Jumbo Underwriting Guidelines

142

Jumbo Underwriting Guidelines

Transcript of Jumbo Underwriting Guidelines

Jumbo Underwriting

Guidelines

Jumbo Underwriting Guidelines | Table of Contents

10.04.2021 2

Table of Contents Jumbo AUS_________________________________________________________________________________ 10

Eligibility Matrix _________________________________________________________________________________ 10 Eligibility Requirements ___________________________________________________________________________ 11

Available Products _____________________________________________________________________________________ 11 DTI _________________________________________________________________________________________________ 11 Ineligible Product Types ________________________________________________________________________________ 11 Underwriting _________________________________________________________________________________________ 11 Documentation Requirements ___________________________________________________________________________ 11

Age of Documents __________________________________________________________________________________ 12 Borrowers ___________________________________________________________________________________________ 12

Eligible ___________________________________________________________________________________________ 12 Ineligible __________________________________________________________________________________________ 12

First Time Homebuyers _________________________________________________________________________________ 12 Multiple Properties Financed/Owned ______________________________________________________________________ 13 Rate/Term Refinance Transactions ________________________________________________________________________ 13 Cash Out Refinance Transactions _________________________________________________________________________ 13

Texas 50(a)(6) ______________________________________________________________________________________ 13 LTV/CLTV/HCLTV Calculation for Refinance Transactions _______________________________________________________ 14 Continuity of Obligation ________________________________________________________________________________ 15 Delayed Financing Refinances ____________________________________________________________________________ 15 Construction to Permanent Financing______________________________________________________________________ 15 Non-Arm’s Length Transactions __________________________________________________________________________ 16 Secondary/Subordinate Financing ________________________________________________________________________ 16

Downpayment / Closing Cost Assistance _________________________________________________________________ 16 Credit Requirements _____________________________________________________________________________ 17

Significant Derogatory Credit ____________________________________________________________________________ 17 Forbearance _______________________________________________________________________________________ 18

Housing History _______________________________________________________________________________________ 19 Credit Report _________________________________________________________________________________________ 19

Disputed Tradelines _________________________________________________________________________________ 19 Frozen Credit ______________________________________________________________________________________ 19

Minimum Credit Requirements ___________________________________________________________________________ 19 Credit Score Requirements ______________________________________________________________________________ 19 Debts and Liabilities ___________________________________________________________________________________ 20

HELOC on Subject ___________________________________________________________________________________ 20 Tax Liens and Payment Plans __________________________________________________________________________ 20

Lawsuit/Pending Litigation ______________________________________________________________________________ 20 Income/Employment Requirements ________________________________________________________________ 20

Employment and Income Stability ________________________________________________________________________ 20 Declining Income ___________________________________________________________________________________ 20

General Documentation Requirements ____________________________________________________________________ 21 Salaried Borrowers ____________________________________________________________________________________ 21

Commission/Bonus Income ___________________________________________________________________________ 21 Self-Employment ______________________________________________________________________________________ 22

Documentation Requirements _________________________________________________________________________ 22 Retirement Income (Pension, Annuity, 401(k), IRA Distributions) ________________________________________________ 23 Trust Income _________________________________________________________________________________________ 23 Restricted Stock and Stock Options________________________________________________________________________ 23 Asset Depletion _______________________________________________________________________________________ 24 Unacceptable Income Sources ___________________________________________________________________________ 26

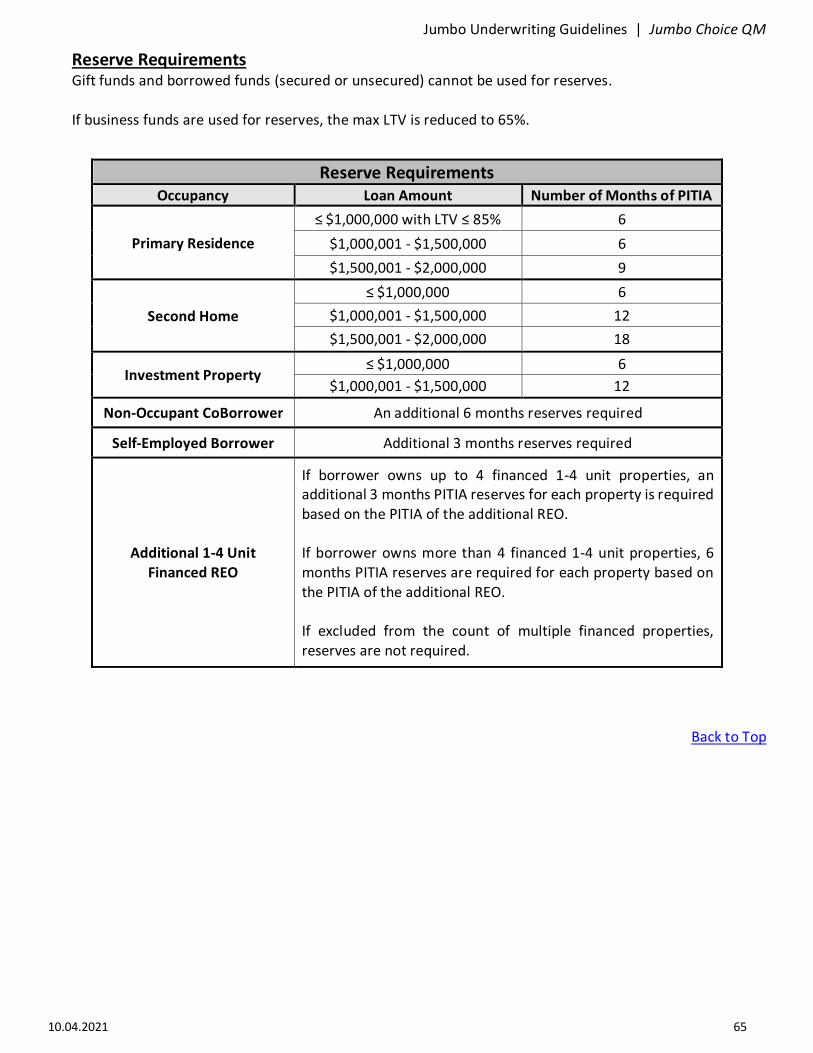

Asset Requirements ______________________________________________________________________________ 27 Gift Funds ___________________________________________________________________________________________ 27 Business Funds _______________________________________________________________________________________ 27 Retirement Accounts ___________________________________________________________________________________ 27 Reserves ____________________________________________________________________________________________ 28

Jumbo Underwriting Guidelines | Table of Contents

10.04.2021 3

Collateral Requirements __________________________________________________________________________ 29 Eligible Collateral ______________________________________________________________________________________ 29 Ineligible Collateral ____________________________________________________________________________________ 29 Appraisal Requirements ________________________________________________________________________________ 30 Properties Located in a Disaster Area ______________________________________________________________________ 31

Re-Inspection Requirements __________________________________________________________________________ 31 Loans with Appraisals ________________________________________________________________________________ 31

Jumbo Choice ______________________________________________________________________________ 32

Eligibility Requirements ___________________________________________________________________________ 32 Eligible Products ______________________________________________________________________________________ 32 Qualifying Rate _______________________________________________________________________________________ 32 ARM Specifics ________________________________________________________________________________________ 32

Interest Rate Adjustment Caps _________________________________________________________________________ 32 Index _____________________________________________________________________________________________ 32 Margin ___________________________________________________________________________________________ 32 Interest Rate Floor __________________________________________________________________________________ 32 Conversion Option __________________________________________________________________________________ 32 Assumption Feature _________________________________________________________________________________ 32

Ineligible Products _____________________________________________________________________________________ 33 Documentation Requirements ___________________________________________________________________________ 33 Occupancy ___________________________________________________________________________________________ 34 Maximum DTI ________________________________________________________________________________________ 34 LTV/CLTV/HCLTV ______________________________________________________________________________________ 34 Borrowers ___________________________________________________________________________________________ 36

Eligible ___________________________________________________________________________________________ 36 Ineligible __________________________________________________________________________________________ 38

Multiple Properties Financed ____________________________________________________________________________ 39 Properties Listed for Sale _______________________________________________________________________________ 39 Rate/Term Refinance Restrictions _________________________________________________________________________ 40

Texas 50(f)(2) Refinances _____________________________________________________________________________ 40 Cash Out Refinance Restrictions __________________________________________________________________________ 41

Texas 50(a)(6) Refinances _____________________________________________________________________________ 41 Continuity of Obligation ________________________________________________________________________________ 43 Delayed Purchase Refinances ____________________________________________________________________________ 43 LTV/CLTV/HCLTV Calculation for Refinances_________________________________________________________________ 44 Construction to Permanent Refinance Restrictions ___________________________________________________________ 44 Non-Arm’s Length Transactions __________________________________________________________________________ 45 Secondary / Subordinate Financing________________________________________________________________________ 45

Credit Requirements _____________________________________________________________________________ 46 Derogatory Credit _____________________________________________________________________________________ 46

Past Mortgage Forbearances __________________________________________________________________________ 47 Exceptions for Derogatory Credit _______________________________________________________________________ 47

Outstanding Judgments/ Tax Liens/Charge-Offs/Past-Due Accounts ______________________________________________ 47 Housing Payment History _______________________________________________________________________________ 47

Mortgage History Requirements _______________________________________________________________________ 47 Rental History Requirements __________________________________________________________________________ 48

Credit Report _________________________________________________________________________________________ 48 Age of Credit Report _________________________________________________________________________________ 48 “Frozen” Credit Reports ______________________________________________________________________________ 48 Tradeline Requirements ______________________________________________________________________________ 48 Credit Score Requirements ____________________________________________________________________________ 48 Disputed Tradelines _________________________________________________________________________________ 49 Inquiries __________________________________________________________________________________________ 49 Student Loans ______________________________________________________________________________________ 49 Liability Requirements _______________________________________________________________________________ 49

Departure Residence ___________________________________________________________________________________ 50

Jumbo Underwriting Guidelines | Table of Contents

10.04.2021 4

Departure Residence Pending Sale ______________________________________________________________________ 50 Departure Residence Subject to Guaranteed Buy-out with Corporation Relocation ________________________________ 50

Co-Signed Loans ______________________________________________________________________________________ 50 Court Order __________________________________________________________________________________________ 50 Assumption with No Release of Liability ____________________________________________________________________ 50 Tax Liability __________________________________________________________________________________________ 51 Loans Secured by Financial Assets ________________________________________________________________________ 51

Income/Employment Requirements ________________________________________________________________ 51 Declining Income ______________________________________________________________________________________ 51 Gaps in Employment ___________________________________________________________________________________ 52 Residual Income ______________________________________________________________________________________ 52 Paystub Requirements _________________________________________________________________________________ 52 W2 Requirements _____________________________________________________________________________________ 52 Verification of Employment Requirements __________________________________________________________________ 53 Tax Return Requirements _______________________________________________________________________________ 53

Unfiled Tax Returns _________________________________________________________________________________ 54 Taxpayer Identification Theft __________________________________________________________________________ 55

Specific Income Documentation Requirements ______________________________________________________________ 55 Salaried Income ____________________________________________________________________________________ 55 Hourly and Part-Time Income__________________________________________________________________________ 55 Commission Income _________________________________________________________________________________ 55 Overtime and Bonus Income __________________________________________________________________________ 55 2106 Expenses _____________________________________________________________________________________ 56 Alimony/Child Support/Separate Maintenance ____________________________________________________________ 56 Asset Depletion_____________________________________________________________________________________ 56 Borrowers Employed by Family ________________________________________________________________________ 56 Capital Gains _______________________________________________________________________________________ 56 Disability Income (Long-Term) _________________________________________________________________________ 57 Dividends and Interest Income _________________________________________________________________________ 57 Foreign Income _____________________________________________________________________________________ 57 K1 Income/Loss on Schedule E _________________________________________________________________________ 57 Non-Taxable Income _________________________________________________________________________________ 57 Note Income _______________________________________________________________________________________ 57 Rental Income ______________________________________________________________________________________ 58 Restricted Stock and Stock Options _____________________________________________________________________ 59 Retirement Income Sources ___________________________________________________________________________ 59 Trust Income _______________________________________________________________________________________ 60

Self-Employed Income Sources ___________________________________________________________________________ 60 Sole Proprietorship __________________________________________________________________________________ 61 Partnership/S-Corporation ____________________________________________________________________________ 61 Corporation________________________________________________________________________________________ 61

Unacceptable Income Sources ___________________________________________________________________________ 62 Asset Requirements ______________________________________________________________________________ 62

Documentation Requirements ___________________________________________________________________________ 62 Checking and Savings Accounts, Money Markets, CDs _________________________________________________________ 62 Publicly Traded Stocks/Bonds/Mutual Funds ________________________________________________________________ 63 Retirement Accounts (401(k), IRAs, etc) ____________________________________________________________________ 63 Cash Value of Life Insurance/Annuities _____________________________________________________________________ 63 1031 Exchange________________________________________________________________________________________ 63 Business Funds _______________________________________________________________________________________ 64 Gift Funds ___________________________________________________________________________________________ 64 Reserve Requirements _________________________________________________________________________________ 65 Financing Concessions __________________________________________________________________________________ 66 Seller Concessions _____________________________________________________________________________________ 66

Personal Property ___________________________________________________________________________________ 66 Collateral Requirements __________________________________________________________________________ 67

Appraisal Requirements ________________________________________________________________________________ 67 Appraisal Requirements by Loan Amount ________________________________________________________________ 68

Jumbo Underwriting Guidelines | Table of Contents

10.04.2021 5

Eligible Collateral ______________________________________________________________________________________ 68 Ineligible Collateral ____________________________________________________________________________________ 69

General Provisions _______________________________________________________________________________ 70 FEMA Declared Disaster Area Policy _______________________________________________________________________ 70

Effective Date of Disaster Policy ________________________________________________________________________ 70 Appraisal and Re-Inspection Requirements _______________________________________________________________ 70 Appraisal Performed On or Before Disaster Incident End Date ________________________________________________ 70 Standard Appraisal Performed After Incident Period End Date for Disaster ______________________________________ 71

Power of Attorney _____________________________________________________________________________________ 71 Requirements ______________________________________________________________________________________ 71 Restrictions on the Use of a Power of Attorney ____________________________________________________________ 71

Title Requirements ____________________________________________________________________________________ 71

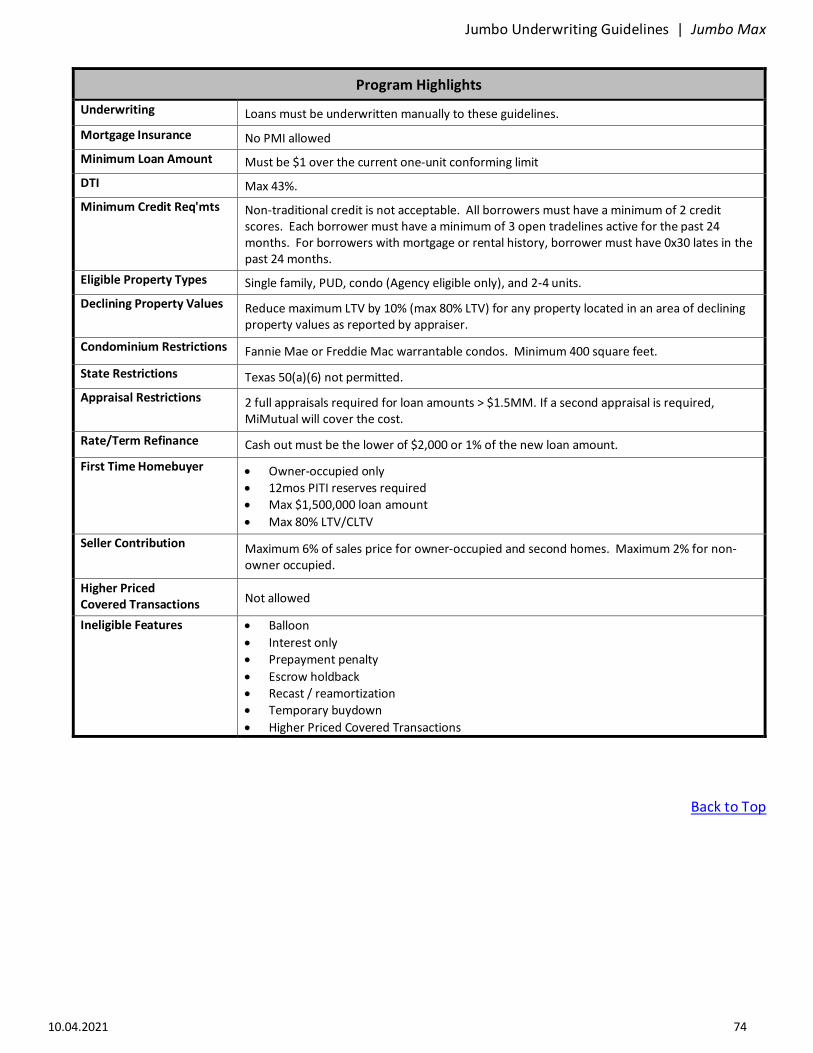

Jumbo Max ________________________________________________________________________________ 72

Eligibility Requirements ___________________________________________________________________________ 72 Available Products _____________________________________________________________________________________ 72 Qualifying Rate _______________________________________________________________________________________ 72 Documentation Requirements ___________________________________________________________________________ 72 Occupancy ___________________________________________________________________________________________ 72

Primary Residence __________________________________________________________________________________ 72 Second Home ______________________________________________________________________________________ 72 Investment Property (Non-Owner Occupied)______________________________________________________________ 73

LTV/CLTV/HCLTV ______________________________________________________________________________________ 73 Borrowers ___________________________________________________________________________________________ 75

Eligible ___________________________________________________________________________________________ 75 Ineligible __________________________________________________________________________________________ 76

Multiple Properties Financed ____________________________________________________________________________ 76 Purchases ___________________________________________________________________________________________ 77 Rate/Term Refinance Restrictions _________________________________________________________________________ 77 Cash Out Refinance Restrictions __________________________________________________________________________ 78 Continuity of Obligation ________________________________________________________________________________ 78 Delayed Financing Refinances ____________________________________________________________________________ 78 Land Contract /Contract for Deed ________________________________________________________________________ 79 Construction Loan Refinancing ___________________________________________________________________________ 79 Non-Arm’s Length Transactions __________________________________________________________________________ 79 Secondary / Subordinate Financing________________________________________________________________________ 80

Credit Requirements _____________________________________________________________________________ 80 Bankruptcy/Foreclosure/Deed-in-Lieu/Short Sale ____________________________________________________________ 80 Modifications_________________________________________________________________________________________ 80 Judgments/Liens/Collections ____________________________________________________________________________ 81 Mortgage/Rental History________________________________________________________________________________ 81 Inquiries _____________________________________________________________________________________________ 81 Credit Report _________________________________________________________________________________________ 82

Minimum Credit Requirements ________________________________________________________________________ 82 Credit Score Requirements ____________________________________________________________________________ 82

Debts and Liabilities ___________________________________________________________________________________ 83 Debt-to-Income Ratio ________________________________________________________________________________ 83 Installment Debt ____________________________________________________________________________________ 83 Revolving Debt _____________________________________________________________________________________ 84 Home Equity Line of Credit (HELOC) _____________________________________________________________________ 84

Income/Employment Requirements ________________________________________________________________ 84 Employment and Income Stability ________________________________________________________________________ 85 Tax Transcript Requirements ____________________________________________________________________________ 85 Income Documentation Requirements _____________________________________________________________________ 85

Salaried Borrowers __________________________________________________________________________________ 85 Self-Employed Borrowers _____________________________________________________________________________ 86

Jumbo Underwriting Guidelines | Table of Contents

10.04.2021 6

Rental Income ______________________________________________________________________________________ 88 Alimony/Child Support Income ________________________________________________________________________ 89 Non-Taxable Income _________________________________________________________________________________ 89 Retirement or Pension Income _________________________________________________________________________ 89 Social Security Income _______________________________________________________________________________ 89 Foreign Income _____________________________________________________________________________________ 90

Unacceptable Income Sources ___________________________________________________________________________ 90 Asset Requirements ______________________________________________________________________________ 90

Source of Funds _______________________________________________________________________________________ 90 Cash Reserves ________________________________________________________________________________________ 91 Interested Party Contributions ___________________________________________________________________________ 91

Collateral Requirements __________________________________________________________________________ 92 Appraisal Requirements ________________________________________________________________________________ 92 Third Party Appraisal Review_____________________________________________________________________________ 92 Eligible Collateral ______________________________________________________________________________________ 92 Ineligible Collateral ____________________________________________________________________________________ 93 Declining Markets _____________________________________________________________________________________ 93 Land-to-Value ________________________________________________________________________________________ 93 Properties Located in a Disaster Area ______________________________________________________________________ 94

General Provisions _______________________________________________________________________________ 94 Title Requirements ____________________________________________________________________________________ 94

Chain of Title _______________________________________________________________________________________ 94 Hazard Insurance ______________________________________________________________________________________ 94 HERO/PACE/Solar Panels________________________________________________________________________________ 95 Escrow Accounts ______________________________________________________________________________________ 95

Jumbo Select _______________________________________________________________________________ 96

Eligibility Requirements ___________________________________________________________________________ 96 Eligible Products ______________________________________________________________________________________ 96 Qualifying Rate _______________________________________________________________________________________ 96 ARM Specifics ________________________________________________________________________________________ 96

Interest Rate Adjustment Caps _________________________________________________________________________ 96 Index _____________________________________________________________________________________________ 96 Margin ___________________________________________________________________________________________ 96 Interest Rate Floor __________________________________________________________________________________ 96 Conversion Option __________________________________________________________________________________ 96 Assumption Feature _________________________________________________________________________________ 96

Ineligible Products _____________________________________________________________________________________ 97 Documentation Requirements ___________________________________________________________________________ 97 Occupancy ___________________________________________________________________________________________ 98 Maximum DTI ________________________________________________________________________________________ 98 LTV/CLTV/HCLTV ______________________________________________________________________________________ 99 Borrowers __________________________________________________________________________________________ 100

Eligible __________________________________________________________________________________________ 100 Ineligible _________________________________________________________________________________________ 102

Multiple Financed Properties ___________________________________________________________________________ 102 Properties Listed for Sale ______________________________________________________________________________ 103 Rate/Term Refinance Restrictions ________________________________________________________________________ 103

Texas 50(f)(2) Refinances ____________________________________________________________________________ 103 Cash Out Refinance Restrictions _________________________________________________________________________ 104

Texas 50(a)(6) Refinances ____________________________________________________________________________ 104 Continuity of Obligation _______________________________________________________________________________ 106 Delayed Purchase Refinances ___________________________________________________________________________ 106 LTV/CLTV/HCLTV Calculation for Refinances________________________________________________________________ 107 Construction to Permanent Refinance Restrictions __________________________________________________________ 107 Non-Arm’s Length Transactions _________________________________________________________________________ 108

Jumbo Underwriting Guidelines | Table of Contents

10.04.2021 7

Secondary / Subordinate Financing_______________________________________________________________________ 109 Credit Requirements ____________________________________________________________________________ 110

Derogatory Credit ____________________________________________________________________________________ 110 Past Mortgage Forbearances _________________________________________________________________________ 110 Exceptions for Derogatory Credit ______________________________________________________________________ 110

Outstanding Judgments/ Tax Liens/Charge-Offs/Past-Due Accounts _____________________________________________ 111 Housing Payment History ______________________________________________________________________________ 111

Mortgage History Requirements ______________________________________________________________________ 111 Rental History Requirements _________________________________________________________________________ 111

Credit Report ________________________________________________________________________________________ 111 Age of Credit Report ________________________________________________________________________________ 111 “Frozen” Credit Reports _____________________________________________________________________________ 111 Tradeline Requirements _____________________________________________________________________________ 112 Disputed Tradelines ________________________________________________________________________________ 112 Inquiries _________________________________________________________________________________________ 112 Student Loans _____________________________________________________________________________________ 112 Liability Requirements ______________________________________________________________________________ 113

Departure Residence __________________________________________________________________________________ 113 Departure Residence Pending Sale _____________________________________________________________________ 113 Departure Residence Subject to Guaranteed Buy-out with Corporation Relocation _______________________________ 113

Co-Signed Loans _____________________________________________________________________________________ 113 Court Order _________________________________________________________________________________________ 114 Assumption with No Release of Liability ___________________________________________________________________ 114 Tax Liability _________________________________________________________________________________________ 114 Loans Secured by Financial Assets _______________________________________________________________________ 114

Income/Employment Requirements _______________________________________________________________ 115 Declining Income _____________________________________________________________________________________ 115 Gaps in Employment __________________________________________________________________________________ 115 Residual Income Requirement __________________________________________________________________________ 116 Paystub Requirements ________________________________________________________________________________ 116 W2 Requirements ____________________________________________________________________________________ 116 Verification of Employment Requirements _________________________________________________________________ 116 Tax Return Requirements ______________________________________________________________________________ 117

Unfiled Tax Returns ________________________________________________________________________________ 118 Taxpayer Identification Theft _________________________________________________________________________ 118

Specific Income Documentation Requirements _____________________________________________________________ 119 Salaried Income ___________________________________________________________________________________ 119 Hourly and Part-Time Income_________________________________________________________________________ 119 Commission Income ________________________________________________________________________________ 119 Overtime and Bonus Income _________________________________________________________________________ 119 2106 Expenses ____________________________________________________________________________________ 119 Alimony/Child Support/Separate Maintenance ___________________________________________________________ 119 Asset Depletion____________________________________________________________________________________ 120 Borrowers Employed by Family _______________________________________________________________________ 120 Capital Gains ______________________________________________________________________________________ 120 Disability Income (Long-Term) ________________________________________________________________________ 120 Dividends and Interest Income ________________________________________________________________________ 120 Foreign Income ____________________________________________________________________________________ 120 K1 Income/Loss on Schedule E ________________________________________________________________________ 121 Non-Taxable Income ________________________________________________________________________________ 121 Note Income ______________________________________________________________________________________ 121 Rental Income _____________________________________________________________________________________ 122 Restricted Stock and Stock Options ____________________________________________________________________ 123 Retirement Income Sources __________________________________________________________________________ 123 Trust Income ______________________________________________________________________________________ 124

Self-Employed Income Sources __________________________________________________________________________ 124 Sole Proprietorship _________________________________________________________________________________ 125 Partnership/S-Corporation ___________________________________________________________________________ 125

Jumbo Underwriting Guidelines | Table of Contents

10.04.2021 8

Corporation_______________________________________________________________________________________ 125 Unacceptable Income Sources __________________________________________________________________________ 126

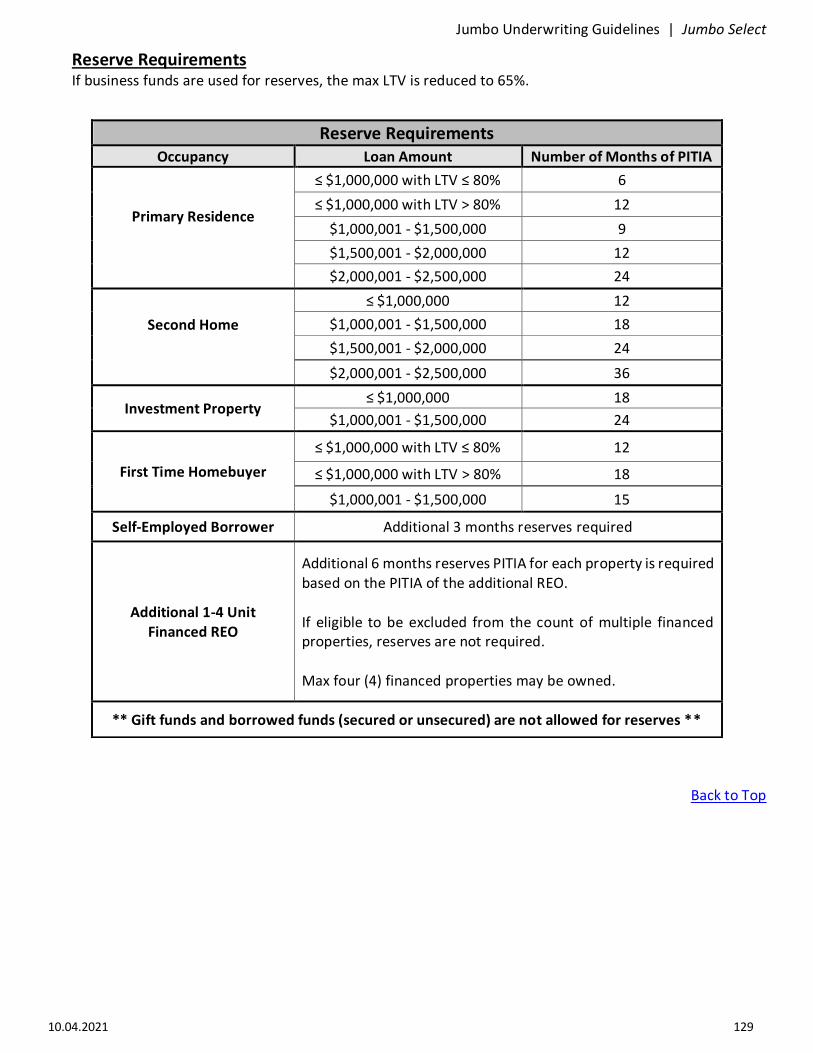

Asset Requirements _____________________________________________________________________________ 126 Documentation Requirements __________________________________________________________________________ 126 Checking and Savings Accounts, Money Markets, CDs ________________________________________________________ 126 Publicly Traded Stocks/Bonds/Mutual Funds _______________________________________________________________ 127 Retirement Accounts (401(k), IRAs, etc) ___________________________________________________________________ 127 Cash Value of Life Insurance/Annuities ____________________________________________________________________ 127 1031 Exchange_______________________________________________________________________________________ 127 Business Funds ______________________________________________________________________________________ 128 Gift Funds __________________________________________________________________________________________ 128 Reserve Requirements ________________________________________________________________________________ 129 Financing Concessions _________________________________________________________________________________ 130 Seller Concessions ____________________________________________________________________________________ 130

Personal Property __________________________________________________________________________________ 130 Collateral Requirements _________________________________________________________________________ 131

Appraisal Requirements _______________________________________________________________________________ 131 Appraisal Requirements by Loan Amount _______________________________________________________________ 132

Eligible Collateral _____________________________________________________________________________________ 132 Ineligible Collateral ___________________________________________________________________________________ 133

General Provisions ______________________________________________________________________________ 134 FEMA Declared Disaster Area Policy ______________________________________________________________________ 134

Effective Date of Disaster Policy _______________________________________________________________________ 134 Appraisal and Re-Inspection Requirements ______________________________________________________________ 134 Appraisal Performed On or Before Disaster Incident End Date _______________________________________________ 134 Standard Appraisal Performed After Incident Period End Date for Disaster _____________________________________ 135

Power of Attorney ____________________________________________________________________________________ 135 Requirements _____________________________________________________________________________________ 135 Restrictions on the Use of a Power of Attorney ___________________________________________________________ 135

Title Requirements ___________________________________________________________________________________ 135

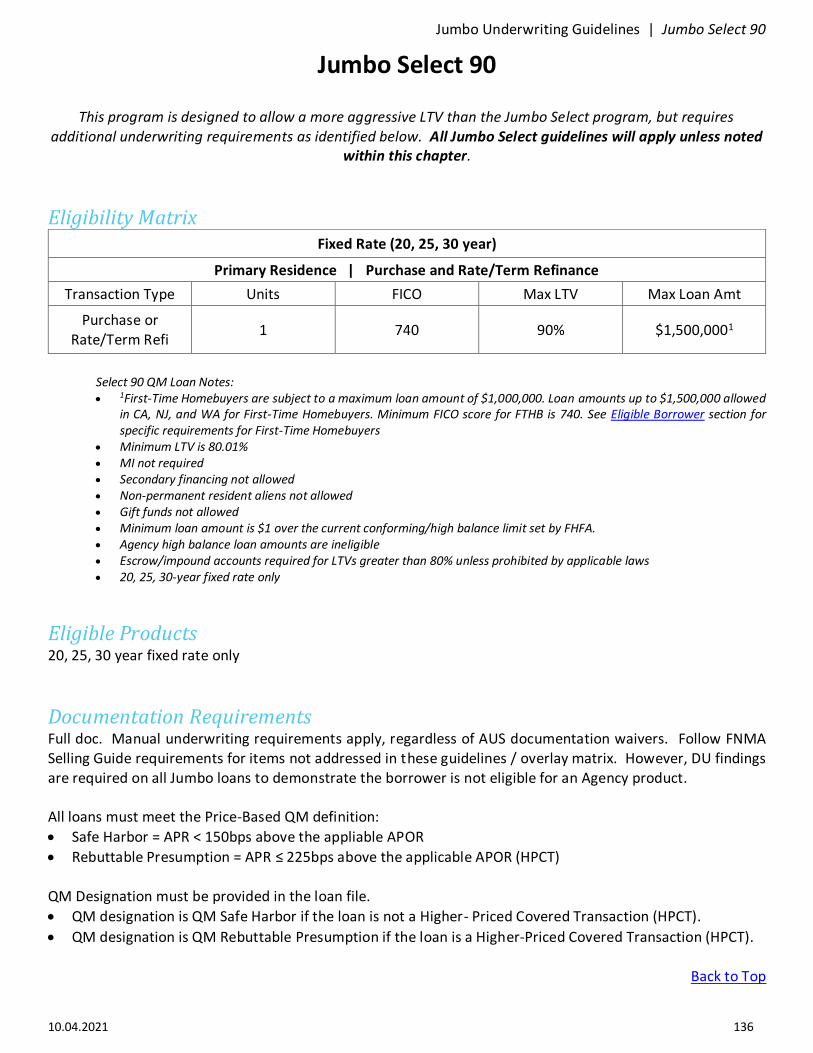

Jumbo Select 90 ___________________________________________________________________________ 136

Eligibility Matrix ________________________________________________________________________________ 136 Eligible Products ________________________________________________________________________________ 136 Documentation Requirements ____________________________________________________________________ 136 Occupancy ____________________________________________________________________________________ 137 Maximum DTI __________________________________________________________________________________ 137 Borrowers _____________________________________________________________________________________ 137

Eligible _____________________________________________________________________________________________ 137 Ineligible ___________________________________________________________________________________________ 137

Multiple Financed Properties _____________________________________________________________________ 138 Properties Listed for Sale_________________________________________________________________________ 138 Credit_________________________________________________________________________________________ 138

Derogatory Credit ____________________________________________________________________________________ 138 Income/Employment ____________________________________________________________________________ 139

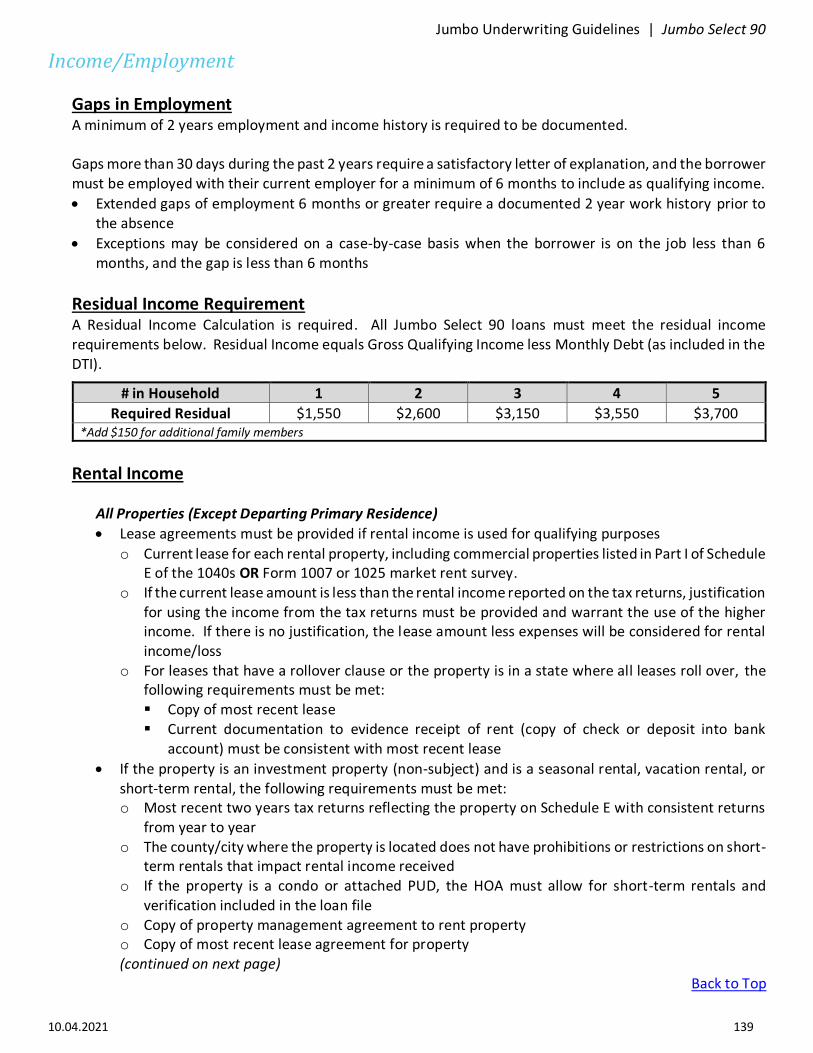

Gaps in Employment __________________________________________________________________________________ 139 Residual Income Requirement __________________________________________________________________________ 139 Rental Income _______________________________________________________________________________________ 139

All Properties (Except Departing Primary Residence)_______________________________________________________ 139 Departing Residence ________________________________________________________________________________ 140

Assets ________________________________________________________________________________________ 141 Gift Funds __________________________________________________________________________________________ 141 Reserve Requirements ________________________________________________________________________________ 141

Collateral______________________________________________________________________________________ 142 Eligible Collateral _____________________________________________________________________________________ 142

Jumbo Underwriting Guidelines | Table of Contents

10.04.2021 9

Ineligible Collateral ___________________________________________________________________________________ 142 Appraisal Requirements by Transaction Type _______________________________________________________________ 142

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 10

Jumbo AUS

The Jumbo AUS program allows for documentation requirements per DU findings / FNMA guidelines, except in limited circumstances, such as investment properties and/or when self-employment income is used to qualify.

Eligibility Matrix Primary Residence | Purchase and Rate/Term Refinance

Transaction Type Units FICO Maximum

LTV/CLTV/HCLTV Maximum

Loan Amount1

Purchase or Rate/Term Refinance

1

740 89.99%2,3 $1,500,000

720 85%2,3 $1,500,000

700 80%2 $1,500,000

720 75%2 $2,000,000 720 70% $2,500,000

680 60% $1,000,000

2-4 700 65% $1,000,000 720 60% $1,500,000

Primary Residence | Cash Out Refinance

Transaction Type Units FICO Maximum

LTV/CLTV/HCLTV Maximum

Loan Amount

Cash Out Refinance

1

700 75% $1,000,000

720 70% $1,500,000

720 60% $2,000,000 720 50% $2,500,000

2 700 60% $1,000,000

Second Home | Purchase and Rate/Term Refinance

Transaction Type Units FICO Maximum

LTV/CLTV/HCLTV Maximum

Loan Amount

Purchase 1 720 80%2 $1,000,000

Purchase or Rate/Term Refinance

1 720

75%2 $1,000,000 70% $1,500,000

65% $2,000,000

50% $2,500,000

Second Home | Cash Out Refinance

Transaction Type Units FICO Maximum

LTV/CLTV/HCLTV Maximum

Loan Amount

Cash Out Refinance

1 740 60% $1,500,000 1 740 50% $2,000,000

Investment | Purchase and Rate/Term Refinance

Transaction Type Units FICO Maximum

LTV/CLTV/HCLTV Maximum

Loan Amount Purchase 1-4 740 70% $1,500,000

Rate/Term Refinance 1-4 740 70% $1,500,000

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 11

1First Time Homebuyer (FTHB) maximum loan amount is $1,500,000 2Self-Employment Income: Minimum 720 FICO when any self-employment income is required for qualifying purposes. If the self-employment income is not needed to qualify, then the 720 FICO minimum is not applicable. 3The following requirements apply for transactions with LTVs greater than 80%:

• MI not required • Escrow/impound accounts required for LTVs > 80% unless prohibited by applicable law • Self-employed borrowers not allowed. If the self-employed income is not needed for qualifying purposes, then the

restriction is not applicable

Eligibility Requirements

Available Products 20, 25, 30 year fixed

DTI • LTVs ≤ 80% = 45%

• LTVs > 80% = 36%

Ineligible Product Types • Higher Priced Mortgage Loans (HPMLs)

• Non-Standard to Standard Refinance Transactions (ATR Exempt)

• Higher-Priced Covered Transactions (HPCT QM-Rebuttable Presumption)

• Balloons

• Graduated Payments

• Interest Only Products

• Temporary Buydowns

• Loans with Prepayment Penalties

• Adjustable Rate Terms

Underwriting All loans must have a Fannie Mae Approve/Ineligible (ineligible due to loan amount or maximum cash -out on a rate/term refinance transaction) included in the loan file. The final data submitted to DU must match the closed loan. Manual underwrite is not permitted.

Documentation Requirements DU findings may be followed to document a number of items. The Jumbo AUS Documentation Matrix is a good resource for knowing when additional documentation requirements apply. All documentation requirements detailed in this guide are to be followed in the event of a discrepancy.

Back to Top

NOTE: Minimum loan amount $548,251 for 1 unit properties, and $1 above the conforming loan limits for 2-4 unit properties.

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 12

Age of Documents

• All credit documents, including title commitment must be no older than ninety (90) days from the Note date o FNMA age of documentation guidance applies for loans locked on/after September 9, 2021

• Self-employment age of docs for YTD Profit and Loss must be no older than ninety (90) days from the Note date

Borrowers

Eligible

• US Citizens

• Permanent Resident Aliens with evidence of lawful residency o Must be employed in the US for the past twenty-four (24) months o Legal residency may be documented with one of the following:

▪ A valid and current Permanent Resident Alien card (Form I-551), also known as a green card ▪ A passport stamped “Processed for I-551, temporary evidence of lawful admission for

permanent residence. Valid until _________. Employment authorized”. This evidences the holder has been approved for, but not issued, a Permanent Resident Alien card.

• Non-Permanent Resident Aliens with evidence of lawful residency are eligible with the following restrictions: o Primary Residence Only o Maximum LTV/CLTV/HCLTV 75% o Unexpired H1B, H2B, E1, L1, and G Series Visas issued by the USCIC only

▪ G Series Visas must have no diplomatic immunity ▪ Visa must allow the non-permanent resident alien to work and live in the United States

o Borrower must have a current twenty-four (24) month employment history in the US

• Illinois Land Trust

• Inter Vivos Revocable Trust

• All borrowers must have a valid Social Security Number

• Non-Occupant Borrower – Follow Fannie Mae requirements with exception of non-occupant relationship who must be a related family member of the borrower(s)

Ineligible

• Foreign Nationals

• Borrowers with Diplomatic Immunity status

• Life Estates

• Non-Revocable Trusts

• Guardianships

• LLCs, Corporations or Partnerships

• Land Trusts, except for Illinois Land Trust

• Borrowers with any ownership in a business that is Federally illegal, regardless if the income is not being considered for qualifying

First Time Homebuyers • Maximum loan amount is $1,500,000

• Not allowed on investment property transactions

• See Reserve section for additional requirements

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 13

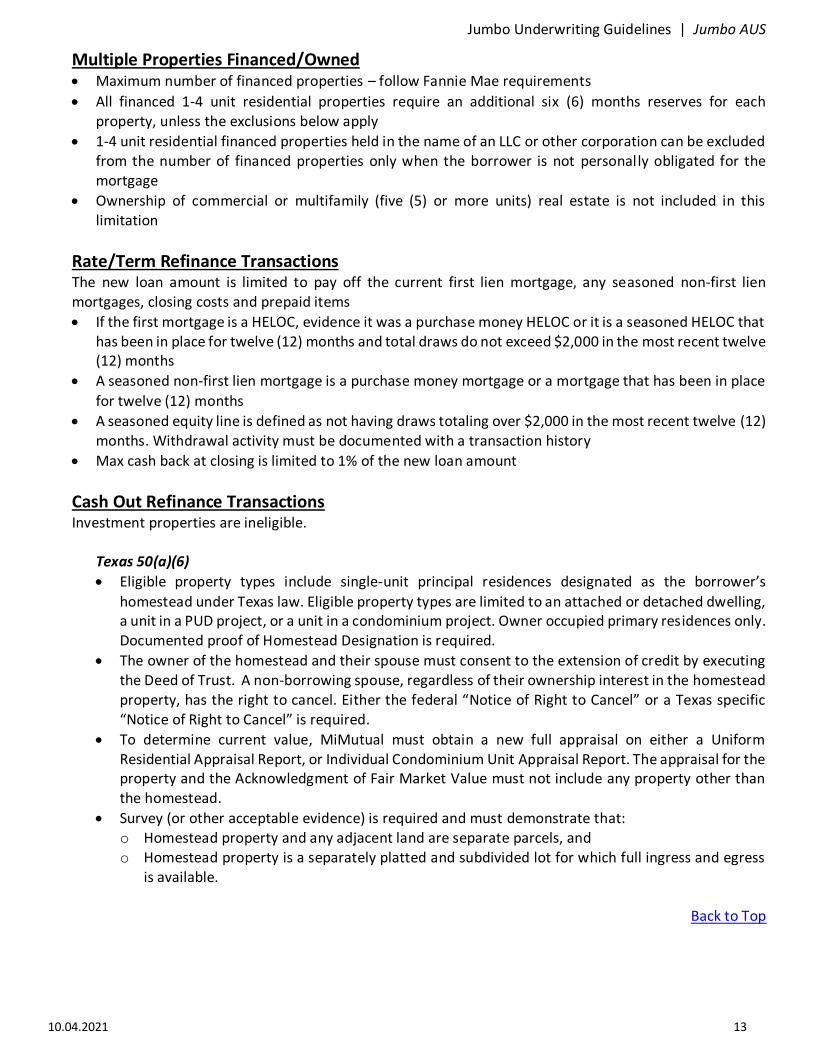

Multiple Properties Financed/Owned • Maximum number of financed properties – follow Fannie Mae requirements

• All financed 1-4 unit residential properties require an additional six (6) months reserves for each property, unless the exclusions below apply

• 1-4 unit residential financed properties held in the name of an LLC or other corporation can be excluded from the number of financed properties only when the borrower is not personally obligated for the mortgage

• Ownership of commercial or multifamily (five (5) or more units) real estate is not included in this limitation

Rate/Term Refinance Transactions The new loan amount is limited to pay off the current first lien mortgage, any seasoned non-first lien mortgages, closing costs and prepaid items

• If the first mortgage is a HELOC, evidence it was a purchase money HELOC or it is a seasoned HELOC that has been in place for twelve (12) months and total draws do not exceed $2,000 in the most recent twelve (12) months

• A seasoned non-first lien mortgage is a purchase money mortgage or a mortgage that has been in place

for twelve (12) months

• A seasoned equity line is defined as not having draws totaling over $2,000 in the most recent twelve (12) months. Withdrawal activity must be documented with a transaction history

• Max cash back at closing is limited to 1% of the new loan amount

Cash Out Refinance Transactions Investment properties are ineligible.

Texas 50(a)(6)

• Eligible property types include single-unit principal residences designated as the borrower’s

homestead under Texas law. Eligible property types are limited to an attached or detached dwelling, a unit in a PUD project, or a unit in a condominium project. Owner occupied primary residences only. Documented proof of Homestead Designation is required.

• The owner of the homestead and their spouse must consent to the extension of credit by executing the Deed of Trust. A non-borrowing spouse, regardless of their ownership interest in the homestead property, has the right to cancel. Either the federal “Notice of Right to Cancel” or a Texas specific “Notice of Right to Cancel” is required.

• To determine current value, MiMutual must obtain a new full appraisal on either a Uniform Residential Appraisal Report, or Individual Condominium Unit Appraisal Report. The appraisal for the property and the Acknowledgment of Fair Market Value must not include any property other than the homestead.

• Survey (or other acceptable evidence) is required and must demonstrate that: o Homestead property and any adjacent land are separate parcels, and o Homestead property is a separately platted and subdivided lot for which full ingress and egress

is available.

Back to Top

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 14

• Additional Restrictions and Requirements: o Fees and charges to make the Mortgage Loan may not exceed 2% of the Mortgage Loan amount.

The following fees and charges can be excluded from the testing: ▪ Bona Fide Discounts to lower the rate selected ▪ Appraisal Fee ▪ Survey Fee ▪ Lender’s Title Policy

o The Borrower’s first payment must be due no later than two (2) months after closing. o The lender must provide the title company with a detailed closing instruction letter and require

acknowledgement of its receipt. o If this Mortgage Loan is being used to pay off a previous Texas Equity Loan, the Mortgage Loan

may not close before twelve (12) months have passed from the closing date of the Texas Equity Loan being paid off. (See Section D.3 for additional information)

o If the new Mortgage Loan is a Texas Equity Loan originated to cure a failure in the original mortgage to comply with Section 50(a)(6), then the Texas law requirement that at least twelve (12) months have passed since any previous Texas Home Equity loan secured by a homestead property was closed does not apply.

o The Mortgage Loan may not close before twelve (12) days after the Mortgage Loan application was taken by the lender or the Borrower receives the “NOTICE CONCERNING EXTENSIONS OF CREDIT DEFINED BY SECTION 50(a)(6), ARTICLE XVI, TEXAS CONSTITUTION” disclosure, whichever date is later AND may not close, without the Borrower’s consent, one (1) business day after the date on which the Borrower receives a copy of the Mortgage Loan application, if not previously provided, and a final itemized disclosure of the actual fees, points, interest, costs and charges that will be charged at closing.

o The Mortgage Loan may only close at the office of the lender, title company or an attorney at law.

o Power of Attorney may not be used on a Texas Equity Loan. o The use of FNMA approved Texas Equity legal documents (Note, Deed, Riders, etc.) is required. o If the new refinance Mortgage Loan is classified under Texas law as a Texas 50(a)(6), the loan

must be locked as a cash out refinance

LTV/CLTV/HCLTV Calculation for Refinance Transactions • If subject property is owned more than twelve (12) months, the LTV/CLTV/HCLTV is based on the current

appraised value. The twelve (12) month time frame may be based on subject transaction Note date

• If subject property is owned less than twelve (12) months, the LTV/CLTV/HCLTV is based on the lesser of the original purchase price plus documented improvements made after the purchase of the property, or the appraised value. Documented improvements must be supported with receipts. The twelve (12) month time frame may be based on subject transaction Note date

Back to Top

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 15

Continuity of Obligation When at least one (1) borrower on the existing mortgage is also a borrower on the new refinance transaction, continuity of obligation requirements have been met. If continuity of obligation is not met, the following permissible exceptions are allowed for the new refinance to be eligible:

• The borrower has been on title for at least twelve (12) months but is not obligated on the existing mortgage that is being refinanced and the borrower meets the following requirements: o Has been making the mortgage payments (including any secondary financing) for the most recent

twelve (12) months, or o Is related to the borrower on the mortgage being refinanced

• The borrower on the new refinance transaction was added to title twenty- four (24) months or more prior to the disbursement date of the new refinance transaction

• The borrower on the refinance inherited or was legally awarded the property by a court in the case of divorce, separation or dissolution of a domestic partnership

• The borrower on the new refinance transaction has been added to title through a transfer from a trust, LLC or partnership. The following requirements apply: o Borrower must have been a beneficiary/creator (trust) or 25% or more owner of the LLC or

partnership prior to the transfer o The transferring entity and/or borrower has had a consecutive ownership (on title) for at least the

most recent six (6) months prior to the disbursement of the new loan

Delayed Financing Refinances • Follow Fannie Mae requirements

• LTV/CLTV/HCLTV for rate and term refinances must be met. The loan is treated as a rate/term refinance except for primary residence transactions in Texas, which do not allow for delayed financing

Construction to Permanent Financing The borrower must hold title to the lot which may have been previously acquired or purchased as part of the transaction.

• LTV/CLTV/HCLTV is determined based on the length of time the borrower has owned the lot. The time frame is defined as the date the lot was purchased to the Note date of the subject transaction

• For lots owned twelve (12) months or more, the appraised value can be used to calculate the LTV/CLTV/HCLTV

• For lots owned less than twelve (12) months, the LTV/CLTV/HCLTV is based on the lesser of the current appraised value of the property or the total acquisition costs (documented construction costs plus documented purchase price of lot)

Back to Top

NOTE: Transfer of ownership from a corporation to an individual does not meet the continuity of obligation requirement.

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 16

Non-Arm’s Length Transactions A non-arm’s length transaction exists whenever there is a personal or business relationship with any parties to the transaction which may include the seller, builder, real estate agent, appraiser, lender, title company or other interested party. The following non-arm’s length transactions are eligible:

• Family sales or transfers

• Property seller acting as their own real estate agent

• Relative of the property seller acting as the seller’s real estate agent

• Borrower acting as their own real estate agent

• Relative of the borrower acting as the borrower’s real estate agent

• Borrower is the employee of the originating lender and the lender has an established employee loan program. Evidence of employee program to be included in loan file

• Originator is related to the borrower

• Borrower purchasing from their landlord (cancelled checks or bank statements required to verify

satisfactory pay history between borrower and landlord)

Gifts from relatives that are interested parties to the transaction are not allowed, unless it is a gift of equity. Real estate agents may apply their commission towards closing costs and/or prepaids if the amounts are within the interested party contribution limitations. Investment property transactions must be arm’s length.

Secondary/Subordinate Financing Allowed up to maximum CLTV per matrix. Secondary financing term must conform to FNMA guidelines.

Downpayment / Closing Cost Assistance Downpayment and closing cost assistance subordinate financing is not permitted.

Back to Top

(Remainder of page intentionally left blank)

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 17

Credit Requirements

Significant Derogatory Credit • Bankruptcy, Chapter 7, 11, 13: seven (7) years since discharge / dismissal date

• Foreclosure: seven (7) years since completion date

• Notice of Default: seven (7) years

• Short Sale/Deed-in-Lieu: seven (7) years since completion / sale date

• Forbearance Resulting in Subsequent Loan Modification: seven (7) years since exit from forbearance (see below Forbearance section for additional requirements)

• Mortgage accounts that were settled for less, negotiated or short payoffs: seven (7) years since settlement date

• Loan modifications:

o Lender initiated modification will not be considered a derogatory credit event if the modification did not include debt forgiveness and was not due to hardship as evidenced by supporting documentation. No seasoning requirement would apply

o If the modification was due to hardship or included debt forgiveness – seven (7) years since modification

• Multiple derogatory credit events not allowed, regardless if seasoned over seven (7) years

o A mortgage with a Notice of Default filed that is subsequently modified is not considered a multiple event

o A mortgage with a Notice of Default filed that is subsequently foreclosed upon or sold as a short sale is not considered a multiple event

• Tax liens, judgments, charge-offs, and past-due accounts must be satisfied or brought current prior to or at closing o Cash-Out proceeds from the subject transaction may not be used to satisfy judgments, tax liens,

charge-offs or past-due accounts o Payment plans on prior year tax liens/liabilities are not allowed; they must be paid in full

Back to Top

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 18

Forbearance Any loans that are shown to be in active or previous forbearance but where the borrower continued to make regularly scheduled payments and has made at least one (1) regularly scheduled payment since forbearance inception date are eligible.

• All payments must have been made within the month due

• The forbearance plan must be terminated at or prior to closing and the loan file must contain documentation that the forbearance is no longer active (i.e. removal letter from servicer, etc.).

Any loans (including but not limited to the subject mortgage) where a mortgage reflects reduced or missed payments under a forbearance and borrower has accepted a payment deferral, initiated a repayment plan or has reinstated the mortgage to return to a current status must meet the requirements below:

• Purchase & Rate/Term Refinance: o Three (3) consecutive months of required payments since completed forbearance plan o All payments must have been made within the month due

• Cash-out Refinance: o Twelve (12) consecutive months of required payments since completed forbearance plan o All payments must have been made within the month due

Payment Deferral

The refinance of a loan that has a payment deferral and where the amount of the deferred payments is included in the new loan is eligible as a rate/term transaction. Funds applied to pay off the prior loan, including the deferred portion, are not considered cash out.

Repayment Plan The full amount of the repayment plan monthly payment must be considered in meeting the required consecutive payment requirements (Purchase/Rate Term or Cash-out) detailed above

A mortgage subject to forbearance must utilize the mortgage payment history in accordance with the forbearance plan in determining late housing payments. Loan file must contain a letter of explanation from the borrower detailing the reason for forbearance and that the hardship no longer exists. Forbearance resulting in subsequent loan modification is considered a significant derogatory credit event and subject to a seven (7) year waiting period.

Back to Top

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 19

Housing History Mortgage history requirements:

• If the borrower(s) has a Mortgage in the most recent twenty-four (24) months, a mortgage rating must be obtained, reflecting 0x30 in the last twenty-four (24) months

• The mortgage rating may be on the credit report or a VOM

• Applicable to all borrowers on the loan

• The borrower(s) credit report must be reviewed to determine status of all mortgage loans, including documenting the mortgage is not subject to a loss mitigation program, repayment plan, loan modification or payment deferral plan. In addition to reviewing the credit report, MiMutual must also apply due diligence for each mortgage loan on which a borrower is obligated, including co-signed mortgage loans and mortgage loans not related to the subject transaction, to determine the loan payments are current as of the Note date of the subject transaction. Current means the borrower has made all payments due in the month prior to the Note date of the subject transaction and no later than the last business day of that month. Acceptable documentation includes one of the following: o Loan payment history from the servicer or third party verification service o Payoff statement for loans being refinanced o Current mortgage statement from the borrower o Verification of mortgage (VOM)

• If the mortgage holder is a party to the transaction or relative of the borrower, cancelled checks or bank statements to verify satisfactory mortgage history is required

Credit Report

Disputed Tradelines

• All disputed tradelines must be included in the DTI if the account belongs to the borrower unless documentation can be provided that authenticates the dispute.

• Derogatory accounts must be considered in analyzing the borrower’s willingness to repay. However, if a disputed account has a zero balance and no late payments, it can be disregarded.

Frozen Credit Credit reports with bureaus identified as “frozen” are required to be unfrozen, and a current credit report with all bureaus unfrozen is required for loans locked prior to September 9, 2021. For locks on/after September 9, 2021, FNMA guidance should be followed regarding frozen credit. However, the Jumbo AUS program requirement for all borrowers to have a minimum of two credit scores is still applicable, and must be from the remaining two unfrozen accounts.

Minimum Credit Requirements Non-traditional credit is not allowed.

Credit Score Requirements All borrowers must have a minimum of two (2) credit scores.

Back to Top

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 20

Debts and Liabilities

HELOC on Subject If subject property has a HELOC that is not included in the CLTV/HCLTV calculation, the loan file must contain evidence the HELOC has been closed. Tax Liens and Payment Plans If the most recent tax return or tax extension indicate a borrower owes money to the IRS or State Tax Authority, evidence of sufficient liquid assets to pay the debt must be documented if the amount due is within ninety (90) days of loan application date or if the tax transcripts show an outstanding balance due. A payment plan for the most recent tax year is allowed if the following requirements are met:

• Payment plan was setup at the time the taxes were due. Copy of the payment plan must be included in the loan file

• Payment is included in the DTI

• Satisfactory pay history based on terms of payment plan is provided

• Payment plan is only allowed for taxes due for the most recent tax year, prior years not allowed.

• For example, borrower files their 2019 return or extension in April 2020. A payment plan would be allowed for taxes due for 2019 tax year. Payment plans for 2018 or prior years would not be allowed

• Borrower does not have a prior history of tax liens

Lawsuit/Pending Litigation If the 1003, title commitment or credit documents indicate that the borrower is party to a lawsuit, additional documentation must be obtained to determine no negative impact on the borrower’s ability to repay, assets or collateral.

Income/Employment Requirements

Employment and Income Stability A two-year employment history is generally required. If the borrower(s) have less than a two-year employment and income history, a written analysis must be provided to justify the determination that the income used to qualify the borrower is stable.

Declining Income When the borrower has declining income, the most recent twelve (12) months should be used or the most conservative income calculation if the declining period is shorter than 12 months. Income must be stabilized and not subject to further decline in order to be considered for qualifying purposes. The employer or the borrower should provide an explanation for the decline and the underwriter should provide a written justification for including the declining income in qualifying.

Back to Top

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 21

General Documentation Requirements • Borrower(s) must have a minimum of two (2) years employment and income history

• Tax transcripts for personal tax returns are required when tax returns are used to document borrower’s income or any loss and must match the documentation in the loan file

• A 4506-C form is required to be signed at closing by all borrowers for all transactions

• Taxpayer consent form signed by all borrowers

• Verification of the existence of borrower’s self-employment must be verified through a third party source and no more than twenty (20) business days prior to the Note date. In addition, confirmation that the business is currently operating must be provided. Below are acceptable examples of documentation to confirm the business is currently operating:

• Evidence of current work (executed contracts or signed invoices) that indicate the business is operating on the day the lender verifies self-employment;

• Evidence of current business receipts within 10 days of the Note date (payment for services performed);

• Lender certification the business is open and operating (lender confirmed through a phone call or other means); or

• Business website demonstrating activity supporting current business operations (timely appointments for estimates or service can be scheduled

• Losses for secondary self-employment must be included in the DTI and self-employed documentation

requirements must be met

• Losses for co-borrower’s self-employment must be included in DTI and self-employed documentation requirements must be met

Salaried Borrowers • Income and Employment must be documented per the DU findings and all income sources and methods

of income calculation must meet the requirements in chapters B3-3 through B3-6 of the Fannie Mae Single Family Selling Guide, published June 3, 2020 and the requirements below.

• Secondary verification of the income documentation is required via W-2 transcripts or 3rd party verification (i.e., The Work Number) with separation of income types (base, bonus, OT, etc.). The number of years provided will be based on the DU findings. o Manual verification of employment, even if through a 3rd party are not permitted o Borrower pulled transcripts are not acceptable o The IRS transcripts and the supporting income documentation must be consistent o If 3rd party (i.e., TheWorkNumber) is the source used to verify income, then W-2 transcripts are also

required as the secondary verification of the income – see below.

Commission/Bonus Income

• Follow requirements above for salaried borrowers, and

• Commission/Bonus income must be documented for the most recent 2 (two) years with a year-to-date paystub and W-2s

Back to Top

Income Documentation Source Allowable Secondary Verification

Paystub and W2s W2 transcript(s) or TheWorkNumber

TheWorkNumber W2 transcript(s)

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 22

Self-Employment Self-Employed borrowers are defined as having 25% or greater ownership.

• Minimum 720 FICO when any self-employment income is required for qualifying purposes. If the self-employment income is not needed for qualifying purposes, then the 720 minimum is not applicable.

• In order to use self-employment income for qualifying purposes, the underwriter must consider the impact of COVID-19 on the business and the stability of income

Documentation Requirements The requirements below apply for Self-Employed Borrowers with Self-Employment income used for qualifying:

• Follow the requirements per the DU findings and the requirements in chapters B3-3 through B3-6 of the Fannie Mae Single Family Selling Guide, published June 3, 2020 except as detailed below: o If DU returns a recommendation for one (1) year of tax returns, the most recent year’s tax return

must be provided. IRS extensions are not permitted ▪ If borrower has filed an extension, the most recent prior two (2) years tax returns are required

• YTD profit and loss statement (audited or unaudited) up to and including the most recent month preceding the loan application date. YTD profit and loss statement must not be more than 60 days aged prior to the Note date o Audited P&L:

▪ An audited year-to-date profit and loss statement reporting business revenue, expenses, and net income up to and including the most recent month preceding the loan application date; OR

o Unaudited P&L: ▪ An unaudited year-to-date profit and loss statement signed by the borrower, reporting

business revenue, expenses, and net income up to and including the most recent month preceding the loan application date and three business depository account statements no older than the latest three months represented on the year-to-date profit and loss statement

• The three most recent business depository account statements must be reviewed and must support and/or not conflict with the level of business revenue reported in the current year-to-date profit and loss statement

• The business revenue analysis of the bank statements includes bank deposits from gross receipts from the business. Transfers and proceeds from the Small Business Administration PPP or any other similar COVID-19 related loans or grants should not be included

• If the year-to-date profit and loss statement cannot be supported by account statements, the self-employment income is not eligible for use in qualifying

o If the borrower has filed an extension for the current tax year, the year-to-date profit and loss statement must be provided to cover the full year

o If the year-to-date business income is less than the historically calculated income derived from the tax returns, the borrower may qualify by reducing the historical income to no more than the current level of stable monthly income using details from the year-to-date profit and loss statement and business account statements (if applicable)

Back to Top

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 23

Retirement Income (Pension, Annuity, 401(k), IRA Distributions) Existing distribution of assets from an IRA, 401(k) or similar retirement asset must be sufficient to continue for a minimum of three (3) years. If any retirement income will cease within the first three (3) years of the loan, the income may not be used.

Trust Income • Income from trusts may be used if guaranteed and regular payments will continue for at least three (3)

years

• Regular receipt of trust income for the past twelve (12) months must be documented

• Copy of trust agreement or trustee statement showing: o Total amount of borrower designated trust funds o Terms of payment o Duration of trust o Evidence the trust is irrevocable

• If trust fund assets are being used for down payment or closing costs, the loan file must contain adequate documentation to indicate the withdrawal of the assets will not negatively affect income

Restricted Stock and Stock Options • May only be used as qualifying income if the income has been consistently received for two (2) years

and is identified on the paystubs, W-2s and tax returns as income and the vesting schedule indicates the income will continue for a minimum of two (2) years at a similar level as prior two (2) years

• A two (2) year average of prior income received from RSUs or stock options should be used to calculate

the income, with the continuance based on the vesting schedule using a stock price based on the lower of the current stock price or the 52-week average for the most recent twelve (12) months reporting at the time of application. The income used for qualifying must be supported by future vesting based on the stock price used for qualifying and vesting schedule.

• Additional awards must be similar to the qualifying income and awarded on a consistent basis

• There must be no indication the borrower will not continue to receive future awards consistent with historical awards received

• Borrower must be currently employed by the employer issuing the RSUs/stock options for the RSUs/stock options to be considered in qualifying income

• Stock must be a publicly traded stock

• Vested restricted stock units and stock options cannot be used for reserves if using for income to qualify

• RSU income must be entered into DU as bonus income

Back to Top

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 24

Asset Depletion • Maximum 80% LTV/CLTV/HCLTV

• Primary residence 1-2 units only

• Purchase and rate/term refinances only

• Eligible assets must be held in a US account

• At least one borrower who is an account holder must be age 62 or older unless assets have been derived from the sale of a business

• Minimum post-closing assets:

o Borrowers ≥ 62 years of age = $500,000 o Borrowers < 62 years of age = $1,000,000

• Qualifying Asset Income = Net Eligible Assets divided by 240

• Net Eligible Assets equals Total Assets minus: o Funds required to be paid by borrower for closing (i.e. downpayment, closing costs, etc) o Gifts and/or borrowed funds o Reserves o Any portion of assets pledged as collateral for a loan

• Business funds not permitted to be included in total asset amount

• Assets must meet the eligibility and documentation requirements outlined in the below table

Asset Type Eligibility Requirements Documentation Requirements

Retirement Assets

• The retirement assets must be in a retirement account recognized by the Internal Revenue Service (IRS) (e.g., 401(k), IRA)

• Borrower must be the sole owner

• The asset must not currently be used as a source of income by the Borrower

• As of the Note Date, the Borrower must have access to withdraw the funds in their entirety, less any portion pledged as collateral for a loan or otherwise encumbered, without being subject to a penalty or an additional early distribution tax

• The Borrower's rights to the funds in the account must be fully vested

• Most recent retirement asset account statement

• Documentation evidencing asset eligibility requirements are met

*table continues on next page

Back to Top

Jumbo Underwriting Guidelines | Jumbo AUS

10.04.2021 25

Asset Type Eligibility Requirements Documentation Requirements

Lump-Sum Distribution Funds Not Deposited to an Eligible Retirement Asset

If the lump-sum distribution funds have been deposited to an eligible retirement asset, follow the requirements for retirement assets described above, otherwise:

• Lump-sum distribution funds must be derived from a retirement account recognized by the IRS (e.g., 401(k), IRA) and must be deposited to a depository or non-retirement securities account

• A Borrower must have been the recipient of the lump-sum distribution funds

• Parties not obligated on the Mortgage may not have an ownership interest in the account that holds the funds from the lump-sum distribution

• The proceeds from the lump-sum distribution must be immediately accessible in their entirety