Juan Pablo Jiménez - Tax Compact · Juan Pablo Jiménez [email protected] ITC-Workshop...

28

Juan Pablo Jiménez Economic Commission for Latin America and the Caribbean ITC-Workshop “How to Operationalize the International Tax and Development Agenda” 12-14 September 2011 Bonn, Germany

-

Upload

phungquynh -

Category

Documents

-

view

215 -

download

0

Transcript of Juan Pablo Jiménez - Tax Compact · Juan Pablo Jiménez [email protected] ITC-Workshop...

Juan Pablo Jiménez Economic Commission for Latin America and the Caribbean

ITC-Workshop “How to Operationalize the International Tax and Development Agenda”

12-14 September 2011 Bonn, Germany

I. Diagnosis and Challenges for Latin America Countries

II. Agenda and proposals

In average: low tax revenues But this is partially true

High heterogeneity between countries

Importance of non tax revenues

High volatility of fiscal revenues. Importance of fiscal revenue from commodities.

The tax structure is highly unbalanced:

Primacy of indirect taxes.

Low collection of income taxes.

Personal income tax is basically a tax on wage income.

Property taxes are insignificant.

Personal Income Taxes generate little revenue due to:

Significant levels of informality

Low tax compliance

Extensive use of tax incentives and preferential treatment of capital income

Political economy problems in implementing reforms

The widespread use of “tax expenditures” erodes the tax base

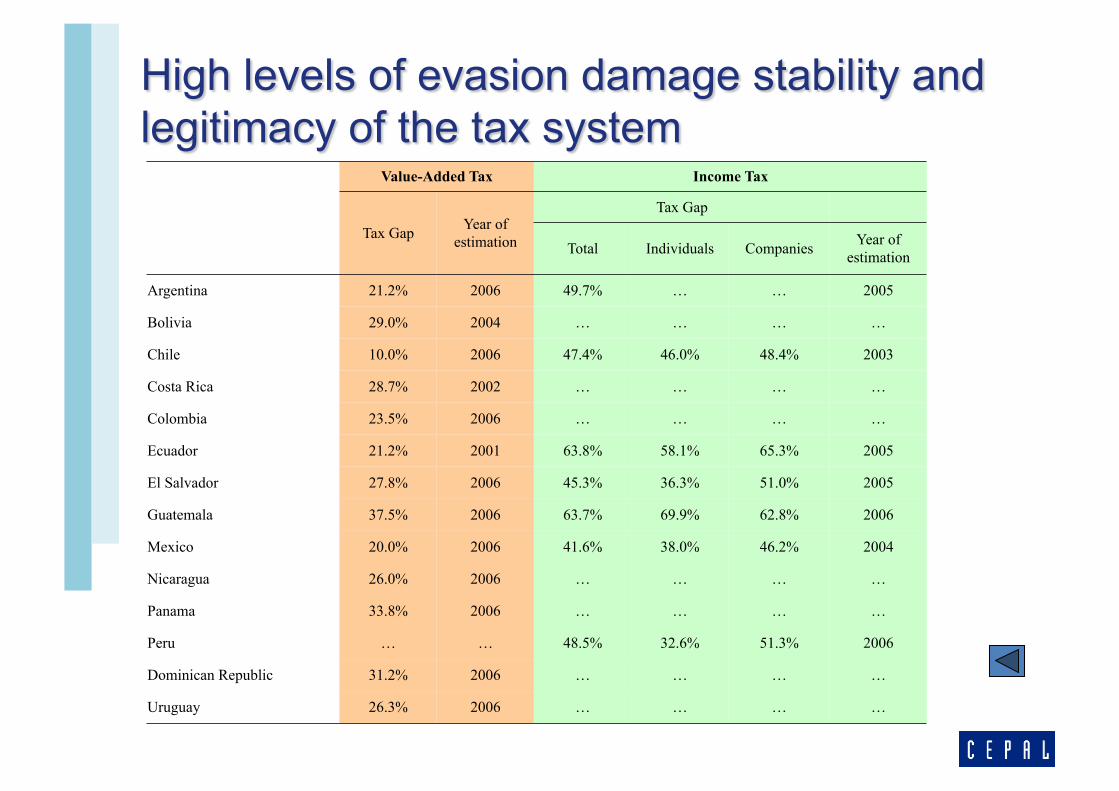

High levels of evasion damage stability and legitimacy of the tax system

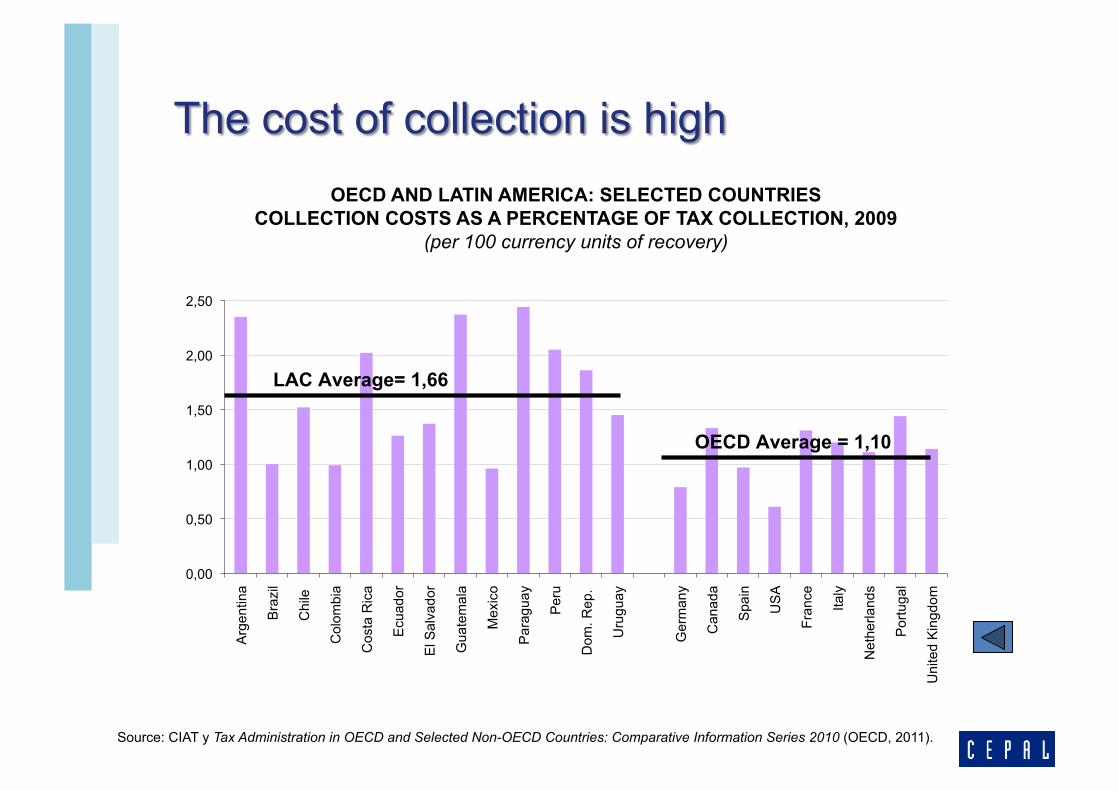

The cost of collection is high

These Declaration Principles are one step forward, but to advance it is necessary to include different regional and structural characteristics: Social inequality Informality Subregional disparities, Different institutional organizations (federal, unitary,

decentralized countries), Productive specialization, Strong concentration of power in elites…………….

The regional organizations could help to tailor an adequate regional and country responses.

Strengthen direct taxation, especially the personal income tax. Expand the tax bases Taxing capital income

Review the use of tax incentives: Set clear goals Improve measurement of tax expenditures Analyze the impact of these incentives

Improve capacity management and effective control of tax administrations

Measuring the tax evasion and tax gap.

Strengthen property taxes, especially at subnational levels.

Taxation of natural resources Political economy of the tax reform in LA So we could face two major challenges:

Rebuilding the fiscal space Addressing the multiple dimensions of

inequality in the region

Juan Pablo Jiménez [email protected]

ITC-Workshop “How to Operationalize the International Tax and Development Agenda”

12-14 September 2011 Bonn, Germany

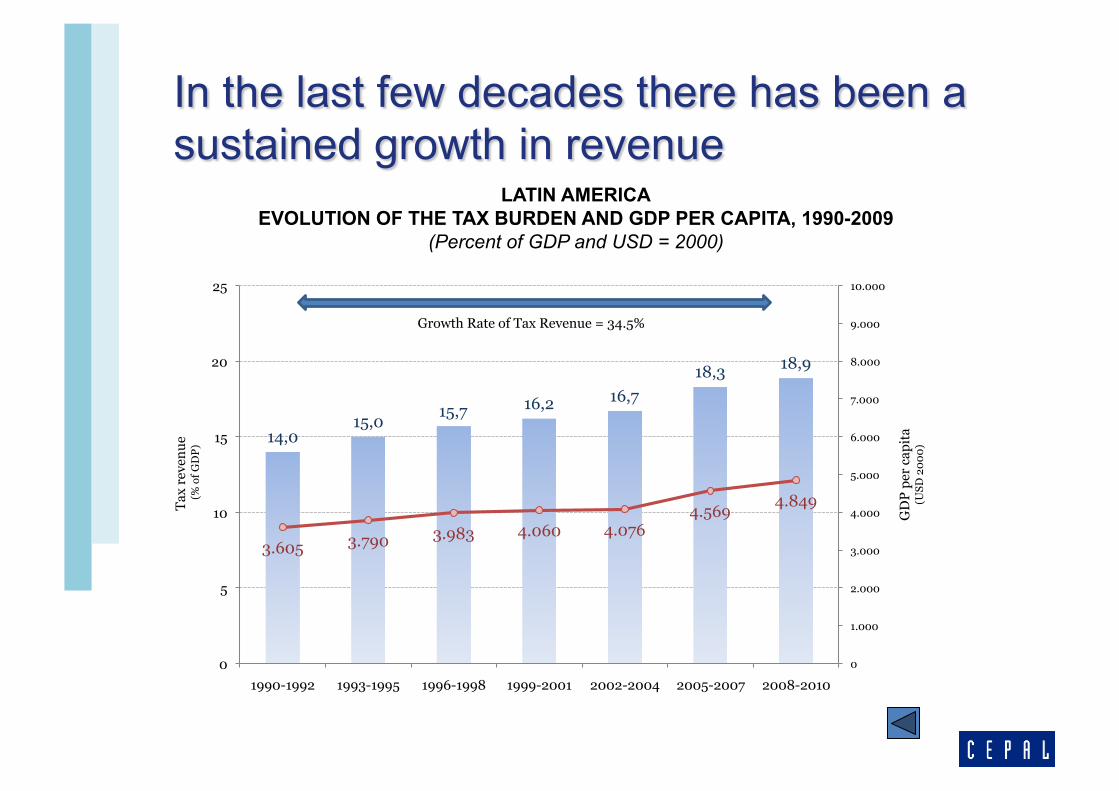

LATIN AMERICA EVOLUTION OF THE TAX BURDEN AND GDP PER CAPITA, 1990-2009

(Percent of GDP and USD = 2000)

14,0 15,0

15,7 16,2 16,7 18,3 18,9

3.605 3.790 3.983 4.060 4.076 4.569

4.849

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

0

5

10

15

20

25

1990-1992 1993-1995 1996-1998 1999-2001 2002-2004 2005-2007 2008-2010

GD

P pe

r ca

pita

(U

SD 2

000)

Tax

reve

nue

(% o

f GD

P)

Growth Rate of Tax Revenue = 34.5%

Note: Coverage is for central government, except for Argentina, Brazil, Bolivia, Chile, and Mexico which refers to general government (including tax revenues of subnational levels of government)..

0 5 10 15 20 25 30 35

México

Guatemala

Paraguay

Rep. Dominicana

El Salvador

Costa Rica

Venezuela

Ecuador

Colombia

Panamá

Perú

Honduras

Chile

Bolivia

Nicaragua

Uruguay

Argentina

Brasil

Percentage of GDP

2002-2010 1990-2001

GROUP 1

GROUP 2

GROUP 3

6

8

10

12

14

16

18

20

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011(p)

Other income Tax Revenue

LATIN AMERICA AND THE CARIBBEAN: COMPOSITION OF REVENUE, 1990-2011 (Percentages of GDP)

LATIN AMERICA AND EUROPE: SELECTED COUNTRIES VOLATILITY OF TAX REVENUE (WITHOUT SOCIAL SECURITY) 1980-2008

(Standard deviation of the tax revenue growth in USD, 2000)

12,3

4,5

0,0

5,0

10,0

15,0

20,0

25,0

Vene

zuel

a E

cuad

or

Cos

ta R

ica

Per

u B

oliv

ia

Arg

entin

a P

anam

a D

omin

ican

R

. P

arag

uay

ElS

alva

dor

Gua

tem

ala

Uru

guay

N

icar

agua

C

hile

H

ondu

ras

Mex

ico

Bra

zil

Col

ombi

a

Gre

ece

Icel

and

P

ortu

gal

Finl

and

Japa

n S

wed

en

Spa

in

US

A N

orw

ay

Net

herla

nds

Italy

A

ustra

lia

Uni

ted

Kin

gdom

D

enm

ark

Aus

tria

Fran

ce

Bel

gium

Latin America Developed countries

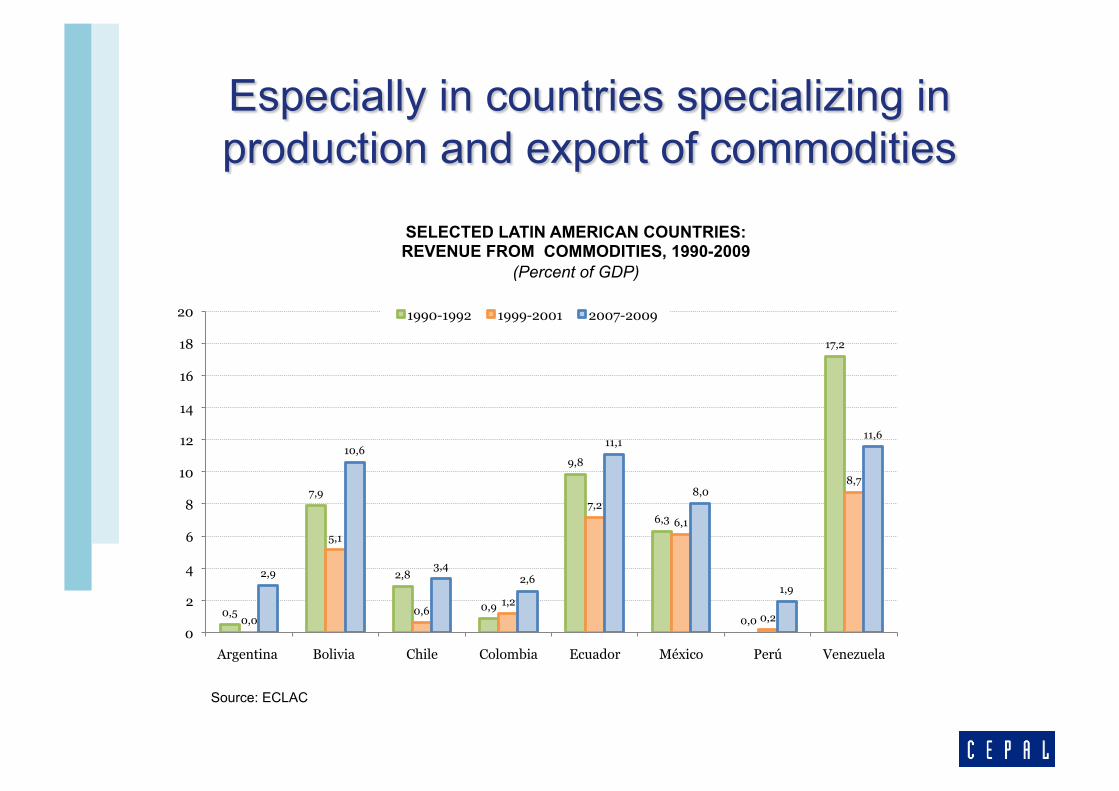

SELECTED LATIN AMERICAN COUNTRIES: REVENUE FROM COMMODITIES, 1990-2009

(Percent of GDP)

0,5

7,9

2,8

0,9

9,8

6,3

0,0

17,2

0,0

5,1

0,6 1,2

7,2

6,1

0,2

8,7

2,9

10,6

3,4 2,6

11,1

8,0

1,9

11,6

0

2

4

6

8

10

12

14

16

18

20

Argentina Bolivia Chile Colombia Ecuador México Perú Venezuela

1990-1992 1999-2001 2007-2009

Source: ECLAC

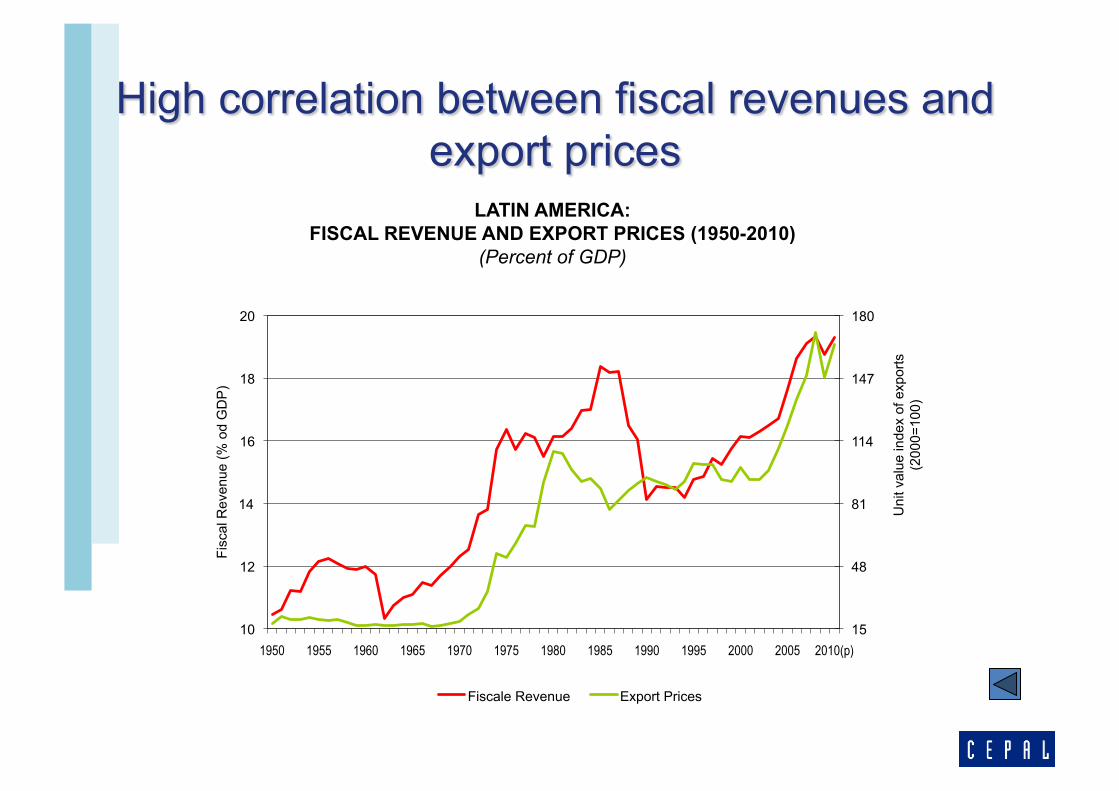

LATIN AMERICA: FISCAL REVENUE AND EXPORT PRICES (1950-2010)

(Percent of GDP)

15

48

81

114

147

180

10

12

14

16

18

20

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010(p)

Uni

t val

ue in

dex

of e

xpor

ts

(200

0=10

0)

Fisc

al R

even

ue (%

od

GD

P)

Fiscale Revenue Export Prices

Between 1990 and 2009, in the average tax structure at the regional level, the relative weight of indirect taxes (as VAT ) increased 54%, from 22.8% to 35.1% of total collections per year.

AMÉRICA LATINA : EVOLUCIÓN DE LA ESTRUCTURA TRIBUTARIA PROMEDIO, 1990-2009

(En porcentaje del total recaudado)

25,5

22,8

20,3

14,1

17,3

30,1

35,1

11,6

5,7

17,5

0

10

20

30

40

Direct Taxes (Income + Property)

VAT

Excises & others International trade & transactions

Social security contributions

1990 2009

LATIN AMERICA , OECD and USA AVERAGE REVENUE OF INCOME TAX

SELECTED LATIN AMERICAN COUNTRIES: TAX EXPENDITURES, 2007

The major methodological differences in the estimates of tax expenditures among countries restrict comparative analysis.

Country

As percentage of

GDP Tax Revenue

Argen8na 2.21 8.90

Brazil 2.29 9.10

Chile 4.97 24.60

Colombia 3.52 22.00

Ecuador 4.60 35.30

Guatemala 7.91 63.50

Mexico 5.92 50.70

Peru 2.05 11.90

OECD AND LATIN AMERICA: SELECTED COUNTRIES COLLECTION COSTS AS A PERCENTAGE OF TAX COLLECTION, 2009

(per 100 currency units of recovery)

Source: CIAT y Tax Administration in OECD and Selected Non-OECD Countries: Comparative Information Series 2010 (OECD, 2011).

0,00

0,50

1,00

1,50

2,00

2,50

Arg

entin

a

Bra

zil

Chi

le

Col

ombi

a

Cos

ta R

ica

Ecu

ador

El S

alva

dor

Gua

tem

ala

Mex

ico

Par

agua

y

Per

u

Dom

. Rep

.

Uru

guay

Ger

man

y

Can

ada

Spa

in

US

A

Fran

ce

Italy

Net

herla

nds

Por

tuga

l

Uni

ted

Kin

gdom

LAC Average= 1,66

OECD Average = 1,10

Value-Added Tax Income Tax

Tax Gap Year of estimation

Tax Gap

Total Individuals Companies Year of estimation

Argentina 21.2% 2006 49.7% … … 2005

Bolivia 29.0% 2004 … … … …

Chile 10.0% 2006 47.4% 46.0% 48.4% 2003

Costa Rica 28.7% 2002 … … … …

Colombia 23.5% 2006 … … … …

Ecuador 21.2% 2001 63.8% 58.1% 65.3% 2005

El Salvador 27.8% 2006 45.3% 36.3% 51.0% 2005

Guatemala 37.5% 2006 63.7% 69.9% 62.8% 2006

Mexico 20.0% 2006 41.6% 38.0% 46.2% 2004

Nicaragua 26.0% 2006 … … … …

Panama 33.8% 2006 … … … …

Peru … … 48.5% 32.6% 51.3% 2006

Dominican Republic 31.2% 2006 … … … …

Uruguay 26.3% 2006 … … … …

LATIN AMERICA TAX BURDEN, 1990-2001, 2002-2010

(Percentage of GDP)

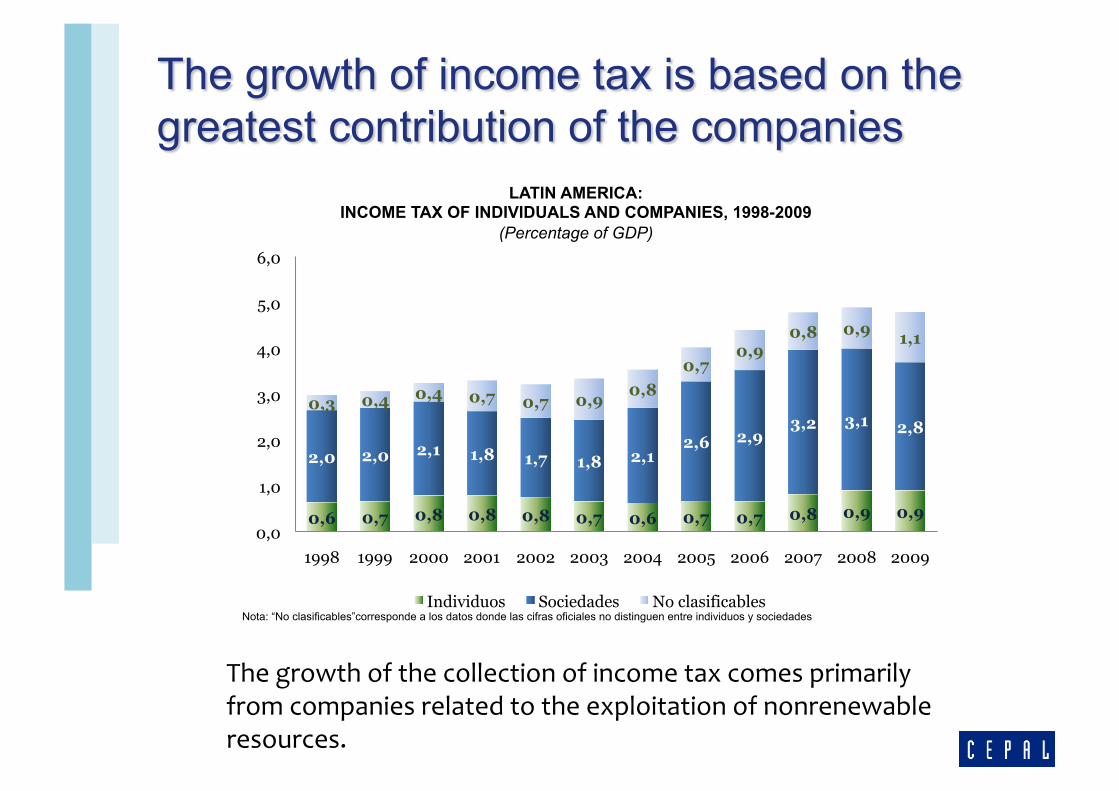

Nota: “No clasificables”corresponde a los datos donde las cifras oficiales no distinguen entre individuos y sociedades

LATIN AMERICA: INCOME TAX OF INDIVIDUALS AND COMPANIES, 1998-2009

(Percentage of GDP)

0,6 0,7 0,8 0,8 0,8 0,7 0,6 0,7 0,7 0,8 0,9 0,9

2,0 2,0 2,1 1,8 1,7 1,8 2,1 2,6 2,9

3,2 3,1 2,8 0,3 0,4 0,4 0,7 0,7 0,9 0,8

0,7 0,9

0,8 0,9 1,1

0,0

1,0

2,0

3,0

4,0

5,0

6,0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Individuos Sociedades No clasificables

The growth of the collection of income tax comes primarily from companies related to the exploitation of nonrenewable resources.

SELECTED COUNTRIES: STRUCTURE OF THE PERSONAL INCOME TAX, 2007

(Percentage of GDP)

Some issues related to fiscal policy: Undertake reforms, such as public management reform,

that may be necessary to launch and fuel sustainable capacity development processes

Strengthen public financial management capacity: Intensify efforts to mobilise domestic resources, strengthen

fiscal sustainability, and create an enabling environment for public and private investments.

Publish timely, transparent and reliable reporting on budget execution.

Take leadership of the public financial management reform process.

Strengthen as appropriate the parliamentary role in national development strategies and/or budgets

Some issues related to fiscal policy: Countercyclical policies should be expanded Public investment should be consistent with medium- and

long-term fiscal sustainability Continue to undertake fiscal reform, including tax reform. Continue to improve budgetary processes and to enhance

the transparency of public financial management and the quality of expenditures

Enhance tax revenues through modernized tax systems, more efficient tax collection, broadening the tax base and effectively combating tax evasion

Make tax systems more pro‑poor Promote international cooperation in tax matters