Just the Facts Become NFIP & Flood Insurance...

56

Aon Affinity Proprietary & Confidential Just the Facts Become NFIP & Flood Insurance Savvy Note: These materials may become dated as NFIP rules and regulations change April 1, 2016

-

Upload

nguyenxuyen -

Category

Documents

-

view

220 -

download

4

Transcript of Just the Facts Become NFIP & Flood Insurance...

Aon Affinity

Proprietary & Confidential

Just the Facts

Become NFIP & Flood Insurance Savvy

Note: These materials may become dated as NFIP rules and

regulations change

April 1, 2016

HISTORY OF THE NFIP Established when Congress passed the

National Flood Insurance Act of 1968 Made flood insurance available for the first time

The Flood Disaster Protection Act of 1973 amended the 1968 Act Made the purchase of flood insurance mandatory for the protection

of properties located in Special Flood Hazard Areas (SFHAs)

1983: The Write-Your-Own Program Allows participating property and casualty insurance companies

to write and service Federal flood insurance in their own names

Administered by the Federal Insurance Administration, a component of the Federal Emergency Management Agency (FEMA)

Aon Affinity

Proprietary & Confidential

CONGRESSIONAL GOALS

Relieve the burden unforeseen flooding disasters place on the nation’s disaster relief resources

Authorize a program that over time could be made available across the country

Encourage state and local governments to consider possible flood hazards when determining the usage of lands under their jurisdiction

Flood Mitigation efforts

Aon Affinity

Proprietary & Confidential

Disaster Assistance

Federal disaster assistance declarations are awarded in less than 50% of flooding incidents

Most typical form of disaster assistance is a loan that must be repaid with interestAdministered by the Small Business Administration (SBA)

Average duration of a Small Business Administration (SBA) Disaster Assistance loan is 30 years

Individual and Household Program Award (IHP Award) approximately $31,900 (as of April,

2013)

Most forms of federal disaster assistance require a Presidential declaration

Aon Affinity

Proprietary & Confidential

Benefits of Flood Insurance

Property owner is in control

Claims are paid even if a disaster is not declared by the President

No payback requirement

Flood Insurance reimburses property owner for all covered losses up to policy limits or program maximums

$250,000 Homeowners

$500,000 Businesses

Who Needs Flood Insurance?

All owners of insurable property

Over the span of a 30 year mortgage

26% chance of Flood

versus

10% chance of Fire

Aon Affinity

Proprietary & Confidential

Relationship of Parties Within

The National Flood Insurance Program

Aon Affinity

Proprietary & Confidential

Where Can Flood Insurance Be Written?

As of August 4, 2015 – 22,085 participating communities

Refer to the Community Status Book at www.fema.gov/nfip for listing of

participating and non-participating communities by state

Aon Affinity

Proprietary & Confidential

Community Participation & Program Coverages

Emergency Program

Emergency Program Coverage LimitsBuildings: Single Family $ 35,000

Other Residential $100,000

Non-residential $100,000

Contents: Residential $ 10,000

Non-residential $100,000

Regular Program

Regular Program Coverage LimitsBuildings: Single Family Dwelling $250,000

2-4 Family Dwelling $250,000

Other Residential $500,000

Non-Residential $500,000

Contents: Residential $100,000

Non-Residential $500,000

Aon Affinity

Proprietary & Confidential

Definition of Flood (per the NFIP)

As stated in the Flood Insurance Manual

Two or more acres, normally dry land areas; ORtwo or more properties

Overflow of inland or tidal waters;

Accumulation / run off of surface waters

-ANY SOURCE;

Mudflow

Flooding

can even

happen

in the

winter

Photos of Mudflow versus Landslide

Landslide

Mudflow

Aon Affinity

Proprietary & Confidential

Single Peril Policy Coverage provided for Direct Physical Loss by or from

Flood only to the insured building and/or contents

Following items are not covered by the NFIP flood policy

Loss of revenue or profits

Loss of access to insured property

Loss from interruption of business or production

Any additional living expenses (ALE) incurred while the insured building is being repaired or is unstable for use for any reason

Cost of complying with any ordinance or law requiring demolition, remodeling, renovation or repair of property including removal of any resulting debris Does not apply to any eligible activities provided under Coverage D – Increase Cost of

Compliance (ICC)

Any other economic loss

Aon Affinity

Proprietary & Confidential

Coverage A and B

Coverage A – Building Coverage

Additions and extension

Detached garage

Materials and supplies for construction

Manufactured home or travel trailer

Coverage B – Personal Property Coverage

Property owned by the policyholder or household family members

At insureds option – property owned by guests or servants

Aon Affinity

Proprietary & Confidential

Coverage C

Coverage C – Other Coverages:DWELLING FORM:

Debris Removal

Loss Avoidance Measures

• Sandbags, supplies and labor

• Property removed to safety

Condominium Loss Assessment

GENERAL PROPERTY FORM

Debris Removal

Loss Avoidance Measures

• Sandbags, supplies and labor

• Property removed to safety

Pollution Damage

RESIDENTIAL CONDOMINIUM ASSOCATION POLICY (RCBAP)

Debris Removal;

Loss Avoidance Measures

• Sandbags, supplies and labor

• Property removed to safety

Aon Affinity

Proprietary & Confidential

Coverage D - Increased Cost of Compliance Policyholder may collect up to $30,000 in order to bring structure

into compliance with building codes (FRED)

Floodproof

Relocate

Elevate

Demolish

Policy Fees $4 - $70; dependent upon:

Flood zone

Date of construction

Amount of coverage purchased

Mandatory on all policies except contents only policies, condo unit policies or policies on properties in the emergency program

Applies to repetitive loss structure or substantially damaged structures when the community has a substantial damage or repetitive loss provision in its flood plain management law

Program Maximum Coverages apply

Eligible Properties

Aon Affinity

Proprietary & Confidential

Properties Not Eligible for Coverage

1316 Listed Properties

Coastal Barrier Resource System (CBRS) Properties

Container Type Buildings

Buildings Entirely Over Water

Buildings Partially Underground

Decks

Aon Affinity

Proprietary & Confidential

Examples of Ineligible Building Risks

Co-Op Units

Sports Stadiums

Gasoline Pump

Swimming Pool

Tent

Aon Affinity

Proprietary & Confidential

Ineligible Contents

Automobiles Bailee’s Goods Contents located in an ineligible

structure Contents located in a building not

fully enclosedUnder the Dwelling Form, coverage provided as long as

contents are secured to prevent flotation out of the building

Motorcycles Aircraft, watercraft, trailers, and

recreational vehicles, including their furnishings or equipment

Accounts, bills, coins, currency, etc

A car

can

easily be

carried

away by

just two

feet of

water

Aon Affinity

Proprietary & Confidential

Special Considerations

Renters Coverage

Condo Unit

Fine Arts, Collectibles and Business Contents

$2500 limit of liability

Subject to deductible

Aon Affinity

Proprietary & Confidential

Policies Available STANDARD FLOOD INSURANCE POLICY (SFIP)

Dwelling Form Actual Cash Value (ACV) policy with Replacement Cost

provision • Principal Residence

• 80% of Replacement Cost or Program Maximum

General Property Form Actual Cash Value (ACV)

No replacement cost option

Residential Condominium Building Association Policy (RCBAP)

Co-insurance penalty

Aon Affinity

Proprietary & Confidential

Additional Insurance Products Preferred Risk Policy (PRP)

Low-cost coverage for eligible buildings located in low to moderate flood zones – B, C, X only

Combined building/contents amounts of insurance available for eligible occupancy types up to the maximums allowable for the program

1-4 family, individual condominium units, other residential and non-residential properties

Contents only coverage available for eligible occupancies

No Elevation Certificates required

Eligibility based on flood loss history on the property

Newly Mapped Policy New procedure for structures Newly Mapped from a Non-Special

Flood Hazard Area (non-SFHA) to a Special Flood Hazard Area (SFHA)

Mortgage Portfolio Protection Program (MPPP) Forced place coverage

Only a few

inches of

water in

your home

can cost

tens of

thousands

of dollars in

damage.

25-30%of Flood

Insurance

Claims

originate in

LOW to

Moderate

RISK

areas

Aon Affinity

Proprietary & Confidential

Exclusion - LOSS IN PROGRESS

The NFIP does not insure for a loss directly or indirectly caused by a flood that is already in progress at the time and date:

1. The policy term begins or

2. Coverage is added at your request

Aon Affinity

Proprietary & Confidential

Exclusion - EARTH MOVEMENT

Losses to property caused directly by earth movement even if the earth movement is caused by flood, are not covered. Some examples of earth movement not covered are:

1. Earthquake2. Landslide3. Land subsidence4. Sinkholes5. Destabilization or movement of land that results from

accumulation of water in subsurface land area6. Gradual erosion

However losses from mudflow and land subsidence as a result of erosion that are specifically covered under the definition of flood (See II.A.1.c and II.A.2)

Aon Affinity

Proprietary & Confidential

Exclusion - WATER, MOISTURE,

MILDEW OR MOLD

The NFIP does not insure for direct

physical loss caused directly or indirectly by:

Water, moisture, mildew, or mold damage that results primarily from any condition:

That is within the insureds control, including but not limited to:

1. Design, structural, or mechanical defects;

2. Failure, stoppage, or breakage of water or sewer lines, drains, pumps, fixtures or equipment, or;

3. Failure to inspect and maintain the property after a flood recedes

Aon Affinity

Proprietary & Confidential

Exclusion - SEWER BACK-UP AND SEEPAGE

There is no coverage for direct physical loss caused directly or indirectly by:

Water or waterborne material that:a. Backs up through sewers or drains

b. Discharges or overflows from a sump, sump pump or related equipment of

c. Seeps or leaks on or through the covered property;

Unless there is a flood in the area and the flood is the proximate cause of the sewer or drain backup, sump pump discharge or overflow, or seepage of water

Aon Affinity

Proprietary & Confidential

Exclusion - HYDROSTATIC PRESSURE

No coverage for direct physical loss caused directly or indirectly by:

The pressure or weight of water unless there is a flood in the area and the flood is the proximate cause of the damage from the pressure or weight of water

Aon Affinity

Proprietary & Confidential

Additional Exclusions Following are additional exclusions found in

the NFIP flood policyPower, heating or cooling failure unless failure results

from direct physical loss by or from flood to power, heating or cooling equipment on insured premises

Theft, fire, explosion, wind or windstormAnything the insured or a family member of the

household conspire to do to cause loss by flood deliberately

Alteration of the insured property that significantly increases the risk of flooding

No coverage for loss to any building or personal property located on land leased from the Federal Government

Policy does not pay for testing for or monitoring of pollutants unless required by law or ordinance

Aon Affinity

Proprietary & Confidential

Deductibles Apply separately to building and contents All Full Risk Zones– A, AE, A01-A30, AH, AO, V, VE, V01-V30,

AR/AR Dual with Elevation Data and B, C, X, A99 and D Building coverage does not exceed $100,000 - $1,000 for building or contents Building coverage exceeds $100,000 - $1,250 for building or contents

All Pre-FIRM subsidized zones – Zones A, AE, A01-A30, AH, AO, V, VE, V01-V30, AR/AR Dual without Elevation Data Building coverage does not exceed $100,000 - $1,500 for building or contents Building coverage exceeds $100,000 - $2,000 for building or contents

Contents only Contents only policies will use the same minimum deductibles that apply to building

coverage that does not exceed $100,000

Preferred Risk Policies (PRP) Building coverage does not exceed $100,000 - $1,000 Building coverage exceeds $1,000 - $1,250

Emergency Program Building coverage does not exceed $100,000 - $1,500 for building and/or contents Building coverage exceeds $100,000 - $2,000 for building or contents

Aon Affinity

Proprietary & Confidential

Effective Dates

Voluntary Purchase and Lender Portfolio Review 30-Day Waiting Period from the date of

application and presentment of premium

10 day window

Loan Closing 30 day wait waived

Map Revision 1 day wait applied

10 day window

If a loss

occurs

during the

first 30 days

of a policy,

proof of

lender

requirement

will be

required

BINDING

AUTHORITY

Aon Affinity

Proprietary & Confidential

Flood Facts

Flood Policy Duration - 1 year

Policy Renewal Process 30 Day Grace Period, no lapse

31st-90th days – lapse in coverage with reinstatement

After 91st day policy officially lapses, no reinstatement

Community Rating System (CRS) Voluntary program for National Flood Insurance Program (NFIP)

participating communities

Goals are to reduce flood damages to insurable properties, strengthen and support the National Flood Insurance Program (NFIP) and encourage a comprehensive approach to floodplain management

Developed to provide incentives in the form of premium discounts for communities to go beyond minimum floodplain management requirements

Discounts range 5%-45%

Aon Affinity

Proprietary & Confidential

Flood Insurance Policy Fees Federal Policy Fee

Mandated by Congress

Standard Policy (includes Newly Mapped) - $50

Preferred Risk Policy (PRP) - $25

Community Probation Surcharge All impacted polices - $50 per policy

Reserve Fund Assessment PRP – 15%

Newly Mapped – 15%

All other policies – 15%

Homeowners Flood Insurance Affordability Act (HFIAA) Surcharge Primary Residences = $25

Non-Primary Residences = $250

Non-Residential Buildings/Non-Condominium Multi-Family Buildings = $250

Aon Affinity

Proprietary & Confidential

Flood Maps

Flood Hazard Boundary Map (FHBM)

Flood Insurance Rate Map (FIRM)

Base Flood Elevation (BFE)

Aon Affinity

Proprietary & Confidential

Pre-FIRM versus Post-FIRM

Was the building constructed prior to 12/31/1974? If ‘yes’, the building is Pre-FIRM

If ‘no’, ask:

What is the community’s FIRM date? Community Status Listing

Was the building constructed after the FIRM date? If ‘yes’ – building is Post-FIRM

If ‘no’ – building is Pre-FIRM

1974 Date Community Entered Program

Always Pre FIRM Pre FIRM Post-FIRM

Elevation Certificates

Aon Affinity

Proprietary & Confidential

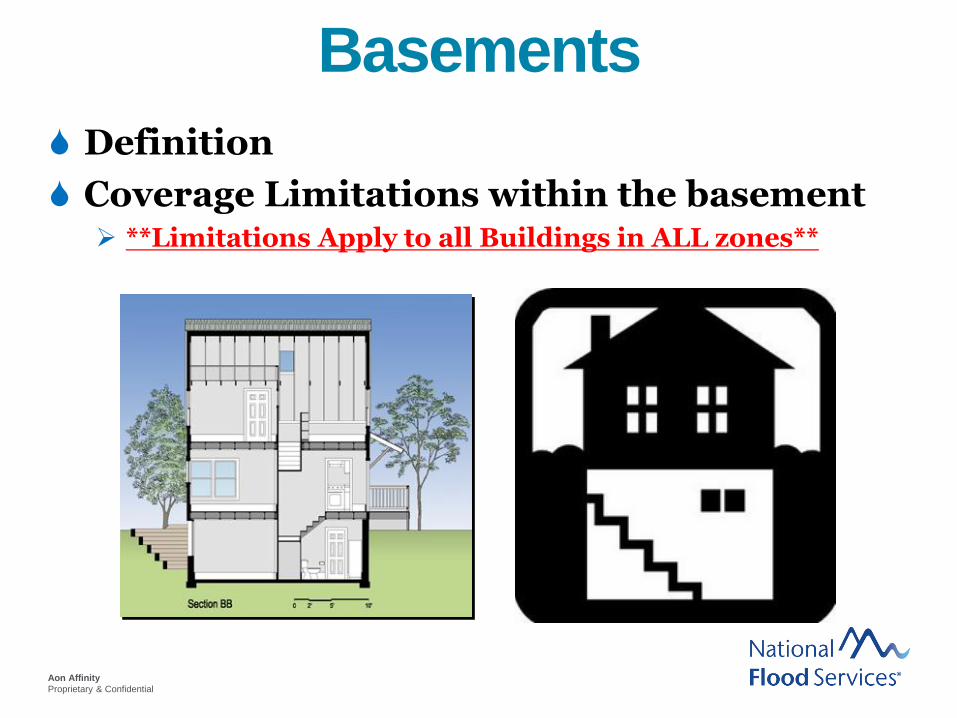

Basements

Definition

Coverage Limitations within the basement **Limitations Apply to all Buildings in ALL zones**

Aon Affinity

Proprietary & Confidential

Elevated Buildings

Definition

Coverage Limitations within EnclosureApplies only to Post-Firm buildings in Special

Flood Hazard Areas (SFHAs) designated in Zones A1-A30, AE, AH, AR, AR Dual Zones, and V1-V30, VE

Aon Affinity

Proprietary & Confidential

Condominium Associations

High Rise Condominiums

3 or more floors; 5 or more units

Maximum coverage available = number of units x $250,000 or replacement cost, whichever is less

Low Rise Condominiums

Less than 5 units; 5 or more units but less than 3 floors

Townhouse/Rowhouse Condominiums

Maximum coverage available = number of units per building x $250,000 or the replacement cost, whichever is less

Contents

Basic limit of insurance = $25,000

Maximum amount of insurance available = $100,000

Aon Affinity

Proprietary & Confidential

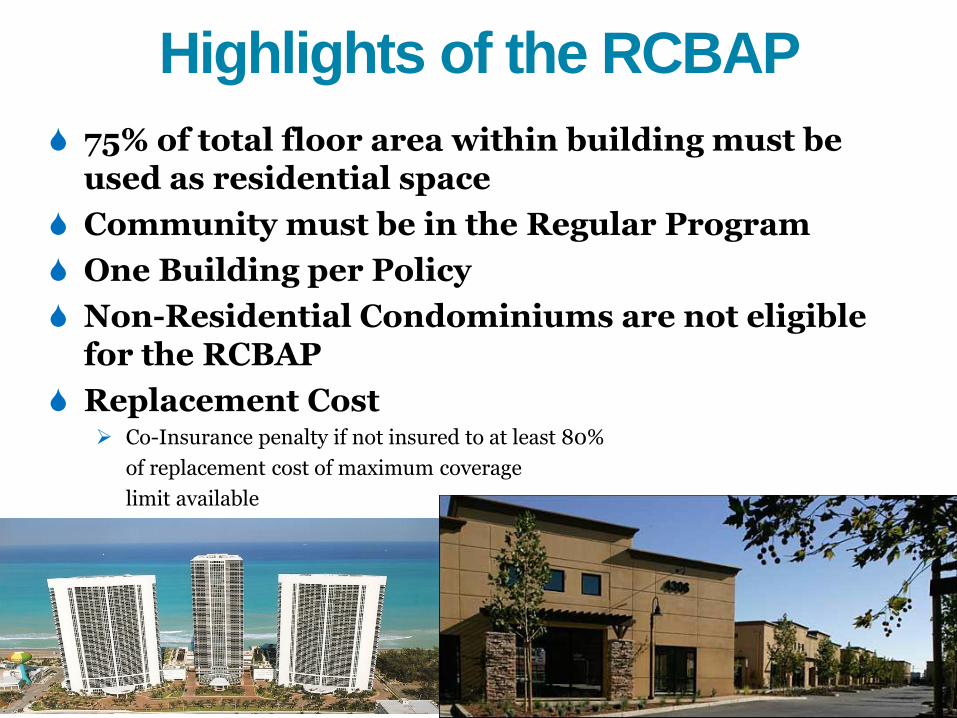

Highlights of the RCBAP

75% of total floor area within building must be used as residential space

Community must be in the Regular Program

One Building per Policy

Non-Residential Condominiums are not eligible for the RCBAP

Replacement Cost Co-Insurance penalty if not insured to at least 80%

of replacement cost of maximum coverage

limit available

Aon Affinity

Proprietary & Confidential

Condominium Units

Written under the Standard Flood Insurance Policy

Dwelling Form

May purchase building and/or contents coverages

Rated as single family structures

Unit owner policy contains Assessment coverage

Non-Residential condominium unit owners can only purchase contents coverage

Aon Affinity

Proprietary & Confidential

Flood Insurance Reform Act of 2004 (FIRA)

Aon Affinity

Proprietary & Confidential

Biggert-Waters Flood Insurance Reform Act of 2012 (BW12) Reform Act passed July 6, 2012

Implemented in stages

Section 205 effective 10/1/2013 Premium and Rate Increases

Premiums will increase an average of 10% for policies written or renewed on or after 10/1/13

Reserve Fund established

Introduction of Reserve Fund

Federal Policy Fee Increases

Elimination of No Waiting Period due to Lender Requirement Applies to a new application when the lender determines that a loan on a building in an

SFHA that requires flood insurance does not have it

NFIP Form changes

Aon Affinity

Proprietary & Confidential

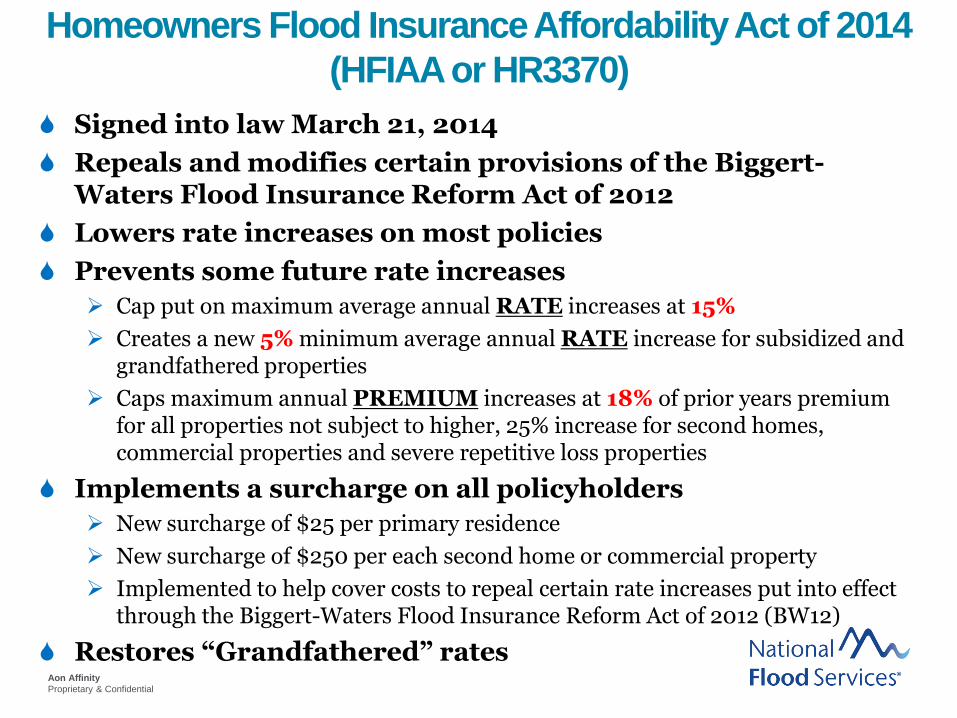

Homeowners Flood Insurance Affordability Act of 2014

(HFIAA or HR3370)

Signed into law March 21, 2014

Repeals and modifies certain provisions of the Biggert-Waters Flood Insurance Reform Act of 2012

Lowers rate increases on most policies

Prevents some future rate increases

Cap put on maximum average annual RATE increases at 15%

Creates a new 5% minimum average annual RATE increase for subsidized and grandfathered properties

Caps maximum annual PREMIUM increases at 18% of prior years premium for all properties not subject to higher, 25% increase for second homes, commercial properties and severe repetitive loss properties

Implements a surcharge on all policyholders

New surcharge of $25 per primary residence

New surcharge of $250 per each second home or commercial property

Implemented to help cover costs to repeal certain rate increases put into effect through the Biggert-Waters Flood Insurance Reform Act of 2012 (BW12)

Restores “Grandfathered” rates

Aon Affinity

Proprietary & Confidential

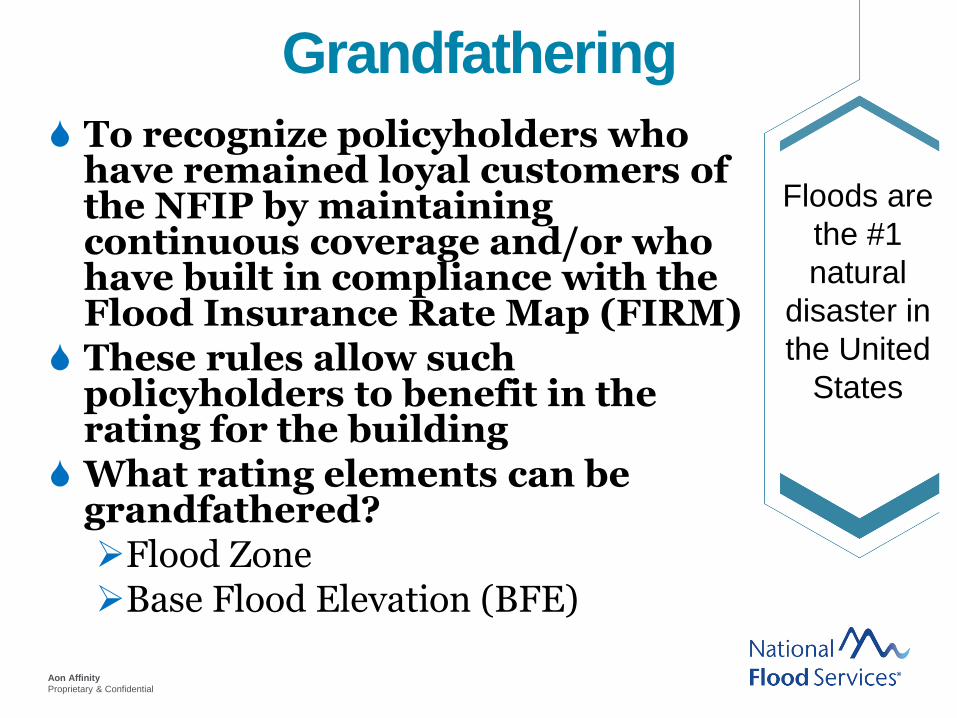

Grandfathering

To recognize policyholders who have remained loyal customers of the NFIP by maintaining continuous coverage and/or who have built in compliance with the Flood Insurance Rate Map (FIRM)

These rules allow such policyholders to benefit in the rating for the building

What rating elements can be grandfathered?Flood ZoneBase Flood Elevation (BFE)

Floods are

the #1

natural

disaster in

the United

States

Aon Affinity

Proprietary & Confidential

Reduction and Reformation of Coverage

Policies issued with reduced coverage amounts due to insufficient premium or incomplete rating information can

be reformed following NFIP guidelines

Discovery of insufficient premium or incomplete rating information before a loss:

Request sent for additional premium or required information

If not received by due date, changes/corrections can only be made by endorsement subject to appropriate waiting period

Discovery of insufficient premium or incomplete rating information after a loss:

Coverage reduced due to insufficient premium – request sent for additional premium. If received within 30- days of notice, coverage will be reformed to original amounts requested back to inception date of policy

Coverage reduced due to incomplete rating information – required information must be submitted before claim can be settled

Cancellations

A flood policy may be cancelled at any time

BUT

A refund of premium money will only be made when a validreason for cancellation is

provided

What Do I Do If

I Have a Loss?

Aon Affinity

Proprietary & Confidential

Fax: 406-257-1629

Telephone Toll Free: 800-759-8656

Monday - Friday

(Mountain Time) 6:00 a.m. – 6:00 p.m.

Aon Affinity

Proprietary & Confidential

Errors & Omissions Concerns

Failure to offer Coverage Offer Building coverage

Offer Contents coverage

Offer Excess coverage

Did you get a signed Waiver / Rejection Form?

Aon Affinity

Proprietary & Confidential

Errors & Omissions Concerns

One Building per Policy Additions and Extensions

Common Wall Scenarios

One (1) policy or two (2)?

Aon Affinity

Proprietary & Confidential

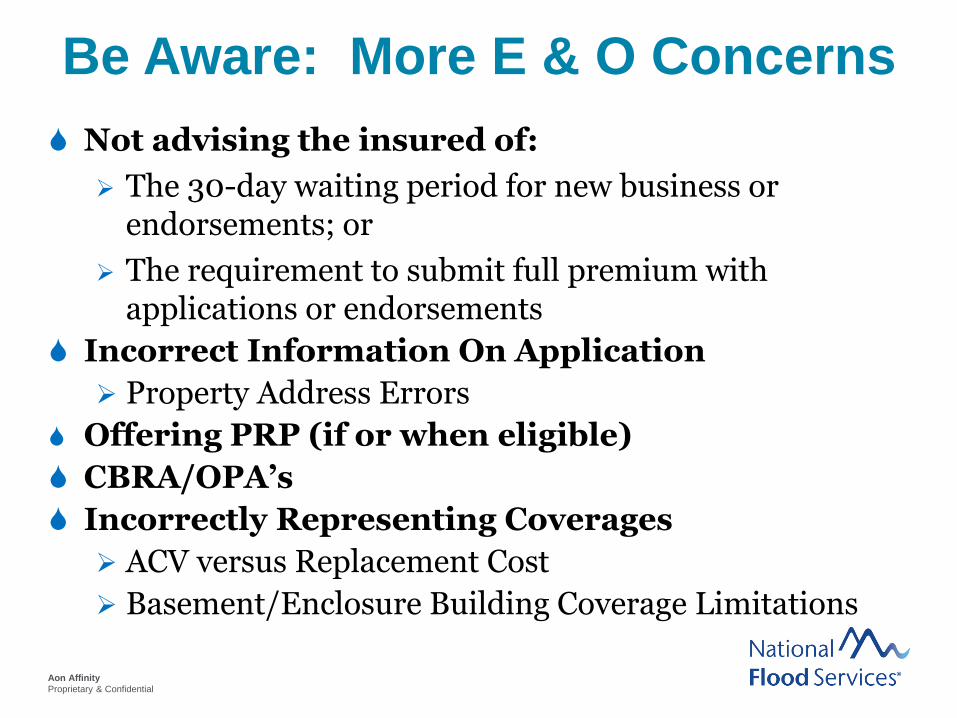

Be Aware: More E & O Concerns

Not advising the insured of:

The 30-day waiting period for new business or endorsements; or

The requirement to submit full premium with applications or endorsements

Incorrect Information On Application

Property Address Errors

Offering PRP (if or when eligible)

CBRA/OPA’s

Incorrectly Representing Coverages

ACV versus Replacement Cost

Basement/Enclosure Building Coverage Limitations

Aon Affinity

Proprietary & Confidential

Connect with Us

Aon Affinity

Proprietary & Confidential

National Flood Services Inc

PO Box 2057

Kalispell, MT 59903-2057

Opt In to NFS email communications http://www2.floodresource.com/l/34032/2015-02-06/3gbb7p

Write Your Own (WYO) Company

NFIP and FEMA resources

www.nfipiservie.com

www.fema.gov/nfip

www.floodsmart.gov

www.agents.floodsmart.gov