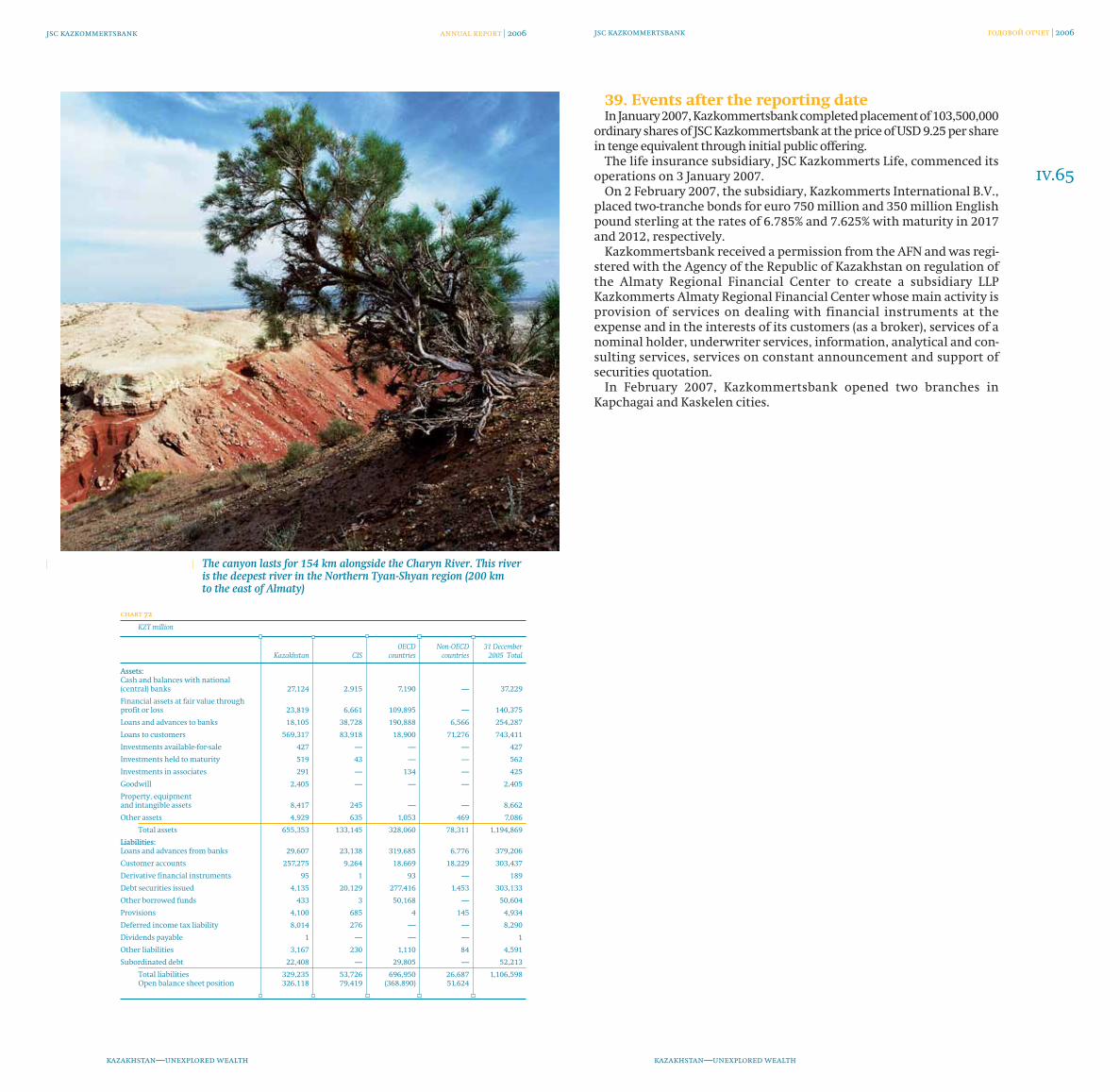

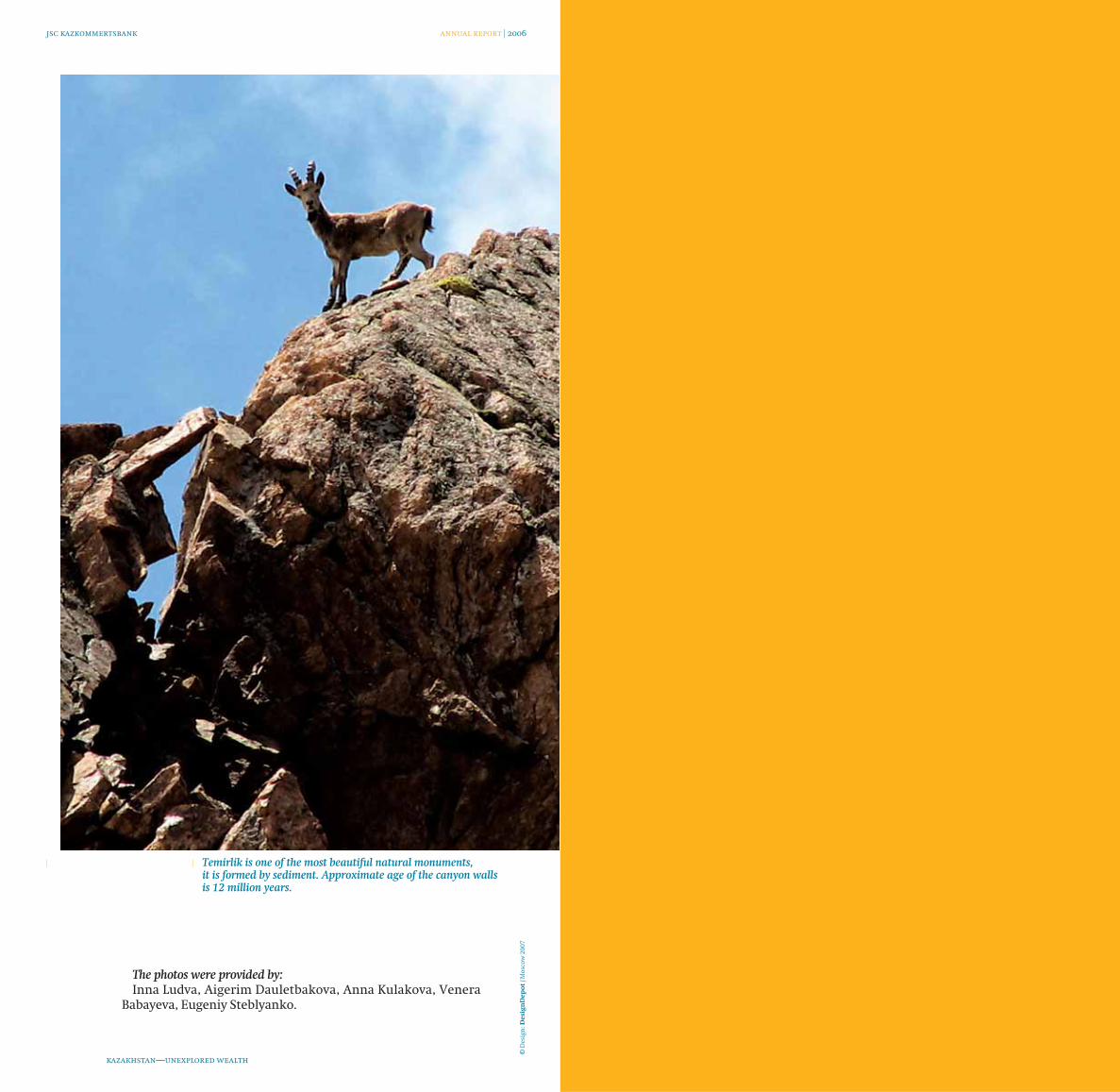

Kazakhstan– unexplored Wealth -...

69

KAZKOMMERTSBANK Kazakhstan– unexplored Wealth 2006 annual report

Transcript of Kazakhstan– unexplored Wealth -...

KAZKOMMERTSBANK

Kazakhstan–unexploredWealth

2006

annual report

Tyan-ShanfoothillsLatitude 54-12-38

North

Ongitude 112-61-22

East

part iii

Social Report

FinancialStatements

Singingsand-dunesLatitude 54-12-38

North

Ongitude 112-61-22

East

part ii

part iv

Results of the year

TimerlikcanyonLatitude 54-12-38

North

Ongitude 112-61-22

East

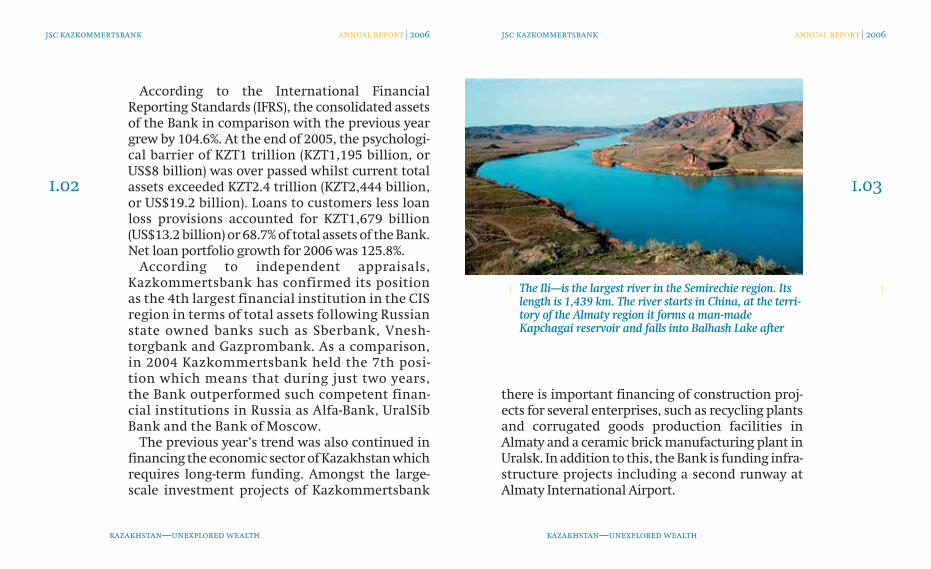

Ili river

Opening address of the Chairperson of the Board

Latitude 54-12-38

North

Ongitude 112-61-22

East

part i

annual report

2006

kazkommertsbank

contents

Opening Address of the Chairman of the Board

Results of the Year

Social Report

Financial Statements

I

II

III

IV

OpeningAddress of the Chairman of the Board

part i

Ili River Latitude 54-12-38

North

Longitude 112-61-22

East

Dear Sha rehol ders,Inves tors, Part ners and Cli ents!

The financial results for 2006 pro ve thatthe year has been of a remarkable success forKazkommertsbank. Recently, the Bank hasdemon stra ted stab le growth by strengthe ning itslea dership posi tion amongst the banks of theRepublic of Kazakhstan in terms of total assets,loan port fo lio and pro fits. Moreover for the firsttime the Bank beca me a lea der in terms of totaldepo sits as at the end of 2006.

The suc cess of the Bank’s finan cial year did nothap pen by chan ce, having alre a dy been fore cast assuch and dog ged ly imple men ted through theefforts of the Bank’s highly pro fes sio nal team.During the year, the acti vi ti es of the Bank weremar ked by a num ber of events which pro ved to bevery effec ti ve with ste a dy growth having beenachi e ved in three key seg ments—reta il ban king,small and medi um-sized busi nes ses and cor po ra teban king. These sec tors made a sig ni fi cant con tri -bu tion to the Bank’s suc cess.

i.01

jsc kazkommertsbank

kazakhstan—unexplored wealth

annual report | 2006

Nina ZhussupovaChairman

of the Board

According to the International FinancialReporting Standards (IFRS), the con so li da ted assetsof the Bank in com pa ri son with the pre vio us yeargrew by 104.6%. At the end of 2005, the psycho lo gi -cal bar ri er of KZT1 tril lion (KZT1,195 bil lion, orUS$8 bil lion) was over pas sed whilst cur rent totalassets exce e ded KZT2.4 tril lion (KZT2,444 bil lion,or US$19.2 bil lion). Loans to cus to mers less loanloss pro vi sions accoun ted for KZT1,679 bil lion(US$13.2 bil lion) or 68.7% of total assets of the Bank.Net loan port fo lio growth for 2006 was 125.8%.

According to independent appraisals,Kazkommertsbank has confirmed its positionas the 4th largest financial institution in the CISregion in terms of total assets fol lowing Russianstate owned banks such as Sberbank, Vnesh-torgbank and Gazprombank. As a com pa ri son,in 2004 Kazkommertsbank held the 7th posi -tion which means that during just two years,the Bank out per for med such com pe tent finan -cial insti tu tions in Russia as Alfa-Bank, UralSibBank and the Bank of Moscow.

The pre vio us year’s trend was also con ti nu ed infinan cing the eco no mic sec tor of Kazakhstan whichrequi res long-term fun ding. Amongst the large-scale invest ment proj ects of Kazkommertsbank

there is impor tant finan cing of con struc tion proj -ects for seve ral enter pris es, such as recy cling plantsand cor ru ga ted goods pro duc tion faci lit ies inAlmaty and a cera mic brick manu fac tu ring plant inUralsk. In addit ion to this, the Bank is fun ding infra -struc tu re proj ects inc lu ding a second runway atAlmaty International Air port.

i.03

jsc kazkommertsbank

The Ili—is the largest river in the Semirechie region. Itslength is 1,439 km. The river starts in China, at the terri-tory of the Almaty region it forms a man-madeKapchagai reservoir and falls into Balhash Lake after

kazakhstan—unexplored wealth

annual report | 2006

i.02

jsc kazkommertsbank

kazakhstan—unexplored wealth

annual report | 2006

Also, a seri es of large-scale proj ects have alre a dybeen imple men ted or are in the pro cess of rea li za -tion in the real esta te sec tor. Last year, such elitehotels as the “Renaissance Atyrau”, the “RenaissanceAktau” and also the “Ritz-Carlton” were con struc tedin Atyrau, Aktau and Moscow. This year, the Esentai-park and Regional Financial Center, where the Headoffi ce of Kazkommertsbank will even tu al ly be loca -

ted, are being con struc ted in Almaty. Finally, the inte -gra ted deve lop ment proj ect of Chimbulak andMedeo, which was star ted at the end of 2006, willtran sform these loca tions into first-class moun tainlei su re resorts at the international standards.

Having started in 2005 re-structuring the loanportfolio in favor of the sectors of economy havinghighest growth and development prospects con-tinued last year. Financing of large-scale con struc -tion in Astana, Almaty and Atyrau inc re as ed ourexpo su re to the con struc tion in the loan port fo liofrom 27.1% to 29% and together with finan cingtrade (17.6%) and reta il (15.6%) sec tors res ul ted into62.2 % of the total loan port fo lio as at 31 December2006.

2006 was a remar ka ble year for reta il growth inc -lu ding small and medium-sized businesses whichwas obser ved in four main direc tions:

Branches. The expan sion and moder ni za tion ofope ra tio nal divi sions con ti nu ed during the yearwith 111 new branches having been esta blished incom pa ri son to 40 in the pre vio us year.

Client seg men ta tion. Special focus was made toattrac ting cli ents from small and medium-sizedbusinesses and mid dle class indi vi du als and unitscove ring these busi ness seg ments were for med.

i.05

jsc kazkommertsbank

kazakhstan—unexplored wealth

annual report | 2006

i.04

jsc kazkommertsbank

kazakhstan—unexplored wealth

annual report | 2006

The Ili River falls into Balhash Lake through severalbranches (so called bakanases) and forms a wide delta

Product lines spe ci fi cal ly for small and medium-sized businesses are being acti ve ly ren ewed.

Process auto ma ti on. The eli mi na tion of manu alpro ces ses at the Bank and the expan sion of alter -na ti ve ser vi ce chan nels are being con ti nu ed. Since2002, the latest com pu ter systems have beeninstalled which have helped to auto ma te morethan 200 banking pro ces ses. The ATM and theInter net ban king chan nels are con stan tly expan -ding and finan cial Inter net-por tals for remo te ban -king are being acti ve ly deve lo ped. With the help ofthe inter net-exchan ge cal led MP.kz, cre a ted by theBank’s spe cia lists, the pro cess of buy ing goods andser vi ces for the Bank has been opti miz ed.

Risk mana ge ment in the line with the worldbest practice. In the line with the world bestprac ti ce in cre dit risk mana ge ment, the inte gra -tion of a Market Risk Management (MRM) andOperational Risk Management (ORM) systemshas been star ted. With this aim stan dar di za tionand cen tra li za tion pro ces ses for deci sion mak-ing pur po ses in reta il ban king were under ta ken.Behavioral sco ring models for dif fe rent reta iland small and medium-sized businesses ban -king pro ducts are also being deve lo ped andimple men ted.

With the rapid inc re ase in reta il len ding (168.6%in 2006 com pa red to the end of 2005) it is worthmen tio ning that mort ga ge len ding and car loansdec re as ed cor res pon din gly from 64.7% to 56.7% andfrom 8.8% to 6%. Such decrease was primarily due toan increase in the popu la ri ty of con su mer len ding(28.6%) and other types of loan (8.7%).

i.07

jsc kazkommertsbank

kazakhstan—unexplored wealth

annual report | 2006

i.06

jsc kazkommertsbank

kazakhstan—unexplored wealth

annual report | 2006

The name of the river comes from Mongolian “ilansy”meaning “blinking, glittering”. The Ili is formed byjunction of the Kunges and Tekes Rivers originatedin the North Tyan-Shan mountains

Customer accounts remain the main sour ce ofthe Bank’s fun ding sour ce. By the end of the year,cus to mer accounts had inc re as ed by 2.3 timesand reached KZT687.8 bil lion (US$5.4 bil lion).This figu re repres ents almost 20% mar ket shareand as such, Kazkommertsbank beca me the num -ber 1 Bank in Kazakhstan in terms of gen era ted

depo sits. Corporate cus to mers’ depo sits growthaccoun ted for KZT298.3 bil lion. (or 154.3%) asrepor ted on 31 December 2006 from KZT193.4bil lion as at 31 December 2005 to KZT491.7 bil -lion as at the end of 2006. The value of pri va te sec -tor funds for this period inc re as ed by KZT86.1 bil -lion (or by 78.2%) from KZT110 bil lion to KZT196.1 bil lion.

The 2006 report reflects the prio ri ty thatKazkommertsbank pla ced on small and medi um-sized busi nes ses and len ding in this sec tor during2006 had more than doub led since the pre vio usyear.

2006 also reflec ted a period of inter nal pro ces -ses res truc tu ring to pro vi de for the futu re deve -lop ment of busi ness effec ti ven ess and pro fi ta bi li -ty with par ti cu lar empha sis on sig ni fi cant chan -ges to the risk mana ge ment system which wasaccom plished in close coop era tion with ABNAMRO Risk Management Advisory. As a res ult,ongo ing res earch into the real esta te and secu rit -ies mar kets enab les bet ter mana ge ment of mar -ket risks. Rating and eco no mic price for ma ti onmodels are being impro ved in rela tion to cre ditrisks in cor po ra te ban king. Finally, a major pro -gram on reta il acti vi ti es inc lu des acti ve usage of

i.09

jsc kazkommertsbank

kazakhstan—unexplored wealth

annual report | 2006

i.08

jsc kazkommertsbank

kazakhstan—unexplored wealth

annual report | 2006

It is very peculiar that coming through endless rowof sand-dunes the river as if poured into the clearestlakes covered with water-lilies, surrounded by fruitybirds and brakes of cane

CRM system and the pro-acti ve use of sco ringmodels which help to sim pli fy and stre am li ne thelen ding pro cess.

On 31 December 2006, the most autho ri ta ti vefinan cial maga zi ne “The Banker” once againnamed Kazkommertsbank as the best Bank inKazakhstan and spe ci fi cal ly highlighted its sta tusas a techno lo gi cal lea der. By 31 December 2006,

the Bank’s pro ces sing system ser ved 556 ATMs inc -lu ding 71 with cash depo sit capa bi lit ies, 190 ban -king inter net booths and near ly 4,400 POS ter mi -nals. The amount of cards issu ed by the Bank leaptfrom 400 thou sand to 615 thou sand during a sin gleyear. In addit ion to this, the use of on-line finan cialinter net-por tals for remo te banking (HomeBank.kzfor indi vi du als and OnlineBank.kz for cor po ra te cli -ents) inc re as ed sig ni fi can tly with the total num -ber of HomeBank.kz users having jum ped from40,000 to 80,000.

As a res ult of two suc ces sful invest ments into theBank’s com mon sha res and the issue of subor di na -te obli ga tions during 2006, the Bank’s capi tal inc -re as ed thre e fold from KZT81 bil lion to KZT249 bil -lion (US$2 bil lion). As a res ult of ste a dy ope ra tio nalgrowth, the expan sion of the cli ent base and thelaunch of new pro ducts, the net inco me of theBank in 2006 tota led to KZT29,586 bil lion(US$234.6 mil lion) repres en ting a sub stan ti algrowth of 49.3% over the pre vio us year. Earningsper share inc re as ed from KZT50.95 in 2005 toKZT64.83. Moreover, amongst the pri va te finan cialinsti tu tions, Kazkommertsbank has the mostendu ring cre dit rating of BB+ from Standard &Poor’s and Fitch Ratings.

i.11

jsc kazkommertsbank

kazakhstan—unexplored wealth

annual report | 2006

i.10

jsc kazkommertsbank

kazakhstan—unexplored wealth

annual report | 2006

There are a lot of colorful fishes splashing in thewaters of small lakes on their way to Balhash Lake.All this picturesque landscape is approachable whiletraveling by the Ili River

Unlike other banks in Kazakhstan, which werecre a ted on the basis of sovi et banks with strong capi -tal and per manent cli ents, Kazkommertsbank star -ted its acti vi ti es from zero and during 15 years sinceits for ma ti on it has beco me the lar gest pri va te Bankon the ter ri to ry of the for mer Soviet Union. At theend of 2006, Kazkommertsbank was the first bankfrom Kazakhstan to undertake and successfullyfinalize its inter na tio nal public offe ring on theLondon Stock Exchan ge and in doing so, the yearmar ked the foun da tion for the Bank’s futu re deve -lop ment.

Finally, it is worth say ing that the Bank con si dersthe deve lop ment of part ner rela tionship as themain way to orga ni ze effec ti ve coop era tion withits cli ents, cre di tors and inves tors, and also aims inevery pos si ble ways to con tri bu te towards theirsuc ces ses.

We are gra te ful to our sha rehol ders, cli ents andpart ners, with whom we have experienced manyyears of productive and mutually beneficial coop-eration.

N.A. Zhussupova,Chairman of the Board

i.12

jsc kazkommertsbank

kazakhstan—unexplored wealth

annual report | 2006

Results of the Year

part ii

Singingsand-dunesLatitude 54-12-38

North

Longitude 112-61-22

East

ii.01

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealth

Balance Analysis

The Bank has con ti nu ed to keep high rateof assets growth. Thus, as at 31 December 2006 thevolu me of the Bank’s assets came up to 2,444.3 bil -lion tenge (19.2 bil lion US dol lars), having inc re as -ed by 104.6% com pa red to 1,194.9 bil lion tenge (8.9bil lion US dol lars) as at 31 December 2005. TheBank’s assets growth rate in 2005 came up to 69.7%com pa red to the one as at the end of 2004.

Basic assets growth took place on account of inc re -ase of the loan port fo lio volu me by 125.8% (or by935.4 bil lion KZT). As at 31 December 2005 net volu -me of loan port fo lio inc re as es to 1,678.8 bil lion tenge(13.2 bil lion US dol lars) com pa red to 743.4 bil liontenge (5.5 bil lion US dol lars) as at the end of 2005.

The Bank’s assets struc tu re has under gone sig ni -fi cant chan ges during the year of 2006. The lar gestshare in the Bank’s assets struc tu re con ti nu o uslybelongs to loans to cus to mers and as at 31December 2006 the share of loan to cus to mers’ inc -re as es to 68.7% com pa red to 62.2% as at the end of2005. The share of finan cial assets, esti ma ted byfair value through inco me or loss, has inc re as ed to13.2 % as at the end of 2006 com pa red to 11.7% as atthe begin ning of the year. As a res ult of tighte ningof mini mal res er ve requi re ments poli cy by theNational Bank of the Republic of Kazakhstan in2006, the share of mon eta ry assets in the National(cen tral) Bank of the gen eral assets of the Bank inc -re as ed to 8.6% as at 31December 2006 com pa red to3.1% as at 31 December 2005. The share of bank tobank pla ce ment in the assets of the Bank dec re as -ed to 8.1% as at the end 2006 from 21.3% as at theend of 2005. graph 1,2, 3

Loan portfolioAs at 31 December 2006 loan portfolio (gross)

increases to 1,936.9 billion tenge compared to 885.5billion tenge as at 31 December 2005, the growthrate increases to 118.7% (or by 1,051.4 billion tenge)

Other assetsLoans to customers(net)

68

.7%

13

.4% 8

.6%

8.1

%

0.6

%

0.6

%

graph 2

68.7% Loans to customers

13.4% Marketable securities through income or loss,securities and stocks investments

8.6% Money assets and accounts in national (central) banks, precious metals

8.1% Bank to bank loans and banks assets

0.6% Fixed assets and intangible assets

Assets structure as at 31 December 2006

Assetsas at 31 December 2006

graph 1

74

3.4

45

1,5

1 6

78

.87

65

,5

20

05

20

06

Billion KZT

20

04

50

3.3

20

0,7

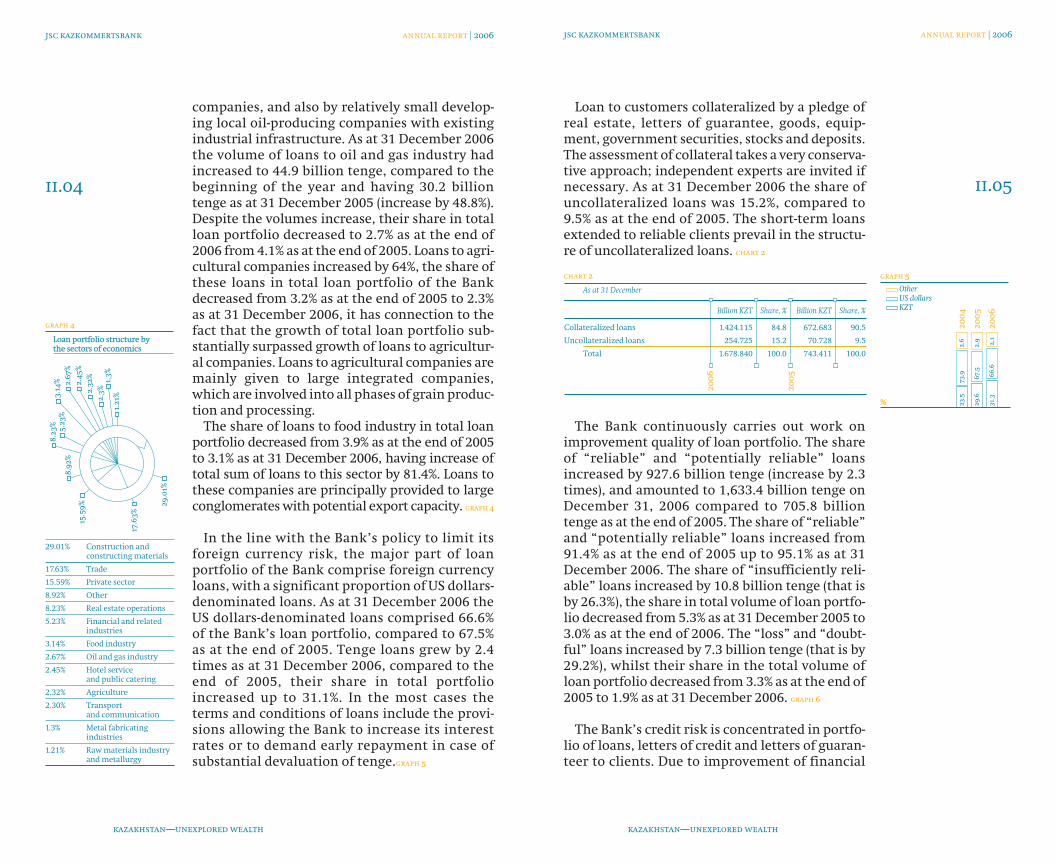

economics, such as: construction and buildingmaterials, private sector crediting, metal-fabricatingindustries, trade, and operations with real estate.Lending to construction, trade, private sector havethe biggest share in the loan portfolio—their cumu-lative share in loan portfolio as at the end of the yearincreased to 62.2% against 59.4% as at the beginningof the year. Besides this, the Bank offered funding tomedium companies, acting as sub-contractors orattending companies, which carry out large interna-tional projects in Kazakhstan.

As at the year ended 31 December 2006 the struc-ture of loan portfolio underwent some changes.Thus, loans to construction and building materialsincreased by 2.4 times and their share increasedfrom 27.1% as at the end of 2005 to 29% as at theend of 2006 due to the development of large-scaleconstruction in Astana, Almaty and Atyrau. Loansto trade companies increased by 2.1 times, in spiteof the decrease of their share in the total portfolioto 17.6% as at the end of 2006 compared to 19.1% asat the end of 2005. The volume of loans to privatesector continued to grow (the growth is by 2.7times compared to as at the end of 2005), the shareof these loans in the total portfolio had increasedfrom 13.1% as at 31 December 2005 to 15.6% as at31 December 2006.

The volume of loans for real estate purchaseincreased by 9.2 times during the year 2006, theshare became 8.2 %. The loans to transport compa-nies and communication enterprises decreased by1.4%, their share in total loan portfolio decreasedto 2.3% as at the end of 2006 from 5.3% as at theend of 2005. The Bank considers metallurgy andmining industry sector as one of the sectors,where decrease of borrowings is expected in thefollowing years. During the year of 2006 the vol-umes reduction by 15.3% is becoming evident,their share in total portfolio remains insignificantand decreases to 1.2% as at the end of 2006, com-pared to 3.2% as at the beginning of the year. Oiland gas sector is presented by large Kazakhstan

ii.03

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealth

compared to 75.9% as at the end of 2005. Includingbut not exclusively, the loan portfolio (gross)increased to 1,752.8 billion tenge, having increasedby 967.2 billion tenge (by 123.1%) compared to thebeginning of the year (785.6 billion tenge). Growthrate of the documentary crediting (gross), presentedby the Bank along with the trade and project fund-ing, during the 2006 came to 84.3%, that led to theincrease of 184,1 billion tenge as at the end of 2006compared to 99.9 billion tenge as at the end of 2005.

The credit portfolio structure is shown in thetable below. chart 1

The Bank also pro vi des its ser vi ces to large andmedi um Kazakhstan indu stri al com pa ni es andtran sna tio nal com pa ni es, ope ra ting inKazakhstan, through offe ring a wide range of ban -king pro ducts inc lu ding trade fun ding, proj ect fun -ding, short term len ding, small and medi um-scalebusi ness len ding. At the same time the Bank offersits ser vi ces to a pri va te sec tor, car ry ing out con su -mer and mort ga ge loans, cre dit cards loans, andalso loans to pri va te entre pren eurs under the smallbusi ness sup port pro gram.

In the year of 2006 the Bank continued toincrease the volumes of loans to different sectors of

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealth

Loan portfolio structure as at 31 December

Billion KZT Share, % Billion KZT Share, %

Loans to customers 1.717.756 92.4 772.006 91.8

Loans, by REPO contracts 35,020 1.9 13.567 1.6

Total loans to customers 1.752.776 94.3 785.573 93.4

Provisions for losses on loans to customers (73,936) (4.0) (42.162) (5.0)

Net loans to customers 1.678.840 90.3 743.411 88.4

Contingent liabilities

Letters of guarantee 91.683 4.9 39.928 4.8

Letters of credit 92.413 5.0 59.951 7.1

Total letters of guarantee and letters of credit 184.096 9.9 99.879 11.9

Provisions for losses on contingent liabilities (4.055) (0.2) (2.589) (0.3)

Total contingent liabilities, net 180.041 9.7 97.290 11.6

Total Loan portfolio, net 1.858.881 100.0 840.701 100.0

20

06

20

05

chart 1

62

.2%

21.3

%

11.9

%

3.1

%

0.7

%

0.8

%

graph 3

62.2% Loans to customers

21.3% Marketable securitiesthrough profit or loss,securities and investments in stocks

11.9% Money assets and accounts in national (central) banks, precious metals

3.1% IBC (inter-bank credits) and assets in banks

0.8% Other assets

0.7% Fixed assets and intangible assets

Assets structure as at 31 December 2005

Loan to cus to mers col la te ra liz ed by a pled ge ofreal esta te, let ters of gua ran tee, goods, equip -ment, govern ment secu rit ies, stocks and depo sits.The asses sment of col la te ral takes a very con ser va -ti ve appro ach; inde pen dent experts are invi ted ifneces sa ry. As at 31 December 2006 the share ofuncol la te ra liz ed loans was 15.2%, com pa red to9.5% as at the end of 2005. The short-term loansexten ded to reli ab le cli ents pre vail in the struc tu -re of uncol la te ra liz ed loans. chart 2

The Bank continuously carries out work onimprovement quality of loan portfolio. The shareof “reliable” and “potentially reliable” loansincreased by 927.6 billion tenge (increase by 2.3times), and amounted to 1,633.4 billion tenge onDecember 31, 2006 compared to 705.8 billiontenge as at the end of 2005. The share of “reliable”and “potentially reliable” loans increased from91.4% as at the end of 2005 up to 95.1% as at 31December 2006. The share of “insufficiently reli-able” loans increased by 10.8 billion tenge (that isby 26.3%), the share in total volume of loan portfo-lio decreased from 5.3% as at 31 December 2005 to3.0% as at the end of 2006. The “loss” and “doubt-ful” loans increased by 7.3 billion tenge (that is by29.2%), whilst their share in the total volume ofloan portfolio decreased from 3.3% as at the end of2005 to 1.9% as at 31 December 2006. graph 6

The Bank’s credit risk is concentrated in portfo-lio of loans, letters of credit and letters of guaran-teer to clients. Due to improvement of financial

ii.04

jsc kazkommertsbank annual report | 2006 jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealthkazakhstan—unexplored wealth

companies, and also by relatively small develop-ing local oil-producing companies with existingindustrial infrastructure. As at 31 December 2006the volume of loans to oil and gas industry hadincreased to 44.9 billion tenge, compared to thebeginning of the year and having 30.2 billiontenge as at 31 December 2005 (increase by 48.8%).Despite the volumes increase, their share in totalloan portfolio decreased to 2.7% as at the end of2006 from 4.1% as at the end of 2005. Loans to agri-cultural companies increased by 64%, the share ofthese loans in total loan portfolio of the Bankdecreased from 3.2% as at the end of 2005 to 2.3%as at 31 December 2006, it has connection to thefact that the growth of total loan portfolio sub-stantially surpassed growth of loans to agricultur-al companies. Loans to agricultural companies aremainly given to large integrated companies,which are involved into all phases of grain produc-tion and processing.

The share of loans to food industry in total loanportfolio decreased from 3.9% as at the end of 2005to 3.1% as at 31 December 2006, having increase oftotal sum of loans to this sector by 81.4%. Loans tothese companies are principally provided to largeconglomerates with potential export capacity. graph 4

In the line with the Bank’s policy to limit itsforeign currency risk, the major part of loanportfolio of the Bank comprise foreign currencyloans, with a significant proportion of US dollars-denominated loans. As at 31 December 2006 theUS dollars-denominated loans comprised 66.6%of the Bank’s loan portfolio, compared to 67.5%as at the end of 2005. Tenge loans grew by 2.4times as at 31 December 2006, compared to theend of 2005, their share in total portfolioincreased up to 31.1%. In the most cases theterms and conditions of loans include the provi-sions allowing the Bank to increase its interestrates or to demand early repayment in case ofsubstantial devaluation of tenge.graph 5

15

.59

% 29

.01%

17

.63

%

8.2

3%

5.2

3%

3.1

4%

8.9

2%

2.3

2%

2.4

5%

2.6

7%

2.3

%

1.2

1%

1.3

%

graph 4

29.01% Construction and constructing materials

17.63% Trade

15.59% Private sector

8.92% Other

8.23% Real estate operations

5.23% Financial and related industries

3.14% Food industry

2.67% Oil and gas industry

2.45% Hotel service and public catering

2.32% Agriculture

2.30% Transportand communication

1.3% Metal fabricating industries

1.21% Raw materials industry and metallurgy

Loan portfolio structure by the sectors of economics

graph 5

2,1

20

06

2,9

20

05

2.6

66

.6

67

.5

73

.9

31.3

29

.6

23

.52

00

4

%

OtherUS dollarsKZT

As at 31 December

Billion KZT Share, % Billion KZT Share, %

Collateralized loans 1.424.115 84.8 672.683 90.5

Uncollateralized loans 254.725 15.2 70.728 9.5

Total 1.678.840 100.0 743.411 100.0

20

06

20

05

chart 2

ii.05

Cash assets and accounts with national (central) banksAs at 31 December 2006 the volume of cash and

assets with the National Bank of the Republic ofKazakhstan and in central banks of the RussianFederation and the Republic of Kyrgyzstan (includ-ing precious metals) amounted to 209.8 billiontenge, that is by 5.6 times (or by 172.6 billion tenge)higher than the volumes at the end of the last year.The substantial growth took place in assets hold onthe correspondent account with the National Bankof Kazakhstan (by 155.5 billion tenge). It becamepossible due to to tightening of minimal reserverequirements for calculation by the National Bankof Kazakhstan in the year of 2006. As a result ofthese requirements the Bank has to reserve 6% and8% for all its internal and external obligationsrespectively. In the structure of money assets andaccounts with in the National (Central) Bank by tothe types of currencies as at 31 December 2006,90.4% are presented by tenge assets, compared to44.1% of tenge assets as at 31 December 2005.

Operations on purchase/sale of cashIn the year of 2006 the turnover of the Bank on

purchase / sale of cash increased by 63.8% in com-parison to 2005 due to substantial increase of salesvolume (by 69.1%). chart 3

state of borrowers, due to stable development ofKazakhstan economics, the effective rate of pro-visions on loans to clients continues to decreaseand as at 31 December 2006 it amounted to 4.3%in comparison to 5.5% as at 31 December 2005.graph 7

As at 31 December 2006 total credit risk shareof twenty largest borrowers of the total loanportfolio amounted to 25.3%, having decreasedfrom 26.8% as at 31 December 2005. The Bankexpects further decrease of concentration ofloan portfolio through attraction of new bor-rowers. graph 8

The general tendency of last several years wasloan terms maturity in accordance with theclients’ demands. The volume of loans with therepayment term from one year to five years roseby 2.2 times. However, their share in the loanportfolio decreased to 37.6% as at 31 December2006, compared to 39.2% as at 31 December2005. The decrease of their share is connectedwith a fact, that the growth rate of long-termloans with the repayment term of more thanfive years was higher. Thus, as at 31 December2006 the growth of loans volumes with therepayment term of more than five years hadincreased by 2.4 times and their share in theloan portfolio increased up to 28.2% as at the endof 2006 from 27% as at 31 December 2005. Thisfactor reflects a higher client’s demand forlonger-term loans, which the Bank providesboth from its own funds and in the framework offacilities from EBRD, international financialorganizations and the Government of theRepublic of Kazakhstan. The share of short-termloans (either less than one month and from onemonth to one year) as at the end of 2006 also hadchanged and amounted to 6.6% and 27.6% , com-pared to 5.3% and 28.5% as at the end of 2005respectively. graph 9

jsc kazkommertsbank annual report | 2006

ii.07

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealthkazakhstan—unexplored wealth

graph 6

1.2

20

06

2.4

20

05

3.7

39

.9

38

.5

36

.2

55

.2

52

.9

52

.52

00

4

5.4

0.7

0.9

0.6

3.6

35

.04

7.0

20

03

%

3.0

5.3

7.0

9.1

Provisions / loan portfolio

graph 7

20

04

5.7

5.5

4.3

20

05

20

06

%

20

03

6.3

Loans concentration (20 largest risk exposures)

graph 8

20

04

24

.8

26

.8

25

.3

20

05

20

06

%

20

03

30

.3

LossDoubtfulInsufficiently reliable Potentially reliableReliable

graph 9

20

06

20

05

37

.6

39

.2

36

.3

28

.2

27

.0

25

.32

00

4

6.6

5.37

.7

%

27

.6

28

.530

.7

Less than 1 monthFrom 1 to 12 monthsFrom 1 to 5 yearsMore than 5 years

Operations on purchase/sale of cash

Annual volume of currency sale, billion US dollars 868.4 513.5 69.1

Annual volume of currency purchase, billion US dollars 186.7 130.5 43.1

Net profit, billion KZT 645 475 35.8

Net profit / Sale volume, % 0.6 0.7

20

06

20

05

сh

an

ge

, %

chart 3

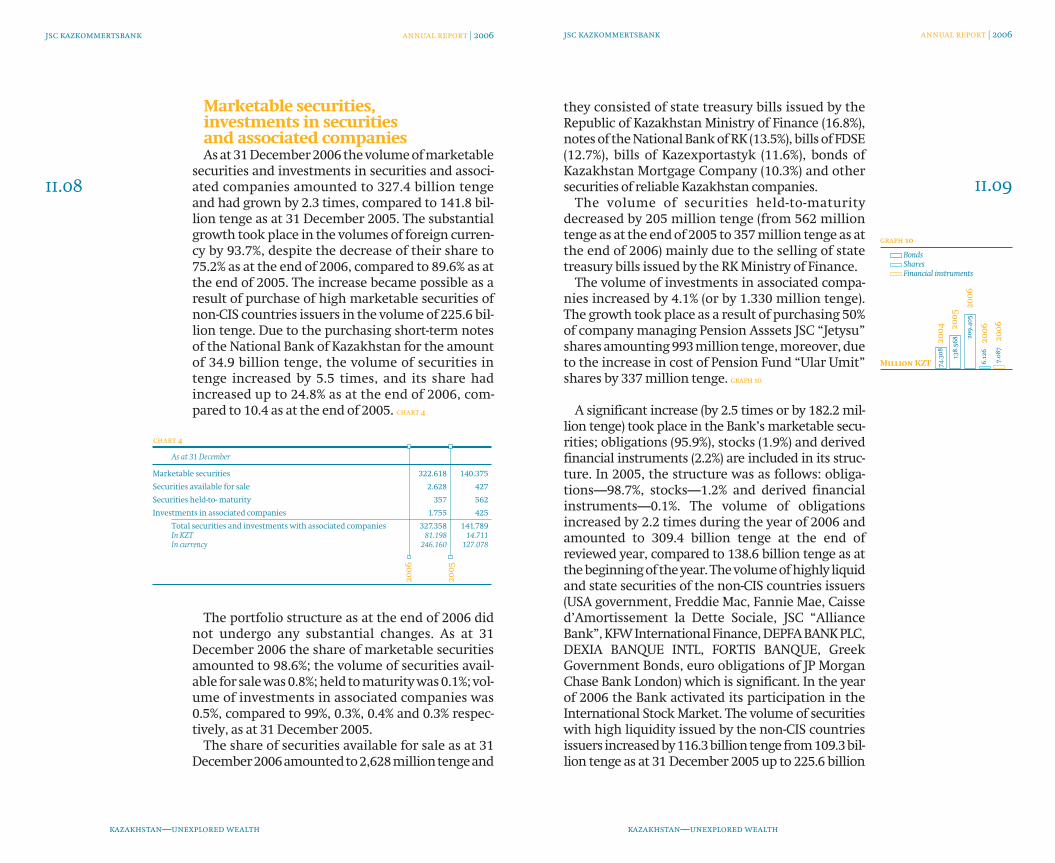

they consisted of state treasury bills issued by theRepublic of Kazakhstan Ministry of Finance (16.8%),notes of the National Bank of RK (13.5%), bills of FDSE(12.7%), bills of Kazexportastyk (11.6%), bonds ofKazakhstan Mortgage Company (10.3%) and othersecurities of reliable Kazakhstan companies.

The volume of securities held-to-maturitydecreased by 205 million tenge (from 562 milliontenge as at the end of 2005 to 357 million tenge as atthe end of 2006) mainly due to the selling of statetreasury bills issued by the RK Ministry of Finance.

The volume of investments in associated compa-nies increased by 4.1% (or by 1.330 million tenge).The growth took place as a result of purchasing 50%of company managing Pension Asssets JSC “Jetysu”shares amounting 993 million tenge, moreover, dueto the increase in cost of Pension Fund “Ular Umit”shares by 337 million tenge. graph 10

A significant increase (by 2.5 times or by 182.2 mil-lion tenge) took place in the Bank’s marketable secu-rities; obligations (95.9%), stocks (1.9%) and derivedfinancial instruments (2.2%) are included in its struc-ture. In 2005, the structure was as follows: obliga-tions—98.7%, stocks—1.2% and derived financialinstruments—0.1%. The volume of obligationsincreased by 2.2 times during the year of 2006 andamounted to 309.4 billion tenge at the end ofreviewed year, compared to 138.6 billion tenge as atthe beginning of the year. The volume of highly liquidand state securities of the non-CIS countries issuers(USA government, Freddie Mac, Fannie Mae, Caissed’Amortissement la Dette Sociale, JSC “AllianceBank”, KFW International Finance, DEPFA BANK PLC,DEXIA BANQUE INTL, FORTIS BANQUE, GreekGovernment Bonds, euro obligations of JP MorganChase Bank London) which is significant. In the yearof 2006 the Bank activated its participation in theInternational Stock Market. The volume of securitieswith high liquidity issued by the non-CIS countriesissuers increased by 116.3 billion tenge from 109.3 bil-lion tenge as at 31 December 2005 up to 225.6 billion

ii.09

jsc kazkommertsbank annual report | 2006

Marketable securities, investments in securities and associated companiesAs at 31 December 2006 the volume of marketable

securities and investments in securities and associ-ated companies amounted to 327.4 billion tengeand had grown by 2.3 times, compared to 141.8 bil-lion tenge as at 31 December 2005. The substantialgrowth took place in the volumes of foreign curren-cy by 93.7%, despite the decrease of their share to75.2% as at the end of 2006, compared to 89.6% as atthe end of 2005. The increase became possible as aresult of purchase of high marketable securities ofnon-CIS countries issuers in the volume of 225.6 bil-lion tenge. Due to the purchasing short-term notesof the National Bank of Kazakhstan for the amountof 34.9 billion tenge, the volume of securities intenge increased by 5.5 times, and its share hadincreased up to 24.8% as at the end of 2006, com-pared to 10.4 as at the end of 2005. chart 4

The portfolio structure as at the end of 2006 didnot undergo any substantial changes. As at 31December 2006 the share of marketable securitiesamounted to 98.6%; the volume of securities avail-able for sale was 0.8%; held to maturity was 0.1%; vol-ume of investments in associated companies was0.5%, compared to 99%, 0.3%, 0.4% and 0.3% respec-tively, as at 31 December 2005.

The share of securities available for sale as at 31December 2006 amounted to 2,628 million tenge and

ii.08

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealth

As at 31 December

Marketable securities 322.618 140.375

Securities available for sale 2.628 427

Securities held-to- maturity 357 562

Investments in associated companies 1.755 425

Total securities and investments with associated companies 327.358 141.789In KZT 81.198 14.711In currency 246.160 127.078

20

06

20

05

chart 4

kazakhstan—unexplored wealth

graph 10

20

04

20

06

20

06

Million KZT

BondsShares Financial instruments

20

06

20

05

74

.30

8

13

8.5

68 2

09

.40

5

6.1

26

7.0

87

December 2006 amounted to 857 million tenge,compared to 1.245 million tenge as at 31December 2005. The decrease of provisions vol-ume by 31.2% became possible as a result ofdecrease of advances volumes to banks.

ii.11

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealth

tenge as at 31 December 2006, the growth was by 2.1times, despite of the decrease of the share to 69.9% asat the end of 2006 from 77.8% as at the end of 2005.

Also the volume of the Government securities(notes of the National Bank of RK, treasury bills ofthe Ministry of Finance of RK, bonds of theDevelopment Bank of Kazakhstan) increased from7.8% as at the end of 2005 up to 11.6% as at the endof 2006. The growth took place basically due to thepurchase of notes of the National Bank of RK for theamount of 33.9 billion KZT.

The Bank continues investing assets into securi-ties of reliable Kazakhstan companies and munici-pal bonds (their volume as at 31 December 2006amounted to 44.7 billion KZT), also into securitiesof the Russian Federation (the volume amountedto 8.3 billion tenge as at 31 December 2006, com-pared to 6.7 billion tenge as at the beginning of theyear). graph 11

Loans and advances to banks The volume of loans and advances to other banks,

net provisions by the end of the year 2006 amount-ed to 197.191 billion KZT, and decreased by 22.5% ,compared to the end of the year 2005, mainly due tothe short-term deposits repayments. The share ofbank to bank placement in the Bank’s assets struc-ture amounted to 8.1%, compared to 21.3% as at theend of 2005. The Bank keeps using conservativeapproach, in respect of placing funds within theother banks. The funds are usually placed for shortterms in accordance with the established limits ofbanks, unless the deposits are secured by theGovernment securities or money assets, moreoverthose deposits are placed within the first classWestern banks. Particularly the basic volume ofloans and advances to banks as at 31 December 2006was deposited for the period of up to three months(88.3%). The share of advances to banks in US dollarsamounted to 45.8%, in national currency—to 38.9%.

The volumes of formed provisions for possiblelosses on loans and advances to banks as at 31

ii.10

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealth

72

.9%

12

.3%

12

.1%

2.7

%

graph 11

Bonds structure as a breakdown on issuers as at 31 December 2006

12.1% Notes of the National Bank of RK

2.7% Notes of the Russian Federation

72.9% Securities of non-CIS countries

12.3% Securities of CIS countries and Baltics, except Russia

On the right bank of the Ili River, in the north-eastdirection from Almaty city there is one unique sand-dune called Singing—it is other miracle of the world

As at 31 December, million KZT

Correspondent accounts 30.277 18.478

KZT 845 199

Foreign currency 29.432 18.279

Loans and deposits to banks 122.266 236.671

KZT 30.296 3.532

Foreign currency 91.970 233,139

Provisions for loan losses (857) (1.245)

Loans and advances to banks, net 151.686 253.904

Loans to banks under REPO contracts 45.505 383

KZT 45.505 383

Foreign currency 0 0

Loans and advances to banks, total 197.191 254.287

20

06

20

05

chart 5

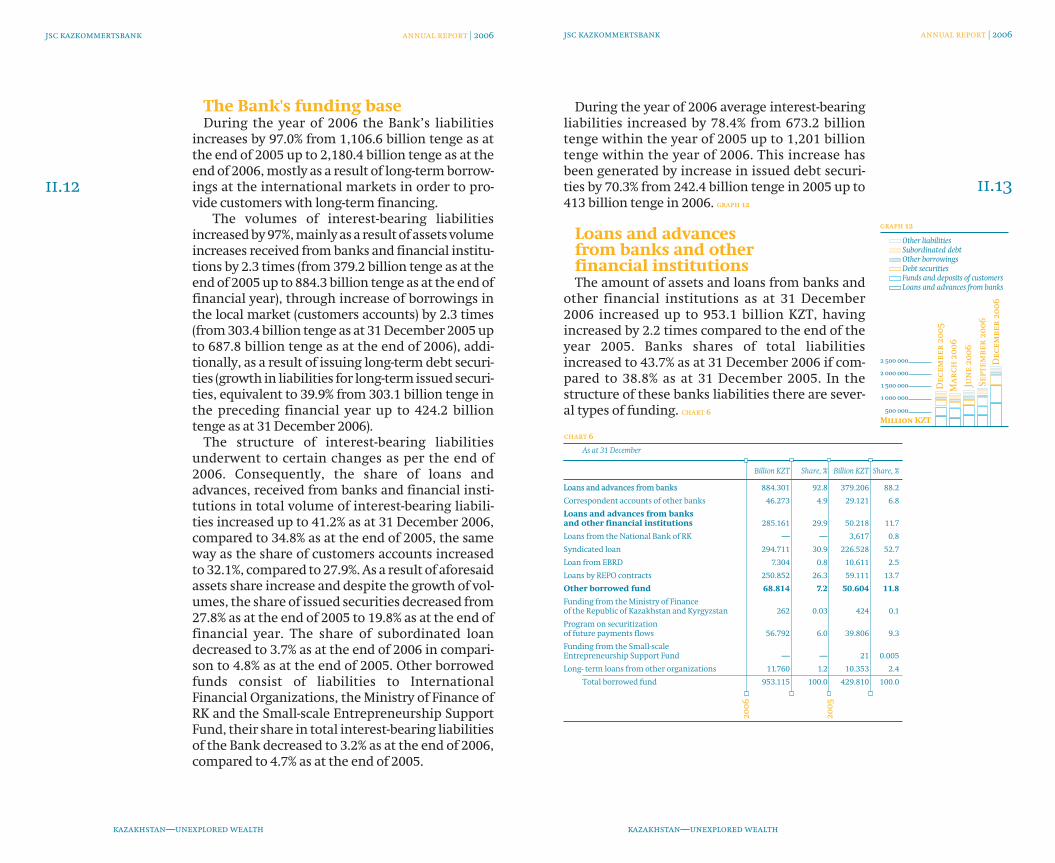

During the year of 2006 average interest-bearingliabilities increased by 78.4% from 673.2 billiontenge within the year of 2005 up to 1,201 billiontenge within the year of 2006. This increase hasbeen generated by increase in issued debt securi-ties by 70.3% from 242.4 billion tenge in 2005 up to413 billion tenge in 2006. graph 12

Loans and advances from banks and other financial institutionsThe amount of assets and loans from banks and

other financial institutions as at 31 December2006 increased up to 953.1 billion KZT, havingincreased by 2.2 times compared to the end of theyear 2005. Banks shares of total liabilitiesincreased to 43.7% as at 31 December 2006 if com-pared to 38.8% as at 31 December 2005. In thestructure of these banks liabilities there are sever-al types of funding. chart 6

The Bank's funding baseDuring the year of 2006 the Bank’s liabilities

increases by 97.0% from 1,106.6 billion tenge as atthe end of 2005 up to 2,180.4 billion tenge as at theend of 2006, mostly as a result of long-term borrow-ings at the international markets in order to pro-vide customers with long-term financing.

The volumes of interest-bearing liabilitiesincreased by 97%, mainly as a result of assets volumeincreases received from banks and financial institu-tions by 2.3 times (from 379.2 billion tenge as at theend of 2005 up to 884.3 billion tenge as at the end offinancial year), through increase of borrowings inthe local market (customers accounts) by 2.3 times(from 303.4 billion tenge as at 31 December 2005 upto 687.8 billion tenge as at the end of 2006), addi-tionally, as a result of issuing long-term debt securi-ties (growth in liabilities for long-term issued securi-ties, equivalent to 39.9% from 303.1 billion tenge inthe preceding financial year up to 424.2 billiontenge as at 31 December 2006).

The structure of interest-bearing liabilitiesunderwent to certain changes as per the end of2006. Consequently, the share of loans andadvances, received from banks and financial insti-tutions in total volume of interest-bearing liabili-ties increased up to 41.2% as at 31 December 2006,compared to 34.8% as at the end of 2005, the sameway as the share of customers accounts increasedto 32.1%, compared to 27.9%. As a result of aforesaidassets share increase and despite the growth of vol-umes, the share of issued securities decreased from27.8% as at the end of 2005 to 19.8% as at the end offinancial year. The share of subordinated loandecreased to 3.7% as at the end of 2006 in compari-son to 4.8% as at the end of 2005. Other borrowedfunds consist of liabilities to InternationalFinancial Organizations, the Ministry of Finance ofRK and the Small-scale Entrepreneurship SupportFund, their share in total interest-bearing liabilitiesof the Bank decreased to 3.2% as at the end of 2006,compared to 4.7% as at the end of 2005.

ii.12

jsc kazkommertsbank annual report | 2006

ii.13

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealthkazakhstan—unexplored wealth

As at 31 December

Billion KZT Share, % Billion KZT Share, %

Loans and advances from banks 884.301 92.8 379.206 88.2

Correspondent accounts of other banks 46.273 4.9 29.121 6.8

Loans and advances from banks and other financial institutions 285.161 29.9 50.218 11.7

Loans from the National Bank of RK — — 3,617 0.8

Syndicated loan 294.711 30.9 226.528 52.7

Loan from EBRD 7.304 0.8 10.611 2.5

Loans by REPO contracts 250.852 26.3 59.111 13.7

Other borrowed fund 68.814 7.2 50.604 11.8

Funding from the Ministry of Finance of the Republic of Kazakhstan and Kyrgyzstan 262 0.03 424 0.1

Program on securitization of future payments flows 56.792 6.0 39.806 9.3

Funding from the Small-scale Entrepreneurship Support Fund — — 21 0.005

Long- term loans from other organizations 11.760 1.2 10.353 2.4

Total borrowed fund 953.115 100.0 429.810 100.0

20

06

20

05

chart 6

graph 12

De

ce

mb

er

20

05

500 000

1 000 000

1 500 000

2 000 000

2 500 000

Se

pte

mb

er

20

06

De

ce

mb

er

20

06

Million KZT

Ju

ne

20

06

Ma

rc

h 2

00

6

Other liabilitiesSubordinated debt Other borrowingsDebt securitiesFunds and deposits of customersLoans and advances from banks

of small-scale entrepreneurship, developmentof import-substitutional and export-orientedproduction.

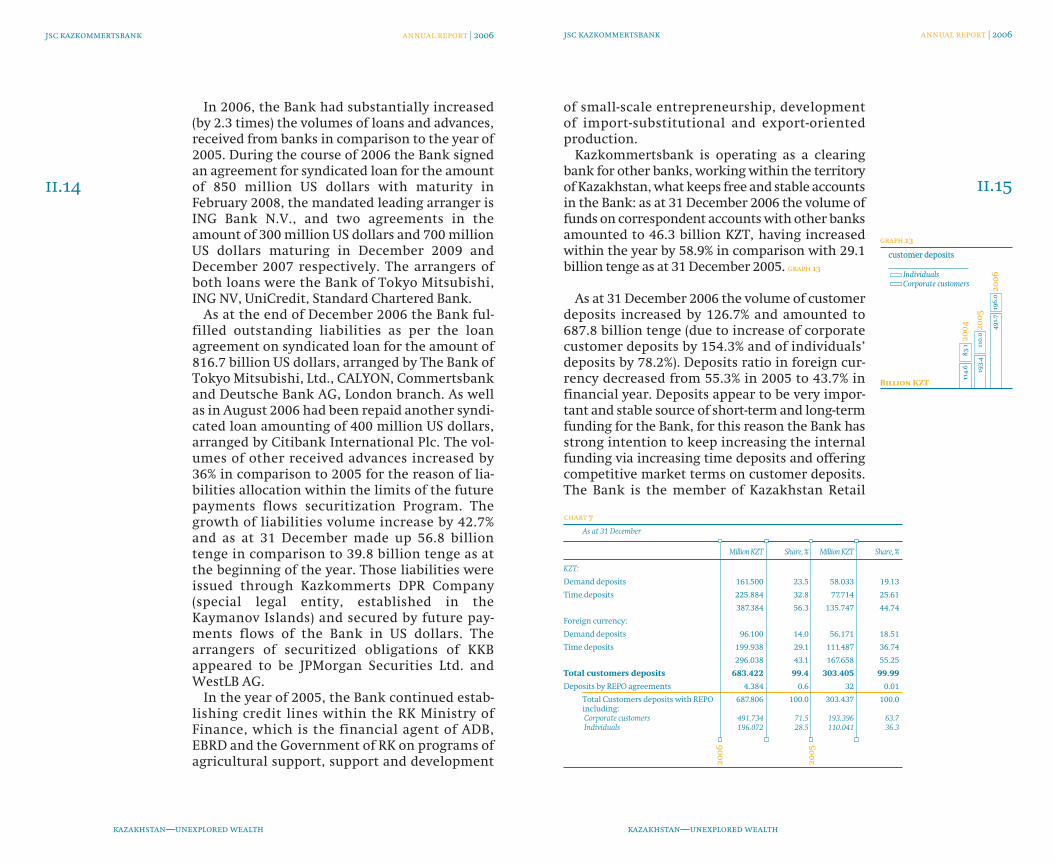

Kazkommertsbank is operating as a clearingbank for other banks, working within the territoryof Kazakhstan, what keeps free and stable accountsin the Bank: as at 31 December 2006 the volume offunds on correspondent accounts with other banksamounted to 46.3 billion KZT, having increasedwithin the year by 58.9% in comparison with 29.1billion tenge as at 31 December 2005. graph 13

As at 31 December 2006 the volume of customerdeposits increased by 126.7% and amounted to687.8 billion tenge (due to increase of corporatecustomer deposits by 154.3% and of individuals’deposits by 78.2%). Deposits ratio in foreign cur-rency decreased from 55.3% in 2005 to 43.7% infinancial year. Deposits appear to be very impor-tant and stable source of short-term and long-termfunding for the Bank, for this reason the Bank hasstrong intention to keep increasing the internalfunding via increasing time deposits and offeringcompetitive market terms on customer deposits.The Bank is the member of Kazakhstan Retail

In 2006, the Bank had substantially increased(by 2.3 times) the volumes of loans and advances,received from banks in comparison to the year of2005. During the course of 2006 the Bank signedan agreement for syndicated loan for the amountof 850 million US dollars with maturity inFebruary 2008, the mandated leading arranger isING Bank N.V., and two agreements in theamount of 300 million US dollars and 700 millionUS dollars maturing in December 2009 andDecember 2007 respectively. The arrangers ofboth loans were the Bank of Tokyo Mitsubishi,ING NV, UniCredit, Standard Chartered Bank.

As at the end of December 2006 the Bank ful-filled outstanding liabilities as per the loanagreement on syndicated loan for the amount of816.7 billion US dollars, arranged by The Bank ofTokyo Mitsubishi, Ltd., CALYON, Commertsbankand Deutsche Bank AG, London branch. As wellas in August 2006 had been repaid another syndi-cated loan amounting of 400 million US dollars,arranged by Citibank International Plc. The vol-umes of other received advances increased by36% in comparison to 2005 for the reason of lia-bilities allocation within the limits of the futurepayments flows securitization Program. Thegrowth of liabilities volume increase by 42.7%and as at 31 December made up 56.8 billiontenge in comparison to 39.8 billion tenge as atthe beginning of the year. Those liabilities wereissued through Kazkommerts DPR Company(special legal entity, established in theKaymanov Islands) and secured by future pay-ments flows of the Bank in US dollars. Thearrangers of securitized obligations of KKBappeared to be JPMorgan Securities Ltd. andWestLB AG.

In the year of 2005, the Bank continued estab-lishing credit lines within the RK Ministry ofFinance, which is the financial agent of ADB,EBRD and the Government of RK on programs ofagricultural support, support and development

ii.14

jsc kazkommertsbank annual report | 2006

ii.15

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealthkazakhstan—unexplored wealth

customer deposits

graph 13

20

04

114

.68

3.1

19

3.4

110

.0

49

1.7

19

6.0

20

05

20

06

Billion KZT

IndividualsCorporate customers

As at 31 December

Million KZT Share, % Million KZT Share, %

KZT:

Demand deposits 161.500 23.5 58.033 19.13

Time deposits 225.884 32.8 77.714 25.61

387.384 56.3 135.747 44.74

Foreign currency:

Demand deposits 96.100 14.0 56,171 18.51

Time deposits 199.938 29.1 111.487 36.74

296.038 43.1 167.658 55.25

Total customers deposits 683.422 99.4 303.405 99.99

Deposits by REPO agreements 4.384 0.6 32 0.01

Total Customers deposits with REPO 687.806 100.0 303.437 100.0including:Corporate customers 491.734 71.5 193.396 63.7Individuals 196.072 28.5 110.041 36.3

20

06

20

05

chart 7

to 24.5% in 2005. Despite the fact that depositsvolume is continuing to be significant, the Bankintends to decrease the total local funding, byoffering services to individuals, small and medi-um-sized corporate customers. graph 14

Issued debt securities The important source of funding turns to be

debt securities, and from 1998 the Bank displayshigh activity in euro liabilities market. As at31 December 2006 the volume of issued debtsecurities increased up to 39.9% and made up424.4 billion KZT. This increase took place due tothe additional issues of euro liabilities. In thisrespect, in February 2006 the Bank placed 3-yeareuro liabilities in exotic currency (Singapore dol-lars), amounting 100 million Singapore dollarswith coupon rate 4.25%. In March 2006, the Bankplaced euro liabilities for the amount of 300 mil-lion euro with the coupon of 5.125% and maturi-ty of 5 years, and in November 2006, the Bankplaced euro liabilities in the amount of 500 mil-lion US dollars with the coupon of 7.5% with thematurity of 10 years. The share of debt securitiesin total liabilities of the Bank decreased to 19.5%as at 31 December 2006 in comparison to 27.4%as at 31 December 2005 due to decrease inclients’ assets share.

Subordinated debtSubordinated debt of the Bank increases to

78.9 billion tenge as at 31 December 2006, whichrises by 51.2% from 52.2 billion tenge as at 31December 2005. The increase in 2006 was due tothe release of 10-year subordinated liabilitiesamounting for 200 million US dollars in July2006 with coupon of 8.625% and additionally bythe release of 10-year subordinated liabilities ofJSC “Moskommertsbank” in the amount of20 million US dollars with coupon rate 10%.

The share of individual’s deposits decreasedfrom 36.3% as at the end of 2005 to 28.5% as at theend of 2006 from total volume of customerdeposits due to advance growth rates of corporatecustomer deposits. In accordance with strategyconcerning retail customers the Bank believes,that by providing a wider range of services andwider services as electronic banking, credit anddebit cards, payrolls services, public utilities pay-ment, asset management, moreover, insuranceproducts for individuals, there is a strong abilityto attract more customers and to improve capaci-ties for providing services.

In 2006, the concentration of 20 largest cus-tomer deposits of the Bank increased up to 44.4%of total volume of customers deposits, compared

ii.16

jsc kazkommertsbank annual report | 2006

ii.17

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealthkazakhstan—unexplored wealth

Top 20 largest depositors

graph 14

20

04

30

.7

24

.5

44

.4

20

05

20

06

%

The sand-dune sings only in some certain conditions.Only clean quarts sand can produce sounds, at that thegrains should be 0.3–0.5 mm in diameter. Sand doeskeep silence in wet weather, after rains

Capitalization

The total capitalization of the Bankincreased by the end of 2006 up to 9.9 billion USdollars (compared to 116.7% as at the end of2005). This increase occurred as a result ofgrowth in long-term borrowings (by 105%), sub-ordinated debt (by 58.2%), and also equity capitalby 222.7%. The growth in equity capital tookplace mainly as a result of IPO performance anddomestic placement of the Bank’s shares (138.6billion KZT), and capitalization of current profits(27.8 billion KZT). chart 1

The Bank’s equity capital, calculated for the pur-poses of securing capital adequacy, as at 31December 2006 amounted to 327.1 billion tenge(including Tier I capital to 270.4 billion KZT). Theincrease of equity capital during the year of 2006amounted to 144.6% (or by 193.3 billion KZT). TheBank’s Tier I capital adequacy ratio and the Bank’stotal capital adequacy ratio, calculated according tothe Basel Accord, as at 31 December 2006 amountedto 12.45% and 15.05% respectively (as at 31 December2005—to 11.02% and 14.38% respectively). graph 1

ii.18

jsc kazkommertsbank annual report | 2006

ii.19

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealth

As at 31 December

Liabilities

Long-term liabilities 7.349.370 3.585.184 933.370 480.343

Subordinated long term debts 608.228 384.431 77.245 51.506

Total liabilities 7.957.598 3.969.615 1.010.615 531.849

Equity capital

Common shares 45.252 27.989 5.747 3.750

Preference shares 9.827 9.300 1.248 1.246

Chartered capital 55.079 37.289 6.995 4.996

Shares premiums 1.201.055 118.689 152.534 15.902

Reserves from revaluation 19.181 11.345 2.436 1.520

Reserves from income 682.591 439.446 86.689 58.877

Total equity capital 1.957.906 606.769 248.654 81.295

Total capitalization 9.915.504 4.576.384 1.259.269 613.144

Thousand US dollars Million KZT

20

06

20

05

20

06

20

05

chart 1

Charter Capital and provisions’structure for the year ended 2006

graph 1

20

04

20

05

20

06

Million KZT

15

.0%

50

10

0

75

00

0

25

0 0

00

14

.37

% 15

.7%

Total charter capital and provisionsCapital adequacy

kazakhstan—unexplored wealth

Period ended 31 December

Assets Million KZT % Million KZT %

Loans and deposits to financial institutions (net) 110.681 5.78 93.017 4.13

Loans and deposits to financial institutions 111.285 5.75 93.488 4.11in KZT 22.037 3.72 7.343 3.98in foreign currency 89.248 6.25 86.145 4.12

Provisions for loans (604) — (471) —in KZT (35) — (146) —in foreign currency (569) — (325) —

Correspondent account with NBK 62.933 — 8.073 —in KZT 55.257 — 5.611 —in foreign currency 7.676 — 2.462 —

Securities 155.115 5.80 79.989 5.92in KZT 44.680 6.05 36.514 4.11in foreign currency 110.435 5.70 43.475 7.43

Loans to customers (net) 965.170 13.65 547.371 14.09

dividends on loans 996.623 13.22 559.749 13.78in KZT 267.517 13.46 157.763 13.94in foreign currency 729.106 13.13 401.986 13.72

non-performing and overdue 18.738 — 20.462 —in KZT 5.988 — 6.743 —in foreign currency 12.750 — 13.719 —

Provisions for loans (50.192) — (32.840) —in KZT (15.832) — (10.830) —in foreign currency (34.360) — (22.010) —

Cash and balances 18.441 — 12.904 —in KZT 9.452 — 6.634 —in foreign currency 8.990 — 6.270 —

NOSTRO accounts 14.917 0.88 10.710 0.76in KZT 1.547 0.00 1.048 0.00in foreign currency 13.370 0.98 9.662 0.84

Fixed and intangible assets after amortization revaluation 13.817 — 9.252 —in KZT 12.380 — 8.442 —in foreign currency 1.437 — 810 —

Goodwill 2.405 — 254 —in KZT 2.405 — 254 —in foreign currency — — — —

Investments 637 — 328 —in KZT 637 — 328 —in foreign currency — — — —

Other assets 39.479 — 20.682 —in KZT 14.926 — 9.371 —in foreign currency 24.553 — 11.311 —

Total 1.383.595 10.64 782.580 10.96in KZT 420.960 9.39 229.075 10.38in foreign currency 962.635 11.19 553.505 11.20

Average Averagevolume Interest rate volume Interest rate

20

05

20

06

chart 2

ii.20

jsc kazkommertsbank annual report | 2006

ii.21

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealthkazakhstan—unexplored wealth

Period ended 31 December

Liabilities and charter capital Million KZT % Million KZT %

customer demand deposits 113.642 0.13 74.115 0.32in KZT 76.963 0.15 44.897 0.36in foreign currency 36.679 0.08 29.218 0.25

customer time deposits 266.606 6.72 158.225 6.40in KZT 163.124 7.95 62.161 8.03in foreign currency 103.482 4.79 96.064 5.35

LORO accounts 7.968 0.13 3.200 0.31in KZT 4.397 0.19 2.480 0.37in foreign currency 3.571 0.06 720 0.07

Short-term bank to bank loans 85.382 6.00 22.289 4.19in KZT 1.624 4.42 3.755 2.53in foreign currency 83.758 6.03 18.534 4.53

Long-term borrowing from banks and financial institutions 256.272 6.51 160.664 6.03in KZT 3.213 5.88 2.939 5.97in foreign currency 253.059 6.52 157.725 6.03

Other borrowed funds 58.164 6.9 12.270 6.22in KZT 188 2,17 243 3.01in foreign currency 57.976 6.91 12.027 6.29

Securities issued 412.954 9.34 242.428 9.66in KZT 15.931 7.39 10.409 7.31in foreign currency 397.023 9.42 232.019 9.77

Other liabilities 47.688 — 32.759 —in KZT 25.201 — 15.273 —in foreign currency 22.487 — 17.486 —

TOTAL liabilities 1.248.676 6.61 705.950 6.40in KZT 290.641 5.00 142.157 4.36in foreign currency 958.035 7.09 563.793 6.91

Charter capital and Funds 8.817 — 6.271 —in KZT 1.134 — — —in foreign currency 7.683 — 6.271 —

Minority interest 126.102 — 70.359 —in KZT 126.102 — 70.359 —in foreign currency — — — —

Total 1.383.595 5.96 782.580 5.77in KZT 417.877 3.48 212.516 2.92in foreign currency 965.718 7.04 570.064 6.84KZT /US dollars average exchange rate 126.12 — 132.87 —

Average Averagevolume Interest rate volume Interest rate

20

05

20

06

chart 3

Results of the Bank's operations for the year 2006 compared to the year 2005, million KZT

Net interest income 31.248 22.719 37.5

Net non-interest income 28.967 14.567 98.9

Operating incomes 60.215 37.286 61.5

Operating expenses (18.039) (13.368) 34.9

Insurance provision formation and provisions on devaluation of other operations (383) (880) (56. 5)

Securities provision formation and other off-balance debts (1.548) (1.059) 46.2

Income from associates 1.130 174 549.4

Income before taxation 41.375 22.153 86.8

Income tax (11.789) (2.338) 404.2

Net profit 29.586 19.815 49.3

Related to:Associated Share holders 27.810 18.392 51.2Minority interest 1.776 1.423 24.8

Profit ratioROA 2.1% 2.5%ROE 22.1% 26.1%

20

06

20

05

сh

an

ge

, %

chart 4

As of 2006, the associated company related incomeamounted to 27.810 million KZT, which is 51.2%higher comparing to 2005. High level of incomecompared to the last year is primarily resulted fromnet interest income and net non-interest incomeincrease in 2006; the growth is by 37.5% and by98.9%, respectively, compared to 2005. chart 5

Net interest income in 2006 increases to 31.248 mil-lion tenge and had grown by 37.5% in comparison to2005. This increase became possible on account of thegrowth of average volumes of the Bank’s assets bearinginterest income by 70.4% and the growth of their cost

Net interest incomecompared to the year 2005, million KZT

Interest income 147,250 86,407 70.4

Interest expense (83,115) (45,855) 81.3

Net interest income before provisionon devaluation of interest-bearing assets 64,135 40,552 58.2

Provision on devaluation of interest-bearing assets (32,887) (17,833) 84.4

Net interest income 31,248 22,719 37.5

20

06

20

05

сh

an

ge

, %

chart 5

from 11.73% to 11.82%. The factor of net interest marginafter formation of provisions for devaluation of interestassets towards average interest assets decreased a littlefrom 3.1% in 2005 to 2.5% in 2006. Such decrease ismainly stipulated by the growth of average cost of inter-est-bearing liabilities from 6.71% within the year of2005 to 6.78% within the year of 2006.

Net interest income before formation of provi-sions for devaluation of interest assets increasedby 58.2% up to 64.135 million tenge in comparisonto 40.552 million tenge in 2005. The factor of netinterest margin before formation of provisionstowards average interest assets decreased from5.5% in 2005 to 5.1% in 2006. graph 2, 3, 4

Interest income for the year of 2005 increased by70.4% or by 60.843 million tenge and came to147.250 million tenge against 86.407 million tengefor the year of 2005. This increase is connected to thegrowth of average interest-bearing assets by 70.4%and small growth of their cost from 11.73% for 2005up to 11.82% for 2006. Thus average volume of inter-est-bearing assets for 2006 came to 1.246 billiontenge in comparison with 731 billion tenge for 2005.

Basic growth took place as a result of interest incomeon customer loans , despite the fact that its share in thestructure of interest income remained on the samelevel with the last year and came to 88.6% (in compari-son to 88.3% in 2005). The growth of interest income onloans to customers by 71.1% is stipulated by sufficientincrease of average volume of loans issued to cus-tomers (gross) from 580 billion tenge for the year of2005 to 1.015 billion tenge for 2006. The growth ofaverage volume of loans to customers (gross) came to435 billion tenge or 75 %. In the structure of averageinterest assets loans to customers continue to keep themajor part, their share for the year of 2006 came to77.5% in comparison to 74.9% in 2005. Interest incomeon loans to customers issued by agreements of reverseREPO in the structure of interest income on loansissued to customer occupy insignificant share (1.0%and 0.8% for 2006 and 2005, respectively).

jsc kazkommertsbank annual report | 2006

ii.23

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealthkazakhstan—unexplored wealth

graph 2

22

.719

20

05

40

.55

2

17

.79

8

20

04

29

.02

0

64

.13

5

31.2

48

20

06

million

tenge

graph 3

20

04

6.1

13

.75

3.1

1

2.5

1

5.5

5

5.1

5

20

05

20

06

%

Interest margin before provisions / average assetsInterest margin after provisions / average assets

graph 4

20

04

12

6

5.8 5

6 6.9 7

12

12

20

05

20

06

%

Interest rate on assetsInterest rate on liabilitiesNet interest margin (before provisions)

Interest margin before provisionsInterest margin after provisions

Average net interest margin The growth of interest income on loans issued tobanks came to 76.6% from 3.962 million tenge in2005 to 6.994 million tenge in 2006, its share in thestructure of interest income did not change and cameto 4.7% (in comparison to 4.6% in 2005). The growthby 3.033 million tenge (by 1.8 times) took place as aresult of the growth of average interest rates from4.11% for 2005 up to 5.75% for 2006 and the increaseof average volume of loans issued to clients (gross) by17.8 billion tenge or by 19% in comparison with theyear of 2005. Average volume of loans issued to banks(gross) for 2006 came to 111.3 billion tenge in com-parison to 93.5 billion tenge for the year of 2005. Theshare of interest income on loans issued to banks byagreements of reverse REPO in the structure of loaninterest income increased from 1% in 2005 up to 6.6%for the year of 2006.

Interest income on marketable securities for theyear of 2006 increased up to 7.183 million tengefrom 4.087 million tenge for the year of 2005. Thegrowth was stipulated by the increase of averagevolume of securities portfolio for the year of 2006 by

Interest income and average interest-bearing assets of the Bank

Net-income, KZT million Average profitability, % annually

Foreign ForeignKZT currency KZT currency

Interests income on loans to customers 130.468 76.256 71.1 13.16 12.9 13.37 13.26interests income on loans and advances to bank( incl. reverse REPO operations) 1.351 608 122.2Interests income on loans to customers 129.117 75.648 70.7

Interests income on loans to banks 6.994 3.961 76.6 3.72 6.25 3.98 4.12Interests income on loans to banks 6.532 3.923 66.5interests income on loans and advances to bank(incl. reverse REPO operations) 462 38 1115.8

Interests on marketable securities 7.183 4.087 75.8 6.05 5.7 4.11 7.43

Amortization of discount on loans 2.605 2.103 23.9

Interest income, total 147.250 86.407 70.4 12.13 11.71 11.99 11.64

20

06

20

06

20

05

сh

an

ge

, %

chart 6

20

05

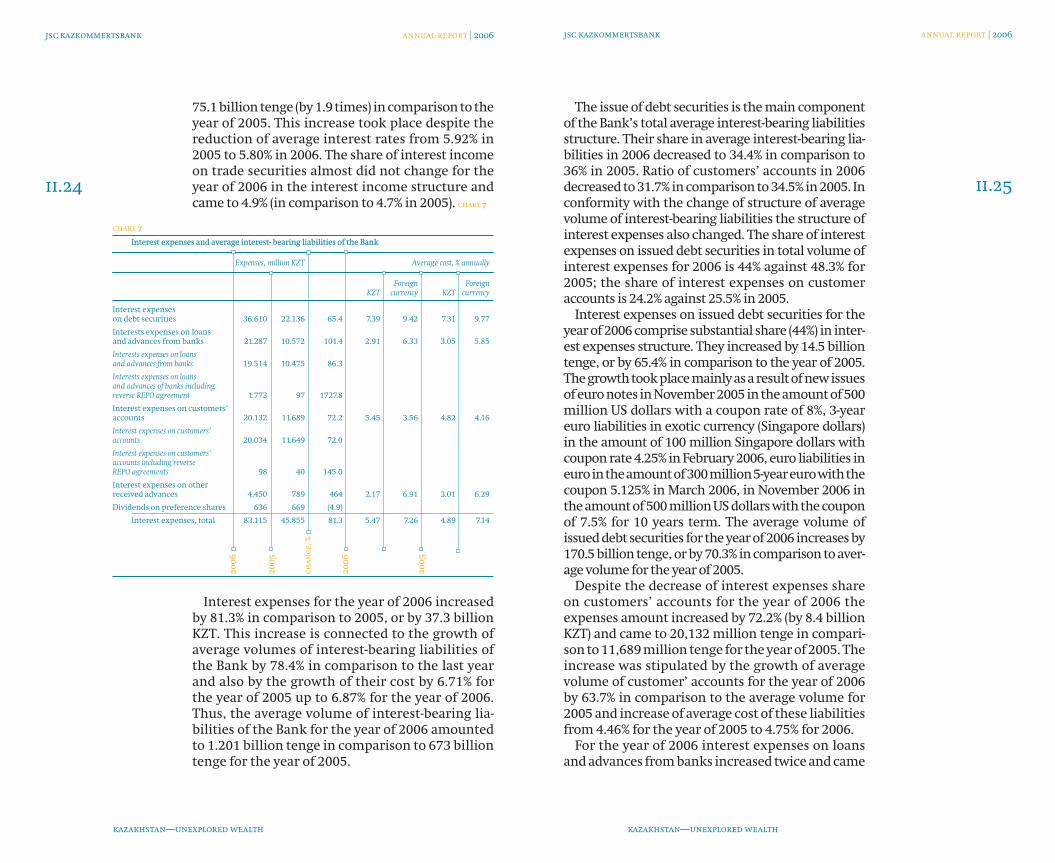

75.1 billion tenge (by 1.9 times) in comparison to theyear of 2005. This increase took place despite thereduction of average interest rates from 5.92% in2005 to 5.80% in 2006. The share of interest incomeon trade securities almost did not change for theyear of 2006 in the interest income structure andcame to 4.9% (in comparison to 4.7% in 2005). chart 7

Interest expenses for the year of 2006 increasedby 81.3% in comparison to 2005, or by 37.3 billionKZT. This increase is connected to the growth ofaverage volumes of interest-bearing liabilities ofthe Bank by 78.4% in comparison to the last yearand also by the growth of their cost by 6.71% forthe year of 2005 up to 6.87% for the year of 2006.Thus, the average volume of interest-bearing lia-bilities of the Bank for the year of 2006 amountedto 1.201 billion tenge in comparison to 673 billiontenge for the year of 2005.

ii.24

jsc kazkommertsbank annual report | 2006

ii.25

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealthkazakhstan—unexplored wealth

The issue of debt securities is the main componentof the Bank’s total average interest-bearing liabilitiesstructure. Their share in average interest-bearing lia-bilities in 2006 decreased to 34.4% in comparison to36% in 2005. Ratio of customers’ accounts in 2006decreased to 31.7% in comparison to 34.5% in 2005. Inconformity with the change of structure of averagevolume of interest-bearing liabilities the structure ofinterest expenses also changed. The share of interestexpenses on issued debt securities in total volume ofinterest expenses for 2006 is 44% against 48.3% for2005; the share of interest expenses on customeraccounts is 24.2% against 25.5% in 2005.

Interest expenses on issued debt securities for theyear of 2006 comprise substantial share (44%) in inter-est expenses structure. They increased by 14.5 billiontenge, or by 65.4% in comparison to the year of 2005.The growth took place mainly as a result of new issuesof euro notes in November 2005 in the amount of 500million US dollars with a coupon rate of 8%, 3-yeareuro liabilities in exotic currency (Singapore dollars)in the amount of 100 million Singapore dollars withcoupon rate 4.25% in February 2006, euro liabilities ineuro in the amount of 300 million 5-year euro with thecoupon 5.125% in March 2006, in November 2006 inthe amount of 500 million US dollars with the couponof 7.5% for 10 years term. The average volume ofissued debt securities for the year of 2006 increases by170.5 billion tenge, or by 70.3% in comparison to aver-age volume for the year of 2005.

Despite the decrease of interest expenses shareon customers’ accounts for the year of 2006 theexpenses amount increased by 72.2% (by 8.4 billionKZT) and came to 20,132 million tenge in compari-son to 11,689 million tenge for the year of 2005. Theincrease was stipulated by the growth of averagevolume of customer’ accounts for the year of 2006by 63.7% in comparison to the average volume for2005 and increase of average cost of these liabilitiesfrom 4.46% for the year of 2005 to 4.75% for 2006.

For the year of 2006 interest expenses on loansand advances from banks increased twice and came

Interest expenses and average interest- bearing liabilities of the Bank

Expenses, million KZT Average cost, % annually

Foreign ForeignKZT currency KZT currency

Interest expenses on debt securities 36.610 22.136 65.4 7.39 9.42 7.31 9.77

Interests expenses on loans and advances from banks 21.287 10.572 101.4 2.91 6.33 3.05 5.85

Interests expenses on loans and advances from banks 19.514 10.475 86.3

Interests expenses on loans and advances of banks including reverse REPO agreement 1.773 97 1727.8

Interest expenses on customers’ accounts 20.132 11.689 72.2 5.45 3.56 4.82 4.16

Interest expenses on customers’ accounts 20.034 11.649 72.0

Interest expenses on customers’ accounts including reverse REPO agreements 98 40 145.0

Interest expenses on other received advances 4.450 789 464 2.17 6.91 3.01 6.29

Dividends on preference shares 636 669 (4.9)

Interest expenses, total 83.115 45.855 81.3 5.47 7.26 4.89 7.14

20

06

20

06

20

05

сh

an

ge

, %

chart 7

20

05

volume (gross) as at 31December 2006 by 2.2 times(or by 945.8 billion KZT) in comparison to the vol-ume as at 31 December 2005. Despite the growth involumes of customers’ loans, the effective provi-sions rate decreased to 4.3% as at 31December 2006in comparison with 5.5% as at the end of 2005. It isdue to improvement of general economic situationin Kazakhstan and also to general improvement ofquality of the Bank’s loan portfolio.

Average volume of formed provisions for cus-tomer loan losses for the year of 2006 came to50.192 million tenge in comparison with 32.840million tenge during the year of 2005. The growthby 17.352 billion tenge or by 52.8% took place owingto increase of average volumes of performing loansby 436.9 billion tenge or by 78%. The share of aver-age overdue loans in total average loan portfolio forthe year of 2006 came to 1.8% against 3.5% in 2005.

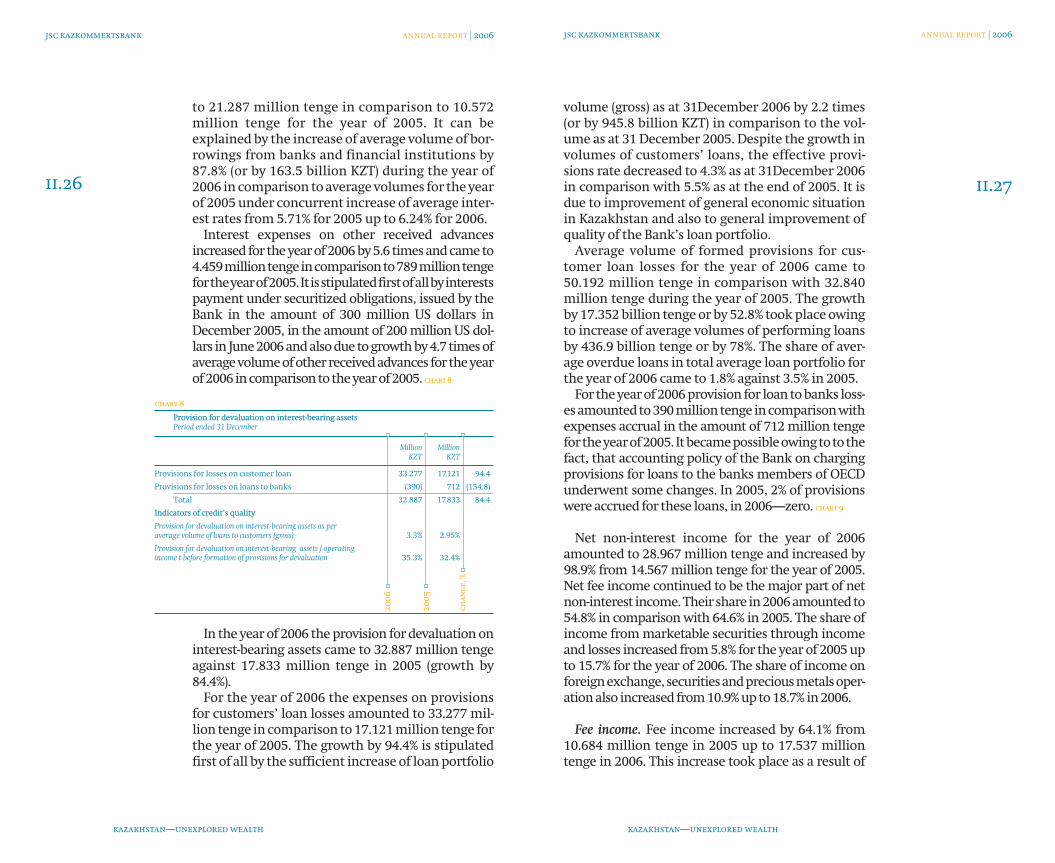

For the year of 2006 provision for loan to banks loss-es amounted to 390 million tenge in comparison withexpenses accrual in the amount of 712 million tengefor the year of 2005. It became possible owing to to thefact, that accounting policy of the Bank on chargingprovisions for loans to the banks members of OECDunderwent some changes. In 2005, 2% of provisionswere accrued for these loans, in 2006—zero. chart 9

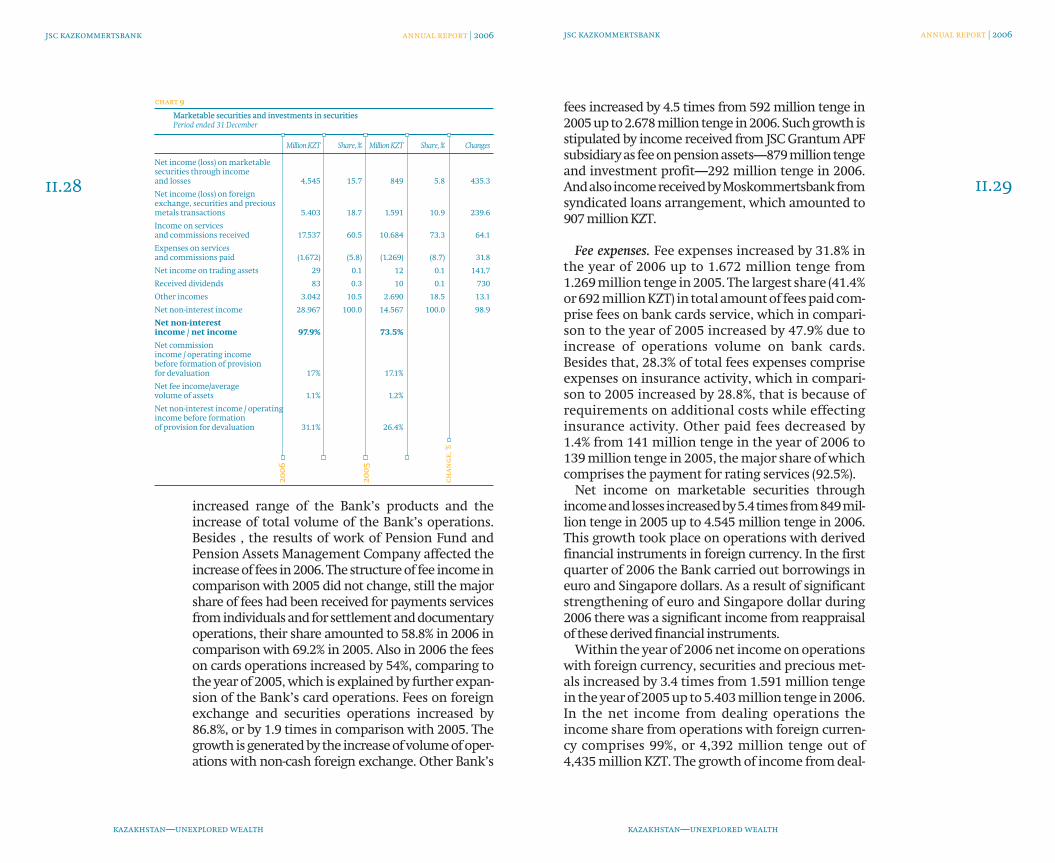

Net non-interest income for the year of 2006amounted to 28.967 million tenge and increased by98.9% from 14.567 million tenge for the year of 2005.Net fee income continued to be the major part of netnon-interest income. Their share in 2006 amounted to54.8% in comparison with 64.6% in 2005. The share ofincome from marketable seсurities through incomeand losses increased from 5.8% for the year of 2005 upto 15.7% for the year of 2006. The share of income onforeign exchange, securities and precious metals oper-ation also increased from 10.9% up to 18.7% in 2006.

Fee income. Fee income increased by 64.1% from10.684 million tenge in 2005 up to 17.537 milliontenge in 2006. This increase took place as a result of

ii.27

to 21.287 million tenge in comparison to 10.572million tenge for the year of 2005. It can beexplained by the increase of average volume of bor-rowings from banks and financial institutions by87.8% (or by 163.5 billion KZT) during the year of2006 in comparison to average volumes for the yearof 2005 under concurrent increase of average inter-est rates from 5.71% for 2005 up to 6.24% for 2006.

Interest expenses on other received advancesincreased for the year of 2006 by 5.6 times and came to4.459 million tenge in comparison to 789 million tengefor the year of 2005. It is stipulated first of all by interestspayment under securitized obligations, issued by theBank in the amount of 300 million US dollars inDecember 2005, in the amount of 200 million US dol-lars in June 2006 and also due to growth by 4.7 times ofaverage volume of other received advances for the yearof 2006 in comparison to the year of 2005. chart 8

In the year of 2006 the provision for devaluation oninterest-bearing assets came to 32.887 million tengeagainst 17.833 million tenge in 2005 (growth by84.4%).

For the year of 2006 the expenses on provisionsfor customers’ loan losses amounted to 33.277 mil-lion tenge in comparison to 17.121 million tenge forthe year of 2005. The growth by 94.4% is stipulatedfirst of all by the sufficient increase of loan portfolio

ii.26

jsc kazkommertsbank annual report | 2006 jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealthkazakhstan—unexplored wealth

Provision for devaluation on interest-bearing assetsPeriod ended 31 December

Million MillionKZT KZT

Provisions for losses on customer loan 33.277 17.121 94.4

Provisions for losses on loans to banks (390) 712 (154.8)

Total 32.887 17.833 84.4

Indicators of credit’s quality

Provision for devaluation on interest-bearing assets as per average volume of loans to customers (gross) 3.3% 2.95%

Provision for devaluation on interest-bearing assets / operating income t before formation of provisions for devaluation 35.3% 32.4%

20

06

20

05

сh

an

ge

, %

chart 8

fees increased by 4.5 times from 592 million tenge in2005 up to 2.678 million tenge in 2006. Such growth isstipulated by income received from JSC Grantum APFsubsidiary as fee on pension assets—879 million tengeand investment profit—292 million tenge in 2006.And also income received by Moskommertsbank fromsyndicated loans arrangement, which amounted to907 million KZT.

Fee expenses. Fee expenses increased by 31.8% inthe year of 2006 up to 1.672 million tenge from1.269 million tenge in 2005. The largest share (41.4%or 692 million KZT) in total amount of fees paid com-prise fees on bank cards service, which in compari-son to the year of 2005 increased by 47.9% due toincrease of operations volume on bank cards.Besides that, 28.3% of total fees expenses compriseexpenses on insurance activity, which in compari-son to 2005 increased by 28.8%, that is because ofrequirements on additional costs while effectinginsurance activity. Other paid fees decreased by1.4% from 141 million tenge in the year of 2006 to139 million tenge in 2005, the major share of whichcomprises the payment for rating services (92.5%).

Net income on marketable securities throughincome and losses increased by 5.4 times from 849 mil-lion tenge in 2005 up to 4.545 million tenge in 2006.This growth took place on operations with derivedfinancial instruments in foreign currency. In the firstquarter of 2006 the Bank carried out borrowings ineuro and Singapore dollars. As a result of significantstrengthening of euro and Singapore dollar during2006 there was a significant income from reappraisalof these derived financial instruments.

Within the year of 2006 net income on operationswith foreign currency, securities and precious met-als increased by 3.4 times from 1.591 million tengein the year of 2005 up to 5.403 million tenge in 2006.In the net income from dealing operations theincome share from operations with foreign curren-cy comprises 99%, or 4,392 million tenge out of4,435 million KZT. The growth of income from deal-

increased range of the Bank’s products and theincrease of total volume of the Bank’s operations.Besides , the results of work of Pension Fund andPension Assets Management Company affected theincrease of fees in 2006. The structure of fee income incomparison with 2005 did not change, still the majorshare of fees had been received for payments servicesfrom individuals and for settlement and documentaryoperations, their share amounted to 58.8% in 2006 incomparison with 69.2% in 2005. Also in 2006 the feeson cards operations increased by 54%, comparing tothe year of 2005, which is explained by further expan-sion of the Bank’s card operations. Fees on foreignexchange and securities operations increased by86.8%, or by 1.9 times in comparison with 2005. Thegrowth is generated by the increase of volume of oper-ations with non-cash foreign exchange. Other Bank’s

ii.28

jsc kazkommertsbank annual report | 2006

ii.29

jsc kazkommertsbank annual report | 2006

kazakhstan—unexplored wealthkazakhstan—unexplored wealth

Marketable securities and investments in securities Period ended 31 December

Million KZT Share, % Million KZT Share, % Changes

Net income (loss) on marketable securities through incomeand losses 4,545 15.7 849 5.8 435.3

Net income (loss) on foreign exchange, securities and precious metals transactions 5.403 18.7 1.591 10.9 239.6

Income on services and commissions received 17.537 60.5 10.684 73.3 64.1

Expenses on services and commissions paid (1.672) (5.8) (1.269) (8.7) 31.8

Net income on trading assets 29 0.1 12 0.1 141,7

Received dividends 83 0.3 10 0.1 730

Other incomes 3.042 10.5 2.690 18.5 13.1

Net non-interest income 28.967 100.0 14.567 100.0 98.9

Net non-interest income / net income 97.9% 73.5%

Net commission income / operating incomebefore formation of provision for devaluation 17% 17.1%

Net fee income/average volume of assets 1.1% 1.2%

Net non-interest income / operating income before formation of provision for devaluation 31.1% 26.4%

20

06

20

05

chart 9

сh

an

ge

, %

tion systems, into development and implementa-tion of new banking products.

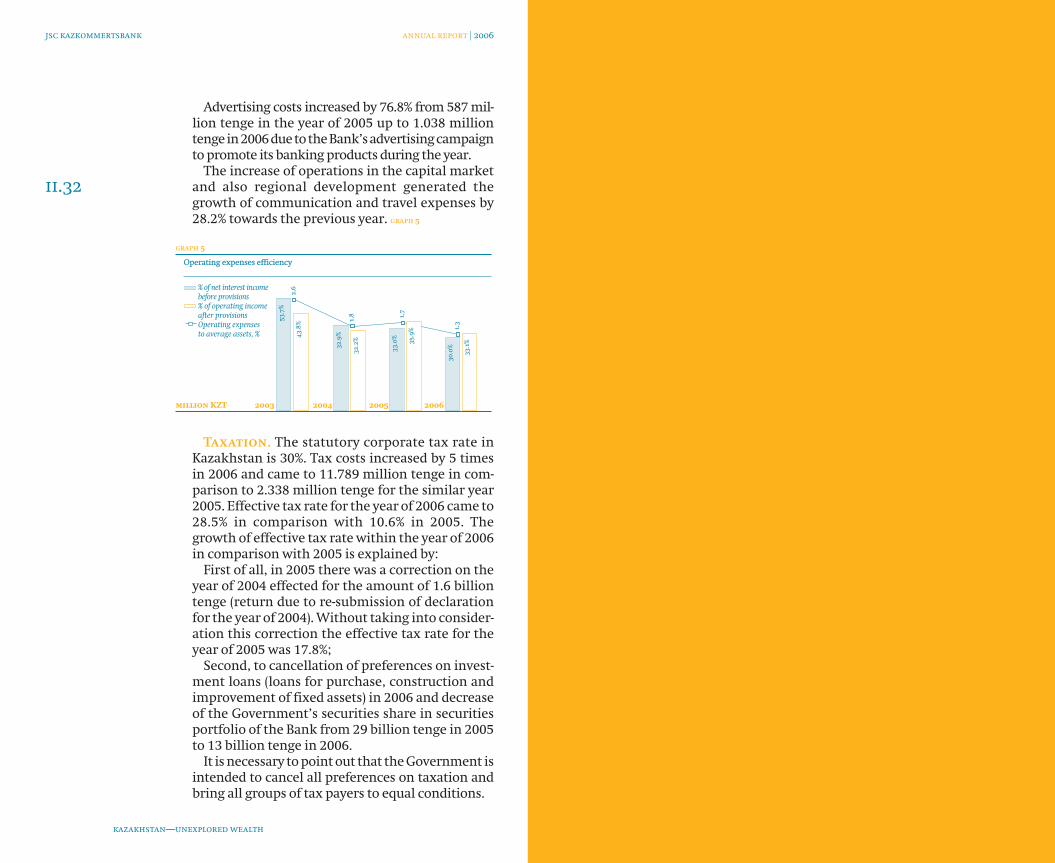

Operating expenses of the Bank increased by 34.9%in the year of 2006 in comparison to 2005 (from13.368 million tenge up to 18.039 million tengerespectively). However as a result of sufficient growthof operating income the coefficient of operatingexpenses towards operating income after accrual ofprovisions on possible loan losses in 2006 decreasedto 30.0% in comparison to 35.9% in 2005. At that,interest share of operating expenses from averageassets decreased for periods analyzed to 1.3% from1.7% respectively.

Basic part of operating expenses of the Bank arestaff costs, which in the year of 2006 comprised50.7% from total operating expenses in comparisonto 48.8% in 2005. The increase is stipulated by thegrowth of the number (+40% to the last year, mainlydue to enlarging of subsidiary network) and increasein salaries in accordance with market conditions.

In the year of 2006 amortization deductionsincreased by 17.2% and came to 1.833 million tengecompared to 1.564 million tenge in 2005. Thisincrease is connected to the Bank’s investments intocustomer service network. Thus, the volume of aver-age fixed and non-tangible assets in the year of 2005increased by 49.3% in comparison to the volumes in2004.

Current expenses for maintenance of fixed assets,which include expenses on maintenance and repairof owned and rented buildings, furniture, comput-ers and other equipment, on maintenance of soft-ware, expenses for property insurance, rent andsecurity of premises, in the year of 2006 came to2.183 million tenge compared to 1.475 milliontenge in 2005, having increased by 48%.

Taxes and dues paid by the Bank for the years2006 are higher than in the last year, increase by33.8%. In total amount of these expenses 52.5%comprises the value added tax, 33%—fees intoKazakhstan Investments Guarantee Fund (of insur-ance) and 14.5%— other taxes and dues.

ing operations with foreign currency came to 2.2times or the increase from 2,019 million tenge up to4,392 million KZT. The income growth in the year of2006 in comparison to 2005 can be explained by theincrease of dealing operations volume in 3.9 times.

Received dividends. In the year of 2006 the Bankreceived dividends on the stocks of the trade securi-ties portfolio in the amount of 83 million tenge (stocksof Kazakhtelecom, Kaztsink, JSC UKTMP) in compari-son to 10 million tenge in 2005 (stocks of Kazakhmys).

Net income on withdrawal of investments avail-able for sale increased by 2.4 times from 12 milliontenge in 2005 up to 29 million tenge in 2006.

Other income. In the year of 2006 the Bank receivedother income in the amount of 3.042 million tengeagainst 2.690 million tenge in 2005, the growth cameto 13.1%. Insurance premiums of JSC “KazkommertsPolicy” are the major article of other income, despitethe fact that their share in other income decreased andcame to 80.6% in 2006 in comparison to 89% in 2005.Insurance premiums increased from 2.394 milliontenge in 2005 up to 2.451 million tenge in 2006(growth by 2.4%), which in the Bank’s opinion is aresult of continuing development of Kazakhstaninsurance market.