JOURNAL - hubinvest.com · It is an oral gel to treat mucositis caused by cancer treatment ... THE...

12

JUNE 2015 JOURNAL 03 EXPERT VIEWS Front line views on AIM FEATURE 20 years of AIM ADVISERS finnCap invests for growth STATISTICS Market indices and statistics 08 09 11 Malaysian AIM spin-off 02 GENERAL NEWS New hope for Accsys In this issue Malaysian property company Eastern & Oriental (E&O) is planning to spin off its UK property project management business onto AIM later this year. The flotation will raise additional cash to help expand these activities and give the UK business a higher profile. Eastern & Oriental Property (UK) (E&O UK) has acquired a number of London property assets, including ESCA House, Landmark House and Thames Tower. The plan is to redevelop them into residential and mixed-use developments. For example, ESCA House in Bayswater was acquired for £27.7m in 2014 and the plan is to make it wholly residential. The flotation is being handled by Peel Hunt. The plan is to offer shares to new investors and also give E&O shareholders the chance to subscribe for new shares in the UK company. E&O itself will sell part of its existing stake to members of its own management. The amount of money to be raised is still to be decided. AllianceDBS Research says that it expects E&O to reduce its shareholding in E&O UK to below 50% but remain the largest shareholder. This means that the UK business will no longer be consolidated. The flotation of E&O UK should help the Malaysian holding company to cut its gearing to 30%. US expansion for Midatech Midatech Pharma appears to have found an ideal way to gain entry to the US cancer treatment market. Midatech’s all-share bid for Nasdaq-listed DARA BioScience is valued at $24m (£15.8m). The deal provides Midatech with a revenue-generating business with a US sales force that can be used to sell Midatech products, the first of which could be Q-Octreo, which is for treating excessive growth-hormone production. Midatech is offering 0.272 of one of its shares (subject to final adjustment) and a contingent value right for each DARA share. As part of the process, Midatech will admit ADRs to Nasdaq and this is why the bid will not be completed until later in the second half of 2015. The contingent value rights could be worth up to $5.7m (£3.8m) depending on the sales of the main products. If sales targets of Gelclair and Oravig are met they should generate the cash to finance the additional payment. Gelclair is already on sale and accounted for most of the bid target’s 2014 revenues of $1.9m. It is an oral gel to treat mucositis caused by cancer treatment. Oravig, which is an oral thrush treatment, is due to launch by the end of the year. DARA had $9.8m in the bank at the end of March 2015 but this will have fallen by completion. 06 NEWS Upmarket Safestay 04 NEWS Real Good disposal 07 DIVIDENDS Income Vertu THE ONLINE MONTHLY FOR THE ALTERNATIVE INVESTMENT MARKET finnCap www.finnCap.com HubInvest publishes AIM Journal www.hubinvest.com

Transcript of JOURNAL - hubinvest.com · It is an oral gel to treat mucositis caused by cancer treatment ... THE...

JUNE 2015

JOURNAL

03

EXPERT VIEWS

Front line views on AIM

FEATURE

20 years of AIM

ADVISERS

finnCap invests for growth

STATISTICSMarket indices and statistics

080911

Malaysian AIM spin-off02 GENERAL NEWS

New hope for Accsys

In this issue

Malaysian property company Eastern & Oriental (E&O) is planning to spin off its UK property project management business onto AIM later this year. The flotation will raise additional cash to help expand these activities and give the UK business a higher profile.

Eastern & Oriental Property (UK) (E&O UK) has acquired a number of London property assets, including ESCA House, Landmark House and Thames Tower. The plan is to redevelop them into residential and mixed-use developments. For example, ESCA House in Bayswater was acquired for £27.7m in 2014 and the plan is to make it wholly residential.

The flotation is being handled by Peel Hunt. The plan is to offer shares to new investors and also give E&O shareholders the chance to subscribe for new shares in the UK company. E&O itself will sell part of its existing stake to members of its own management. The amount of money to be raised is still to be decided.

AllianceDBS Research says that it expects E&O to reduce its shareholding in E&O UK to below 50% but remain the largest shareholder. This means that the UK business will no longer be consolidated. The flotation of E&O UK should help the Malaysian holding company to cut its gearing to 30%.

US expansion for Midatech Midatech Pharma appears to have found an ideal way to gain entry to the US cancer treatment market. Midatech’s all-share bid for Nasdaq-listed DARA BioScience is valued at $24m (£15.8m). The deal provides Midatech with a revenue-generating business with a US sales force that can be used to sell Midatech products, the first of which could be Q-Octreo, which is for treating excessive growth-hormone production.

Midatech is offering 0.272 of one of its shares (subject to final adjustment) and a contingent value right for each DARA share. As part of the process, Midatech will admit ADRs to Nasdaq and this is why the bid

will not be completed until later in the second half of 2015. The contingent value rights could be worth up to $5.7m (£3.8m) depending on the sales of the main products. If sales targets of Gelclair and Oravig are met they should generate the cash to finance the additional payment.

Gelclair is already on sale and accounted for most of the bid target’s 2014 revenues of $1.9m. It is an oral gel to treat mucositis caused by cancer treatment. Oravig, which is an oral thrush treatment, is due to launch by the end of the year.

DARA had $9.8m in the bank at the end of March 2015 but this will have fallen by completion.

06 NEWS

Upmarket Safestay

04 NEWS

Real Good disposal

07 DIVIDENDS

Income Vertu

THE ONLINE MONTHLY FOR THE ALTERNATIVE INVESTMENT MARKET

finnCapwww.finnCap.com www.finnCap.com

HubInvest publishes AIM Journal www.hubinvest.com

June 20152

Shell buys Accsys’ Chinese licenseeStandard list shell Cleantech Building Materials (CBM)'s takeover deal could be good news for AIM-quoted Accsys Technologies if it means that production of Accoya, a treated softwood that is more durable than normal softwoods, finally commences in China. CBM plans to acquire Diamond Wood China, the Hong Kong-based company that has an exclusive licence from Accsys to manufacture and sell Accoya in China.

Accsys entered into this licence agreement with Diamond Wood in 2007 and tried to terminate it in 2013. An arbitration tribunal in 2014 ruled that the licence should not be terminated even though Diamond Wood had failed to secure finance and build an Accoya manufacturing plant. This ruling cost Accsys €3.1m in costs and damages, the latter at €250,000 were much lower than the €100m claimed. As part of the arbitration

ruling, Diamond Wood still has to try to construct an Accoya manufacturing plant.

CBM has around £700,000 in cash but that will not be enough to finance a plant and initial sales of Accoya. Possibly taking advantage of the lower regulatory requirements for a standard listing, CBM has revealed little detail about the transaction and it is not clear whether Diamond Wood has any cash. More information will become available once CBM applies to join AIM and the company says it then plans to seek equity and debt funding to build a manufacturing plant.

The bid is six CBM shares for every 25 Diamond Wood shares. Limited liquidity has enabled the CBM share price to rise from the initial placing price of 1p in February to the suspension price of 7.88p – with a bid-offer spread of 6p-9.25p.

general news

Online gaming technology supplier Playtech has launched an agreed bid of 400p a share for spreadbetting company Plus500, whose share price had previously slumped on the back of UK money-laundering compliance issues. The bid is well above the Plus500 flotation price of 115p a share from a couple of years ago but major shareholder Odey Asset Management does not believe that the offer is high enough despite the current woes of the Israel-based firm. Odey believes the bid is opportunistic and it owns 19.5% of Plus500 and rather appropriately holds a further 6% under a contract-for-difference instrument. This puts Odey in a strong position to influence the outcome of any bid. JP Morgan has also recently increased its stake to 8.5%. If there is a rival bid, Playtech will receive a break fee of £20.7m.

Plus500 battle

Merger peril for EIS investorsIn a ruling that is relevant to any Enterprise Investment Scheme (EIS) investor a tribunal has ruled that HMRC was correct in withdrawing EIS relief from investors in LED lighting technology developer PhotonStar following its reversal into AIM-quoted LED lighting business Enfis.

However, tribunal judge Robin Vos said that “it is surprising and, for the appellants, very unfortunate that relief should be withdrawn in these circumstances”. He added that it is a matter for the legislature to decide whether to amend the law for “what is perhaps an unintended consequence” of the

existing legislation. PhotonStar had 12 to 15 EIS

investors who put money into the company in the 2008-09 and 2009-10 tax years and four of them, who invested £160,000 out of a total of £712,000 raised, were appellants in the case. At the end of 2010, PhotonStar reversed into Enfis via an all-share offer, which left PhotonStar shareholders with 77.5% of the enlarged group, renamed PhotonStar LED Group. A year later only one group employee had originally been an employee of Enfis.

In October 2010, PKF wrote to HMRC to request confirmation that

finnCap www.finnCap.com

Enfis still qualified for EIS relief and this was confirmed. Even though, the holding company still qualified the company it acquired did not. In April 2011, HMRC wrote to PhotonStar saying that it no longer qualified for EIS purposes because it had become a subsidiary of PhotonStar LED. This meant that the EIS relief was clawed back from the investors.

If PhotonStar had acquired Enfis, the PhotonStar shareholders would have retained their EIS relief. This does appear unfair and it means that EIS-qualifying companies will have to consider this potential consequence of a reversal.

HubInvest publishes AIM Journal www.hubinvest.com

HubInvest publishes AIM Journal www.hubinvest.com

June 2015 3

advisers

finnCapwww.finnCap.com www.finnCap.com

COMPANY NEW BROKER OLD BROKER NEW NOMAD OLD NOMAD DATE

Botswana Diamonds Northland/Dowgate Westhouse/Dowgate Northland Westhouse 01/05/2015Connemara Mining Northland/Dowgate Westhouse/Dowgate Northland Westhouse 01/05/2015 CompanyGemfields Macquarie/JP Morgan JP Morgan Cazenove/ Grant Thornton Grant Thornton 01/05/2015 Cazenove/BMO BMOEleco finnCap Cenkos finnCap Cenkos 05/05/2015Atlas Development & Stifel Nicolaus Cantor Fitzgerald/ Stifel Nicolaus Cantor Fitzgerald 06/05/2015 Support Services Ltd MC Peat/GMPGulfsands Petroleum Cantor Fitzgerald/ RBC/First Energy Cantor Fitzgerald RBC 06/05/2015 FirstEnergySula Iron & Gold VSA VSA Strand Hanson Cairn 06/05/2015Caledonia Mining WH Ireland Numis/WH Ireland WH Ireland Numis 08/05/2015 CorporationAction Hotels Investec finnCap Investec finnCap 11/05/2015Lekoil Ltd BMO/Mirabaud Mirabaud/UBS Strand Hanson Strand Hanson 11/05/2015Vipera Sanlam Beaumont Cornish Sanlam Beaumont Cornish 11/05/2015Cdialogues Allenby Mirabaud Allenby Strand Hanson 12/05/2015Castle Street Investments N+1 Singer Peel Hunt N+1 Singer Peel Hunt 14/05/2015Amphion Investments Northland/Panmure Panmure Gordon Panmure Gordon Panmure Gordon 19/05/2015 GordonImmedia Group SI Capital/Daniel Stewart Daniel Stewart SPARK SPARK 21/05/2015Jubilee Platinum Beaufort /Daniel Stewart Daniel Stewart SPARK SPARK 22/05/2015Mosman Oil & Gas SP Angel SP Angel/SI Capital SP Angel ZAI 22/05/2015Publishing Technology Cenkos Westhouse Cenkos Westhouse 26/05/2015APC Technology Group Cantor Fitzgerald Northland Strand Hanson Strand Hanson 28/05/2015Ferrum Crescent Ltd Beaufort Beaufort Strand Hanson RFC Ambrian 29/05/2015Magnolia Petroleum Sanlam/Cornhill Capital Northland Cairn Cairn 29/05/2015NAHL Group Investec Investec/Espirito Santo Investec Investec 29/05/2015StatPro Group Panmure Gordon Cenkos Panmure Gordon Cenkos 29/05/2015

ADVISER CHANGES - MAY 2015

finnCap invests for growthDespite a tough market backdrop AIM adviser finnCap, a sponsor of AIM Journal, raised more than £220m for its clients in the year to April 2015 and its corporate retainer income has risen by 11%. According to finnCap chief executive Sam Smith: "We have had another good year and consolidated our position as the lead broker and adviser to growth companies. We have invested in new areas of the business and senior hires, providing us with the right foundations to continue our positive trajectory."

In the year to April 2015, revenues

were 4% higher at £16.1m, while pre-tax profit was slightly reduced from £2.4m to £2.2m due to the additional hires and investment in new business areas. The broker was able to repay its debt in the period and still have cash in the bank.

Retainer income grew by 11% to £4.6m and corporate fees were more than one-fifth higher at £7.2m. Market making had a tough first half but recovered in the second half, while secondary trading levels remain weak.

finnCap has been the top AIM broker in terms of number of clients

for some time and the size of client is increasing so that it has become one of the top ten brokers to the constituents of the FTSE AIM 100 index. finnCap is also a top five adviser and broker to all London Stock Exchange companies and last year became a Main Market sponsor.

Recent hires include Tim Redfern, who joined from Canaccord Genuity, in corporate broking and Carl Holmes and Jonny Franklin-Adams, previously with Charles Stanley and N+1 Singer respectively, in corporate finance.

HubInvest publishes AIM Journal www.hubinvest.com

June 20154

company news

finnCap www.finnCap.com

Real Good deal enables focus on higher-margin bakery and ingredients operations

Real Good Food has completed the disposal of its sugar business, Napier Brown. This has strengthened significantly the balance sheet. Changes in the European sugar market and a price war with British Sugar had caused difficulties for Napier Brown and its performance had been patchy. Real Good Food will be able to grow its other operations, which are not so dependent on the sugar market.

Even though Napier Brown had returned to profit it makes sense to sell it to France-based Tereos, which is the fifth-largest sugar supplier in the world. The EU is ending sugar beet production quotas from 2017 and the combined business is better placed to cope with the

changes. Last year, Tereos generated revenues of €4.7bn. The Napier Brown business, which includes the Whitworths retail brand, generated revenues of £172m in the year to March 2015.

This leaves Real Good Food with three main activities, which have higher margins. Cake decoration operations include Renshaw and Rainbow Dust Colours, which was acquired in January. The food ingredients division includes Garrett Ingredients and R&W Scott. Garrett is a business that is still subject to

sugar price movements. The third division is the Haydens bakery business, which supplies retailers including Waitrose.

These continuing businesses made EBITDA of £5.3m on revenues of £104m in the year to March 2015. The full-year figures will be published in July.

Year-end net debt was £30.1m but this will be wiped out by the £34m received from the disposal of Napier Brown, plus an additional £7m payment covering working capital at completion. The strengthened balance sheet will enable Real Good Food to seek acquisitions.

GVC mulls over bid for bwin.party digital

GVC is joining forces with Amaya Inc, a much larger TSX-listed gaming businesses operator, to put forward proposals to acquire fully listed bwin.party digital entertainment, although 888.com is a rival. Daniel Stewart believes the deal, which would be valued at £900m plus, makes sense for both bidders.

Amaya owns a number of gaming brands, including PokerStars and Full Tilt. There is no indication about what parts of the business GVC and Amaya want but the latter is likely to be interested in the online poker operations. In 2011, bwin reported revenues of €611.9m. That includes

€81.7m from poker – down by nearly one-third on the previous year. Group EBITDA was €101.2m, whereas GVC made EBITDA of €49.2m on revenues of €225m.

GVC and Amaya would jointly finance a bid for bwin. GVC had a similar agreement with William Hill when the two firms acquired Sportingbet, with William Hill taking the Australian and Spanish operations. The Sportingbet acquisition has proved an excellent deal for GVC and

it wasted little time reducing costs and generating significantly improved profit from the purchase.

If the bid is successful, this could possibly hold back the GVC dividend as the business is integrated. The GVC dividend policy is to pay at least three-quarters of net operating cash flow each year and dividends have been growing. When Sportingbet was acquired the integration went so well it did not have a significant effect on the payout, though. A dividend of more than 40p a share is forecast for 2015, although as it is announced in euros –the quarterly dividend is €0.14 a share – it depends on the exchange rate.

GVC HOLDINGS (GVC) 461p

12 MONTH CHANGE % + 2.7 MARKET CAP £m 287.8

Bakery products and ingredients www.realgoodfoodplc.com

Online gaming www.gvc-plc.com

REAL GOOD FOOD (RGD) 47.5p

12 MONTH CHANGE % + 33.8 MARKET CAP £m 28.5

The balance sheet has been strengthened

company news

finnCapwww.finnCap.com www.finnCap.com

June 2015 5

Cross-selling opportunities enable APC to improve energy efficiency

Energy efficiency has become the largest revenues generator for APC Technology and it is reducing dependence on a limited number of customers.

Last year, Morrison generated the bulk of energy efficiency-related revenues and this meant that a break in LED lighting installations at the supermarkets operator had an enormous affect on revenues. Morrison started spending again in the second quarter of this financial year but, even with an expected upturn in the second half, it will no longer dominate energy efficiency revenues, which are running at annualised rate of more than £14m and growing rapidly.

In the six months to February 2015, revenues grew from £12.1m to £14.5m – £8.3m from energy efficiency business Minimise and £6.2m from

electronic component distribution. Water compliance services provider Green Compliance was acquired at the beginning of the period and included for the first time in these figures. Additional investment has been made to cope with future growth and increased costs mean that underlying pre-tax profit fell from £761,000 to £115,000. Net debt was £1.35m at the end of 2014.

Royal Mail is a major customer for monitoring systems and LED lighting which help the postal service to reduce energy consumption. Bringing Green Compliance into the group significantly increases the number of group customers and provides cross-

selling opportunities. For example, Minimise has installed LED lighting for Canary Wharf and it has proposed the installation of a toilet flushing system that could reduce water consumption by 85%.

New house broker Cantor Fitzgerald does not expect a significant full-year profit. The investment will start to pay off next year and a profit of £1m is forecast for the year to August 2016, rising to £2.7m the following year as margins improve. The shares are trading on 15 times 2015-16 prospective earnings, falling to seven in 2016-17. If APC does manage to grow this quickly there will be a need for additional working capital and borrowings will increase.

Nature on course for recovery

Maritime and offshore waste treatment business Nature has had challenges in recent years but the future appears more positive. Nature is rebuilding its Gibraltar facility having sorted out insurance payments and planning constraints. This means management can concentrate on growing the business. A US business has been acquired and an Oman-based operation is due to be launched early in 2016.

Nature dominates the oily waste collection market in the port of Rotterdam and there are signs of an

upturn in demand. A 65% stake was acquired in a Houston-based business and it is investing £350,000 on equipment.

Despite the weak oil price, there continues to be demand from offshore explorers for the company’s transportable compact treatment and sludge treatment units. There are 12 units in operation in five different

offshore regions of the world. Treating waste on rigs can save 50% or more of the cost of transporting it back to shore to be treated.

In 2014, revenues declined from £21.8m to £17.7m. Having made a pre-tax profit of £1.3m, before exceptional write-downs and gains, the previous year, Nature lost nearly £3m in 2014. Net debt was £1.27m at the end of 2014. The cash position was subsequently improved by the sale of the storage vessel M/T Crystalwater for £1.9m. Nature is in a good position to start its move back towards profit.

NATURE GROUP (NGR) 13.63p

12 MONTH CHANGE % - 53.8 MARKET CAP £m 10.8

Energy efficiency www.apc-plc.co.uk

Wastewater treatment www.ngrp.com

APC TECHNOLOGY (APC) 17.5p

12 MONTH CHANGE % - 64.5 MARKET CAP £m 15.4

Minimise installed LED lighting for Canary Wharf

June 20156

company news

Upmarket hostels operator Safestay has been quoted on AIM for just over a year and it has made strong progress in this period. In the summer, there will be three hostels in operation in the UK and there are plans to acquire further sites in the UK and the rest of Europe. There could be scope for up to six hostels in London and the plan is to grow to more than 20 hostels in total.

When it joined AIM, Safestay’s only hostel was the former Labour party headquarters in Walworth Road, Elephant & Castle, and this had an occupancy rate of 78% in 2014. Just after flotation a York hostel was acquired for £2.35m and at the end of 2014 a 50-year lease was acquired on a former Jacobean mansion in Holland Park, which was formerly

run as a hostel by the Youth Hostels Association, £2m is being spent on refurbishment. There will be more than 900 beds once the three hostels are all up and running.

Net debt was £5.8m at the end of 2014. The £1.024m of loan notes issued to acquire the York hostel have been repaid from a £1m, five-year loan facility provided by Coutts. The investment in Holland Park and York is likely to increase net debt to £7.1m at the end to 2015.

It will take time for the Holland Park occupancy to build up and York and Elephant & Castle still

have further to go in reaching their optimal occupancy levels. House broker Westhouse forecasts a profit of £800,000 in 2015, rising to £1.4m as the investment starts to generate a higher return.

Safestay has the backing of a number of institutional investors that are ready to put up more cash to finance the right acquisitions. Miton Group owns 29.9% and River & Mercantile 7.8% and there are other institutions with smaller stakes. Safeland, the AIM-quoted property investor which formed the Safestay business, still owns 12.1%.

SAFESTAY (SSTY) 68p

12 MONTH CHANGE % + 12.9 MARKET CAP £m 13.1

finnCap www.finnCap.com

Safestay seeks to roll out upmarket hostel chainHostel operator www.safestay.co.uk

Palace makes Northampton leisure bet

UK regional property investor Palace Capital is acquiring a leisure scheme in Northampton by acquiring O&H Northampton Ltd for £1 and repaying £20.7m of debt and money owed to creditors. The cost equates to the valuation of the site by DTZ. This valuation can be increased by improving the rental returns on the site and refinancing the debt.

Santander is providing a loan facility of £11.39m to cover part of the debt taken on with the

acquisition. A placing at 360p a share is raising £20m – the costs of the placing and acquisition will absorb £1.3m of this cash.

The property being purchased is a 190,000 square foot scheme called Sol Central, which includes an Ibis Hotel and a ten-screen Vue cinema. There is also a gym and a sports club, plus vacant units

leased to Gala Casinos and a pub operator. On top of this there is an unlet restaurant site. Net annual rental income of £1.89m, including £287,000 a year from car park income, provides a yield of 8.86% on the buying price, including costs.

Palace’s existing property portfolio was valued at £102.8m at the end of March 2015, while net debt was £24.7m. Just after this, Bank House in Leeds was acquired for £10m. The NAV at the end of March 2015 was 396p a share.

PALACE CAPITAL (PCA) 389p

12 MONTH CHANGE % + 49 MARKET CAP £m 78.7

Property www.palacecapitalplc.com

The plan is to grow to more than 20 hostels

Dividend

Motor dealer Vertu Motors announced a final dividend of 0.7p a share, taking the total for 2014-15 to 1.05p a share. The dividend is covered more than 4.5 times by underlying earnings. The dividend is forecast to grow to 1.2p a share this year and 1.35p a share in the year to February 2017. The dividend cover is expected to remain well above four times.

Vertu started life as a shell at the end of 2006, when it raised £25m at 60p a share in order to become a consolidator in the motor dealer sector, and in the following March Bristol Street Group, which was then the thirteenth-largest motor dealer in the UK, was acquired for £31m in cash and up to £9m in shares. A further £26.2m was raised at 75p a share. The share price fell to 10p at the end of 2008 but it has recovered since then.

Vertu paid its maiden dividend of 0.2p a share in January 2011 and the total dividend for the financial year to February 2011 was 0.5p a share. The dividend has increased every year since then, with the latest dividend providing the fastest annual growth of 31%.

Business

Selling cars is a low-margin business and that is why Vertu is keen to grow its aftersales revenues, which managed gross margins of 43.5% last year, against 7.5% for new cars and 2.5% for new fleet car sales. Used cars have a slightly higher gross margin of 10.4%. This means that although aftersales account for less than 9% of sales they generate nearly one-third of gross profit for the company.

The key to getting those aftersales revenues is making sure that customers bring back the cars they have purchased from the dealer for servicing in subsequent years. Vertu’s strategy is to offer three-year service plans to customers. These plans offer fixed prices for the regular services and they provide regular monthly payments for Vertu.

Vertu has 116 dealerships, with Ford and Vauxhall accounting for nearly 30% of them. Vertu is the third-largest Ford retailer in the UK. In all, Vertu has dealerships covering a total of eighteen car manufacturers and two that are Honda motorcycle dealers. The latest acquisitions were a Jaguar dealer in Bradford and a Land Rover dealer in Bury. Car makers are reducing the number of dealerships that represent them and this should lead to larger outlets, which need a financially secure operator to invest in them in order to secure the profit potential.

In the year to February 2015, revenues grew 23% to £2.07bn and underlying pre-tax profit was a quarter higher at £22m. That progress came from a combination of organic and acquisitive growth. A profit of £24.5m is forecast for the current year, which puts the shares on eleven times prospective earnings. There is still scope to enhance these earnings with further acquisitions.

Aftersales focus for Vertu MotorsMotor dealer www.vertumotors.com

Dividend newsUtility services provider Fulcrum Utility Services returned to profit in the year to March 2015 and it is paying a maiden dividend of 0.4p a share. Net cash was £5.58m at the end of March 2015 so Fulcrum can afford to start paying a growing dividend. The reported 2014-15 pre-tax profit of £606,000 was better than expected, even after £500,000 of exceptional charges. This compares with a loss of £4.49m, after £3.68m of exceptional charges, in 2013-14. The fixed cost base has been cut from £11m to £7m over the past two years. Fulcrum plans to invest in further pipeline assets which will provide a predictable revenue stream. House broker Cenkos has upgraded its 2015-16 pre-tax profit forecast to £2.4m.

Carpets retailer United Carpets has declared a special dividend of 1p a share. This follows last year’s capital reorganisation to eliminate the deficit on the company’s distributable reserves and the reporting of the latest interim figures when pre-tax profit improved from £452,000 to £534,000. Net cash was £1.73m at the end of September 2014. United Carpets has not paid a dividend since 2011 even though it had returned to profit in the year to March 2013. United Carpets has eleven of its own stores and 47 franchised stores.

Touch sensors manufacturer Zytronic increased its interim dividend by 10% to 3.14p and it is still on course to pay a total full-year dividend of 11p a share, up from 10.3p a share. In the six months to March 2015, pre-tax profit improved from £1.41m to £1.62m on revenues that increased from £8.83m to £10m. Net cash, after financial liabilities, was £6.77m at the end of March 2015. Demand for touch screens for cash and vending machines is increasing and there are newer markets such as gaming machines.

dividends

Price (p) 64

Market cap £m 222.9

Historical yield 1.6%

Prospective yield 1.9%

finnCapwww.finnCap.com www.finnCap.com

June 2015 7

VERTU MOTORS (VTU)

June 20098

Wolf nears tungsten production in DevonBy MARTIN POTTS

Wolf Minerals offers exposure to a tungsten mining business with imminent first production and

cash flow. Construction of the company’s Drakelands mine in Devon is around 95% complete, with first production on schedule for Q3 2015. At full capacity, the mine will produce more than 4,500 tonnes of WO3 in concentrate per year (around 3.5% of global demand). We have a 23p price target and a Buy recommendation.

Wolf was admitted to the ASX in February 2007 and then AIM on 30

November 2011. The company initially focused on exploring for tungsten in Australia, but before the end of 2007 it acquired the rights to the Hemerdon project in Devon. This became the sole focus.

Wolf is expected to be significantly profitable at current tungsten prices, although these prices are expected to strengthen considerably in the second half of 2015 and beyond. This will be driven by rising global demand, particularly in China, versus constrained supply, with no new tungsten mines apart from Drakelands currently under construction globally.

The project has been thoroughly studied, not least by experts retained by Resource Capital Funds (RCF), the largest shareholder. On the back of those studies, RCF committed c$91m to the project, most of which has been spent.

The UK is a particularly low-risk country by the standards of the mining industry, and offers an incentivising tax regime. The project enjoys almost unanimous local support, where the creation of around 300 direct and indirect jobs is a key benefit.

Tungsten

Tungsten has the highest melting point (3,422 °C, 6,192 °F), lowest vapour pressure (at above 1,650 °C, 3,000 °F) and the highest tensile strength of any metal in its pure form. The largest use of tungsten is in cemented and tungsten carbides (55%), which are used to make wear-abrasive materials and cutting tools. This makes it essential for many industries including mining, oil and gas, construction, automotive and aerospace. Tungsten components are also used in

many other sectors, including lighting technology, electronics and jewellery.

China is responsible for around 82% of global production; the second-largest producer, Russia, has a 4.4% share. Despite its dominant position, China remains a net importer. The government has responded to this by increasing regulation in the tungsten industry by establishing production and export quotas to favour value-adding downstream products, imposing export taxes on tungsten materials, limiting or forbidding foreign investment, and stopping illegal mining and small inefficient mines as it strives to drive up productivity.

As a result, supply has become tighter, thereby concerning Western governments. The World Trade Organisation recently ruled that China’s export restraints were inconsistent with its WTO obligations. As a result, China cancelled its export quota for 2015 but has increased control of domestic production by adding a 6.5% tax.

Against this backdrop, demand is set to continue to grow, closely tied to GDP growth, especially in China. In the

next few years, mine production from outside China is expected to increase. Several companies are working to develop tungsten deposits or restart tungsten production from inactive mines. However, the amount and timing of future production will depend on the companies’ ability to acquire funding.

The medium- to long-term outlook for the tungsten price is positive, with costs of production steadily moving up in real terms as low-cost production from Chinese mines becomes exhausted, the mines get deeper and Chinese wages increase.

In the short term, prices have been unusually depressed and the price is expected to recover from current levels, with a supply squeeze helping to sustain higher prices. We are looking for a price of $300/MTU for the year to June 2016 and $375/MTU thereafter.

Financials

Wolf should start to generate cash later this year. We forecast revenues to rise from zero in the present year to A$97.4m in 2015-16 and A$182.7m in 2016-17. Profits will rise similarly, with 2016-17 being effectively a steady state in terms of our model.

For the purpose of valuation, we have assumed that the capital programme at Drakelands will be complete by our valuation date of 30 June 2015 – in other words, our DCF model of the mine assumes that the capex is all sunk and the debt has been fully drawn down and is included in the valuation.

We have used DCF methodology to set our target price of 23p. This is some 27% above the present price of the stock.

MARTIN POTTS is a finnCap research director specialising in mining

i

Expert view: The broker

June 20158

expert views

finnCap www.finnCap.com

finnCap www.finnCap.com

Wolf is expected to be significantly profitable at current tungsten prices

HubInvest publishes AIM Journal www.hubinvest.com

feature

finnCapwww.finnCap.com www.finnCap.com

June 2015 9

www.finnCap.com

Robin Boyle has been involved with AIM since day one. One of the first ten companies to join AIM on the first day of trading on 19 June 1995 was Athelney Trust, the investment company that he manages. Athelney has moved to the Main Market but it is the only one of the first ten AIM companies that is still quoted.

Athelney initially raised money at 50p a share in July 1994 and the shares were traded on rule 4.2, a London Stock Exchange rule that enabled matched bargains trading in the shares of companies that did not have a stockmarket quotation. In fact, seven of the initial ten companies on AIM transferred from rule 4.2.

Athelney invests in smaller companies that have solid balance sheets, pay dividends and have good growth prospects. Athelney is small itself but its asset value has grown from just under £1m to more than £4m.

Athelney switched markets because of the preferential tax treatment of fully listed investment companies in areas such as capital gains tax. This means that the gains can be retained by the company.

Since moving to the Main Market on 24 September 2008, Athelney has increased its NAV from 135.8p a share to 231.7p a share at the end of April 2015, with AIM companies accounting for just under one-third of the portfolio. That is an impressive performance considering the timing of the move in the early days of the global financial collapse.

This asset growth underplays the performance. Since launch, 59.3p a share has been paid in dividends so the original investors have got more than their initial investment back.

Although Athelney does not purely invest in AIM companies this

Twenty years of AIM

performance does indicate that careful selection of AIM companies can lead to profitable investment. Robin Boyle looks at the individual companies and their characteristics rather than what market they are on.

Robin Boyle is a long-term supporter of small companies and he predicted that AIM could grow to more than 1,000 companies. However, he admits that “many with hindsight have been poor in terms of quality” and he believes that the nominated advisers and the companies they floated could have been better policed by the authorities.

These poor-quality companies have had some affect on the disappointing

performance of AIM as a whole. Another reason is investors chasing risk in areas such as mining and early-stage technology or other sectors that become fashionable for a period of time, leading to a flood of poor-quality copycat companies.

Robin Boyle does believe that the recent trend is for more solid companies, such as windows supplier Epwin, which he has invested in.

Progress

Online fashion retailer ASOS, even after its more recent share price decline, is still valued at more than the whole of AIM at the end of 1995, when there were 121 companies. New Europe Property Investments is valued at near to the end 1995 AIM value of £2.38bn.

In the past ten years a large numbers of companies have left AIM. At the end of May 2005, there were 1,197

AIM reaches its twentieth year in the middle of June. It has come a long way in that time.

companies on AIM and this number has fallen to below 1,100. In contrast, the value of AIM has increased from £35.8bn to £72.6bn. That means that the average value of an AIM company has more than doubled to £67.4m.

The longest-serving AIM company is Multimedia Corporation, which floated on 13 July 1995, within the first month of the junior market opening. This made it the eighteenth company to join and the third to raise new funds on joining. Multimedia has a patchy track record and it is a good example of how some AIM companies have reinvented themselves on one or more occasions. The company became a technology

investment company called Illuminator in 2001. Technology went out of fashion in the stockmarket and it switched its strategy to investment in assets in South Africa in 2006.

The company is currently known as Blackstar Group SE although it will change its name to Tiso Blackstar Group SE during June when it completes the reverse takeover of Times Media and 22.9% of South African investment company Kagiso Tiso. This deal should value the enlarged company at £210m, against £13m when it floated. The Malta registered company also has a quotation on AltX in South Africa and a number of other AIM companies also have quotations on other markets.

Main

Pharma company Skyepharma was the first AIM company to move to the Main Market. Skyepharma had used

There are 14 companies in the FTSE 250 index which were previously on AIM

HubInvest publishes AIM Journal www.hubinvest.com

June 201510

feature

finnCap www.finnCap.com

There are at least two other constituents that were on AIM in a previous guise. Both software supplier SSP and life insurer Just Retirement were acquired by private equity firms when they were on AIM and refloated on the Main Market a few years later. Many of these FTSE 250 companies have grown significantly since they floated on AIM.

Information security products supplier Zergo Holdings moved to the Main Market in 1998 and subsequently became Baltimore Technologies. Baltimore, which at one point was valued at £7bn, was in the FTSE 100

index for a period in 2000 and it is the only former AIM company to have achieved this, even if it was short lived. In August 2006, after Baltimore had moved back to AIM, Oryx acquired the company via a share swap equivalent to Baltimore's NAV, although some minority shareholders remained. The estimated value at the time of the bid was £28.4m.

Booker is worth more than £3bn so it could be the next former AIM company to approach a valuation where it could get into the FTSE 100 index. It will need to get to £4bn before that becomes a possibility, though.

Black & Edgington as a shell to gain its AIM quotation on 9 January 1996 and it moved to the Main Market in May of the same year.

In March 2003, Center Parcs was the 100th company to move from AIM to the Main Market. Most of the transfers happened between 1997 and 2000. In total, there have been 173 moves from AIM to the Main Market or other London Stock Exchange Markets, including the Specialist Fund Market.

Many of these companies subsequently returned to AIM. For example, security technology company Toad was the third company to move from AIM to the Main Market but it subsequently returned in April 2005 and is currently known as 21st Century Technology. Dean Corporation moved to the Main Market in November 1997 and subsequently returned to AIM as Lupus Capital in April 2006. Renamed as Tyman, it moved back to the Main Market in July 2013.

There are 14 companies in the FTSE 250 index that were previously on AIM – Big Yellow, Booker Group, Domino’s Pizza, Genus, Hansteen, Hiscox, IP Group, Lancashire, Melrose Industries, Petra Diamonds, Playtech, Redefine International (was Wichford), Synergy Healthcare and Unite. That is a wide spread of sectors, including services, property, retail, technology, engineering, healthcare, mining and financials.

Outlook

There appears to be greater positivity towards small and micro companies, with new funds being launched, but there has been a longer-term draining of investment funds from this area and it will take a lot more to recover the lost ground.

At the annual Quoted Companies Alliance conference, the fund managers on the final panel of the day were positive about the sector as a whole not just AIM companies. Leigh Himsworth of Fidelity said there is “a string of very good companies at the small end”, while

Daniel Nickols of Old Mutual stated that “there are still pricing anomalies”. Judith MacKenzie of Downing argued: “The list of potential new investments is as long as ever and it is one of the best periods I have been through.”

Although Robin Boyle is positive about AIM one thing he would like to see is a matched bargain facility set up for trading in small AIM companies. He believes that this could be a platform run by the company’s broker that would be available to all investors and every bargain would take place at the mid price. This could help to offset the large spreads of some AIM companies.

NAME ACTIVITY CAP (£M) WHERE ARE THEY NOW?

Athelney Trust Investment company 0.95 Currently fully listed and has a NAV of £4.6m. Brancote Mining 5.7 All-share bid by Meridian Gold worth $368m in August 2002. Country Gardens Garden centres 11.68 Wyevale Garden Centres paid £111m in November 2000.Dawson Holdings Newspapers distributor 22.41 Smiths News paid £17.3m for Dawson in 2011.Formscan IT and software services 4.73 Renamed Inspectron and left AIM on 11 August 2009. Gander Holdings Property investor 23.1 All-share bid by Orb Estates in August 1999 valued Gander at £60m.Lorien IT staffing provider 5.7 Bid from Contracting Solutions valued Lorien at £18.6m in 2007.Norcity II Property investor 0.74 Placed in liquidation at end of 1996 and dissolved in September 1997. Norhomes Property investor 1.27 Taken over in February 1997. Old English Pub Co Pubs operator 6 Greene King bid £59m for the company in September 2001.

FIRST TEN AIM COMPANIESMARKET

Over the past 10 years, the average value of AIM companies has more than doubled to £67.4m

HubInvest publishes AIM Journal www.hubinvest.com

HubInvest publishes AIM Journal www.hubinvest.com

June 2015 11

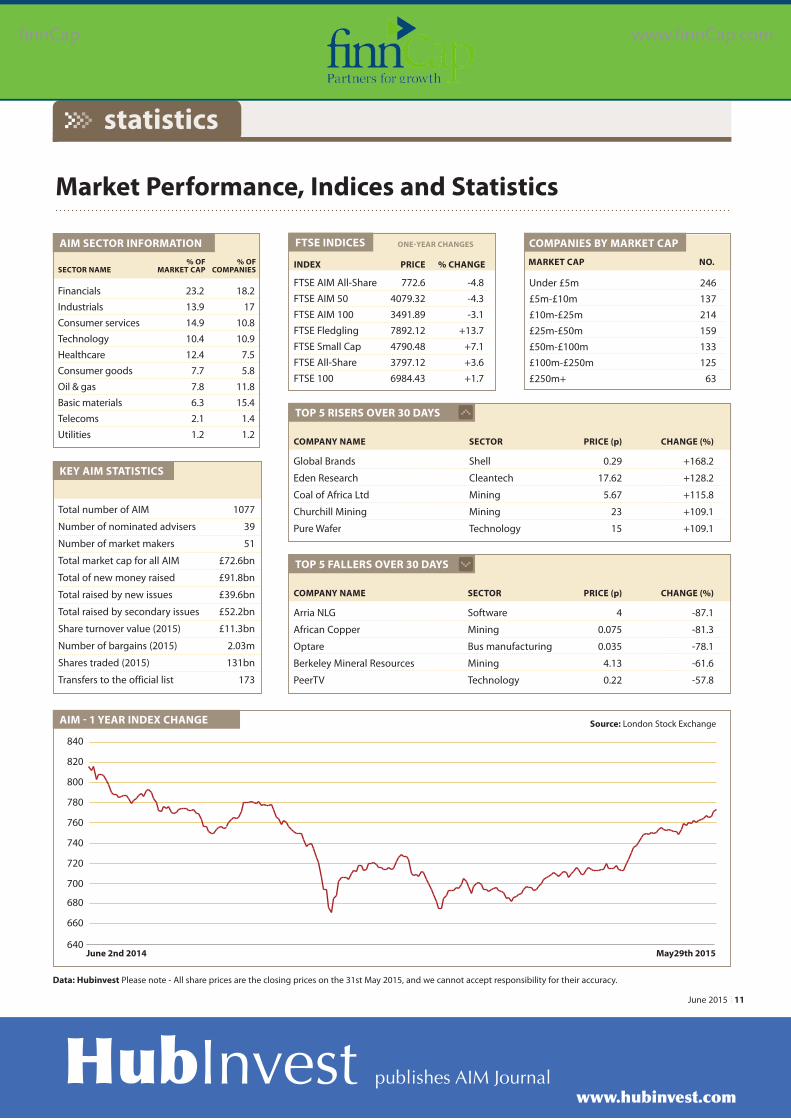

Financials 23.2 18.2Industrials 13.9 17Consumer services 14.9 10.8Technology 10.4 10.9Healthcare 12.4 7.5Consumer goods 7.7 5.8Oil & gas 7.8 11.8Basic materials 6.3 15.4Telecoms 2.1 1.4Utilities 1.2 1.2

Market Performance, Indices and Statistics

AIM SECTOR INFORMATION

4KEY AIM STATISTICS

Total number of AIM 1077

Number of nominated advisers 39

Number of market makers 51

Total market cap for all AIM £72.6bn

Total of new money raised £91.8bn

Total raised by new issues £39.6bn

Total raised by secondary issues £52.2bn

Share turnover value (2015) £11.3bn

Number of bargains (2015) 2.03m

Shares traded (2015) 131bn

Transfers to the official list 173

AIM - 1 YEAR INDEX CHANGE

TOP 5 RISERS OVER 30 DAYS

COMPANY NAME SECTOR PRICE (p) CHANGE (%)

Global Brands Shell 0.29 +168.2

Eden Research Cleantech 17.62 +128.2

Coal of Africa Ltd Mining 5.67 +115.8

Churchill Mining Mining 23 +109.1

Pure Wafer Technology 15 +109.1

% OF % OFSECTOR NAME MARKET CAP COMPANIES

FTSE INDICES

FTSE AIM All-Share 772.6 -4.8FTSE AIM 50 4079.32 -4.3FTSE AIM 100 3491.89 -3.1FTSE Fledgling 7892.12 +13.7FTSE Small Cap 4790.48 +7.1FTSE All-Share 3797.12 +3.6FTSE 100 6984.43 +1.7

ONE-YEAR CHANGES

INDEX PRICE % CHANGE

COMPANIES BY MARKET CAP

Under £5m£5m-£10m £10m-£25m £25m-£50m £50m-£100m £100m-£250m £250m+

246137214159133125

63

MARKET CAP NO.

Data: Hubinvest Please note - All share prices are the closing prices on the 31st May 2015, and we cannot accept responsibility for their accuracy.

Source: London Stock Exchange

statistics

TOP 5 FALLERS OVER 30 DAYS

COMPANY NAME SECTOR PRICE (p) CHANGE (%)

Arria NLG Software 4 -87.1

African Copper Mining 0.075 -81.3

Optare Bus manufacturing 0.035 -78.1

Berkeley Mineral Resources Mining 4.13 -61.6

PeerTV Technology 0.22 -57.8

June 2nd 2014 May29th 2015 640

660

680

700

720

740

760

780

800

820

840

finnCapwww.finnCap.com www.finnCap.com

HubInvest publishes AIM Journal www.hubinvest.com

June 201512

finnCap’s mission is to help ambitious companies grow and to be the leading independent broker to ambitious companies, focused on fuelling growth through long term partnerships. We will exceed client expectations through faultless execution, joined-up service and proactive thinking, all tailored to the needs of each individual client.

finnCap, whose chairman is Jon Moulton, is 95% employee-owned and is the top AIM broker by overall client numbers, according

to research compiled by financial website Morningstar. The broker is also the number one adviser in the technology, industrials and healthcare sectors, number three broker in the oil and gas sector and in the top five in the basic materials sector.

In 2013, finnCap commenced market making and launched fAN Club, a new offering aimed at providing specialist support to ambitious small private businesses seeking pre-IPO funding.

finnCap was presented with the

Best Research award at the 2012 AIM Awards, while finnCap’s corporate broking and sales trading teams have achieved Extel Top 10 rankings for three years running. finnCap is a sponsor of the AIM Awards, the plc Awards and the UK tech Awards.

In the year to April 2015, finnCap’s reported revenues were 4% higher at £16.1m, while pre-tax profit was £2.2m. The finnCap 40 Mining index, finnCap 40 E&P index and finnCap 40 Tech index were all launched during 2014.

PUBLISHED BY: Hubinvest Ltd,

ADDRESS: 1C Beaufort Road, Kingston-upon-Thames, Surrey. KT1 2TH.

TELEPHONE: 020 8549 4253

Mobile: 07849 669 572

EDITOR: Andrew Hore

DATA: Andrew Hore

PRODUCTION & DESIGN: David Piddington

sponsors

finnCap www.finnCap.com

SPONSORSHIP & [email protected] or telephone 020 8549 4253

Hubinvest Ltd uses due care and diligence in the preparation of the AIM Journal but is not responsible or liable for any mistakes, misprints or typographical errors. Information in the AIM Journal is for general information only and is not intended to be relied upon by individual readers in making or not making investment decisions. Appropriate independent advice should be sought. You acknowledge and agree that you bear responsibility for your own investment research and investment decisions, and that Hubinvest or its employees shall not be held liable by you or any others for any decision made or action taken by you or others based upon reliance on or use of information or materials obtained or accessed through use of the AIM Journal. Journalists and contributors to the AIM Journal, from time to time, may hold shares in the companies they write about. The views expressed by contributors, both professional and amateur, are not necessarily those of the publishers. All rights reserved, reproduction in whole or in part without written permission from the publisher is strictly prohibited.

finnCap www.finnCap.com