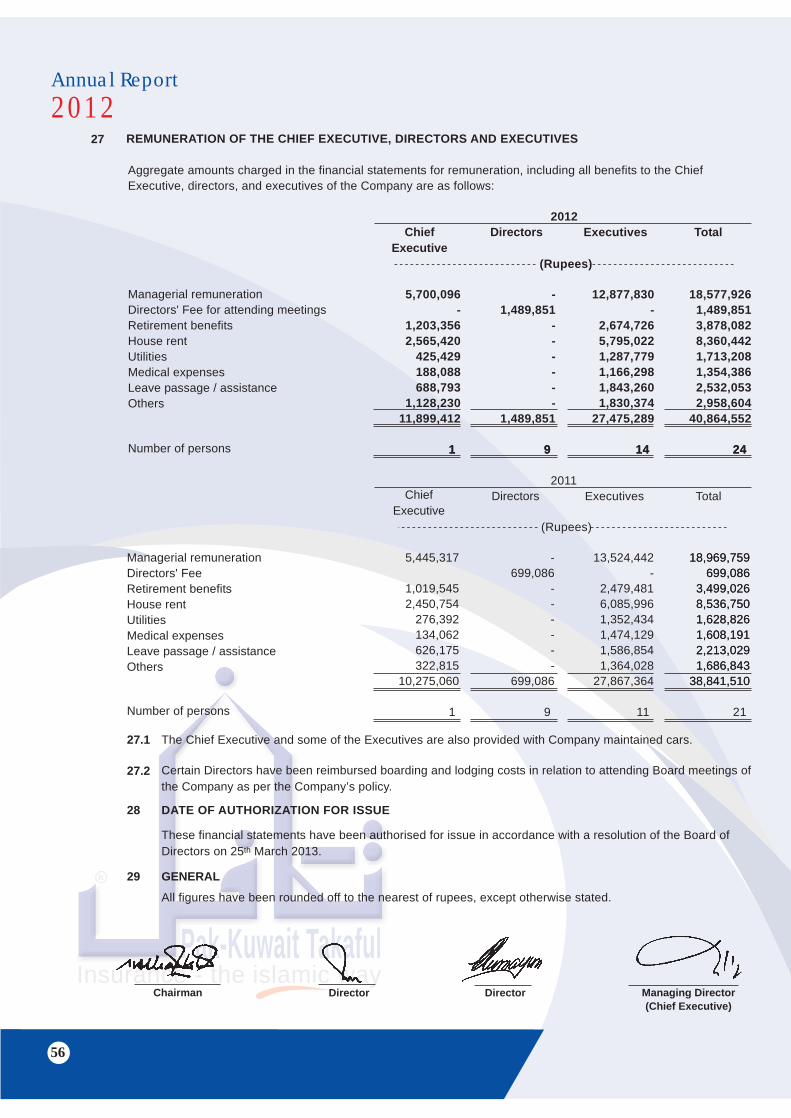

JCR-VIS Reaffirms ‘A-‘ Financial Strength Rating … REPORT-12.pdfPak-Kuwait Takaful Insurance -...

56

Pak-Kuwait Takaful Insurance - the islamic way R Annual Report 2012 17 JCR-VIS Reaffirms ‘A-‘ Financial Strength Rating With “Stable” Outlook Pak-Kuwait Takaful Insurance - the islamic way R

Transcript of JCR-VIS Reaffirms ‘A-‘ Financial Strength Rating … REPORT-12.pdfPak-Kuwait Takaful Insurance -...

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

17

JCR-VISReaffirms

‘A-‘ FinancialStrength RatingWith “Stable”

Outlook

Pak-Kuwait TakafulInsurance - the islamic way

R

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

2

PKTCL ANNUAL SALES CONFERENCE-2013

From left to Right, M. Iftekhar Ahmed, Chief Operating Officer,Mr. Imtiaz Bhatti, MD & CEO,

Syed Wajahatullah Quadri, Chief Financial Officerand Syed Waqar Azeem, Head of Marketing & Sales.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

3

Mr. IMTIAZ BHATTIManaging Director & Chief ExecutivePak-Kuwait Takaful Company Limited

is receiving the “BRANDS OF THE YEAR AWARD-2011”from

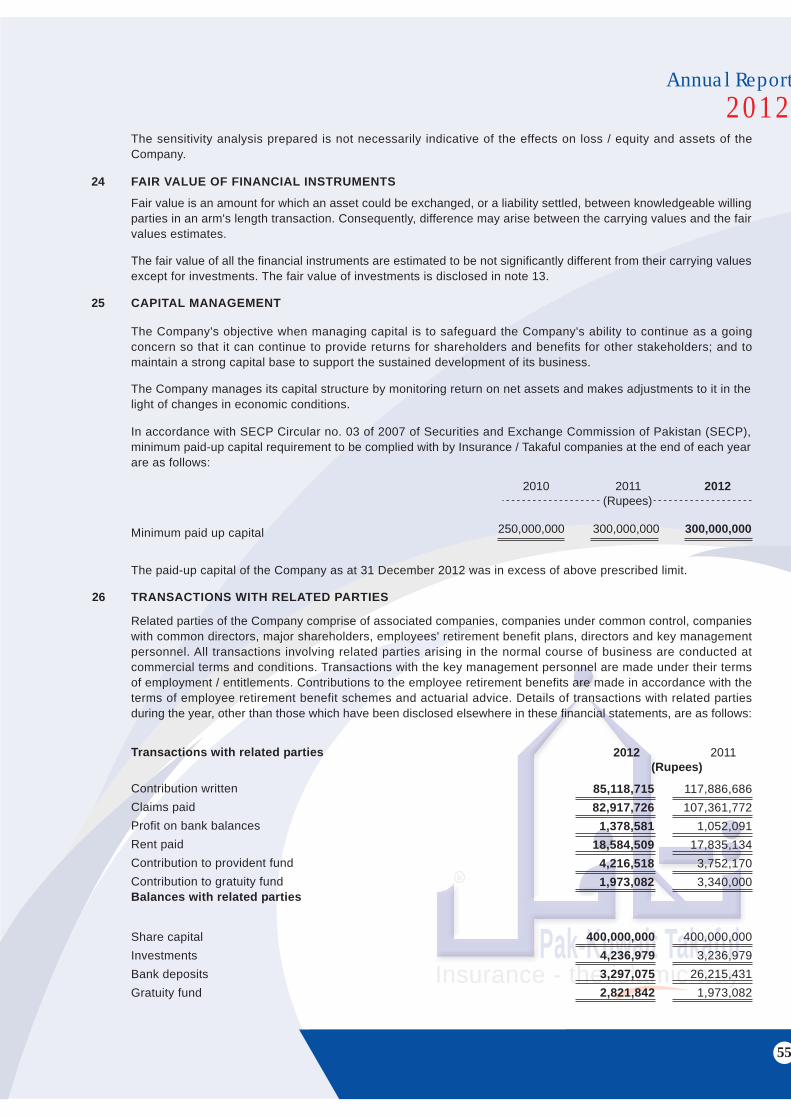

Mr. Abdul Hafeez Shaikh,Federal Minister Finance, Islamic Republic of Pakistan

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

04

MISSION

To promote Takaful as a viable alternative to conventional insuranceTo be the trend-setter in excellent service standards and highest businessethicsTo provide a congenial work environment to our employees that keepsthem motivated and brings out their bestTo contribute positively and proactively for the welfare of our society atlarge as well as for the preservation of our environment

VISION

To be acknowledged as the synonym for Takaful in Pakistan

Takaful

Pak-Kuwait TakafulInsurance - the islamic way

R

37

Annual Report2012

Contents

Corporate information

Board Committees

Management Team

Director’s Report

Shariah Report

Statement of Compliance with the Code of Corporate Governance

Review Report to the Members

Auditor’s Report to the Members

Balance Sheet

Profit & Loss Account

Statement of Comprehensive Income

Statement of Cash Flows

Statement of Changes in Equity

Statement of Contribution

Statement of Claims

Statement of Expenses

Statement of Investment Income

Notes to the Financial Statements

06

07

08

09

14

15

17

18

20

22

23

24

26

27

28

29

30

31

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

06

CORPORATE INFORMATION

Chairman of the Board of Directors

Directors

Managing Director & Chief Executive

Company Secretary

Shariah Supervisory Board

Auditors

Legal Advisor

Head office

Datuk Syed Othman Bin Syed Husin Alhabshi

Shaharyar AhmadRana Ahmed HumayunOsman KassimIrfan SiddiquiAhmad Shahril Azuar JiminFozia FakharMohd Nasir Bin HarunTalal B A KH Al-Mesallam

Imtiaz Ahmed Bhatti

Aziz T. Kapadia

Muhammad Taqi Usmani ChairmanDr. Muhammad Imran Ashraf Usmani MemberMuhammad Hassan Kaleem Member

KPMG Taseer Hadi & Co.Chartered Accountants

Sattar & SattarAttorneys at Law

Finance & Trade Centre, 4th Floor, Block-AShhrah-e-Faisal, Karachi-74400. PakistanUAN : 111-121-131Tel : 35630707 (10 Lines)Fax : 35630699E-mail : [email protected] : www.pktcl.com

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

07

BOARD COMMITTEES

Audit Committee

Human Resource Committee

Underwriting Committee

Claims Committee

Re-Takaful Committee

Osman Kassim ChairmanDatuk Syed Othman Bin Syed Husin Alhabshi MemberRana Ahmed Humayun MemberTalal B A KH Al-Mesallam MemberAziz T. Kapadia Secretary

Talal B A KH Al-Mesallam ChairmanMohd Nasir Bin Harun MemberImtiaz Ahmed Bhatti MemberAziz T. Kapadia Secretary

Ahmad Shahril Azuar Jimin ChairmanImtiaz Ahmed Bhatti MemberAziz T. Kapadia Secretary

Ahmad Shahril Azuar Jimin ChairmanImtiaz Ahmed Bhatti MemberAziz T. Kapadia Secretary

Datuk Syed Othman Bin Syed Husin Alhabshi ChairmanImtiaz Ahmed Bhatti MemberM. Iftekhar Ahmed MemberAziz T. Kapadia Secretary

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

08

MANAGEMENT TEAM

Managing Director & Chief Executive

Chief Operating Officer

Chief Financial Officer

Head of Marketing & Sales

Assistant General Manager

Senior Manager

Managers

Branch Heads

Imtiaz Ahmed Bhatti

M. Iftekhar Ahmed

Syed Wajahatullah Quadri

Syed Waqar Azeem

Aziz T. Kapadia

M. Waqaruddin Rauf

M. Tariq DaraShahnawaz AkhtarM. Elahi IbrahimSaquib Obaid-ur-RehmanParvez RajaniAbdul Waheed Tariq

Mian Allah Nawaz (Lahore)Abdul Haleem Mughal (Islamabad)Malik Farooq Mustafa (Faisalabad)Rana Abdul Hameed (AGM Sales-Multan)

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

09

DIRECTORS’ REPORT

The Directors are pleased to present Annual Report and Audited Accounts for the year ended December 31, 2012.

ECONOMIC OVERVIEW

The Pakistan economy has endured several challenges to achieve economic stability. The current year is displayingsigns of improvement despite being faced with various regional and domestic challenges. However, themacroeconomic conditions weakened during 2012 despite improvement in current account deficit and workers’remittances. CPI inflations softened to 6.9% by November-2012, the lowest in the last four years which gave StateBank of Pakistan space to cut policy rates by 250bps. Real GDP is expected to rise to 4% in FY13 from 3.7% inFY12 while the Current Account reflected a surplus after the release of US $ 1.8 billion towards Coalition SupportFund. There are improvements in business confidence and the KSE 100 Index has rallied 49% in 2012 makingit one of the world’s best performing equity markets for the period. Similarly, the manufacturing sector grew by3.6% (FY-201: 3.1%) and services sector grew by 4% (FY-2011: 4.4%) in FY-2012. The growth in the non-lifeinsurance sector over last year remained stagnant at around 10%.

PERFORMANCE

PARTICIPANTS’ TAKAFUL FUND

During the year 2012, by the grace of Allah (SWT), your Company has achieved a business growth of 12%. Thegross contribution during the year stands increased from Rs. 642 million to Rs. 720 million, recording a growthof 12% over the corresponding year. The business mix has also improved during the year. The share of non motorbusiness in total has increased from 50% in 2011 to 54% in 2012 diluting thereby the share of motor businessfrom 50% in 2011 to 46% in 2012. The Company is gradually moving towards further improving the share ofmarine, fire and other business in the Company’s portfolio.

Net contribution revenue earned during the year amounted to Rs. 306 million as compared to Rs. 266 millionearned during 2011. Net investment & other income of the Fund at the close of the year was Rs. 3 million. Netclaims, expenses, commission and contribution deficiency reserve during the year amounted to Rs. 350 millionas compared to Rs. 300 million during last year. As such the Fund ended up with a deficit of Rs. 40 million during2012 as against a deficit of Rs. 33 million in the previous year. Softening of contribution (premium) rates coupledwith deteriorating law and order situation have led to increased pressure on the PTF results. The increasedincidents of Theft/Snatching claims arising out of Motor business have worsened the PTF results in absolute termsfollowing an increase in the prices of motor vehicles due to inflation during 2012.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

10

SHAREHOLDERS’ FUND

Total income of the shareholders’ fund during 2012 amounted to Rs. 263 million as compared to Rs. 238 millionduring previous year. General, administration and other expense during the year were Rs. 202 million as comparedto Rs. 189 million during 2011. Profit before taxation is recorded at Rs. 61 million as compared to Rs. 49 millionin 2011. The retained earnings accumulated to Rs. 145 million against opening of Rs. 90 million.

EARNINGS PER SHARE

The Company has reported earnings per share of Rs. 1.38 in 2012 as compared to earnings per share ofRs. 1.07 in 2011.

CREDIT RATING

The Company has been successfully able to retain and maintain A- (A minus) rating from the Credit Rating AgencyJCR-VIS despite tougher business conditions. During the year 2012, the rating agency has reaffirmed A- (A minus)with stable outlook.

BOARD MEETINGS

In 2012 the Board of Directors held four (4) meetings, at least one meeting was held in each quarter. The attendancerecord of the Directors is as follows:

Name of Director AttendanceDr. Datuk Syed Othman Bin Syed Husin Alhabshi 4 Mr. Shaharyar Ahmad 0 (Appointed on December 06, 2012)Mr. Rana Ahmed Humayun 4Mr. Irfan Siddiqui 3Mr. Osman Kassim 3Mr. Ahmad Shahril Azuar Jimin 2Mr. Mohd Nasir Bin Harun 4Ms. Fauzia Fakhar 4Mr. Suleman Shah 1 (Resigned on May 14, 2012)Mr. Muhammad Tauseef Ansari 4 (Resigned on December 06, 2012)Mr. Talal B A KH Al-Mesallam 3 (Appointed on May 14, 2012)Mr. Imtiaz Bhatti 4

During the year, Mr. Suleman Shah and Mr. Tauseef Ansari (Directors) resigned from the Board and Mr. Talal BA KH Al-Mesallam and Mr. Shaharyar Ahmad were appointed as Directors of the Company. The Board wishesto place on record its appreciation of the services rendered by Mr. Suleman Shah and Mr. Tauseef Ansari. TheBoard also welcomes the new members and looks forward to their valuable contribution and guidance.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

11

Statement of Directors’ Responsibilities:

In compliance with the Corporate and Financial Reporting Framework under the Code ofCorporate Governance, the Directors confirm the following:- The Financial Statement, prepared by the Company, fairly present its state of affairs, theresult of its operations, cash flows and changes in equity.- Proper books of accounts of the Company have been maintained.- Appropriate accounting policies have been consistently applied in preparation of FinancialStatements except as fully disclosed in the audited accounts, if any, and accounting estimatesare based on reasonable and prudent judgment.- International Accounting Standards, as applicable in Pakistan have been followed in thepreparation of financial statements and departure, if any, there from has been adequatelydisclosed.- The system of internal control is sound in design and has been effectively implementedand monitored.- There are no significant doubts upon the Company’s ability to continue as a goingconcern.- There is no material departure from the best practices of corporate governance.

Key Financial Data:

Key financial data for the last six years is summarized below: PKR ‘000

Paid up capitalTotal AssetsGross contribution revenueNet contribution revenueWakala FeeMudarib ShareInvestment Income:Participants FundShare Holders FundProfit/(loss) after taxation:Participants FundShare Holders FundEarnings per share (Rs.)

400,000 664,268 720,406 306,416 226,928

837

2,511 33,970

(39,759 55,404 1.38

)

400,000 681,037 642,246 266,026 202,308 359

1,499 35,407

(32,694 42,895

1.07

)

400,000 606,714 535,258 239,644 187,340

635

1,904 39,370

(76,327 59,000 1.47

)

400,000528,760438,815159,952153,585 203

610 19,467

(67,760 10,151

0.41

)

250,000348,921342,240143,043119,784

695

558 11,225

(59,616 1,707

0.07

250,000409,089260,222106,340 91,078 1,096

3,288 17,418

(49,317 1,345

0.05

)) ))

2012 2011 2011 2009 2008 2007

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

12

Pattern of Shareholding:

The information on pattern of shareholding as at December 31, 2012 is as follows:

13,000,000

12,000,000

6,000,000

4,000,000

2,500,000

2,500,000

No. of Shares

32.5

30.0

15.0

10.0

6.25

6.25

%Name of Shareholders

Etiqa Overseas Investment Pte. Ltd. Malaysia

Pakistan Kuwait Investment Co.(Private) Ltd.

Noor Financial Investment Co. Kuwait

Saudi Pak Industrial & Agricultural Investment Co.(Pvt) Ltd.

Takaful Holdings Ltd. Dubai

Meezan Bank Ltd.

Value of investments in Provident Fund and Gratuity Fund:

The value of investment in employees retirement funds based on audited accounts for the year endedDecember 31, 2011 is as follows.

Employees Provident Fund 23,646,679

Employees Gratuity Fund 7,814,329

PKR

Auditors:

M/S. KPMG, Taseer Hadi & Co. Chartered Accountants have audited the accounts for the year ended December31, 2012 and have offered themselves for reappointment for the year ending December 31, 2013. The Board AuditCommittee recommends their reappointment and the Board endorses the recommendation.

FUTURE OUTLOOK

While the country is heading for election this year, there has been an increased spending of development fundsby the government which will eventually raise demands for Takaful. The Energy Crisis will continue to be a majorchallenge; the government has taken appropriate long-terms step by signing and inaugurating the Pak-Iran GasLine Project and Sindh Thar Coal-II Project.

Despite the challenging internal environment, we believe opportunities exist and intend to follow a prudent growthstrategy at the back of our brand equity strength, effective risk management practices and unique TakafulLeader’s capabilities. In line with the strategic priorities, PKTCL will continue to focus on deepening marketpenetration in non-motor segments and further improve customer service and engagement. With the key enablers

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

13

well in place, we are confident that execution of our focused Business Plan should lead us to sustained growthboth in terms of Company’s revenues and profitability.

ACKNOWLEDGEMENT:

We thank our valued clients and the shareholders for their continuous support. We are also thankful to ourexecutives, staff members and marketing/sales force for putting in committed efforts for business developmentand growth of the Company. May Allah Almighty bestow His blessings on them and their families!

We are also grateful to our Retakaful Operators for their valuable professional services. We would like to recordour appreciation for the cooperation to us by the Regulators, Securities and Exchange Commission of Pakistanand the State Bank of Pakistan.

For and on behalf of the Board of Directors.

Karachi: March 25, 2013. Chairman

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

14

Muhammad Hassaan Kaleem(Member Shariah Board)

Karachi : 19thMarch, 2013

Shariah Report

Overview

By the Grace of Allah, December 31, 2012 was the seventh complete year of operations for Pak-Kuwait Takaful Company Limited. During the year the Company executed variety of establishedTakaful transactions after due approval from Shariah Supervisory Board. The Company is offering Shariah Compliantservices in the following areas:

V Fire and Property TakafulV MarineV MotorV Miscellaneous

The Company invests its funds with the approval of Shariah Supervisory Board in ShariahCompliant Instruments.

Conclusion & Recommendations

The services provided by the Company were reviewed on random basis and activities andtransactions undertaken by the Company during the year ended on December 31, 2012 werefound in conformity with the Principles and guidelines of Islamic Shariah, issued and providedby Shariah Supervisory Board of the Company. However, the following is recommended:

Nacessary steps should be taken to develop Shariah training program in order to educatethe staff about the very concept of Takaful and Shariah requirements of its practice.

Internal Shariah Department with knowledge and dedicated staff should be instigatedunder the supervision of SSB to help the management in assuring Shahriah compliance atall levels of the operation.

May Allah bless us with the best Tawfeeq to accomplish these cherished tasks and bestow uswith success in this world and in the world hereafter, and forgive us for our mistakes.

Wassalam Alaikum Wa Rehmat Allah Wa Barakatuh.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

15

PAK-KUWAIT TAKAFUL COMPANY LIMITEDSTATEMENT OF COMPLIANCE WITH THE BEST PRACTICES OFTHE CODE OF CORPORATE GOVERNANCE

FOR THE YEAR ENDED 31 DECEMBER 2012This statement is being presented to comply with the Code of Corporate Governance (the Code)for Insurance Companies / Takaful Operators for the purpose of establishing a framework of good governance,whereby Insurance Company / Takaful Operator is managed in compliance with the best practices ofcorporate governance.

The Company has applied the principles contained in the Code in the following manner:

1. The directors have confirmed that none of them is serving as a director in more than ten listed companies.

2. All the resident directors of the Company are registered as taxpayers and none of them has defaulted inpayment of any loan to a banking Company, a DFI or NBFC or, being a member of a stock exchange, hasbeen declared as a defaulter by that stock exchange.

3. During the year, two causal vacancies occurred in Board of Directors which has been filled within theprescribed time limit by the Board.

4. The Company has prepared a ‘Statement of Ethics and Business Practices’ which has been signed byall the directors and employees of the Company.

5. The Board has developed a vision/mission statement, overall corporate strategy and significant policiesof the Company. A complete record of particulars of significant policies along with the dates on which theywere approved or amended has been maintained.

6. All the powers of the Board have been duly exercised and decisions on material transactions, includingappointment and terms and conditions of employment of the CEO have been taken by the Board.

7. The meetings of the Board were presided by the Chairman and in his absence by a director elected bythe Board for this purpose and the Board met at least once in every quarter. Written notices of the Boardmeetings, along with agenda and working papers, were circulated at least seven days before the meetings.The minutes of the meetings were appropriately recorded and circulated.

8. The Board has established a system of sound internal control, which is effectively implemented at alllevels within the Company. The Company has adopted all necessary aspects of internal control given inthe Code.

9. Directors are well conversant with the legal requirements and operational imperatives of the company andas such fully aware of their duties and reponsibilities. Regular update on corporate requirements is takencare of.

10. During the year, the Board has approved appointment of CFO. No vacancy arises in the position ofCompany Secretary / Head of Internal Audit during the year. Remuneration and terms and conditions oftheir employment are determined by CEO.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

16

11. The Directors Report for this year has been prepared in compliance with the requirements of the Codeand fully describes the salient matters required to be disclosed.

12. The financial statements of the Company were duly endorsed by the CEO and CFO before approval ofthe Board.

13. The Directors, CEO and Executives do not hold any interest in the shares of the Company other than thatdisclosed in the pattern of shareholding.

14. The Company has complied with all the corporate and financial reporting requirements of the Code.

15. The Board has formed an under writing, claim settlement, retakaful & co-takaful committee.

16. The Board has formed an audit committee comprising four members all of whom are non-executivedirectors including the chairman of the committee.

17. The meetings of the Audit Committee were held at least once every quarter prior to approval of interimand final results of the Company and as required by the Code. The terms of reference of the Committeehave been formed and advised to the Committee for compliance.

18. The Board has setup an effective internal audit function which is fully conversant with the policies andprocedures of the Company

19. The statutory auditors of the Company have confirmed that they have been given a satisfactory ratingunder the quality control review program of the Institute of Chartered Accountants of Pakistan, that theyor any of the partners of the firm, their spouses and minor children do not hold shares of the Companyand that the firm and all its partners are in compliance with International Federation of Accountants (IFAC)guidelines on Code of ethics as adopted by Institute of Chartered Accountants of Pakistan.

20. The statutory auditors or the persons associated with them have not been appointed to provide otherservices except in accordance with the listing regulations and the auditors have confirmed that they haveobserved IFAC guidelines in this regard.

21. We confirm that all other material principles contained in the Code have been complied with exceptotherwise stated.

Managing Director & Chief Executive OfficerDate: 25 March 2013

R

17

Review Report to the Members on Statement of Compliance

with Best Practices of Code of Corporate Governance

We have reviewed the Statement of Compliance with the Code of Corporate Governance (the Statement) prepared

by the Board of Directors of Pak-Kuwait Takaful Company Limited (”the Company”) to comply with the best

practices of Code of Corporate Governance.

The responsibility for compliance with the Code is that of the Board of Directors of the Company. Our responsibility

is to review, to the extent where such compliance can be objectively verified, whether the Statement reflects the

status of the Company’s compliance with the provisions of the Code and report if it does not. A review is limited

primarily to inquiries of the Company personnel and review of various documents prepared by the Company to

comply with the Code.

As part of our audit of financial statements we are required to obtain an understanding of the accounting and

internal control systems sufficient to plan the audit and develop an effective audit approach. We have not carried

out any special review of the internal control system to enable us to express an opinion as to whether the Board’s

statement on internal control covers all controls and the effectiveness of such internal controls.

Based on our review, nothing has come to our attention, which causes us to believe that the Statement does not

appropriately reflect the Company’s compliance, in all material respects, with the best practices contained in the

Code as applicable to the Company, for the year ended 31 December 2012.

Date: 25 March 2013Karachi

KPMG Taseer Hadi & Co.Chartered Accountants

KMPG Taseer Hadi & Co.Chartered AccountantsSheikh sultan Trust Building No. 2beaumont RoadKarachi, 75530 Pakistan

Telephone + 92 (21) 3568 5847Fax + 92 (21) 3568 5095Internet www.kpmg.com.pk

KPMG Taseer Hadi & Co., a Partnership firm registered in Pakistanand a member firm of the KPMG network of independent memberfirms affilated with KPMG International Cooperative(“KPMG International”), a Swiss entity.

18

Auditors’ Report to the Members of Pak-Kuwait Takaful Company Limited

We have audited the annexed financial statements comprising of:

(i) balance sheet ;(ii) profit and loss account ;(iii) statement of comprehensive income(iv) statement of changes in equity;(v) statement of cash flows;(vi) statement of contributions;(vii) statement of claims;(viii) statement of expenses; and

(ix) statement of investment income

of Pak-Kuwait Takaful Company Limited (”the Company”) as at 31 December 2012 togetherwith the notes forming part thereof , for the year then ended.

It is the responsibility of the Company’s board of Directors to establish and maintain a systemof internal control, and prepare and present the financial statements in conformity with the approvedaccounting standards as applicable in Pakistan and the requirements of the Insurance Ordinance,2000 (XXXIX of 2000) and the Companies Ordinance, 1984 (XL VII of 1984). Our responsibility isto express an opinion on these statements based on our audit.

We conducted our audit in accordance with the International Standards on Auditing as applicablein Pakistan. Those standards require that we plan and perform the audit to obtain reasonableassurance about whether the financial statements are free of material misstatement. An audit includesexamining, on a test basis, evidence supporting the amounts and disclosures in the financialstatements. An audit also includes assessing the accounting policies used and significant estimatesmade by management, as well as, evaluating the overall financial statements presentation. Webelieve that our audit provides a reasonable basis for our opinion.

In our opinion:

a) proper books of account have been kept by the Company as required by the InsuranceOrdinance, 2000;

b) the financial statements together with the notes thereon have been drawn up in conformitywith the Insurance Ordinance, 2000 and the Companies Ordinance, 1984, and accuratelyreflect the books and records of the Company and are further in accordance withaccounting policies consistently applied;

KMPG Taseer Hadi & Co.Chartered AccountantsSheikh sultan Trust Building No. 2beaumont RoadKarachi, 75530 Pakistan

Telephone + 92 (21) 3568 5847Fax + 92 (21) 3568 5095Internet www.kpmg.com.pk

KPMG Taseer Hadi & Co., a Partnership firm registered in Pakistanand a member firm of the KPMG network of independent memberfirms affilated with KPMG International Cooperative(“KPMG International”), a Swiss entity.

19

KPMG Taseer Hadi & Co.

c) the financial statments together with the notes thereon present fairly, in all material respects, the state ofthe Company’s affairs as at 31 December 2012 and of its financial performance, cash flows and changesin equity for the year then ended in accordance with approved accounting standards as applicable inPakistan, and give the information required to be disclosed by the Insurance Ordinance, 2000 and theCompanies Ordinance, 1984; and

d) no Zakat was deductible at source under the Zakat and Ushr Ordinance, 1980.

Date : 25 March 2013

Karachi

KPMG Taseer Hadi & Co.Chartered AccountantsMohammad Nadeem

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

20

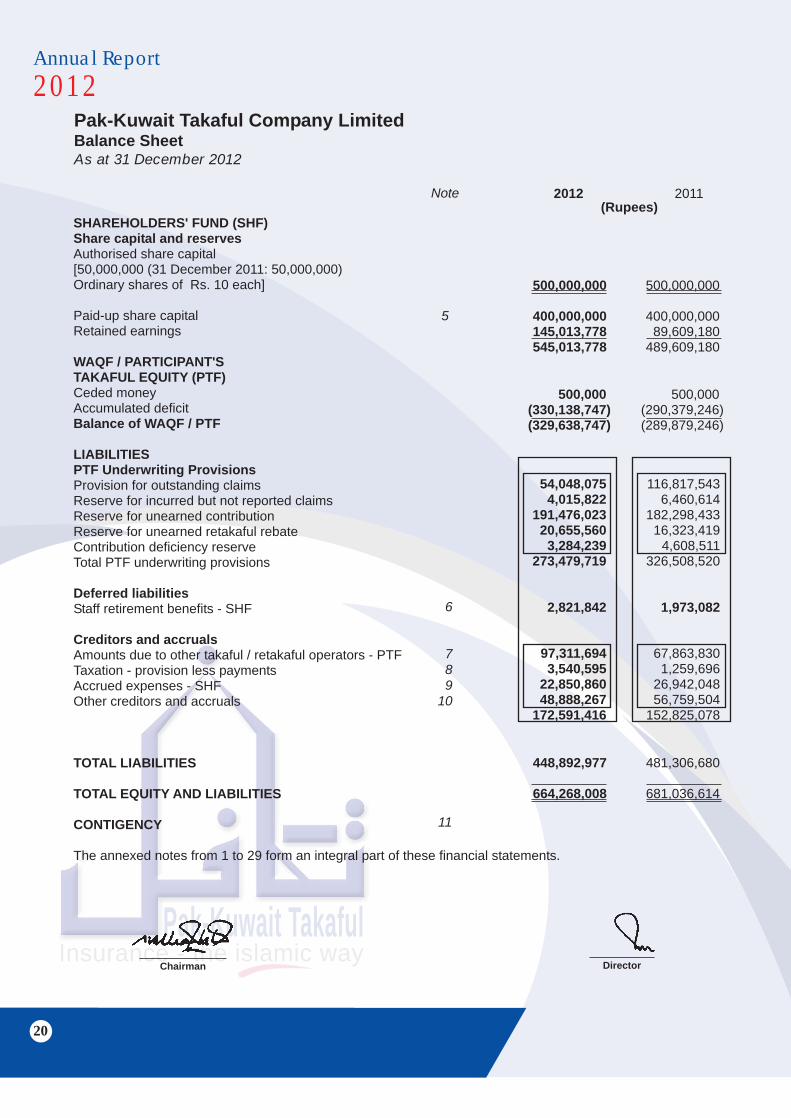

Pak-Kuwait Takaful Company LimitedBalance SheetAs at 31 December 2012

Chairman Director

SHAREHOLDERS' FUND (SHF)Share capital and reservesAuthorised share capital[50,000,000 (31 December 2011: 50,000,000)Ordinary shares of Rs. 10 each]

Paid-up share capitalRetained earnings

WAQF / PARTICIPANT'STAKAFUL EQUITY (PTF)Ceded moneyAccumulated deficitBalance of WAQF / PTF

LIABILITIESPTF Underwriting ProvisionsProvision for outstanding claimsReserve for incurred but not reported claimsReserve for unearned contributionReserve for unearned retakaful rebateContribution deficiency reserveTotal PTF underwriting provisions

Deferred liabilitiesStaff retirement benefits - SHF

Creditors and accrualsAmounts due to other takaful / retakaful operators - PTFTaxation - provision less paymentsAccrued expenses - SHFOther creditors and accruals

TOTAL LIABILITIES

TOTAL EQUITY AND LIABILITIES

CONTIGENCY

The annexed notes from 1 to 29 form an integral part of these financial statements.

6

789

10

11

500,000)(330,138,747)(329,638,747)

500,000)(290,379,246)(289,879,246)

97,311,6943,540,595

22,850,86048,888,267

172,591,416

67,863,8301,259,696

26,942,04856,759,504

152,825,078

481,306,680

681,036,614

448,892,977

664,268,008

500,000,000

400,000,000145,013,778545,013,778

500,000,000

400,000,00089,609,180

489,609,180

2012(Rupees)

2011

5

Note

54,048,0754,015,822

191,476,02320,655,560

3,284,239273,479,719

2,821,842

116,817,5436,460,614

182,298,43316,323,419

4,608,511326,508,520

1,973,082

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

21

Pak-Kuwait Takaful Company LimitedBalance SheetAs at 31 December 2012

Contribution due but unpaid -PTFAmounts due from other takaful / retakaful operator -PTFSalvage recoveries accrued -PTFAccrued investment incomeRetakaful recoveries against outstanding claims -PTFDeferred commissionexpense -PTFPrepaymentsSundry receivables - SHF

ASSETSCash and bank depositsCash and other equivalentsCurrent and other accountsDeposits maturing within 12 months

Furniture and fixturesOffice equipmentMotor vehiclesComputersComputer software

Investments

Current assets - other

Fixed assets - SHFTangible and intangible

TOTAL ASSETS

402,8587,314,678

228,944,063236,661,599

126,51326,330,269

231,142,100257,598,882

56,870,735

195,249,896

2,382,7803,229,662

378,108

6,736,928

21,446,62686,520,97313,505,387

329,450,360

178,253,691

12,551,45612,475,526

669,339

35,947,162

22,625,01965,618,059

8,644,468336,784,720

13,773,4882,483,618

11,264,821765,552

-28,287,479

16,814,5542,862,8518,994,339

935,403175,130

29,782,277

664,268,008 681,036,614

13

12

14

1516

17

Managing Director(Chief Executive)

Director

Note 2012(Rupees)

2011

69,868,570

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

22

Pak-Kuwait Takaful Company LimitedProfit and Loss AccountFor the year ended 31 December 2012

Chairman Director Director Managing Director(Chief Executive)

Note

PTF Revenue account

Net contributionNet claimsDirect expensesNet commission

18

Reversal / (charge) of contributiondeficiency reserveDeficit before investment income

Net investment incomeOther IncomeDeficit for the year

Accumulated deficit:Balance at commencement of the yearDeficit for the yearBalance of accumulated deficit at end of the year

SHF Revenue account

Wakala feeManagement expenses 19

Mudarib's share of PTF investment incomeNet investment incomeOther income

Profit and loss appropriation account:Balance at commencement of the yearProfit for the yearBalance unappropriated profit at end of the year

20General and administrative expensesProfit before taxationTaxation - currentProfit for the year

21

The annexed notes from 1 to 29 form an integral part of these financial statements.

Fireand

property

Marine,aviation and

transport

Motor Miscellaneous AggregateAggregate20112012

(Rupees)

39,180,230(29,026,866)

(2,692,202) 9,199,32616,660,488

36,578,366 (13,018,901)

(834,889)(2,171,949)

20,552,627

212,425,628(216,493,112)(56,053,366)(14,568,584)(74,689,434)

18,231,742(23,241,838)

(432,557)(1,392,667)(6,835,320)

306,415,966(281,780,717)

(60,013,014)(8,933,874)

(44,311,639)

266,025,805(225,945,650)

(65,138,252)(14,855,684)(39,913,781)

1,468,402(73,221,032)

(144,130)(6,979,450)

1,324,272(42,987,367)

5,720,703(34,193,078)

-16,660,488

-20,552,627

2,511,422 716,444 (39,759,501)

1,498,629-

(32,694,449)

(257,684,797)(32,694,449)

(290,379,246)

(290,379,246)(39,759,501)

(330,138,747)

202,307,548(129,910,861) 72,396,687

226,928,077(140,681,581)

86,246,496

837,141 33,970,108 919,463121,973,208 (61,021,023) 60,952,185 (5,547,587)

55,404,598

89,609,18055,404,598

145,013,778

359,334 35,407,433 200,714108,364,168(59,046,246)

49,317,922 (6,422,462) 42,895,460

46,713,72042,895,460

89,609,180

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

Chairman Director Director Managing Director(Chief Executive)

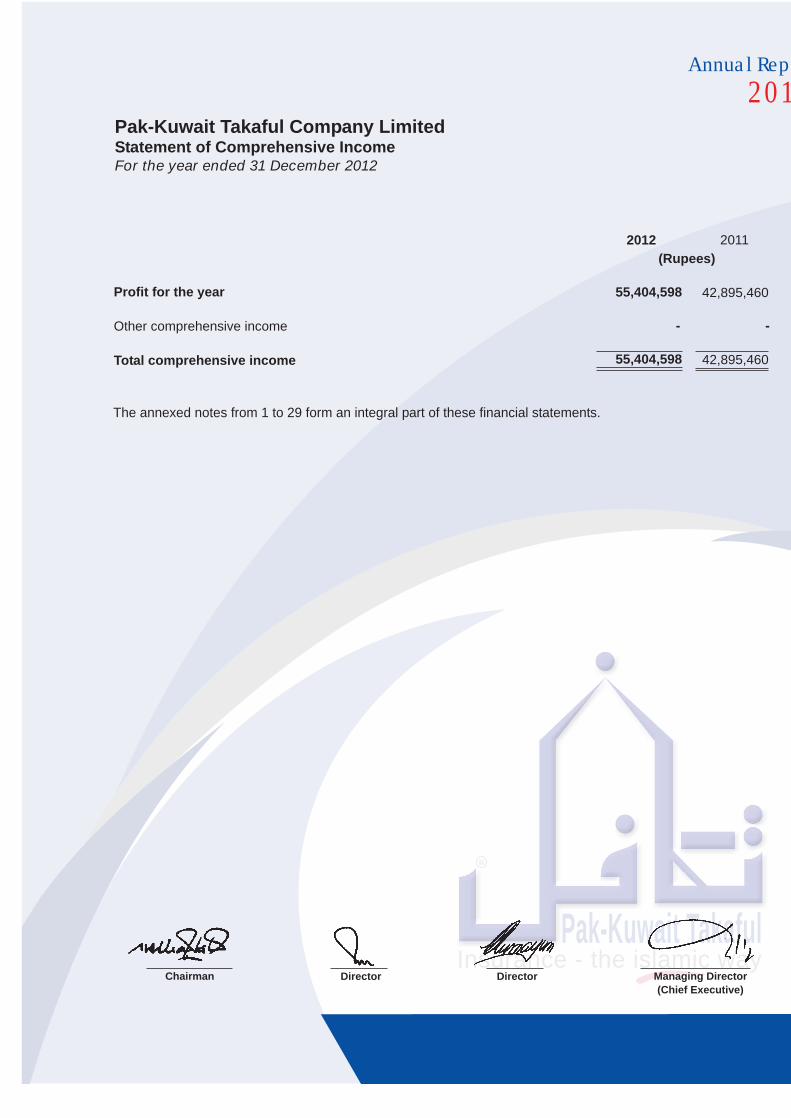

Pak-Kuwait Takaful Company LimitedStatement of Comprehensive IncomeFor the year ended 31 December 2012

Profit for the year

Other comprehensive income

Total comprehensive income

The annexed notes from 1 to 29 form an integral part of these financial statements.

55,404,598

2012(Rupees)

- -

2011

42,895,460

55,404,598 42,895,460

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

24

Pak-Kuwait Takaful Company LimitedStatement of Cash FlowsFor the year ended 31 December 2012

Operating cash flows

(a) Takaful activities Contribution received Retakaful ceded Claims paid Re-takaful and other recoveries received Commission paid Re-takaful rebate received Other takaful related payments Net cash inflows from takaful activities

(b) Other operating activities Income tax paid General, administration and management expenses paid Other operating receipts - net Net cash (outflows) from other operating activities

Total cash outflows from operating activities

Investment activitiesProfit / return receivedPayments for investmentsProceeds from disposal of investmentsFixed capital expenditureProceeds from disposal of fixed assetsTotal cash inflows from investing activities

Net cash outflows from all activities

Cash at beginning of the year

Cash at end of the year

31 December 31 December 2012 2011

(Rupees)

Note

703,410,386(161,493,418)(396,323,477) 97,953,271

(59,869,946) 56,446,606

(78,867,259)161,256,163

584,720,340(134,934,573)(318,320,327) 66,521,277(52,274,893)46,611,822)

(74,572,145)117,751,501

(3,266,688)(206,330,366)

7,658,800)

(4,204,260)(174,881,966)

9,798,926)(169,287,300)

(51,535,799)

(201,938,254)

(40,682,091)

34,256,118(56,694,024) 47,118,125

(6,518,117) 1,582,706 19,744,808

36,716,663)(59,534,000)58,510,188)(4,727,519)

762,500)31,727,832)

(20,937,283)

257,598,882)

236,661,599)

(19,807,967)

277,406,849

257,598,88212

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

25

Chairman Director Director Managing Director(Chief Executive)

(40,682,091) (7,310,012) 36,481,530 879,803 (7,043,129) 43,453,213 (9,177,590) 1,324,272 3,266,688 21,192,684

(39,759,501) 60,952,185

31 December2012

31 December2011

Reconciliation to profit and loss account

Operating cash flowsDepreciation/amortisationInvestment incomeGain on sale of fixed assets(Decrease) / Increase in assetsDecrease / (Increase) in liabilities(Increase) in unearned contributionDecrease in contribution deficiency reserveIncome tax paidNet profit for the year

(Rupees)

Definition of cash

Participants' Takaful FundShareholders' Fund

Cash comprises of cash in hand, policy stamps, bond papers, bank balances and other deposits whichare readily convertible to cash in hand and which are used in the cash management function on aday-to-day basis.

The annexed notes from 1 to 29 form an integral part of these financial statements.

(51,535,799) (8,116,639) 37,265,394 200,714 97,467,378(39,567,808)(29,014,730) 5,720,703 4,204,260 16,623,473

(32,694,449) 49,317,922

21,192,684 16,623,473

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

26

Chairman Director Director Managing Director(Chief Executive)

Balance as at 1 January 2011

Total comprehensive income for the year - profit for the year

Balance as at 31 December 2011

Total comprehensive income for the year - profit for the year

Balance as at 31 December 2012

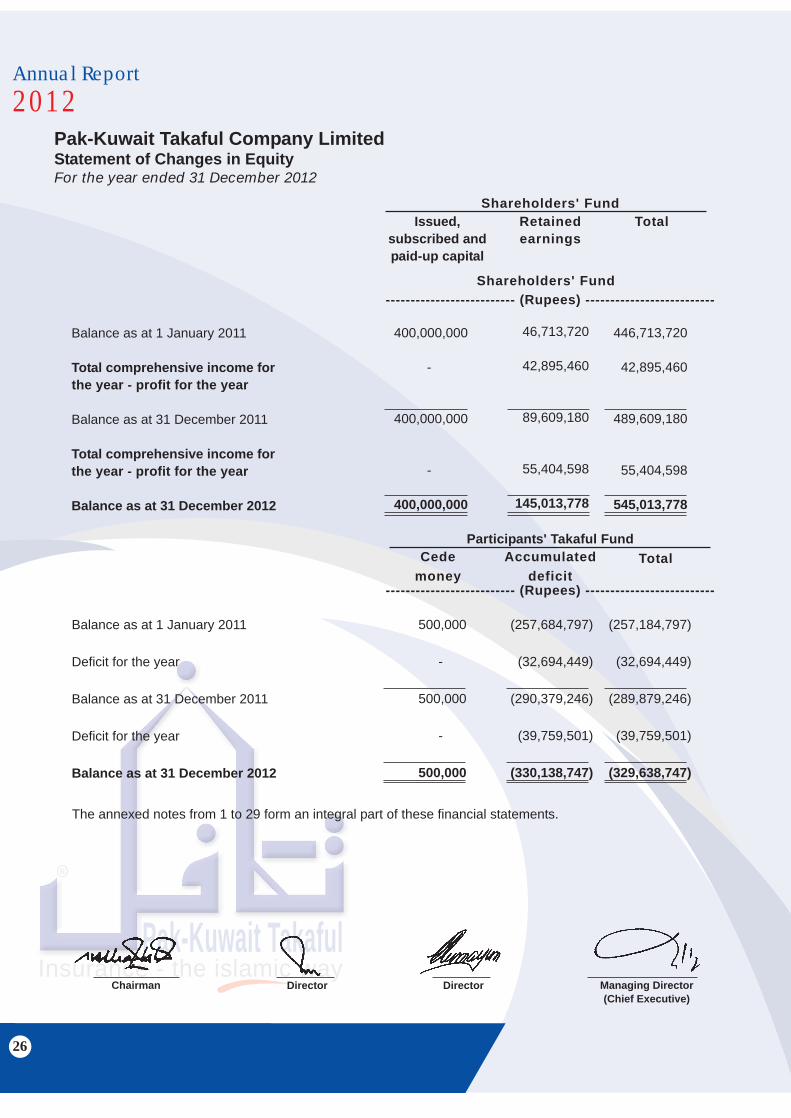

Pak-Kuwait Takaful Company LimitedStatement of Changes in EquityFor the year ended 31 December 2012

Balance as at 1 January 2011

Deficit for the year

Balance as at 31 December 2011

Deficit for the year

Balance as at 31 December 2012

Shareholders' Fund

400,000,000

-

400,000,000

-

400,000,000

Shareholders' Fund

Issued,subscribed andpaid-up capital

Retainedearnings

Total

-------------------------- (Rupees) --------------------------

446,713,720

42,895,460

489,609,180

55,404,598

545,013,778

46,713,720

42,895,460

89,609,180

55,404,598

145,013,778

Participants' Takaful Fund

500,000

-

500,000

-

500,000

Cedemoney

Total

(257,184,797)

(32,694,449)

(289,879,246)

(39,759,501)

(329,638,747)

Accumulateddeficit

-------------------------- (Rupees) --------------------------

(257,684,797)

(32,694,449)

(290,379,246)

(39,759,501)

(330,138,747)

The annexed notes from 1 to 29 form an integral part of these financial statements.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

27

Pak-Kuwait Takaful Company LimitedStatement of ContributionsFor the year ended 31 December 2012

GrossContribution

Written *

Wakalafee

Netcontribution

written

Unearnedcontribution

reserveContribution

earnedRe-takaful

ceded

PrepaidRe-takaful

contributionRe-takafulexpense

Netcontribution

revenue

Netcontribution

revenue

20112012

Opening Closing Opening Closing(Rupees)------------------------------------------------------------------------------------------- ----------------------------------------------------------------------------------------------

ClassDirect and facultative1. Fire and property damage

2. Marine, aviation and transport

3. Motor

4. Miscellaneous

193,173,193

106,704,425

328,841,716

91,687,257

720,406,591

60,849,556

33,611,894

103,585,141

28,881,486

226,928,077

132,323,637

73,092,531

225,256,575

62,805,771

493,478,514

51,110,369

10,323,862

107,139,301

13,724,901

182,298,433

58,396,223

9,175,292

100,338,206

23,566,302

191,476,023

125,037,783

74,241,101

232,057,670

52,964,370

484,300,924

93,464,069

35,119,983

19,273,296

43,083,934

190,941,282

34,564,472

7,115,374

2,568,345

8,162,766

52,410,957

42,170,988

4,572,622

2,209,599

16,514,072

65,467,281

85,857,553

37,662,735

19,632,042

34,732,628

177,884,958

39,180,230

36,578,366

212,425,628

18,231,742

306,415,966

41,419,599

14,029,683

189,789,467

20,787,056

266,025,805

The annexed notes from 1 to 29 form an integral part of these financial statements.

* This includes administrative surcharge in aggregate of all classes amounting to Rs. 22.626 million.

Total

Business underwritten inside Pakistan

Chairman Director Director Managing Director(Chief Executive)

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

Pak-Kuwait Takaful Company LimitedStatement of ClaimsFor the year ended 31 December 2012

Claimspaid

Outstanding claimsClaims

expense

Re-takaful andother

recoveriesreceived

Re-takaful and otherrecoveries in respect of

outstanding claims

Re-takafuland otherrecoveries

revenue

Net claimsexpense

Net claimsexpense

20112012

Opening Closing(Rupees)------------------------------------------------------------------------------------------- -------------------------------------------------------------------------------------------

57,727,522

32,301,928

275,641,969

39,897,919

405,569,338

19,518,622

12,564,211

76,601,038

14,594,286

123,278,157

10,216,509

6,485,272

33,495,642

7,866,474

58,063,897

48,425,409

26,222,989

232,536,573

33,170,107

340,355,078

26,863,208

16,920,759

29,067,181

14,933,447

87,784,595

9,552,107

5,910,905

14,312,430

6,171,720

35,947,162

2,087,442

2,194,234

1,288,710

1,166,542

6,736,928

19,398,543

13,204,088

16,043,461

9,928,269

58,574,361

29,026,866

13,018,901

216,493,112

23,241,838

281,780,717

20,491,551

16,532,556

173,461,702

15,459,841

225,945,650

ClassDirect and facultative1. Fire and property damage

2. Marine, aviation and transport

3. Motor

4. Miscellaneous

Total

The annexed notes from 1 to 29 form an integral part of these financial statements.

Business underwritten inside Pakistan

Chairman Director Director Managing Director(Chief Executive)

Opening Closing

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

29

Chairman Director Director Managing Director(Chief Executive)

Pak-Kuwait Takaful Company LimitedStatement of ExpensesFor the year ended 31 December 2012

Business underwritten inside Pakistan

Commissionpaid orpayable

a

Deferred commission

Openingb

Closingc

Netcommission

expense

d=a+b-c

Othermanagement

expense

e

Underwritingexpenses

f=d+e

Rebate from re.takaful

operators*

g

Nettakaful

expense

h=f-c

Nettakaful

expense

20112012Class

1. Fire and property damage

2. Marine, aviation and transport

3. Motor

4. Miscellaneous

Total

Direct and facultative17,882,487

14,911,905

13,247,285

13,828,269

59,869,946

9,439,974

2,210,524

7,463,317

3,511,204

22,625,019

8,068,578

1,941,530

6,136,142

5,300,376

21,446,626

19,253,883

15,180,899

14,574,460

12,039,097

61,048,339

2,692,202

834,889

56,053,366

432,557

60,013,014

21,946,085

16,015,788

70,627,826

12,471,654

121,061,353

28,453,209

13,008,950

5,876

10,646,430

52,114,465

(6,507,124)

3,006,838

70,621,950

1,825,224

68,946,888

(1,071,173)

(220,225)

75,253,622

6,031,712

79,993,936

* Rebate from retakaful operators is arrived at after taking the impact of opening and closing unearned retakaful commission.

The annexed notes from 1 to 29 form an integral part of these financial statements.

(Rupees)----------------------------------------------------------------------------------------- -----------------------------------------------------------------------------------------

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

30

Chairman Director Director Managing Director(Chief Executive)

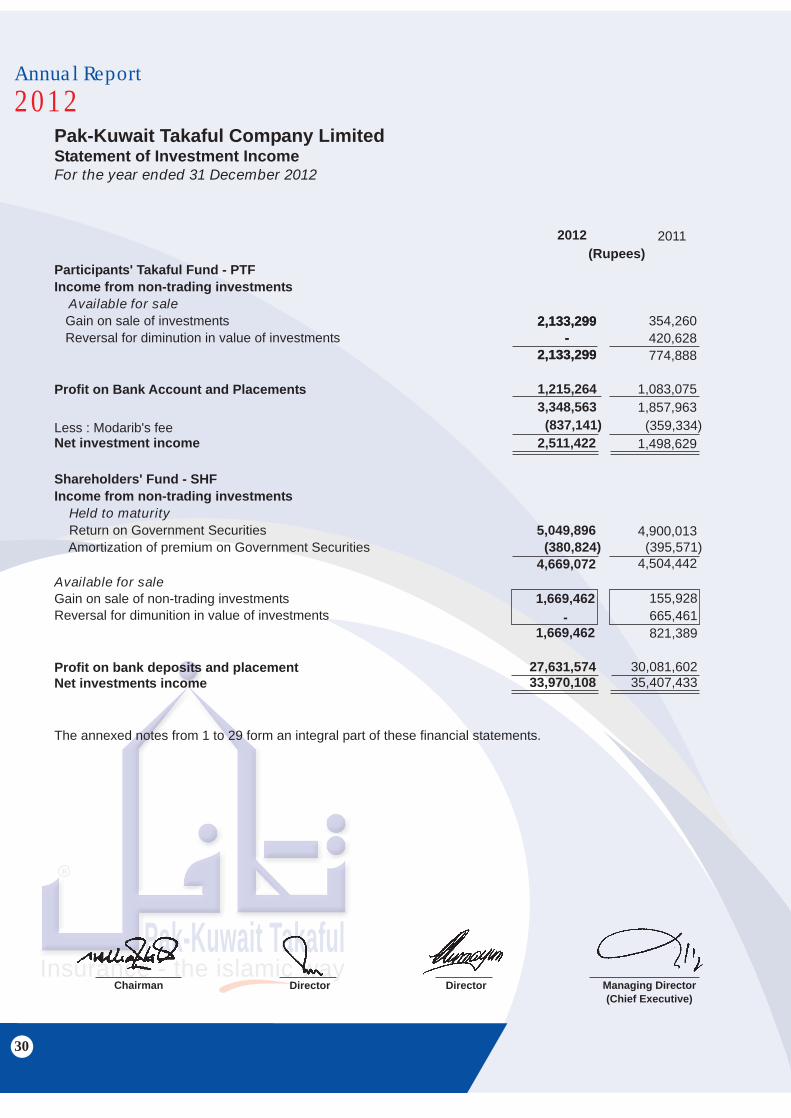

Pak-Kuwait Takaful Company LimitedStatement of Investment IncomeFor the year ended 31 December 2012

(Rupees)2012 2011

5,049,896 (380,824)4,669,072

4,900,013 (395,571)4,504,442

1,669,462-

1,669,462

155,928665,461821,389

2,133,299-

2,133,299

354,260420,628774,888

2,133,299-

2,133,299

1,215,2643,348,563 (837,141)2,511,422

1,083,0751,857,963 (359,334)1,498,629

27,631,57433,970,108

30,081,60235,407,433

Participants' Takaful Fund - PTFIncome from non-trading investments Available for sale Gain on sale of investments Reversal for diminution in value of investments

Less : Modarib's feeNet investment income

Profit on Bank Account and Placements

Profit on bank deposits and placementNet investments income

Available for saleGain on sale of non-trading investmentsReversal for dimunition in value of investments

Shareholders' Fund - SHFIncome from non-trading investments Held to maturity Return on Government Securities Amortization of premium on Government Securities

The annexed notes from 1 to 29 form an integral part of these financial statements.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

31

Pak-Kuwait Takaful Company LimitedNotes to the Financial StatementsFor the year ended 31 December 2012

1. STATUS AND NATURE OF BUSINESS

Pak-Kuwait Takaful Company Limited (the Company) was incorporated in Pakistan as an unlistedpublic limited company on 06 June 2003. The registered office of the Company is situated at 4th Floor,Block-A, Finance and Trade Centre, Karachi. The business activity of the Company is to undertaketakaful business. The Company operates with 04 (2011: 04) branches in Pakistan.

For the purpose of carrying on the takaful business, the Company has formed a Waqf for Participants'equity. The Waqf, namely Pak-Kuwait Takaful Waqf (hereinafter referred to as the Participants'Takaful Fund or PTF) was formed on 02 December 2005 under the Waqf deed executed by theCompany with a cede money of Rs. 500,000. The cede money is required to be invested in Shariahcompliant investments and any profit thereon can be utilized only to pay benefits to participants ordefray PTF expenses. The accounts of the Waqf are maintained by the Company in a manner that theassets and liabilities of the Waqf remain separately identifiable. The financial statements are preparedsuch that the financial position and results of operations of the Waqf and the Company are shownseparately. Waqf Deed governs the relationship of shareholders and participants for management oftakaful operations, investments of participants' funds and investment of shareholders' funds approved bythe Shariah Board established by the Company.

2. BASIS OF PREPARATION

These financial statements have been prepared in line with the format issued by the Securities andExchange Commission of Pakistan (SECP) through SEC (Insurance) Rules, 2002, vide SRO 938 dated12 December 2002 with appropriate modifications based on the approval of the Shariah Board of theCompany.

These financial statements reflect the financial position and results of operations of both the Companyand PTF in a manner that the assets, liabilities, income and expenses of the Company and PTF remainseparately identifiable. For this purpose, the receivables and payables between the Company and PTFhave been eliminated.

2.1 Statement of compliance

These financial statements have been prepared in accordance with approved accounting standards asapplicable in Pakistan. Approved accounting standards comprise of such International FinancialReporting Standards (IFRS) issued by the International Accounting Standards Board and IslamicFinancial Accounting Standards (IFAS) issued by the Institute of Chartered Accountants of Pakistan(ICAP) as are notified under the Companies Ordinance, 1984, provisions of and directives issued underthe Companies Ordinance, 1984, Insurance Ordinance, 2000, SEC (Insurance) Rules, 2002 and TakafulRules, 2005. In case requirements differ, the provisions or directives of the Companies Ordinance, 1984,Insurance Ordinance, 2000, SEC (Insurance) Rules, 2002 and Takaful Rules, 2005 shall prevail.

2.2 Basis of measurement

These financial statements have been prepared under the historical cost convention.

2.3 Functional and presentation currency

These financial statements are presented in Pak Rupees which is also the Company’s functionalcurrency.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

32

2.4 Use of estimates and judgements

The preparation of financial statements in conformity with approved accounting standards as applicablein Pakistan requires management to make judgments, estimates and assumptions that affect theapplication of policies and reported amounts of assets and liabilities, income and expenses. Theestimates and associated assumptions are based on historical experience and various other factors thatare believed to be reasonable under the circumstances, the result of which form the basis of making thejudgments about carrying values of assets and liabilities that are not readily apparent from othersources, actual results may differ from these estimates. The estimates and underlying assumptions arereviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in whichthe estimate is revised if the revision affects only that period, or in the period of the revision and futureperiods if the revision affects both current and future periods.

Judgments made by the management in the application of approved accounting standards as applicablein Pakistan that have significant effect on the financial statements with a significant risk of materialadjustments in the next year are as follows:

- Provision for outstanding claims including IBNR (Refer Note 4.4)- Investment classification and valuation (Refer Note 4.13)- Staff retirement benefits (Refer Note 4.10)- Useful lives of assets and methods of depreciation and amortisation (Refer Note 4.15)- Re-takaful recoveries against outstanding claims (Refer Note 4.3)- Provision for unearned contribution (Refer Note 4.2)- Taxation (Refer Note 4.14)- Contribution due but unpaid (Refer Note 4.2)- Re-takaful contribution (Refer Note 4.3)

3. Initial Application of Rules, Standard, Amendement or an interpertation to an existing standard

3.1 Implementation of Takaful Rules 2012Securities and Exchange Commission of Pakistan through Notification S.R.O 877(I)/2012 dated 16 July2012 has issued Takaful Rules, 2012 and requires that existing Takaful Operators shall comply with therequirements of these Rules within period of six months from the notification in Official Gazette. TheSRO has not yet been notified through Official Gazette till date. However, Takaful Pakistan Limitedand others filed constitution Petition no. D-2791/2012 before Honorable High Court of Sindh againstnotification issued by SECP in respect of (i) Rules have been framed without hearing the petitionerswhereby it was proposed that conventional insurers could operate takaful windows alongside theirexisting conventional insurance business and conduct takaful business and (ii) contention of petitionersthat if new Takaful Rules, 2012 are to be implemented these would be seriously prejudiced. TheHonorable High Court of Sindh directed the parties to maintain status-quo. Currently, the proceedings onthe hearing have further been adjourned with status-quo. Keeping in view of above current status andbased on the legal counsel’s opinion the Company is of the view that these rules are not applicable andaccordingly have not been implemented.

3.2 New accounting standards and IFRIC interpretations that are not yet effective

The following standards, amendments and interpretations of approved accounting standardswill be effective for accounting periods beginning on or after 01 January 2013:

IAS 19 Employee Benefits (amended 2011) - (effective for annual periods beginning on or afterJanuary 2013). The amended IAS 19 includes the amendments that require actuarial gains and lossesto be recognised immediately in other comprehensive income; this change will remove the corridor methodand eliminate the ability for entities to recognise all changes in the defined benefit obligation and in planassets in profit or loss, which currently is allowed under IAS 19; and that the expected

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

33

return on plan assets required to recognize unrecognized actuarial gains and losses in othercomprehensive income. Presently, acutarial gains / losses are recoginsed in profit and loss accounton corridor basis.The unrecognized actuarial gain in aggregate amount to Rs 0.468 million as at 31December 2012 as disclosed in note 6.1 which would be required to recognize in other comprehensiveincome.

IAS 27 Separate Financial Statements (2011) - (effective for annual periods beginning on or afterJanuary 2013). IAS 27 (2011) supersedes IAS 27 (2008). Three new standards IFRS 10 - ConsolidatedFinancial Statements, IFRS 11- Joint Arrangements and IFRS 12- Disclosure of Interest in OtherEntities dealing with IAS 27 would be applicable effective 1 January 2013. IAS 27 (2011) carriesforward the existing accounting and disclosure requirements for separate financial statements, withsome minor clarifications The amendments have no impact on financial statements of the Company.

IAS 28 Investments in Associates and Joint Ventures (2011) - (effective for annual periods beginningon or after 1 January 2013). IAS 28 (2011) supersedes IAS 28 (2008). IAS 28 (2011) makes theamendments to apply IFRS 5 to an investment, or a portion of an investment, in an associate or ajoint venture that meets the criteria to be classified as held for sale; and on cessation of significantinfluence or joint control, even if an investment in an associate becomes an investment in a jointventure. The amendments have no impact on financial statements of the Company.

Offsetting Financial Assets and Financial Liabilities (Amendments to IAS 32) - (effective for annualperiods beginning on or after 1 January 2014). The amendments address inconsistencies in currentpractice when applying the offsett ing criteria in IAS 32 Financial Instruments:Presentation. The amendments clarify the meaning of 'currently has a legally enforceable right ofset-off'; and that some gross settlement systems may be considered equivalent to net settlement.The amendments have no significant effect on financial statements of the Company.

Offsetting Financial Assets and Financial Liabilities (Amendments to IFRS 7) - (effective for annualperiods beginning on or after 1 January 2013). The amendments to IFRS 7 contain new disclosurerequirements for financial assets and liabilities that are offset in the statement of financial positionor subject to master netting agreement or similar arrangement. The amendments have no significanteffect on financial statements of the Company.

Annual Improvements 2009-2011 (effective for annual periods beginning on or after 1 January 2013).The new cycle of improvements contains amendments to the following five standards, with consequentialamendments to other standards and interpretations.

IAS 1 Presentation of Financial Statements is amended to clarify that only one comparative periodwhich is the preceding period - is required for a complete set of financial statements. If an entitypresents additional comparative information, then that additional information need not be in theform of a complete set of financial statements. However, such information should be accompaniedby related notes and should be in accordance with IFRS. Furthermore, it clarifies that the 'thirdstatement of financial position', when required, is only required if the effect of restatement is materialto statement of financial position. The amendments have no significant effect on financial statementsof the Company.

IAS 16 Property, Plant and Equipment is amended to clarify the accounting of spare parts, stand-by equipment and servicing equipment. The definition of 'property, plant and equipment' in IAS 16is now considered in determining whether these items should be accounted for under that standard.If these items do not meet the definition, then they are accounted for using IAS 2 Inventories. Theamendments have no impact on financial statements of the Company.

IAS 32 Financial Instruments: Presentation - is amended to clarify that IAS 12 Income Taxes appliesto the accounting for income taxes relating to distributions to holders of an equity instrument andtransaction costs of an equity transaction. The amendment removes a perceived inconsistency

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

34

between IAS 32 and IAS 12. The amendments have no significant effect on financial statements of theCompany.

IAS 34 Interim Financial Reporting is amended to align the disclosure requirements for segment assetand segment liabilities in interim financial reports with those in IFRS 8 Operating Segments.IAS 34 now requires the disclosure of a measure of total assets and liabilities for a particular reportablesegment. In addition, such disclosure is only required when the amount is regularly provided to the chiefoperating decision maker and there has been a material change from the amount disclosed in the lastannual financial statements for that reportable segment.The amendments would have no impact on financialstatements of the Company.

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The significant accounting policies as set below have been applied consistently to all periods presentedin these financial statements.

4.1 Takaful contracts

The takaful contracts are based on the principles of Wakala. The takaful contracts so agreed usually inspireconcept of tabarru (to donate for benefit of others) and mutual sharing of losses with the overall objectiveof eliminating the element of uncertainty.

A separate Participants Takaful Fund (PTF) is created in which all contribution received under generaltakaful contribution net off any government levies are credited to one or more PTF(s). The role of Takafuloperator is of the management of the PTF. At the initial stage of the setup of the PTF, the takaful operatormakes an initial donation to the PTF. The terms of the takaful contracts are in accordance with the generallyaccepted principles and norms of insurance business suitably modified with guidance by the Shariah Boardof the Takaful operator.

4.2 Contribution

Contribution income net off wakala fee and administrative surcharge under a policy is recognised overthe period of takaful from the date of inception of the policy to which it relates to its expiry as follows:

i) For direct business, evenly over the period of the policy.ii) For proportional re-takaful business, evenly over the period of the underlying takaful policies.

Revenue from contribution - net off wakala fee and administrative surcharge, is recognised aftertaking into account the unearned portion of contribution which is calculated using the ratio of theunexpired period of the policy and the total period, both measured to the nearest day. The unearnedportion of contribution is recognised as liability.

Administrative surcharge is recognised as contribution at the date of inception of policy to which it relates.

Contribution due but unpaid represents the amount due from participants on account of takaful contracts.These are recognised at cost, which is the fair value of the consideration to be received less provisionfor impairment, if any.

4.3 Re-takaful

Retakaful expense is recognised evenly in the period of indemnity. The portion of retakaful contributionnot recognised as an expense is shown as a prepayment which is calculated in the same manner as ofunearned contribution.

Rebate from retakaful operators is recognised at the time of issuance of the underlying takaful policy bythe company. This income is deferred and brought to account as revenue in accordance with the

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

35

pattern of recognition of the retakaful contribution to which it relates.

Receivable against claims from the retakaful operators are recognised as an asset at the same time asthe claims which gives rise to the right of recovery are recognised as a liability and are measured at theamount expected to be recovered after considering an impairment in relation thereto.

Amount due from other takaful / re-takaful are carried at cost less provision for impairment, if any. Costrepresents the fair value of consideration to be received in the future.

Amount due to takaful / re-takaful companies represent the balance due to re-takaful companies.

Re-takaful assets or liabilities are derecognised when the contractual rights are extinguished or expired.

4.4 Claims

Claims expense include all claims occurring during the year, whether reported or not. Internal and externalclaim handling costs that are directly related to the processing and settlement of claims, a reduction forthe value of salvage and other recoveries, and any adjustments to claims outstanding from previous years.

Outstanding claims comprise the estimated cost of claims incurred but not settled at the balance sheetdate, whether reported or not. Provisions for reported claims not paid as at the reporting date are madeon the basis of individual case estimates. In addition, a provision based on management’s judgment andthe Company’s prior experience is maintained for the cost of settling claims incurred but not reported(IBNR) at the reporting date and the claims intimated subsequent to the reporting date, except for accidentpolicies where the management estimate provision for IBNR based on actuarial valuation as required bySRO 16 (I) / 2012 issued by Securities and Exchange Commission of Pakistan on 9 January 2012 atreporting date. This change has been accounted for as change in accounting estimate in accordance withthe requirements of approved International Accounting Standard (IAS-8) "Accounting Policies, Changesin Estimates and Errors" whereby the effects of these changes are recognised prospectively by includingthe same in determination of profit and loss in the period of the change, that is, during the current andfuture periods. However, the effect of the change is not material to the financial statements.

Any difference between the provisions at the reporting date and settlements in the following period isincluded in the financial statement of that period.

4.5 Commission

Commission expense incurred in obtaining and recording policies is deferred and recognised as anexpense in accordance with pattern of recognition of contribution revenue.

4.6 Contribution deficiency reserve

The Company is required to maintain a provision in respect of contribution deficiency for the class ofbusiness where the unearned contribution reserve is not adequate to meet the expected future liability,after re-takaful from claims, and other supplementary expenses expected to be incurred after the reportingdate in respect of the unexpired policies in respective class of business at the reporting date.The movement in the contribution deficiency reserve is recorded as a charge / (reversal) in the profitand loss account.

The management considered the requirements of contribution deficiency reserve for each class of businessat reporting date, including accident policies where actuary advised that no provision is required, andestimated that adequate provision has been maintained in respective class of business wherever required.The actuarial valuation has been carried out to determine the amount of contribution deficiency reservein respect of accident insurance as required by SRO 16 (I) / 2012 issued by Securities and ExchangeCommission of Pakistan on 9 January 2012.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

36

4.7 Takaful surplus

Takaful surplus attributable to the participants is calculated after charging all direct cost and setting asidevarious reserves. Allocation to participants, if applicable, is made after adjustment of claims paid to themduring the year.

4.8 Wakala and Mudarib fees

The Takaful operator manages the general takaful operations for the participants' and charge 31.5% ofgross contribution as wakala fee to meet the general and administrative expenses of the Company. Wakalafee under a policy is recognised upfront at the date of inception of policy to which it relates in shareholders'fund.

The Takaful operator also manages the participants' investment as Mudarib and charges 25% of thegeneral takaful investment income as Mudarib's share earned by the participants' fund.

4.9 Qard-e-Hasna

Qard-e-hasna is provided by shareholders' fund to participants takaful fund in case of deficit in PTF.However, such amount is eliminated while consolidating the financial statements.

4.10 Employees' benefits

4.10.1 Defined benefit plan

The Company operates an approved defined gratuity scheme for all its permanent employees who attainthe minimum qualification period for entitlement to gratuity. Contributions to the fund are made based onactuarial recommendations and in line with the provisions of the Income Tax Ordinance, 2001. The mostrecent actuarial valuation was carried out for the year ended 31 December 2012 using the Projected UnitCredit Method. Actuarial gains / losses in excess of corridor limit (10% of the higher of fair value of assetsand present value of obligation) are recognised over the average remaining service life of the employees.

4.10.2 Defined contribution plan

The Company contributes to a provident fund scheme which covers all employees. Equal contributionsare made both by the Company and the employees to the fund at the rate of ten percent of basic salary.

4.10.3 Employees' compensated absences

The Company accounts for the liability in respect of employees’ compensated absences in the period inwhich they are earned.

4.11 Creditors, accruals and provisions

Liabilities for creditors and other amounts payable are carried at cost which is the fair value of theconsideration to be paid in the future for the services received, whether or not billed to the Company.

Provisions are recognized when the Company has a present legal or constructive obligation as a resultof past events, it is probable that an outflow of resources embodying economic benefits will be requiredto settle the obligation and a reliable estimate of the amount can be made. Provisions are reviewed ateach reporting date and adjusted to reflect the current best estimate.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

37

4.12 Cash and cash equivalents

Cash and cash equivalents consist of cash in hand, policy stamps, balances with banks, short-termdeposits maturing within 12 months of the year end, and are subject to insignificant risk of changein value.

4.13 Investments

4.13.1 Recognition

All investments are initially measured at fair value and include transaction costs that are directly attributableto acquisition except in the case of investment not at fair value through profit and loss account. Theseare recognized and classified as follows:

- Investment at fair value through profit and loss- Held to maturity- Available for sale

4.13.2 Measurement

4.13.2. Investments at fair value through profit and loss account

These include held-for-trading investments and those designated under this category upon initialrecognition. Subsequent to initial recognition, these are carried at fair value.

4.13.2.2 Held to maturity

Investments with fixed maturity, where management has both the intent and the ability to hold to maturity,are classified as held to maturity.

Subsequently, these are measured at amortised cost less provision for impairment, if any. Any premiumpaid or discount availed on acquisition of held to maturity investment is deferred and amortised over theterm of investment using the effective yield.

4.13.2.3 Available for sale

These are investments that do not fall under investment at fair value through profit or loss or heldto maturity categories.

Subsequent to initial recognition at cost, quoted investments are stated at the lower of cost or marketvalue (market value on an individual investment basis being taken as lower if the fall is other thantemporary) in accordance with the requirements of the SEC (Insurance) Rules, 2002 vide S.R.O. 938dated December 2002. Stock exchange quotations are used to determine market value.

Had the Company adopted International Accounting Standard (IAS) 39 "Financial Instruments:Recognition and Measurement" the investments and net equity of the Company would have beenhigher by Rs. 2.1 million (2011: 1.3 million).

4.13.2.4 Date of recognition

Regular way purchases and sales of investments that require delivery within the time frame establishedby regulations or market convention are recognised at the trade date. Trade date is the date on whichthe Company commits to purchase or sell the investment.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

38

4.14 Taxation4.14.1 Current

Provision for current taxation is based on taxable income at the rates enacted or substantively enactedat the balance sheet date after taking into account available tax credits and rebates, if any or minimumtax under section of the Income Tax Ordinance, 2001, whichever is higher.

4.14.2 Deferred

Deferred tax is accounted for using the balance sheet liability method in respect of all temporarydifferences at the balance sheet date between the tax bases and carrying amounts of assets andliabilities for financial reporting purposes. Deferred tax liabilities are generally recognized for all taxabletemporary differences and deferred tax assets are recognized to the extent that it is probable thattaxable profits will be available against which the deductible temporary differences, unused tax lossesand tax credits can be utilized.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to theperiod when the asset is realized or the liability is settled, based on the tax rates (and tax laws)that have been enacted or substantively enacted at the balance sheet date. Deferred tax is chargedor credited in the profit and loss account, except in the case of items credited or charged to equity inwhich case it is included in equity.

4.15 Fixed Assets

4.15.1 Tangibles

These are stated at cost less accumulated depreciation and impairment loss, if any. Depreciation ischarged over the estimated useful life of the asset on a systematic basis to income applying the straightline method at the rates specified in note 17.1 to the financial statements, after taking into accountresidual value.

Depreciation on additions is charged from the month in which the asset is put to use where as nodepreciation is charged from the month the asset is disposed off.

Subsequent cost are included in the assets' carrying amount or recognized as a separate asset, asappropriate, only when it is possible that the future economic benefits associated with the items willflow to the company and the cost of the item can be measured reliably. Maintenance and normal repairsare charged to profit and loss account currently.

An item of tangible asset is derecognized upon disposal or when no future economic benefits areexpected from its use or disposal. Any gain or loss arising on derecognition of the asset (calculatedas the difference between the net disposal proceeds and the carrying amount of the asset) is includedin the profit and loss in the year the asset is derecognized.

Depreciation methods, useful lives and residual values that is significant in relation to the total costof the asset are reviewed, and adjusted if appropriate, at each balance sheet date.

4.15.2 Capital work in progress

Capital work in progress including advances made for capital expenditure is stated at cost lessimpairment, if any.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

39

4.15.3 Intangibles

These are stated at cost less accumulated amortisation and impairment loss, if any. Amortisation is chargedover the estimated useful life of the asset on a systematic basis to income applying the straight line methodat the rates specified in note 17.2 to the financial statements.

Amortisation on additions is charged from the month in which the asset is acquired or capitalised whereasno amortisation is charged from the month the asset is disposed off. Software development costs are onlycapitalised to the extent that future economic benefits are expected to be derived by the Company.

The carrying amounts are reviewed at each balance sheet date to assess whether these are recorded inexcess of their recoverable amounts, and where carrying values exceed estimated recoverable amount,assets' are written down to their estimated recoverable amounts.

4.16 Ijarah

The Company accounts for assets under Ijarah arrangements in accordance with IFAS - 2 "Ijarah" wherebyperiodic Ijarah payments for such assets are recognised as an expense in profit and loss account on straightline basis over the ijarah term.

4.17 Impairment

The carrying amount of assets (other than deferred tax asset) are reviewed at each balance sheet date todetermine whether there is any indication of impairment of any asset or group of assets. If such indicationexists, the recoverable amount of the asset is estimated. An impairment loss is recognised whenever thecarrying amount of an assets exceeds its recoverable amount.Impairment losses are recognised in profit and loss account. An impairment loss is reversed if the reversalcan be objectively related to an event occurring after the impairment loss was recognised.

4.18 Financial instruments

Financial assets and financial liabilities other than those arising out of takaful contracts are recognized atthe time when the Company becomes a party to the contractual provisions of the instrument. Financialassets are de-recognised when the contractual right to future cash flows from the asset expire or is transferredalong with the risk and reward of the asset. Financial liabilities are de-recognised when obligation specifiedin the contact is discharged, cancelled or expired. Any gain or loss on de-recognition of the financial assetand liabilities is recognised in the profit and loss account of the current period.

4.19 Foreign currency translation

Transactions in foreign currencies are recorded at the rate ruling at the date of the transaction.Monetary assets and liabilities denominated in foreign currencies are retranslated at the rate of exchangeruling at the balance sheet date. Exchange differences, if any, are taken to profit and loss account.

4.20 Offsetting of financial assets and liabilities

Financial assets and financial liabilities are only offset and the net amount reported in the balance sheetwhen there is a legally enforceable right to set off the recognised amount and the Company intends to eithersettle on a net basis, or to realise the asset and settle the liability simultaneously.

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

40

4.21 Investment income

Income from held to maturity investments is recognised on a time proportion basis taking into account the effectiveyield on the investments. The difference between the redemption value and the purchase price of the held to maturityinvestments is amortised and taken to the profit and loss account over the term of the investment.

Dividend income from investments is recognised when the Company's right to receive the payment is established.

Gain or loss on sale of investment is included in income currently.

Profit on bank deposits and Islamic investment products is recognised on a time proportionate basis taking into accountthe effective yield.

Management expenses

All direct management expenses and expenses not allocable to the underwriting business are charged as administrativeand investment related expenses.

PAID-UP SHARE CAPITAL

4.22

5

6.2 Movement in liability during the year

Opening balanceCharge for the yearContribution to fund made during the yearClosing balance

2,540,000)2,773,082)

(3,340,000) 1,973,082

1,973,082)2,821,842)

(1,973,082) 2,821,842

6.1 Liability in balance sheet

Present value of defined benefit obligationsFair value of plan assetsUnrecognised actuarial gains / (losses)

2012 2011(Rupees)

11,638,200)(9,283,889)

467,531 2,821,842

10,348,900 (8,194,610) (181,208) 1,973,082

Ordinary shares of Rs. 10 each issued as fully paid in cash

40,000,000 40,000,000

12,000,00013,000,000

6,000,0002,500,0002,500,0004,000,000

40,000,000

12,000,00013,000,000

6,000,0002,500,0002,500,0004,000,000

40,000,000

(Number of Shares)

400,000,000 400,000,000

Ordinary shares of the Company held by the related parties are as follows:5.1

Pak- Kuwait Investment Company (Private) LimitedEtiqa Overseas Investment Pte. Limited, MalaysiaNoor Financial Investment Company, KuwaitTakaful Holdings Limited, U.A.EMeezan Bank LimitedSaudi Pak Industrial and Agricultural Investment Company (Private) Limited

2012 2011(Number of shares)

2012 2011(Rupees)

- Discount rate 11.5% (2011: 12.5%) per annum.- Expected rate of increase in the salaries of the employees 11.5% (2011: 12.5%) per annum.- Expected interest rate on plan assets of the fund 9% (2011: 12.5%) per annum.

6 STAFF RETIREMENT BENEFITS

Defined benefit plan - Gratuity fund

The actuarial valuations are carried out annually and contributions are made accordingly. Following were the significantassumptions used for valuation of the scheme:

-

-

-

-

Pak-Kuwait TakafulInsurance - the islamic way

R

Annual Report2012

41