Gymnopus subnudus (Ellis:Pk.) Halling...3/7/2018 Gymnopus subnudus (Ellis:Pk.) Halling 1/2 …

Upload

duongkhanhCategory

view

218download

0

(Job Market Paper)

Anticipating Takeovers and their Payment Methods:A New Approach Using U.S. Acquisitions

Mohammad Irani ∗

First version : September 08, 2013

This version : November 10, 2015

ABSTRACT

This paper introduces a new approach for identifying the dates on which the market anticipates

both takeovers and their payment forms, prior to their announcement dates. This approach

predicts that the variance-covariance of the stock returns shifts when the market is informed by

signals about potential takeovers with synergistic gains. Using a sample of acquisitions between

U.S. public firms, I find that 86% of takeovers (62% of payment forms) are anticipated on

average nine (six) months in advance. This is much earlier than reported by previous studies

(two months). Moreover, when I add anticipation dates to the cross-sectional determinants of

payment methods, some of the preceding results change. The reason for this finding is that the

firm characteristics are not only related to the choice of payment method but also to the extent

to which takeovers are anticipated.

JEL classification: G14; G17; G34

Keywords: Mergers and acquisitions, payment method, prediction, structural breaks, variance,

covariance

∗The author is a PhD candidate in Finance at Stockholm Business School, Stockholm University, SE-10691 Stockholm, E-mail:[email protected], https://sites.google.com/site/movairani/. I would especially like tothank my supervisors Lars Norden and Rickard Sandberg for their helpful comments and numerous discussions.I am grateful for comments from Chris Adcock, Thomas Bates, Mariassunta Giannetti, Michael Halling, MartinHolmen, Catalin Starica, Johan Stennek, and Joakim Westerlund. I also thank seminar discussants and partici-pants at the second National PhD Workshop in Finance (Stockholm, 2013), the 3rd PhD Conference (StockholmUniversity, 2014), the 63rd Annual Meeting of the Midwest Finance Association (Orlando, 2014), the 23rd AnnualMeeting of the European Financial Management Association (Rome, 2014), Stockholm Business School (2015),and the Annual Meeting of Financial Management Association (Orlando, 2015). I am gratefully acknowledge theJan Wallander and Tom Hedelius foundation for research support. Any errors are my own.

1 Introduction

Jensen and Ruback (1983) and Martynova and Renneboog (2008) review takeover studies

and report that the target shareholders gain large abnormal returns while the returns to the

acquiring firms are negligible (or even negative). Travlos (1987) and Schwert (1996) also doc-

ument that gains in cash-financed offers exceed those in equity-financed and mixed-financed

offers. These differential returns induce investors to try to profit from anticipating takeovers

and their payment forms. The extant studies provide cross-sectional predictions, which provide

no guidance about anticipation dates.1 However, identifying those dates can have important

implications for our understanding of takeovers. Edmans, Goldstein, and Jiang (2012) explain

that stock prices of merging firms are endogenous as they are contaminated with takeover an-

ticipations. The dates can hence be used to remove the effect of takeover anticipation on prices,

which in turn can improve measurement of explanatory variables that use stock prices (e.g., To-

bin’s Q, price-earnings ratio, the discount rate, the acquisition stock returns, return variance,

covariance and correlation of merging stocks). The aim of this paper is to investigate whether

the market can anticipate mergers and acquisitions (M&As) and their payment methods prior

to their announcement dates. If so, when do those anticipations occur, and what are their

consequences for the choice of payment method in M&As?

Detecting the dates on which M&As are anticipated is a challenging task. Li and Prabhala

(2007) argue that M&As occur neither randomly nor unexpectedly, but takeover studies provide

indirect evidence regarding ex-ante predictability of M&As. Schwert (1996) shows that the

cumulative average abnormal returns (CAARs) to the target shareholders start to accumulate

42 trading days before the announcement date. He finds that there is a one-for-one relation

between this pre-announcement run-up and the total premium paid to the target shareholders

(the sum of run-up and post-announcement markup returns). Based on this result, Schwert

concludes that the target pre-announcement run-up is not affected by takeover anticipations,

otherwise it should not be added to the total premium paid by acquirers. However, Betton,

Eckbo, Thompson, and Thorburn (2014) illuminate that the relation is significantly smaller

after they account for the anticipation effect on the target run-up. Overall, findings of event

studies suggest that the market anticipates the target firms on average two months in advance,

but the acquirers are unpredictable because their CAARs do not show any trend in the pre-

announcement period.2 Furthermore, the event-study methodology focuses on just one of the

pair of firms at a time (either the target or the acquirer firm), thereby neglecting the additional

information contained in their joint return distribution (e.g., the covariance), which might be

useful for anticipating M&As. To deal with the unpredictability issue, this paper introduces a

new time-series and direct approach for identifying both the deal-anticipation (a pair of target

and acquirer firms) and payment-form-anticipation dates. This approach is based on analyzing

1Amihud, Lev, and Travlos (1990), Hasbrouck (1985), and Martin (1996), among others, employ a cross-sectional (binary discrimination) approach to examine investors’ predictions of acquirer and target merger can-didacy and their predictions of payment methods.

2Similarly, Smith and Kim (1994) find that the CAARs of the target firms in their sample start accruing 60days before the announcement day; however, the returns to the acquiring firms do not deviate from zero in thisperiod. I find comparable CAARs to theirs for the target and acquirer firms in my sample.

1

breaks in the variance-covariance structure of the joint target and acquirer daily return series.

Betton et al. (2014) suggest that M&As are anticipated when the market receives infor-

mative signals about potential takeovers with synergistic gains. Accordingly, when the market

anticipates a potential deal for the first time during the pre-announcement period, the merging

likelihood should increase significantly. Simultaneously, the market also discounts the expected

synergy value of that merger and incorporates it into the price process of the merging firms,

which in turn can affect the moments of the stocks’ returns (including levels, variances, co-

variance, etc.). The merging likelihood and the expected synergy are generally unobservable,

while shifts in the second-order moments can be estimated, allowing the anticipation dates to be

identified. Not every shift during the pre-announcement period, however, is related to takeover

anticipation. Restrictions are imposed on the sign of shifts in the variance-covariance structure

to disentangle consistent from inconsistent ones. A break date is interpreted as an anticipation

date if shifts around that date are consistent with the expected ones. The expected shift for

the anticipation of a deal is a significant decline in the target’s variance and any significant

changes in the rest of the moments (the acquirer’s variance, the acquirer-target covariance, or

the acquirer-target correlation) during the pre-announcement period. Anticipating the payment

form requires the correlation and (or) the covariance to shift upwards in the case of equity offers

and shift towards zero in the case of cash offers.

This paper contributes to the M&A literature by documenting anticipation shifts. Using

a sample of 125 completed acquisitions of U.S. public companies between 2003 and 2006, the

proposed approach finds that a takeover is anticipated on average 187 trading days before the

announcement date in 86% of the deals. The market anticipates the payment form in 62% of

the deals on average 123 trading days in advance. The anticipation dates that are identified are

much earlier than in previous event studies (e.g., Schwert, 1996) that find only the target (and

not the acquirer) firms to be anticipatable, and just two months prior to the announcement

date. The results suggest that breaks in the variance-covariance structure reveal significant

information about future M&As. Moreover, splitting the sample based on the offered payment

form (54 cash, 33 equity, and 38 mixed-payment deals) indicates that the market anticipates

the cash offers almost at the same time as it anticipates the deals themselves, but on average

there is a lag of 90 trading days in the equity and mixed subsamples. This evidence reveals

that the announcement of cash (equity and mixed) offers contains the least (most) unexpected

information for market investors. The market is less successful in anticipating mixed offers

because this requires the forecasting of an additional parameter, i.e. the portion of cash in the

total bid payment.

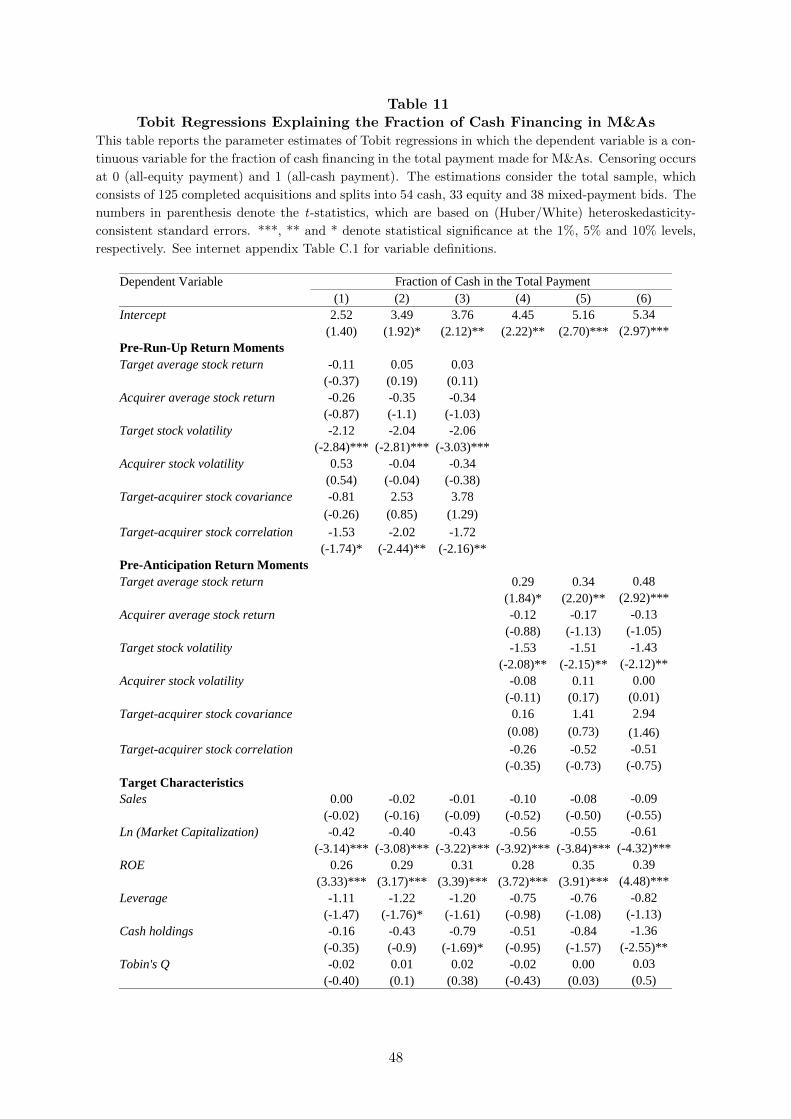

Additionally, controlling the deal-anticipation and payment-form-anticipation dates in this

paper provides new insights into the choice of payment method in M&As.3 The first and second-

order moments of the target and acquirer stock returns are used as cross-sectional predictors

in the payment-method regressions. Among them, the correlation plays an important role

in explaining the choice because it is a proxy for the relatedness of the target and acquirer

3Various competing hypotheses (the asymmetric information, tax consideration, capital structure, managerialcontrol, and behavioral motives, among others) explain this choice. See, for instance, Martin (1996) and Betton,Eckbo, and Thorburn (2008) and the references therein.

2

businesses. However, previous findings are mixed. On the one hand, Houston and Ryngaert

(1997), Officer (2004), and Bhagwat and Dam (2014) find that, if the stand-alone target and

acquirer stock prices co-move (are highly correlated), offering equity as the medium of payment

reduces the risk of an “unfair” merger, i.e., one in which the terms of the merger become

“unfair” to one party at the deal completion date. On the other hand, Faccio and Masulis

(2005), Rhodes-Kropf and Viswanathan (2004), and Aggarwal and Baxamusa (2013) argue

that the acquirer should pay in equity when buying uncorrelated target firms if those targets

have an informational disadvantage in that the acquirer’s stock is overvalued. Consistent with

the first of the above strands, I find that the greater the pre-merger correlation, the larger is

the fraction of the acquirer’s equity in the bid payment. However, adding new variables (i.e.

the deal-anticipation and payment-form-anticipation dates) to this regression changes some of

the previous results. Namely, the significance of the correlation disappears, the coefficient of

the average target return becomes significant, and the coefficient of the target volatility is

attenuated.

The above evidence suggests that assuming the unpredictability of M&As in payment-

method regressions may result in some endogeneity issues. First, the moments are usually

estimated from the pre-announcement period, but the anticipation of M&As can affect them.

The moments hence need to be estimated from a period in which the takeovers are totally unex-

pected (i.e. from the pre-anticipation segment); otherwise, they might be mismeasured, which

in turn may lead to a “measurement error” in the regressions. In fact, the evidence here indi-

cates that the pre-announcement target and acquirer variances are underestimated compared

with those from the pre-anticipation period. Similarly, the covariance and correlation are un-

derestimated in cash offers and overestimated in equity offers. Second, the target, acquirer, and

acquisition characteristics are used as predictors in those regressions. My findings demonstrate

that the anticipation variables are significantly correlated with some of those characteristics,

making them relevant for inclusion in the regressions. In other words, excluding the anticipation

variables may cause “omitted-variable bias”. My results indeed confirm that this is the case, at

least for my sample of takeovers.

I find robust support in the data for two theoretical factors (merging likelihood and expected

synergy) that generate the anticipation shifts. Using a measure for the takeover probability

(from Samuelson and Rosenthal, 1986), the merging likelihood of the target and the acquirer

firms become significant for the first time during the pre-announcement period after the detected

deal-anticipation dates, and then trend upwards. Moreover, the CAARs of both the target

and acquirer shares also show positive and significant trends after those anticipation dates,

suggesting that the market discounts part of the expected synergy of future M&As around

those dates. These findings confirm the assumptions in the theoretical model of Betton et al.

(2014), in which takeovers are anticipated when the market is informed by strong signals about

potential takeovers with synergistic gains.

I perform robustness tests in an attempt to rule out several alternative explanations of the

results: (1) If those anticipation shifts are caused by firm-specific events (and not anticipation

of M&As), then the portfolio theory would suggest that the variance-covariance structure of the

3

portfolios of merging firms should be stable due to the diversification effect. However, I also find

similar shifts in the variance-covariance structure of the portfolios, indicating that firm-specific

news is not the source of anticipation shifts in the individual bivariate return series. (2) If

some market-wide events during the sample period of this paper cause those anticipation shifts,

then similar shifts should also be observed in a benchmark sample (i.e., a random sample of

non-M&A firms). The anticipation shifts occur much less frequently and in a less expected way

in the benchmark sample than in the M&A sample, implying that the likely mechanism for the

later shifts is anticipation of takeovers and not market-wide events.4

I also apply cross-sectional analyses to determine the significant predictors that explain why

some takeovers are anticipated and some not, and why some are anticipated earlier than others.

I find that some of the cross-sectional characteristics of merging firms in the pre-anticipation

segment are significant in discriminating anticipated from unanticipated deals and in explain-

ing cross-sectional variation in the anticipation dates. While Meulbroek (1992) and Schwert

(1996) consider leakage of information by insiders as the main source of M&A anticipation, my

results propose another source: the existence of M&A anticipators in the market who use public

information that is available prior to the deal-anticipation date to predict likely M&As.

The rest of the paper is organized as follows: Section 2 reviews the merger arbitrage literature

to identify expected shifts that signal the anticipation of takeovers. Section 3 presents the

methodology and the anticipation hypotheses. Section 4 provides data and descriptive statistics.

Section 5 documents the anticipation results. Section 6 discusses the robustness of the results.

Section 7 reports the cross-sectional results, and finally Section 8 concludes.

2 Anticipation Shifts

According to the efficient market hypothesis (EMH), all relevant information should be

instantly incorporated into stock prices. Therefore, if the market anticipates a takeover and its

payment method, this information should be reflected in the price process of the target and the

acquirer stocks at the anticipation time. The merger arbitrage literature documents changes in

the second-order moments of stock returns after the announcement of takeovers. If the market

is efficient, one can expect to observe similar changes during the pre-announcement period when

a deal and (or) its payment form are anticipated.

The expected shifts that would indicate the anticipation of the deal and payment form can be

summarized as follows: a significant decline in the target volatility indicates the anticipation of

the target firm while any significant shift in the acquirer’s volatility would imply the anticipation

of the acquirer firm. The existence of a significant decline in the target’s variance and of any

significant changes in the rest of the moments (the acquirer’s variance, the acquirer-target

covariance, or the acquirer-target correlation) during the pre-announcement period signal the

anticipation of the takeover. If the market anticipates equity offers, the covariance should

4The anticipation shifts exist regardless of the use of alternative approaches. The alternatives include thefollowing: three univariate tests as opposed to one multivariate test for detecting breaks in the variance-covariancestructure, the use of raw instead of winsorized returns series, and the employment of returns from the pre-announcement period rather than from both the pre- and post-announcement periods in the above tests.

4

increase and (or) the correlation should become one. In the case of cash offers, the covariance

and (or) the correlation should converge to zero. A mixed-payment offer will follow the rule for

equity (cash) offers if the equity (cash) is the dominant portion in the total bid payment.

2.1 Target Return Volatility

Bhagat, Brickley, and Loewenstein (1987) report an anomaly in the relation between risk and

return in targets’ stocks during the post-announcement period. They find significant declines

in both the beta and the sample unconditional volatility of the target of a cash bid, but rising

returns. Bhagat et al. (1987) propose that the price of a target share during that period is the

sum of the value of common stock and the value of a put option. The target shareholders have

the option to sell their shares to the acquirer firm in the post-announcement period. Bhagat et

al. (1987) then show via option theory that a portfolio containing a stock and a put option has

a lower standard deviation than the stock itself. This conjecture explains the observed decline

in the target’s volatility.

Hutson and Kearney (2001, 2005) extend this analysis to the targets of both cash and equity

offers and to completed and failed ones. They document that, regardless of the payment form

and the final outcome of the pending bid-offer, the conditional volatility of the target’s shares

declines significantly after the bid announcement. The greatest (smallest) decline is in the

cash (equity) subsample. Hutson and Kearney (2001) claim that this observation is due to a

fundamental change in the price formation process, i.e. traders’ opinions about the value of the

target stock converge during the post-announcement period. Overall, the decline in the target

volatility regardless of the payment method and the offer outcome indicates an increase in the

likelihood of a firm being the target of an acquisition.

2.2 Acquirer Return Volatility

Various competing hypotheses have been developed about the post-acquisition (i.e., long-

run) risk profile of the acquirers. First, the “portfolio effect” hypothesis predicts that the risk of

the acquiring firm in this period is nothing more than the risk of a market-value-weighted port-

folio formed from the shares of the two firms in the pre-announcement period (e.g., Langetieg,

Haugen, and Wichern, 1980), thereby suggesting a decline in its risk. Second, the “leverage

effect” hypothesis expects acquisitions that worsen the leverage (debt-to-equity ratio) of the

acquirer firm to induce an increase in the risk of the consolidated firm (Hamada, 1972). Third,

the “integration risk” hypothesis conjectures an increase in the risk of the consolidated firm

if the acquirer’s management is inefficient in merging the two firms into a single corporation

(Bharath and Wu, 2006). Fourth, the “merger wave effect” hypothesis posits that industry

shocks trigger inter-industry acquisitions (Mitchell and Mulherin, 1996; Harford, 2005). Since

completed inter-industry acquisitions have stabilizing effects, this hypothesis predicts a decline

in the risk of the consolidated firm. Finally, the “synergy effect” hypothesis predicts a decline

in the acquirer’s risk since the synergistic gains increase the value of the consolidated firm due

to the following reasons: cost reductions due to economies of scale, economies of scope, more di-

5

verse corporate skills, more efficient redeployment of the combined assets, and enhanced market

power, among others (e.g., Bradley, Desai, and Kim, 1988; Chatterjee and Lubatkin, 1990).

Given the opposing predictions, the net impact of acquisitions on the risk of the acquirer

firm is an empirical question. The empirical findings are indeed mixed. For example, Langetieg

et al. (1980) show an increase in various unconditional risk measures of the acquirers in the

post-acquisition period. They relate this result to aggressive management of the acquirer firms

together with an increase in their leverage. Geppert and Kamerschen (2008) find a statistically

greater implied volatility of the acquirer firms than the value predicted by the portfolio hypoth-

esis in the post-announcement period. They argue that the integration risk and uncertainty

about potential efficiency gains explain this result. However, after controlling for the system-

atic risk of target firms, Chatterjee et al. (1990) find the acquirers’ systematic risk to decline

over both short and long horizons after the acquisitions due to synergistic gains. Hutson and

Kearney (2005) find that the average unconditional volatility of the acquiring firms declines

significantly after the announcements, but that the reduction is only significant in cash offers.

Declining shifts are more consistent with the proposed anticipation mechanism in which a

takeover is anticipated if the market perceives a synergistic gain from the merger. A decline in

the acquirer risk during the pre-announcement period hence suggests that the diversification and

synergy effects dominate the leverage and integration impacts. Overall, the opposing hypotheses

and mixed evidence predict changes in the acquirer risk in different directions. Therefore, any

change in the pre-announcement period is interpreted in this paper as an indicator of the

anticipation of the acquirer firm.

2.3 Acquirer-Target Return Correlation

Houston et al. (1997), Officer (2004), and Bhagwat et al. (2014) report a positive relation

between the fraction of the acquirer’s equity in the bid payment and the pre-announcement

correlation. Bhagwat et al. (2014) propose that the risk of overpayment is reduced by an equity

offer if the acquirer and target returns are highly correlated but the risk increases with weak

correlation. This result suggests that shifts in the correlation can be used to anticipate the

payment method in M&As.

Subramanian (2004) constructs a theoretical model and provides empirical evidence in which

the announcement of an equity offer causes the correlation to shift towards perfect correlation.

He argues that if the market assigns a high likelihood to the success of a merger attempt, the two

stock price processes must be perfectly correlated after the bid announcement since the acquirer

offers a constant equity-exchange ratio to acquire each share of the target firm in an equity

bid. This paper extends the work by Subramanian (2004) by documenting the behavior of the

correlation around the announcements of cash and mixed-payment offers. When the likelihood

of the success of a cash offer is high, the target volatility should drop significantly due to the

offered bid premium. In this case, the two return processes will become uncorrelated. Moreover,

the proportion of cash in a mixed payment will determine whether the correlation should shift

towards zero or one. If the cash portion is dominant, the above argument predicts that the

correlation should converge to zero. Otherwise, it should shift towards perfect correlation.

6

2.4 Acquirer-Target Return Covariance

The behavior of the acquirer-target return covariance around the announcement of cash,

equity and mixed-payment offers has not been studied previously. This paper does so for the

first time. Both the covariance and the correlation measure the degree of covariation between

the target and acquirer returns. However, standardization via individual volatilities in the

denominator of the correlation can mean that useful variations necessary for anticipating the

payment form are discarded. It is likely that the correlation will be stable, while the covariance

will shift in response to the market’s anticipation of the payment form. This suggests that shifts

in the covariance can be used along with shifts in the correlation to detect the payment-form-

anticipation dates. Overall, the expected shifts in the correlation apply to the covariance as

well.

3 Methodology and Anticipation Hypotheses

First, each return series is prepared (i.e., adjusted for outliers, and for breaks in the mean,

and then demeaned) before the structural break test is applied to investigate whether a deal and

its payment form are anticipated or not. Second, if the test detects break(s) in the variance-

covariance structure of a bivariate return series, the significance of shifts in its second-order

moments are examined individually around each break date. Finally, an inference about the

existence of anticipation dates is made based on the signs of the significant shifts.

3.1 Data Preparation

The daily log returns (henceforth, the returns) of the acquirer and target stocks are used in

all the tests in this paper and are computed in the following way:

ri,n,t = ln

(Pi,n,t

Pi,n,t−1

), (1)

where i =Acq, Trg ; n is the index for the deals in the sample; t=(-379, . . . , 0, 1, . . . , C ) is

the daily subscript; rAcq,n,t and rTrg,n,t represent the realized returns to acquirer and target

shareholders involved in deal n on day t ; and PAcq,n,t and PTrg,n,t are their adjusted closing

prices on day t. Similarly to in Schwert (1996), the sample observation period for each of the

target and acquirer return series starts 379 days prior to the announcement date (t = 0) and

ends at the delisting date of the target’s shares, which is C days after the announcement.5 The

pre (post)-announcement period runs from Day -379 (Day 0) to Day -1 (Day C ).

The largest absolute returns of each series are identified and winsorized at 99%. The mean

of the returns should be stable during the whole observation period in order that breaks in

the second-order moments can be identified. The structural breaks methodology developed by

5The cross-sectional regressions (e.g., Amihud et al., 1990; Hasbrouck, 1985; Martin, 1996) use predictorsfrom the last year to discriminate merging from non-merging firms. Starting the sample observation period atDay -379 (one and a half years before the announcement day) here corresponds to the idea in those papers thatthe relevant information about future M&As can be revealed one year in advance.

7

Bai and Perron (1998, 2003, 2006) detects shifts in the mean of each return series, each series

then being adjusted for the detected shifts. See the “Data Preparation” section in the internet

appendix for further details about the adjustment of outliers and the structural break test. All

tests used in this paper assume the sample mean of each return series to be zero. The following

transformation is therefore applied to each series:

ri,n,t = ri,n,t − ri,n,t, (2)

where ri,n,t =1

380 + C

C∑t=−379

ri,n,t is the sample mean of the observed return series and ri,n,t is

the mean-adjusted return series.

3.2 Detecting Breaks in the Variance-Covariance Structure

I use a cumulative sum (CUSUM) type test proposed by Aue, Hormann, Horvath, and

Reimherr (2009). This test is suitable since it does not impose any normality or parametric

assumptions, which are usually assumed in parametric and cross-sectional tests. However, it re-

quires the finiteness of the fourth sample moment of the bivariate series. The 99% winsorization

is thus necessary and used to fulfill this requirement. The appealing feature of CUSUM-type

tests is their ability to use a non-parametric HAC (heteroskedasticity- and autocorrelation-

consistent) type estimator to capture the dependence structure in the data. As recommended

by Aue et al. (2009), the Bartlett estimator is used as a proxy for the asymptotic covariance

matrix in the testing procedure.6,7

Since shifts in the variance-covariance structure can occur in both the pre- and post-

announcement periods, I use the multiple break detection version of Aue et al. (2009), which is

based on the binary segmentation approach. When this test detects a significant break date, it

is reapplied separately across the two new segments that are obtained from splitting the data

into two subsamples around that break date. This approach ends when the test can no longer

detect any significant breaks in the new segments.

Henceforth, the identity subscript of the deals is excluded from the notation for simplicity,

but the following procedure is applied for each deal in the sample. Let (y−379, . . . , y0, . . . , yC)

be a sequence of two-dimensional random return vectors over the sample observation period of

a deal. For example,

y−379 =

(rAcq,−379

rTrg,−379

)(3)

is the bivariate vector of mean-adjusted realized returns for the target and acquirer shareholders

6Berkes, Horvath, Kokoszka, and Shao (2005) show that the Bartlett estimator to be a consistent estimatorof the asymptotic covariance matrix since it converges almost surely.

7The data-dependent approach of Newey and West (1994) is also applied to determine an optimal truncationlag in the Bartlett estimator. Rodrigues and Rubia (2007) show this truncation lag to be able to improve thefinite-sample performance of CUSUM-type tests.

8

on Day -379.

Cov(y−379) =

(σ2Acq,−379

σ2AcgTrg,−379 σ2Trg,−379

)=

(r2Acq,−379

rAcq,−379.rTrg,−379 r2Trg,−379

)(4)

is the realized variance-covariance matrix of the bivariate returns on Day -379, which contains

the realized target and acquirer variances and their realized covariance on that date. The test

statistic of Aue et al. (2009, p. 4050) detects structural breaks in the variance-covariance

structure of a bivariate return process by examining the following hypotheses:

H0 : Cov(y−379) = . . . = Cov(yC) (5)

HA : Cov(y−379) = . . . = Cov(yK1) 6= Cov(yK1+1) = . . . = Cov(yK2)

6= . . . = . . . 6= Cov(yKm+1) = . . . = Cov(yC). (6)

While the null hypothesis indicates the constancy of the variance-covariance structure of a

bivariate return series in the sample observation period, the alternative allows several change-

points (m ≥ 1). The test itself identifies the unknown number of change-points (m) and their

unknown locations (-379<K1<. . .<Km<C ). I do not impose any restrictions on these unknown

parameters so as to capture all informational events of each bivariate series.

The merger arbitrage literature usually compares the cross-sectional average pre- and post-

announcement second-order moments by assuming the announcement day to be the only break

date (e.g., Bhagat et al., 1987; Hutson and Kearney, 2001; Subramanian, 2004). To the best of

my knowledge, Jayaraman, Mandelker, and Shastri (1991) is the only study that documents pre-

dictability for the target firms by assuming three uniform break dates in their implied volatility

during the pre-announcement period. Gelman and Wilfling (2009) apply a Markov-switching

GARCH model to detect shifts in the conditional volatility of target stocks during the post-

announcement period. However, the use here of the test provided by Aue et al. (2009) extends

the above studies because it relaxes any assumptions about the number and location of break

dates.

3.3 Tests for Equality of Second-Order Moments around the Break Dates

Since Aue et al.’s (2009) test is a joint test, it does not identify which of the second-

order moments changes significantly after each break date, knowledge of which is necessary in

order to examine the anticipation hypotheses. Therefore, I perform tests for the equality of

those moments to determine significant shifts after each break. Since the sample second-order

moments are locally stationary in each segment, I use them as estimates for the population

moments across the detected segments. Suppose, e.g., that the joint test finds one break in the

variance-covariance structure at time K1. Then the estimates of the target’s variance in the

9

pre- and post-break segments are

σ2Trg,pre =1

(379 +K1)

K1∑t=−379

r2Trg,t (7)

σ2Trg,post =1

(C −K1)

C∑t=K1+1

r2Trg,t. (8)

Other sample second-order moments (i.e., acquirer variance, covariance and correlation) in

the pre- and post-break segments are estimated in a similar way.

The modified version of Levene’s (1960) F-test, proposed by Brown and Forsythe (1974),

examines whether the sample variance is the same across two adjacent segments. This test

is proper since it uses the median instead of the mean in computing the absolute deviations,

and thereby robust against non-normality.8 For example, this test examines whether the target

variance is constant around a break date:

H0 : σ2Trg,pre = σ2Trg,post (9)

HA : σ2Trg,pre 6= σ2Trg,post. (10)

The F-statistic is always positive, but the covariance can be negative. Thus, the absolute

value of the covariance is used here for computing the common F-test for the equality of co-

variances across two adjacent segments. However, using absolute values can lead to a more

conservative test in detecting heterogeneity when the sign of the covariance is different in the

two segments. The number of significant changes might hence be underestimated if the absolute

values are small.

Jennrich’s (1970) test examines the equality of sample correlations across two adjacent

segments:

H0 : ρAcqTrg,pre = ρAcqTrg,post (11)

HA : ρAcqTrg,pre 6= ρAcqTrg,post, (12)

where ρAcqTrg,pre and ρAcqTrg,post are the sample acquirer-target return correlation in the pre-

and post-break segments.

3.4 Anticipation Hypotheses

Previous studies document that information about the pair of firms (e.g., the size of the

target relative to the size of the acquirer) explains the choice of payment method in M&As.

Thus, first, the deal anticipation should be examined and then the payment-form anticipation.

If the deal is unanticipated, the procedure for detecting the payment-form-anticipation date is

abandoned. Moreover, the payment form can be anticipated either at the deal-anticipation date

or at a later date during the pre-announcement period.

8Lim and Loh (1996) compare seven existent tests for the equality of variances in a simulation exercise andfind that the modified Levene test is the most powerful.

10

The following conjectures help to interpret the results of the structural break test, and in

turn to detect the anticipation dates. First, the existence of multiple consistent breaks will

indicate that expectations about the potential deal are updated sequentially. Such breaks will

occur due to the release of new information about the deal, the reinterpretation of existing

information, and (or) the reassessment of the perceived synergy of the deal and its division

between the target and acquirer shareholders. Second, assuming a threshold of 50% shows

whether a mixed offer is anticipated or not. Thus, if more than 50% of a deal value is paid in

cash (equity), then cash (equity) is the dominant payment form in the mixed-payment offer.

Table 1 summarizes possible outcomes of the test (by Aue et al., 2009), which are inferred

to identify break date(s) consistent with the deal and payment-form-anticipation hypotheses.

First, if there is no break during the pre-announcement period of a bivariate (target-acquirer)

return series, then the deal and its payment form are unanticipated. Furthermore, non-M&A

reasons can increase the volatility of the target shares. Thus, any increasing shift in this moment

will lead to a break date not being recognized as a deal and payment-form-anticipation date,

regardless of the observation of expected shifts in other moments (see, e.g., outcomes 2 and 5

in Table 1).

Insert Table 1 here

Second, suppose that the test detects only one break date (K1). If at least one of the

second-order moments (other than the target variance) changes significantly after this break,

then K1 is the deal-anticipation date (outcomes 3 and 4). A decline in the target variance may

only indicate that the market anticipates the target firm and not the deal (which is a pair of

target and acquirer firms). Therefore, in addition to a declining target variance, the existence

of at least one significant shift in another moment is required for a break to be considered as

the deal-anticipation date.

The deal-anticipation date is the first candidate for assessing the payment-form-anticipation

hypothesis. If at least one of the covariance and the correlation shifts significantly towards its

expected level after this date, then K1 is also the payment-form-anticipation date. An expected

shift would be a rise in the case of equity offers, or a shift towards zero in the case of cash

offers. A mixed offer would follow the rule for an equity (cash) offer if equity (cash) made up

the dominant portion of the total payment.

Finally, let us assume for simplicity a two-break case (K1 and K2), though this can easily

be generalized to a case with more than two breaks. In the multiple break case, the procedure

starts from the closest break to the announcement date (K2) since it captures the most recent

expectations of the market about the M&A activity of the pair of firms. If there are any

inconsistent shifts (e.g., increasing target variance), then the deal and its payment form are

inferred to be unanticipated (outcomes 5 and 6). However, if K2 contains consistent shifts,

then the anticipation procedure considers the farther break (K1) as well. If there are consistent

break(s) around this date, then the market starts to anticipate the deal and (or) its payment

form from the date of the distant break, i.e., K1 (outcomes 9 and 10), otherwise the deal

and (or) its payment form are anticipated at K2 (outcomes 7 and 8). Moreover, a reversal in

11

the co-movement moments across breaks can cause the deal-anticipation and payment-form-

anticipation dates to differ, and can even cause the payment form to be unanticipated (if an

inconsistent break is detected at the closest break date). If the dates are different, then the deal

is anticipated (K1) earlier than the payment form (K2), e.g., outcomes 11 and 12.

The choice of payment method at the acquisition time can differ from the anticipated one. If

so, then the payment form is found to be unanticipated (anticipated incorrectly). For instance,

according to possible outcomes 3 and 9 (7 and 12), the market anticipates at date K1 (K2)

that the acquirer will use its own shares to finance the acquisition, but if instead it uses cash at

the acquisition time, then the payment form will have been unanticipated. This example shows

cases in which the deal is anticipated but not its payment form. Section 6.1 below provides an

example of how the above procedures are performed so as to identify the anticipation dates.

4 Data and Descriptive Statistics

4.1 Sample Selection

I sample takeovers from the Bureau Van Dijk Zephyr database using the transaction form

of “merger” or “acquisition”. The sample consists of all completed acquisitions between U.S.

publicly listed target and acquirer firms. The sample period is from June 2003 to June 2006,

which corresponds to the sixth M&A wave in which both the equity and the takeover markets

are stable (Martinova and Renneboog, 2008). Macroeconomic and industry factors are less

likely to generate breaks in this period than is the release of information about firms (e.g.,

takeover transactions). This definition leads to 1647 deals being identified. Table 2 summarizes

how this sample is then reduced based on the following filters.

Insert Table 2 here

I focus on the sample of deals in which the following hold: (i) An acquirer gains entire

control of a target firm by acquiring 100% of the target shares in one takeover transaction. The

most relevant cases in which to verify the anticipation mechanism are those in which the ex-ante

merging likelihood is trivial. I thus exclude acquisitions in which an acquirer has acquired some

stake in the target firm before the current bid, because previous bids (of even a minority or

“toehold” stake) can raise the likelihood to a significant level. (ii) The method of payment is all-

cash, all-equity or a mixture of cash and equity payments. (iii) A bid offer takes between 19 and

253 trading days from its first announcement date to complete. According to the William Act

of 1968, only bid offers for subsidiaries of U.S. public targets or private targets can be completed

in a shorter period (Officer, 2004; Bhagwat and Dam, 2014). The daily prices (and thus the

returns) are usually unobservable for these firms, and so the anticipation mechanism would

be unverifiable for these types of deals. (iv) The deal value exceeds $50 million. (v) Neither

the acquirer nor the target firm is a bank since the latter are highly leveraged and subject to

different regulations. The noise that would be added to the estimation of the cross-sectional

regressions due to their different characteristics is the primary reason for ignoring banks. (vi)

An acquirer has only one bid record in the sample period. If an acquirer has multiple bids, a

12

consistent break would not be identifiable as the anticipation break of a specific bid, as it might

be related to another bid made by that acquirer. (vii) The target has a stock price exceeding

$2 on Day -42. Schwert (1996) argues that the returns on low-priced stocks could be imprecise

as they are more heavily exposed to frictions in the market microstructure. (viii) Both firms

have more than 120 adjusted daily-closed stock prices during the pre-announcement period in

Thomson Financial DataStream.

The final sample contains 125 deals with enough return data, and splits into 54 all-cash, 32

all-equity and 38 mixed-payment deals. This sample size might be considered small compared

to the sample of the usual takeover study. The reason is that more restrictive filters are used

here to construct the sample, which is necessary for testing the anticipation hypotheses. For

example, filter (i), requiring bids for a 100% stake of the target, reduces the sample significantly

by 1120 deals, and other studies do not impose this requirement.

The target and acquirer firms’ accounting and deal information are retrieved from Thom-

son Financial DataStream and the Bureau Van Dijk Zephyr database. The internet appendix

provides further details of the data analysis, including the definition of the variables for the

cross-sectional analysis, descriptive statistics of the deal, target and acquirer characteristics,

the sample higher-order moments before and after winsorizing the return series, and the results

for the breaks in the mean returns.

4.2 Summarized Statistics of Sample Second-Order Moments

Table 3 provides descriptive statistics for the sample second-order moments of the acquirer

and target returns in the pre- and post-announcement periods. I use the sample moments

and not the realized moments in order to compare the results with those of previous studies.

The cross-sectional average (median) annual target volatility for the full sample declines by

a highly significant 44.1% (47.1%), from 0.483 (0.463) to 0.27 (0.245), from the pre- to the

post-announcement periods.9 This average decline is similar to Hutson and Kearney’s (2001)

report of an average decline of 46% after the bid announcement. While the analysis of variance

(ANOVA) indicates that the average target volatility is comparable across payment subsamples

during the pre-announcement period, its large F-value (16.28) for the post-announcement period

suggests the opposite. Consistent with Hutson and Kearney (2001), the largest (smallest) risk

reduction is seen for the targets of cash (equity) offers. Overall, the announcement of a takeover

significantly reduces the target’s volatility regardless of the payment method offered. This is

consistent with that part of the deal-anticipation hypothesis that partially anticipates a takeover

due to a significant decline in this moment.

Insert Table 3 here

The decline in the average acquirer volatility is significant at the 1% level. It changes from

0.384 to 0.318 between the pre- and post-announcement periods. Again, this average decline

9I will report the volatilities (and not the variances) throughout the paper for comparability of the resultswith previous literature, and annualize all moments (over 252 trading days) to match them with the annualcross-sectional data used in the regressions.

13

(17.4%) is similar to the 21% drop reported in Hutson and Kearney (2005). This average

reduction in the risk of acquirers after bid announcements is less than that found for the targets

(44.1%) since the above-mentioned opposing factors affect the acquirer’s volatility. Moreover,

the average reduction is significant across all payment subsamples, ranging from 15% to 19%.

Overall, the synergy and diversification effects dominate the leverage and integration effects in

this sample, such that the bid announcements lead to a decrease in the acquirers’ volatility.

The difference between the average post- and pre-announcement covariance is insignificant,

which is surprising at first glance. However, the unreported results of the individual equality

tests indicate that the covariance changes significantly in 110 out of 125 (88% of) deals after the

announcement. The decreasing and increasing changes cancel each other out in this case, causing

the average change to be insignificant. Furthermore, the significant ANOVA results (with F-

values of 5.72 and 22.93) imply that both the average pre- and post-announcement covariance

differ significantly across payment subsamples. The firm-pairs that are more linearly dependent

during the pre-announcement period use more equity as the medium of exchange. Moreover,

consistent with the payment-form-anticipation hypothesis, announcing an equity (cash) offer

significantly raises (declines) the average covariance by 65.7% (99.1%), from 0.066 (0.029) to

0.11 (0.0003), from the pre- to the post-announcement periods. Overall, the covariance changes

significantly after the bid announcement, dependent on the offered payment method.

Consistent with Bhagwat et al. (2014), I find that the more correlated is the pair of firms

in the pre-announcement period, the more shares are used by the acquirer to finance the M&A

(F-value of 8.32). Announcements of equity offers significantly increase the average correlation

from 0.305 to 0.685. This result supports the evidence in Subramanian (2004) in which it is

proposed that the correlation of firm-pairs involved in equity deals should shift upward after

the announcement. The average correlations decline significantly by 84.4% (from 0.17 to 0.026)

after cash announcements. Similarly to in the covariance case, the results for the correlation

are consistent with the expected changes for the anticipation of the payment method.

All in all, the sample post-announcement moments are different from the pre-announcement

ones. The differences are consistent with the previous findings in the literature, showing this

sample to be comparable with previous ones. Moreover, the announcements move the second-

order moments towards the aforementioned expected levels.

5 Evidence on the Anticipation of Deal and Payment Form

5.1 Breaks in the Variance-Covariance Structure

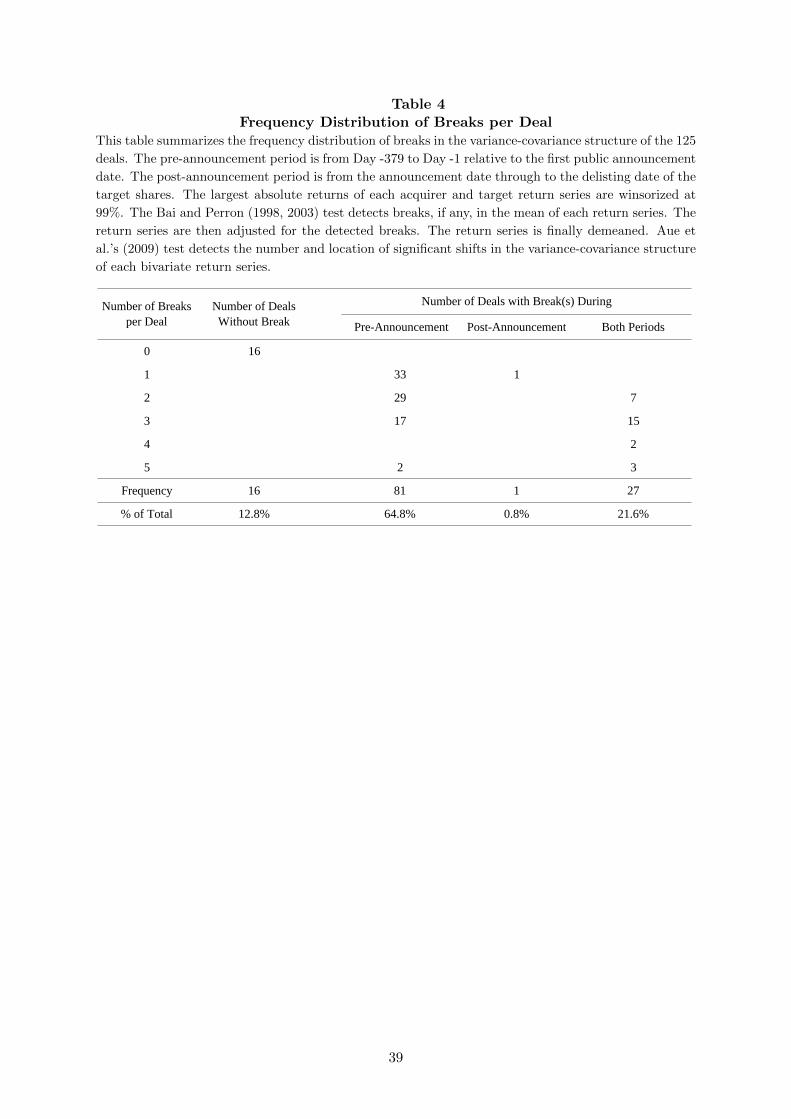

Table 4 and Figure 1 summarize the results of performing Aue et al.’s (2009) test on the

125 bivariate return series. There is at least one significant break in 87.2% of the deals (109 out

of 125) and multiple breaks in 60% of them (Table 4). However, this test does not detect any

breaks in 16 of the deals, indicating that they are unanticipated. The market may not perceive

a substantial synergy in their mergers; otherwise there should be shift(s), at least after their

announcements.

Insert Table 4 here

14

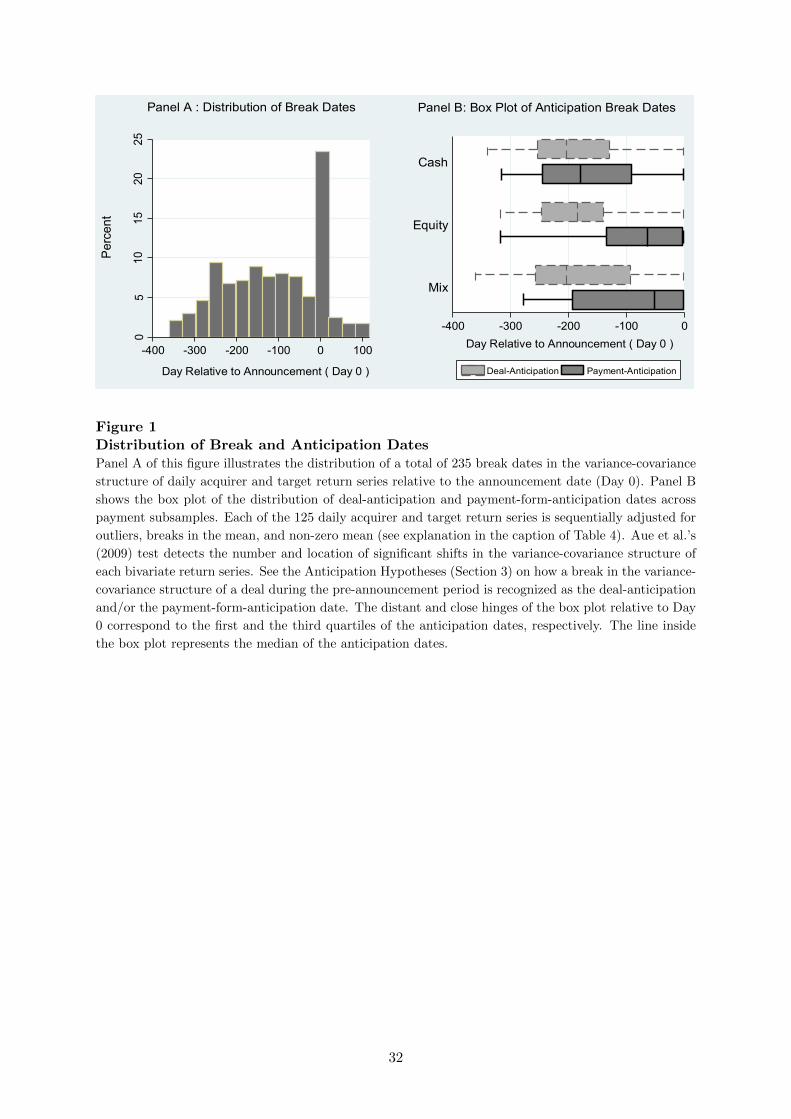

The findings imply a significantly skewed location of breaks towards the pre-announcement

period, since 108 (out of the abovementioned 109) deals have shifts in this period (Table

4). Moreover, Panel A of Figure 1 illustrates a considerable variation in the distribution

of break dates during the sample observation period; however, its mass is located in the

pre-announcement period. The merger arbitrage literature assumes a break only on the an-

nouncement date of each bid, and the spike around the announcement (Day 0) in Panel A

of Figure 1 supports this assumption. However, 27 out of 28 deals with break(s) during the

post-announcement period indeed have break(s) in the pre-announcement period as well. The

existence of these additional post-announcement breaks indicates that the market only revises

its pre-announcement predictions after the bid offers have been made. If we assume that a shift

in the variance-covariance structure reveals some relevant information about M&As, the results

here indicate that much of the information is leaked during the pre-announcement period.

Insert Figure 1 here

5.2 Deal Anticipation

Table 5 presents the deal-anticipation results. I find that 108 deals are anticipated. The

rest of the deals (17) are unanticipated due to the absence of breaks in the pre-announcement

period. The anticipated deals consist of 46 cash, 30 equity and 32 mixed-payment deals. The

fraction of anticipated deals is similar across the payment subsamples, implying that a deal is

anticipated regardless of the payment form offered. Overall, the existence of consistent shifts in

a large fraction of deals (86.4%) indicates that anticipation is a key characteristic of the deals

in this M&A sample, and that the anticipation mechanism is successful in identifying them.

Insert Table 5 here

5.2.1 Deal-Anticipation Dates

A deal is anticipated on average 187 trading days prior to the announcement day (Table

5). The interquartile range of the deal-anticipation dates is between Day -252 and Day -133,

implying that 75% of deals are anticipated at least six months prior to their announcement.

Panel B of Figure 1 demonstrates relatively similar distributions of deal-anticipation dates across

the cash, equity and mixed subsamples. A very small F-value of the ANOVA test (0.05) in Table

5 also indicates the similarity of the average anticipation dates across payment subsamples.

This leads me to conclude that the market starts to anticipate a potential takeover on average

almost nine months prior to the announcement date. This result indicates that takeovers are

anticipatable much earlier than has been documented in the previous event studies (i.e., two

months prior to the announcement as reported by Schwert, 1996).

5.2.2 Sample Moments around Deal-Anticipation Dates

The unreported results of the equality tests indicate that a significant decline in the acquirers’

volatility (in the correlation) leads to the anticipation of five deals (one deal). The majority

15

of deals (102 out of 108) are anticipated due to expected significant shifts in at least two of

the second-order moments. This evidence suggests that the deal anticipation markedly affects

the variance-covariance structure of the bivariate series during the pre-announcement period,

though the anticipation hypotheses do not require that at least two of the moments to shift.

Table 6 documents the sample second-order moments around the 108 deal-anticipation dates.

As expected, the target volatility decreases significantly after the deal is anticipated. The

average (median) for the total sample of anticipated deals declines significantly from 0.552

(0.509) to 0.443 (0.404) from the pre- to the post-anticipation segments. This average decline

(19.8%) due to the anticipation of the deal is smaller than that after the bid announcement

(44.1%). This result is explainable by the existence of multiple breaks per deal in the majority of

the sample (75 out of 125 deals). The target volatility decreases substantially across segments,

so assuming its break date to be equal to the announcement date overestimates the size of the

decline. Moreover, the target volatility decreases significantly in the cash and mixed subsamples

and is unchanged in the equity bids. Similarly to in the merger arbitrage literature and the

descriptive results, the largest volatility decline is observed for those bids for which the medium

of payment consists of at least some fraction of cash.

Insert Table 6 here

According to the expected shifts, any (positive or negative) shift in the acquirer volatility

is interpretable as a deal-anticipation signal. However, the declining shifts dominate at the

anticipation time. The average (median) acquirer volatility for the total sample declines by

a significant 15.7% (8.9%), from 0.443 (0.368) to 0.374 (0.336), from the pre- to the post-

anticipation segments. The median comparison tests in Table 6 indicate that this reduction

is significant across all payment subsamples. These results indicate that the reduction in the

acquirer volatility due to the perceived synergistic gains at the anticipation time outweigh the

increases due to the leverage and integration risks. Thus, this evidence verifies the proposed

synergy hypothesis: i.e. the most likely time for the market to anticipate a deal is when

it perceives some synergistic gains to be made from the merger of the anticipated firm-pair.

Furthermore, the ANOVA analyses indicate that the average decline in the acquirer volatility

differs across payment subsamples. Similarly to in the target case, the largest declines are in

the cash and mixed subsamples and the smallest one is in the equity bids. A t-statistic of -1.15

indicates that the average decline (7.4%) is insignificant in the equity subsample. This result is

expected since the acquirer and target firms are about the same size in this subsample, which

exposes the acquirers greatly to integration and leverage risks.

The unreported results of the equality tests indicate that the number of deals in which the

covariance changes significantly due to the anticipation of the deal is 91. This number is greater

than those for both the target and acquirer volatilities (78 and 80 deals). This result implies that

the shift in the covariance is the main source for recognizing breaks as deal-anticipation dates.

Moreover, while the ANOVA analysis (an F-value of 1.59) indicates that the average covariance

is similar across payment subsamples in the pre-anticipation segment, the significant F-value

(4.56) indicates that those averages diverge in the post-anticipation segment. This suggests that

16

shifts in the covariance at the deal-anticipation time can capture some expectations about the

likely payment form. In other words, anticipating a deal affects the covariance in a way that is

consistent with the offered payment form. Therefore, this moment should be controlled for in

the payment-method regressions.

The correlation is the most stable moment since it has the smallest number of significant

changes (40) after the 108 deal-anticipation breaks. The results of the mean and median tests

presented in Table 6 support this evidence by showing that the correlations are unaffected by

the anticipation of the deals. These insignificant results are not odd since the standardization

in the correlation removes some of the useful variation, and in turn confirms the usefulness of

examining shifts in the covariance in order to identify both deal-anticipation and payment-form-

anticipation dates.

5.3 Payment-Form Anticipation

Table 5 also summarizes the payment-form-anticipation results. By definition, the payment-

form-anticipation procedure examines the subsample of 108 anticipated deals. It identifies 77

of them as having shifts consistent with the offered payment form, which splits into 37 cash,

21 equity and 19 mixed-payment bids. The portion of the total deals for which payment form

is anticipated (61.6%) is significantly lower than that for which deals are anticipated per se

(86.4%). This is expected since anticipating the payment form requires the detection of more

precise changes in the second-order moments during the pre-announcement period. Moreover,

the fraction of anticipated mixed offers (50%) is lower than the fractions of cash and equity offers

(68.5% and 63.6%), implying that the market is less successful in anticipating the mixed offers.

This result is not surprising since there is an additional parameter that must be anticipated in

the mixed offers, i.e. the portion of cash in the total payment.

5.3.1 Payment-Form-Anticipation Dates

Table 5 reports the average (median) payment-form-anticipation date to be Day -123 (Day

-106), six (five) months prior to the announcement date. The mean test (with a t-statistic of

-4.49) indicates that a deal is anticipated on average 63 trading days before its payment form. It

takes on average three months for the market either to receive stronger signals or to reinterpret

the available information so as to pinpoint the most likely payment form of the anticipated

deals. This difference between the average dates is due to the fact that the deal-anticipation

and payment-form-anticipation dates do not coincide in 32 of the deals, i.e. another more recent

break date identifies their payment-form-anticipation date.

Panel B of Figure 1 suggests that the distribution of the payment-form-anticipation date

varies across the cash, equity and mixed subsamples. In contrast to the deal-anticipation results,

a large F-value of the ANOVA test (6.11) supports cash offers being anticipated on average much

earlier than both equity and mixed offers. Moreover, the mean tests (t-statistics of -4.29 and

-3.07) indicate that a deal is anticipated on average at least four months before the market

anticipates that its payment form will be either equity or mixed. Nevertheless, this is not

17

the case for the cash subsample. In fact, cash offers are anticipated to a greater extent in

simultaneous breaks (i.e. both the deal and the payment form are anticipated in one break)

compared to equity and mixed offers. Therefore, the market receives stronger signals when

anticipating cash offers. Overall, these results lead me to conclude that the announcement

of cash (equity and mixed) offers contains the least (most) unexpected information across the

payment subsamples for the market investors.

5.3.2 Sample Moments around Payment-Form-Anticipation Dates

The unreported results of the equality tests indicate that consistent shifts in both the covari-

ance and correlation lead to the anticipation of the payment form in 44 out of the 77 deals, while

in 28 of them it is anticipated solely due to shifts in the covariance. This result implies that the

covariance is better than the correlation not only in capturing instabilities in the covariation

between the target and the acquirer returns, but also in anticipating the payment form.

Table 7 summarizes the sample second-order moments around the 77 payment-form-anticipation

dates. Similarly to in the deal-anticipation case, both the mean and median tests indicate that

the target volatility declines significantly after the payment-anticipation date in the total sam-

ple and in the payment subsamples. However, the target returns are significantly less volatile

in the post-payment-anticipation segments (0.369) compared to in the post-deal-anticipation

ones (0.443). The target volatility hence declines substantially across regimes during the pre-

announcement period. This evidence suggests that the market incorporates both anticipation

signals by reducing the risk of investing in the target stocks. Moreover, payment-form antici-

pation also decreases the acquirer volatility. However, the results of the mean and median tests

show that the decline is only significant in the cash subsample. Therefore, the acquirer’s risk

declines significantly only when the market anticipates that it will use cash to finance the bid.

Insert Table 7 here

As expected, the covariance increases significantly after the anticipation of equity offers,

since its average (median) shift is upward from 0.039 (0.023) to 0.120 (0.076) from the pre- to

the post-anticipation segments. The average size of the increase in this case (210.5%) is much

greater than those around the deal-anticipation dates (15%). Moreover, the anticipation of cash

offers reduces the average (median) covariance by a highly significant -78% (-83.1%), from 0.054

(0.031) to 0.012 (0.005), from the pre- to the post-anticipation segments. Again, the opposing

consistent shifts lead the mean and median difference between the post- and pre-anticipation

covariances to be insignificant in the mixed subsample. Overall, these sizable shifts indicate

that the market receives strong signals about the deal and its payment form, and incorporates

them into the covariance of the firm-pair around the payment-form-anticipation dates.

In contrast to the insignificant results around the deal-anticipation dates, the average and

median differences between the post- and pre-payment anticipation correlations are significant in

the payment subsamples. These shifts are in line with the expected payment-form-anticipation

breaks: i.e. increasing in the equity cases and declining in the cash cases. For example, the

average (median) correlation increases after the anticipation of the equity offers by a highly

18

significant 142.2% (188.5%), from 25.2% (22.7%) to 61% (65.5%), between the pre- and post-

anticipation segments. The average and median sizes of the shifts in this case are substantially

greater than those around the deal-anticipation dates (11.1%, 10.6%).

6 Robustness Tests

6.1 Firm-Specific Events as Source of M&A Anticipation

Do firm-specific (non-M&A) events cause those anticipation shifts? The portfolio theory

suggests that the effects of firm-specific news should be diversified in a large portfolio, leaving

its volatility unchanged. Groß-Klußmann and Hautsch (2011) find that the arrival of firm-

specific news generates volatility dynamics only at the intraday level (the changes last for only

a few hours). To address the above question, I examine whether the second-order moments

of portfolios of merged firms shift. If so, then those shifts do not originate from firm-specific

(non-M&A) events. Moreover, if they follow the expected shifts, then the related break dates

serve as alternative average anticipation dates.

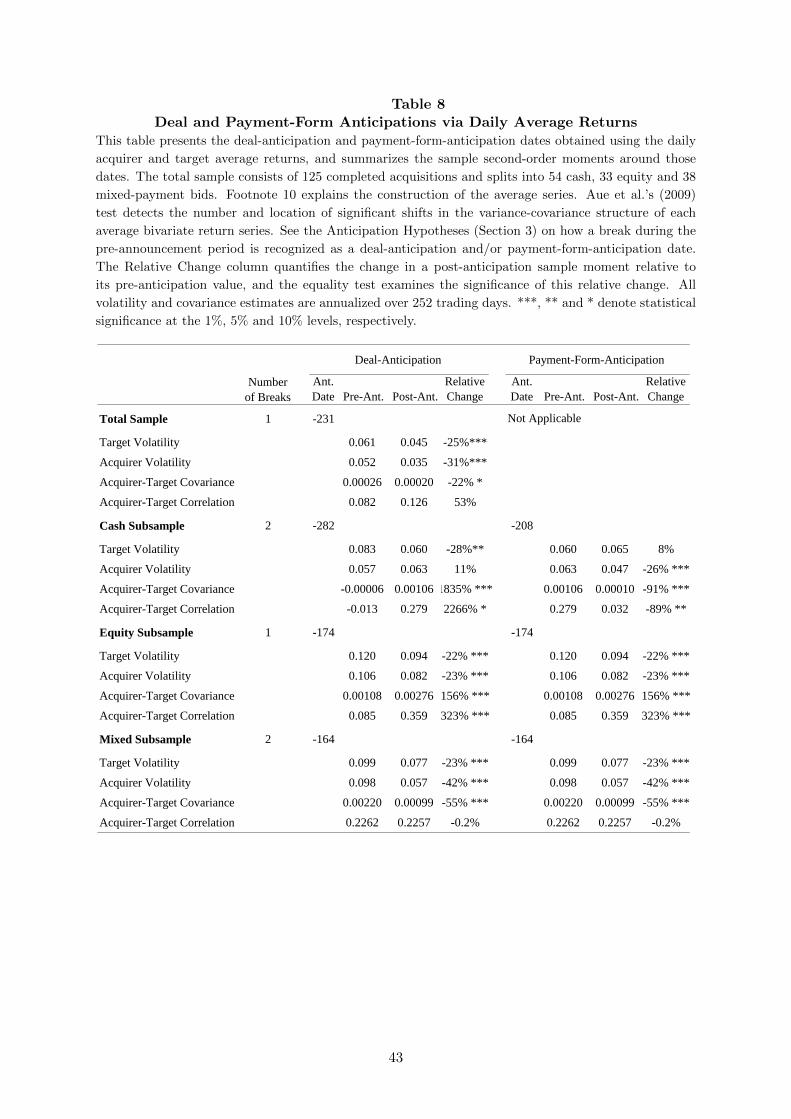

Table 8 reports the results of Aue et al.’s (2009) test performed on the daily average acquirer

and target return series for the total and the payment subsamples.10 The test detects either

one or two breaks in the variance-covariance structure, both of which are located before the

announcement date. This finding implies that the source of the observed anticipation breaks in

the individual bivariate return series is not firm-specific (non-M&A) events.

Insert Table 8 here

There is one significant break in the variance-covariance structure of the acquirer and target

average return series for the total sample, on Day -231. Both the target and acquirer volatilities

and the covariance decline significantly, by 25%, 31%, and 22% after this break date, respec-

tively. All these consistent shifts imply that a deal is anticipated on average 231 days prior to

the announcement day. This evidence verifies that the M&A anticipation is the key feature of

this sample since it is not removed even by the daily cross-sectional aggregation.

Figure 2 illustrates how the moments change significantly around the break dates of the

payment portfolios. The test detects only one break, on Day -174, for the portfolio of equity

deals. All moments change significantly after this date, so the deal is anticipated on Day -174.

Moreover, since both the covariance and the correlation increase, the market also anticipates

that the payment form will be equity. Thus, both the deal itself and equity payment are

anticipated simultaneously, at one break, i.e. on Day -174.

10The daily average return series are equally weighted portfolio returns: ri,j,t =1

Nj

Nj∑n=1

ri,n,t, where ri,n,t is

the realized return, i is the subscript for the acquirer and target series, j is the subscript for the total sample andfor the cash, equity and mixed subsamples, t is the subscript for Day t and runs from trading day -379 to +78,and Nj is the subscript for the number of stocks in the subsample j that have return observation on Day t. Atleast 120 (54) out of the 125 series are used to construct the daily average return series during the pre- (post-)announcement period for the total sample. Each daily average return series is then adjusted for outliers, breaksin the mean and non-zero mean before Aue et al.’s (2009) test is applied.

19

Insert Figure 2 here

The portfolio of cash deals contains two breaks, on Day -282 and Day -208. Significant shifts

after these breaks are consistent with the deal-anticipation hypothesis, implying that the deal

is anticipated from the earlier point in time (i.e., Day -282). However, both the covariance and

the correlation diverge from zero (the expected level), and so the market incorrectly anticipates

that equity is the most likely payment form. It corrects its anticipation at the next break (Day

-208), and anticipates cash to be the most likely payment form as those moments converge to

zero. This is a case in which the anticipation dates do not coincide and the deal is anticipated

earlier than the payment method.

The portfolio of mixed-payment deals has two breaks, on Day -164 and Day -9. Significant

shifts are compatible with both of the anticipation hypotheses, suggesting that the market starts

to anticipate the deal and its payment form from the time of the distant break (i.e., Day -164).

The acquirers pay around 56% of the deal value in cash in this subsample. This explains why

the covariance declines and converges to zero after those breaks, because the market anticipates

that cash will make up the dominant portion of the payment. This is an example of consistent

updating breaks when the market anticipated the features of forthcoming M&As. Overall, the

anticipation results based on the portfolio approach confirm those based on the 125 individual

bivariate return series.

6.2 Placebo Analysis: Market-Wide Events as Source of M&A Anticipation

If firm-specific (non-M&A) events are not the main drivers of the anticipation dates, do

some market-wide events during the sample period of this paper cause them? If so, then similar

consistent shifts should be detected in a benchmark sample. To investigate this issue, I consider

a random sample of non-M&A firms, whose results also serve as the empirical identification of

the proposed anticipation mechanism.

A non-M&A firm is a firm that has not been involved in any sort of takeover activity during

the sample period of this paper. A pair of non-M&A firms is selected randomly from the

same industry as the M&A pair. This sampling is done without replacement. M&As are more

likely to cluster in some industries (e.g., the IT industry in this sample period), so the market

assigns some merging likelihood to these placebo pairs as well. The industry matching can

hence generate a greater portion of anticipated deals compared to a case in which placebo pairs

are selected randomly from the entire population of non-M&A firms.

First, the test detects shifts consistent with the deal-anticipation and the payment-form-

anticipation hypothesis in 38 and 15 (out of 125) placebo pairs, respectively. These figures are

considerably smaller than those for the M&A sample (105 and 75). Second, if the market-wide

and (or) industry-wide news causes those shifts in both the benchmark and M&A samples,

their anticipation dates should be comparable. However, this is not the case since only 4

(out of the 38) placebo anticipation dates lie within (an absolute) one-month interval of their

M&A counterparts’ anticipation dates. Third, the levels of the moments around the placebo

dates are less consistent with the expected ones. For example, the anticipation of an equity

20

offer causes the correlation to increase on average from 9% to 16% in the benchmark sample

while it increases from 25% to 61% in the M&A sample. The shifts in the benchmark sample

deviate considerably from the expected correlation (100%), so they seem unrelated to the equity

anticipation. Finally, the test fails to reject the null of stability (at the conventional levels) for

the daily average return series of the benchmark sample. The cross-sectional aggregation via

the portfolio approach removes the observed shifts in the individual placebo pairs. The portfolio

theory suggests that those shifts are highly likely to be driven by firm-specific events, and are

unrelated to the anticipation of M&As. The placebo results lead me to conclude that market-

wide events are not the driver of the observed shifts in the M&A sample, and those shifts indeed

capture informational events about the future M&As.11

6.3 Anticipation Mechanism

6.3.1 Probability of Takeover

The anticipation mechanism conjectures that the anticipation shifts occur when the merging

likelihood increases significantly during the pre-announcement period. If those shifts are iden-

tified randomly and are unrelated to M&As, then the merging likelihood remains on average

unchanged and trivial around those dates. A measure for the takeover probability, based on the

work of Samuelson and Rosenthal (1986), is considered here to examine this issue.

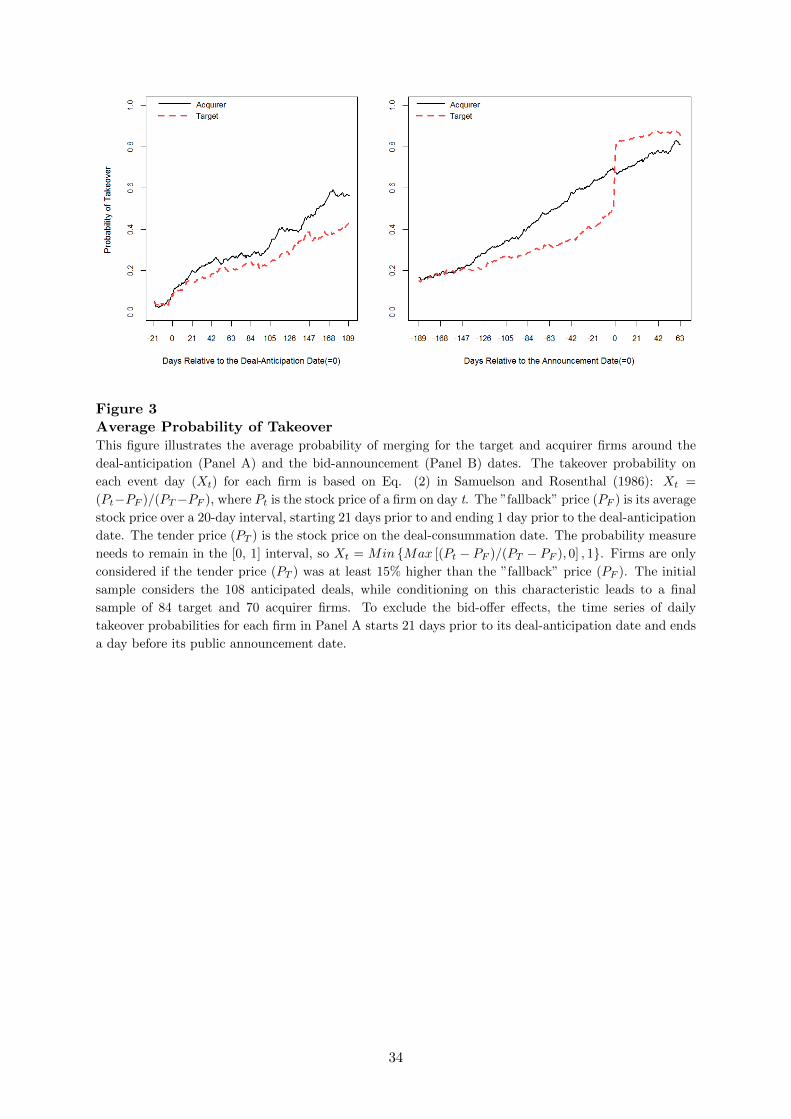

Fig. 3 depicts the average takeover probability for the merging firms around the deal-

anticipation date (Panel A) and around the bid-announcement date (Panel B). As expected,

the takeover probabilities first materialize around the detected anticipation dates, and show a

positive trend afterwards. This evidence confirms that the anticipation shifts detect increases

in the likelihood of mergers.

Insert Figure 3 here

Consistent with Cornett, Tanyeri, and Tehranian (2011), both plots indicate that the acquir-

ers are more anticipatable than the target firms during the pre-announcement period. Moreover,

the increases in the probabilities are not abrupt but occur gradually. This finding suggests that

only a portion of investors in the market anticipate future M&As, and (or) stronger signals

about takeovers are released as time passes. In fact, the takeover probabilities reach their maxi-

mum (for target firms in particular) around the bid-announcement date, when the most relevant

information about the takeover terms is revealed publicly. This result is in line with previous

studies (Samuelson and Rosenthal, 1986; Brown and Raymond, 1986).

6.3.2 Abnormal Gains around the Deal-Anticipation Dates

According to the proposed mechanism, a takeover is anticipated when the market perceives

some synergistic gains to be had by the consolidated firm. If this is the case, then part of those

gains should be incorporated in the share prices of the merging firms around the anticipation

11The results of analyzing the benchmark sample are not reported here, so as to save space, but they areavailable upon request.

21

date. In fact, Figure 4 illustrates that the CAARs to both the target and acquirer shares

show a positive trend after the deal-anticipation dates.12 This evidence hence supports that

prediction of the anticipation mechanism. Moreover, previous studies examine CAARs in the

post-announcement (even in the post-acquisition) period to identify the synergistic gains made

by M&As. However, the findings here indicate that some of those gains are indeed discounted

and incorporated in the share prices long before the announcement, i.e. at the anticipation

time. Overall, the above results lead me to conclude that anticipating a takeover based on both

synergistic gains and a fairly high merging probability shifts the second-order moments in the

expected directions.

Insert Figure 4 here

6.4 Methodological Issues

6.4.1 Univariate versus Multivariate Tests

In addition to the test from Aue et al. (2009), three univariate tests separately detect

multiple breaks in the variances, covariance and correlation. The internet appendix (Sections

B and D) gives a detailed presentation of these univariate tests and their results. First, the

tests are performed to determine the main source of non-stationarity in the variance-covariance

structure of the bivariate return series. Is it instability in the target variance, for example, that

causes shifts in the variance-covariance structure? If this is the case, then non-stationarity in the

variance-covariance structure is nothing more than non-stationarity in the target variance, and

extending the analysis to the variance-covariance structure will be useless. Second, detecting

breaks in the moments of the univariate series will provoke its own interpretations. A decline

(a shift) in the target (acquirer) variance during the pre-announcement period will suggest that

the market anticipates the target (acquirer) firm. Similarly, the existence of consistent shifts in

the covariance and the correlation will indicate payment-form anticipation.

The instability in the target and acquirer variances is the major source of non-stationarity

in the variance-covariance structure of the 125 bivariate return series. The univariate results

indicate that both acquirer and target firms are anticipatable. However, the acquirers are more

so than the target firms, being anticipated on average one month earlier than the targets. The

fraction of anticipated deals identified via the univariate tests is significantly smaller than that

obtained via the multivariate test. Furthermore, Aue et al.’s (2009) test is more powerful than

the univariate tests in detecting payment-form-anticipation dates. These results are expected

since Aue et al.’s (2009) test efficiently uses variations in all second-order moments of the joint

return distribution to identify breaks in the variance-covariance structure.

6.4.2 Raw versus Winsorized Return Series