KalKalbarbbaarrbar Resources Resources Resources ... · Kalbar Resources (KBR) is an unlisted...

8

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report Page 1 28 June 2017 This note is to highlight interesting stocks which come across our desk. Kal Kal Kal Kalbar bar bar bar Resources Resources Resources Resources Limited Limited Limited Limited (KBR) (KBR) (KBR) (KBR) In brief Kalbar Resources (KBR) is an unlisted company which is exploring and proposing to develop a zircon rich mineral sand deposit in Gippsland, Victoria. The board and management have a wide variety of experience in developing mineral sands deposits in Victoria and in marketing titanium dioxide (TiO2) and zircon products into Asia. They are working to take a high grade zircon resource from Preliminary Feasibility Study (PFS) to development by 2019. The aim is to sell a heavy mineral (HM) concentrate to processors in China and Thailand rather than build a processing facility in Australia and simply be paid for the zirconium dioxide (ZrO2), TiO2 and rare earth elements in the concentrate. What looks interesting? 1. The zircon market appears to be on the rise with Iluka Resources (ILU), the global leader in zircon, recently announcing an increase in its benchmark price and the restart of Jacinth-Ambrosia in South Australia. 2. KBR is intending to produce a heavy mineral concentrate and sell it to consumers in China and Thailand rather than building a mineral separation plant and producing final product. This is a similar approach to many mining companies selling base metal concentrates and is somewhat more widespread in the mineral sands industry than we had previously understood. 3. Revenue is dominated by zircon (69% on our estimates) with the balance split roughly equally between TiO2 minerals and rare-earth elements. 4. We have done a preliminary estimate of the project value based on the data provided in the PFS to generate an after tax NPV of $350m at a discount rate of 10% (~$5.56ps on current 63m issued shares) and after start-up capital expenditure of $106m. There appears to be potential for optimising the mining schedule, which could have a positive impact on the cash flow profile in the first five years. 5. The project has the potential to deliver an average annual EBITDA of $83m pa. What is the asset? Fingerboards KBR purchased 100% of the Fingerboards heavy mineral sands (HMS) deposit from Rio Tinto (RIO) in 2013. RIO discovered the Glenaladale and Mossiface deposits in 2004 – its focus was on outlining a large TiO2 resource rather than zircon. KBR is focussing on developing a high grade portion of the much larger low grade Glenaladale resource. Fingerboards is 200km east of Melbourne, near Bairnsdale. The total resource is 2,241Mt @ 1.8% HM and contains two higher grade zones, Marker and Sub-Marker, which are plotted in FIG.1. These will be the zones processed and amount to 117.8Mt @ 4.4% HM, with HM grades of 30.7% zircon, 15.0% rutile, 33.6% ilmenite, 6.9% leucoxene and 3.5% rare earth oxides (REO). The HM concentrate produced and sold is expected to contain 18% ZrO2, 36% TiO2 and 46% other minerals including trash and REO such as monazite. An environmental effects statement (EES) is being prepared and should be completed in mid-2018. From an environmental perspective the mining’s impact will be on dust and noise levels and the source/amount of water used or consumed in processing. The proposed mine site is largely covered by dry-land grazing properties. The mining license application process could start in 2017 and given the history of mineral sands mining in Victoria we believe the issue of negotiating land access agreements or purchasing of the farms, which overlie the deposit, will be resolved as it was with the deposits in the Murray Basin. Stocks Mentioned Mkt Cap Kalbar Resources (unlisted) Iluka Resources* (ILU.AX) $3,571m Rio Tinto* (RIO.AX) $25.052m Sheffield Resources (SFX.AX) $96m * Full research available Research Analyst Warren Edney +613 9602 9384 [email protected] The author of this report does not hold shares in any of the stocks mentioned. Baillieu Holst Ltd and/or its associates may receive fees or commissions, calculated at normal client rates, from transactions involving the Company and may hold interests in the Company from time to time. Your adviser will earn a commission of up to 55% of any brokerage resulting from transactions you may undertake as a result of this document. This document is not intended to constitute general or personal advice to any retail client. There has been no consideration of the investment objectives, financial situation or particular needs of any particular person or entity and the recipient of this information must not rely on the veracity of the information in making any investment decisions. This report is only intended to be distributed to “wholesale” clients as defined in section 761G of the Corporations Act 2001 (Cth). No representation, warranty or undertaking is given or made in relation to the accuracy of information contained in this document, such document being based solely on public information which has not been verified by Baillieu Holst Ltd. Save for any statutory liability that cannot be excluded, Baillieu Holst Ltd and its employees and agents shall not be liable (whether in negligence or otherwise) for any error or inaccuracy in, or omission from, this advice or any resulting loss suffered by the recipient or any other person. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment at its original date of publication and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Baillieu Holst Ltd assumes no obligation to update this document or correct any inaccuracy which may become apparent after it is given.

Transcript of KalKalbarbbaarrbar Resources Resources Resources ... · Kalbar Resources (KBR) is an unlisted...

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report Page 1

28 June 2017

This note is to highlight

interesting stocks which come

across our desk.

KalKalKalKalbarbarbarbar Resources Resources Resources Resources LimitedLimitedLimitedLimited (KBR)(KBR)(KBR)(KBR)

In brief

Kalbar Resources (KBR) is an unlisted company which is exploring and proposing to develop a zircon rich mineral sand deposit in Gippsland, Victoria. The board and management have a wide variety of experience in developing mineral sands deposits in Victoria and in marketing titanium dioxide (TiO2) and zircon products into Asia. They are working to take a high grade zircon resource from Preliminary Feasibility Study (PFS) to development by 2019. The aim is to sell a heavy mineral (HM) concentrate to processors in China and Thailand rather than build a processing facility in Australia and simply be paid for the zirconium dioxide (ZrO2), TiO2 and rare earth elements in the concentrate.

What looks interesting?

1. The zircon market appears to be on the rise with Iluka Resources (ILU), the global leader in zircon, recently announcing an increase in its benchmark price and the restart of Jacinth-Ambrosia in South Australia.

2. KBR is intending to produce a heavy mineral concentrate and sell it to consumers in China and Thailand rather than building a mineral separation plant and producing final product. This is a similar approach to many mining companies selling base metal concentrates and is somewhat more widespread in the mineral sands industry than we had previously understood.

3. Revenue is dominated by zircon (69% on our estimates) with the balance split roughly equally between TiO2 minerals and rare-earth elements.

4. We have done a preliminary estimate of the project value based on the data provided in the PFS to generate an after tax NPV of $350m at a discount rate of 10% (~$5.56ps on current 63m issued shares) and after start-up capital expenditure of $106m. There appears to be potential for optimising the mining schedule, which could have a positive impact on the cash flow profile in the first five years.

5. The project has the potential to deliver an average annual EBITDA of $83m pa.

What is the asset?

Fingerboards

� KBR purchased 100% of the Fingerboards heavy mineral sands (HMS) deposit from Rio Tinto (RIO) in 2013. RIO discovered the Glenaladale and Mossiface deposits in 2004 – its focus was on outlining a large TiO2 resource rather than zircon. KBR is focussing on developing a high grade portion of the much larger low grade Glenaladale resource.

� Fingerboards is 200km east of Melbourne, near Bairnsdale. The total resource is 2,241Mt @ 1.8% HM and contains two higher grade zones, Marker and Sub-Marker, which are plotted in FIG.1. These will be the zones processed and amount to 117.8Mt @ 4.4% HM, with HM grades of 30.7% zircon, 15.0% rutile, 33.6% ilmenite, 6.9% leucoxene and 3.5% rare earth oxides (REO). The HM concentrate produced and sold is expected to contain 18% ZrO2, 36% TiO2 and 46% other minerals including trash and REO such as monazite.

� An environmental effects statement (EES) is being prepared and should be completed in mid-2018. From an environmental perspective the mining’s impact will be on dust and noise levels and the source/amount of water used or consumed in processing. The proposed mine site is largely covered by dry-land grazing properties.

� The mining license application process could start in 2017 and given the history of mineral sands mining in Victoria we believe the issue of negotiating land access agreements or purchasing of the farms, which overlie the deposit, will be resolved as it was with the deposits in the Murray Basin.

Stocks Mentioned Mkt Cap Kalbar Resources (unlisted) Iluka Resources* (ILU.AX) $3,571m Rio Tinto* (RIO.AX) $25.052m Sheffield Resources (SFX.AX) $96m * Full research available Research Analyst Warren Edney +613 9602 9384 [email protected]

The author of this report does not hold shares in any of the stocks mentioned.

Baillieu Holst Ltd and/or its associates may receive fees or commissions, calculated at normal client rates, from transactions involving the Company and may hold interests in the Company from time to time. Your adviser will earn a commission of up to 55% of any brokerage resulting from transactions you may undertake as a result of this document.

This document is not intended to constitute general or personal advice to any retail client. There has been no consideration of the investment objectives, financial situation or particular needs of any particular person or entity and the recipient of this information must not rely on the veracity of the information in making any investment decisions. This report is only intended to be distributed to “wholesale” clients as defined in section 761G of the Corporations Act 2001 (Cth).

No representation, warranty or undertaking is given or made in relation to the accuracy of information contained in this document, such document being based solely on public information which has not been verified by Baillieu Holst Ltd.

Save for any statutory liability that cannot be excluded, Baillieu Holst Ltd and its employees and agents shall not be liable (whether in negligence or otherwise) for any error or inaccuracy in, or omission from, this advice or any resulting loss suffered by the recipient or any other person.

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment at its original date of publication and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments.

Baillieu Holst Ltd assumes no obligation to update this document or correct any inaccuracy which may become apparent after it is given.

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report Page 2

27 June 2017

FIG.1: RESOURCE GRADE (Bubble size reflects in situ value per tonne of resource)

ILU-Eucla

Fingerboards

Donald

SFX-Thunderbird HG

Sri Lanka

WIM150

Kwale

Perth BasinUSA Atlantic

MZ-Mindarie

Tanzania

Tanzania

Eneabba

WA

Grande Cote

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

0.00% 0.20% 0.40% 0.60% 0.80% 1.00% 1.20% 1.40% 1.60% 1.80%

In situ TiO2 m

inerals

In situ zircon grade

Source: Baillieu Holst, Company data

Preliminary feasibility highlights some interesting issues

Grade enables treatment by other without value destruction

� Concentrating on mining and processing the Marker & Sub-Marker higher grade resource should allow KBR to generate returns relative to RIO’s bulk low grade option.

� The driver is to produce a concentrate with a high revenue to cost ratio – we have it starting at 2.5x and gradually declining to 1.5x (the latter being similar to those disclosed by ILU over the last few years).

Pricing the concentrate

� The terms are negotiated with the processor and largely dependent on market conditions, the quality of the final products, and other constituents in the concentrate (credits and penalties). Essentially the pricing ends up being a payment for the percent of ZrO2 or TiO2 in the concentrate after charging for processing and adjusting for quality.

� The following is an example of how we have priced the zircon concentrate in our preliminary cash flow analysis. To calculate the revenue per % ZrO2 in the concentrate we used our:

- forecast FOB zircon price deducted 5% for quality; added US$20/t to get the CIF price in China; deducted US$155/t for processing; deducted 20% for processing losses; converting zircon sand to ZrO2 by multiplying by 0.66; which equals the price per % of ZrO2 available for sale.

- At a price of US$1,300/t of zircon sand this equates to US$13.30 per % ZrO2, and at target grade of 18% of ZrO2 the value of ZrO2 is equivalent to US$240/t of HMC.

� The TiO2 pricing formula works much the same way although we have used a 40% quality discount on our base TiO2 mineral price forecasts – using the average TiO2 contents for ilmenite, rutile and leucoxene, and the forecast concentration we end up with a value per % of TiO2 of US$2.20.

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report Page 3

27 June 2017

Getting your head around quality

� We have always focused on yields and production of final product and the quality of the product when analysing mineral sands assets. Issues we have noted with the Fingerboards Project include the elevated levels of U+Th content of the zircon concentrate and impurities in the rutile, leucoxene and ilmenite.

� Discussions with management indicate that the quality issues are manageable and a reflection of changing industry standards as coarse grained strandline resources are mined out and most development projects in Australia are increasingly fine grained. KBR’s approach is more like selling a base metal concentrate and receiving payment for it after making adjustments for quality and penalty elements, the quality components make up for those which are less desirable.

� We are reassured by TZMI’s assessment that 100% of the zircon produced from the Fingerboards Project is classified as ‘Premium’ due to its very low impurities (Al2O3, Fe2O3), which the management advises us is driving significant market interest in the zircon concentrate. We note that Management has been realistic in applying lower pricing to reflect the impurities in the TiO2 minerals and on the positive side we the high rare earth content of the Fingerboards HMC is clearly seen as big plus by the industry.

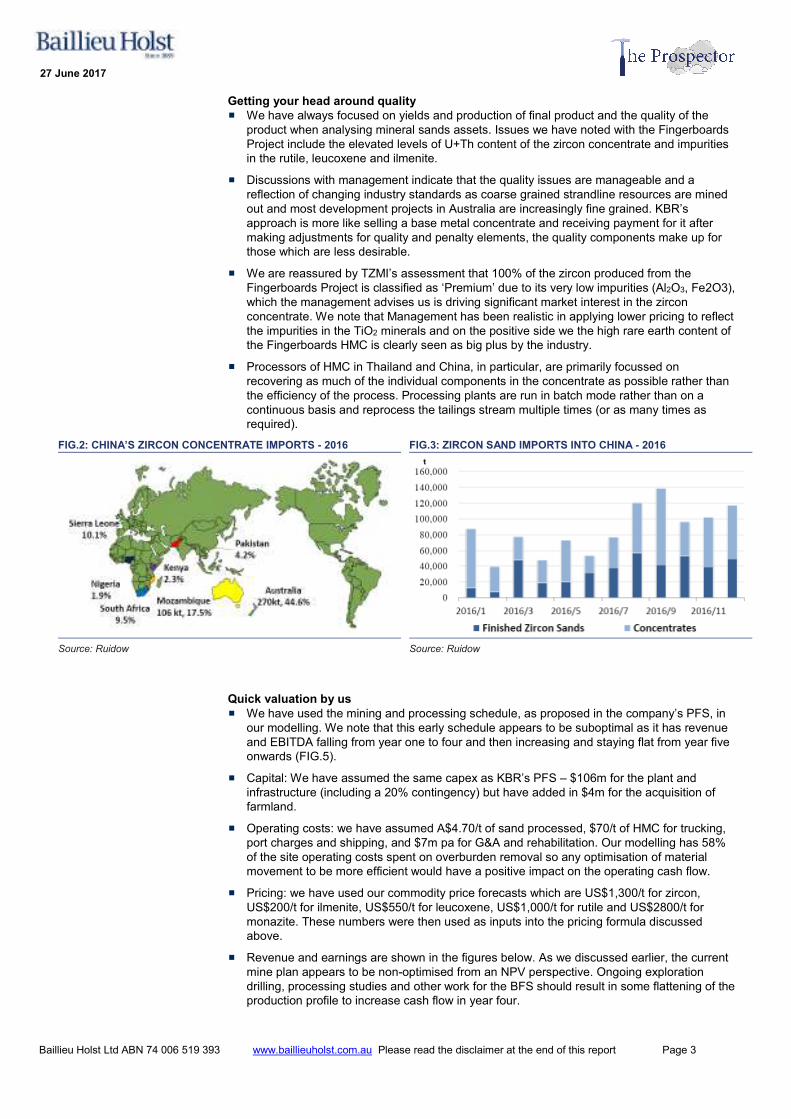

� Processors of HMC in Thailand and China, in particular, are primarily focussed on recovering as much of the individual components in the concentrate as possible rather than the efficiency of the process. Processing plants are run in batch mode rather than on a continuous basis and reprocess the tailings stream multiple times (or as many times as required).

FIG.2: CHINA’S ZIRCON CONCENTRATE IMPORTS - 2016 FIG.3: ZIRCON SAND IMPORTS INTO CHINA - 2016

Source: Ruidow Source: Ruidow

Quick valuation by us

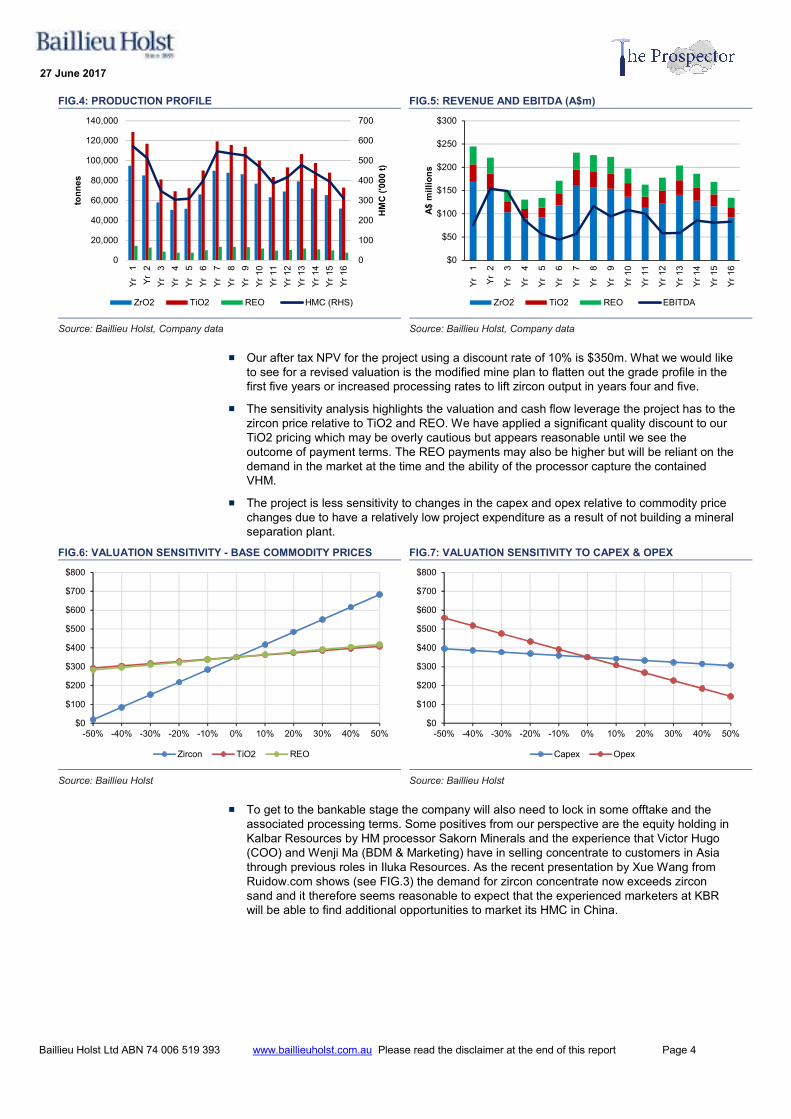

� We have used the mining and processing schedule, as proposed in the company’s PFS, in our modelling. We note that this early schedule appears to be suboptimal as it has revenue and EBITDA falling from year one to four and then increasing and staying flat from year five onwards (FIG.5).

� Capital: We have assumed the same capex as KBR’s PFS – $106m for the plant and infrastructure (including a 20% contingency) but have added in $4m for the acquisition of farmland.

� Operating costs: we have assumed A$4.70/t of sand processed, $70/t of HMC for trucking, port charges and shipping, and $7m pa for G&A and rehabilitation. Our modelling has 58% of the site operating costs spent on overburden removal so any optimisation of material movement to be more efficient would have a positive impact on the operating cash flow.

� Pricing: we have used our commodity price forecasts which are US$1,300/t for zircon, US$200/t for ilmenite, US$550/t for leucoxene, US$1,000/t for rutile and US$2800/t for monazite. These numbers were then used as inputs into the pricing formula discussed above.

� Revenue and earnings are shown in the figures below. As we discussed earlier, the current mine plan appears to be non-optimised from an NPV perspective. Ongoing exploration drilling, processing studies and other work for the BFS should result in some flattening of the production profile to increase cash flow in year four.

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report Page 4

27 June 2017

FIG.4: PRODUCTION PROFILE FIG.5: REVENUE AND EBITDA (A$m)

0

100

200

300

400

500

600

700

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000Yr 1

Yr 2

Yr 3

Yr 4

Yr 5

Yr 6

Yr 7

Yr 8

Yr 9

Yr 10

Yr 11

Yr 12

Yr 13

Yr 14

Yr 15

Yr 16

HMC ('000 t)

tonnes

ZrO2 TiO2 REO HMC (RHS)

$0

$50

$100

$150

$200

$250

$300

Yr 1

Yr 2

Yr 3

Yr 4

Yr 5

Yr 6

Yr 7

Yr 8

Yr 9

Yr 10

Yr 11

Yr 12

Yr 13

Yr 14

Yr 15

Yr 16

A$ millions

ZrO2 TiO2 REO EBITDA

Source: Baillieu Holst, Company data Source: Baillieu Holst, Company data

� Our after tax NPV for the project using a discount rate of 10% is $350m. What we would like to see for a revised valuation is the modified mine plan to flatten out the grade profile in the first five years or increased processing rates to lift zircon output in years four and five.

� The sensitivity analysis highlights the valuation and cash flow leverage the project has to the zircon price relative to TiO2 and REO. We have applied a significant quality discount to our TiO2 pricing which may be overly cautious but appears reasonable until we see the outcome of payment terms. The REO payments may also be higher but will be reliant on the demand in the market at the time and the ability of the processor capture the contained VHM.

� The project is less sensitivity to changes in the capex and opex relative to commodity price changes due to have a relatively low project expenditure as a result of not building a mineral separation plant.

FIG.6: VALUATION SENSITIVITY - BASE COMMODITY PRICES FIG.7: VALUATION SENSITIVITY TO CAPEX & OPEX

$0

$100

$200

$300

$400

$500

$600

$700

$800

-50% -40% -30% -20% -10% 0% 10% 20% 30% 40% 50%

Zircon TiO2 REO

$0

$100

$200

$300

$400

$500

$600

$700

$800

-50% -40% -30% -20% -10% 0% 10% 20% 30% 40% 50%

Capex Opex

Source: Baillieu Holst Source: Baillieu Holst

� To get to the bankable stage the company will also need to lock in some offtake and the associated processing terms. Some positives from our perspective are the equity holding in Kalbar Resources by HM processor Sakorn Minerals and the experience that Victor Hugo (COO) and Wenji Ma (BDM & Marketing) have in selling concentrate to customers in Asia through previous roles in Iluka Resources. As the recent presentation by Xue Wang from Ruidow.com shows (see FIG.3) the demand for zircon concentrate now exceeds zircon sand and it therefore seems reasonable to expect that the experienced marketers at KBR will be able to find additional opportunities to market its HMC in China.

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report Page 5

27 June 2017

FIG.8: PROJECT TIMELINE

Source: Company data

Possible comparable assets – Tier One Deposit

Jacinth Ambrosia (Iluka Resources)

� On care and maintenance since April 2016, Iluka recently announced that it will be re-commencing operations at the Jacinth Ambrosia (JA) deposit in the Eucla Basin, South Australia. This has been the pre-eminent zircon producing deposit in the world over the last 10 years and in 2011 the deposit produced close to 400,000 tonnes of zircon representing over 30% of world zircon consumption.

� Upon resumption, planned for late 2017, it is anticipated that the JA deposit will be mining similar zircon grades (1.5% in situ) to the Fingerboards Project. While the initial reserve contained approximately 3% in situ zircon, it is expected that mining will resume at a similar grade to that at Fingerboards (1.4%).

� While JA concentrate will be shipped to Western Australia for processing to final zircon product, the Fingerboards HMC will be shipped directly to China for processing.

� Both deposits have approximately 2Mt of zircon contained, while Fingerboards contains higher by-product credits due to the REO content.

Possible comparable assets – Junior Developer

Sheffield Resources

� BFS on development of Thunderbird HMS project in Broome, WA. Internally calculated pre-tax NPV of A$676m; Stage 1 for first 10 years NPV is $348m; Stage 1 capex is A$350m; and Stage 2 A$195m (years 11-20). The company expects the first 10 years to have a revenue to cost ratio of 2:1. The current market cap of SFX is $96m. The project is unfunded.

� Reserves are 680Mt with a HM content of 11.3%. In situ zircon grade is 0.87% (on an HMC basis the SFX’s resource has a zircon grade of 9% vs KBR’s 31%). First production is expected late 2019. Ilmenite (magnetics) will undergo a low temperature reduction process to reduce the iron content, while the non-magnetics (zircon, leucoxene and non-magnetic trash) undergo hot acid leach to remove iron coating.

� The ratio of capex to NPV for stage 1 is 1:1 and for stages 1 & 2 is 1.24:1 – without the need to build an MSP or treatment facilities, KBR’s capex to NPV ratio on our estimates is 0.31:1.

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report Page 6

27 June 2017

Catalysts

� Revised resources and a reserve statement.

� A revised mining plan which smooths production in the first five years – achievable through a different scheduling of mining areas or through increasing the processing rate by adding another module.

� Completion of BFS.

� Completion of Environment Effects Statement and public consultation.

� Land acquisition or access agreements.

� Product offtake agreements.

Risks

� Delays in the environmental impact statement and granting of a mining license.

� Delays in the bankable feasibility study.

� A slower than expected resolution to land access where the high grade resource exists – KBR have some freehold land but would need to reach agreement, either directly or through VCAT, with a number of landowners to lease or purchase the farmland.

Mineral sands skills held by Board & Management

ROBERT BISHOP, EXECUTIVE CHAIRMAN

� Rob is a Chemical Engineer with significant experience in mineral sands metallurgy. He started his career at Tiwest Mineral Sands and most recently supervised Kalbar’s Kalimantan development program, which defined two major bauxite deposits. As a result of this work, two alumina refineries are currently under construction. As well as practical mining experience, Rob has spent over 10 years in the finance industry focusing on the resources sector.

BRAD FARRELL, DIRECTOR

� Brad Farrell has some 45 years’ experience in the resources industry as a successful exploration geologist and developer involved in a variety of commodities. In this time, he has been involved in several significant mineral sands discoveries and developments, including Sierra Leone (Rotifunk); Western Australia (Scott Coastal Plain and Gwindinup (currently being mined)); and the Murray Basin of Victoria and NSW. Brad was the founder and major shareholder of Basin Minerals Limited, taken over by Iluka Resources Limited in 2002 for its major Douglas Project (now mined). Brad has a Bachelor of Science (Honours Economic Geology), a Master of Science and Doctor of Philosophy. He is a Fellow and Chartered Professional Geologist of the Australasian Institute of Mining and Metallurgy, a member of Mineral Industry Consultants Association, and a member and a Chartered Engineer of Institute of Materials, Minerals and Mining (formerly Institution of Mining and Metallurgy (London)).

NEIL O’LOUGHLIN, MANAGING DIRECTOR

� Neil is a geologist with over 25 years’ experience in mineral exploration and mine development in Australia and overseas in a range of commodities. In the mineral sands industry he is well known as the co-founder and Executive Director of Basin Minerals Ltd, which discovered and brought to feasibility the Douglas Mineral Sands Project in Victoria prior to the purchase by Iluka Resources Limited in 2003. The Douglas deposits (Bondi, Bondi East and Echo) have since been mined by Iluka Resources Ltd, while other commercially significant deposits discovered by Basin Minerals include the Gallipoli and Balranald projects in NSW.

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report Page 7

27 June 2017

VICTOR HUGO, CHIEF OPERATING OFFICER

� Victor has over 25 years of experience in the titanium and zircon industries, having worked in a variety of roles for Richards Bay Minerals, Cable Sands, RGC, TZMI and Iluka. He joined Kalbar in February 2017 following 13 years working for Iluka in senior leadership roles including GM Exploration, GM Product and Technical Development and GM Sales and Marketing. Victor has a PhD in Geology and wrote his thesis on titanium minerals along the east coast of South Africa.

DR. WENJIE (IDA) MA, BUSINESS DEVELOPMENT AND MARKETING MANAGER

� Ida has been actively involved global mining industry since 2008 in range of roles in key mining and investment hubs in London, Hong Kong, Shanghai and Perth. With a background in investment banking, specialising in resources, Ida has held critical business and market development roles in leading companies including Barclays Capital, Azure Capital and Iluka Resources. During her time in Iluka Resources, her insights into the mineral sands market contributed to Iluka’s global market footprint expansion, and the development and deployment of the zircon pricing and payment framework. Ida graduated from University of Sydney with a PhD in Materials Engineering, and holds an MBA from Macquarie Graduate School of Management.

Baillieu Holst Ltd ABN 74 006 519 393 www.baillieuholst.com.au Please read the disclaimer at the end of this report Page 8

27 June 2017

This document has been prepared and issued by:

Baillieu Holst Ltd ABN 74 006 519 393

Australian Financial Service Licence No. 245421

Participant of ASX Group

Participant of NSX Ltd

Disclosure of potential interest and disclaimer:

Baillieu Holst Ltd (Baillieu Holst) and/or its associates may receive commissions, calculated at

normal client rates, from transactions involving securities of the companies mentioned herein and

may hold interests in securities of the companies mentioned herein from time to time. Your adviser

will earn a commission of up to 55% of any brokerage resulting from any transactions you may

undertake as a result of this advice.

When we provide advice to you, it is based on the information you have provided to us about your

personal circumstances, financial objectives and needs. If you wish to rely on our advice, it is

important that you inform us of any changes to your personal investment needs, objectives and

financial circumstances.

If you do not provide us with the relevant information (including updated information) regarding your

investment needs, objectives and financial circumstances, our advice may be based on inaccurate

information, and you will need to consider whether the advice is suitable to you given your personal

investment needs, objectives and financial circumstances. Please do not hesitate to contact our

offices if you need to update your information held with us. Please be assured that we keep your

information strictly confidential.

No representation, warranty or undertaking is given or made in relation to the accuracy of

information contained in this advice, such advice being based solely on public information which has

not been verified by Baillieu Holst Ltd.

Save for any statutory liability that cannot be excluded, Baillieu Holst Ltd and its employees and

agents shall not be liable (whether in negligence or otherwise) for any error or inaccuracy in, or

omission from, this advice or any resulting loss suffered by the recipient or any other person.

Past performance should not be taken as an indication or guarantee of future performance, and no

representation or warranty, express or implied, is made regarding future performance. Information,

opinions and estimates contained in this report reflect a judgment at its original date of publication

and are subject to change without notice. The price, value of and income from any of the securities

or financial instruments mentioned in this report can fall as well as rise. The value of securities and

financial instruments is subject to exchange rate fluctuation that may have a positive or adverse

effect on the price or income of such securities or financial instruments.

Baillieu Holst Ltd assumes no obligation to update this advice or correct any inaccuracy which may

become apparent after it is given.

Baillieu Holst Ltd

ABN 74 006 519 393

Australian Financial Service Licence No. 245421

Participant of ASX Group

Participant of NSX Ltd

www.baillieuholst.com.au

Melbourne (Head Office)

Address Level 26, 360 Collins Street

Melbourne, VIC 3000 Australia

Postal PO Box 48, Collins Street West

Melbourne, VIC 8007 Australia

Phone +61 3 9602 9222

Facsimile +61 3 9602 2350

Email [email protected]

Adelaide Office

Address Ground Floor, 226 Greenhill Road,

Eastwood SA 5063

Postal PO Box 171

Fullarton SA 5063

Phone +61 8 7074 8400

Facsimile +61 8 8362 3942

Email [email protected]

Bendigo Office

Address Level 1, 10-16 Forest Street

Bendigo, VIC 3550

Postal PO Box 84

Bendigo, VIC 3552

Phone +61 3 4433 3400

Facsimile +61 3 4433 3430

Email [email protected]

Geelong Office

Address 16 Aberdeen Street

Geelong West Vic 3218

Postal PO Box 364

Geelong Vic 3220 Australia

Phone +61 3 5229 4637

Facsimile +61 3 4229 4142

Email [email protected]

Gold Coast Office

Address Suite 202 Level 2, Eastside Building

6 Waterfront Place, Robina QLD 4226

Phone +61 7 5628 2670

Facsimile +61 7 5677 0258

Email [email protected]

Newcastle Office

Address Level 1, 120 Darby Street

Cooks Hill, NSW 2300 Australia

Postal PO Box 111

The Junction, NSW 2291 Australia

Phone +61 2 4037 3500

Facsimile +61 2 4037 3511

Email [email protected]

Perth Office

Address Level 10, 191 St Georges Terrace

Perth WA 6000 Australia

Postal PO Box 7662, Cloisters Square

Perth, WA 6850 Australia

Phone +61 8 6141 9450

Facsimile +61 8 6141 9499

Email [email protected]

Sydney Office

Address Level 18, 1 Alfred Street

Sydney, NSW 2000 Australia

Postal PO Box R1797

Royal Exchange, NSW 1225 Australia

Phone +61 2 9250 8900

Facsimile +61 2 9247 4092

Email [email protected]