Kames UK Active Value Property Unit Trust Royal Borough of ...

14

Kames UK Active Value Property Unit Trust Royal Borough of Kensington & Chelsea Pension Fund 17 February 2015 Philip Bach – Fund Manager Fiona Hope – Institutional Client Director

Transcript of Kames UK Active Value Property Unit Trust Royal Borough of ...

Kames UK Active Value Property Unit Trust

Royal Borough of Kensington & Chelsea

Pension Fund

17 February 2015

Philip Bach – Fund Manager

Fiona Hope – Institutional Client Director

Principal terms – Kames UK Active Value PUT (closed-ended vehicle)

2

As at 19 January 2015

Fund structure Fund type

Fund equity

Domicile

Currency

Launched

Jersey Property Unit Trust

Target £250m, currently £275m (approx. 40 – 50 properties)

Jersey

Sterling

October 2013 (Final close December 2014)

Fund tenure Fund term

Investment period

7 years

36 months from the initial closing

Target returns Fund IRR 10% per annum

Target distribution yield 6%+ (paid quarterly)

Leverage No leverage

Managers Direct Property Investment team led by David Wise

Fund Manager Philip Bach

• GFC caused worst property

downturn since 1930’s

• Values recovered for prime

properties in global cities

• UK investor sentiment turned

positive in Q4 2012

• Recovery led by prime element

of market

• Recovery now evident in

secondary market

Where are we in the property cycle?

Source: IPD, December 2014

3

A long time coming... but tide has turned for property

-40

-30

-20

-10

0

10

20

30

40

Dec 87 Dec 90 Dec 93 Dec 96 Dec 99 Dec 02 Dec 05 Dec 08 Dec 11 Dec 14

%

Income Return ERV Growth Yield Impact Total Return

• Flight to safety led to recent

outperformance of prime assets

– Yield gap of c.100 bps in January 2007

– Yield gap of c.505 bps in January 2014

– Yield gap of c.440 bps in June 2014

– Yield gap of c. 400 bps in December 2014

• Active Value property will offer

attractive, higher yields than prime in

the long term

Prime vs Active Value property yields

Source: CBRE, as at end December 2014. Past performance is not a guide to future performance

4

UK Prime vs. Secondary All Property yield

(exc. central London)

Market now rewards risk

0%

2%

4%

6%

8%

10%

12%

2004 2006 2008 2010 2012 2014

All Prime All Secondary

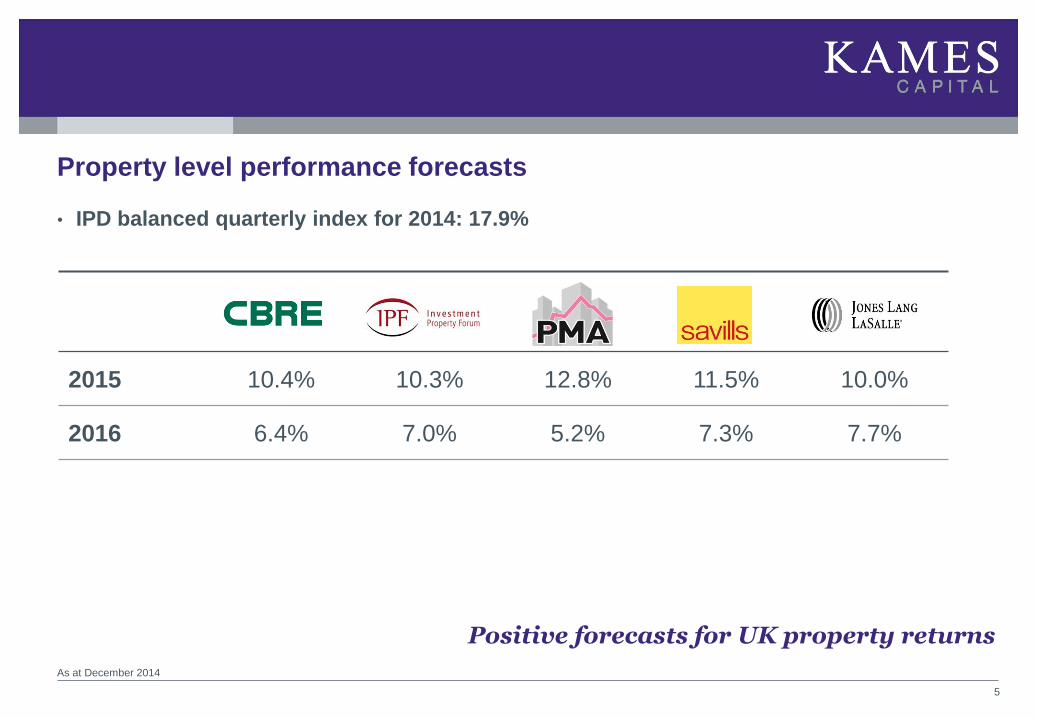

Property level performance forecasts

As at December 2014

5

2015 10.4% 10.3% 12.8% 11.5% 10.0%

2016 6.4% 7.0% 5.2% 7.3% 7.7%

Positive forecasts for UK property returns

• IPD balanced quarterly index for 2014: 17.9%

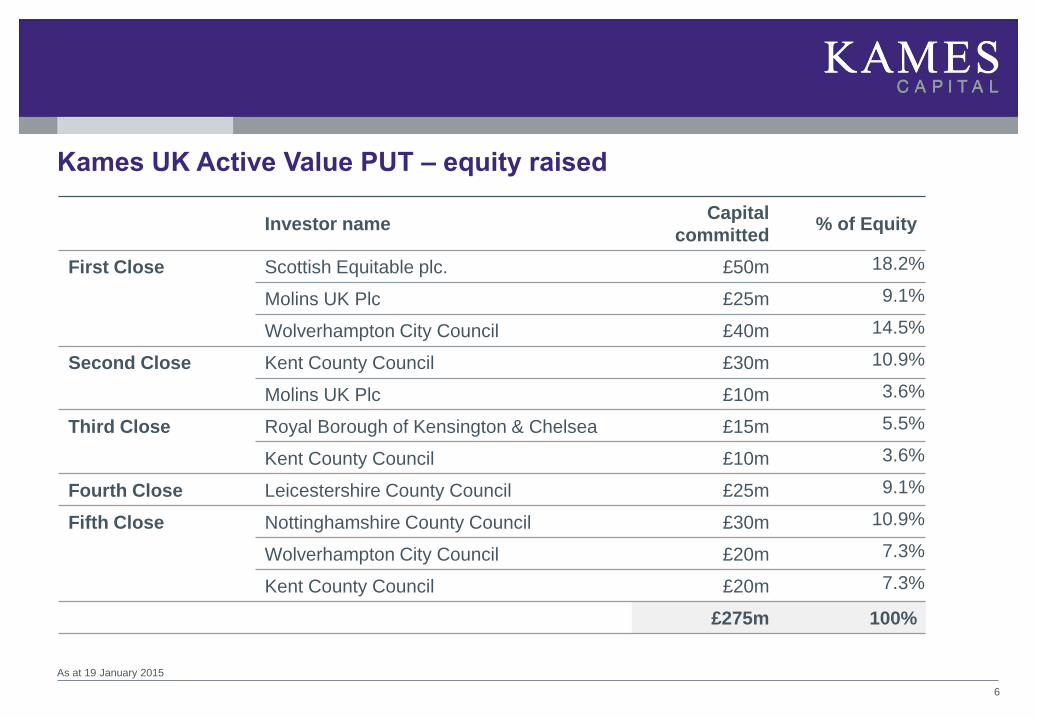

Kames UK Active Value PUT – equity raised

6

As at 19 January 2015

Investor name Capital

committed % of Equity

First Close Scottish Equitable plc. £50m 18.2%

Molins UK Plc £25m 9.1%

Wolverhampton City Council £40m 14.5%

Second Close Kent County Council £30m 10.9%

Molins UK Plc £10m 3.6%

Third Close Royal Borough of Kensington & Chelsea £15m 5.5%

Kent County Council £10m 3.6%

Fourth Close Leicestershire County Council £25m 9.1%

Fifth Close Nottinghamshire County Council £30m 10.9%

Wolverhampton City Council £20m 7.3%

Kent County Council £20m 7.3%

£275m 100%

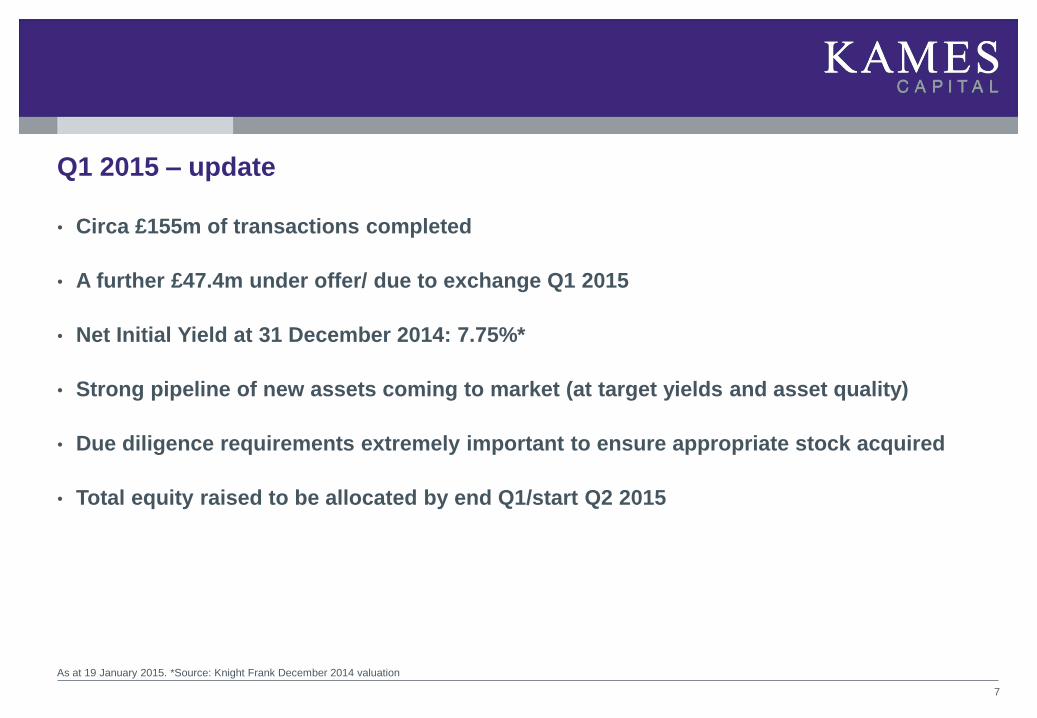

• Circa £155m of transactions completed

• A further £47.4m under offer/ due to exchange Q1 2015

• Net Initial Yield at 31 December 2014: 7.75%*

• Strong pipeline of new assets coming to market (at target yields and asset quality)

• Due diligence requirements extremely important to ensure appropriate stock acquired

• Total equity raised to be allocated by end Q1/start Q2 2015

Q1 2015 – update

As at 19 January 2015. *Source: Knight Frank December 2014 valuation

7

Existing Property Portfolio information

As at 19 January 2015. Includes assets completed and under offer

8

1. Transaction pipeline: sector split

WAULT: 8.06 years to breaks

NIY: 7.75%

Total capital committed: circa. £202m

2. Transaction pipeline: geographical split

28.08%

40.31%

7.30%

20.91%

3.39%

Industrial

Office

Retail Warehouse

Retail

Leisure

Assumptions

• All funds committed will be drawn and

invested by the end of Q2 2015

• Purchase costs are 5.8%

• Cash will be invested at the NIY of the

existing properties in the Fund

• It takes 42 days to get funds drawn

from investors into the market

• 50% of leases which end will lead to a

Void

• On average, units will remain void for

9 months

Income distributions – cashflow forecast

As at 1 December 2014. Forecasts are not a guarantee of future performance. There is no guarantee that properties currently under offer will complete.

9

£0

£100,000

£200,000

£300,000

£400,000

£500,000

£600,000

£700,000

£800,000

Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015

7.02% 6.69%

6.99%

7.68% 7.37%

Recent fund acquisitions

10

• £9.83m (purchased December 2014)

• Freehold office building with retail on the ground floor and

purpose built offices on upper floors

• Let to tenants with strong retail covenants

• 8.92% net initial yield

• Capital Value of £204 per sq. ft.

• Active Value investment strategy

– Prime retail pitch with opportunity to re-gear retail leases

– Longer term ‘Basildon Master Plan’ will improve the town centre

Basildon – Office and Retail Sheffield – Retail

11

• £5.75m (exchanged December 2014)

• Retail building occupying a prominent location

• Let to Sports Direct, Poundland, British Heart Foundation –

all strong covenants

• 7.56% net initial yield

• Active Value investment strategy

– Improving rental levels off an historically low base

– Potential to convert upper floors for an alternative use

(residential/student accommodation), especially in relation to city

centre location and proximity to University

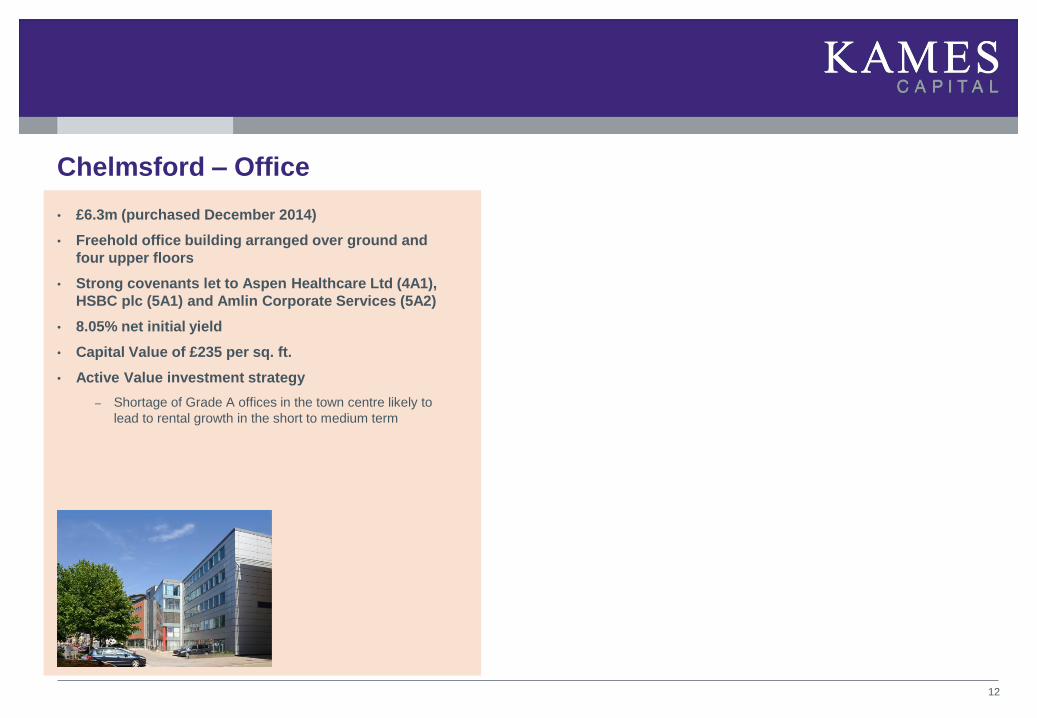

Chelmsford – Office

12

• £6.3m (purchased December 2014)

• Freehold office building arranged over ground and

four upper floors

• Strong covenants let to Aspen Healthcare Ltd (4A1),

HSBC plc (5A1) and Amlin Corporate Services (5A2)

• 8.05% net initial yield

• Capital Value of £235 per sq. ft.

• Active Value investment strategy

– Shortage of Grade A offices in the town centre likely to

lead to rental growth in the short to medium term

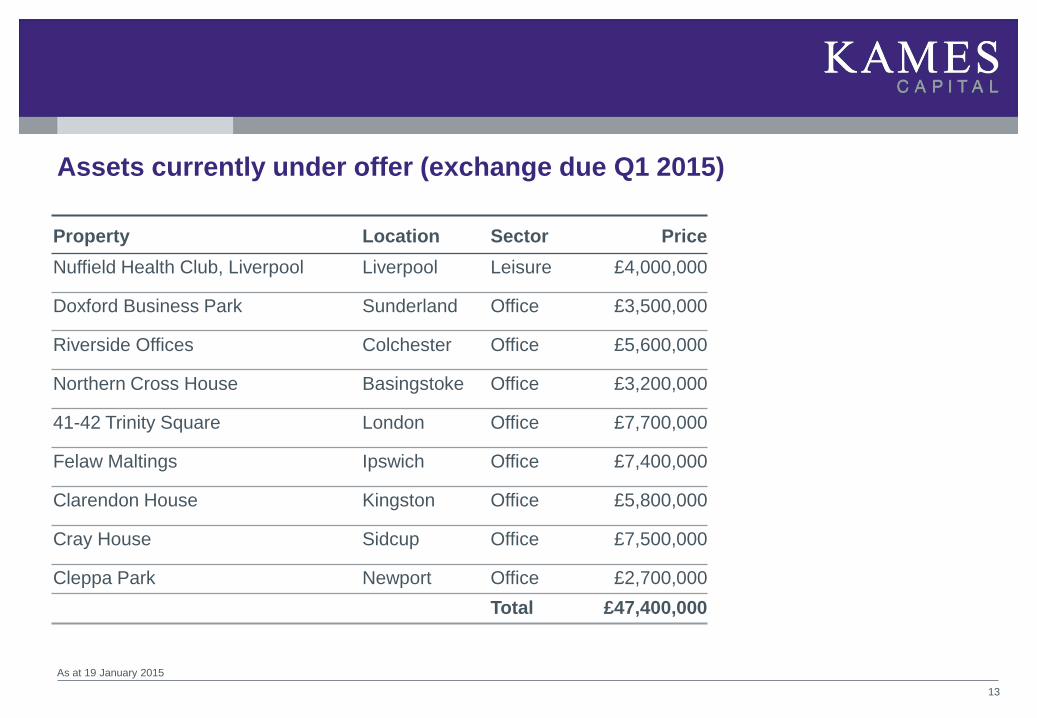

Assets currently under offer (exchange due Q1 2015)

As at 19 January 2015

13

Property Location Sector Price

Nuffield Health Club, Liverpool Liverpool Leisure £4,000,000

Doxford Business Park Sunderland Office £3,500,000

Riverside Offices Colchester Office £5,600,000

Northern Cross House Basingstoke Office £3,200,000

41-42 Trinity Square London Office £7,700,000

Felaw Maltings Ipswich Office £7,400,000

Clarendon House Kingston Office £5,800,000

Cray House Sidcup Office £7,500,000

Cleppa Park Newport Office £2,700,000

Total £47,400,000

This document is not intended for retail distribution and is directed only at investment professionals. It should not be distributed to, or relied upon

by, private investors. All data in this presentation is sourced to Kames Capital unless otherwise stated. The views expressed in this document

represent our understanding of the current and historical positions of the market. They should not be interpreted as a recommendation or advice.

Past performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and is

not guaranteed.

All yields are stated as at 31 December 2014. We calculate yields in compliance with the industry standard formula we are obliged to use which

takes no account of potential future defaults. This may mean that, depending on future economic factors, the actual yield could be less than

those shown.

Where funds are invested in property, investors may not be able to switch or cash in their investment when they want because property in the

fund may not always be readily realisable. If this is the case we may defer a request to switch or cash in units. Whilst property valuation is

conducted by an independent expert, any such valuation is a matter of the valuer's opinion. Property funds invest in a specialist sector, which

may be less liquid and produce more volatile performance than an investment in broader investment sectors.

This document is accurate at the time of writing but can be subject to change without notification. Kames Capital is an Aegon Asset Management

company and includes Kames Capital plc (Company Number SC113505) and Kames Capital Management Limited (Company Number

SC212159). Both are registered in Scotland and have their registered office at Kames House, 3 Lochside Crescent, Edinburgh, EH12 9SA.

Kames Capital plc is authorised and regulated by the Financial Conduct Authority (FCA reference no: 144267). Kames Capital plc provides

segregated and retail funds and is the Authorised Corporate Director of Kames Capital ICVC, an Open Ended Investment Company. Kames

Capital Management Limited provides investment management services to Aegon, which provides pooled funds, life and pension contracts.

Kames Capital Management Limited is an appointed representative of Scottish Equitable plc (Company Number SC144517), an Aegon

company, whose registered office is 1 Lochside Crescent, Edinburgh Park, Edinburgh, EH12 9SE (PRA/FCA reference no: 165548).

Important Information

FPID: 2015/CS2591

14