JERRY NAGY & MEGAN BOOTH NATIONAL ASSOCIATION OF REALTORS® Federal Housing Response.

15

JERRY NAGY & MEGAN BOOTH NATIONAL ASSOCIATION OF REALTORS® Federal Housing Response

-

Upload

della-mitchell -

Category

Documents

-

view

215 -

download

0

Transcript of JERRY NAGY & MEGAN BOOTH NATIONAL ASSOCIATION OF REALTORS® Federal Housing Response.

JERRY NAGY & MEGAN BOOTHNATIONAL ASSOCIATION OF REALTORS®

Federal Housing Response

Federal Housing Programs

FHA Loan limits equal to 125% 2008 median home price – up to $729,750 3.5% downpayment – 6% seller concessions allowed MIP = 1.75 upfront/.5-.55 annual/1.50 refi No minimum credit score Loan limits – https://entp.hud.gov/idapp/html/hicostlook.cfm

VA Loan limits equal to 125% 2008 median home price – up to $1,094,625 Zero-downpayment Fees = 2.15% on zero-down (3.3% for repeat) – no fee if service-connected

disability No minimum credit score Loan limits - http://www.homeloans.va.gov/docs/2009_county_loan_limits.pdf

RHS Income eligible up to 115% local area median income Flexible downpayment (including zero-down) Eligible areas - http://eligibility.sc.egov.usda.gov/eligibility/welcomeAction.do

Specific Loan Programs

203k rehabilitation mortgage FHA

Energy Efficient Mortgages FHA Freddie Mac/Fannie Mae

Location Efficient Mortgages Freddie Mac/Fannie Mae

HECM FHA

HECM for Purchase FHA

Homebuyer Tax Credit

$8000 Tax Credit for first time homebuyers**may not have owned a home in previous 3 yrs

Any single family residence (including condos and coops) that is a principal residence

Income Limits ($75,000-$95,000/$150,000-$170,000)

Recapture if sold in first 3 years

Effective January 1, 2009 – November 30, 2009

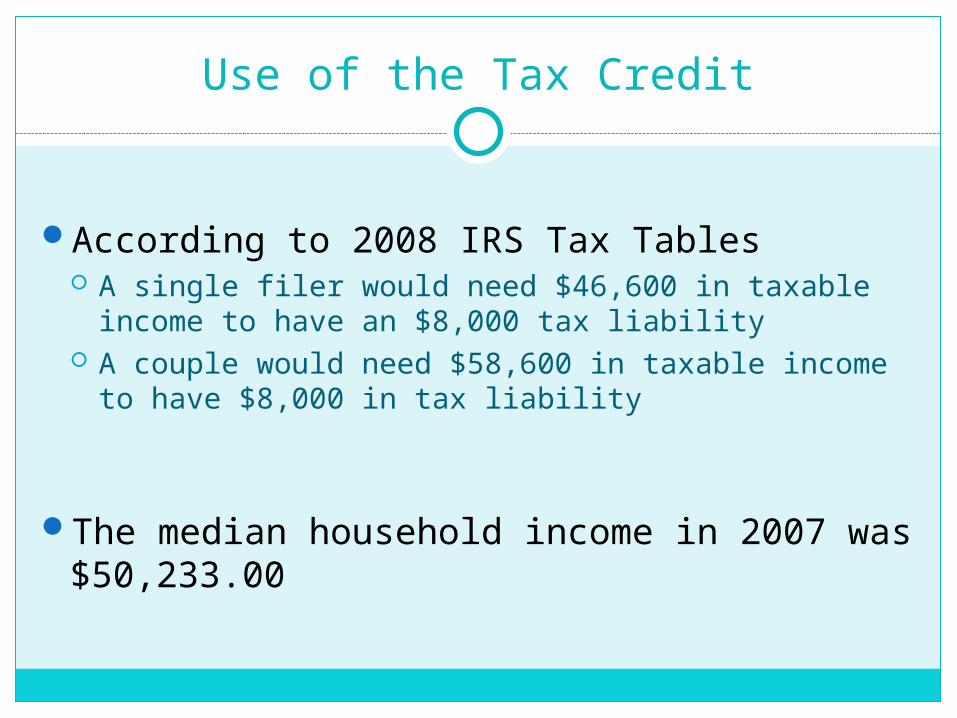

Use of the Tax Credit

According to 2008 IRS Tax Tables A single filer would need $46,600 in taxable income to

have an $8,000 tax liability A couple would need $58,600 in taxable income to

have $8,000 in tax liability

The median household income in 2007 was $50,233.00

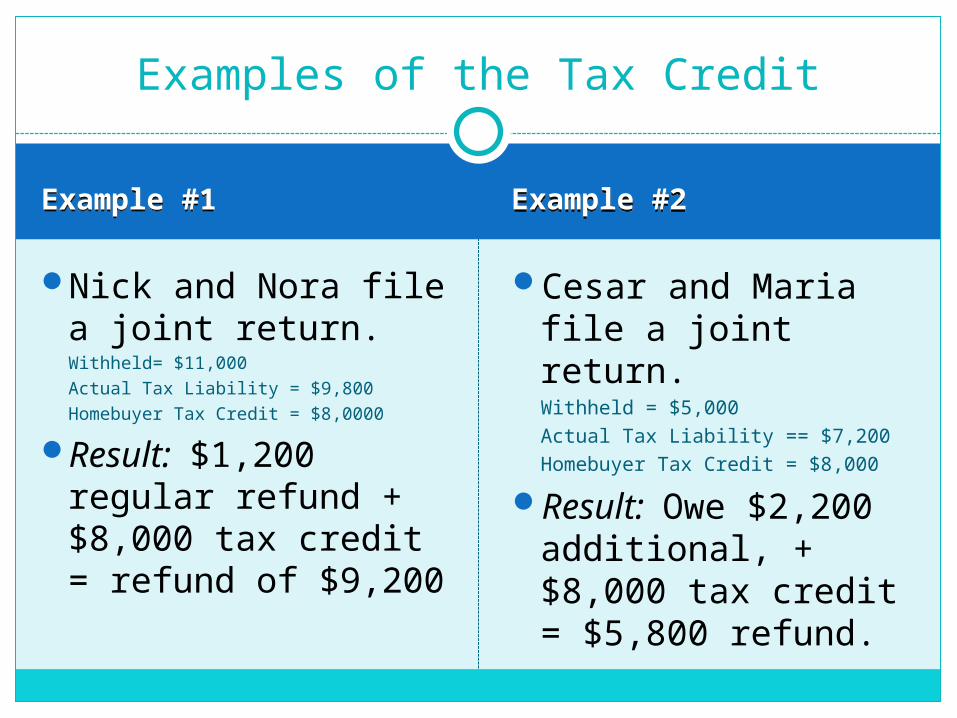

Example #1Example #1 Example #2Example #2

Nick and Nora file a joint return. Withheld= $11,000Actual Tax Liability = $9,800Homebuyer Tax Credit = $8,0000

Result: $1,200 regular refund + $8,000 tax credit = refund of $9,200

Cesar and Maria file a joint return. Withheld = $5,000Actual Tax Liability == $7,200Homebuyer Tax Credit = $8,000

Result: Owe $2,200 additional, + $8,000 tax credit = $5,800 refund.

Examples of the Tax Credit

Homeowners in Trouble

Hope for HomeownersGSE RefinancingGSE Loan ModificationOther Resources

1 888 995 HOPE (4673)

HOPE for Homeowners (H4H)

Updates being debated in Congress

Effective October 1, 2008

Voluntary for lender and homeowner

New loan at 90% (93%) current appraised value

FHA must approve loans and borrowers

National loan limit of $550,400

(Incentives to lenders/servicers)

More information at www.fha.gov/hopeforhomeowners

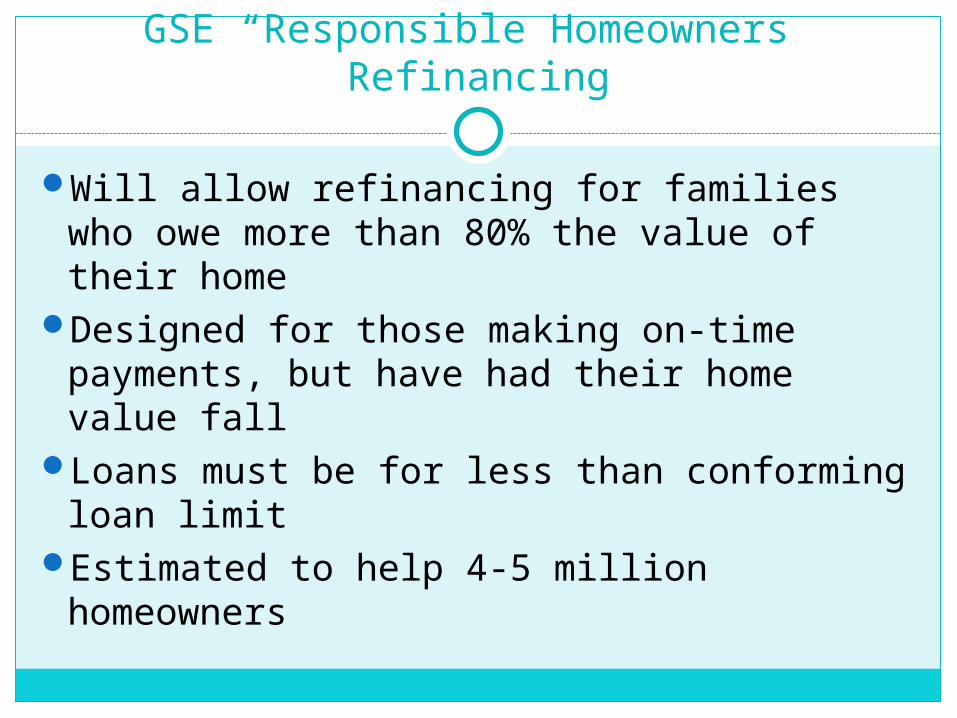

GSE “Responsible Homeowners” Refinancing

Will allow refinancing for families who owe more than 80% the value of their home

Designed for those making on-time payments, but have had their home value fall

Loans must be for less than conforming loan limit

Estimated to help 4-5 million homeowners

GSE “Responsible Homeowners” RefinancingEXAMPLE

In 2006, the family took out a 6.5% 30-year fixed rate mortgage for $207,000 on a house appraised at $260,000.

Home is now worth $221,000, and they owe $200,000. They would have a hard time refinancing because they don’t

have 20% equity. They could refinance into today’s rates (near 5.1%), reducing

their annual payment by $2,300.

Existing Mortgage

Refinancing

Balance $199,584 $203,575

Remaining Years

27 30

Interest Rate 6.50% 5.16%

Monthly Payment

$1,308 $1,113

Savings $196 per month, $2,347 per year

Homeowner Stability Initiative

For homeowners who are at risk of foreclosureShared effort to reduce mortgage payments

Lender must reduce interest rate, so that the payment is no more than 38% of income

Federal government will further reduce interest rate to bring the ratio down to 31%

Interest rate stays low for 5 years, then gradually increased up to conforming rate at time loan was made

Payment incentives to homeowners to reduce principal (up to $1000/year) for up to 5 years

Incentives for servicers to participate and for lenders/servicers to reach borrower before delinquent

Partial guaranteesGuidelines for Loan Modifications

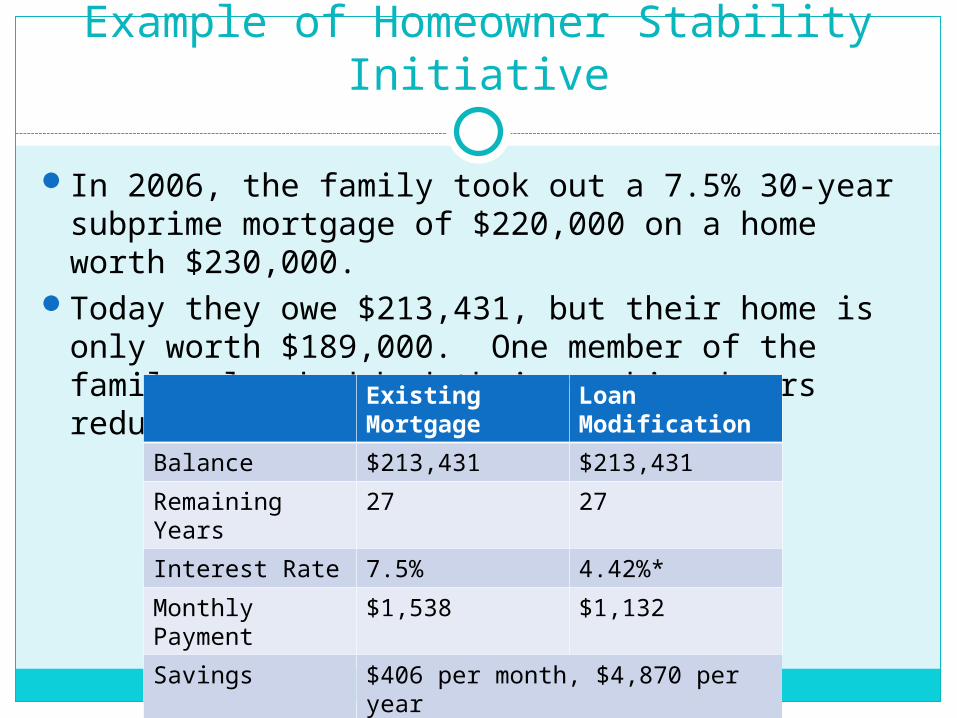

Example of Homeowner Stability Initiative

In 2006, the family took out a 7.5% 30-year subprime mortgage of $220,000 on a home worth $230,000.

Today they owe $213,431, but their home is only worth $189,000. One member of the family also had had their working hours reduced, lowering their income.

Existing Mortgage

Loan Modification

Balance $213,431 $213,431

Remaining Years

27 27

Interest Rate 7.5% 4.42%*

Monthly Payment

$1,538 $1,132

Savings $406 per month, $4,870 per year

What do Homeowners Do?

As of March 4, the programs are availableThe information a homeowner will need to

provide: #1- call lender and ask if you are Freddie/Fannie Loan Gross monthly income of all borrowers, including pay

stubs Most recent income tax return Information about any second (or third) mortgages

(only the first mortgage will be modified) Payment information on all credit cards Any payments on other loans (student, car)

CDBG – Neighborhood Stabilization Program

$4 billion allocated to states/localities based on foreclosure rate, # of subprime mortgages, # homes in default or delinquency – additional $2b allocated in ARRA – competitive bid

Funds provided through the CDBG Program Funds used to:

Provide financing Purchase Manage Repair Resell foreclosed and abandoned properties

Homes must be: used to assist individuals and families with incomes at or below

120% of area median income. Twenty-five percent of funds must be used for households with

incomes at or below 50% of area median income.

Resources for More Information

www.realtor.org/governmentaffairs

www.fha.gov

![George Nagy - List of Publications Journal papers and book ...nagy/allpubs.pdf · Sept. 9, 2018 Nagy – Journal papers and book chapters 3 of 26 [33] G. Nagy and L. Wilson, "Program](https://static.fdocuments.us/doc/165x107/5c67b1b009d3f2c85f8c4bc8/george-nagy-list-of-publications-journal-papers-and-book-nagy-sept.jpg)