Others34.9%

Banking System

MBB-i29.2%

CIMB-i10.9%Bank

Islam9.5%

PBB-i8.1%

AmIslamic7.4%

Others34.9%

Islamic Banking System

^ based on Bank Negara Malaysia Monthly Statistical Bulletin @ June 2014# based on latest available financial statements of respective banks

FINANCIAL HIGHLIGHTS - FINANCING GROWTH

Managing Director’s Office Page 53

Growth↑ 10.6%

Growth↑ 22.9%

FINANCIAL HIGHLIGHTS – MARKET SHARE OF FINANCING ASSETS

Managing Director’s Office Page 54

MBB29.5%

PBB18.4%

CIMB 15.1%

AmBank6.8%

Bank Islam2.1%

Others28.1%

Banking System

MBB-i31.5%

CIMB-i11.4%Bank

Islam8.8%

AmIslamic8.1%

PBB-i8.0%

Others32.2%

Islamic Banking System

RM BillionBanking System^

Selected Banking Group #

Net financing 1,249.5 26.3 368.3 230.4 189.3 84.4

6 monthsgrowth 46.8 2.5 12.7 11.0 3.8 0.9

% growth 3.9% 10.6% 3.6% 5.0% 2.1% 1.1%

Marketshare

June 14 2.1% 29.5% 18.4% 15.1% 6.8%

Dec 13 2.0% 29.6% 18.2% 15.4% 6.9%

RM Billion

Islamic Banking System^

Selected Islamic Banks #

Net financing 298.5 26.3 94.0 34.1 24.2 24.0

6 monthsgrowth 20.6 2.5 7.9 (1.0) 1.0 1.1

% growth 7.4% 10.6% 9.1% -2.9% 4.4% 4.8%

Marketshare

June 14 8.8% 31.5% 11.4% 8.1% 8.0%

Dec 13 8.5% 31.0% 12.6% 8.3% 8.2%

^ based on Bank Negara Malaysia Monthly Statistical Bulletin @ June 2014# based on latest available financial statements of respective banks

FINANCIAL HIGHLIGHTS – CUSTOMER DEPOSITS

Managing Director’s Office Page 55

Financing toDeposits % 51.5% 61.2% 62.7% 65.0% 70.2%

IndividualDeposits* to Total Deposits %

16.8% 16.2% 14.6% 14.1% 14.6%

Growth↑ 2.4%

Growth↑ 9.5%

FINANCIAL HIGHLIGHTS – MARKET SHARE OF DEPOSITS

Managing Director’s Office Page 56

RM BillionBanking System^

Selected Banking Group #

Deposits 1,554.3 38.2 406.5 264.5 225.2 87.6

6 monthsgrowth 41.5 0.9 10.9 13.7 5.0 (0.5)

% growth 2.7% 2.4% 2.8% 5.4% 2.3% -0.5%

Marketshare

June 14 2.5% 26.2% 17.0% 14.5% 5.6%

Dec 13 2.5% 26.2% 16.6% 14.6% 5.8%

RM Billion

Islamic Banking System^

Selected Islamic Banks #

Deposits 366.4 38.2 92.0 40.1 29.4 25.2

6 monthsgrowth 17.5 0.9 9.0 1.6 1.0 2.5

% growth 5.0% 2.4% 10.9% 4.2% 3.6% 11.1%

Marketshare

June 14 10.4% 25.1% 10.9% 8.0% 6.9%

Dec 13 10.7% 23.8% 11.0% 8.1% 6.5%

Selected Islamic Banks #

MBB26.2%

PBB17.0%

CIMB 14.5%AmBank

5.6%

Bank Islam2.5%

Others34.2%

Banking System

MBB-i25.1%

CIMB-i10.9%Bank

Islam10.4%

PBB-i8.0%

AmIslamic6.9%

Others38.7%

Islamic Banking System

^ based on Bank Negara Malaysia Monthly Statistical Bulletin @ June 2014# based on latest available financial statements of respective banks

FINANCIAL HIGHLIGHT-LOWER COST OF FUNDING

Managing Director’s Office Page 57

FINANCIAL HIGHLIGHTS – MARKET SHARE OF CASA

Managing Director’s Office Page 58

RM BillionBanking System^

Selected Banking Group #

CASA 408.4 13.9 145.2 73.1 66.7 19.2

6 monthsgrowth 3.7 (0.7) 2.5 1.6 2.6 1.5

% growth 0.9% -4.5% 1.7% 2.2% 4.1% 8.5%

% to Total Deposit 26.3% 36.4% 35.7 % 32.5% 25.2% 21.9%

Marketshare

June 14 3.4% 35.6% 17.9% 16.3% 4.7%Dec 13 3.6% 35.3% 17.7% 15.8% 4.4%

RM Billion

Islamic Banking System^

Selected Islamic Banks #

CASA 94.3 13.9 29.5 10.4 8.2 6.1

6 monthsgrowth 4.0 (0.7) 2.6 0.4 0.3 0.8

% growth 4.4% -4.5% 9.6% 3.6% 3.2% 15.6%

% to Total Deposit 25.7% 36.4% 32.0% 25.8% 27.8% 24.3%

Marketshare

June 14 14.7% 31.3% 11.0% 8.7% 6.5%Dec 13 16.1% 29.8% 11.1% 8.8% 5.8%

Selected Islamic Banks #

MBB35.5%

CIMB 17.9%

PBB16.3%

AmBank4.7%

Bank Islam3.4%

Others22.2%

Banking System

MBB-i31.3%

Bank Islam14.7%CIMB-i

11.0%

PBB-i8.7%

AmIslamic6.5%

Others27.8%

Islamic Banking System

^ based on Bank Negara Malaysia Monthly Statistical Bulletin @ June 2014# based on latest available financial statements of respective banks

FINANCIAL HIGHLIGHTS – CREDIT QUALITY TRENDS

Managing Director’s Office Page 59

FINANCIAL HIGHLIGHTS – ASSET QUALITY

Managing Director’s Office Page 60

of which Gross Impaired Financing (GIF) by Business Units:by Business Units:

FINANCIAL HIGHLIGHTS – CAPITAL ADEQUACY

Managing Director’s Office Page 61

RM million Dec 11 Dec 12 Dec 13 June 14

Total Risk-Weighted Assets 16,863 22,466 25,449 27,488

CONCLUSION - EVOLUTION OF ISLAMIC FINANCIAL LANDSCAPE

Managing Director’s Office Page 62

Banking Comprehensive Financial System

Monopoly Diversity of Players

Windows Full-Fledged Islamic Banks

Alternative Banking & Specific Agenda National Agenda

Traditional Markets Non-Traditional Market

… changing financial landscape has accelerated expansion of Islamic finance industry

EVOLUTION OF ISLAMIC FINANCIAL LANDSCAPE …CONT

Managing Director’s Office Page 63

Basic Shariah Principles(i.e. BBA & Murabaha)

Variety of Shariah Principles(i.e. Ijarah, Ujrah, Istisna’ etc)

Basic Infrastructure Comprehensive Infrastructure

Limited Tax Neutrality Universal Tax Neutrality

“Plain Vanilla” Products Hybrid & Structured Products

(Investment Accounts)

Domestic/Local Players Cross-Border /Regional/Global Players

… wide spectrum of financial products and services to cater the needs of all customers from small businesses to conglomerates, from common households to high net-worth individuals

EVOLUTION OF ISLAMIC FINANCIAL LANDSCAPE …CONT

Managing Director’s Office Page 64

… accompanied by development of ancillary support services

Commercial Islamic Banks Mega Islamic Banks

Shariah Compliant Products Shariah Based Products

… increased focus on financial stability(…strengthened prudential standards focusing on building capital and capital buffers, increased

transparency in financial transactions and exposures)

… evolves to become more diversified and more comprehensive to meet the changing requirements of the real economy & international connectivity (cross-border transaction)

Financial Intermediary Financial & Investment Intermediary

EVOLUTION OF ISLAMIC FINANCIAL LANDSCAPE …CONT

Acts as both, financial intermediary and investment intermediary

Managing Director’s Office Page 65

InvestorsBank As Agent (Wakalah); or As Entrepreneur (Mudarabah); or As Business Partner (Musharakah)

Venture

1st Leg 2nd Leg

Contract under IA : Wakalah Mudarabah Musharakah

Contract between Bank and business owner Equity financing

(Musharakah, Mudarabah) Lease-based financing

(Ijarah) Sale-based (Murabahah,

Istisna’, Inah) Fee based (Wakalah ,

Ujra’)) Guarantee (Kafalah)

Principal non-guaranteed Shariah contracts

INVESTMENT ACCOUNT(Assets ring-fenced to meet

liabilities-account upon winding up)

EVOLUTION OF ISLAMIC FINANCIAL LANDSCAPE …CONT

Moving Forward - Balance Sheet Structure

Managing Director’s Office Page 66

Liabilities

Demand Deposits(Qard / Wadiah Yad Dhamanah)

Term Deposits (Tawarruq)

Investment Accounts (Mudharabah/Wakalah/Musharakah)

Shareholders’ Funds

Capital Instruments (Tier I/II Sukuk)

Assets

Financing Assets (Debt-based : i.e. MPO, IMBT, Istisna’ Parallel Istisna’, InahEquity –based : Mudharabah,

Musharakah, MM)

Treasury Assets (Cash, Sukuk, Money Market)

Ijarah Assets (Operating lease)

Investments (Subsidiary or Associates)

Inventory

Non-Financial Assets

Demand DepositsQard / Wadiah

Term Deposits

Excluded from calculation of

Statutory Reserve Requirement

Assets

Zero capital charge for assets tagged

to investment account

FLAGBEARER OF ISLAMIC BANK

Managing Director’s Office Page 67

Source : Annual Report Bank Islam

Managing Director’s Office Page 68