JPM_Spring_Mtgs_Apr_2014.pdf

54

(*) Deputy-Governor, International Affairs and Financial Regulation, Banco Central do Brasil. These remarks are personal and do not necessarily reflect the opinions of the Banco Central do Brasil (BCB) 1 Luiz Awazu Pereira da Silva* April 2014 Brazil Economic Outlook & Challenges when Normalization begins IMF-World Bank Spring Meetings 2014 Washington DC

-

Upload

angela-kulaif -

Category

Documents

-

view

212 -

download

0

Transcript of JPM_Spring_Mtgs_Apr_2014.pdf

(*) Deputy-Governor, International Affairs and Financial Regulation, Banco Central do Brasil. These remarks are

personal and do not necessarily reflect the opinions of the Banco Central do Brasil (BCB) 1

Luiz Awazu Pereira da Silva*

April 2014

Brazil Economic Outlook

& Challenges when

Normalization begins

IMF-World Bank Spring Meetings 2014

Washington DC

Outline

• Global Economy

• EMEs

• Brazil

– Fundamentals, Differentiation, Policy Reaction

– Inflation

– Growth

– Challenges

2

Main Messages (1)

• Global economy a bit better (e.g., US recovery, less tail risks/false positive in EuroZone, China)

• Normalization has begun, it’s a net positive; better coordination, FED’s communication on UMP exit (e.g., separation, spillovers, caution); repricing underway of EMEs assets w/ some volatility

• Nothing really new in challenges faced by EMEs (Impossible Trinity, Mundell-Fleming) during GFC (e.g., transmission of K flows into inflation, asset prices, exchange rate, credit market, etc.), except for unprecedented speed+intensity + simultaneity of UMP (ZIF+QE+FG) in 3 major monetary areas

3

Main Messages (2)

• EME monetary policy frameworks (IT or not) had to address challenges posing significant risks to monetary and/or financial stability (e.g., typical “boom” & “feel good” moment, followed by “sudden stop”, reversal); but not only an EME bp (e.g., EZ periphery, Baltics, East-Asia)

• Good news: many EMEs had experienced, more prepared are always riding some global financial cycle (local MP in AE have global effects), we are always into some kind of “beauty contest”, especially deficit-savings countries

• Bad news (in a while): UMP unprecedented, AEs’ exit not synchronized (FED, BoJ, ECB), “New Normal”’ equilibria?

4

Main Messages (3) • Brazil’s textbook response in this transition is working

well: flexible ER, AD management (FP+MP) with sizeable buffer of self-insurance (reserves); MaPs worked well for financial stability and complemented MP in upswing; FX buffer is important to reduce volatility during “tapering” and help financial stability (FS)

• Brazil’s took early action (MP), prepared the reversal, addressed inflation pressure (early 2013), put in place FX hedge program, but challenges remain: ST high-persistent inflation, sticky expectations, supply shock food prices, growth-confidence nexus; MLT rotating growth from C to I, more TFP through increasing physical & human K stocks

5

Slightly Better but Complex, Why?

• UMP unprecendented policy framework, despite the FED’s much improved FG for exit there are the Known Unknowns and the Unknown Unknowns, like what?

• AEs: NAIRU, labor market & wage, transmission into inflation, neutral rate, risks of new bubbles, potential growth & “secular decline”, etc. Issue: anxiety about “control” over slope of yield curve & timing of future changes in monetary conditions (anticipation?)

• EMEs: life after “easy money” and the commodity super-cycle? “Decoupling” or “middle-income growth traps”? Issue: anxiety about how local political economy conditions would allow necessary & timely adjustments

6

7

Different Studies for Nairu, Phillips Curve and ST-LT Unemployment & Inflation wages in the US

Source: Krueger, Alan B. Cramer, Judd, and Cho. Are the Long-Term Unemployed on the Margins of the Labor Market?, Brookings Panel on Economic Activity, March 20–21, 2014, Princeton University & NBER

8

US-Nairu

Source: Deutsche Bank. U.S. Employment Outlook. Sep., 2013.

9

US-Do you look by duration?

Source: Krueger, Alan B. Cramer, Judd, and Cho. Are the Long-Term Unemployed on the Margins of the Labor Market?, Brookings Panel on Economic Activity, March 20–21, 2014, Princeton University & NBER

US-Do you look by skills?

10

0

2

4

6

8

10

12

14

16

18m

ar-

00

nov-0

0

jul-01

mar-

02

nov-0

2

jul-03

mar-

04

nov-0

4

jul-05

mar-

06

nov-0

6

jul-07

mar-

08

nov-0

8

jul-09

mar-

10

nov-1

0

jul-11

mar-

12

nov-1

2

jul-13

mar-

14

%

Unemployment Rates by Education

Less than a high school diploma High school graduates, no college

Less than a bachelor's degree College graduates

Source: US Bureau of Census for the Bureau of Labor Statistics - Current Population Survey (CPS)

11

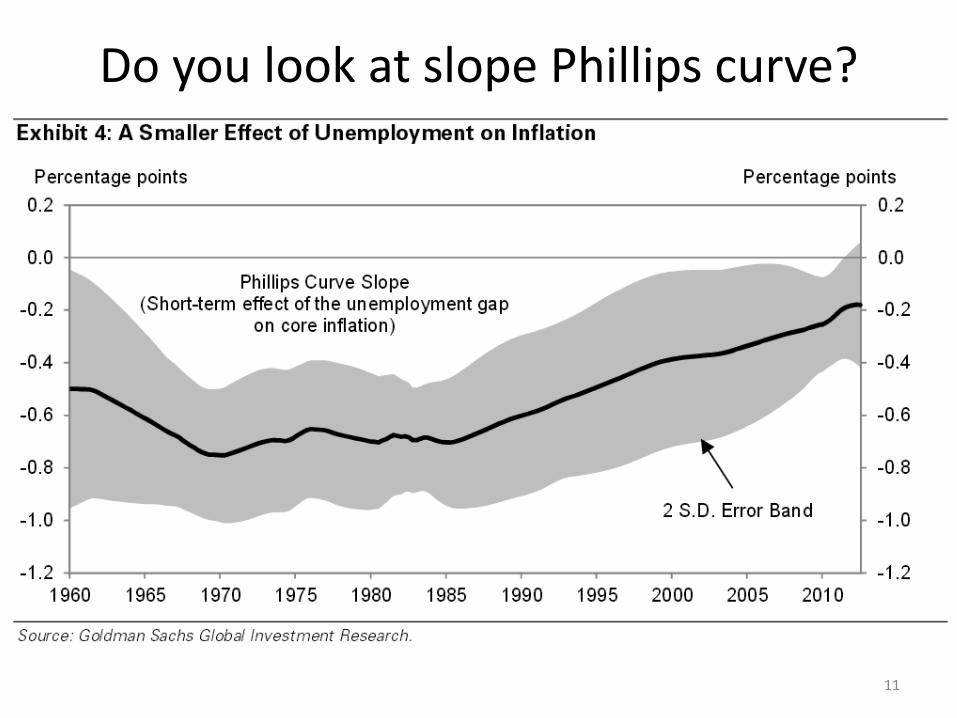

Do you look at slope Phillips curve?

Do you look at slope Phillips curve?

12 Source: IMF, Monetary Policy In the New Normal, SDN April 2014

13

US-Which Unemployment Projects Better Wage Growth?

14

US-Which Unemployment Measure Projects Better CPI?

US-Unskilled Labor Wage Moderation

15

70

75

80

85

90

95

100

105

110

115

mar

00

set 00

mar

01

se

t 0

1

mar

02

set 02

mar

03

set 03

mar

04

set 04

mar

05

set 05

mar

06

set 06

mar

07

set 07

mar

08

se

t 0

8

mar

09

set 09

mar

10

set 10

mar

11

set 11

mar

12

set 12

mar

13

set 13

méd

ia d

e 2

008

= 1

00

Weekly and hourly earnings data from the Current Population Survey

Less than a high school diploma High school graduates, no college*Some college or associate degree Bachelor's degree or higher

Source: US Bureau of Census for the Bureau of Labor Statistics - Current Population Survey (CPS)

US: No inflationary surprises

16

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%J

an

12

Fe

b 1

2

Ma

r 1

2

Ap

r 1

2

Ma

y 1

2

Ju

n 1

2

Ju

l 1

2

Au

g 1

2

Se

p 1

2

Oc

t 1

2

No

v 1

2

De

c 1

2

Ja

n 1

3

Fe

b 1

3

Ma

r 1

3

Ap

r 1

3

Ma

y 1

3

Ju

n 1

3

Ju

l 1

3

Au

g 1

3

Se

p 1

3

Oc

t 1

3

No

v 1

3

De

c 1

3

Ja

n 1

4

Fe

b 1

4

Yo

Y

PCE PCE - Core Dallas FED - trimmed mean

Sources: US Bureau of Economic Analysis (BEA), FED and Bloomberg

17

Similar Nairu Changes – selected AEs

Source: la Serve, M.E.; Lemoine, M. 2011. Measuring the Nairu: a complementary approach. Document de Travail 342. Banque de France.

Thin line: unemployment rate; bold line: tv-Nairu; dotted lines: 95%-confidence interval; dashed line: unemployment gap.

18 Source: The Neutral Interest Rate and the Stance of Monetary Policy in Brazil. Anpec 2013

And Great Moderation Neutral interest rate?

19

And Great Moderation Neutral interest rate?

Source: THE EFFECTIVENESS OF MONETARY POLICY SINCE THE ONSET OF THE FINANCIAL CRISIS ECONOMICS DEPARTMENT WORKING PAPER No. 1081. OECD

And Policy Rates in EMEs? My Taylor is Poor?

Sources: IMF, International Financial Statistics and World Economic Outlook; Bloomberg; CEIC;

Consensus Economics; Datastream; national data; BIS calculations.

Baseline for Exiting UMP in the US

• Net positive for the rest of the World, despite ST volatility that will also depend on local policy stances and conditions

• FED communication is working, separation “tapering” & “tightening”, cautious approach, mindful of spillovers

• Labor market conditions, different Studies for Nairu, Phillips Curve and ST-LT unemployment & inflation wages in the US nominal wage rigidity in downturn might moderate and/or delay wage adjustment in upturn

• Neutral interest rates different studies for AEs levels after Great Moderation and GFC might have changed

• For the moment: despite these uncertainties, stick to Baseline, as the most likely scenario

21

Chronicle of a Death Foretold: EME

• As the Story goes: EMEs benefitted from “easy money” and allowed excessive relaxation of policy stances

• Local political economy favored counter-cyclical policy (especially the expansionary bit)

• Fundamentals deteriorated (e.g., asset-credit bubbles, higher current account deficits, inflationary pressure, fiscal stance-debt-to-GDP ratios, external financing for both corporates and sovereigns, etc.)

• No structural reforms in good times: lower growth prospects in the future

• Perfect storm in the making: higher vulnerability to “sudden stops” crisis looming

22

Our Answer in Brazil: No Quite So..

23

Brazil: Fundamentals

• Floating ERR, repricing of assets and depreciation is part of the solution and is not vulnerability

• Financial Sector has proven resilience, strong capital, provision and liquidity indicators

• Ratios of external financing (stocks and flows) are strong & sustainable

• Hedge program is contributing to reduce volatility, including after “perfect storm” events (e.g., tapering, EME January sell-off, Brazil’s downgrading)

24

External Financing

25 Source: IIF e Datastream

0 10 20 30 40 50

India

Colombia

Indonesia

Brazil

Mexico

Peru

SouthAfrica

Chile

Turkey

%

External Debt/GDP

0 10 20 30

Brazil

Colombia

Peru

SouthAfrica

Chile

Mexico

India

Indonesia

Turkey

%

Short Debt/Total External Debt

2013*

2012

Source: BCB

External Debt Ratios

120,6%

63,4%

38,8%

19,9% 27,8%

13,9%

0

20

40

60

80

100

120

140

short term debt/intl.reserves

debtservices/exports

external debt/GDP

Dec 03 Feb 14*

%

*estimate

Liquid Assets to Short Term

Liabilities

11,6

12,0

13,3

13,4

13,9

14,0

14,3

14,4

14,4

14,7

14,8

15,7

16,1

16,4

17,1

19,1

10 12 14 16 18 20

Australia

Spain

India

Russia

Italy

South Korea

France

United States

Canada

Japan

South Africa

Turkey

Mexico

United Kingdom

Brazil

Germany

26,1

36,1

40,0

44,9

45,0

46,7

49,9

72,5

76,4

82,0

96,9

121,4

140,3

160,0

0 50 100 150 200

India

South Africa

United Kingdom

Canada

Australia

Mexico

Japan

Turkey

United States

Russia

Italy

South Korea

Germany

Brazil

-86,3

-31,9

-22,2

-19,2

-14,7

-14,5

-13,6

-13,6

-10,9

-6,0

-3,9

-3,2

7,7

10,6

-120 -20 80

Italy

Spain

South Africa

Japan

Australia

United Kingdom

United States

India

Russia

Canada

South Korea

Turkey

Mexico

Brazil

Source: IMF (FSI – latest available data)

Sound financial system Regulatory Capital to

Risk-Weighted Assets ( Provisions – NPL) / Capital

Source: BCB

Feb 14

Origin of Bank Funding

Banks: Low Share of External Funding

95,6

88,7 85,6

91,2

4,4

11,3 14,4

8,8

60%

80%

100%

public-owned private-owned foreign-controlled total

Domestic External

Source: Bloomberg

UMP exit brought higher volatility

5,0

7,5

10,0

12,5

15,0

17,5

jan 1

3

fev 1

3

mar

13

abr

13

mai 13

jun

13

jul 1

3

ago

13

set

13

out 1

3

nov 1

3

dez 1

3

jan 1

4

BRL Volatility (3-Months At-the-money Implied)

Chairman BB May 22 Speech

But FX hedge program effect

30

2,1

2,15

2,2

2,25

2,3

2,35

2,4

2,45

2,5-6000

-5000

-4000

-3000

-2000

-1000

0

1000

2000

3000

USD millions

Swap Repo FX USD.BRL

Brazil: Resulting Differentials

31

-10

-5

0

5

10

SinceMay

22,2013

2 Weeks 2014

NEER (chg %) *

* Positive sign indicates appreciation of the country's currency / group.

-8-6-4-202468

10

Since May22,2013

2 Weeks 2014

USD/Currency (chg %) *

Brazil: Resulting Differentials

32

-40-30-20-10

010203040

Since May22,2013

2 Weeks 2014

CDS (chg bps)

-15

-10

-5

0

5

10

Since May22,2013

2 Weeks 2014

Equity (chg %)

Brazil: Reversal of Sentiment?

33

IOF on fixed income at 6% IOF on fixed income at 0% IOF on equities at 2% IOF on equities at 0%

-200

-100

0

100

200

300

400

500

Portfolio Investment - Net Flows (USD Millions)

Equities Bonds Other Flows

Monthly Avg.

USD Millions

Source: Central Bank of Brazil. Inflows from forex contracts.

Brazil: Policy Anticipation & Reaction

• We knew that reversal of market sentiment would eventually come and prepared ourselves, accumulated sizeable reserves to be used as buffers (alternative strategy: less reserves and more reliance on multilateral support like IMF-FCL)

• Preventive measures during upswing (MaPs for tightening excessive credit growth); keep strong capital, provisions & liquidity in our financial system, cautious reliance on external sources of funding

• Took early and sizeable action on Monetary Policy, complemented by Fiscal Policy

34

Brazil: Why Then Such Variance? Because there are legitimate albeit difficult analytical challenges everywhere and in particular in Brazil:

• Where is our NAIRU? Effects on wage bargaining process?

• Where is our Neutral interest rate? Down and MP more effective in an environment of less confidence

• How long would our J-Curve take? And then to affect domestic absorption and growth?

And in addition:

• Inflation headline hit by temporary supply shock, headline inflation impacts expectations, issue of persistence (see Roache, IMF (2014))

• Growth: confidence indicators in transition; supply policies (investment in infrastructure underway)

35

Skilled Wage Moderation?

36

Are we in the opposite symetric of the US case? Would it also affect unskilled wage cycles?

80

90

100

110

120

130

140

150

ago

02

fev 0

3

ago

03

fev 0

4

ago

04

fev 0

5

ago

05

fev 0

6

ago

06

fev 0

7

ago

07

fev 0

8

ago

08

fev 0

9

ago

09

fev 1

0

ago

10

fev 1

1

ago

11

fev 1

2

ago

12

fev 1

3

ago

13

fev 1

4

200

8 A

ve

rag

e+

10

0

Without formal education 1 to 3 years of schooling

4 to 7 years of schooling 8 to 11 years of schooling

Source: Ministry of Labor and Employment/CAGED.

Sources: BM&FBovespa / BCB

Real Actual Interest Rate %

an

nu

al

Apr 4th

4.9%

360-day market rate discounted by the IPCA expected for the next 12 months (Focus)

0

5

10

15

20

25abr

02

abr

03

abr

04

abr

05

ab

r 0

6

abr

07

abr

08

abr

09

abr

10

abr

11

ab

r 1

2

abr

13

abr

14

38

Neutral interest rate - literature review shows large variation

Source: The Neutral Interest Rate and the Stance of Monetary Policy in Brazil. Anpec 2013

39 Source: Nicolas E. Magud and Evridiki Tsounta. To Cut or Not to Cut? That is the (Central Bank’s) Question. IMF Working Paper. October 2012

Compared to our Region?

Brazil: Headline Inflation

• Inflation has been high and resistant, reflecting the elevated services inflation inertia and administrated prices realignment

• BCB has acted to secure the convergence of inflation to the target.

• MP effects on inflation are cumulative and take place with lags. In this sense, significant part of prices response to the tightening cycle is yet to materialize.

• At this moment, there are renewed external and domestic food price pressure, but in a much tighter monetary conditions environment

40

Sources: IBGE / FGV

% in 1

2 m

on

ths

3.22% IPP Nov 11

6.25% IPA-10 Nov 11

8.05% IPA-DI Mar 14

8.24% IPP Feb 14

0

2

4

6

8

10n

ov 1

1

jan 1

2

mar

12

mai 12

jul 1

2

set 12

nov 1

2

jan 1

3

mar

13

mai 13

jul 1

3

set 13

nov 1

3

jan 1

4

mar

14

IPP IPA (10, M and DI)

Producer Price Indexes

Sources: IBGE / Fipe / FGV

% in 1

2 m

onth

s

IPC-Fipe = 5.12% 1st/Apr 14

IPC-DI = 6.09% Mar 14

IPCA = 6.15% Mar 14

INPC = 5.62% Mar 14

3,5

4,0

4,5

5,0

5,5

6,0

6,5

7,0

7,5fe

v 1

2

abr

12

jun 1

2

ago

12

out 1

2

dez 1

2

fev 1

3

abr

13

jun 1

3

ago

13

out 1

3

dez 1

3

fev 1

4

abr

14

IPCA-15 and IPCA INPC IPC-Fipe IPC (10, M and DI)

Consumer Price Indexes

-3

0

3

6

9

12

15

18

21

24

27ja

n 0

1

jan 0

2

jan 0

3

jan 0

4

jan 0

5

jan 0

6

jan 0

7

jan 0

8

jan 0

9

jan 1

0

jan 1

1

jan 1

2

jan 1

3

jan 1

4

Variation (

%)

12 m

on

ths a

ccum

ula

ted

IPCA Alimentação e bebidas IPCA exceto Alimentação e bebidas

Source: IBGE

IPCA and Food Prices Component

5,47

Abr/2013

14,0

5,68

June/2008

15,8

May/2003

27,0

6,31

Food and Beverages IPCA ex-Food and Beverages

Headline Dependent Expectations?

44

y = 1,7299x + 0,0106 R² = 0,79

y = 3,0765x + 0,0661 R² = 0,50

y = 1,527x - 0,0011 R² = 0,81

-3,0

-2,0

-1,0

0,0

1,0

2,0

3,0

4,0

5,0

-1 -1 0 1 1

Ch

ange

in E

xpec

ted

An

nu

al IP

CA

an

ual

aft

er a

Su

rpri

se in

Mo

nth

ly IP

CA

(in

m+1

, v-

a-v

m-1

)

Surprise in monthly IPCA mensal (v-a-v expected IPCA of each period)

Change in Expected Annual IPCA anual after a Surprise in Monthly IPCA

m-1 m m-2

Source: BCB/DEPEC.

Sources: BCB / IBGE

Inflation – Convergence to Target %

yo

y

*Central Bank of Brazil Forecast (Inflation Report – Mar 14)

reference

scenario*

target (4.5%)

0

2

4

6

8

10m

ar

05

mar

06

mar

07

mar

08

mar

09

mar

10

mar

11

mar

12

mar

13

mar

14

mar

15

mar

16

46

J – Curve Lags, about one year?

Sources: MOURA, GUILHERME and SERGIO DA SILVA, (2005) "Is There a Brazilian J−Curve?", Economics Bulletin, Vol. 6, No. 10 pp. 1−17, July 2005. HSING, Y. “A Study of the J-Curve for Seven Selected Latin American Countries”, Global Economy Journal, 2008, 8(4). KALYONCU, H., OZTURK, I., ARTAN, S., KALYONCU, K. “Devaluation and trade balance in Latin American countries”, Zb. rad. Ekon. fak. Rij., 2009, vol. 27, sv.1, 115-128. ONAFOWORA, OLUGBENGA, (2003) "Exchange rate and trade balance in east asia: is there a J−curve?." Economics Bulletin, Vol. 5, No. 18 pp. 1−13, 2003. BAHMANI-OSKOOEE, M. and GOSWAMI, G. G. “A Disaggregated Approach to Test the J-Curve Phenomenon: Japan versus Her Major Trading Partners” Journal of Economics and Finance, Volume 27, Number 1, Spring 2003. AHMAD, J. AND YANG, J. “Estimation of the J-Curve In China”, East-West Center Working Papers”, Economic Series, nº 67, March 2004. HALICIOGLU, F. “The Bilateral J-curve: Turkey versus her 13 Trading Partners”, Munich Personal RePEc Archive Paper No. 3564, 15. June 2007. BAHMANI-OSKOOEE, M., GOSWAMI, G. G. and TALUKDAR, B. K. “The Bilateral J-Curve: Australia Versus her 23 Trading Partners”, Australian Economic Papers, Blackwell Publishing Ltd/University of Adelaide and Flinders University, June 2005 and Moodley, S. “An estimation of the J-Curve effect between South Africa and the BRIC countries”, University of Pretoria, nov. 2010.

No evidence / partial evidence (p)

N ot specify the lag

South Africa 1 Argentina 1 3,5 Austr a lia p

Chile 1 China 1 Colo mbia 1 Ec uador 1 Indon e sia 4 Japan p Malaysia 4 Me xico 1 Peru 1 4 T hailand 1 Tur key 1 Uruguay 4

Number of citations Lag (quarter s)

Source: Bloomberg

Ind

ex D

ec 0

7 =

100

Cumulative Real GDP Growth

Growth since the Global Financial Crisis

118.0 117.7

117.7

110.2

106.3

97.9

90

95

100

105

110

115

1204

Q 0

7

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

Poland Brazil South Korea Mexico US Euro Area

Source: UNCTAD

Brazil - Leading destination for FDI

197,9

114,7

85,7

82,7

50,6

48,6

48,5

46,9

43,3

42,8

40,8

35,2

32,5

30,6

29,2

0 50 100 150 200

US

China

Belgium

Hong Kong

UK

Singapore

Brazil

Germany

Russia

Ireland

Spain

Australia

Switzerland

France

Saudi Arabia

Thousands

2010

226,9

124,0

103,3

96,1

66,7

65,8

64,0

52,9

51,1

41,4

40,9

40,4

34,3

31,6

29,5

0 50 100 150 200

US

China

Belgium

Hong Kong

Brazil

Australia

Singapore

Russia

UK

Canada

France

Germany

Italy

India

Spain

Thousands

2011

146,7

119,7

72,5

65,3

62,5

58,9

54,4

48,5

47,2

44,1

39,6

27,3

26,4

22,6

19,3

0 50 100 150

US

China

Hong Kong

Brazil

UK

France

Singapore

Australia

Canada

Russia

Ireland

India

Chile

Luxembourg

Belgium

Thousands

2012

49

5%

7%

7%

7%

7%

10%

12%

17%

30%

33%

0 5 10 15 20 25 30 35

Mexico

Japan

Indonesia

Russia

India

UK

Brazil

Germany

US

China

%

Which 3 countries, excluding the country in which the CEO is based, do they consider most

important for their overall growth prospects over the next 12 months? *

Source: PwC 17th Annual Global CEO Survey *Base: 1,344 respondents

Global CEO Survey 2014: Key Countries

Model Rotation: GFCF / GDP (%)

50

Brazil: Prospects & Challenges • Brazilian economy is also passing through a transition,

with investment expansion and families’ consumption moderation.

• Brazil has been conducing a structural reform agenda to qualify work force, amplify investments and boost productivity, as well as improving business environment.

• Concerning investments, it is noteworthy the ample concessions program, which includes the transfer of airport, road, railroad and port management to private sector.

51

Brazil: Prospects & Challenges

• Brazilian economy faces a transition period pursuing new engines to growth: productivity gains and investment expansion. In 2014, economic activity should be somewhat lower than in 2013.

• Industry – recovery, but not very strong signs of support.

• Services – lower growth rates than previous years.

• Agribusiness – record harvest year after year, besides bad weather in 2014.

52

Brazil: Prospects & Challenges

• Investiment started to grow again in 2013 (~6% more than the ~2% for private consumption) – continuity will depend on confidence and tends to gain traction led by infrastructure projects and oil fields exploration.

• Reform agenda – more efficient allocation of production factors of the economy and productivity gains.

53

Thank You!

54