© 2013 IBM Corporation1 Business Partner CoMarketing Center Training (CMC) 2013.

Upload

praneeth-kumar-v-rCategory

view

44download

2

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

INDUSTRY PROFILE

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 1

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

INTRODUCTION ABOUT FINANCIAL INSTITUTIONS: The financial institutions are also known as ‘Development Banks’.

Development banks are those financial institutions, which provide term finance, promote

entrepreneur, and enhance organizational effectiveness and upgrade know-how and do-

how. They provide either loan or equity capital or both, as also advisory, promotional and

entrepreneurial services.

The first development bank was the Industrial Development Bank of Japan

established in 1902. Initially, it provided ship mortgage loans. After 1927, it started

financing small-scale industries. But it was after the Second World War, it started

functioning as a development bank in the modern sense of the term. Development Banks

were also started in a number of developed and developing countries in the post-war era.

The Asian Development Bank came into existence in 1967. The first development bank

in India was the Industrial Finance Corporation (IFC) established in 1946.

DEVELOPMENT BANK IN INDIA: There are three types of development banks in India. Firstly, there are

Development Banks for agriculture at local, state and national level. They are Primary

Land Development Banks, state / Central Land Development Banks and NABARD.

Secondly, there are Development Banks for industry at the National and State

level. At the national level are included -

Industrial Development Bank of India (IDBI),

Industrial Credit and Investment Corporation of India (ICICI),

Small Industries Development Bank of India (SIDBI),

Industrial Reconstruction Bank of India (IRBI),

Risk Capital and Technology Finance Corporation (RCTFC),

Technology Development and Information Company of India (TDICI),

Shipping Credit and Investment Corporation of India (SCICI) and

Tourism Finance Corporation of India (TFCI).

At the same level are

‘State Financial Corporations (SFCs) and

State Industrial Development Corporations (SIDCI).

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 2

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE Thirdly, there is the Export-Import (EXIM) Bank of India for the foreign sector.

STATE FINANCIAL CORPORATION (SFCs) State Financial Corporations are the state level development banks for the

development of small and medium scale industries in 18 states of India. They aim at

bringing about balanced regional development by wider dispersal of industries,

promoting greater investment and generating larger employment opportunities. Besides

their paid-up capital, State Financial Corporations augment their funds by borrowings

from Governments, RBI, SIDBI and Banks and by way of Bonds / Debentures, by

accepting Deposits and sale of Investment in shares and debentures of industrial

concerns.

FUNCTIONS:

State Financial Corporations perform the following functions:

1) They provide financial assistance to industries by way of term loans, direct

subscription to equity / debentures, discounting of bills of exchange and providing

guarantees.

2) They meet the term loan requirement of small and medium scale industries for

acquisition of fixed assets like land, building, machinery and equipment.

3) They provide loans for setting up new industrial units as well as for expansion

and modernization of the existing units.

4) They also promote the development of medium and small-scale industries in

backward areas of the country.

5) Under the special capital scheme, SFCs provide equity type support up to Rs.4

lakhs on short terms to entrepreneurs for bridging the gap in equity or promoters

contribution, entrepreneurs with viable projects but lacking adequate own funds

are assisted under the scheme.

6) SFCs operate a number of schemes on behalf of the SIDBI. These include

schemes for women entrepreneurs, modernization scheme, equipment finance

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 3

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE scheme, schemes for hospitals and nursing homes, scheme for ex-servicemen,

single window scheme and special capital/seed capital schemes, etc.

NUMBER OF STATE FINANCIAL CORPORATIONS: At present there are 18 SFCs in the country, 17 of which were set up under the SFCs Act 1951.Tamil Nadu Industrial Investment Corporation Ltd. Set up in 1949 under the Companies Act as Madras Industrial Investment Corporation also functions as a full-fledged SFC.

1) Andhra Pradesh State Financial Corporation

2) Assam Financial Corporation

3) Bihar State Financial Corporation

4) Delhi Financial Corporation

5) Gujarat State Financial Corporation

6) Haryana Financial Corporation

7 Himachal Pradesh Financial Corporations

8) Jammu & Kashmir State Financial Corporation

9) Karnataka State Financial Corporation

10) Kerala Financial Corporation

11) Madhya Pradesh Financial Corporation

12) Maharashtra State Financial Corporation

13) Orissa State Financial Corporation

14) Punjab Financial Corporation

15) Rajasthan Financial Corporation

16) Tamil Nadu Industrial Investment Corporation Ltd.

17) Uttar Pradesh Financial Corporation

18) West Bengal Financial Corporation

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 4

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

COMPANY PROFILE:- Introduction:- Karnataka state financial corporation is a state level financial institution

established by the State Government. Today, while the state economy is making rapid

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 5

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE strides in the global market, KSFC is moving in tandem. As a pioneering and

responsive financial institution, KSFC is fine tuned to fulfill the plans and aspirations

of entrepreneurs by extending all possible assistance.

Amendments to the State Financial Corporation Act provide for wide ranging

scope of assistance and operational flexibility. Keeping this in view, KSFC has

reengineered itself to ensure utmost customer satisfaction with new energy, thrust and

speed.

In the 47 year of existence, KSFC has contributed most significantly for the

growth of Small-Scale Industries, backward area development and promotion of first

generation entrepreneurs. Its achievement in these areas is unparalleled.

KSFC, as ISO 9001:2000 certified organization is proud to have played a

major role in the industrial development of the state. It is also the proud privilege of

KSFC to have assisted many industries that are internationally recognized like the

INFOSYS, BIOCON, etc.

Origin and Growth:- KSFC was established by the Karnataka State Government in the year 1959

under State Financial Corporation Act 1951 for extending the financial assistance for

setting up of tiny, small and medium scale industrial units in the state. Since then it has

been working as a regional industrial development Bank of Karnataka.

KSFC has a decentralized system of working. Term loan up to Rs.50.00 lakhs

are sanctioned at branch offices and loans over Rs.50.00 lakhs are processed and

sanctioned at the Head office.

KSFC has branches all over the state. Each district has a branch office. In all,

KSFC has 7 zonal offices, 3 supers A grade branch offices, 12 A grade branch offices

and 14 B grade branch offices.

KSFC extends term loans to new units up to Rs.500.00 lakhs for corporate

bodies and registered co-operative societies. Term loans up to a maximum of Rs.200.00

lakhs are sanctioned to propriety, partnership and Joint Hindu Family concerns. KSFC

gives term loans jointly with Karnataka State Industrial Investment Development

Corporation (KSIIDC) and commercial banks for projects up to RS.20.00 Crore.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 6

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE SCOPE OF KSFC:-

The scope of operation of Karnataka State Financial Corporation is confined

essentially to small and medium scale enterprises and it is constrained from granting

loans to concerns whose paid up capital and reserves together exceeds Rs.20 crore.

Their aggregate contingent liabilities arising from guarantee and under writing

arrangements should not ordinarily exceed twice their paid up capital and reserves, which

can extend up to Rs.12 Crores with the prior approval of the Government. Moreover,

KSFC holding company’s share capital should not exceed 30% of the subscribed capital

of their company or 10% of its own paid capital and reserves whichever is less. It is also

prohibited from financing a concern in which its directors have interest.

KSFC is also authorized to act as the agent of Government both at central and

state level, with any financial institutions like Industrial Development Bank of India

(IDBI), Industrial Financial Corporation of India (IFCI) etc, in matters connected with

grant of advances or subscription.

CORPORATE MISSION:-

KSFC’s corporate plan strategy for resource raising and creating competitive

advantage revolves around an organization mission is based on a clear identification and

perception of KSFC’s core competencies. They are:

1) Reach and cover the entire state of Karnataka.

2) Knowledge of suitability for each region in the state in terms of infrastructure

and natural resources, existing level of industrialization and entrepreneurship.

3) Building a body of multi disciplinary professionals.

4) Specialization in the appraisal, monitoring and recovery of loans of SSI/MSI

and other new fund based and fee based activities. A deep routed commitment

to the development of entrepreneurs and SSI’s.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 7

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

MISSION:- “To be a premier, self sustained financial institution for catalyzing, creating and

sustaining viable investment in the small scale and medium sector of industry and

services and the financial sector in the state of Karnataka”.

VISION:-

Vision of KSFC is to be a premier financial institution in the country, by

providing effective and efficient service to all sectors of people under one roof. Its vision

is “ALL FOR ONE AND ONE FOR ALL”.

GOAL:-

‘OVERALL DEVELOPMENT OF SMALL SCALE AND MEDIUM SCALE INDUSTRIES’

QUALITY POLICY:- KSFC endeavors to create satisfied customers through

adequate and timely financial assistance and guidance. This aim is achieved through

professional management and teamwork.

QUALITY OBJECTIVES:

1) To ensure satisfaction through teamwork and professional management.

2) To extend effective guidance through entrepreneurs for successful

accomplishments of their business.

3) To provide good quality of service on a continued basis to the satisfaction of the

customer.

4) To attain specified level of performance every year and to ensure compliance with

statutory and regularly requirements.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 8

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE 5) To encourage everyone in the organization to upgrade and enhance their skill and

knowledge with appropriate training for improving quality of service to the

entrepreneur.

PURPOSE OF ASSISTANCE:-

The corporation extends financial assistance for acquiring fixed assets like land,

building, plant and machinery and miscellaneous assets required for the project.

However, the corporation also extends working capital under Single Window Scheme to

new units and corporate loan to the existing good units to meet short-term gap in working

capitals requirements.

LIMIT OF ACCCOMODATION:-

The following are the maximum limits of loans that could be availed by entrepreneurs:

Category Maximum loan

01 – Proprietary/partnership Rs.200 lakhs

02 - Corporate bodies (private/public limited)

& registered Co-operative societies Rs.500 lakhs

Note:

In respect of both the categories mentioned above, the minimum loan that could

be sanctioned by the Corporation is Rs.5.00 lakhs. Loan below Rs.5.00 lakhs is

not sanctioned by the Corporation excepting transport loans.

In respect of existing units (category 02 only) operating successfully, maximum

limit can be extended to Rs.1000.00 lakhs depending on the merits of the case

with prior approval of the Small Industries Development Bank of India (SIDBI)

In respect of category 02, the financial assistance can be granted provided the

paid- up capital and free reserves does not exceed Rs.20.00 crore.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 9

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE If the requirement of funds for a project is substantial & cannot be extended by

the Corporation singly, then the requirement of loan of such projects can be made

in consortium with Karnataka State Industrial Investment Development

Corporation (KSIIDC) / BANKS.

LENDING POLICY OF THE CORPORATION:-

The Corporation formulates lending policy at the beginning of the each year.

The loans are given based on the lending policy of the Corporation. The lending policy

covers various aspects like exposure to the group, thrust sectors, sectors in the negative

list (loans are not granted to such sectors). The industrial policy of the state and central

government is taken into account while formulating the lending policy of the

Corporation.

SCHEMES:-

Today, the Karnataka state financial corporation is one of the leading State

Financial Corporations in the country. With a branch network of 29 offices spread

throughout the state of Karnataka. KSFC is a fine tuned, well known organization to meet

the demanding challenges of entrepreneurs, both big and small.

Though, the performance indicators of the corporation have shown a small

slump in the recent years, it is more on account of the bearish forces of the Indian

economy. However with the unprecedented growth in the services and the IT sectors, and

the state of Karnataka advantageously placed in these sectors, the corporation is making

good headway and has potential for a steady growth.

KSFC has evolved loan schemes for extending financial assistance to suit

almost all kinds of industrialist's entrepreneurs and technocrats. KSFC has also evolved

loan schemes for extending financial assistance to service sectors like Hotel and Tourism

related Industry, Industrial Estates, Hospitals, Nursing homes etc.

SERVICE NETWORK:- KSFC services the nook and corner of Karnataka with its extensive network of 7 Zonal offices, 3 super “A” Grade Branch offices, 12 “A” Grade Branch offices and 14 “B” Grade Branch offices with an empowered and decentralized administrative system.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 10

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

ZONAL OFFICES: 1) Bangalore Rural Zone 5) Belgaum

2) Mysore 6) Davangere

3) Mangalore 7) Dharwad

4) Gulbarga

SUPER ‘A’ GRADE BRANCH OFFICES

1) Bangalore M.G. Road Branch

2) Bangalore Jayanagar Branch

3) Bangalore Rajajinagar Branch

‘A’ GRADE BRANCH OFFICES:

1) Bangalore Rural 7) Mangalore

2) Belgaum 8) Hassan

3) Dharwad 9) Mandya

4) Mysore 10) Kolar

5) Gulbarga 11) Bellary

6) Tumkur 12) Udupi

‘B’ GRADE BRANCH OFFICES:1) Shimoga 8) Madikeri

2) Chitradurga 9) Haveri

3) Bijapur 10) Bagalkot

4) Raichur 11) Davangere

5) Bidar 12) Gadag

6) Karwar 13) Chamarajnagar

7) Chikmagalur 14) Koppal

AREA OF OPERTION:-

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 11

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE The area of operation covers the entire state of Karnataka. KSFC has branches

in all the district headquarters. The industrial units / service sectors established or to be

established within the state only are eligible for assistance. The branch offices of the

corporation are adequately delegated with powers of sanction and disbursements.

Requirements of financial assistance up to Rs.50.00 lakhs are handled by the concerned

branch office. If the requirement of loan is more than Rs.50.00 lakhs, entrepreneurs will

have to approach the head office.

The schemes formulation by the corporation:

Bridge loan against state subsidy (highly restricted )

Acquisition of private vehicles.

Corporate loans

Equipments Lease Financial and Hire Purchase (ELF & HP)

Merchant Banking and Financial services

Rental Discounting scheme

Acquisition of Existing Assets/ Enterprises

Financial Assistance to Entertainment Industry

SERVICE NETWORK IN KARNATAKA:

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 12

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

PEOPLE : The prime asset of KSFC

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 13

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE KSFC has professional team of experts drawn from various disciplines lead by

illustrious leadership of senior IAS officer. The personnel of KSFC are top rated

Managers, Engineers, Financial Analysts, Market Researchers, Statisticians, Economists

and Information Technologists. It is this team of professional wizards, which is the

backbone of this mighty organization.

FINANCIAL SERVICES:-

KSFC is a financial super market. It extends all types of financial assistance in

the form of long-term loans, short term loans (in the form of corporate loans), Lease

finance, Hire purchase finance, Merchant Banking and financial services etc. KSFC’s

assistance covers almost all types of industrial and service sectors.

KSFC is a category one merchant banker as approved by Securities and

Exchange Board of India (SEBI). The Merchant Banking Division takes up management

of public issues, DPG, Syndication of loans, Bills Discounting etc. The other activities

are subscription to the non-convertible debentures and factoring services.

AWARDS AND RECOGNITION

ISO CERTIFICATION:

During the year, the corporation obtained the ISO 9001:2000 recertification’s to

the revised standards from M/s Bureau of Indian standards for a further period of 3 years.

Plans are on the avail to extend ISO certification to branch offices in a phased

manner. In the first phase, super ‘A’ grade branch offices are proposed to be taken up in

the ensuring year.

INSURANCE ACTIVITY:

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 14

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE The corporation has taken corporate agency with IFFCO-TOKIO General

Insurance limited for distribution of Non- life insurance products.

IFFCO-TOKIO has awarded KSFC the certification of excellence for

outstanding performances as a service provider in the year 2004-05.

The corporation insured assets in respect of 4,831 cases and mobilized a

premium of Rs.166.39 lakh under general insurance up to March 2007.

BUDGETARY PROVISION: The Government of Karnataka has consented and committed to fund simple

interest in respect of small loans upto Rs. 10.00 lakh which have become Non-

Performing Assets as on 01-04-2006. A budgetary provision of Rs.54.00 crore has been

made for the financial year 2007-08. Provision regarding NPA is considered after taking

credit for this amount.

ACTIVITIES OF KSFC:

KSFC PARTICIPATION IN VISION 2006 INDUSTRIAL EXHIBITION

Small Industries Service Institute (SISI) Bangalore, Indian Lighting Engineers

(ISLE) Bangalore and Karnataka Small Scale Industries Associations (KASSIA)

Bangalore had jointly organized VISION 2006 Lighting & Allied Electrical Products

Industrial Exhibition cum Vendor Development Programme at SISI Campus, Rajajinagar

Industrial Estate. Bangalore from 9th to 11th December 2005.

The objective of the programme was to showcase the potential of small and

medium enterprises and focus the needs of large-scale industries, government

departments, public sector undertakings etc for lighting and allied electrical products,

automobile and solar lightings etc.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 15

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE About 20 industries engaged in the manufacturing /trading of lighting and

allied electrical products and solar lighting participated in the exhibitions. Karnataka

State financial Corporation took up a stall in the exhibition. KSFC participated in the

exhibition and actively propagated its products and services.

PARTICIPATION IN THE 5 TH INTERNATIONAL RICE TECH EXPO

RICE TECH EXPO- Bangalore, the 5th International Exhibition and conference

on Rice Processing Technology was organized by Shiny Trade Expositions (Rice mill

reporter publications Group, Vijay Wada) at Palace Grounds, Bangalore from 9th to 11th

December 2005.The main theme of the exhibition was to create awareness on new

processing and marketing strategies among the rice industry entrepreneurs.

More than 60 industries are engaged in the manufacture of rice milling

machinery. Karnataka State Financial Corporation participated in the exhibition and

actively exhibited its products and services. There were large number of visitors from

Karnataka and neighboring States.

WORKSHOP ON ‘ACCESSS TO FINANCE FOR WOMEN ENTERPRENEURS’:

AWAKE & FICCI Ladies Organization have jointly organized a two day

Workshop on ‘Access to finance for women entrepreneurs’ at Hotel Atria, Bangalore on

2nd and 3rd December 2005.

Nearly 70 entrepreneurs and 34 executives from different banks and financial

institutions participated in the workshop. The workshop was organized with the

objectives;

To improve access to finance for women entrepreneurs

Awareness on the various schemes and policies.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 16

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE To bring about better understanding between bankers and women entrepreneurs.

In this workshop Mr. Ratna Ravikumar represented the KSFC

Seminar on Development of Women Entrepreneurs in the State of Karnataka .

SISI (Small Industries Service Institute), Bangalore in association with SIDBI

and AWAKE has organized a seminar on Development of Women Entrepreneurs in

Karnataka at the SISI campus on 3-1-2006. Besides members of AWAKE and other

women entrepreneurs the meet was attended by representatives of Government

Departments and agencies like Industries and Commerce, Women and Child welfare,

KCTU, TECSOK, CEDOK, NABARD, KSFC,KVIB, KVIC etc. Sri. S. Prabhu, Asst.

General Manager (BD & CR) represented KSFC in the meet and addressed the

participants.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 17

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

SERVICES OFFERED BY KSFC

EQUIPMENT LEASE FINANCE :

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 18

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE Industrial units working profitably can avail services of plant and machinery on

lease without making investment or incurring debt obligation and become more

competitive and efficient. The minimum assistance under the service is Rs. 5 lakhs. The

applying unit should be in production for the last 2 years, earning profits and regular in

repayment to financial institutions.

HIRE PURCHASE :

This scheme provides for a fast, easy alternative to ready cash. Industrial

concerns in commercial production for 2 years and earned profits and are regular in their

repayments to financial institutions can avail the assistance.

MERCHANT BANKING SERVICES:

KSFC has been approved as a category 1 merchant banker by the Security

Exchange Board of India (SEBI) and takes up management of public issues, under

writing of shares, deferred payment guarantees project report preparations, syndication of

loans, pre-issue appraisals, opening foreign letter of credit.

MUTUAL FUND ACTIVITIES:

During the year of 2006-07 the Corporation entered into MoU (Memorandum

of Understanding) with UTI for marketing of Mutual Fund products of UTI. Though, this

activity was started in the last quarter of 2006-07, mutual fund products of Rs. 138.49

lakh were marketed.

CONSULTANCY SERVICES:

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 19

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE The Corporation is also hopeful of earning sizeable income by undertaking the

consultancy services of various works of Municipal Corporations like BBMP, HDFC,

MMP, etc.

DIFFERENT TYPES OF INDUSTRIES COVERED BY KSFC:

Basic Metal

Beverages

Chemical and Chemical products

Coal

Electric machinery

Electric, gas and steam

Fishing

Food excluding Beverages

Footwear and other wearing apparel and made up textile

goods

Furniture and Fixtures

Hotels

Houseboats

Industrial Estates

Leather, leather and furniture products

Machinery excluding electric machinery

Manufacture of textiles

Transport

Various Sectors Covered by KSFC:

Public Sector

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 20

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE Partnership Firms

Co-operative Sector

Private Sector

Joint Hindu Family

Proprietary Concern

From the above, it’s clear that a very important role is played by KSFC. Similar to

the commercial banks, if the State Financial Corporations too had oriented and limited

themselves to bigger and profitable undertaking established by the second and third

generation entrepreneurs, then the bulk of the Small and Medium Enterprises (SME)

segment had to fend for itself with deleterious economic and social consequence.

SCHEMES OF THE CORPORATION:

General scheme:

The corporation extends financial assistance for new enterprise to establish

SSIs / MSIs/ service units for expansion, modernization, diversification etc., by the

existing units to meet a part of cost of land, building, plant and machinery and other fixed

assets.

National Equity Fund Scheme (NEFS):

This scheme provides equity type of assistance (soft seed capital) upto RS.10.00

lakhs to small entrepreneurs for existing and new projects in the tiny, small scale, service

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 21

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE sectors and for rehabilitation of potentially viable sick SSI units. The ceiling on project

cost is Rs.50.00 lakhs and the promoter's contribution is 10% of the project cost

(including working capital margin). While the equity type of assistance (SSC) carries

interest at 5% p.a. the term loan carries normal rate of interest. A net interest rate works

out to 9.69% for loans below Rs.25 lakhs and 10.35% for loans above Rs.25 lakhs.

Mahila Udyam Nidihi Scheme (MUNS):

This scheme is meant for extending financial assistance for first generation

women entrepreneurs to set up SSI units. The scheme provides equity type assistance

(soft seed capital) along with term loan for existing and new projects. The ceiling on the

project cost is Rs.10 lakhs and the minimum equity assistances Rs.2.50 lakhs, which

attracts 1% service charge only p.m. The term loan component carries normal rate of

interest. The women entrepreneurs who seek assistance under this scheme should possess

managerial and necessary skill to run the unit and shall be the chief promoters of the

proposed unit.

Scheme for Technology Upgradation for Textile Industries (TUFs):

The objective of the scheme is to provide encouragement for Textile Industries

(including cotton ginning pressing units) in the small scale industrial sector for

technology upgrading and to modernize their production facilities. The scheme covers

projects costing Rs.5 lakhs to Rs. 50 lakhs. New and existing units are eligible for this

assistance. The prevailing of interest as applicable to SSI is charged. The present lending

rates are 11.00% p.a. and 11.50% p.a. for loans below Rs. 25.00 lakh and above Rs.25.00

lakh respectively.

Credit Linked Capital Subsidy Scheme (CLCSS):

The objective of scheme is to facilitate technology upgradation of SSI units or

SSI units graduating to MSI in specified products / sub-sectors by providing 15% with

maximum subsidy amount of Rs.15.00 lakhs and investment limit to Rs.100 lakhs on the

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 22

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE loan given for machinery. Existing SSI units registered with the State Directorate of

Industries who upgrade with the state of art technology, with or without expansion are

eligible.

Technology Development and Modernization Fund Scheme (TDMF):

To encourage small and medium scale entrepreneurs and to upgrade the

technology and modernise their existing production facilities the Government of

Karnataka has come up with an interest subsidy scheme. The scheme is applicable to the

units financed by KSFC and KSSIIDC only. Existing units who are in operation for at

least 3 years and who are not default to institutions/ banks in payment. Units graduating

from SSI to MSI sector and service sector are also eligible. For availing loan under

TDMF, the project cost shall not exceed Rs.100.00 lakhs. The scheme envisages

reimbursement of 4% interest p.a. as a interest subsidy on the term loan availed from the

Government of Karnataka.

Single Window Scheme (SWS):

This loan scheme is for providing assistance to new tiny and small units whose

project cost (excluding working capital margin) does not exceed Rs.50.00 lakhs and the

total working capital requirement at the normal level of operation is up to Rs.20.00 lakhs.

Term loan on fixed assets and term for working capital is sanctioned based on the debt

equity ratio of 2:1 for loan above Rs.10.00 lakhs and 3:1 for loan up to Rs.10.00 lakhs.

Corporate Loan Scheme (SLS):

The objective of the scheme is to extend short – term loans to the existing

successful units who require urgent working capital funds either to meet the gap in the

working capital requirement or funds required for developing / expanding new market

and opening Letter of Credit for purchase of new equipment till term loan is sanctioned

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 23

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE and released. The repayment period does not exceed 30 month including moratorium

period of 6 months. The corporate loan is restricted normally to the manufacturing sector.

Rental Discounting Scheme:

The objective of the scheme is to provide financial assistance on the strength of

future rental to be earned by non residential proportion located within the city and

municipality limits of Bangalore, Mangalore, Hubli- Dharwad, Gulbarga, Shimoga -

Bhadravathi, Mysore and Belgum subject to gross rent earning of not less than Rs.

25000/- per month.

Foreign Letter of Credit (FLC):

KSFC has been operating the scheme of opening Foreign Letter of Credit for

importing the capital goods through commercial bank exclusively for our borrowers since

1995. The scheme is operated in the Hire Purchase and Financial Service department of

head office.

INSURANCE :

KSFC has entered into a strategic alliance with IFFCO-TOKIO General

Insurance Company to market the Non Life Insurance Products. This would enable the

clients of KSFC to have credit and the insurance under one roof. The premium tariffs

applicable are same as the other insurance companies and at no extra service charges. An

exclusive Insurance Cell with well-trained staff is in operation at Head office. The details

of the general perils covered are:

Fire, Earth quake, Burglary, Machinery breakdown

Marine, Household insurance, Cash safe / transit

Fidelity guarantee, Bankers indemnity, Vehicle insurance

Medical insurance, Personal accident cover

Electronic equipment, Trade and office

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 24

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE Life Insurance Corporation:

An MoU (Memorandum of Understanding) was signed with Life Insurance

Corporation of India in March 2007 for marketing of LIC products.

INFRASTRUCTURE DEVELOPMENT ACTIVITY: Infrastructure is an integral part of the services sector and plays a crucial role in

the industrial development. The services sector has emerged as one of the major

contributors to the country’s GDP growth rate. Inadequacy in infrastructure stunts

economic development. There is now a wide spread consensus that exclusive dependence

on government for provision of all infrastructure services is not feasible and private

public participation is essential for realising optimal outcomes in the sector. Recognizing

this, the Corporation has taken up infrastructure development projects with public /

private participation. The Corporation’s initial focus is to identify valuable vacant lands

in the prime localities in and around the Bangalore city, owned by various government

departments / agencies / registered societies / trusts, etc., including SEZs and explore

joint development ventures.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 25

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

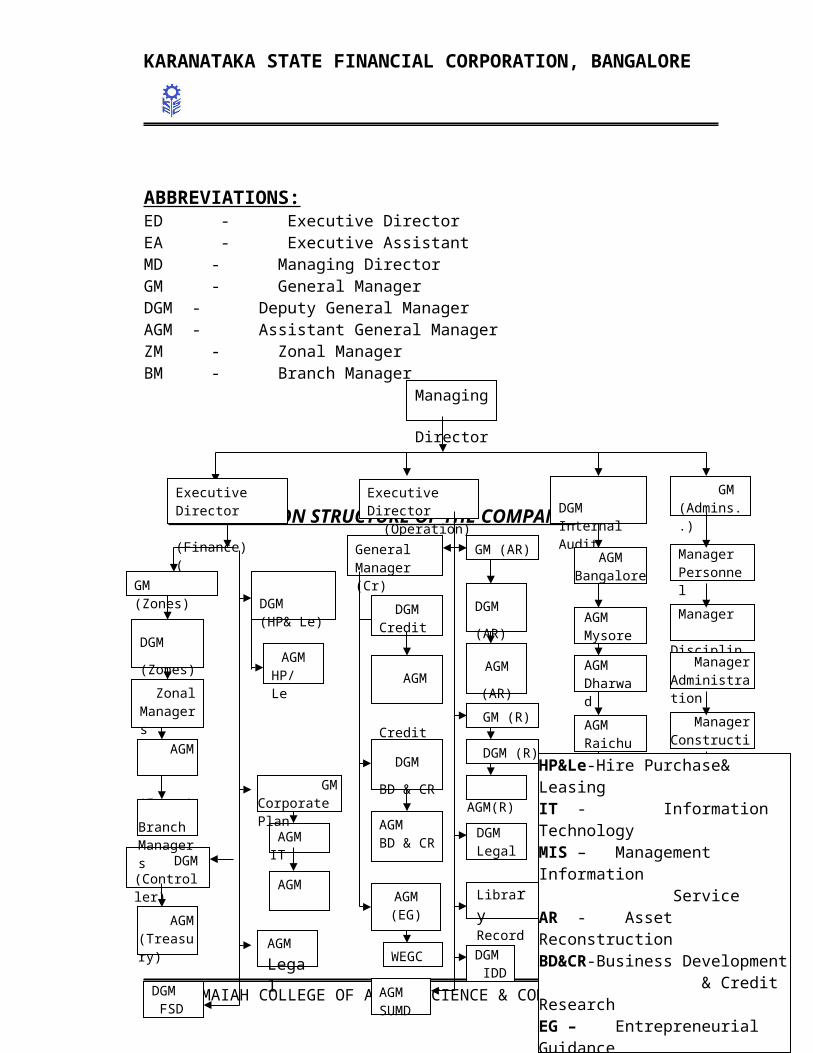

ORGANIZATIONAL STRUCTURE:

KSFC has extensive network office encompassing entire Karnataka. KSFC

serves every nook and corner of Karnataka with its network of 7 zonal offices, 3 super A

grade branch offices, 12 A grade branch offices and 14 B grade branch offices with an

empowered and decentralized administrative system. It is the only term lending financial

institution in the Karnataka with such a widespread network.

Board of Directors of KSFC is headed by the Chairman and the Managing

Director is appointed by state Government. The head offices of the organization have

divisional structures. It has 15 divisions. To assist Managing Director, KSFC has 2

executive director (Finance and Operation) and 6 General Managers-Corporate planning,

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 26

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE Credits, Recovery, Zonal offices, Administration and Asset Reconstruction. At the senior

management level DGMs, AGMs with a legal Advisor and 2 Additional Legal Advisor

are functioning. Managers and Deputy Managers are executing the policies at the middle

level.

Zonal offices and Super A grade branches are headed by DGMs, grade

branches are headed by AGMs. Managers head all B grade branches.

ABBREVIATIONS:ED - Executive DirectorEA - Executive AssistantMD - Managing DirectorGM - General ManagerDGM - Deputy General ManagerAGM - Assistant General ManagerZM - Zonal ManagerBM - Branch Manager

ORGANIZATION STRUCTURE OF THE COMPANY:

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 27

Managing Director

Executive Director (Finance)(

Executive Director (Operation)

DGM Internal Audit

GM(Admins..)

DGM(Controller)

DGMCredit

GM (AR)

AGM IT

AGMHP/ Le

DGM

(Zones)

AGM(Treasury)

AGM

Credit

DGM

(AR)

AGMSUMD

Manager Personnel

DGM(HP& Le)

DGM

BD & CR

AGM

(AR)

AGM(R)

AGM MIS

AGMBD & CR

GM (R)

General Manager (Cr)

AGM(EG)

WEGC

DGM (R)

DGMLegal

AGM Legal

Library Records

AGM Bangalore

AGM Mysore

AGM Dharwad

AGM Raichur

Manager PGC

Manager Disciplinary

Manager Administration

Manager Construction

Manager ISO Cell

GM Corporate Plan

ZonalManagers

GM (Zones)

AGM (Zones)

BranchManagers

DGM FSD

DGM IDD

HP&Le-Hire Purchase& LeasingIT - Information TechnologyMIS – Management Information ServiceAR - Asset ReconstructionBD&CR-Business Development & Credit ResearchEG – Entrepreneurial GuidanceWEGC- Women Entrepreneurial Guidance CellSUMD- Sick Units/ Monitoring DepartmentR – RecoveryPGC- Public Grievances CellFSD-Financial Service DepartmentIDD-Infrastructure Development Dept

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

SHARE HOLDING PATTERN

SL.NO PARTICULARS

NO.OF SHARES(in Units)

PERCENTAGE OF HOLDING

1. STATE GOVERNMENT U/S 4(3) (a)U/S 4(5)Special capital issued U/S 4A

51,73,000

5,37,38811,27,500

69.88%

2. IDBI:U/S 4(3) (a)Special capital issued U/S 4A

22,92,692 6,27,500

29.84%

3. Insurance Companies InvestmentTrusts, Other Financial Institutions.U/S 4(3) (c)

16,090 0.16%

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 28

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

4. Public Sector Banks U/S 4(3) (c) 7,900 0.08%

5. Other Parties. U/S 4(3) (c) 2,475 0.03%

TOTAL 97,84,545 100.00

(All Shares have cost of Rs. 100 each)

BOARD OF DIRECTORS:-

SlNo

Name of the Directors

Period

Under section of SFC’s Act-2000

From To1

Sri.N.Gokulram,IAS Chairman21.12.2005 08-04-2007 10(a)

2 a) Sri.V.Umesh,IAS Managing Directorb) Sri.V.Umesh,IAS, Chairman & Managing Director

23.06.2006

09.04.2007

08.04.2007 10(f) 10(a)

3 Sri.M.R.Kamble,IAS 21.04.2007 10(a)

4 Sri.Mohamed Sanaulla, IASSri .Rajakumar Khatri,IAS

09.11.200516.08.2006

15.08.2006 10(b)

5 Sri.O.S.Vinod 10.10.2005 16.05.2006 10(c)

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 29

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

Sri.Ramesh.G.Dharmaji 17.05.2006

6 Smt.Bhama Krishnamurthy 10.02.2006 10(c)

7 Sri.R.K.AbrolSri.H.Suresh Prabhu

24.11.200311.10.2006

10.10.2006 10(d)

8 Sri.P.K.GuptaSri.S.R.Hanchinamani

05.07.200431.05.2007

30.05.2007 10(d)

9 Sri.S.Nagaraju 15.05.2006 10(e)

10 Sri.G.S.Doreswamaiah24.11.2003

10(e)

11 Sri.S.AnanthanSri.Nataraj.V.Angadi

26.11.200527.03.2007

10(e)10(e)

12 Sri. B. R. Jayaramaraje Urs, IAS, MD 05.01.2005 22.06.2006 10(f)

FUNCTIONAL DEPARMENTS OF KSFC

ENTREPRENEUR GUIDANCE CELL:

The function of the department is to guide the entrepreneur regarding matters

like business opportunities, different schemes available, and procedure to be followed to

get the loan, etc. This is the department through which new client come in contact with

Karnataka State Finance Corporation.

PERSONNEL DEPARTMENT:

This department is in charge of recruitment, promotion, job rotation, transfer of

employees, discipline, welfare and industrial relations and pay rolls. In addition, the

department has a human resources department cell, which carries out training and

development work.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 30

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE LEGAL DEPARTMENT:

This department attends to all the legal matters affecting the interest of the

corporations. The basic function of this department is to appraise the project legally

which the entrepreneurs submit for getting the loan.

SICK AND MONITORING CELL:

The cell, which has been formed for rehabilitation of potentially viable sick units,

conduct in depth studies regarding cases referred and assess the eligibility for

rehabilitation assistance,

BUSINESS DEVELOPMENT AND CREDIT RESEARCH DEPARTMENT:

This department conducts research based on several factors and helps the

management to take decisions.

The following are few activities:

Preparation of district profiles with substantial growth potential among the

existing port folio.

Analysis of high default schemes of KSFC and suggest improvement for the

same.

Evaluation of different scheme of KSFC and suggest changes if necessary.

Publishing the KFSC news letters – KSFC NEWS, MAHITI.

HIRE PURCHASE AND LEASING DEPARTMENT:

This department is incharge of leasing and hire purchase activities of

corporation. This department was started with the introduction of the equipment of

leasing finance scheme. KSFC is the first SFC to start this scheme.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 31

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

MERCHANT BANKING DEPARTMENT:

The activities of this department are broadly categorized into fund based and

non fund based services like deferred payment guarantees, public issues, under writing of

shares, project report preparation, syndication of loans, bills discounting etc., are carried

on.

TREASURY DEPARTMENT:

Treasury Department is given important from these recent years onwards

because of the new challenges faced by KSFC in mobilizing its funds in the era of

liberalization. The main function of treasury department is estimation of funds for lower

possible cost.

CREDIT DEPARTMENT:

The main function of the credit department are appraising the projects,

disbursement of funds and monitoring progress during the implementation of the project

and to keep check on cost overruns and to ensure that funds are utilized for the purpose

intended.

RECOVERY DEPARTMENT :

Recovery of loans sanctioned by the corporation and all other related functions

like rescheduling of loan, effective changes in management of assisted companies,

effective take over of default in units and insisting recovery proceedings are the main

functions of recovery department.

MANAGEMENT INFORMATION SYSTEMS DEPATMENT:

This department is solely responsible for providing up-to-date statistical

information of all the branches, departments etc., required by the management.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 32

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

INFORMATION TECHNOLOY DEPARTMENT:

This department was formed to computerize all the records and documents of

KSFC with large-scale computerization. The corporation aims to function as a paperless

office. This department is incharge of developing and managing the Letter Of Credit

(LOC) etc.,

ASSET RECONSTRUCTION DEPARTMENT:

The asset reconstruction department at the head office is formed to review the

chronic section 29 cases, DC referred cases and suit filed cases. This department verifies

all the cases under review and occupies defaulting units and takes steps to recover the

loan by step to step by selling the units.

APPRAISAL, DISBURSEMENT AND MONITORING DEPARTMENT:

The main functions of this department are to appraise the projects,

disbursement of funds to the loans and to monitor progress during the implementation of

the project and to keep a check on cost over runs and to ensure that funds are utilized for

the purpose intended.

FINANCE AND ACCOUNTS DEPARTMENT: This department is responsible for maintaining various accounts, ledger,

cashbook and other books of accounts, income tax filling of statutory returns and

statements.

INTERNAL AUDIT DEPARTMENT: Auditing of books of accounts, verifying title deeds of properties offered as

securities, business adhered to follow up for compliance of

observations/recommendations made in reports of Statutory Authority and SIDBI’s

inspection report will be verified by this department.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 33

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE INFRASRUCTURE DEVELOPMENT DEPARTMENT:

This department has started from this year. It is a separate and fully

operational department. The department has already initiated realizable joint venture

projects like IT Park, the Shopping Mall, Commercial Complex, or SEZ etc. for

implementation in the near future.

FINANCIAL SERVICES DEPARTMENT: This department has also started from this year. In order to augment income

generation, the corporation initiated several measures directed towards fee-based

activities. As part of restructuring, fee based activities like stamp vending, marketing of

Life and General Insurance products, marketing of UTI mutual fund products, etc have

been taken up by this department.

OBJECTIVES OF KSFC:

The corporation has been established with the basic objective of promoting

industrial development in Karnataka. The KSFC was desired to particularly emphasis to

specialized institution government.

To provide financial assistance in the form of term loans to tiny and small scale

industries, ancillary industries and medium scale industries in Karnataka.

To encourage dispersal of industries to the backward areas to maintain balanced

growth of industries.

To provide equipment leasing, Hire Purchase, working capital and assistance to

Research & Development activities.

To identify entrepreneurs throughout the state.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 34

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE To provide enterprise development programs to women engineering and technical

professionals and agriculturists.

To conduct district level industrial seminars.

To provide special assistance to tiny and small scale industries.

To identify new projects and help local people to set up industries.

To develop data bank on industrial units.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 35

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

ACTIVITES OF KSFC

Assistance to Hotels / Restaurants:

Medium and star category standard hotels proposed in state capital, district and

taluk head quarters and important tourist centers within the state are eligible for financial

assistance. The existing hotels going in for expansion/renovation are eligible for

assistance. The hotel should have boarding, lodging and restaurant facilities and building

plans approved by the local authorities. Hotels proposed as per the specification of

tourism department, government of Karnataka are eligible for incentives as per the

tourism policy of state/central governments.

Mobile canteens/catering units are also considered for assistance subject to

eligible and providing adequate collateral security as per the prevailing lending policy.

Assistance to the Doctors /Hospitals /Nursing Homes:

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 36

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE Hospitals and nursing homes are eligible for financial assistance from KSFC

must be backed by expert services of at least one postgraduate doctor. Assistance is

available for acquiring land, building and equipments for diagnosis monitoring and

therapeutic use and air conditions (for operation theatres and intensive care units)

ambulance etc. Assistance is also extended to acquire ready built shop or for construction

of medical stores subject to conditions. Medical practitioners with relevant qualifications

in general medicine, dentistry, radiology etc are eligible for assistance for acquiring C.T

scanners, X-rays, endoscope and other electronic medical equipments required by

medical practitioners and hospitals. Medical professionals having Bachelor’s degree in

and branch of medicine from recognized university are eligible for financial assistance

for setting up Clinics.

Assistance to Construction activities and Infrastructure Projects:

Commercial complexes are an important infrastructure for the growth of Small

and Medium Enterprise and service units, marketing outlets and for small business.

Assistance under the scheme is provided for construction of building, Interior decoration,

air conditioning, lift and communication facilities etc. The commercial complexes

constructed can be either leased or sold on out right basis with the prior approval of the

corporation. Residential apartments/group housing, industrial estates, IT parks, training

institutions, godown, warehouses and development of layouts are provided financial

assistance. With a view to facilitate the development of infrastructure financial assistance

is also provided for establishing infrastructure projects like roads, flyovers, bridges etc.

Assistance to Tourism related activities:

The corporation provides financial assistance for tourism related activities like

development of amusement parks, setting up of conventional/cultural centers, restaurants,

travel and transport and tourism service agencies.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 37

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE Assistance to Entertainment Industry:

KSFC provides financial assistance for the construction/purchase of cinema

halls and multiplexes, production of short TV serials and feature films/filmed a within

Karnataka. Maximum financial assistance is up to 70% of the cost of the proposed fixed

assets in the case of cinema halls and multiplexes and 50% of the total production and

postproduction cost in the case of features films, TV serial and software for visual media.

Procedure for availing Financial Assistance:

Entrepreneurial guidance (EG) section headed by the Assistant General

Manager at the head office and branch managers will guide the entrepreneurs on various

schemes, loan facilities available etc.

Project clearance committee: A brief project profile along with supporting papers/documents will have to

be given by the promoters, which will be scrutinized by EG (Entrepreneur Guidance)

department as the case may be. The proposal will be placed before the Project Clearance

Committee (PCC) chaired by the Managing Director at Head Office and Zonal

Managers/Branch Managers at Branches. Details are to given as per the checklist. The

promoters are also required to give bio-data and net wroth details as per the format.

On receipt of the project profile and other detail, the main promoters are

called for discussion before the PCC. After discussions, if the project is found support

worthy, loan application form is issued on the spot (a set of three applications). The duly

filled in applications have to be submitted in duplicate along with other documents, as per

the checklist along with applicable processing fee.

Processing fee & other fees:

The following are the processing fee structure prevailing at present:

Application processing fee: ½% of the loan amount.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 38

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

Up-front fee:

SSI and others: ½% of the loan amount.

Medium scale industries: 1% of the loan amount.

The up-front loan fee will have to be paid the time of legal documentation or before

availing the first disbursement of the loan amount.

The application processing fee and up-front fee are non refundable. However, in

case the loan application is rejected, refund up to maximum of 75% of loan processing

fees paid is allowed on a case to case basis after deducting handling charges.

Legal fee:

In addition to the above, documentation fee for legal scrutiny of the title deeds,

execution of hypothecation and mortgage deed etc. at 0.1% of loan amount is being

charged.

Promoter’s contribution: The promoter’s contribution varies between 12.5% and 25% depending on the

location of the project, category, line of activity etc.

Debt equity ratio (DER):(i) For loans up to Rs.10 lakhs 3:1 (ii) For loans above 10 lakhs 2:1

The corporation adopts the norms of promoter’s contribution and debt equity

ratio as per the guidance issued by the SIDBI from time to time.

Debit services coverage ratio (DSCR):

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 39

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

The repayment period of loan is fixed by the corporation with due regard to

the cash generation and profitability of the project. For this purpose, average DSCR

ranging between 1.5:1 and 2: 1 is accepted as reasonable.

The DCSR indicates the ability of the project to services to services the debts

during the currency of the loans.

Repayment of the loan:

The repayment of the term loan varies between 5 to 7 years with a moratorium

of 1 to 2 years depending on the period of implementation. In respect of corporate loan

the maximum repayment period is 30 months including six months moratorium.

Security:

1. Primary Security:

The primary security for loan will be the assets financed i.e. land, building and

machinery. If working capital loan is provided the inventories in the form of raw

materials, work in process and finished goods, besides; bill and book debts, are to be

pledged/hypothecated.

2. Collateral Security:

All loans are to be backed by collaterals in the form of commercial or residential

properties located in the state of Karnataka. Fixed deposits, NSCs (National Saving

Certificates), etc and residential properties of third parties to the corporation will be

further charged.

In case of corporate loan, in the absence of adequate security in the form of

primary assets, collateral security to the extent of 100% of the loan amount is insisted in

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 40

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE respect of existing units assisted by the corporation and in respect of other units collateral

security will by 150% of the loan amount.

NOTE: The primary and collateral are to be by way of simple mortgage at jurisdictional

SRO (Sub Registrar Office).

Sanction and disbursement of loan:

After the proposal is cleared by the project clearance committee the EG

department scrutinizes the application and the enclosures submitted, collects the

processing fee and forwards the papers to the credits department. The credit department

appraises the projects and places them memorandum of sanction before the appropriate

authority for sanction approval. Branch offices also follow the similar procedure.

Legal scrutiny and documentation:

Legal officers in credit department at head office and in branch offices will take

up the legal scrutiny of documents after the sanction of loan. They ensure acceptance of

terms and conditions by promoters and complete legal documentation process.

Thereafter, credit department at HO/ branch office monitors the projects

implementation and disburse the funds based on the securities created and after ensuring

that the promoters have brought in the stipulated equity/contribution to the project is

completed and final disbursement is made. The above is the procedure in brief for

availing financial assistance from the corporation.

For further clarification/ details promoters may contact the General Manager

(credits) or Asst.General manager (EG) at the head offices or the branch managers of the

nearest branch offices.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 41

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 42

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

STRUCTURE:

The Human Resource Management Department called as Personnel

Department, which is headed by Senior Manager and coming under General Manager of

Administration.

The manpower strength of the Corporation stood at 1,266 at the end of 31 st

March 2007 as against 1,281 at the end of 31st March 2006. out of them.

402 are class A employees

721 are class B employees

143 are class C employees

Class A employees consist of Executives, Directors, Deputy General Manager, Assistant

General Manager, Senior Managers, Manager, Deputy Manager.

Class B employees consists of Assistant Managers, Assistants, Stenographers, Typists

and Clerks.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 43

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE Class C employees consist of Drivers, Daffedars, and peons etc.

The Corporation have a unique combination of professionals on its pay rolls - C

As, ICWAs, MBA, MCom, MA, MSc, MTech, LL.M., LL.B, BE etc. Thus, the diversity

in its human resource is one of the great assets of the corporation.

RECRUITMENT AND INCENTIVES:

There is a separate cadre recruitment rule, which governs the appointment of both

direct recruitment and promotions.

There is also staff regulation and rules, which governs the conduct of the employees.

In KSFC there are number of incentives given to the employees in the form of

reimbursement of convenience & medical expenses and advances at concessional

rates to employees such as house building advance, children education advance,

Motor car advance, Consumer durable advance, etc.

There is a cordial relationship between the management and employees.

There are Officers Association, SC/ST employees union and Employees union which

reddress the grievances of the employees.

KSFC has also introduced various schemes for the employees like Voluntary

Retirement Scheme (VRS) where employees can opt for retirement voluntarily.

The performance of the employees is to be assessed yearly. And separate confidential

report of a particular employee will be obtained from the Section head/Department

head.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 44

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE In appraisal the employee’s overall performance is assessed for the fitness of his/her

promotion.

There is a reservation to SC/ST category for recruitment and promotion.

8 in-house need based training programmes were conducted covering 221 employees

during the year of 2006-07

79 employees were deputed to external training programmes during the year of 2006-

07.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 45

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

STRUCTURE: The Accounting and Financial Management includes Finance and accounts

department, Treasury department and Legal department. The Finance and Account

department is responsible for maintaining various accounts, ledger, cashbook and other

books of accounts, income tax filling of statutory returns and statements. The function of

Treasury department is estimation of funds for lower possible cost. The basic function of

Legal department is to appraise the project legally which the entrepreneurs submit for

getting the loan.

These departments are headed by one Executive Director, Deputy General

Manager of Controller, Senior Manager of Treasury and Assistant Manager of Legal.

SIGNIFICANT ACCOUNTING POLICIES

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 46

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

FOLLOWED BY KSFC

1. As required by IDBI wide circular dated 26th April 1994. The corporation follows

cash systems of accounting for recognition of income and expenditure. Further,

all expenses including interest, which is accrued and fallen due, is accounted

irrespective of its payment excepting for guaranteed dividend liability up to 1999-

2000, which is accounted on receipt of subvention money from government of

Karnataka and charged off in the year of profit.

2. Memorandum loan accounts are maintained on mercantile basis for the purpose of

management information system and asset classification.

3. Provisions against Non-Performing Assets have been made as per applicable

guidelines issued by IDBI and SIDBI.

4. Cheques are accounted on receipt basis. Consequential changes, if any, are

effected in the books on the date of knowing their status

5. The corporation has taken a policy under Group Gratuity Scheme with Life

Insurance Corporation of India for payment of gratuity to its employees and

premium there of has been charged to profit and loss account.

6. The guidance note on “ accounting for lease” issued by the Institute of Chartered

Accountants of India (ICAI) has been adopted in respect of assets on lease and the

lease equalization/terminal adjustment is provided on the basis of schedule of

lease rentals due over the period of lease transactions carried out up to 31-3-2001.

Accounting standard 19 issued by ICAI has been adopted I respect of assets given

on lease and hire purchase after 01-04-2001.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 47

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

7. The corporation has own Provident Fund Regulations and contributions to the

fund is accounted for.

8. The income from bills discounting and DPG commission are accounted upfront.

9. The allocation logic adopted by the Corporation for repayment of loan made by

the borrower is to first adjust towards other debits, thereafter to adjust interest

dues and lastly the remaining amount towards repayment of principal. In case of

one time settlement and appropriation of sale proceeds of assets taken over under

sec29 of the State Financial Corporation’s act 1951, the allocation logic is to first

adjust towards principal thereafter towards interest accounted under mercantile

system till the year 1983, then towards other debits and lastly the balance, if any,

towards interest due subsequent to 1983.

10. Sale consideration on the sale of assets offered as security to the corporation on

deferred payment bases is accounted in the year of sale where the borrower’s

accounts were written off in earlier years, and in the other cases the income is

accounted on actual receipt of deferred payment installment.

11. Appropriation of amounts received on account on One Time Settlement is made

on approval by the D.R.C/Board.

12. In terms of R.B.I circular dated 4th may 2001 effective from 31-03-2001

Investments are classified as “Available for sale” and provisioning for net

depreciation in the value of investments is made.

13.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 48

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE a) Depreciation is provided on straight line method at the following rates:-

Depreciation Rate table:1. Building 04%

2. Furniture and Fixture 10%

3. Fans and Electrical Fittings. Internal

Telephone and Equipment

15%

4. Motors cars, bicycles, computers and

motor cycles

20%

b) Fixed assets have been carried at historical cost less depreciation and

include all lease assets acquire up to 31-03-2001.

c) Depreciation on all the leased assets upto 31.03.2001 is provided on straight-

line method over the primary period of lease.

INTEREST RATE TABLE [Term Loans] w.e.f. 01-08-2005 ( Rates in % age)

SL NO

Article I.

CATEGORY OF BORROWERS

EXISTING INTEREST

RATES [as per circular No. ED

(F) 755]

NEW INTEREST RATE

GROSS NET GROSS NET REBATE

I RATE OF INTEREST FOR GENERAL CATEGORIES OF BORROWERS

1 TERM LOAN [INCLUDING WCTL] OVER RS.50000/- UP TO RS.200000 /- TO SSIs , [INCLUDING TDMF & RTUF SCHEMES] AND RTOS -

a] General rate 11.75 10.75 11.75 10.25 1.50

b] Under RSR 10.75 9.75 10.75 9.25 1.50

c] NEF/MUN /SEMFEX [TL] 12.25 11.75 12.25 11.00 1.25

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 49

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

2 TERM LOAN [INCLUDING WCTL] OVER RS.200000/- AND UP TO RS.25,00,000/- TO SSIs , [INCLUDING TDMF & RTUF SCHEMES] AND RTOS

a] General rate 12.00 11.00 12.00 10.50 1.50

b] Under RSR 11.50 10.50 11.50 10.00 1.50

c] NEF/MUN /SEMFEX [TL] 13.00 12.50 13.00 11.50 1.50

3 TERM LOAN [INCL.WCTL] OVER RS .25,00,000/- TO SSI s, [INCLUDING TDMF & RTUF SCHEMES] AND RTO S -

a] General rate 12.50 11.50 12.50 11.00 1.50

b] Under RSR 12.00 11.00 12.00 10.50 1.50

c] NEF/MUN/SEMFEX [TL] - [for Project Cost Rs.50 lakhs & below]

13.50 13.00 13.50 12.00 1.50

II RATE OF INTEREST FOR NON-SSI & MSI CATEGORIES 1 TERM LOAN TO NON-SSI s, MSIs & AMARA SCHEME

a] General rate 13.50 12.50 13.50 11.00 2.50

b] Under RSR 13.00 12.00 13.00 10.50 2.50

c] NEF/MUN/SEMFEX [TL] – [ Excluding MSIs & Amara Scheme]

13.50 13.00 13.50 12.00 1.50

2 (a) LOAN ASSISTNCE FOR COMMERCIAL

COMPLEX -

(b) [not eligible under NEF/MUN/RSR scheme]

13.50

12.50 13.50

11.00 2.50

II RATE OF INTEREST FOR OTHER CATEGORIES OF BORROWERS

1 Section I.02 LOANS SANCTIONED OUT OF CORPORATION'S OWN FUNDS SUCH AS BRIDGE LOAN AGAINST INVESTMENT SUBSIDY, FINANCING EXISTING ASSETS AND ENTERPRISES etc.,

14.00 13.00 14.00 12.00 2.00

2 LOANS UNDER CORPORATE LOAN SCHEMELOANS UNDER CORPORATE LOAN SCHEME

- AAA rated entrepreneurs/units 12.50 12.50 12.50 12.00 0.50

- AA rated entrepreneurs/units 13.00 12.50 13.00 12.00 1.00

- Others 13.50 12.50 13.50 12.00 1.50

PROVISIONS RELATING TO INCOME TAX AND SUPER TAX:-

For the purposes of the Income Tax act, 1961(43 of 194) the financial

corporation shall be deemed to be a company within the meaning of that act and shall be

liable to Income Tax and super tax accordingly on its income, profits and gains:

Provided that any sum paid by the state government under the guarantee given

in pursuance of (sec7 or sec8) shall not be treated as the income profits and gains of the

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 50

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE financial corporation and any interest on debentures, (bonds or depreciation) paid by the

financial corporation out of such sum shall not be treated as expenses incurred by it.

Provided further that in the case of any shareholders such portion of a dividend

as has been paid out of any such sum advanced by the state government shall be deemed

to be income from “interest on securities”. (And the income tax shall be payable there on

as if it were interest receivable on any security of a state government issued income tax

free) within the meaning of Section 8 of that act.

Financial Appraisal :- The purpose of financial appraisal is to find out the financial viability of

the project. The financial appraisal is to find out the finance the projects are concerned

with the successful operation of unit. For this they should be convinced that the project

generates enough cash surplus to meet all the contractual obligations. Further,

institutions will have certain ratios like debt-equity ratio, debt service coverage ratio, etc

against which they examine the project.

Financial appraisal includes profitability estimates, cash flow estimates

and projected balance sheet. They are inter-related and prepared on the basis of cost of

the projects, source of finance and various assumptions of profitability estimates.

FINANCIAL RESULTS:

During the year under review, the corporation generated gross revenue of

Rs.195.71 crore on cash basis as against Rs.210.16 crore in 2005-06. Working of the

corporation for the year resulted in an operating profit of Rs.17.32 crore as against

operating profit of Rs.8.56 crore in 2005-06.

HEAD OFFICE AND BRANCH OFFICE SANCTIONS:

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 51

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE During the year, loan sanctioned by the head office amounted to Rs.

184.57 crore to 73 cases compared to the previous year’s sanctions of 100.27 crore to 65

cases. Loans sanctioned by the branch offices amounted to Rs. 239.96 crore to 1253 cases

compared to Rs. 215.93 crore to 1096 cases in the previous year.

DISBURSEMENTS:

Disbursements made during the year touched Rs.310.39 crore as against

Rs.199.86 crore disbursed during the year 2005-06. Cumulative disbursements reached

Rs.6526.40 crore as on 31.03.2007.

RECOVERY:

The total recovery during the year stood at Rs.502.74 crore as compared to

Rs.555.06 crore made in the previous year. Recovery in respect of loan was Rs.478.78

crore and Rs.1.38 crore in respect of Hire purchase, Rs.1.48 crore in respect of Leasing

and Rs.21.10 crore in respect of financial services.

TREASURY ACTIVITY:

Treasury department headed by Senior Manager and coming under Deputy

General Manager of Controller.

While the year 2005-06 was considered as a milestone year in restructuring

high cost bond obligations of the Corporation. During the year under report utilization

of Rs. 300.00 crore private placement bond proceeds was completed for swapping the

earlier high cost bonds.

During the year corporation availed a refinance of Rs.150.00 crore, while

repaid the principal of amount Rs.212.00 crore to SIDBI, including a pre-payment of Rs

100.00 crore. The line of credit out standing of SIDBI, which was at Rs.937.69 crore as

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 52

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE on 31.03.2006 came down to Rs 875.68 crore at 31.03.2007. The interest cost on

account of line of credit also came down from Rs.90.73 crore for the year 2005-06 to

Rs.78.49 crore for the year 2006-07. The corporation availed a rebate of Rs.2.92 crore

from SIDBI, for the prompt payment of principal and interest installments. The interest

cost on account of bonds reduced from 67.10 crore for the year 2005-06 to Rs.57.55

crore for the year 2006-07.

The Corporation maintained its track record, since inception, of being

prompt in meeting all its payment obligations i.e., to the SIDBI, the bondholders, fixed

deposit holders and all other financiers.

ASSET RECONSTRUCTION: The Asset reconstruction department at Head Office continued to tackle the

chronic Non-Performing Assets. The action basically involved disposal of units under

sec.29, follow up of miscellaneous cases filed against guarantors for decree, execution

of decrees, recovery of dues from MR portfolio etc.

During the year, assets of 30 units were sold involving a sale price of Rs.

427.73 lakh. One time settlement of dues was extended to 16 units involving a

settlement amount of Rs. 925.00 lakh. The AR department also contributed amount of

Rs. 150.00 lakh of interest recovery. The recovery from MR portfolio was Rs. 242.00

lakh, which also contributed to the income of the Corporation.

BALANCE SHEET AS ON 31st MARCH 2006-07 (Rs.in.lakhs)

Sl.No

Particulars Schedule As on31-03-2007

As on31-03-2006

A Capital and Liabilities:

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 53

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

1.2.

3.

4.5.

Share capitalLoan pending conversationTo Share capitalReserve fund and other resourcesTerm borrowingsCurrent liabilities and provisions

AB

C

DE

12467.55917.69

425.00

164985.107816.77

12467.55917.69

425.00

17808.8312434.02

TOTAL 186612.11 203053.09B

1.2.3.4.5.6.

Property and Assets:

Cash and bank balancesInvestments (at cost)Loans and advancesFixed assetsCurrent assetsProfit and loss accounts balance

FGHIJ

4817.07369.91

105790.61748.21

14741.0760091.24

11563.87456.86

106924.43821.85

22970.1660315.92

TOTAL 186612.11 203053.09

PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31stMARCH, 2007 (Rs.in lakhs)

Particulars Schedule As at31-03-2007

As at31-03-2006

INCOME:Interest incomeOther income

KL

16721.70 2849.70

17394.873621.19

TOTAL 19571.40 21016.06

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 54

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

EXPENDITURE:Interest and Other Financial ExpensesPersonal ExpensesAdministrative expensesDepreciationBad Debt Written Off

M

NOI

14110.66

2856.76 827.89 80.72 355.81

16780.62

2581.67758.22174.57155.81

TOTAL 18231.84 20450.89Profit Before TaxLess: provision for fringe Benefit TaxCurrent yearPrevious year

1339.56 _

41.00 3.19

565.17 39.00

Profit after TaxLess: Adjusted towards Dividend deficit Account Dividend provisionLess: brought forward loss from Previous YearSurplus/Deficit carried to Balance Sheet

1295.37247.05

823.64-60315.92

-60091.24

526.17526.17

-60315.92

-60315.92

Notes &Significant Accounting Policies forming part of Accounts

P

OPERATIONS AT A GLANCE: (Amount Rs. in crore)

Particulars 2004-05 2005-06 2006-07Since inception up to 31.03.2007

Paid up capital at the

year end

Gross Sanctions:

97.84 97.84 97.84 -

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 55

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

a. Number

b. Amount

Assistance to SSIs

Disbursements

Loan out standings

Recoveries

Percentage of NPA

Income

Expenditure

Operating Profit

1,244

242.87

131.79

240.34

1,504.83

582.17

51

217.95

217.16

7.76

1,161

316.20

165.00

199.86

1,342.28

555.06

46

210.16

204.50

8.56

1,326

424.53

178.53

310.39

1,320.71

502.74

33

195.71

182.31

17.32

1,58,030

8,168.38

4,286.37

6,526.40

-

-

-

-

-

-

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 56

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

STRUCTURE:

The Management Information System Department is headed by Assistant

General Manager and coming under General Manager of Corporate Planning.

MANAGEMENT INFORMATION SYSTEMS (MIS)

The present reporting system is oriented primarily to statistics .A formal MIS

covering profitability, liquidity, disbursement recoveries and costs is necessary for

monitoring of performance by top management.

M.S.RAMAIAH COLLEGE OF ARTS, SCIENCE & COMMERCE, BANGLORE 57

KARANATAKA STATE FINANCIAL CORPORATION,

BANGALORE

We suggest the following regular reports as parts of MIS for top management.

1. LIQUITIDTY:-

Eligible refinance for disbursement already made—weekly.

Variance analysis of cash flow (month) actual v/s budget,

reimbursements, recoveries, refinance, interest and experience.

2. PROFITABILITY:-

Segment wise profitability (quarterly)

Branches wise profitability(half yearly)

3. PORT FOLIO ANALYSIS:

Distribution of loans by size – quarterly.

Recovery analysis-quarterly.

Age wise analysis of area’s-quarterly.

Loan size wise arrears analysis-quarterly.

Branch wise analysis of recovery and arrears.

ABC analysis of arrears (To cover 75% of the arrears of interest

and principal).

4.COST OF BORROWING –QUARTERLY:

5. INTEREST ON LOANS- QUARTERLY:

6. SANCTIONED LOANS AWAITING DISBURSEMENT –QUARTERLY:

In the design of a computerized system of accounting and statistics collection

using concepts such as those of relation database. Extreme care is necessary describe