Kakwani decomposition of redistributive effect: origins, criticism and upgrades Ivica Urban...

40

Kakwani decomposition of redistributive effect: origins, criticism and upgrades Ivica Urban Institute of Public Finance, Zagreb to be presented at the Fourth Winter School on Inequality and Collective Welfare Theory January 2009

-

Upload

maximilian-valentine-dean -

Category

Documents

-

view

213 -

download

0

Transcript of Kakwani decomposition of redistributive effect: origins, criticism and upgrades Ivica Urban...

Kakwani decomposition of redistributive effect: origins, criticism and upgrades

Ivica UrbanInstitute of Public Finance, Zagreb

to be presented at the Fourth Winter School on Inequality and Collective Welfare Theory

January 2009

Kakwani decomposition of redistributive effect

Kakwani (1984) decomposition of redistributive effect into vertical and reranking (horizontal inequity) terms

One of the most important tools in income redistribution literature in last 25 years

Its popularity rests on...

simplicity and ease of computation comprehensiveness: captures two

different notions of redistributive justice availability for straightforward policy

interpretation: for example, “redistributive power can be enhanced if horizontal inequity is reduced”

decomposability

This presentation...

a critical overview of development of Kakwani dec.

the context in which reranking and vertical index have emerged and how they fit into Kakwani dec.

short review of upgrades

Outline

1 Introduction 2 The decomposition 3 Horizontal inequity or reranking? 4 Origins of the vertical effect 5 Origins of the reranking effect 6 Criticism of Lerman and Yitzhaki and their new

framework 7 Extension to the net fiscal system 8 Frameworks capturing vertical and horizontal

inequity and reranking 9 Kakwani-Lambert “new approach” 10 Approach based on relative deprivation

References

Kakwani (1984) On the measurement of tax progressivity and redistributive effect of taxes with applications to horizontal and vertical equity

Kakwani (1986) Analyzing redistribution policies: A study using Australian data

Section title in both works: “Measures of horizontal and vertical equity”

Modern presentation

TXN

concentration coefficient of post-tax income xN

D

XGN

G Gini coefficients of pre- and post-tax income

xt the average tax rate

and

Kakwani progressivity index

APK RVRE

x

KT

xK

t

PtV

1

0 xNN

AP DGR

NX GGRE

decomposition:

concentration coefficient of tax

XxT

KT GDP

xTD

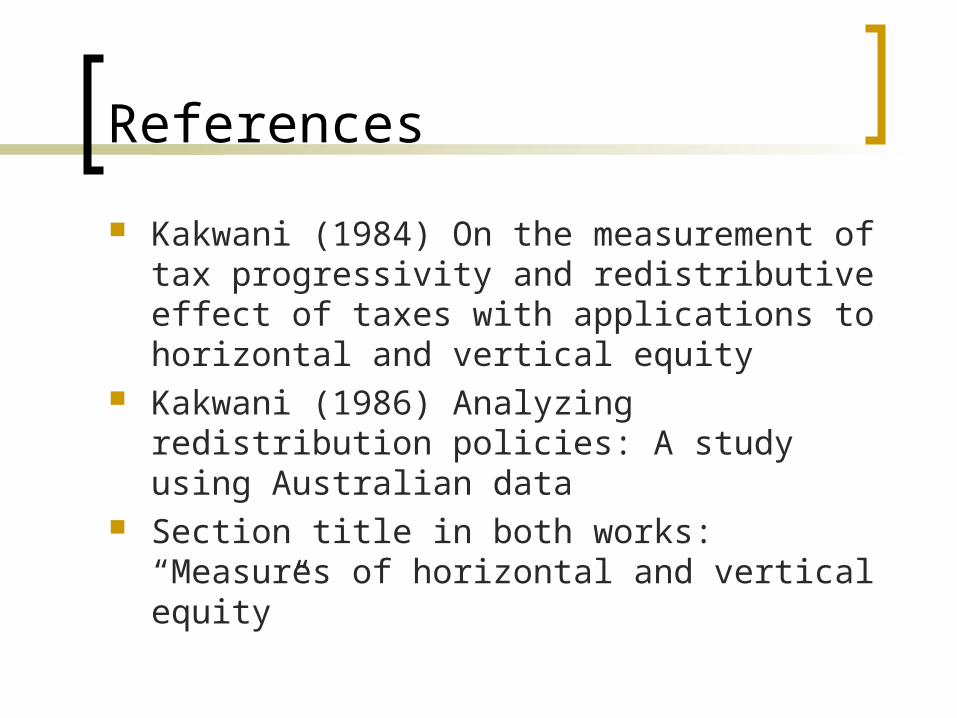

Comparison of presentations

APK RVRE

x

KT

xK

t

PtV

1

0 xNN

AP DGR

NX GGRE

VHR

0

X

NxN

G

GDH

X

NX

G

GGR

Xx

KT

x

Gt

PtV

)1(

OriginalModern

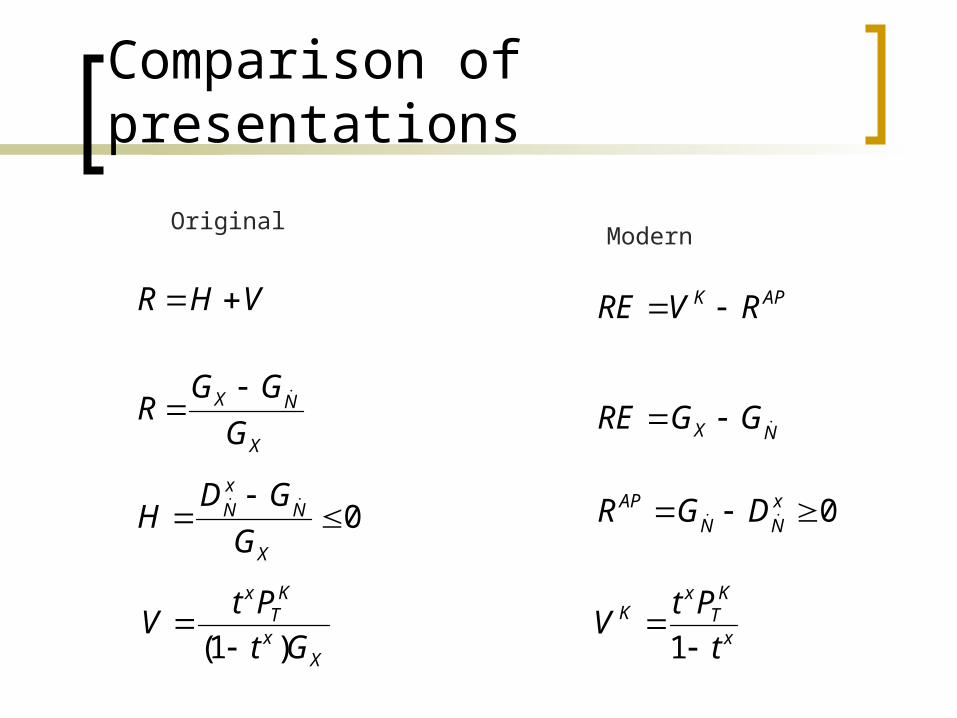

Derivation using L/C curves

0.0

0.2

0.4

0.6

0.8

1.0

0.0 0.2 0.4 0.6 0.8 1.0

_

_

_O

)( pLX

)( pC xT

KTP

x

KT

xK

t

PtV

1

0.0

0.2

0.4

0.6

0.8

1.0

0.0 0.2 0.4 0.6 0.8 1.0

_

_

_O

)( pLX

)( pC xN

KV

Derivation using L/C curves

0.0

0.2

0.4

0.6

0.8

1.0

0.0 0.2 0.4 0.6 0.8 1.0

_

_

_

_O

)( pLX

)( pLN

)( pC xN

APR

0.0

0.2

0.4

0.6

0.8

1.0

0.0 0.2 0.4 0.6 0.8 1.0

_

_

_O

)( pLX

)( pC xN

KV

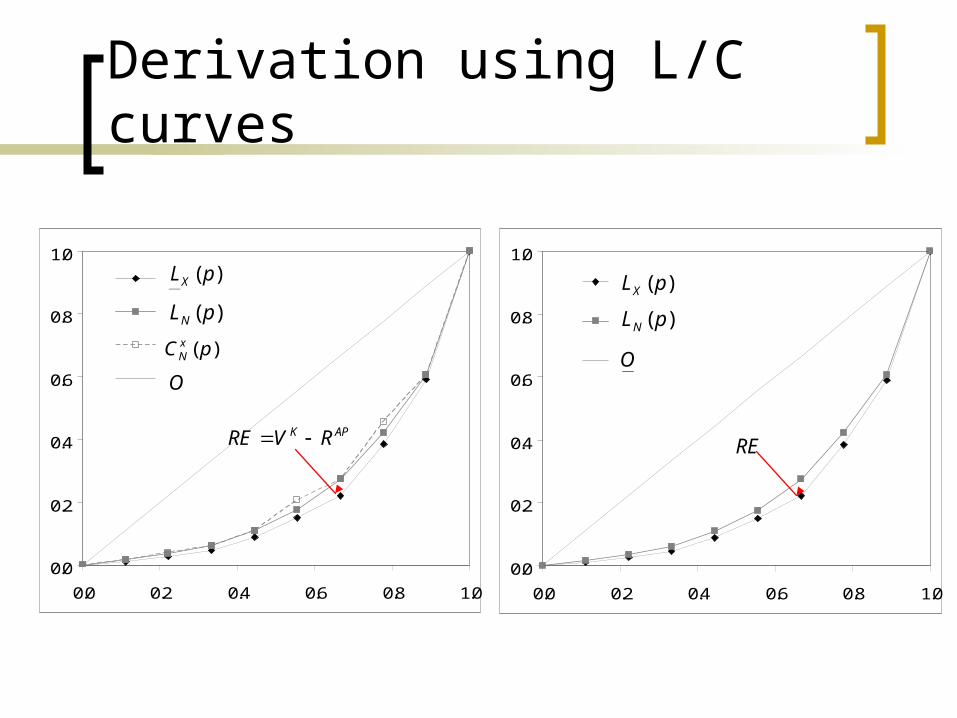

Derivation using L/C curves

0.0

0.2

0.4

0.6

0.8

1.0

0.0 0.2 0.4 0.6 0.8 1.0

_

_

_O

)( pLX

)( pLN

RE

0.0

0.2

0.4

0.6

0.8

1.0

0.0 0.2 0.4 0.6 0.8 1.0

_

_

_

_O

)( pLX

)( pLN

)( pC xN

APK RVRE

Horizontal inequity or reranking?

The principle of vertical equity requires that people with larger incomes pay higher taxes than those with lower incomes

Horizontal equity in taxation requires that people with equal incomes pay equal taxes

Violation of this principle gives rise to horizontal inequity

Following several other authors, Kakwani identifies horizontal inequity with reranking

Horizontal inequity or reranking?

it is common to name the effect “reranking” instead of “horizontal inequity”

Kaplow (1989) Horizontal Equity: Measures in Search of a Principle

Aronson, Johnson, Lambert (1994) Redistributive effect and unequal income tax treatment

Horizontal inequity or reranking?

it seems that by Kakwani dec. we obtain two measures that both deal with unequal treatment of unequals

Example:

pre-fiscal income

post-fiscal income

A 100 500

B 500 100

Origins of the vertical effect

Kakwani (1977) Measurement of Progressivity: An International Comparison

criticizes RE as a progressivity index: it should be an index of redistributive effect

appropriate index of tax progressivity will indicate that two tax systems with equal elasticity (everywhere) are equally progressive

Origins of the vertical effect Kakwani then proposes an index that does

satisfy the requirement:

...and shows why RE doesn’t... (assume there is no reranking: )

(of two systems having the same elasticity, the one with higher ATR will be deemed as more progressive by RE)

XxT

KT GDP

REV K

x

KT

xK

t

PtREV

1

Origins of the reranking effect: Atkinson

Atkinson: some empirical studies used the measure , which understates the true post-fiscal inequality,

in other words, a measure overstates the redistributive effect of fiscal system,

One motive for measurement of reranking: to estimate redistribution correctly

NGxNX DG

xND

RE

Atkinson: “Changes in the ranking of observations as a result of taxation do not in themselves affect the degree of inequality in the post-tax distribution. They do, however, influence certain ways of representing the redistribution and of calculating summary measures of inequality.”

In other words: Reranking is a by-product, not a causing factor;

Reranking does not contribute, positively or negatively, to the redistributive effect

Origins of the reranking effect: Atkinson

In Plotnick’s model: “the structure of postredistribution income inequality is taken as a datum by the measure.”

“...given the change in inequality, the measure should tell us how seriously the redistributive activities violated the norms of horizontal equity.”

the measure of reranking “should not attempt to compare the actual extent of redistribution or change in inequality to some exogenous criterion. Doing so would be an exercise in measuring vertical inequity.”

Origins of the reranking effect: Plotnick

Advice: How to use it

Atkinson and Plotnick: although aware of the strong connection between the concepts of vertical and horizontal equity, they do not attempt to build comprehensive model capturing both of them

they suggest to future users and developers to be cautious about introduction of reranking measure into other, more comprehensive frameworks

Was the advice taken?

However, for Kakwani, the reranking measures the reduction of the redistributive effect caused by fiscal activities or “increase in inequality”

Reranking is not only a by-product, it is a causing factor

Usual interpretation: Progressive fiscal system reduces inequality and is positive: vertical inequity is “good”; In presence of reranking, is positive and increases inequality; this is evidence of the notion that horizontal inequity is “bad”.

KV

APR

Was the advice taken?

Furthermore, actual redistribution is only . Here, measures a potential redistributive effect; one that could be attained if reranking were somehow eliminated:

APK RVRE KV

APKpotential RREVRE

Popular recipe

researcher may offer straightforward advice to policymakers: by reduction of horizontal inequity, without additional resources, you can increase redistributive effect by x percent

Although this interpretation was not present in Kakwani (1984 and 1986), it might be said that these works encouraged it

New decomposition

Lerman and Yitzhaki (1995) Changing ranks and the inequality impacts of taxes and transfers

criticism of Kakwani decomposition They develop their own decomposition of

redistributive effect following the “philosophy” of Kakwani, but arrive at different conclusions about the role of reranking:

it positively contributes to inequality reduction, together with “gap narrowing” (which corresponds to vertical effect)

Comparison of presentations

APK RVRE

0 xNN

AP DGR

NX GGRE

Lerman and Yitzhaki Kakwani

LYLY RVRE

0 nXX

LY DGR

NnT

LYT GDP X

xT

KT GDP

NnXn

LYT

nLY GD

t

PtV

1

xNXx

KT

xK DG

t

PtV

1

Derivation using L/C curves

0.0

0.2

0.4

0.6

0.8

1.0

0.0 0.2 0.4 0.6 0.8 1.0

_

_

_

_O

)( pLX

)( pLN

)( pC xN

APK RVRE

0.0

0.2

0.4

0.6

0.8

1.0

0.0 0.2 0.4 0.6 0.8 1.0

_

_

_

_O

)( pLX

)( pLN

)( pC nX

LYLY RVRE

Interpretations...

the method enables decomposition of redistributive effect “into two exclusive, exhaustive terms”.

As Kakwani, they regard reranking as an independent source of redistributive effect: “...policies may reduce inequality by rearranging rankings as well.”

They even claim that Atkinson supported this view: he indicated “that the reranking effect might be important in explaining a proportion of the impact of taxes on inequality.”

(...but that is not what he meant)

Why new decomposition?

they criticize Kakwani vertical effect: for given redistributive effect it increases automatically when reranking is increased

“the after-tax ranking is the appropriate ranking for calculating progressivity” (because the after-tax ranking is proper ranking in analysis of marginal changes in the tax system)

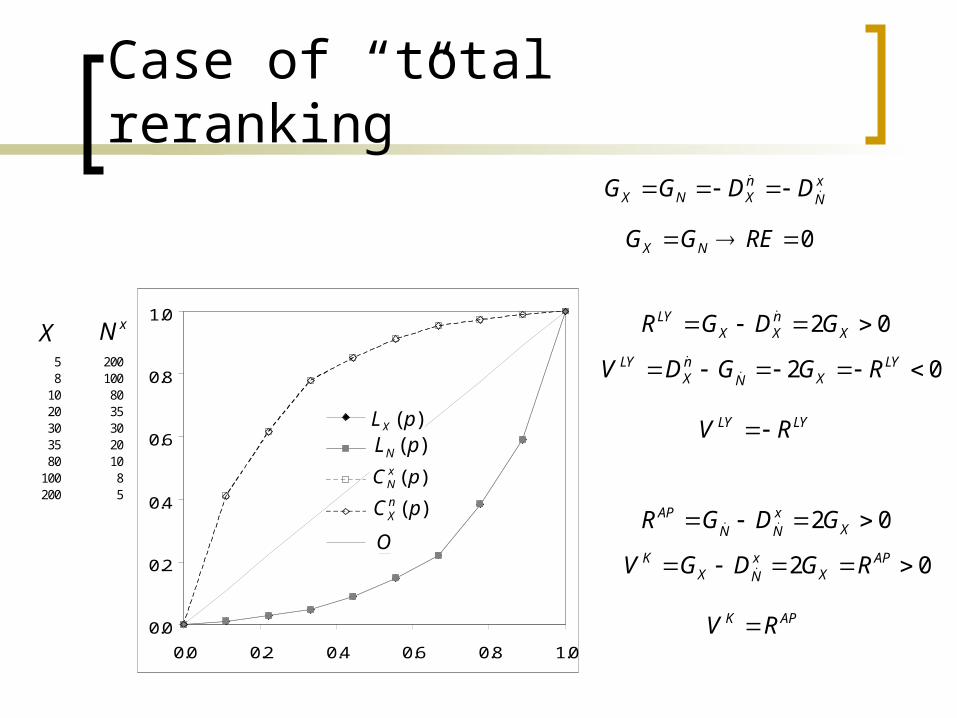

Case of “total reranking”

0 nXX

LY DGR

0.0

0.2

0.4

0.6

0.8

1.0

0.0 0.2 0.4 0.6 0.8 1.0

_

_

_

_

_

)( pLX

)( pLN

)( pC nX

)( pC xN

O

5 2008 100

10 8020 3530 3035 2080 10

100 8200 5

X xN

0 REGG NX

xN

nXNX DDGG

02 XnXX

LY GDGR

02 XxNN

AP GDGR

02 LYXN

nX

LY RGGDV

02 APX

xNX

K RGDGV

LYLY RV

APK RV

Case of “total reranking”

more reranking results in an increase of Kakwani vertical effect, based on pre-tax rankings

this suggests that even more taxation of the “now poor” is desired

unfortunately, they do not involve in deeper technical elaboration of their criticism

no followers, despite interesting framework

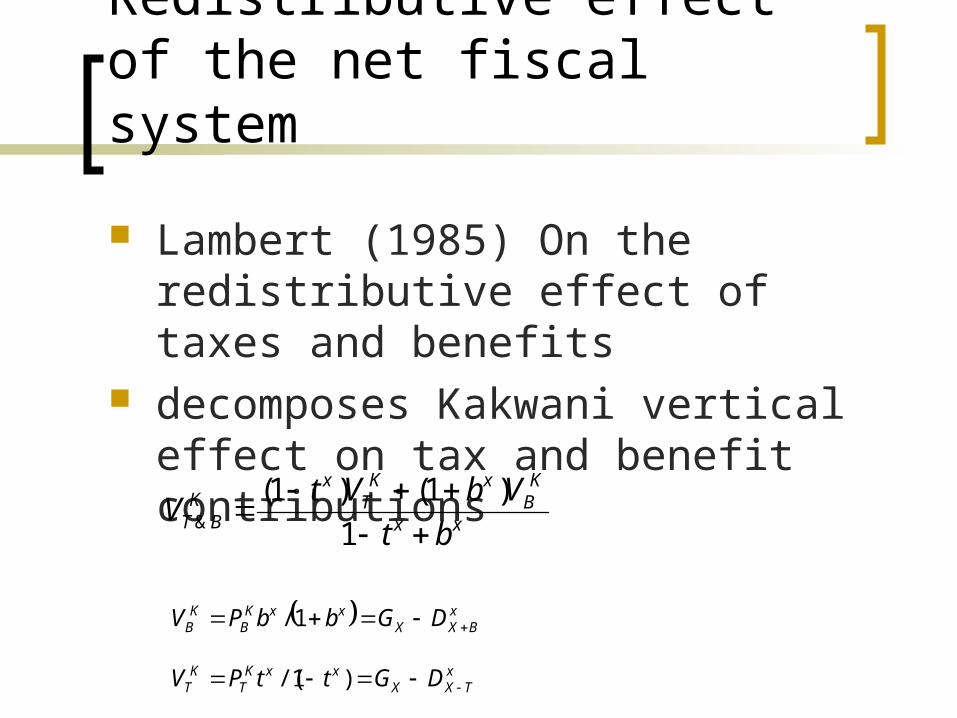

Redistributive effect of the net fiscal system

Lambert (1985) On the redistributive effect of taxes and benefits

decomposes Kakwani vertical effect on tax and benefit contributions

xx

KB

xKT

xK

BT bt

VbVtV

1

)1()1(&

xTXX

xxKT

KT DGttPV )1/(

xBXX

xxKB

KB DGbbPV 1/

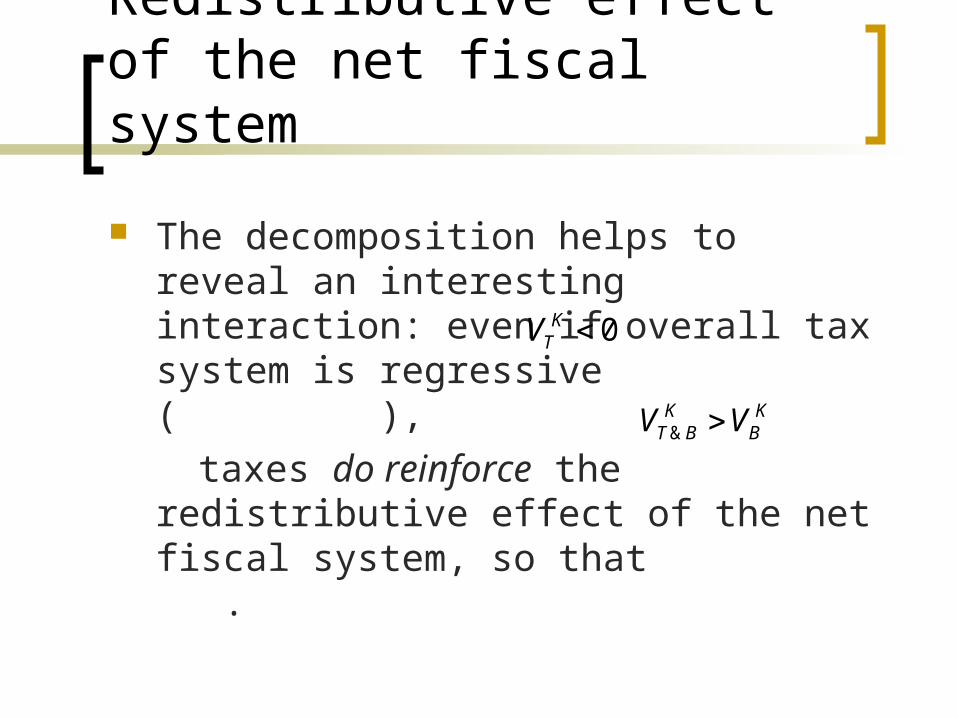

Redistributive effect of the net fiscal system

The decomposition helps to reveal an interesting interaction: even if overall tax system is regressive ( ),

taxes do reinforce the redistributive effect of the net fiscal system, so that .

0KTV

KB

KBT VV &

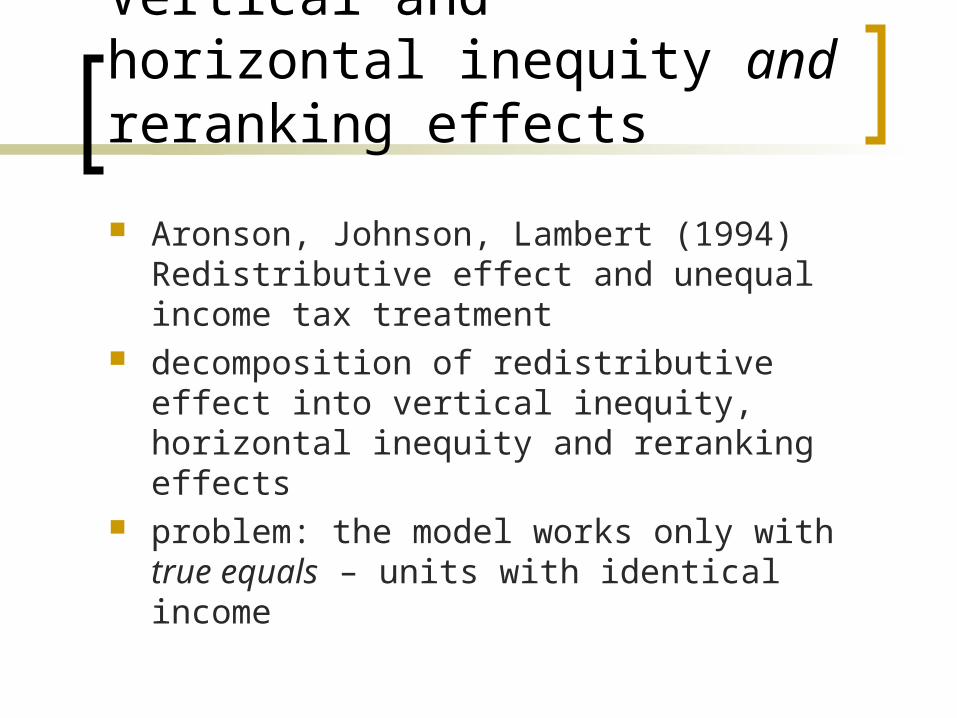

Vertical and horizontal inequity and reranking effects

Aronson, Johnson, Lambert (1994) Redistributive effect and unequal income tax treatment

decomposition of redistributive effect into vertical inequity, horizontal inequity and reranking effects

problem: the model works only with true equals – units with identical income

Vertical and horizontal inequity and reranking effects

AJLAJLAJL RHVRE

xNXX

xTx

xAJL DGGD

t

tV ~~

1

J

ijNjj

AJL GH1

,

APAJL RR

Vertical and horizontal inequity and reranking effects

Duclos, Jalbert and Araar (2003) Classical horizontal inequity and reranking: an integrated approach

DJADJADJA RHVRE

PNN

EN

PN

ENXNX IIIIIIIIRE

dpvpwpXUvWX ,,1

0

1/1yyU 11, vpvvpw

XX WU 1 xX

XI

1

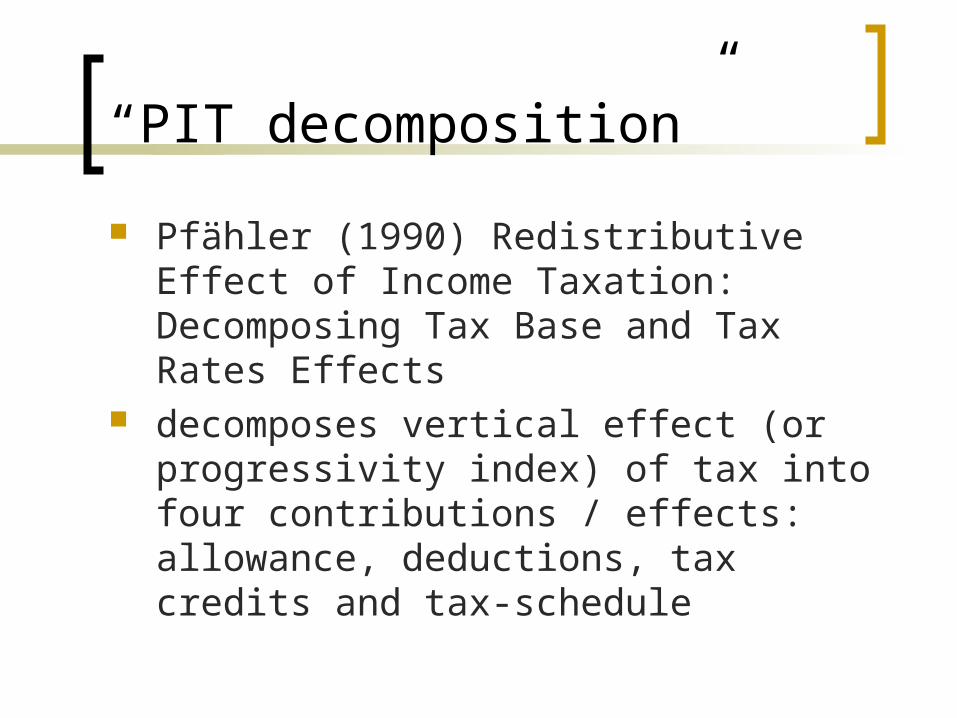

“PIT decomposition”

Pfähler (1990) Redistributive Effect of Income Taxation: Decomposing Tax Base and Tax Rates Effects

decomposes vertical effect (or progressivity index) of tax into four contributions / effects: allowance, deductions, tax credits and tax-schedule

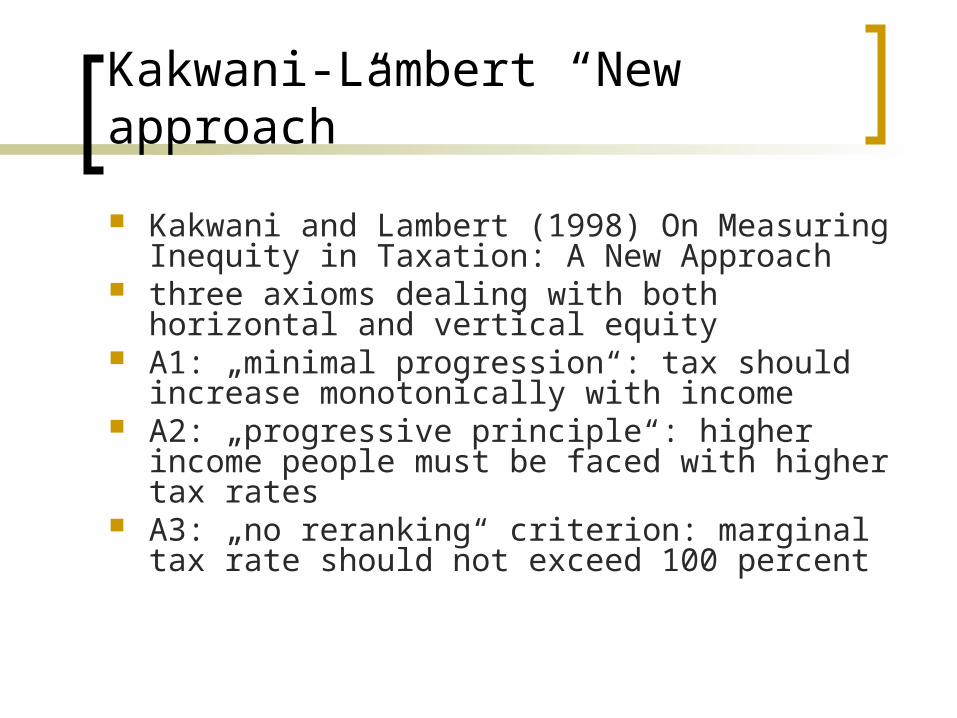

Kakwani-Lambert “New approach”

Kakwani and Lambert (1998) On Measuring Inequity in Taxation: A New Approach

three axioms dealing with both horizontal and vertical equity

A1: „minimal progression“: tax should increase monotonically with income

A2: „progressive principle“: higher income people must be faced with higher tax rates

A3: „no reranking“ criterion: marginal tax rate should not exceed 100 percent

Kakwani-Lambert “New approach”

321 SSSRPtRE AKn

3SPtRE Kn

from calculations based on Australian income tax data in 1984:

0.0240RE

0.1382 AKn RPt

xAAA DGR

(Kakwani decomposition)

RE could be improved by removal of inequities “without change to the marginal rate structure which governs incentives.”

Approach based on relative deprivation

Duclos (2000) Gini Indices and the Redistribution of Income

Gini coefficient can be represented as an average of relative deprivation in population

based on this principle the concepts of “fiscal harshness”, “fiscal looseness” and “ill-fortune” emerge

for each concept a measure is derived

Relative deprivation based approach

all the terms in Kakwani decomposition(s) are “reinvented” using these measures

Kakwani index of progressivity: a difference between the (mean-normalized average) fiscal harshness and average relative deprivation in the population.

Kakwani index of vertical inequity: a difference between the (mean-normalized average) relative deprivation and average fiscal looseness.

Atkinson-Plotnick index of reranking is (mean-normalised average) of ill-fortune in the population