Joseph L. Petrelli Demotech, Inc. Columbus, Ohio.

25

Macquarie Capital (USA) Inc. Bermuda in Boston September 23, 2014 Biggest Challenges and Headwinds Facing the Industry Joseph L. Petrelli Demotech, Inc. Columbus, Ohio

-

Upload

collin-stanley -

Category

Documents

-

view

218 -

download

0

Transcript of Joseph L. Petrelli Demotech, Inc. Columbus, Ohio.

Macquarie Capital (USA) Inc.Bermuda in BostonSeptember 23, 2014

Biggest Challenges and Headwinds Facing the Industry

Joseph L. PetrelliDemotech, Inc.Columbus, Ohio

Demotech, Inc. will become the leading provider of innovative solutions to financial analysis issues by focusing our resources on niches presenting opportunity for corporate growth.

Mission Statement

2

Demotech, Inc. is a financial analysis firm specializing in evaluating the financial stability of regional and specialty insurers. Since 1985, Demotech has served the insurance industry by assigning accurate, reliable and proven Financial Stability Ratings® (FSRs) for Property & Casualty insurers and Title underwriters. FSRs are a leading indicator of financial stability, providing an objective baseline of the future solvency of an insurer.

Demotech's philosophy is to review and evaluate insurers based on their area of focus and execution of their business model rather than solely on financial size. This philosophy was the catalyst for the Demotech Company Classification System to stratify and categorize insurers by broad operational categories.

An Introduction to Demotech, Inc.

3

Florida and Bermuda

4

How interest yield environment Highly volatile economic conditions – next bubble? Labor participation rate at or near historic low Homeownership rate has crept up but tenuous Global government spending has done little to invigorate economies Capital on the sidelines is getting antsy Political unrest

National and Global Challenges

5

Florida Homeowners Marketshare 1995 Top 10

6

CompanyPremium Written

1995% of Total Premium Earned 1995

Loss Incurred 1995

DCC Incurred 1995

State Farm Fire and Casualty Co 504,823,127 30.0% 474,813,735 264,759,435 15,222,703

Allstate Insurance Company 279,704,546 16.6% 279,011,695 158,277,172 6,152,416

Nationwide Mutual Fire Insurance Co 78,843,286 4.7% 71,932,398 56,600,744 1,263,833

United Serv Automobile Assn 68,428,873 4.1% 64,296,071 74,122,137 6,408,625

LM Property and Casualty Ins. Co. 35,081,722 2.1% 34,917,162 5,286,781 1,643,212

Standard Fire Insurance Co 33,479,098 2.0% 29,227,231 14,666,200 705,347

Metropolitan Property & Cas Ins Co 30,481,823 1.8% 22,422,426 10,005,637 230,121

Automobile Ins Co of Hartford CT 28,679,065 1.7% 25,193,068 14,613,745 477,667

Liberty Mutual Fire Insurance 28,241,781 1.7% 26,064,423 13,196,523 352,134

Florida Farm Bureau General Ins Co 23,155,863 1.4% 20,599,639 15,695,697 62,447

Top 10 Total 1,110,919,184 65.9% 1,048,477,848 627,224,071 32,518,505

CompanyPremium Written

1995% of Total Premium Earned 1995 Loss Incurred 1995 DCC Incurred 1995

Federal Insurance Company 22,936,310 1.4% 21,942,547 10,313,733 965,904

Auto Owners Ins Co 22,742,136 1.3% 21,442,796 13,097,842 1,101,356

USAA Casualty Insurance Co 22,701,544 1.3% 20,682,321 15,908,821 847,372

Travelers Indemnity Company 22,321,060 1.3% 19,210,987 10,010,259 700,832

Government Employees Insurance Co 21,203,910 1.3% 21,450,590 12,710,184 810,993

Hartford Insurance Co of The Midwest 21,025,107 1.2% 19,548,122 10,912,815 439,786

State Farm General Insurance Co 18,895,207 1.1% 18,816,099 11,709,711 45,782

Florida Farm Bureau Casualty Ins Co 18,578,858 1.1% 16,320,282 10,380,361 255,991

Firemans Fund Insurance Co 17,663,992 1.0% 15,542,383 9,414,109 648,828

Phoenix Insurance Company 17,477,117 1.0% 16,812,633 10,355,727 329,131

11-20 Total 205,545,241 12.2% 191,768,760 114,813,562 6,145,975

Florida Homeowners Marketshare 1995 Top 11-20

7

CompanyPremium Written

2000% of Total Premium Earned 2000

Loss Incurred 2000

DCC Incurred 2000

State Farm Florida Insurance Co 583,296,400 20.1% 556,952,383 243,081,644 12,540,580

Castle Key Ins Co 312,825,277 10.8% 309,946,075 68,452,480 3,257,969

Clarendon National Insurance Co 158,386,180 5.4% 160,101,577 47,223,948 6,628,920

Clarendon Select Insurance Co 133,975,289 4.6% 133,805,350 34,145,237 4,809,255

United Serv Automobile Assn 104,630,465 3.6% 101,758,648 28,304,629 1,303,005

Nationwide Insurance Co of Florida 74,849,983 2.6% 19,338,331 6,162,260 184,418

First Floridian Auto & Home Ins Co 71,289,644 2.5% 67,653,591 26,774,549 1,228,290

Nationwide Mutual Fire Insurance Co 60,424,757 2.1% 108,096,734 36,432,481 1,637,400

Federal Insurance Company 57,490,362 2.0% 50,946,301 19,784,263 1,670,463

Florida Select Insurance Company 51,366,669 1.8% 47,787,116 14,798,820 -61,220

Top 10 Total 1,608,535,026 55.3% 1,556,386,106 525,160,311 33,199,080

Florida Homeowners Marketshare 2000 Top 10

8

CompanyPremium Written

2000% of Total

Premium Earned 2000

Loss Incurred 2000

DCC Incurred 2000

USAA Casualty Insurance Co 47,457,806 1.6% 44,679,716 10,307,426 305,708

Liberty Mutual Fire Insurance 47,210,221 1.6% 46,391,346 17,822,455 417,053

Tower Hill Preferred Ins Co 40,508,706 1.4% 38,990,205 8,181,954 359,340

Hartford Insurance Co of The Midwest 40,180,606 1.4% 39,315,969 11,914,716 479,763

Harbor Specialty Insurance Company 37,914,874 1.3% 37,485,431 9,590,473 593,285

LM Property and Casualty Ins. Co. 34,094,066 1.2% 35,259,815 11,360,405 219,014

American Superior Ins Co 33,911,175 1.2% 32,480,493 9,881,506 1,428,880

Southern Family Insurance Company 32,975,831 1.1% 34,397,903 11,465,152 -47,603

Qualsure Ins Corp 32,749,248 1.1% 11,716,264 2,390,118 35,246

Omega Insurance Company 32,637,708 1.1% 31,760,586 8,972,537 1,212,257

11-20 Total 379,640,241 13.1% 352,477,728 101,886,742 5,002,943

Florida Homeowners Marketshare 2000 Top 11-20

9

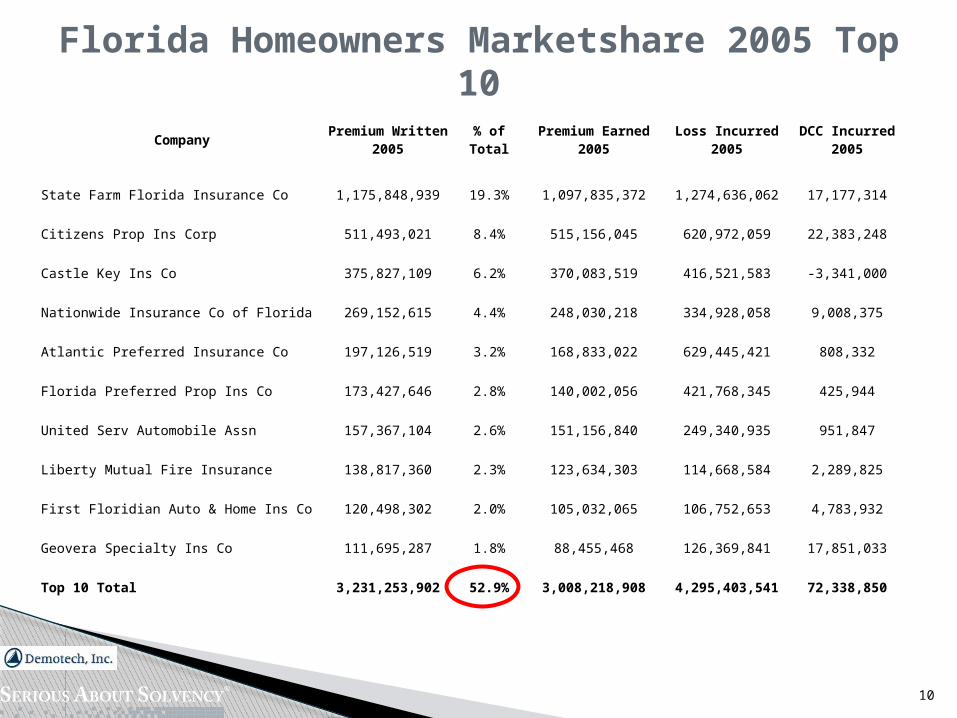

CompanyPremium Written

2005% of Total

Premium Earned 2005

Loss Incurred 2005DCC Incurred

2005

State Farm Florida Insurance Co 1,175,848,939 19.3% 1,097,835,372 1,274,636,062 17,177,314

Citizens Prop Ins Corp 511,493,021 8.4% 515,156,045 620,972,059 22,383,248

Castle Key Ins Co 375,827,109 6.2% 370,083,519 416,521,583 -3,341,000

Nationwide Insurance Co of Florida 269,152,615 4.4% 248,030,218 334,928,058 9,008,375

Atlantic Preferred Insurance Co 197,126,519 3.2% 168,833,022 629,445,421 808,332

Florida Preferred Prop Ins Co 173,427,646 2.8% 140,002,056 421,768,345 425,944

United Serv Automobile Assn 157,367,104 2.6% 151,156,840 249,340,935 951,847

Liberty Mutual Fire Insurance 138,817,360 2.3% 123,634,303 114,668,584 2,289,825

First Floridian Auto & Home Ins Co 120,498,302 2.0% 105,032,065 106,752,653 4,783,932

Geovera Specialty Ins Co 111,695,287 1.8% 88,455,468 126,369,841 17,851,033

Top 10 Total 3,231,253,902 52.9% 3,008,218,908 4,295,403,541 72,338,850

Florida Homeowners Marketshare 2005 Top 10

10

CompanyPremium Written

2005% of Total

Premium Earned 2005

Loss Incurred 2005DCC Incurred

2005

Federal Insurance Company 110,634,180 1.8% 101,749,514 35,361,442 1,209,338

United Prop & Cas Ins Co 104,978,215 1.7% 82,416,156 220,994,558 1,891,269

Castle Key Ind Co 99,239,939 1.6% 99,972,246 4,195,957 1,566,237

USAA Casualty Insurance Co 96,577,252 1.6% 91,172,848 127,892,595 939,464

Tower Hill Preferred Ins Co 96,293,790 1.6% 84,830,989 173,283,859 1,889,115

Clarendon Select Insurance Co 94,207,388 1.5% 111,729,976 355,631,346 -3,455,095

Gulfstream Prop & Cas Ins Co 93,418,769 1.5% 31,969,242 116,485,028 488,702

American Strategic Insurance Co 85,747,547 1.4% 87,791,515 47,538,023 1,640,063

Tower Hill Prime Insurance Company 83,639,919 1.4% 61,726,607 77,743,153 842,160

Universal Ins Co of NA 81,510,111 1.3% 43,798,173 71,190,689 662,906

11-20 Total 946,247,110 15.5% 797,157,266 1,230,316,650 7,674,159

Florida Homeowners Marketshare 2005 Top 11-20

11

CompanyPremium Written

2010% of Total

Premium Earned 2010

Loss Incurred 2010 DCC Incurred 2010

Citizens Prop Ins Corp 1,156,647,315 15.3% 965,072,025 436,092,444 28,888,968

State Farm Florida Insurance Co 980,590,404 13.0% 994,185,248 398,327,276 51,390,548

Universal Property & Casualty Ins 603,334,906 8.0% 557,600,093 159,003,198 14,302,318

St Johns Ins Co Inc 248,124,870 3.3% 259,300,270 71,657,092 6,145,175

United Serv Automobile Assn 221,075,163 2.9% 218,358,777 58,759,762 1,591,624

Florida Peninsula Ins Co 179,228,009 2.4% 180,108,919 58,874,976 7,761,861

Royal Palm Ins Co 147,859,244 2.0% 149,290,461 74,974,441 5,614,930

Federal Insurance Company 138,344,759 1.8% 139,172,213 31,680,608 749,432

American Home Assurance Company 137,667,154 1.8% 141,528,306 24,722,040 1,185,570

Castle Key Ins Co 135,302,913 1.8% 135,703,630 39,043,779 2,387,945

Top 10 Total 3,948,174,737 52.2% 3,740,319,942 1,353,135,616 120,018,371

Florida Homeowners Marketshare 2010 Top 10

12

CompanyPremium Written

2010% of Total

Premium Earned 2010

Loss Incurred 2010 DCC Incurred 2010

United Prop & Cas Ins Co 135,192,152 1.8% 134,463,241 46,259,337 6,461,956

Homewise Ins Co 128,332,164 1.7% 90,074,371 23,415,054 138,102

USAA Casualty Insurance Co 127,838,148 1.7% 127,895,239 27,750,032 1,719,382

Security First Ins Co 127,204,125 1.7% 112,681,814 34,011,914 3,040,452

Liberty Mutual Fire Insurance 123,102,196 1.6% 131,772,177 117,776,009 6,824,017

Tower Hill Prime Insurance Company 119,008,976 1.6% 103,263,952 34,211,394 3,140,489

Homeowners Choice Prop & Cas Ins Co 116,063,121 1.5% 106,084,544 28,458,504 2,736,765

Tower Hill Preferred Ins Co 111,877,610 1.5% 103,373,462 46,498,365 3,858,459

Universal Ins Co of NA 104,973,010 1.4% 110,553,936 57,284,084 5,755,389

Castle Key Ind Co 96,271,718 1.3% 64,979,805 15,262,167 1,557,612

11-20 Total 1,189,863,220 15.7% 1,085,142,541 430,926,860 35,232,623

Florida Homeowners Marketshare 2010 Top 11-20

13

Company Premium Written 2013 % of TotalPremium Earned

2013Loss Incurred 2013

DCC Incurred 2013

Citizens Property Ins Corp. 1,272,335,759 14.5% 1,445,423,995 388,109,714 116,650,999

Universal P&C Insurance Co. 684,379,171 7.8% 695,475,896 141,630,309 15,518,512

State Farm Florida Ins Co. 646,850,723 7.4% 696,037,459 136,310,936 16,653,060

Homeowners Choice P&C Ins Co. 311,550,298 3.6% 271,635,447 45,609,634 2,605,103

Florida Peninsula Insurance Co 310,352,524 3.5% 281,285,300 60,317,347 9,694,585

United Services Automobile 277,431,545 3.2% 264,931,482 57,644,426 1,923,173

United P&C Insurance Co. 263,178,022 3.0% 237,133,881 64,272,690 2,618,554

St. Johns Insurance Co. 255,851,881 2.9% 255,366,419 61,309,982 5,368,990

Federated National Ins Co. 220,639,653 2.5% 153,291,687 40,820,907 7,078,663

People's Trust Insurance Co. 203,009,802 2.3% 118,908,475 30,468,275 4,434,572

Top 10 Total 4,445,579,378 50.7% 4,419,490,041 1,026,494,220 182,546,211

Florida Homeowners Marketshare 2013 Top 10

14

CompanyPremium Written

2013% of Total

Premium Earned 2013

Loss Incurred 2013

DCC Incurred 2013

Security First Insurance Co. 184,487,897 2.1% 187,343,098 39,968,046 10,791,776

Tower Hill Prime Insurance Co. 179,732,931 2.1% 171,250,254 52,238,308 4,032,669

Federal Insurance Co. 162,155,667 1.8% 155,495,792 37,098,378 1,051,901

USAA Casualty Insurance Co. 147,191,648 1.7% 143,249,637 30,450,826 967,332

Amer Integrity Ins Co. of FL 141,915,923 1.6% 120,613,757 24,523,951 2,627,889

Castle Key Insurance Co. 134,209,691 1.5% 134,392,271 32,680,296 2,686,548

Tower Hill Preferred Ins Co. 132,209,409 1.5% 130,084,833 34,895,330 2,955,385

Tower Hill Select Insurance Co 121,368,000 1.4% 107,518,089 32,892,421 3,360,517

AIG Property Casualty Co. 121,279,021 1.4% 116,121,960 31,847,927 1,797,177

Heritage P&C Insurance Co. 120,622,904 1.4% 47,243,382 12,339,086 1,663,929

11-20 Total 1,445,173,091 16.5% 1,313,313,073 328,934,569 31,935,123

Florida Homeowners Marketshare 2013 Top 11-20

15

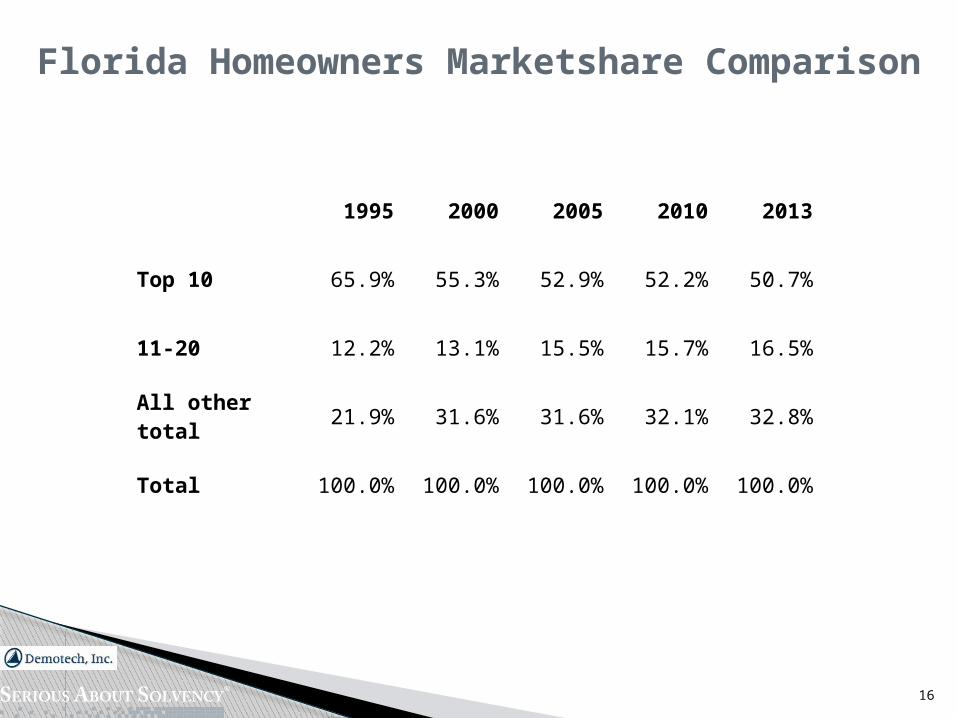

1995 2000 2005 2010 2013

Top 10 65.9% 55.3% 52.9% 52.2% 50.7%

11-20 12.2% 13.1% 15.5% 15.7% 16.5%

All other total 21.9% 31.6% 31.6% 32.1% 32.8%

Total 100.0% 100.0% 100.0% 100.0% 100.0%

Florida Homeowners Marketshare Comparison

16

The structure of Citizens Property Insurance Company makes it a fierce competitor for businesses despite the clearinghouse effort.

2014 estimated direct premium written of $2.42 billion Assessable

Private sector must compete with a huge competitor that is not bound by the terms, conditions and realities that the private sector must address. The competitor has the ability to assess to resolve under-funding and also purchases less reinsurance than a comparable private sector carrier.

Risks Facing Florida

17

Prior legislation mandated that any major structure for which a permit is applied on or after July 1, 2014, for new construction or substantial improvement, is not eligible for coverage by the corporation if the structure is seaward of the coastal construction control line or is within the Coastal Barrier Resources System.

House Bill 1089 changed the effective date for permits from July 1, 2014 to July 1, 2015.

Coastal Construction Control Line (Personal & Commercial Lines)

18

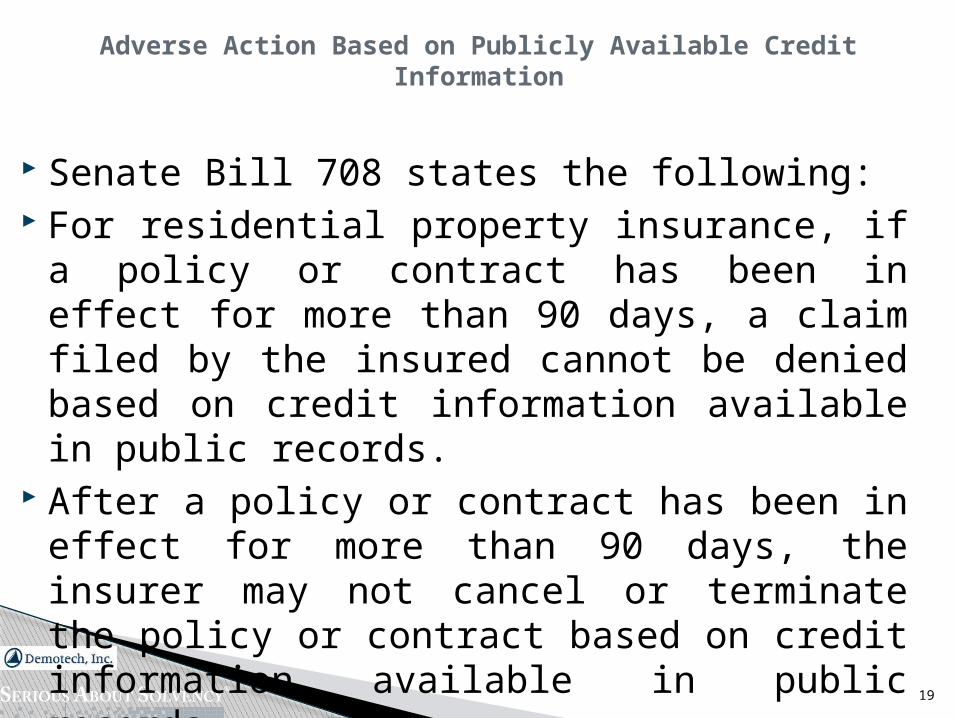

Senate Bill 708 states the following: For residential property insurance, if a policy or

contract has been in effect for more than 90 days, a claim filed by the insured cannot be denied based on credit information available in public records.

After a policy or contract has been in effect for more than 90 days, the insurer may not cancel or terminate the policy or contract based on credit information available in public records.

Adverse Action Based on Publicly Available Credit Information

19

Senate Bill 1672 provides that a mitigation form provided to the Corporation is not subject to independent verification or reinspection, absent material changes to the structure, if the form was signed by an authorized mitigation inspector and reviewed by and verified by a quality assurance program approved by the Corporation.

Citizens’ current practices will be updated to reflect any impact from this provision.

Exemption of Reinspection for Authorized Mitigation Inspectors

20

House Bill 1089 mandates that commercial residential condominiums shall be deemed ineligible for coverage if 50 percent or more of the units are rented more than eight times in a calendar year for a rental agreement period of less than 30 days.

This legislation requires changes to Commercial Residential Wind Only eligibility from the current transient standard of more than three (3) rentals per year for periods less than thirty (30) days, or held out to the public as a place regularly rented out to guests for periods of less than thirty (30) days, to the new standard described above. The legislation applies only to commercial residential condominiums.

Commercial Residential Wind Transient Occupancy Eligibility

21

Senate Bill 1672 requires changes to Citizens coastal account eligibility to state that the corporation shall cease offering new commercial residential policies providing multi-peril coverage for risks located in the wind-only eligible area and shall instead continue to offer commercial residential wind-only policies. This change applies only to new business and specifically states that the corporation may continue to renew existing policies in force as of July 1, 2014.

This change does not affect current eligibility for ex-wind policies written in the commercial lines account.

Commercial Residential Multi-Peril Eligibility

22

Rick Scott

Florida Governor, 2011-present

Political Risk

23

Charlie Crist

Florida Governor, 2007-2011

The Florida Homeowners insurance marketplace has been a laboratory for experimentation. The focus on Citizens and the Cat Fund as insurers sponsored by government has prevented some from viewing the finely toned tools that Florida focused carriers have developed:

◦ Home Hardening

◦ Wind Mitigation

◦ Enhanced catastrophe modeling

◦ Sophisticated underwriting

◦ Arcane pricing models at the catastrophe level

◦ Holistic business models such as People’s Trust Insurance Company

◦ Catastrophe response protocols

◦ Alternatives to reinsurance

◦ Emergence of Demotech as a viable rating alternative (FSU Study and 25 year track record)

24

25

Questions?