Jussi Pesonen President and CEO 29 April, 2009 › siteassets › asset › investors › ...Jussi...

30

UPM Q1 RESULTS 2009 Jussi Pesonen President and CEO 29 April, 2009

Transcript of Jussi Pesonen President and CEO 29 April, 2009 › siteassets › asset › investors › ...Jussi...

UPM Q1 RESULTS 2009

Jussi PesonenPresident and CEO

29 April, 2009

UPM 2

Q1 2009 in brief

Demand for paper, labels, plywood and sawn timber declined significantly - competing devaluations further affected sales from Finland

The company reported an operating loss due to low delivery volumes, despite increases in paper and label prices and cost savings

Focus on cash preservation and cost savings– Operating cash flow was €274 million (€50 million)– Restructuring and flexible way of operating saved costs

Liquidity remained good. The new revolving credit facility was signed in March

UPM 3

24,039

274

-0.27

-78

-17

-95

6.9

128

1,857

Q1/2009

25,841

50

0.19

188

5

193

14.0

337

2,410

Q1/2008

24,983

628

0.42

513

-489

24

12.7

1,206

9,461

2008

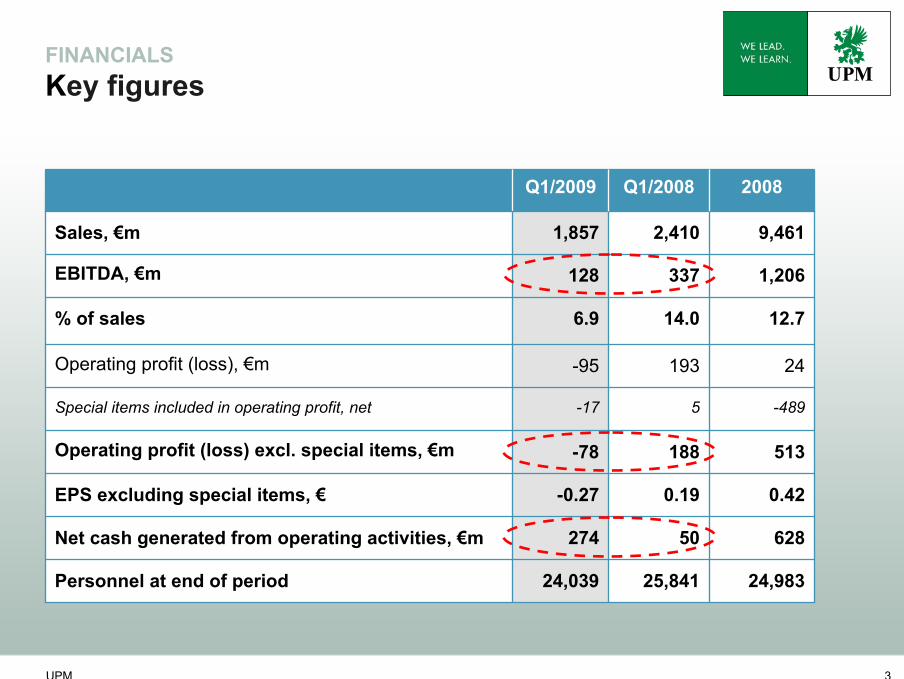

EBITDA, €m

% of sales

Net cash generated from operating activities, €m

Personnel at end of period

Operating profit (loss) excl. special items, €m

Special items included in operating profit, net

EPS excluding special items, €

Operating profit (loss), €m

Sales, €m

FINANCIALSKey figures

UPM 4

-75

-50

-25

0

25

50

75

100

125

150

175

200

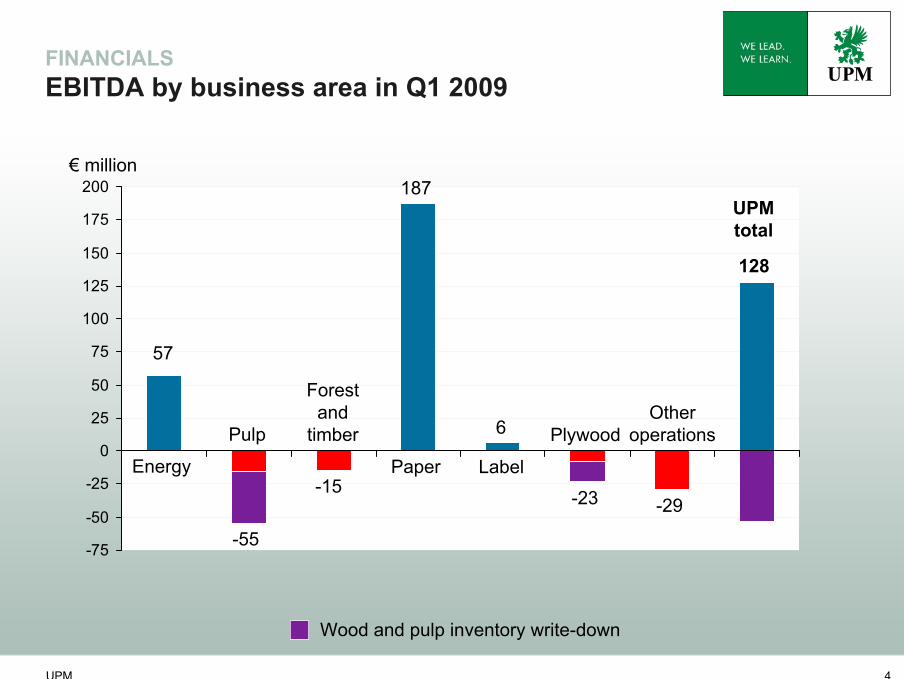

FINANCIALSEBITDA by business area in Q1 2009

57

Energy

Pulp

Forestand

timber

Paper Label

Plywood

€ million

-55

-15

187

6

-23 -29

UPMtotal

128

Wood and pulp inventory write-down

Otheroperations

UPM 5

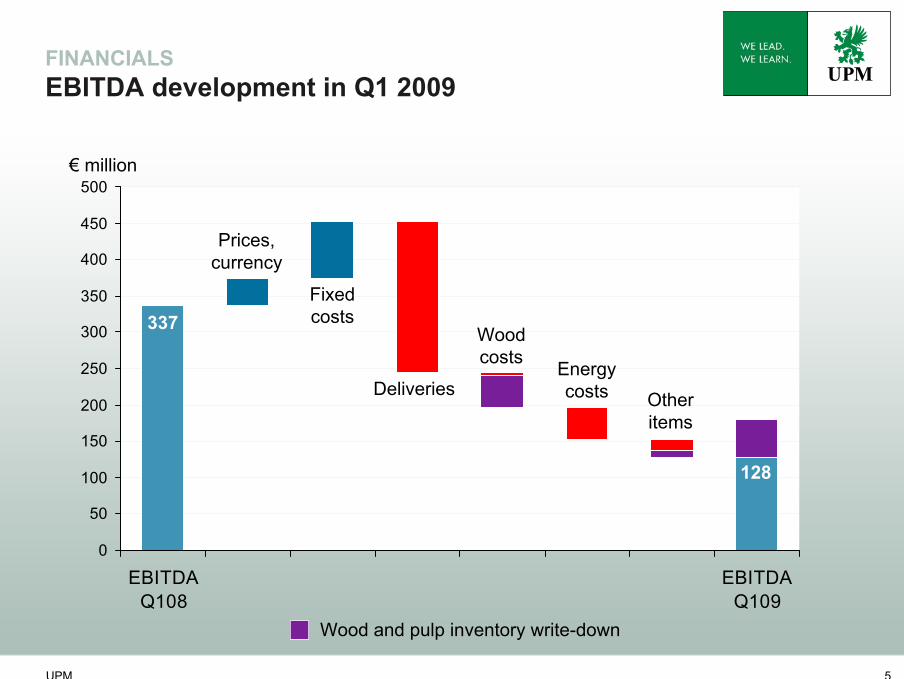

FINANCIALSEBITDA development in Q1 2009

0

50

100

150

200

250

300

350

400

450

500

EBITDAQ108

EBITDAQ109

€ million

337

128

Prices, currency

Deliveries

Wood costs Energy

costs Otheritems

Fixed costs

Wood and pulp inventory write-down

UPM 6

-100

-80

-60

-40

-20

0

20

40

60

80

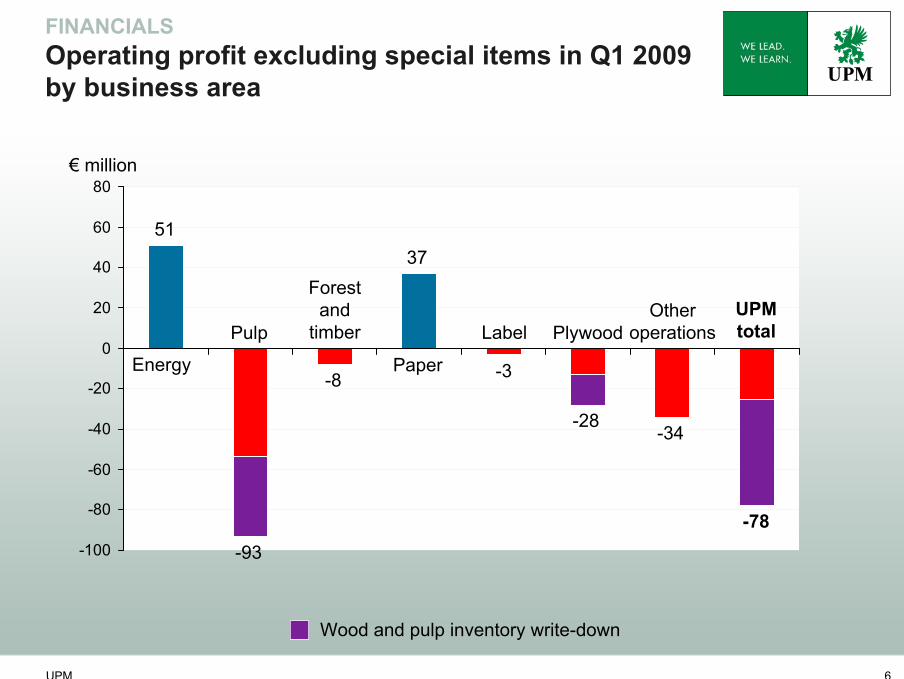

FINANCIALSOperating profit excluding special items in Q1 2009 by business area

51

Energy

Pulp

Forestand

timber

Paper

Label PlywoodOther

operations

€ million

-93

-8

37

-3

-28-34

UPMtotal

-78

Wood and pulp inventory write-down

UPM 7

FINANCIALSOperating in a low-demand environment Case Paper

Sales declined by 22%Higher prices maintainedSignificant reduction in fixed costs through restructuring and flexible way of workingLower pulp costs compensated for the increase in energy costs

EBITDA margin increased to 13.7% (11.8%)

-4%-1%-22%Sales growth, %

10,6412,7532,028Paper deliveries, 1,000 t

885209187EBITDA, M€

0%

50

11.8

1,773

Q1 2008

12,613.7EBITDA, % of sales

-26%

37

1,367

Q1 2009

-7%Paper deliveries, % change

250Operating profit, M€excl. special items

7,011Sales, M€

2008Paper

DEMAND AND DELIVERIES

UPM 9

-9,0

-7,4

-5,9

-4,3

-2,8

-1,2

0,3

1,9

3,4

5,0

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009-25

-20

-15

-10

-5

0

5

10

15

20

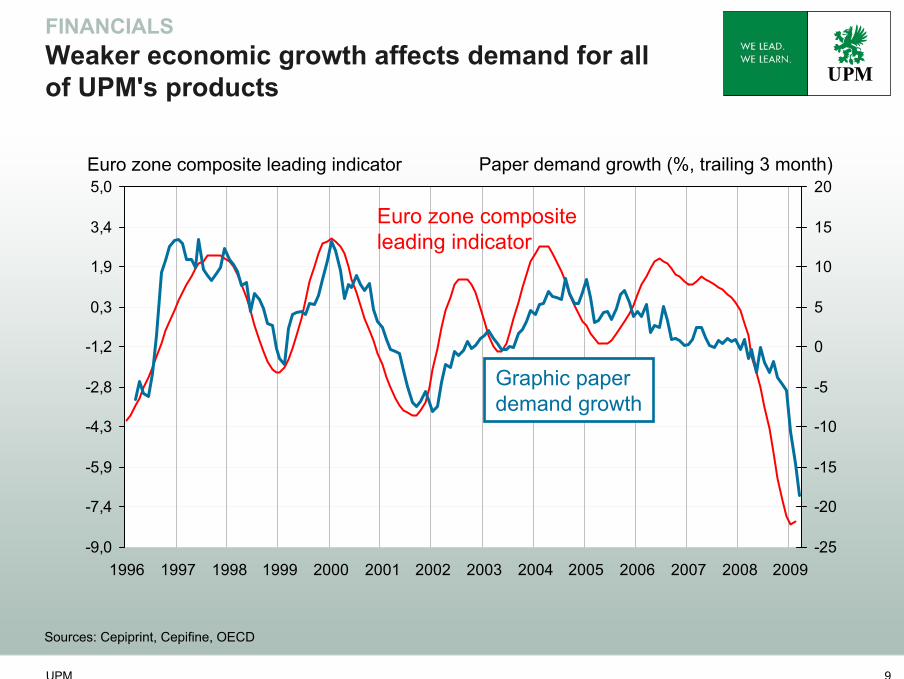

FINANCIALSWeaker economic growth affects demand for all of UPM's products

Paper demand growth (%, trailing 3 month)

Sources: Cepiprint, Cepifine, OECD

Euro zone composite leading indicator

Graphic paper demand growth

Euro zone composite leading indicator

UPM 10

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

Europe Exports

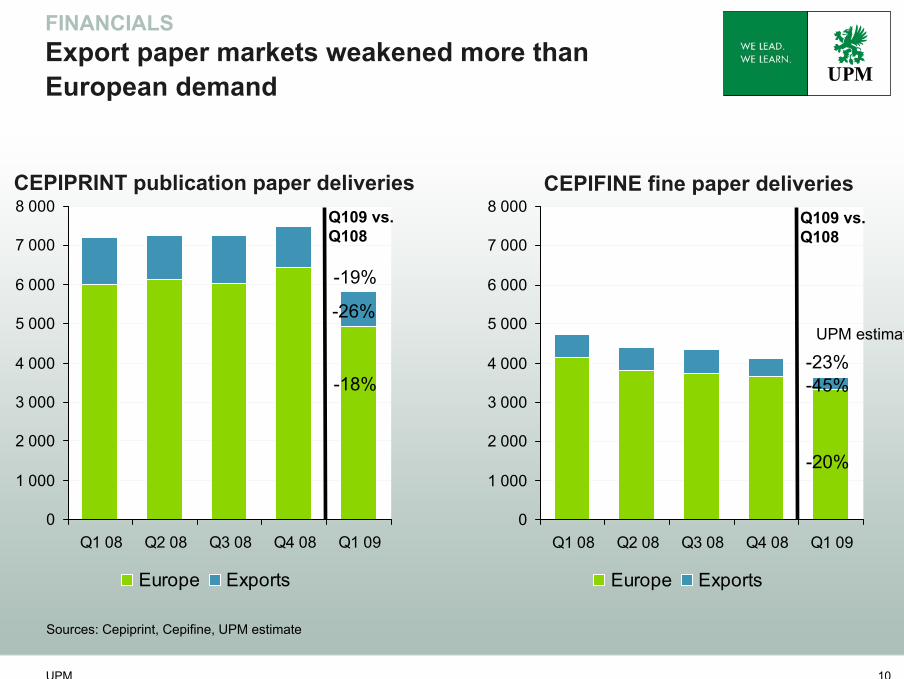

FINANCIALSExport paper markets weakened more than European demand

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

Europe Exports

Sources: Cepiprint, Cepifine, UPM estimate

-19%

-18%

-26%

-23%

-20%

-45%

CEPIPRINT publication paper deliveries CEPIFINE fine paper deliveriesQ109 vs. Q108

Q109 vs. Q108

UPM estimate

UPM 11

-80

-70

-60

-50

-40

-30

-20

-10

0

10

20

Q107 Q207 Q307 Q407 Q108 Q208 Q308 Q408 Q109

Publication papers Fine and speciality papers Sawn timber Plywood

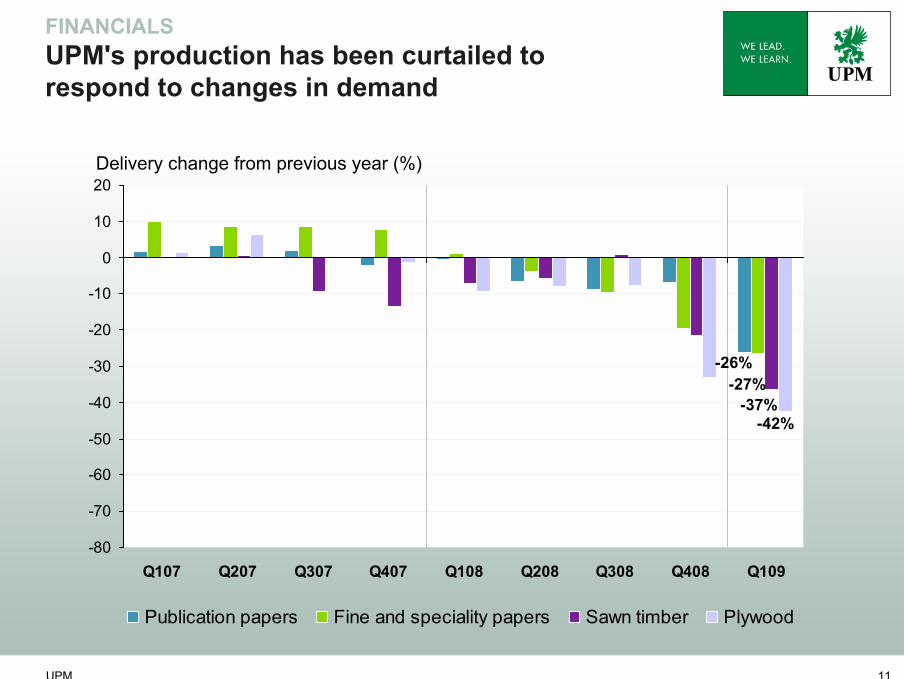

FINANCIALSUPM's production has been curtailed to respond to changes in demand

Delivery change from previous year (%)

-26%-27%

-37%-42%

PRICES AND COSTS

UPM 13

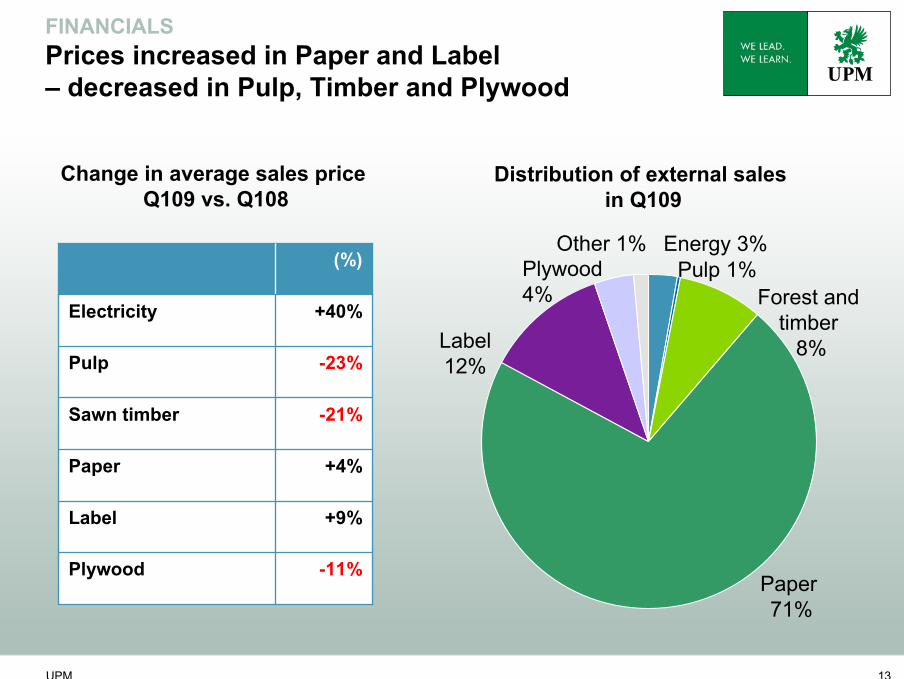

FINANCIALSPrices increased in Paper and Label – decreased in Pulp, Timber and Plywood

-11%Plywood

+9%Label

+4%Paper

-21%Sawn timber

-23%Pulp

+40%Electricity

(%)

Change in average sales price Q109 vs. Q108

Distribution of external sales in Q109

Paper 71%

Forest and timber

8%

Pulp 1%Energy 3%

Label12%

Plywood4%

Other 1%

UPM 14

10

11

12

13

14

15

16

17

18

19

20

2004 2005 2006 2007 2008 2009

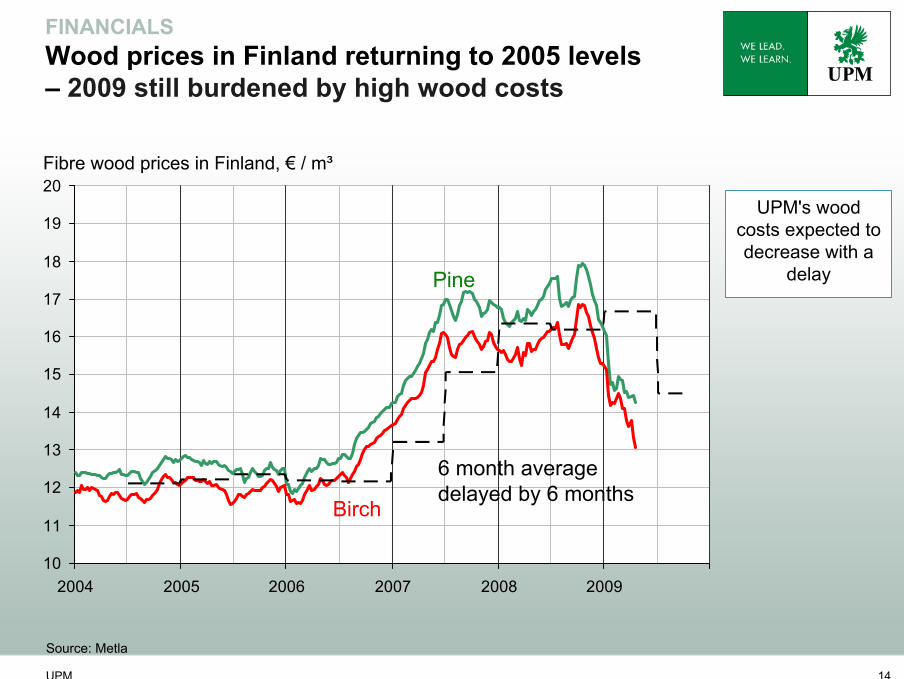

FINANCIALSWood prices in Finland returning to 2005 levels – 2009 still burdened by high wood costs

Fibre wood prices in Finland, € / m³

Source: Metla

UPM's wood costs expected to decrease with a

delay

Birch

Pine

6 month averagedelayed by 6 months

UPM 15

80

90

100

110

120

130

140

150

160

170

2005 2006 2007 2008 200980

90

100

110

120

130

140

150

160

170

2005 2006 2007 2008 2009

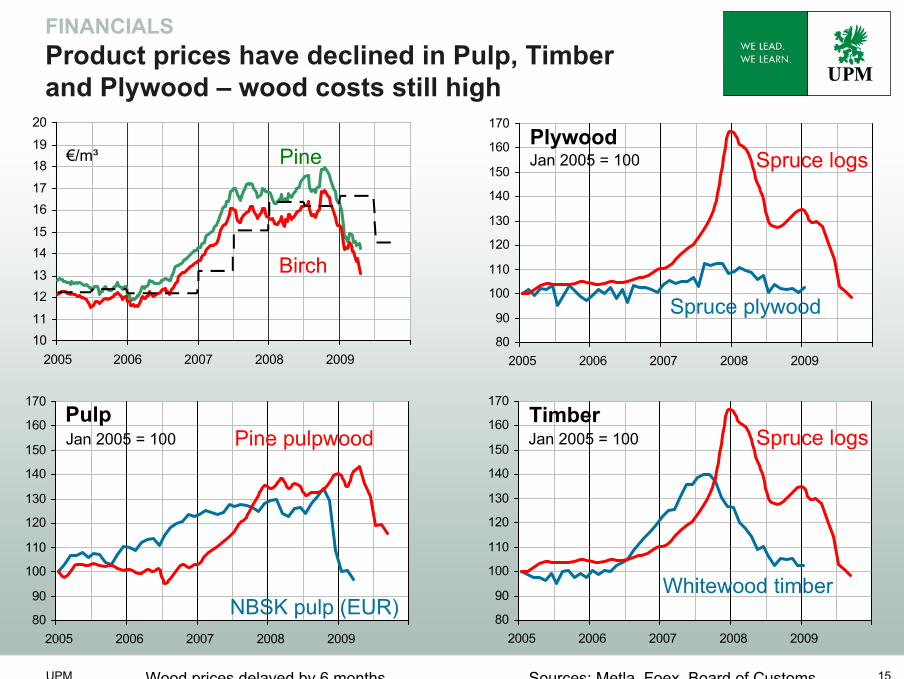

FINANCIALSProduct prices have declined in Pulp, Timber and Plywood – wood costs still high

80

90

100

110

120

130

140

150

160

170

2005 2006 2007 2008 2009

Pine pulpwood

NBSK pulp (EUR)

Spruce logs

Spruce plywood

Spruce logs

Whitewood timber

Wood prices delayed by 6 months Sources: Metla, Foex, Board of Customs

Pulp

Plywood

Timber

1011

1213

1415

1617

1819

20

2005 2006 2007 2008 2009

Birch

Pine Jan 2005 = 100

Jan 2005 = 100Jan 2005 = 100

€/m³

UPM 16

0

10

20

30

40

50

60

70

80

90

100

2004 2005 2006 2007 2008 20090

15

30

45

60

75

90

105

120

135

150

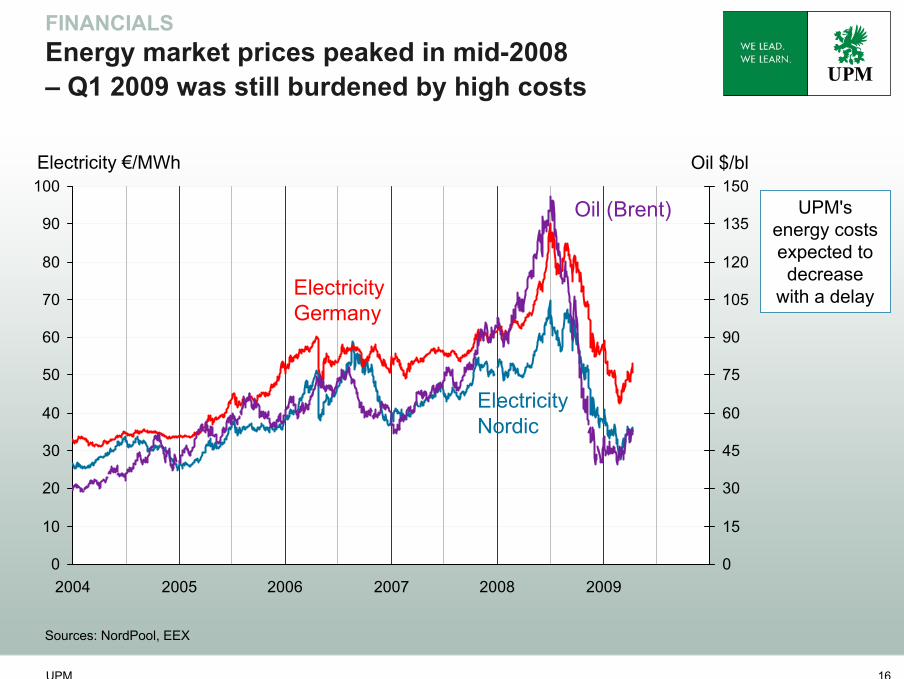

FINANCIALSEnergy market prices peaked in mid-2008 – Q1 2009 was still burdened by high costs

Electricity €/MWh

Sources: NordPool, EEX

Oil $/bl

ElectricityNordic

ElectricityGermany

Oil (Brent) UPM's energy costs expected to decrease

with a delay

FINANCIALS

UPM 18

210

14

196

-78

274

-73

216

131

128

Q1 2009

-121

4

-125

-175

50

-99

-106

255

337

Q1 2008

70Cash flow after capex

-292Finance costs and income taxes

-558Capital expenditure

26Asset sales and acquisitions

96Cash flow after investing activities

-132Change in working capital

628Net cash from operating activities

1,052Cash flow before change in working capital

1,206EBITDA

2008€, million

FINANCIALSCash flow

UPM 19

0

200

400

600

800

1000

04 05 06 07 08 09e

FINANCIALS Capital expenditure2009 estimate lowered to € 300 million

€ million

Depreciation excl. amortization of goodwill

Strategic investments

Operational investments

551

300

Estimate

Q1 2009 capital expenditure was € 67 million

UPM 20

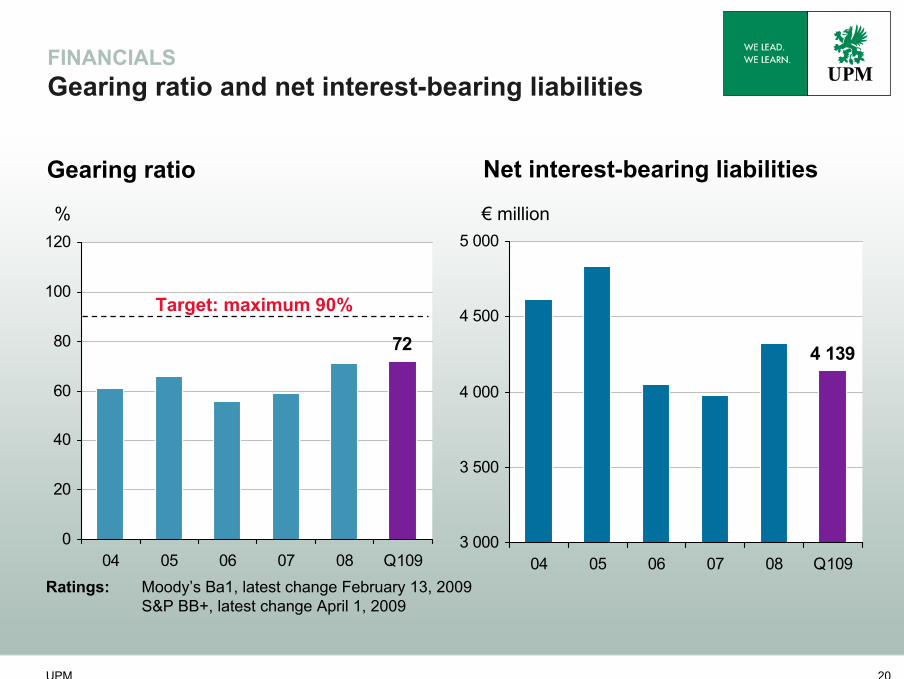

4 139

3 000

3 500

4 000

4 500

5 000

04 05 06 07 08 Q109

72

0

20

40

60

80

100

120

04 05 06 07 08 Q109

Gearing ratio Net interest-bearing liabilities

% € million

Target: maximum 90%

FINANCIALS Gearing ratio and net interest-bearing liabilities

Ratings: Moody’s Ba1, latest change February 13, 2009S&P BB+, latest change April 1, 2009

UPM 21

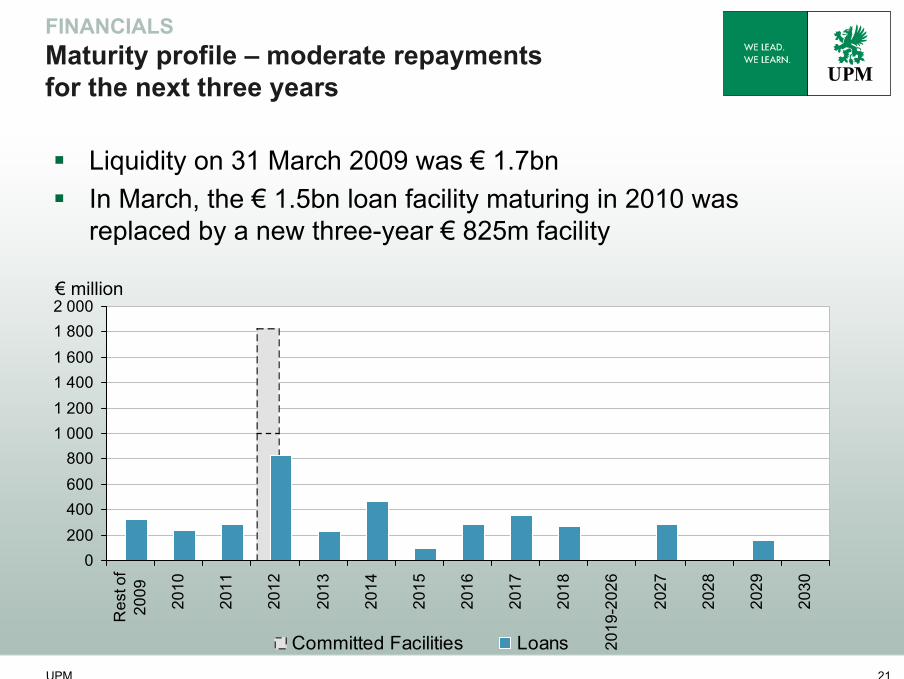

0200400600800

1 0001 2001 4001 6001 8002 000

Res

t of

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

-202

6

2027

2028

2029

2030

Committed Facilities Loans

Liquidity on 31 March 2009 was € 1.7bnIn March, the € 1.5bn loan facility maturing in 2010 was replaced by a new three-year € 825m facility

FINANCIALSMaturity profile – moderate repayments for the next three years

€ million

UPM 22

Outlook for 2009 (*

Economic activity in main markets contracts during 2009

For UPM this is expected to mean:- weak demand in most of products continues- markedly lower deliveries than in 2008 and long production downtime- increased competition and potential loss of sales due tocompeting devaluations (e.g. SEK, GBP and Rouble)

- lower wood costs for the group will materialize with a delay

UPM's own actions continue:- Focus on cost saving and cash preservation- Lower capital expenditure – new estimate €300 million

(* See complete wording of the "Outlook" in the Interim Report Q1 2009

UPM 23

It should be noted that certain statements herein which are not historical facts, including, without limitation, those regarding expectations for market growth and developments; expectations for growth and profitability; and statements preceded by "believes", "expects", "anticipates", "foresees", or similar expressions, are forward-looking statements. Since these statements are based on current plans, estimates and projections, they involve risks and uncertainties which may cause actual results to materially differ from those expressed in such forward-looking statements. Such factors include, but are not limited to: (1) operating factors such as continued success of manufacturing activities and the achievement of efficiencies therein including the availability and cost of production inputs, continued success of product development, acceptance of new products or services by the Group's targeted customers, success of the existing and future collaboration arrangements, changes in business strategy or development plans or targets, changes in the degree of protection created by the Group's patents and other intellectual property rights, the availability of capital on acceptable terms; (2) industry conditions, such as strength of product demand, intensity of competition, prevailing and future global market prices for the Group's products and the pricing pressures thereto, financial condition of the customers and the competitors of the Group, the potential introduction of competing products and technologies by competitors; and (3) general economic conditions, such as rates of economic growth in the Group's principal geographic markets or fluctuations in exchange and interest rates.

Forward-looking statement

UPM 24

UPM 25

FINANCIALSEnergy

Operating profit improvedSales increased by 30%Average sales price for electricity increased by 40%

0

20

40

60

80

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

€, million

33

5131.4%

37.5%

n.a.40%Average price, change %

2.5

51

136

Q1 2009

2.4Electricity sales, TWh

33Operating profit M€excl. special items

105Sales, M€

Q1 2008

Operating profit excluding special items

UPM 26

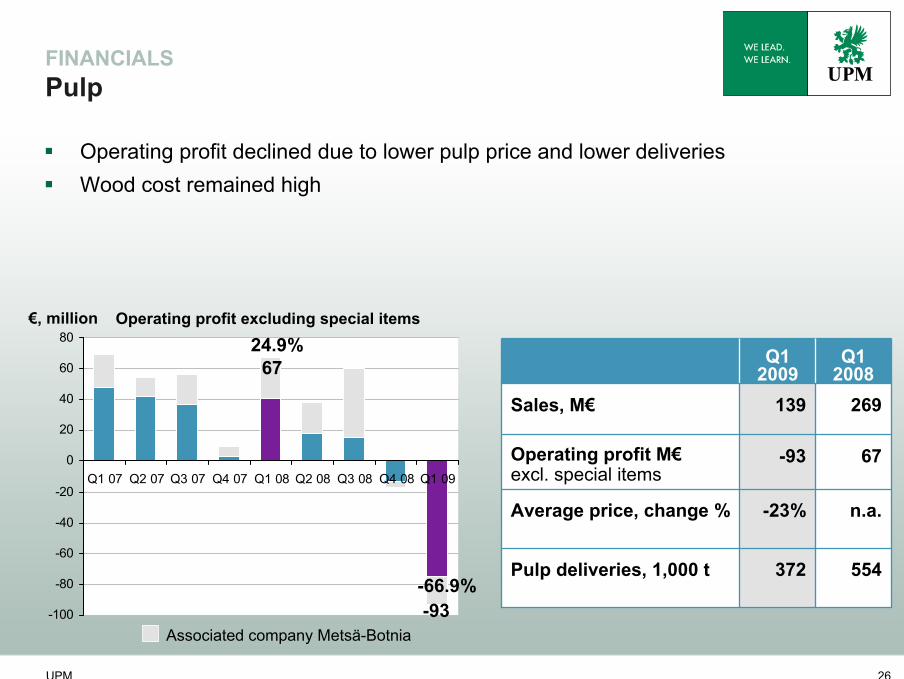

FINANCIALSPulp

Operating profit declined due to lower pulp price and lower deliveriesWood cost remained high

-100

-80

-60

-40

-20

0

20

40

60

80

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

67

-93

24.9%

-66.9%

n.a.-23%Average price, change %

372

-93

139

Q1 2009

554Pulp deliveries, 1,000 t

67Operating profit M€excl. special items

269Sales, M€

Q1 2008

Associated company Metsä-Botnia

€, million Operating profit excluding special items

UPM 27

FINANCIALSForest and timber

-60

-40

-20

0

20

40

60

80

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

26

-8

5.1%

-2.1%2811Fair value change of

biological assets

363

-21%

-8

385

Q12009

573Sawn timber deliveries, 1,000 m3

n.a.Average price of sawn timber, change %

26Operating profit M€excl. special items

508Sales, M€

Q1 2008

Operating profit declined due 21% to lower average price and lower deliveries of sawn timberWood cost remained at a high level

Fair value change of biological assets

€, million Operating profit excluding special items

UPM 28

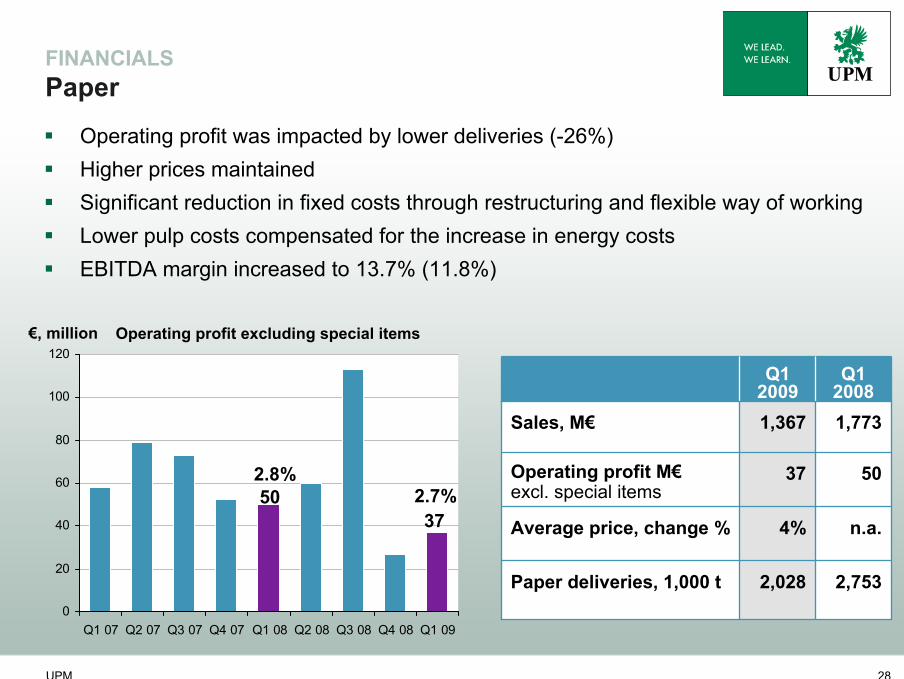

FINANCIALSPaper

0

20

40

60

80

100

120

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

5037

2.8%2.7%

Operating profit was impacted by lower deliveries (-26%)Higher prices maintainedSignificant reduction in fixed costs through restructuring and flexible way of workingLower pulp costs compensated for the increase in energy costsEBITDA margin increased to 13.7% (11.8%)

2,028

4%

37

1,367

Q1 2009

2,753Paper deliveries, 1,000 t

n.a.Average price, change %

50Operating profit M€excl. special items

1,773Sales, M€

Q1 2008

€, million Operating profit excluding special items

UPM 29

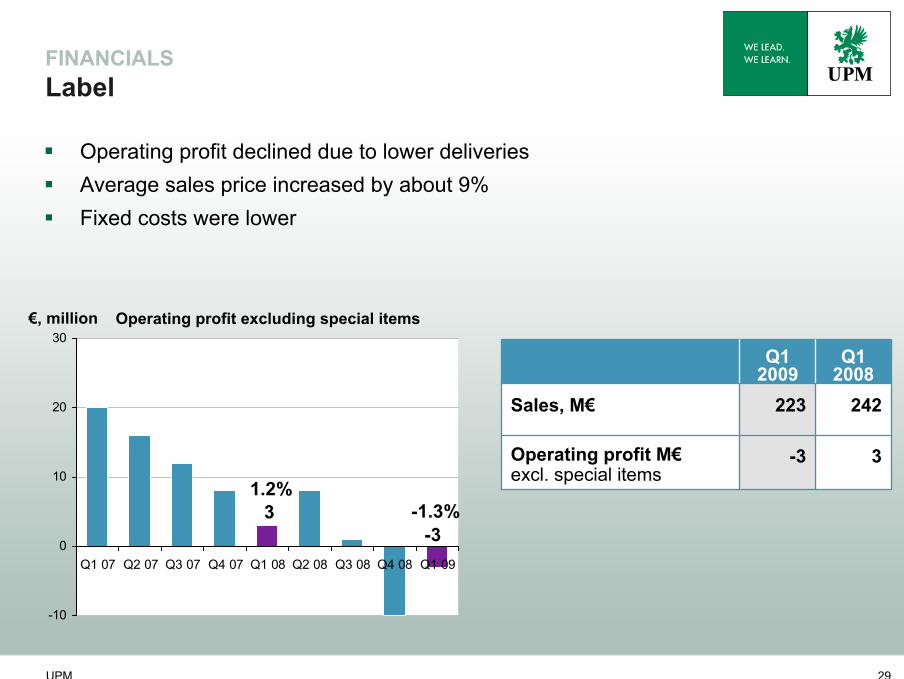

FINANCIALSLabel

-10

0

10

20

30

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

3-3

1.2%-1.3%

-3

223

Q1 2009

3Operating profit M€excl. special items

242Sales, M€

Q1 2008

Operating profit declined due to lower deliveriesAverage sales price increased by about 9%Fixed costs were lower

€, million Operating profit excluding special items

UPM 30

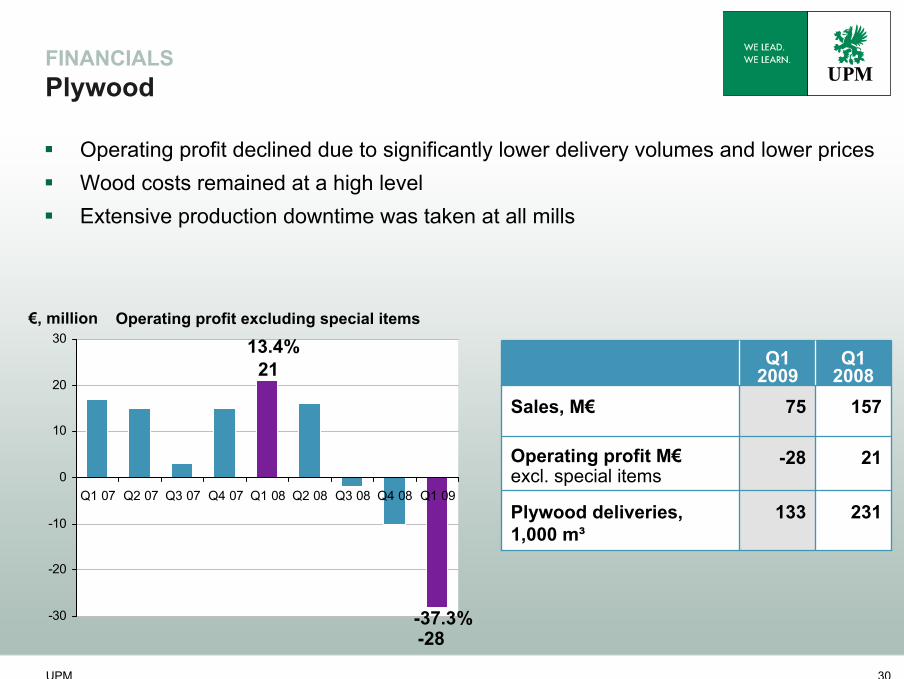

FINANCIALSPlywood

Operating profit declined due to significantly lower delivery volumes and lower pricesWood costs remained at a high levelExtensive production downtime was taken at all mills

-30

-20

-10

0

10

20

30

Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

21

-28

13.4%

-37.3%

133

-28

75

Q1 2009

231Plywood deliveries, 1,000 m³

21Operating profit M€excl. special items

157Sales, M€

Q1 2008

€, million Operating profit excluding special items