Jefferies Global Energy Conference · NYSE: NFX November 28, 2012 Jefferies Global Energy...

13

www.newfield.com NYSE: NFX November 28, 2012 Jefferies Global Energy Conference

Transcript of Jefferies Global Energy Conference · NYSE: NFX November 28, 2012 Jefferies Global Energy...

www.newfield.com NYSE: NFX

November 28, 2012

Jefferies Global Energy Conference

1. Transition to an Oil Company is Real ― Oil/Liquids to be >50% of Total Production in 4Q’12

2. Oil/Liquids Growth Driving Revenues, Cash Flow― ~85% of 2012 Revenues will come from Oil/Liquids

3. Encouraging Assessment Results — Cana Woodford

— Uteland Butte

— Wasatch Horizontal

— SXL Eagle Ford

4. Asset Sales Approximately $1B Since Early 2011

5. NFX Has a Deep Inventory of Oil/Liquids Assets― 2013 Domestic Oil/Liquids Growth >20%

2

3

1. Proven History in Oklahoma Woodford Formation― Arkoma Woodford ~500 Total Wells (374 HZTs)

― 310,000 Net Acres Prospective for the Woodford Shale

Formation

2. Assessing the Anadarko Basin― Oil/Liquids-Rich Basin

― Thick, Quality Resource with Multiple Horizons

― >200,000 Net Acres

3. Cana Woodford ― 142,000 Net Acres

― Up to 1 Billion BOE of Net Unrisked Resource Potential

4

Key Statistics: • Current

― 4 NFX Operated Rigs Running (24 Total Industry Rigs)

― 19 NFX Horizontal Wells Producing

― 5 Wells Waiting on Completion

• 2013 Plan

― Up to 8 NFX Operated Rigs

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

JAN

FEB

MA

R

AP

R

MA

Y

JUN

JUL

AU

G

SEP

OC

T

NO

V

DE

C

JAN

FEB

MA

R

AP

R

MA

Y

JUN

JUL

AU

G

SEP

OC

T

NO

V

DE

C

JAN

FEB

MA

R

AP

R

MA

Y

JUN

JUL

AU

G

SEP

2010 2011 2012

Ne

t B

OE

PD

Gas Sales

NGL

Oil

Legacy Production / Cana Leasing Exploration Assessment

NFX Commences

HZT Drilling

26%

41%

33%

Product Composition

Oil

Gas Sales

NGL

5

Key Takeaways

• 142,000 Net Acres

• 9,300 BOEPD Net Production

― 60% Liquids

• Active Development/Assessment

― 4-6 NFX Operated Rigs

South Cana Results YTD

• 9 Producing Wells (Avg. 75% WI)

• 1,215 BOEPD Avg. IP (32% Oil)

• 901 BOEPD Avg. 30 Day Rate

• 792 BOEPD Avg. 100 Day Rate

North Cana (Klade Well)

• 925 BOEPD (93% Oil)

• 660 BOEPD Avg. 30 Day Rate

• 99% WI

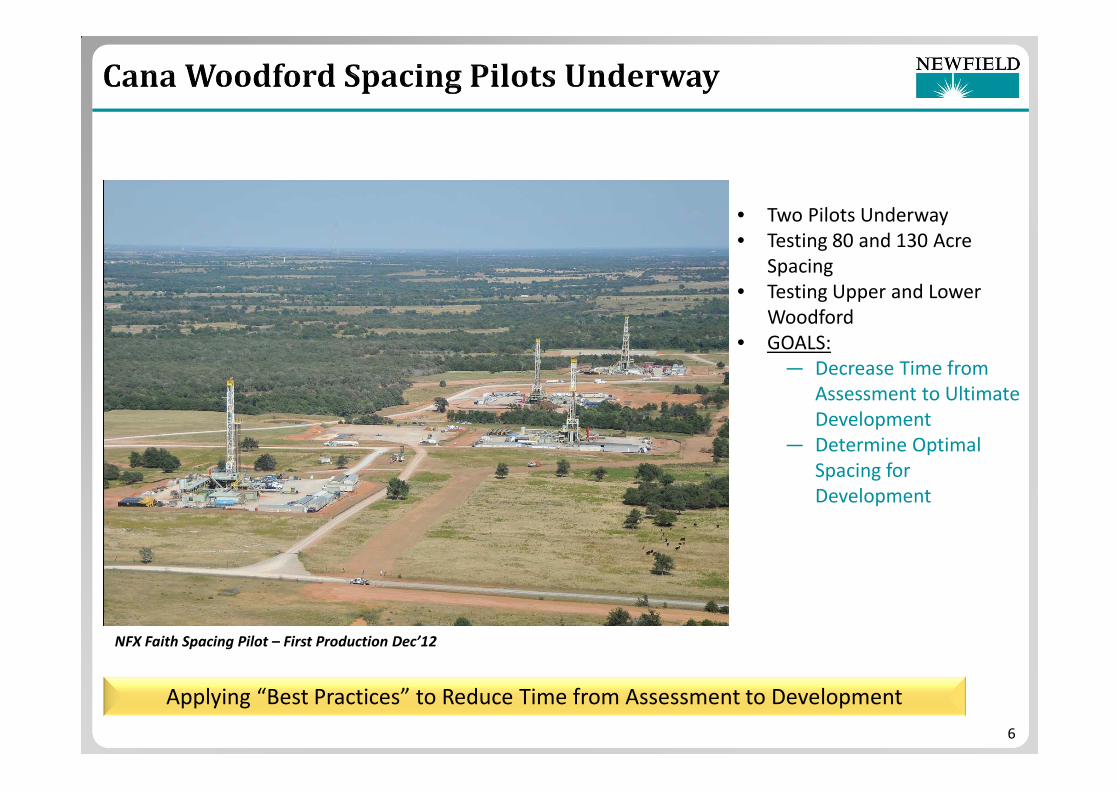

• Two Pilots Underway

• Testing 80 and 130 Acre

Spacing

• Testing Upper and Lower

Woodford

• GOALS:

― Decrease Time from

Assessment to Ultimate

Development

― Determine Optimal

Spacing for

Development

Applying “Best Practices” to Reduce Time from Assessment to Development

NFX Faith Spacing Pilot – First Production Dec’12

6

17% 15% 14% 13%

43% 49% 54% 57%

39% 36% 33% 30%

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

$25.00 $30.00 $35.00 $40.00

% R

ev

en

ue

Co

ntr

ibu

tio

n

BFI

TT

RO

R

NYMEX NGL Price, $/BNGL

ROR vs. NGL Price

Oil Rev. NGL Rev. Gas Rev. 5,000' ROR

$90/BO, $3.5/MCF

7

• LIQUIDS Drive Value Creation

South Cana(5,000’ Lateral)

North Cana(10,000’ Lateral)

77% 79% 81% 82%

13% 12% 11% 10%

10% 9% 8% 8%

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

$80 $90 $100 $110

% R

ev

en

ue

Co

ntr

ibu

tio

n

BFI

TT

RO

R

NYMEX Oil Price, $/BO

ROR vs. Oil Price

Oil Rev. NGL Rev. Gas Rev. 10,000' ROR

$3.5/MCF, $30/BNGL

Delivering Exceptional Returns

• OIL Drives Value Creation

8

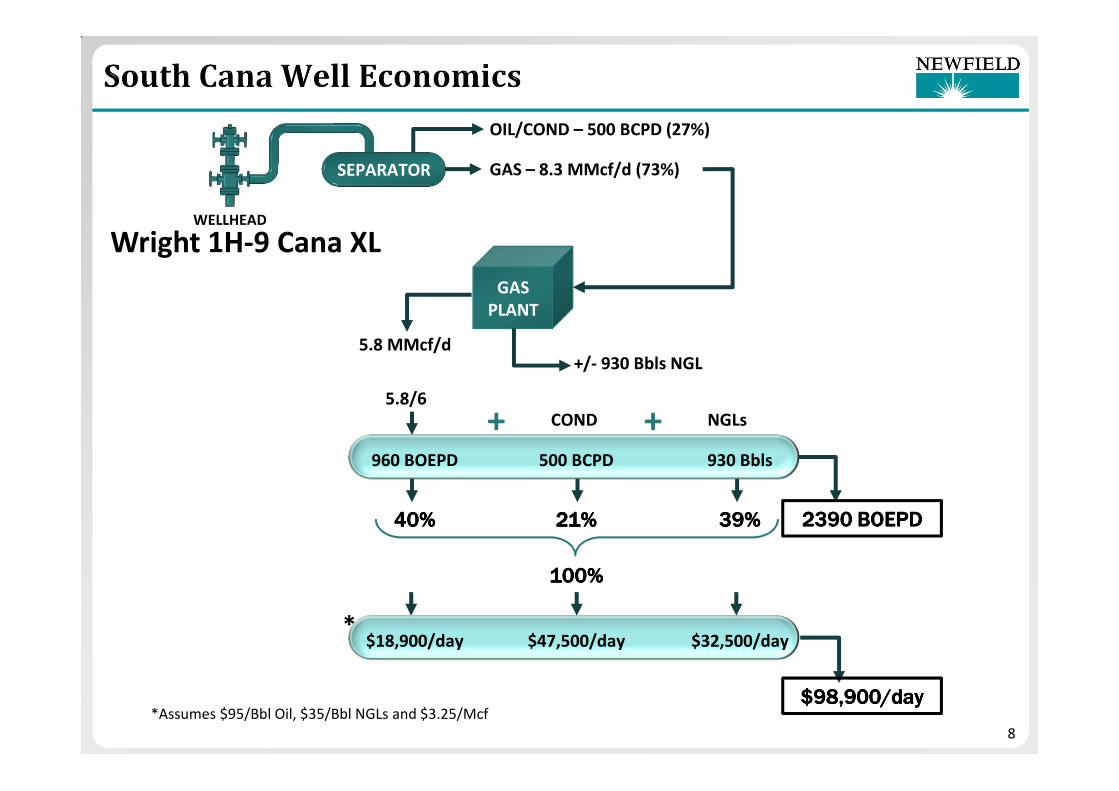

WELLHEAD

OIL/COND – 500 BCPD (27%)

SEPARATOR GAS – 8.3 MMcf/d (73%)

GAS

PLANT

5.8 MMcf/d+/- 930 Bbls NGL

5.8/6

960 BOEPD 500 BCPD 930 Bbls

+ +COND NGLs

40%40%40%40% 21%21%21%21% 39%39%39%39% 2390 BOEPD2390 BOEPD2390 BOEPD2390 BOEPD

100%100%100%100%

Wright 1H-9 Cana XL

$98,900/day$98,900/day$98,900/day$98,900/day

$18,900/day $47,500/day $32,500/day

*Assumes $95/Bbl Oil, $35/Bbl NGLs and $3.25/Mcf

*

9

• > 50% Improvement in Drill Time

and Cost/Lateral foot YTD’12

• New Technology― Rotary Steerable Systems

― New PDC Bits

― Innovative Casing Designs

• Identifying High “Rate of

Penetration” Zones

• Increasing Lateral Lengths to 7,500 -

10,000’

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,0000 10 20 30 40 50 60 70 80 90 100 110

Days

South CanaDays vs. Depth

Q12012

Q22012

Q32012

Best in Class: 40 Days

Faith 4H-12 Well (5,000’ Lateral)

Depth(ft.)

10

OZARK UPLIFT

BRAVODOME

SIERRAGRANDE

Arkoma Basin

Cherokee PlatformWoodford Shale

Woodford - SH

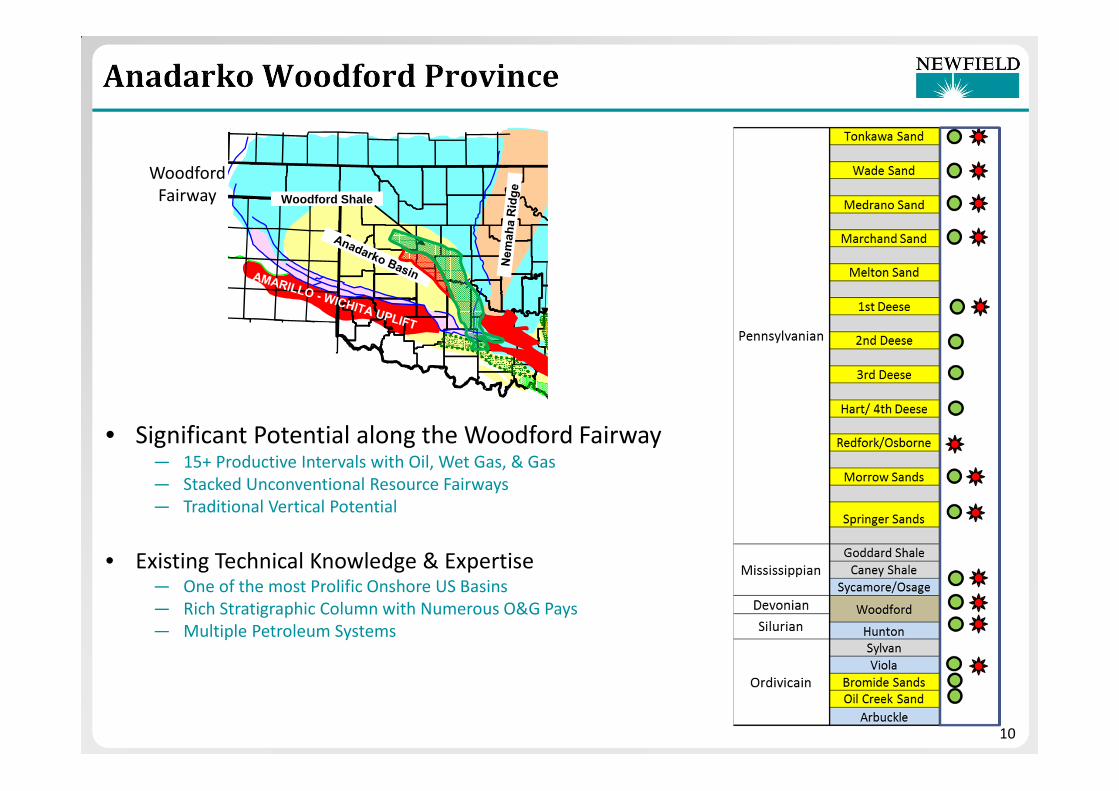

• Significant Potential along the Woodford Fairway― 15+ Productive Intervals with Oil, Wet Gas, & Gas

― Stacked Unconventional Resource Fairways

― Traditional Vertical Potential

• Existing Technical Knowledge & Expertise― One of the most Prolific Onshore US Basins

― Rich Stratigraphic Column with Numerous O&G Pays

― Multiple Petroleum Systems

Woodford

Fairway

Altamont / Bluebell

Natural Buttes

Greater Monument Butte Unit

UTAH

~10 Miles

Horizontal Wasatch Wells Horizontal Uteland Butte

• 5 Total Wells Drilled & Completed

― 1,200 BOEPD (87% Oil) Avg. 24 Hour IP

― 720 BOEPD Avg. 30 Day Rate**

― 550 BOEPD Avg. 60 Day Rate**

― 3,800’ Avg. Lateral Length

• 6 Wells in Various Stages of Completion

Pressured Uteland Butte*

• 35 Total Vertical Wells to Date

― 900 BOEPD (87% Oil) Avg. 24 Hour IP

― 400 BOEPD Avg. 30 Day Rate

― 275 BOEPD Avg. 60 Day Rate

― 250 BOEPD Avg. 90 Day Rate

• 2 HZT Wells Drilled & Completed

― 1,200 BOEPD (88% Oil) Avg. 24 Hour IP

― 900 BOEPD Avg. 30 Day Rate

― 750 BOEPD Avg. 60 Day Rate

― 625 BOEPD Avg. 90 Day Rate

― ~3,200’ Avg. Lateral Length

Wasatch Wells*

Key Takeaways• 230,000 Net Acres

• Gross Production Approximately 39,000 BOEPD

Monument

Butte

Central Basin

*Gross 24-hour rates

** Includes 4 wells 11

12

PeriodVolume Hedged

MMCF/D

Weighted-Average

Fixed Price

Value @

$2 / MMBtu

Value @

$3 / MMBtu

Value @

$4 / MMBtu

4Q ‘12 287 $3.65 $44MM $18MM ($11MM)

2013 271 $4.29 $235MM $136MM $29MM

2014 240 $3.86 $163MM $75MM ($7MM)

2015 60 $4.03 $44MM $23MM $3MM

Period

Volume Hedged

BOPD

Weighted-Average

Fixed Price

Value @

$80 / Bbl

Value @

$90 / Bbl

Value @

$100 / Bbl

Value @

$110 / Bbl

4Q ‘12 35,000 $82.96 $8MM $6MM ($2MM) ($22MM)

2013 35,700 $94.55 $190MM $59MM ($10MM) ($32MM)

2014 21,000 $92.87 $99MM $22MM ($29MM) ($55MM)

* See @NFX on Newfield Website for Detailed Hedging Position

13

This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933,as amended, and Section 21E of the

Securities Exchange Act of 1934, as amended. The words “will”, “believe”, “intend”, “plan”, “expect” or other similar e xpressions are intended to identify

forward-looking statements. Other than historical facts included in this presentation, all information and statements, such as information regarding

estimated reserves, production targets, drilling and development plans and the timing of production and other activities, planned capital expenditures, the

availability of capital resources to fund capital expenditures and other plans and objectives for future operations, are forward-looking statements. Although

as of the date of this presentation Newfield believes that these expectations are reasonable, this information is basedupon assumptions and anticipated results

that are subject to numerous uncertainties and risks. Actual results may vary significantly from those anticipated dueto many factors, including drilling

results, oil and gas prices, industry conditions, the prices of goods and services, the availability of drilling rigs and other support services, the availability of

refining capacity for the crude oil Newfield produces in the Uinta Basin in Utah, the availability of capital resources, labor conditions, severe weather

conditions, governmental regulations and other operatingrisks. Please see Newfield’s 2011 Annual Report on Form 10-Kand subsequent Quarterly Reports

on Form 10-Q filed with the U.S. Securities and Exchange Commission (SEC) for a discussion of other factors that may causeactual results to vary.

Unpredictable or unknown factors not discussed herein or inNewfield’s SEC filings could also have material adverse effects on forward-looking statements.

Readers are cautioned not to place undo reliance on forward-looking statements, which speak only as of the date of this presentation. Unless legally required,

Newfield undertakes no obligation to publicly update or revise any forward-looking statements.

Cautionary Note to Investors – Effective January 1, 2010, the SEC permits oil and gas companies, in their filings with theSEC, to disclose only proved,

probable and possible reserves that meet the SEC’s definitions for such terms. Newfield may use terms in this presentation, such as “resources”, “net

resources”, “net discovered resources”, “net risked resources”, “net lower-risked captured resources”, “net risked captured resources”, “gross resources”,

“gross resource potential”, “gross unrisked resource potential”, “gross unrisked resources”, and similar terms that the SEC’s guidelines strictly prohibit in

SEC filings. Investors are urged to consider closely the oiland gas disclosures in Newfield’s 2011 Annual Report on Form10-K, available at

www.newfield.com, www.sec.govor by writing Newfield at 4 Waterway Square Place, Suite 100, The Woodlands, Texas 77380 Attn: Investor Relations.