Japanese Direct Foreign Investment: Patterns and...

67

INDUSTRY ANDENERGY DEPARTMENT WORKING PAPER INDUSTRY SERIES PAPER No.1 Japanese DirectForeign Investment: Patterns and Implications for Developing Countries February 1989 ThIolFakIds- and Energy- _ t , -PP- -R The World Bankindustry and Energy Department, PPR Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Japanese Direct Foreign Investment: Patterns and...

INDUSTRY AND ENERGY DEPARTMENT WORKING PAPERINDUSTRY SERIES PAPER No. 1

Japanese Direct Foreign Investment:Patterns and Implications forDeveloping Countries

February 1989

ThIolFakIds- and Energy- _ t , -PP- -R

The World Bank industry and Energy Department, PPR

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

JAPANESE DIRECT FOREIGN INVESTMENT:

PATTERNS AND IMPLICATIONS FOR

DEVELOPING COUNTRIES

by

Jung Taik Hyun

Katherine Whitmore

The World Bank

Copyright (c) 1989The World Bank1818 H Street, N.W.Washington, D.C' 20433U. S. A.

This paper is one of a series issued by the Industry and Energy Department forthe information and guidance of Bank staff. The paper may not be published orquoted as representing the views of the Bank Group, nor does the Bank groupaccept responsibility for its accuracy or completeness.

Japanese DFI has grown rapldly and is now the main globalsource of direct forelgn investment flows. It has undergone a struc-tural shift from labor-intensive manufacturing to technologicallysophistLcated, capital-intensive sectors, and from developing todeveloped countries. While large firm characterize Japanese DFI indeveloped countries, general trading companies and small and mediumfirms have been important participants and still play an Lmportant rolein developing countries.

The main objective of Japanese DFI is to expand sales, andthe main operating concern is macroeconomic stability, followed by hostcountry restrictions on operations. Japanese DFI performance indeveloping countries, characterized by a relatively high proportion ofminority owned firms and local market sales, has been as much a reflec-tion of host country policy as firm strategy. As Japanese DFI shifts toindustries characterized by rapid technological change, developingcountry bargaining power to impose restrictions and performance require-ments will diminish.

JAPANUSE DIRECT FOREIGN INVESTMENT

TABLE OF CONTENTS

Page No.

I. INTRODUCTION .... 1*. ... .. oo... .. e 1

II. OVERALL TRENDS OF JAPANESE DIRECT FOREIGN INVESTMENT ...... 3

A. Growth of Japanese DFI 3B. Japanese Share in VJorld DFI Flows 4.................. 4C. Future Prospects of Japanese DPI ..........-........... 5

III. SECTORAL AND REGIONAL DISTRIBUTION OF JAPANESE DFI ......... 8

A. Sectoral Distribution 8B. Regional Distribution . ................. ............ 12Co Conclusion ............................................ 21

IV. CHARACTERISTICS OF JAPANESE DFI ............................ 24

A. Nature of Investors ...... ..... .... ...... *..... 24B. Objectives of Japanese DFI ............................ 29C. Difficulties Perceived by Japanese Firms in

DFI Operation ..... ....... .................... 31D. Ownership Patterns of Japanese DFI .................... 31E. Market Destination of Japanese Manufacturing

Subsidary .............. *...... **..e.. *..**** .... 35F. Management Style of Japanese Subsidiaries ............. 37G. Japanese Government Influence on Private DFI .......... 38H. Conclusion ... .. *........ *...*.*..*... ... aa*.. 39

V. SUMMARY AND IMPLICATIONS FOR DEVELOPING COUNTRIES .......... 41

REFERENCES .................................. ***.*.*.*.*** 44

Table of Cont.nts (Continued)

LIST OF TALES IN TEXT

Table 11.1 Share of Japanese DEI in World FlowsTable 11.2 DFI Stocks as Proportion of National Economy, 1986

Table 11.3 Impact of Yen Appreclation on Japanese Firms'DFI Decisions, FY86

Table 11.4 Future Prospect of Japanese DFI GrowthTable 111.1 Sectoral Share of Japanese DFI FlowsTable 111.2 Japanese WDI Flows to North America (By Country)Table 111.3 Japanese DFI Flows to North America (By Sector)Table 111.4 Japanese DPI Flows to EuropeTable 111.5 Japanese DFI Flows to AsiaTable 111.6 Japanese OFI Composition in Selected Asian

CountriesTable 111.7 Regional Distribution of Japanese DFI Flows

By Sector, FY76 and FY86Table IV.l DFI by Major CorporationsTable IV.2 Share of Small and Medium Investors in

Japanese OFI, FY73-85Table IV.3 Number of Subsidiaries by Type of Parenc Company,

FY85Table IV.4 Share of Sales Subsidiaries Among Total

Subsidiaries of Japanese ManufacturingCompanies, FY85

Table IV.5 Japanese DFI Objectives by Region, FY87Table IV.6 Problems in DFI Operation by RegionTable IV.7 Ownership Pacterns Among Japanese DFI

Affiliates, FY85Table IV.8 Market Destination of Japanese and U.S.

Manufacturing Subsidiaries

LIST OF CHARTS IN TEXT

Chart 11.1 Trends in Japanese DF; Flows, 1951-87Chart III.1 Sectoral Distribution of Japanese and U.S.

DFI StockChart III.2 Percentage Share of Merchandise ExportsChart 111.3 Regional Japanese DFI Flows by PeriodChart 111.4 Japanese OFI Flows to Latin AmericaChart IV.1 Important Factors in Selecting Overseas SitesChart IV.2 Ownership Patterns of Japanese DFI BY

Country, FY86Chart IV.3 Market Destination of Japanese and U.S.

Subsidiaries by RegionChart IV.4 Return on Investment of Foreign Manufacturing

Subsidiaries in the U.S.Chart IV.5 Financing Source of Japanese DFI

Table of Contents (Continued)

APPENDICES

APPENDIX 1 Japaneso DPI Definition and IndustryClassification

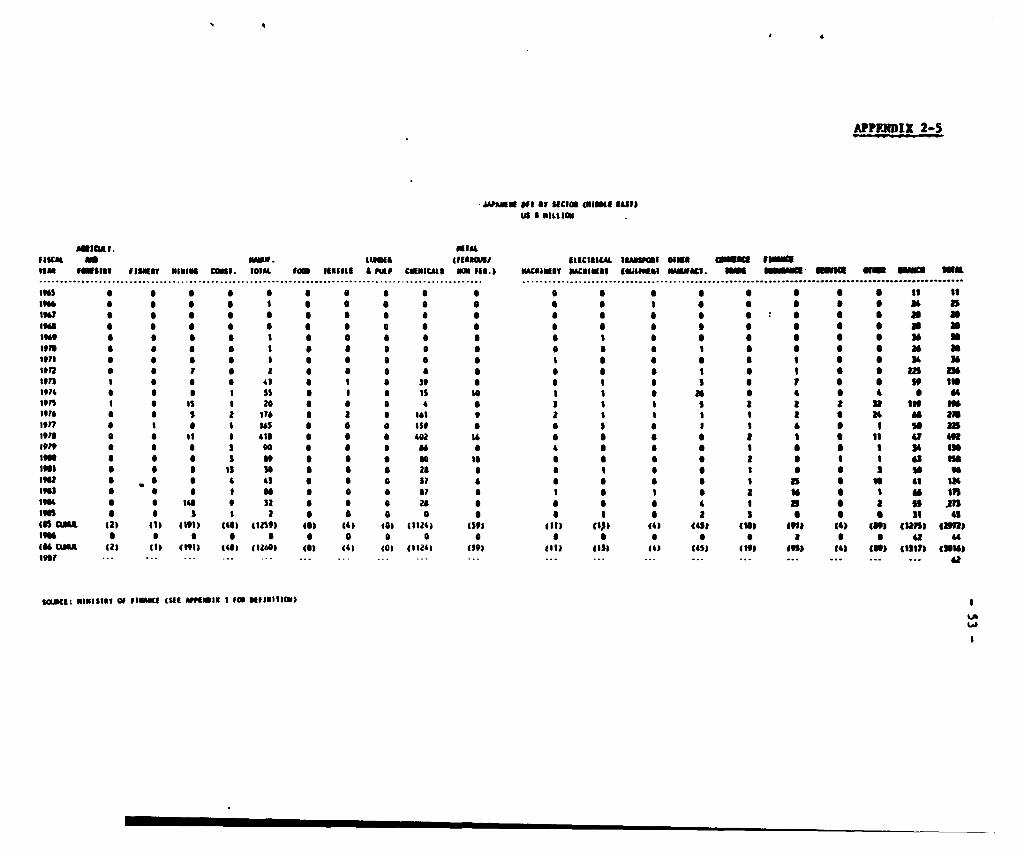

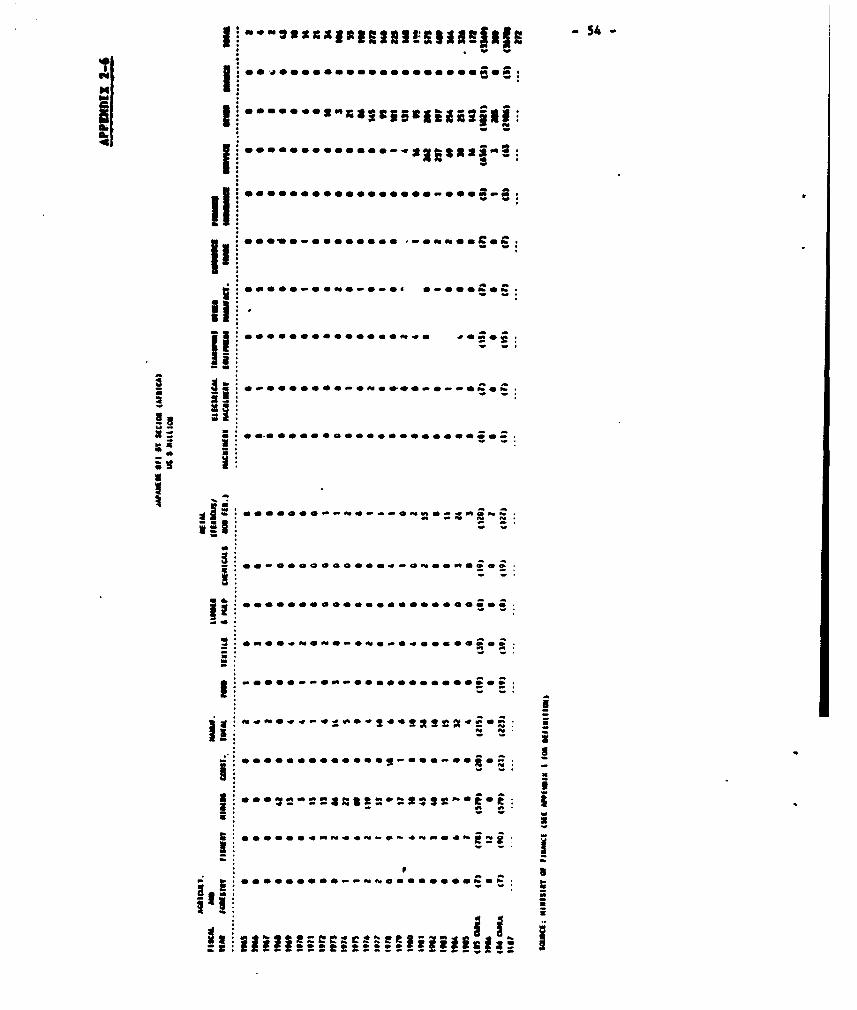

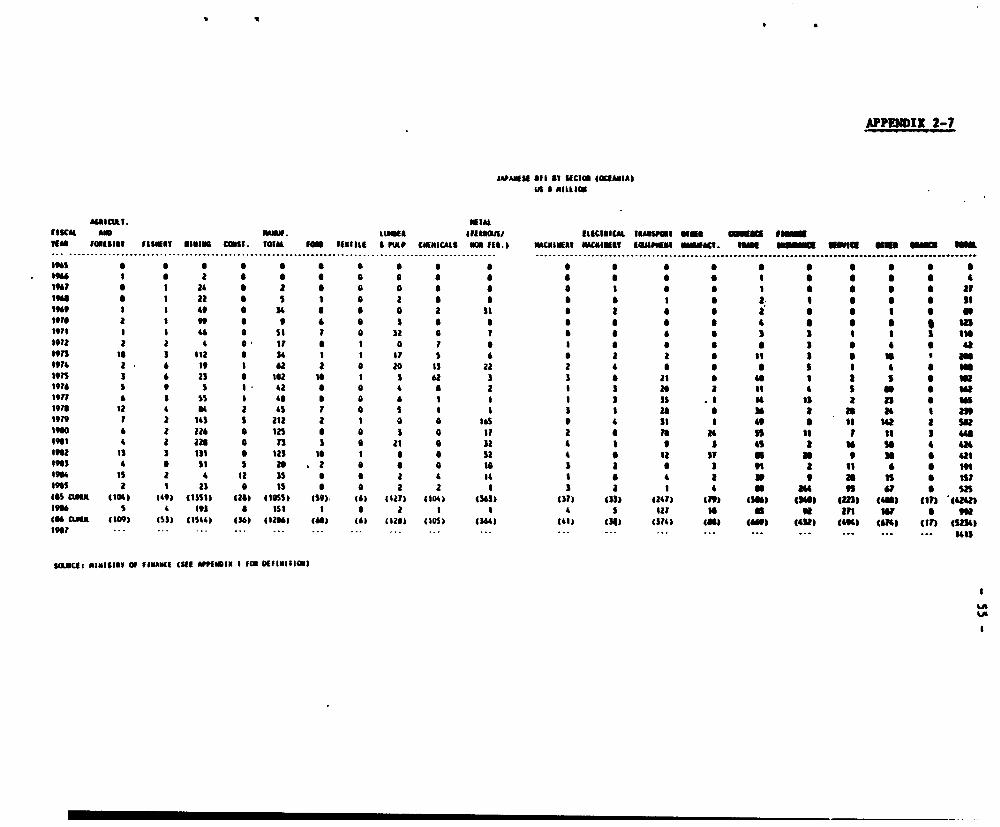

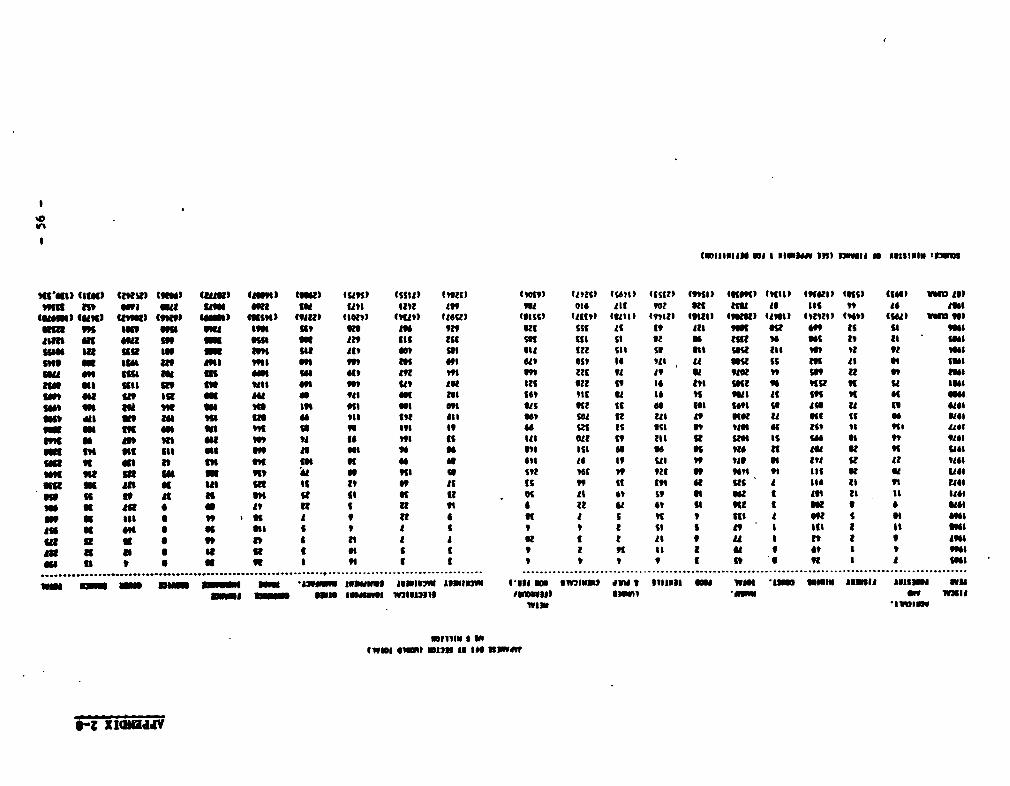

APPENDIX 2 Japanese DFI Flow by Sector and Region, 1965-1987.

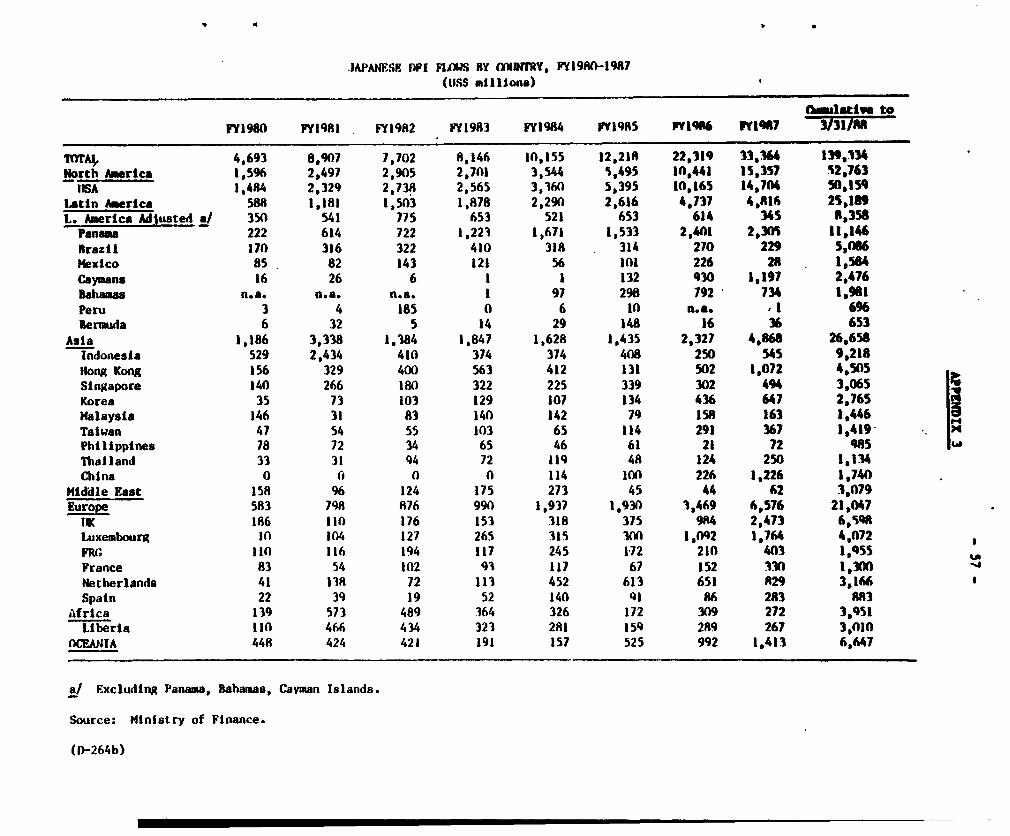

APPENDIX 3 Japaaese DFI Flow by Country, 1980-1987

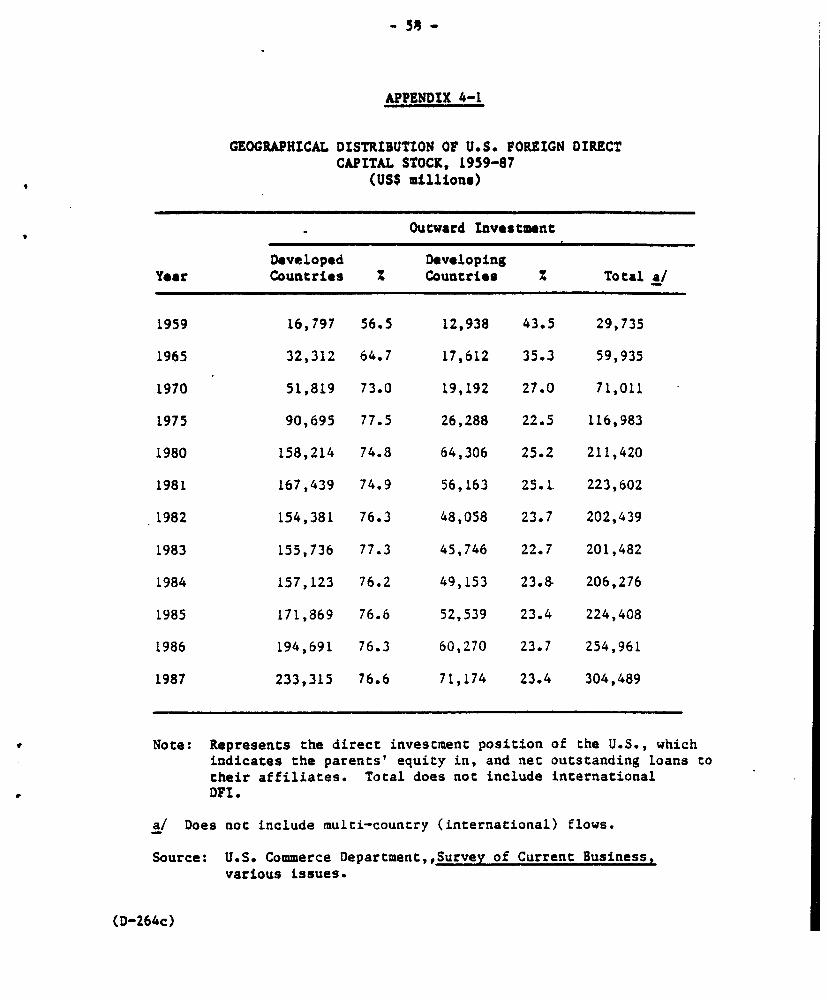

APPENDIX 4-1 Geographical Distribution of U.S. DFI Stock,1959-1987

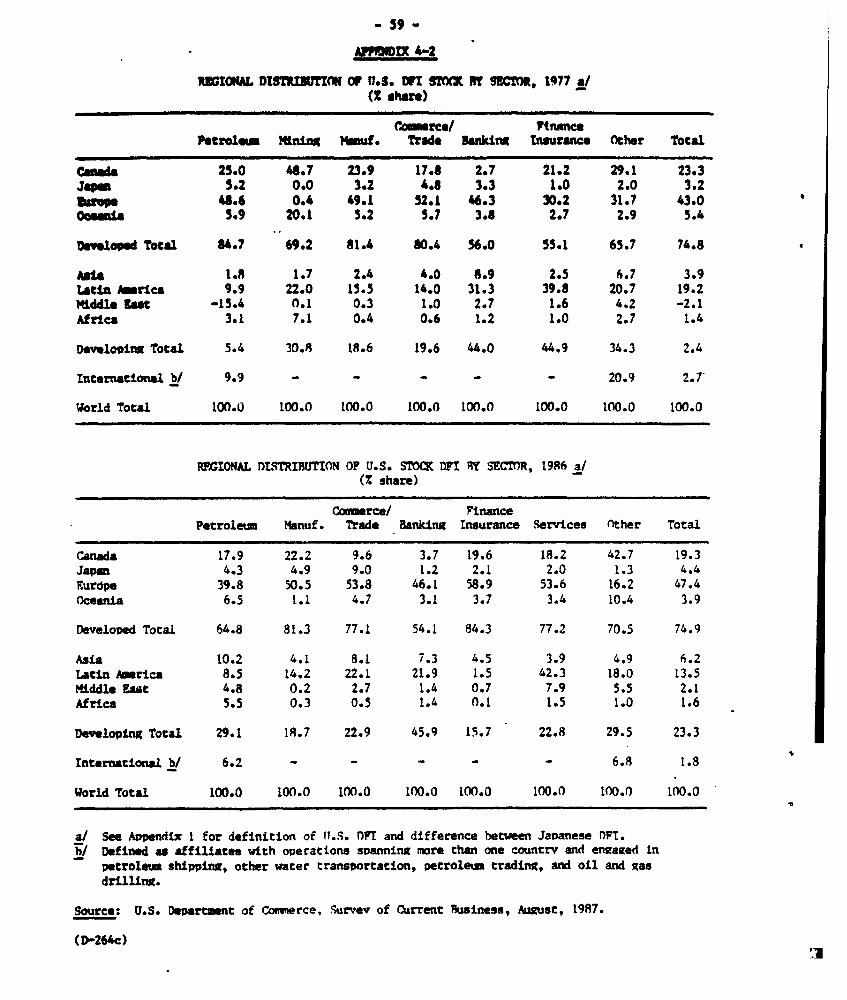

APPENDIX 4-2 Sectoral Distribution of U.S. DFI Stockby Region, 1977 and 1986

APPENDIX 5 Financial Incentives for Japanese DFI

I. INTRODUCTION

1.01 Within the past 20 years, Japan has becom the zost importantdynamic source of global direct foreign investment (DFI). In annual DFIflows, Japan has already taken the global lead. Excluding reinvestedearnings, Japanese DFI flows in 1987 totalled $33.4 billion, compared to$9.5 billion by the United States.1/ Japan has accumulated $139.3 billionin DPI stock, the second largest in the world, following the $308.8 billionstock of the U.S.

1.02 Major Incentives for rapid expansion of Japanese DFI are: theattractiveness of overseas, particularly dollar-based, investments in thewake of the yen revaluation; the enduring Japanese trade surplus, andthrect of protectionist measures against Japanese exports in key markets;and an evolving domestic industrial policy emphasiziag the structural andcost benefits of offshore production. As Japanese firms plan their globalproduction and distribution strategies around direct foreign investment,Japan could meet or exceed in twenty years the stock that took the U.S.more than eighty years to build.

1.03 Japanese firms have been participating in direct investmentabroad since the 1950s, with DPI concentrated on developing countries.About half of Japanese DFI went to developing countries in the 1970s,compared to 25X by the U.S. and 18% by the U.K. In the past decade,Japanese DFI has shifted to developed countries, notably the U.S. and theEuropean Community. A. pronounced sectoral shift has occurred from invest-ment in natural resources and light assembly to intermediace manufacturing,and more recently to commercial, financial and other services. EarlyJapanese DFI differed from western investmenr in the active role played byJapanese general trading companies, participation by small and mediumfirms, emphasis on long-term expansion of market share rather than maximiz-ing profits in the short run, and the influence of Japanese governmentpolicy. However, recent patterns of Japanese DFI have tended to convergewith DFI patterns from western sources.

1.04 This report examines patterns of Japanese DFI and its implica-tions for developing countries. It analyzes the driving forces behindregional and sectoral patterns, assesses potential Japanese DFI in develop-ing countries, and identifies the factors affecting this potential. Thereport identifies factors that have motivated Japanese DFI and describesthe problems investors have faced, with the purpose of helping countriesevaluate Japanese DPI. While there are both positive and negative aspects

1/ The 1987 U.S. net change in DFI position was US$49.2 billion. U.S.flow data (yearly change in net DFI position) include reinvested earn-ings, whereas Japanese data do not. Japanese statistics are based onnotifications and authorizations, not actual flows. Stock figures arecalculated by summing up notifications and auchorizations to a givenpoint in time. In contrast, U.S. official data are based on actualstock positions, and flows are derived from changes in stock. Thus,the two data sources are not strictly comparable, and care should betaken in their evaluation. See Appendix 1 for data and methodologicaldetails.

-2-

associated with OPI from the host country's perspective, the report doesnot attempt to evaluate the overall impact of Japanese DFI, such as income,employment, and technology transfer offects, in developing economies. Dataon DFI perforuance at the regional level, such as export performance, doprovide insight into general trends--some of which may be contrary toconventional wisdom.

1.05 Chapter 11 provides a historic overview of Japanese DPI flows,and Chapter III examines sectoral and regional patterns. The analysis inboth chapters relies on.official Japanese government statistics, the onlysource of detailed information on Japanese DPI. Chapter IV analyzesJapanese firms' motivation, management goals, and performance in DFI, basedon surveys by the Japanese government and private institutions. The roleof the Japanese government in private DPI also is analyzed. Chapter Vprovides a summary of findings and implications for developing countries.Appendixes contain methodological notes and caveats, and comprehensive dataon Japanese DFI.

(D-264c/2)

- 3 -

UI. OVERALL TRENDS OF JAPANESE DIRECT FOREIGN INVESTMENT

A. Growth of Japanese DFI

2.01 For 25 years after the Second World War, Japan concentrated itsavailable resources on domestic reconstruction. Japan's economy andforeign trade had the characteristics of a developing economy, and bo._ -X-Log abroad continued until the aid 1960se Japanese governmnt policiz. ondirect foreign investmnt were restrictive due to capital scarcity, concernabout capital outflow, and the possible negative foreign exchange impact ofoverseas activities.

2.02 As Japan's economy grew and the balance of payments improved, theGovernment took measures to encourage DFI in the late 1960. and early1970s. These policies and improved economic conditions helped Japanese OtIgrow rapidly (Chart 11.1). From 1971 to 1973, DFI flows exceeded all DPIstock ac.-amulated in previous years. Th4 pattern of growth was interruptedby the first oil price upheaval in 1974. In the 1980a, after recoveringfrom the second oil price shock, Japanese DPI experienced another upturn.In fiscal 1984, the annual flow of DPI exceeded US$10 billion for the firsttim. In 1986 it exceeded t'3$20 billion, and in 1987, DFI flows wereUS$33.4 billion. While the number of investments has increased modestly,the average investment amount has grown dramatically; between 1971 and1980, the average Japanese DFI was about US$2 million, by 1984 it was USS4million, and in 1987 almost US$8 million.

CHART 11.1 TRENDS IN JAPAN DFi fLOWS, 1951-1987

S billion S million

4-0 -10

35 _ ANNUAL DFI FLOWS (US 3 billion)_ - AVERAGE SIZE OF D1I (US S million) 8

30

25 6

204.

15

102

5

0 0

1951-70 71727374757677787980.81828384858687

Source: Public Finance and Financial Statistics. Ministry of Finance.

- 4-

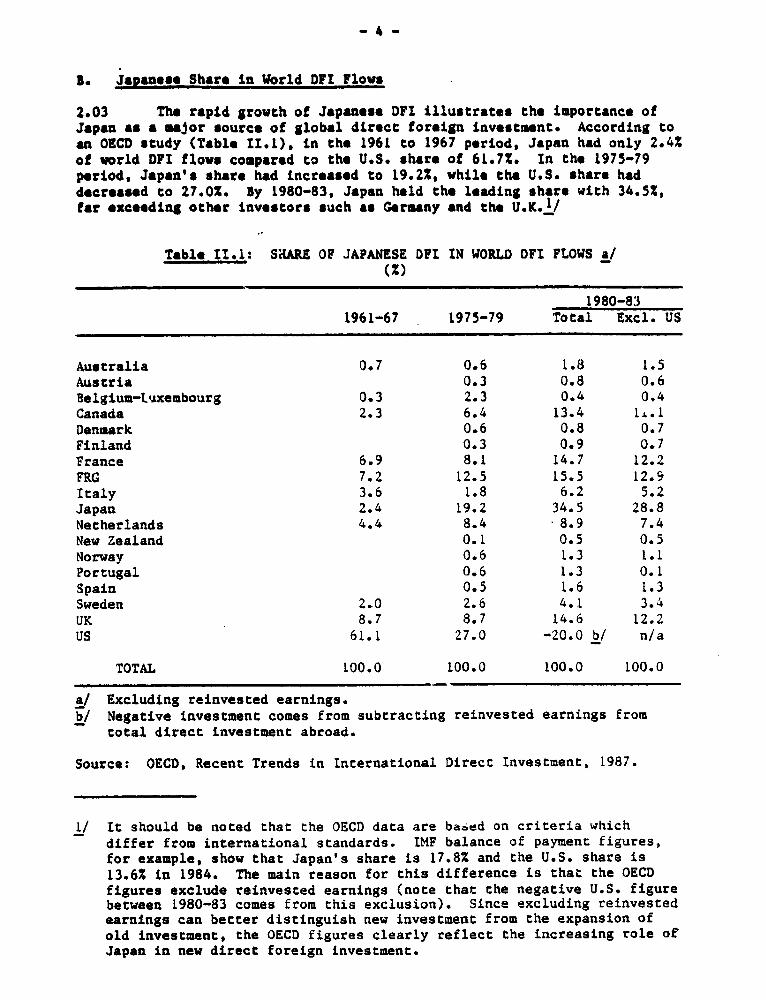

s. Japanese Share in World DFI Flows

2.03 The rapid growth of Japanese DFI illustrates the importance ofJapan as a major source of global direct foreign investment. According toan OECD study (Table 1I.1), in the 1961 to 1967 period, Japan had only 2.4%of world DFI flovs compared to the U.S. share of 61.7%. In the 1975-79period, Japan's share had increased to 19.2%, while the U.S. share haddecreased to 27.0%. By 1980-83, Japan held the leading share with 34.5%,far *xceeding other investors such as Germany and the U.K.1/

Table 11.1: SHARE OF JAPANESE DPI IN WORLD DPI FLOWS a/(%)

1980-831961-67 1975-79 Total Excl. US

Australia 0.7 0.6 1.8 1.5Austria 0.3 0.8 0.6Belgium-tuxembourg 0.3 2.3 0.4 0.4Canada 2.3 6.4 13.4 1L.1Denmark 0.6 0.8 0.7Finland 0.3 0.9 0.7France 6.9 8.1 14.7 12.2ERG 7.2 12.5 15.5 12.9Italy 3.6 1.8 6.2 5.2Japan 2.4 19.2 34.5 28.8Netherlands 4.4 8.4 8.9 7.4New Zealand 0.1 0.5 0.5Norway 0.6 1.3 1.1Portugal 0.6 1.3 0.1Spain 0.5 1.6 1.3Sweden 2.0 2.6 4.1 3.4UK 8.7 8.7 14.6 12.2US 61.1 27.0 -20.0 b/ n/a

TOTAL 100.0 100.0 100.0 100.0

a/ Excluding reinvested earnings.b/ Negative investment comes from subtracting reinvested earnings from

total direct investmenc abroad.

Source: OECD, Recent Trends in International Direct Investment, 1987.

1/ It should be noted that the OECD data are based on criteria whichdiffer from international standards. IMF balance of payment figures,for example, show that Japan's share is 17.8% and the U.S. share is13.6% in 1984. The main reason for this difference is that the OECDfigures exclude reinvested earnings (note that the negative U.S. figurebetween 1980-83 comes from this exclusion). Since excluding reinvestedearnings can better distinguish new investment from the expansion ofold investment, the OECD figures clearly reflect the increasing role ofJapan in new direct foreign investment.

s

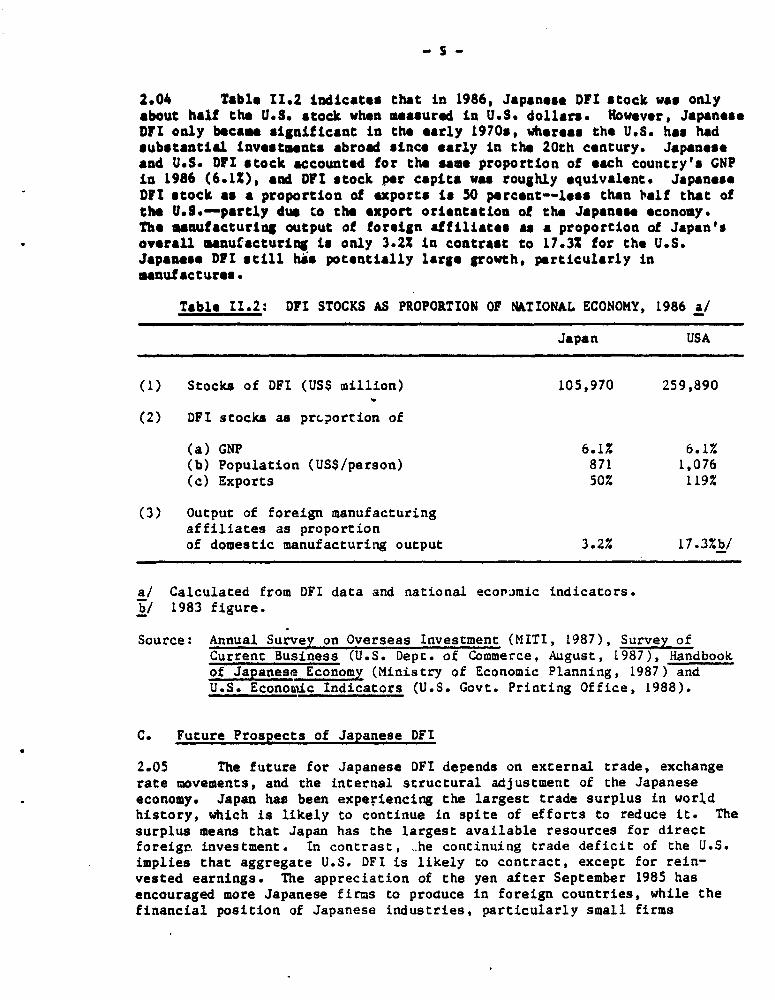

2.04 Table 11.2 indicates that in 1986, Japanese DFI stock was onlyabout half the U.S. stock when measured in U.S. dollars. However, JapaneseDJI only became significant in the early 1970s, whereas the U.S. has hadsubstantial investmsnts abroad since early in the 20th cantury. Japaneseand U.S. DFI stock accounted for the same proportion of each country's GNPln 1986 (6.1%), and DII stock per capita was roughly equivalent. JapaneseDFI stock as a proportion of exports is 50 percent--less than balf that ofthe U.S.--partly due to the export orientation of the Japanese economy.The manufacturing output of foreign affiliates as a proportion of Japan'soverall manufacturing is only 3.2% in contrast to 17.3% for the U.S.Japanese DFI still his potentially large growth, particularly inmanufactures.

Table 11.2: DFI STOCKS AS PROPORTION OF NATIONAL ECONOMY, 1986 a/

Japan USA

(1) Stocks of DFI (USS million) 105,970 259,890

(2) DFI scocks as prcporrion of

(a) GNP 6.1% 6.1%(b) Population (USS/person) 871 1,076(c) Exports 50% 119%

(3) Output of foreign manufacturingaffiliates as proportionof domestic manufacturing output 3.2% 17.3%b/

a/ Calculated from DFI data and national ecor'mic indicators.b/ 1983 figure.

Source: Annual Survey on Overseas Investment (MITI, 1987), Survey ofCurrent Business (U.S. Dept. of Commerce, August, 1987), Handbookof Japanese Economy (Ministry of Economic Planning, 1987) andU.S. EconotLic Indicators (U.S. Govt. Printing Office, 1988).

C. Future Prospects of Japanese DFI

2.05 The future for Japanese DFI depends on external trade, exchangerate movements, and the internal structural adjustment of the Japaneseeconomy. Japan has been experiencing the largest trade surplus in worldhistory, which is likely to continue in spite of efforts to reduce it. Thesurplus means that Japan has the largest available resources for directforeigr investment. In contrast, .he continuing trade deficit of the U.S.implies that aggregate U.S. DFI is likely to contract, except for rein-vested earnings. The appreciation of the yen after September 1985 hasencouraged more Japanese firms to proauce in foreign countries, while thefinancial position of Japanese industries, particularly small firms

Involved in export activities, has been deteriorating. Table 11.3 showsthe effect of the appreciation of the yen on Japanese firms' plans toLavest abroad. About 55Z of sampled firms say that the currency apprecia-tion will expedite their decision to go overseas. In processing andfabricating industries (e.g., electronics, transportation equipment, othermachinery), the impact of currency appreciation appears even stronger.

2.06 The Japanes sconoWy is In the process of substantial structuraladjustment. Japan, which has encouraged exports while restricting domesticconsumption, faces severe internal end external problems. A new program toencourage direct foreign investment was implemented in the aid 1980s. TheGovernment's Structural Adjustment Committee suggested in a report thatJapan should encourage DFI to promote dotestic efficiency and to reduce theexternal imbalance.

Table 11.3: IMPACT OF YEN APPRECIATION ON JAPANESE FIRMS'DFI DECISIONS, FY1986

(Survey result of Japanese firms)

Will Will ConsiderExpedite DFI Additional DFI NoDecisions After Analysis Influence

Total Manufacturing 55.5% 4.3% 40.5%Basic Materials 43.2% 3.8% 53.0%Processing/Fabrication 61.7% 4.8% 33.5%

Source: Annual Survey on Overseas investment (MITI, 1986).

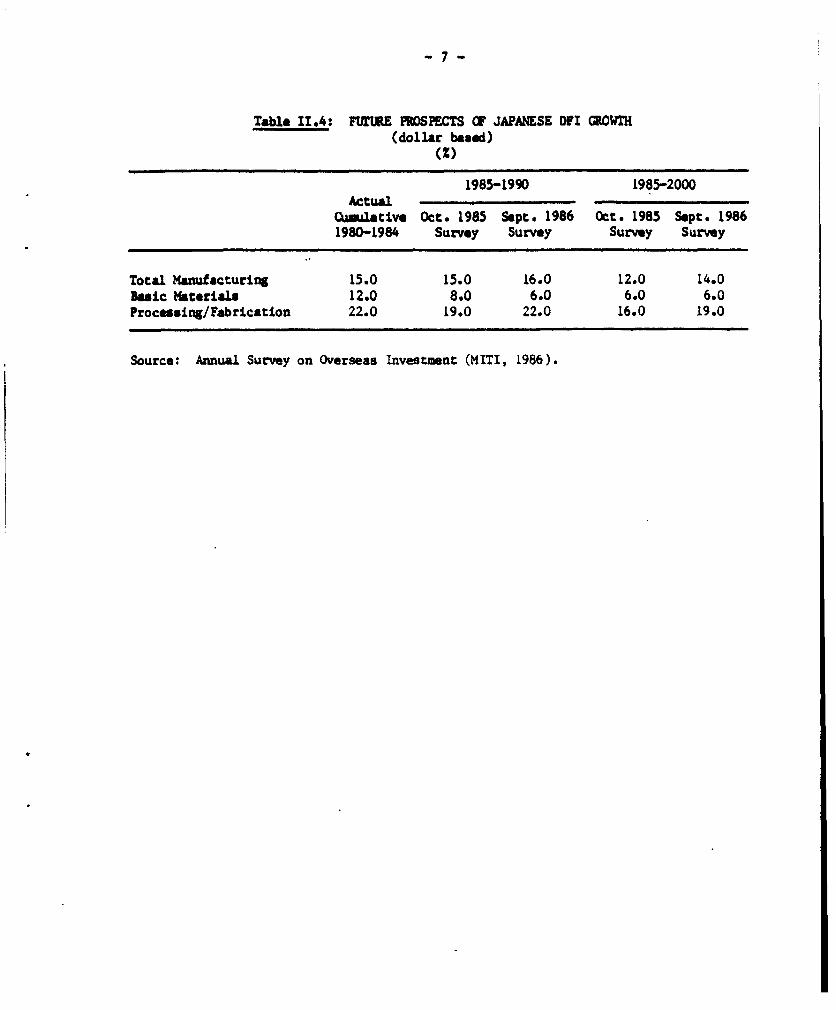

2.07 If external and internal conditions do not change, Japanese DFIis likely to maintain its growth. A survey of Japanese firms' expectationsof DFI growth supports this view in the short cerm (Table 11.4). The DFIgrowth rate for manufacturing in 1980-84 (15%) is expected to continue inthe 1985-90 period, mainly from growth in the processing and fabricatingindustries (19% to 22%). Reflecting longer-term uncertainties in theglobal economy, the projection for 1990-2000 shows slower growth rates inmanufacturing (12% to 14%), particularly in basic materials (6% to 8%).

- 7 -

Table 11.4: FUIURE FROSPECTS CF? JAPANESE DFI GROWTH(dollar based)

(x)

1985-1990 1985-2000Actualaumlative Oct. 1985 Sept. 1986 Oct. 1985 Sept. 1986

1980-1984 Survey Survey Survey Survey

Total Manufacturing 15.0 15.0 16.0 12.0 14.0Basic Materials 12.0 8.0 6.0 6.0 6.0Procesing/Fabrication 22.0 19.0 22.0 16.0 19.0

Source: Annual Survey on Overseas Investment (MITI, 1986).

- 8 -

III. SECTORAL AND REGIONAL DISTRIBUTION OF JAPANESE DFI

A. Sectoral Distribution

3.01 Before 1970, Japanese direct foreign investment was concentratedIn primary natural resources and, to a lesser extent, in labor intensivesecondary manufacturing. With few natural resources of its own, Japan hasbeen heavily dependent on securing resources abroad. MITI indicates thatJapan resains reliant on external sources for virtually all its rawmaterials, especially oil, iron ore, natural gas, copper, aluminum, andtin. By the mid-1960s, Japanese growth in natural resource-consumingindustries such as steel, shipbuilding and petrochemicals had advanced tothe point where arms-length imports alone could not assure a supply ofraw material. Direct foreign investment in raw materials was seen as anecessary element of a strategy to increase Japan's security in suppliesand as insurance against commodity import price fluctuations.

3.02 Japan also invested abroad in technologically standardized,labor-intensive industries such as textiles, metal products and other lightmanufactures. These investments reflected domestic labor shortages, whichbegan in the mid-1960s, and high wage costs relative to developingcountries. Early foreign ventures were initiated primarily by small andmedium manufacturing firms. These firms lacked the managerial skill andexpertise necessary to operate in foreign countries, and thus elected toform joint ventures with local or other foreign counterparts. In additionto the natural resource and labor-intensive manufacturing sectors, sometertiary commercial and service investment was made by general tradingcompanies, mainly to promote exports.

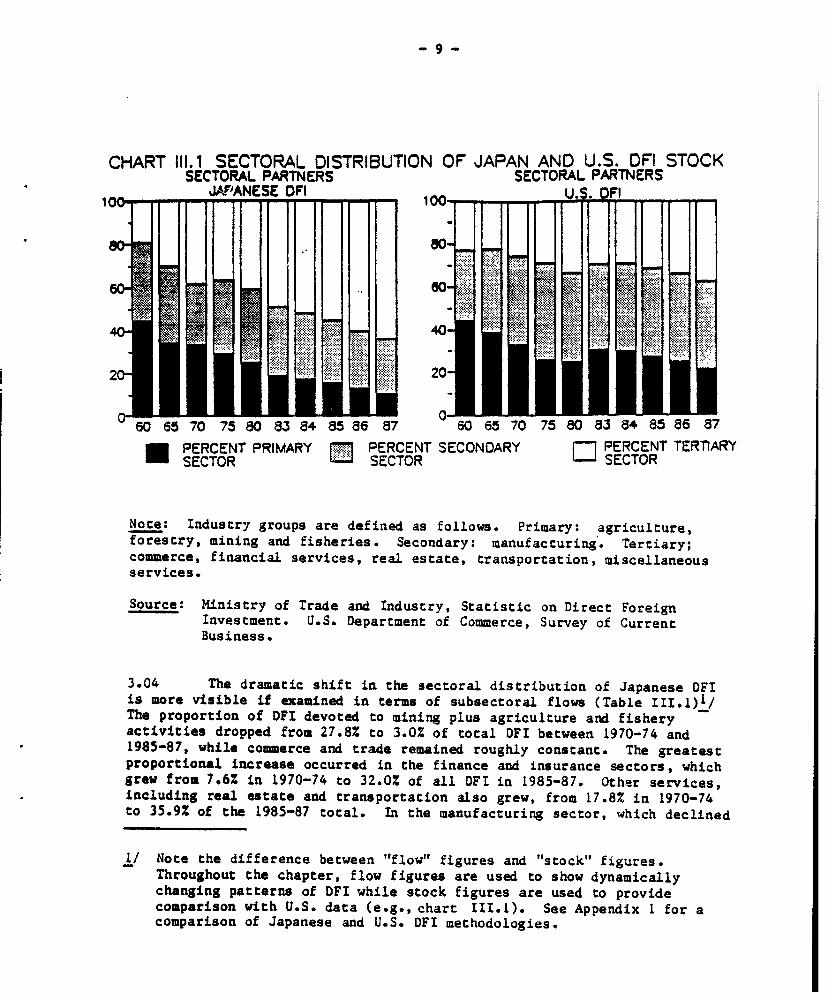

3.03 In the seventies and eighties, the overall value of Japanese DFIincreased sharply, with DFI in services and commerce growing rapidly. By1987, commerce and service DFI comprised over 60% of total Japaneseaccumulated stock. Japan's evolution presents an interesting comparisonwith the U.S. While the manufacturing share of Japanese DFI has beendecreasing (from 36% in 1960 to 25% in 1987), the share of manufacturing inU.S. DPI has remained fairly constant at about 40%. Although bothcountries experienced shifts from primary industries to the commerce andservice sector, Japan's reorientation has been much more substantial.Japan's primary sector decreased from 45% of total DFI in 1960 to 10% in1987, while the corresponding U.S. share fell from 45% to 20%. Japan'stertiary sector DFI increased from 20% in 1960 to over 60% in 1987, whilein the U.S. tertiary DFI increased from 22% to 37% (Chart II.1).

-9-

CHART 111.1 SECTORAL DISTRIBUTION OF JAPAN AND U.S. DFI STOCKSECTORAL PARTNERS SECTORAL PARTNERS

JAF"ANESE DFI U. O eF

80

20

20

60 65 70 75 80 83 84 85687 60657075 348586 87- PERCENT PRIMARY r PERCENT SECONOARY m PERCENT TERTIARY

- S ECTOR SECTOR 'iSECTOR

Note: Industry groups are defined as follows. Primary: agriculture,forestry, mining and fisheries. Secondary: manufacturing. Tertiary;commerce, financial services, real estate, transportation, miscellaneousservices.

Source: Ministry of Trade and Industry, Statistic on Direct ForeignInvestment. U.S. Department of Commerce, Survey of CurrentBusiness.

3.04 The dramatic shift in the sectoral distribution of Japanese DFIis more visible if examined in terms of subsectoral flows (Table III.1)1/The proportion of DEl devoted to mining plus agriculture and fisheryactivities dropped from 27.8% to 3.0% of total DFI between 1970-74 and1985-87, while commerce and trade remained roughly constant. The greatestproportional increase occurred in the finance and insurance sectors, whichgrew from 7.6% in 1970-74 to 32.0% of all OFI in 1985-87. Other services,including real estate and transportation also grew, from 17.8% in 1970-74to 35.9% of the 1985-87 total. In the manufacturing sector, which declined

1/ Note the difference between "flow" figures and "stock" figures.Throughout the chapter, flow figures are used to show dynamicallychanging patterns of DFI while stock figures are used to providecomparison with U.S. data (e.g., chart III.1). See Appendix 1 for acomparison of Japanese and U.S. DFI methodologies.

- 10 -

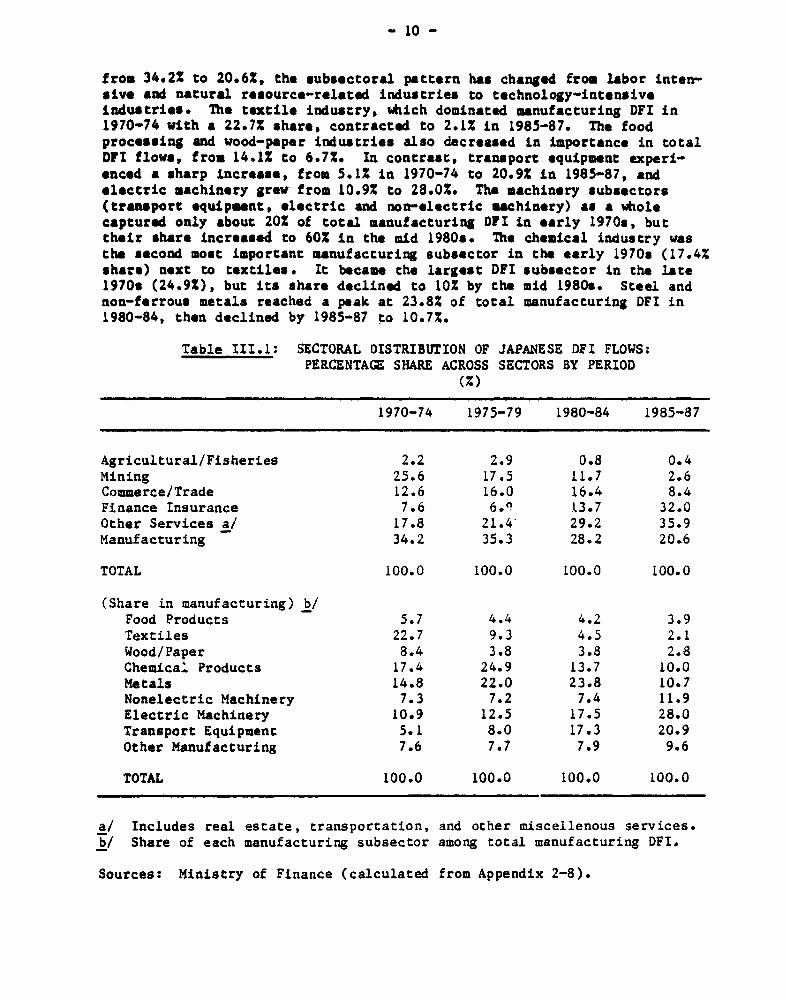

from 34.22 to 20.6%, the subsectoral pattern has changed from labor inten-sive and natural resource-related industries to technology-intensiveindustries. The textile industry, which dominated manufacturing DFI in1970-74 with a 22.7% share, contracted to 2.1% in 1985-87. The foodprocessing and wood-paper industries also decreased in importance in totalDFI flows, from 14X1X to 6.7%. In contrast, transport equipment experi-enced a sharp increase. from 5.1% in 1970-74 to 20.92 in 1985-87, andelectric machinery grew from 10.9% to 28.02. The machinery subsectors(transport equipment, electric and non-electric machinery) as a wholecaptured only about 202 of total manufacturing DPI in early 1970s, buttheir share increased to 60% in the mid 1980s. The chemical industry wasthe second most important manufacturing subsector in the early 1970s (17.4%share) next to textiles. It became the largest DFI subsector in the late1970s (24.92), but its share declined to 10% by the mid 1980t. Steel andnon-ferrous metals reached a peak at 23.8% of total manufacturing DFI in1980-84, then declined by 1985-87 to 10.7%.

Table III.1: SECTORAL DISTRIBUTION OF JAPANESE DFI FLOWS:PERCENTAGE SHARE ACROSS SECTORS BY PERIOD

(Z)

1970-74 1975-79 1980-84 1985-87

Agricultural/Fisheries 2.2 2.9 0.8 0.4Mining 25.6 17.5 11.7 2.6Commerce/Trade 12.6 16.0 16.4 8.4Finance Insurance 7.6 6.9 13.7 32.0Other Services a/ 17.8 21.4 29.2 35.9Manufacturing 34.2 35.3 28.2 20.6

TOTAL 100.0 100.0 100.0 100.0

(Share in manufacturing) b/Food Products 5.7 4.4 4.2 3.9Textiles 22.7 9.3 4.5 2.1Wood/Paper 8.4 3.8 3.8 2.8Chemical Products 17.4 24.9 13.7 10.0Metals 14.8 22.0 23.8 10.7Nonelectric Machinery 7.3 7.2 7.4 11.9Electric Machinery 10.9 12.5 17.5 28.0Transport Equipment 5.1 8.0 17.3 20.9Other Manufacturing 7.6 7.7 7.9 9.6

TOTAL 100.0 100.0 100.0 100.0

a/ Includes real estate, transportation, and other miscellenous services.b/ Share of each manufacturing subsector among total manufacturing DFI.

Sources: Ministry of Finance (calculated from Appendix 2-8).

- 11 -

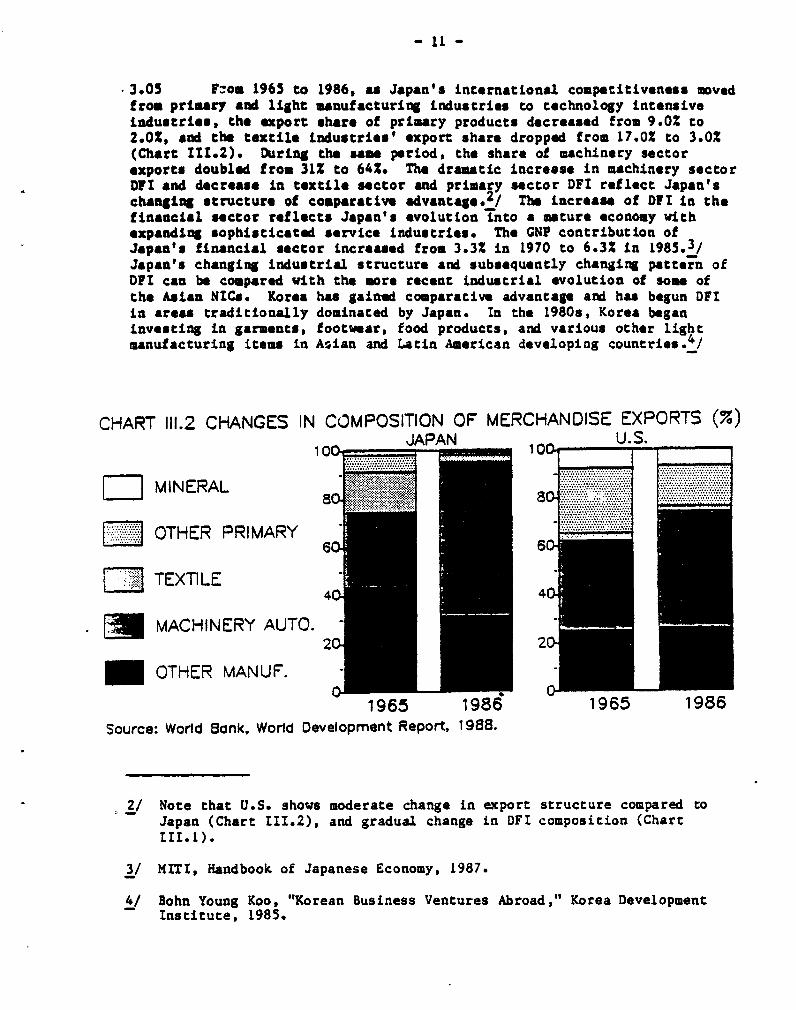

3.05 F-om 1965 to 1986, as Japan's international competitiveness movedfrom primary and light manufacturing Lndustries to technology intensiveindustries, the export share of primary products decreased from 9.0% to2.0%, and the textile industries' export share dropped from 17.0% to 3.0%(Chart 111.2). During the sme period, the share of machinery sectorexports doubled frou 312 to 64%. The draatic increase in machinery sectorDYI and decrease in textile sector and primary sector DFI reflect Japan'schanging structure of comparative advantage.2/ The increase of Oft in thefinancial sector reflects Japan's evolution into a mature economy withexpanding sophisticated service industries. The GNP contribution ofJapan's financial sector increased from 3.3% in 1970 to 6.3% in 1985.3/Japan's changing industrial structure and subsequently changing pattern ofOFI can be compared with the more recent industrial evolution of som ofthe Asian NICs. Korea has gain-d comparative advantage and has begun DFIin areas traditionally dominated by Japan. In the 1980s, Korea beganinvesting in garments, footwear, food products, and various other lightmanufacturing items in Asian and Latin American developing countries.4/

CHART 111.2 CHANGES IN COMPOSITION OF MERCHANDISE EXPORTS (%)10 ~ JAPAN 10.U.S.10C 10C

MINERAL

OTHER PRIMARY 66~~~~~~~

C TEXTILE

MACHINERY AUTO.

OTHER MANUF.

1965 1986 1965 1986Source: World Bank. World Development Report, 1988.

2/ Note that U.S. shows moderate change in export structure compared toJapan (Chart III.2), and gradual change in DFI composition (ChartIII.1).

3/ MITI, Handbook of Japanese Economy, 1987.

4/ Bohn Young Koo, "Korean Business Ventures Abroad," Korea DevelopmentInstitute, 1985.

- 12 -

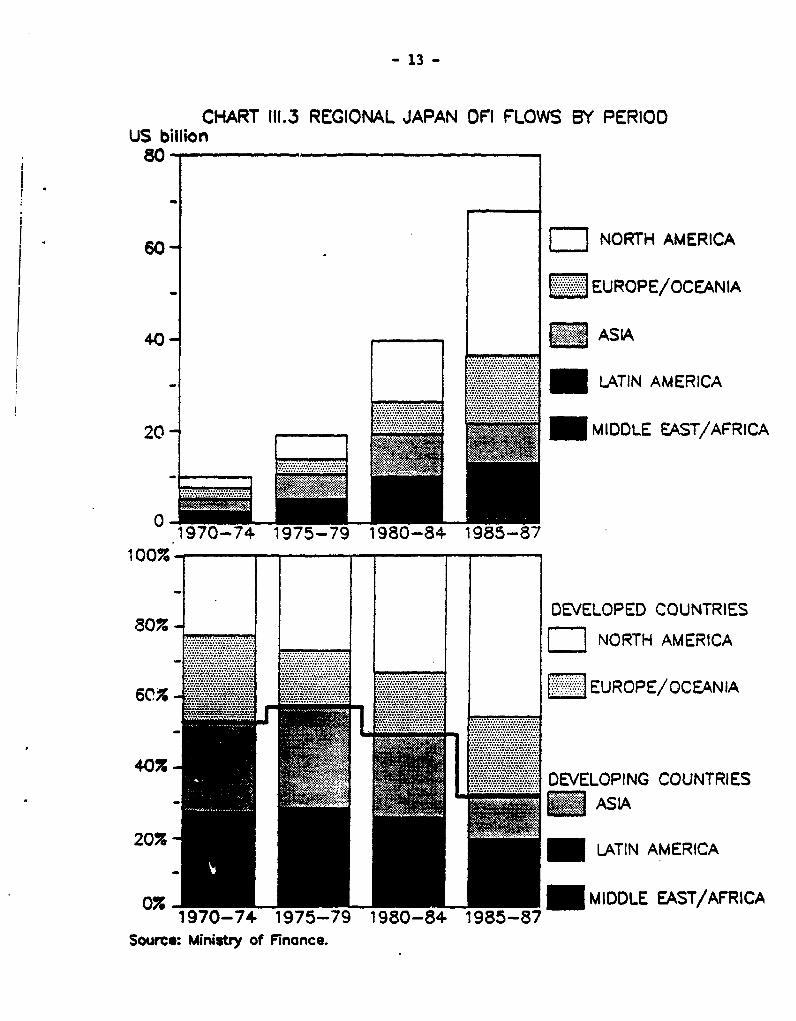

B. RAgional Distribution

3.06 In the eighties, the trend of Japanese DFI flows has been awayfrom developing markets and into irdustrialized countries (Chart 111.3).The share of DFI flows to developing countries has fallen by almost 20%,from 52.32 in 1970-74 to 32.0% in 1985-87.5/ U.S. foreign investment, incontrast, has overwhelmingly favored developed countries (see Appendix 4,Table 1). The proportion of U.S. OFt in doveloping countries reached 44%in 1959, but by 1970 the share fell to 27% aud has not exceeded 25% since.In 1987, U.S. DFI to developing countries amounted to 23%, or US$71 billionout of a total stock of US$305 billion.

3.07 The bulk of Japanese DYI growth since 1970 has beon in NorthAmerica, which between 1985-87 accounted for 46% of Japanese global flows,double the 23% share in the 1970-74 period. The value of flow to NorthAmerica more than doubled, from US$13 billion in 1980-84 to US$31 billionin 1985-87. Europe, with 18% of the total in 1985-87, saw flows more thandouble between 1980-84 and 1985-87. Asia had a slight decrease in thevalue of flown but saw its global share drop by almost half, from 24% to13%. Latin America had a slight decrease in global share but experienced asignificant increase in flow value, from US$7 billion to US$12 billion.Oceania had Little change in share but a modest increase in flow value,while both Africa and the Middle East experienced serious erosion in bothglobal share and value of DFI flows during the 1980s.

3.08 The vast majority of Japanese DFI destined for North America hasgone to the U.S. (Table II1.2). From 1951-87, the U.Sd- received USSS0billion, or 36% of global DPI flows, while Canada received only aboutUS$2.6 billion. Japanese DFI to the U.S. in the 1980s has been growing ata rate well above that of- Japanese DFI worldwide. The U.S. share of worldflows increased from 20% on average before 1970 to 40% in the 1980s; in1987 the share was 44% (see Appendix 3 for specific year flow figures bycountry). Canada was an important host country for Japanese DFI flows inthe earlier period (5.9% global share in 1951-70), but recently itsrelative attractiveness, based primarily on nacural.resources, hasdecreased (1.6% global DFI share in 1981-87).

5/ If DFI in offshore banking and flagship rights in the Caribbean andAfrica are excluded, developing countries share in 1985-87 dropped toless than 20% (see paragraph 3.13).

- 13 -

CHART 111.3 REGIONAL JAPAN DFI FLOWS BY PERIODUS billion

so-

NORTH AMERICA

- E: EUROPE/OCEANIA

40- C03ASIA

U .LATIN AMERICA

20 - MIDDLE EAST/AFRICA

1970-74 1975-79 1980-84 1985-87100% -I -

DEVELOPED COUNTRIES80%H o%W - NORTH AMERICA

_~~~~~~~~~~...... ....

I... ............ _.. EUROPE/OCEANIA

60%

.. DEVELOPING COUNTRIES

207_ LATIN AMERICA

0S _ - ~~~~~~~~MIDDLE EAST/AFRICA0x 1970-74 1975-79 1980-84 1985-87

Source: Ministry of Finance.

- 14 -

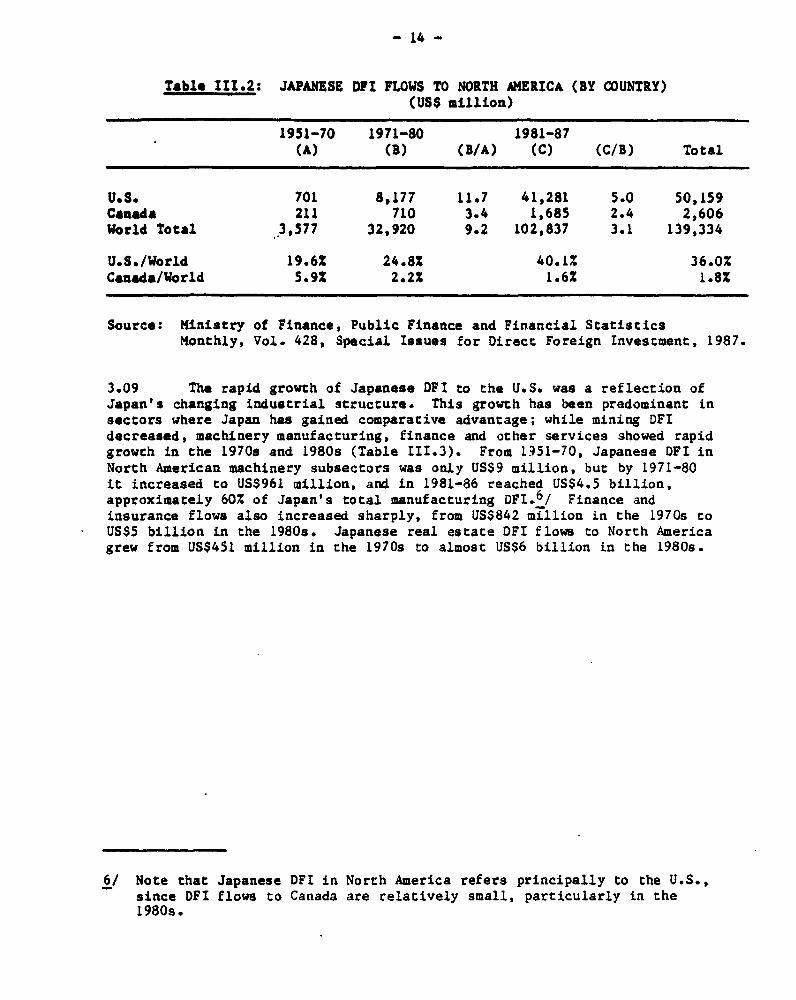

Table 111.2: JAPANESE DFI FLOWS TO NORTH AMERICA (BY COUNTRY)(US$ million)

1951-70 1971-80 1981-87(A) (B) (B/A) (C) (C/B) Total

U.S. 701 8,177 11.7 41,281 5.0 50,159Canada 211 710 3.4 1,685 2.4 2,606World Total 3,577 32,920 9.2 102,837 3.1 139,334

U.S./World 19.6% 24.8% 40.1% 36.0%Canada/World 5.92 2.22 1.6% 1.8%

Source: Ministry of Finance, Public Finance and Financial StatisticsMonthly, Vol. 428, Special Issues for Direct Foreign Investment, 1987.

3.09 The rapid growth of Japanese DFI to the U.S. was a reflection ofJapan's changing industrial structure. This growth has been predominant insectors where Japan has gained comparative advantage; while mining DFIdecreased, machinery manufacturing, finance and other services showed rapidgrowth in the 1970s and 1980s (Table 111.3). From 1351-70, Japanese DFI inNorth American machinery subsectors was only US$9 million, but by 1971-80it increased to US$961 million, and in 1981-86 reached US$4.5 billion,approximately 60% of Japan's total manufacturing DFI. 6 / Finance andinsurance flows also increased sharply, from US$842 million in the 1970s toUS$5 billion in the 1980s. Japanese real estate DFI flows to North Americagrew from US$451 million in the 1970s to almost US$6 billion in the 1980s.

6/ Note that Japanese DFI in North America refers principally to the U.S.,since DFI flows to Canada are relatively small, particularly in the1980s.

- 15 -

Table 111.3: JAPANESE DPI FLOWS TO NORTH AMERICA (BY SECTOR)(USS million)

1951-70 1971-80 1981-86 FY1951-86(A) (B) (B/A) (C) (C/B) Total

Manufacturing 217 2,211 10.2 7,477 3.4 9,915(Machinery) 9 961 106.8 4,503 4.7 5,473(Other Manufacturing) 208 1,250 4.5 2,974 2.4 4,432Mining 176 402 2.3 680 1.7 1,260Trade and Sales 306 3,189 10.4 4,974 1.6 8,479finance/Insurance 110 841 7.6 5,300 6.3 6,259Real Estate 34 451 13.3 5,755 12.8 6,253

Total 912 8,886 9.7 27,608 3.1 37,416

Source: Ministry of Finance (see Table 1114).

3.10 Two other factors have accelerated the rapid growth of JapaneseDFI in the U.S. First, a significant amount of manufacturing DFI was madeto reduce existing and potential trade friction caused by Japan's largetrade surplus with the U.S. In sectors particularly sensitive to protec-tionist pressures, such as automobiles, steel and electronics, productionin the U.S. market became a necessary strategy for many Japanese firmsconcerned with maintaining market share. Largely due to import quotas(referred to as voluntary restraint arrangements, or orderly marketingagreements) introduced by the U.S. in 1981, Japanese annual DFI in theautomobile sector increased from approximately USS20 million between1978-80 to US$200 million between 1981-83. In the steel sector, officialquotas imposed in 1984 led to a quadrupling of Japanese DFI. Similar traderestrictions resulted in increased Japanese DFI in the U.S. electronicssector, where many types of formal and informal trade arrangements existedbetween the U.S. and Japan in the 1970s and 1980s.

3.11 Second, the rapid appreciation of the yen against the dollar,beginning in 1985, created a strong incentive for investments in realestate and financial establishments. Investments in the banking, financialand insurance sectors facilitated the surge of Japanese portfolio anddirect foreign investment. Manufacturing investments also benefitted;Japanese firms made greenfield investments and stock acquisitions in U.S.companies to take advantage of the favorable exchange rate.

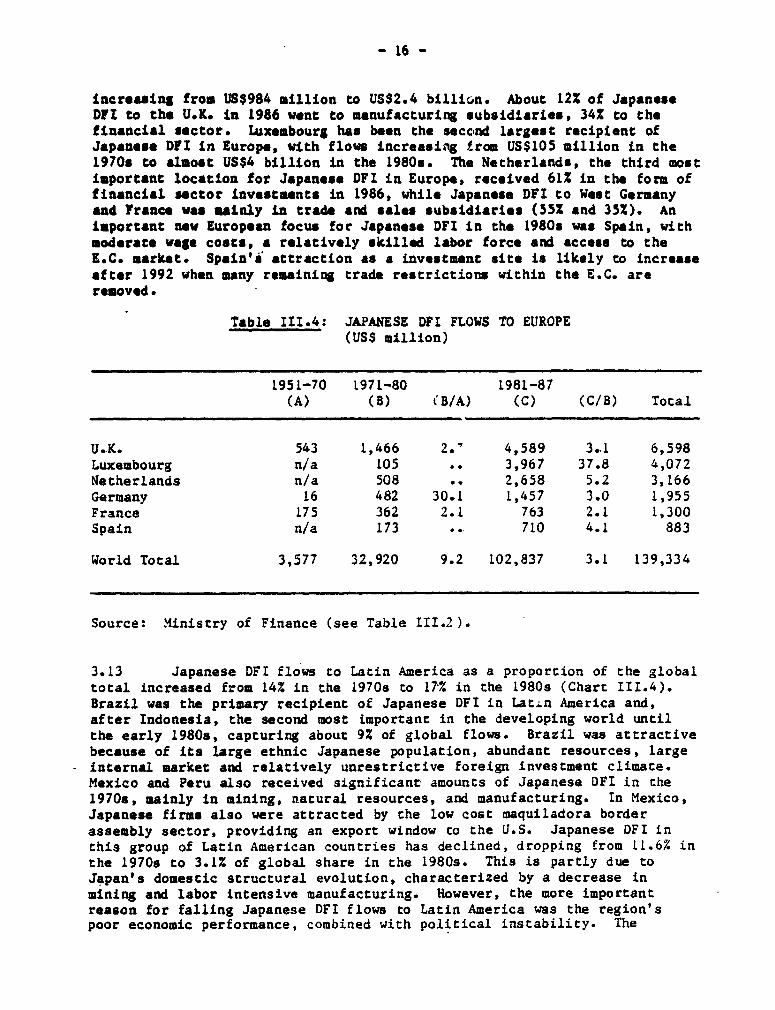

3.12 Europe, particularly the U.K., was a more important destinationthan North America for Japanese DFI during the 1950s and 1960s (Table111.4), with certain European countries receiving over 20% of globalJapanese DFI flows. DFI in these countries increased sharply during the1980s, influenced by the appreciation of the yen and increased tradefriction with European partners. The U.K. continued to be the principaltarget during the 1970s and 1980s, absorbing 5% of global Japanese DFIflows. Between 1986 and 1987, flows to the U.K. more than tripled,

- 16 -

increasing from US$984 million to US$2.4 billion. About 12% of JapaneseDFI to the U.K. in 1986 went to manufacturing subsidiaries, 34% to chefinancial sector. Luxembourg has been the secc,nd largest recipient ofJapanese DFI in Europe, with flows increasing trom US$105 million in the1970s to almost US$4 billion in the 1980s. The Netherlands, the third mostimportant location for Japanese DFI in Europe, received 612 in the form offinancial sector investments in 1986, while Japanese DFI to West Germanyand France wa mainly ln trade and sales subsidiaries (35% and 352). Animportant new European focus for Japanese DFI in the 1980s was Spain, withmoderate wage costs, a relatively skilled labor force and access to theK.C. market. Spain'i attraction as a investment site is likely to increaseafter 1992 when many remaining trade restrictions within the E.C. areremoved.

Table III.4: JAPANESE OFI FLOWS TO EUROPE(USS million)

1951-70 [971-80 1981-87(A) (B) (B/A) (C) (C/B) Total

U.K. 543 1,466 2.' 4,589 3.,1 6,598Luxembourg n/a 105 . 3,967 37.8 4,072Netherlands n/a 508 2,658 5.2 3,166Germany 16 482 30.1 1,457 3.0 1,955France 175 362 2.1 763 2.1 1,300Spain n/a 173 710 4.1 883

World Total 3,577 32,920 9.2 102,837 3.1 139,334

Source: Ministry of Finance (see Table III.2).

3.13 Japanese DFI flows to Latin America as a proportion of the globaltotal increased from 14% in the 1970s to 17% in the 1980s (Chart III.4).Brazil was the primary recipient of Japanese DFI in Latin America and,after Indonesia, the second most important in the developing world untilthe early 1980s, capturing about 9% of global flows. Brazil was attractivebecause of its large ethnic Japanese population, abundant resources, largeinternal market and relatively unrestrictive foreign investment climate.Mexico and Peru also received significant amounts of Japanese DFI in the1970s, mainly in mining, natural resources, and manufacturing. In Mexico,Japanese firms also were attracted by the low cost maquiladora borderassembly sector, providing an export window to the U.S. Japanese DFI inthis group of Latin American countries has declined, dropping from 11.6% inthe 1970s to 3.1% of global share in the 1980s. This is partly due toJapan's domestic structural evolution, characterized by a decrease inmining and labor intensive manufacturing. However, the more importantreason for falling Japanese DFI flows to Latin America was the region'spoor economic performance, combined with political instability. The

- 17 -

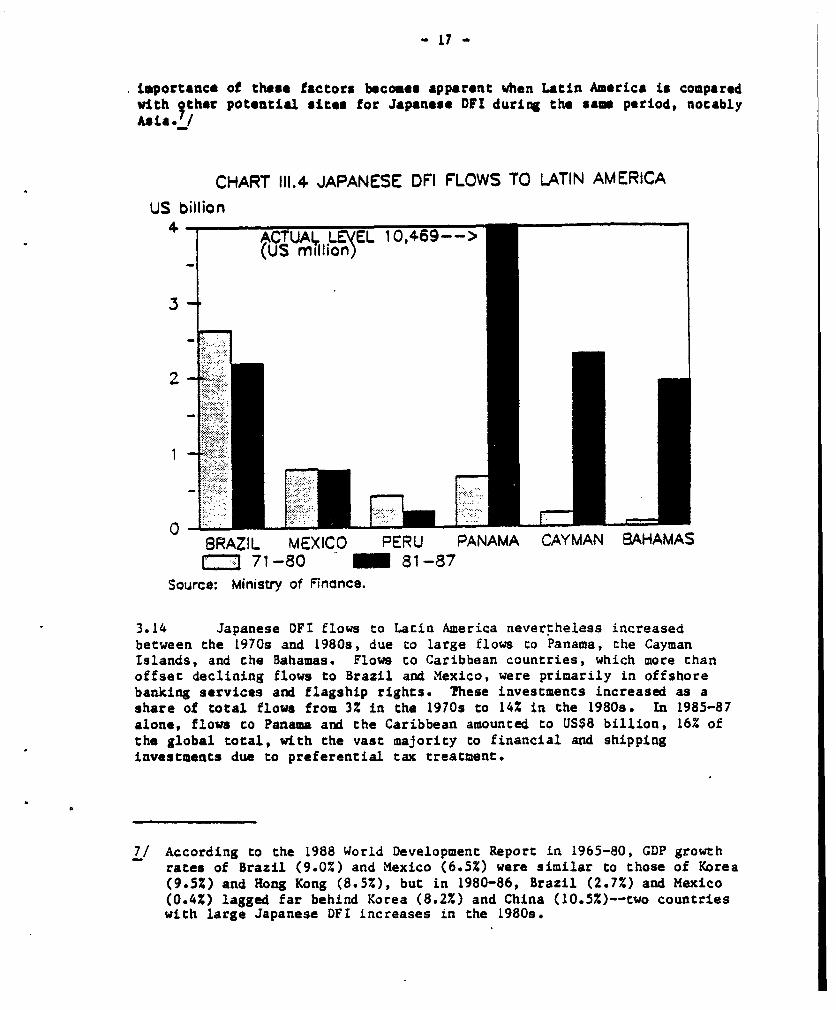

importance of these factors becomes apparent when Latin America is comparedwith gther potential sites for Japanese DFI during the same period, notablyAsia.

CHART 111.4 JAPANESE DFI FLOWS TO LATIN AMERICAUS billion

ACTUAL. L EL 10,469-->(US million

C --BAI E-'BRAZIL MEXICO PERU PANAMA CAYMAN BAHAMAS

71-80 81-87aource: Ministry of Finance.

3.14 Japanese DFI flows to Latin America nevertheless increasedbetween the 1970s and 1980s, due to large flows to Panama, the CaymanIslands, and the Bahamas. Flows to Caribbean countries, which more thanoffset declining flows to Brazil and Mexico, were primarily in offshorebanking services and flagship rights. These investments increased as ashare of total flows from 3% in the 1970s to 14% in the 1980s. In 1985-87alone, flows to Panama and the Caribbean amounted to US$8 billion, 16% ofthe global total, with the vast majority to financial and shippinginvestments due to preferential tax treatment.

7/ According to the 1988 World Development Report in 1965-80, GDP growthrates of Brazil (9.0%) and Mexico (6.5%) were similar to those of Korea(9.5%) and Hong Kong (8.5%), but in 1980-86, Brazil (2.7%) and Mexico(0.4%) lagged far behind Korea (8.2%) and China (10.5X)--two countrieswith large Japanese DFI increases in the 1980s.

- 18 -

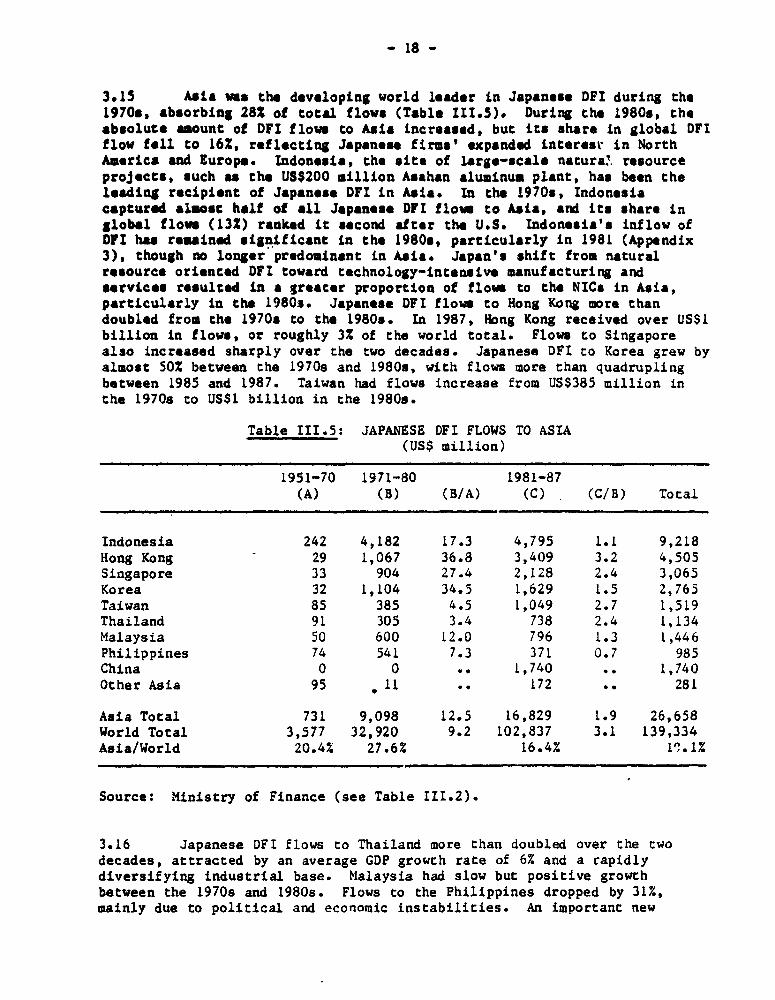

3.15 Asia was the developing world leader in Japanese DFI during the1970s, absorbing 28% of total flows (Table 111.5). During the 1980s, theabsolute amount of DFI flows to Asia increased, but its share in global OFIflow fell to 16%, reflecting Japanes firms' expanded interest in NorthAmerica and Europe. Indonesia, the site of large-scale natura. resourceprojects, such as the US$200 million Asahan aluminum plant, has been theloading recipient of Japanese DFI in Asia. In the 1970s, Indonesiacaptured almost half of all Japanese DPI flow to Asia, and its share inglobal flow (132) ranked it second after the U.S. Indonesia's inflow ofDPI has resained significant in the 1980s, particularly in 1981 (Appendix3), though no longer predominant in Asia. Japan's shift from naturalresource oriented DFI toward technology-intensive manufacturing andservices resulted in a greater proportion of flow to the NICs in Asia,particularly in the 1980-. Japanese DFI flows to Hong Kong more thandoubled from the 1970s to the 1980s. In 1987, Hong Kong received over US$1billion in flows, or roughly 3% of the world total. Flows to Singaporealso increased sharply over the two decades. Japanese DFI to Korea grew byalmost 50% between the 1970s and 19809, with flows more than quadruplingbetween 1985 and 1987. Taiwan had flows increase from US$385 million inthe 1970s to US$1 billion in the 1980s.

Table III.5: JAPANESE DFI FLOWS TO ASIA(US$ million)

1951-70 1971-80 1981-87(A) (B) (B/A) (C) (C/B) Total

Indonesia 242 4,182 17.3 4,795 1.1 9,218Hong Kong - 29 1,067 36.8 3,409 3.2 4,505Singapore 33 904 27.4 2,128 2.4 3,065Korea 32 1,104 34.5 1,629 1.5 2,765Taiwan 85 385 4.5 1,049 2.7 1,519Thailand 91 305 3.4 738 2.4 1,134Malaysia 50 600 12.0 796 1.3 1,446Philippines 74 541 7.3 371 0.7 985China 0 0 .. 1,740 .. 1,740Other Asia 95 . 11 . 172 .. 281

Asia Total 731 9,098 12.5 16,829 1.9 26,658World Total 3,577 32,920 9.2 102,837 3.1 139,334Asia/World 20.4% 27.6% 16.4% 19.1%

Source: Ministry of Finance (see Table II1.2).

3.16 Japanese DFI flows to Thailand more than doubled over the twodecades, attracted by an average GDP growth rate of 6% and a rapidlydiversifying industrial base. Malaysia had slow but positive growthbetween the 1970s and 1980s. Flows to the Philippines dropped by 31%,mainly due to political and economic instabilities. An important new

- 19 -

recipient of Japanes. DFI was the People's Republic of China, Flows toChina began in 1984; by 1987 China had 4% of the global total, aboutUS$1.2 billion out of US$33.4 billion. This was mainly attributed to theChinas economy's rapid growth (annual GDP growth rate of 10.52 in1980-86), large potential market, and the government's relatively openpolicy toward DFI.

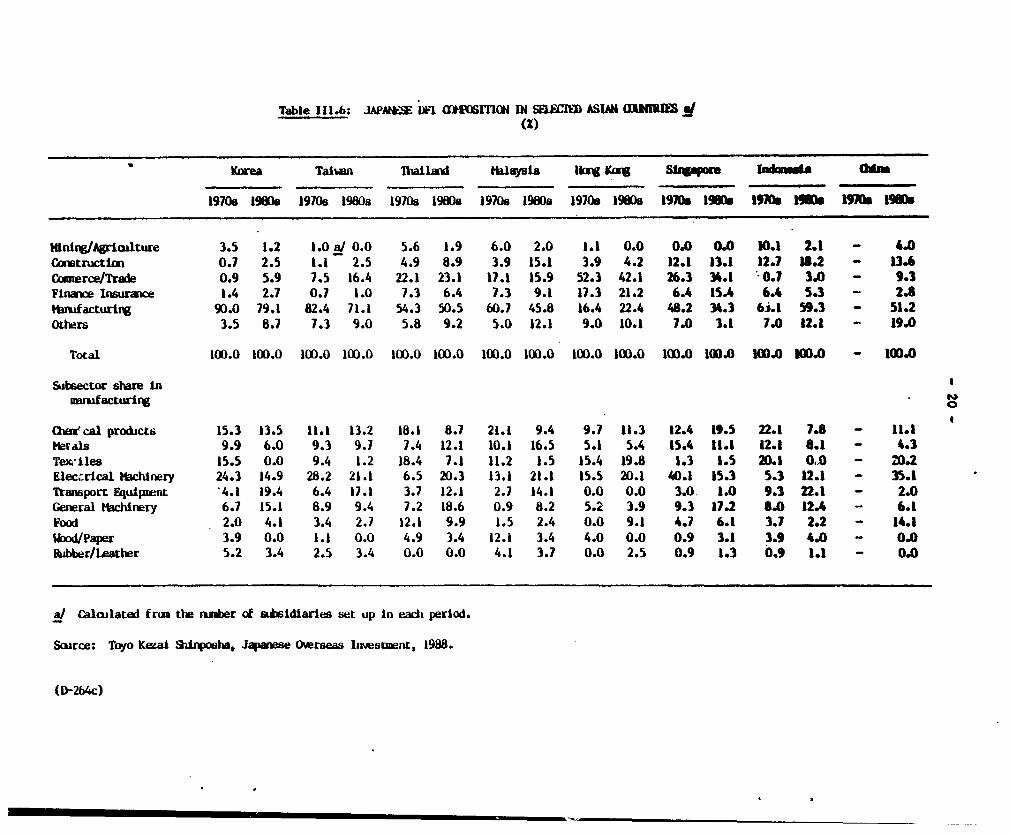

3.17 The composition of Japanese OFt in key Asian countries variedaccording to the economic strengths of the host country (Table ItI.6).8/About 902 of Japan*s" subsidiaries set up in Korea in the 19709 were in themanufacturing sector. The share dropptd to about 802 in the 1980s, butmanufacturing wae still dominant. Taiwan, similar to Korea, has receivedabout 70-80X in the' mnufacturing sector. In Thailand, the manufacturingsector has absorbed about half of Japanese DFI in that country, and thecombined share of commerce and trade sector has been 20%. Some 10% ofinvestment has gone to mining, agriculture and const uction. Malaysiashowed a similar pattern to Thailand but is notable for the increasingshare of DFI in its construction sector (from 3.9% in the 1970s to 15.1% inthe 1980s) and for the decreasing share in its manufacturing sector.

3.18 Hong Kong has had dominance in the commerce, trade and financialsectors (about 60X) with a share of 16% to 22% in the manufacturingsector. Singapore also has had dominance in commerce, trade and finance(about 30% to 502). Compared with Hong Kong, Singapore has received alarger share of manufacturing (30% to 48%) and construction (12%) DFI.Singapore irs also significant for the financial sector's increase in share(from 6.4% in the 1970s to 15.4% in the 1980s) and the sharp decrease inDFI in the manufacturing sector (from 48% to 34%). In Indonesia, theleading sector has been the manufacturing sector (about 60%). Mining,agriculture and construction sectors togeaher have had a relatively largeshare (about 20%). In China, beginning in the 1980s, the main sectors forDFI have been manufacturing (51%) and construction (13%).

3.19 Leading manufacturing subsectors for Japanese DFI in most Asiancountries in the 1970s were electrical machinery, cextiles and cnemicals(Table III.6). In Korea, Taiwan, Hong Kong and Malaysia these were the topthree sectors, but Asian countries, in general, had comparative advantagein these sectors in the 1970s. The only exception is Singapore, whosenegligible textile share indicated a lack of comparative advantage intextiles. In the 1980s, the textile industry dropped from among the topsubsectors in almost every country except China. In Korea, Taiwan,Singapore and Thailand, more capital and technology intensive subsectorssuch as transport equipment and general machinery replaced textiles andchemicals. The direction of Japanese DFI toward electrical machinery couldbe observed in two broad groups: its share dropped in Korea, Taiwan andSingapore but increased in Thailand, Malaysia and Indonesia. Chemicalproducts and other basic material industries, including metals, decreasedin share in the 1980s but were still significant in many Asian countries.

8/ DFI composition used in this section is derived from the number ofinvestments. It can be regarded as an indirect indicator of sectoraldistribution of DFI amount.

Table 111.6: JAPAN.E UF1 O1fM 1T1S 4 IN SECIM ASWIM 1 NIU (Z)

Korea Tai1n lbailld h.laysa lIkwg e SiaUqbo Idm Gum

1970. 196O0 1970s 1980s 1970s M9e08 1970. 1980e 19700 9e 1970l9hs 1970 19W) 1910 19S00

mining/hgriul.ture 3.5 1.2 1.0 a/ 0.0 5.6 1.9 6.0 2.0 1.1 0.0 0.0 0.0 10.1 2.1 - 4.0

mstnuctioE 0.7 2.5 1.1 2.5 4.9 8.9 3.9 15.1 3.9 4.2 12.1 13.1 12.7 18.2 - 13.6

Caerce/Trade 0.9 5.9 7.5 16.4 22.1 23.1 17.1 15.9 52.3 42.1 26.3 34.1 0.7 3.0 - 9.3

Finane Insurance 1.4 2.7 0.7 1.0 7.3 6.4 1.3 9.1 17.3 21.2 6.4 ISA 6.4 5.3 - 2.8

hmuacturtig 90.0 79.1 82.4 71.1 54.3 50.5 60.7 45.8 16.4 22.4 48.2 34.3 6j.1 59.3 - 51.2

Others 3.5 8.7 7.3 9.0 5.8 9.2 5.0 12.1 9.0 10.1 7.0 3.1 7.0 12.1 - 19.0

Total 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 - 100.0

Subsector share inDarufacturirg

O z:cal proicts 15.3 13.5 11.1 13.2 18.1 8.7 21.1 9.4 9.7 11.3 12.4 19.5 22.1 7.8 - 11.1

metals 9.9 6.0 9.3 9.7 7.4 12.1 10.1 16.5 5.1 5.4 15.4 11.1 12.1 6.1 - 4.3

Tex iles 15.5 0.0 9.4 1.2 18.4 7.1 11.2 1.5 15.4 19.8 1.3 1.5 20.1 0o.n - 20.2

Elec.rical Machinery 24.3 14.9 28.2 21.1 6.5 20.3 13.1 21.1 15.5 20.1 40.1 15.3 5.3 12.1 - 35.1

Transport Equipment '4.1 19.4 6.4 17.1 3.7 12.1 2.7 14.1 0.0 0.0 3.0 1.0 9.3 22.1 - 2.0

General Machinery 6.7 15.1 8.9 9.4 7.2 18.6 0.9 8.2 5.2 3.9 9.3 17.2 8.0 12.4 - 6.1

Food 2.0 4.1 3.4 2.7 12.1 9.9 1.5 2.4 0.0 9.1 4.7 6.1 3.7 2.2 - 14.1

WJoodJPaper 3.9 0.0 1.1 0.0 4.9 3.4 12.1 3.4 4.0 0.0 0.9 3.1 3.9 4.0 - 0.0

Rkbber/Leather 5.2 3.4 2.5 3.4 0.0 0.0 4.1 3.7 0.0 2.5 0.9 1.3 0.9 1.1 - 0.0

al Calculated fro the amber of aisidiaries set up in eadc period.

Source: Toyo Kezal Sinposha, Jqapese Overseas Irvestent, 198B.

(D-264c)

- 21 -

3.20 Japanese DFI to Oceania has been dosinated by Australia, whichcaptured an average 6S of global DPI from 1951-80. The absolute value of

Japanese DPI to Australia almost doubled from the 1970s to the 1980s, butthe global share dropped to 3%. Although a significant amount of DFIcontinues in mining (33% of subsidiaries in 1986) and other naturalresources, Australia is also absorbing significant amounts of manufacturingDFI (21x). In Africa, Japanese DPI flows have bean very low, with the

exception of Liberia. Between 1980 and 1987, Liberia accounted for 88% ofJapanese DPI flows to Africa. Liberia received a negligible amount ofJapacese DFI before 1970, but flows increased until they reached over US$3billion in the 1980s, or approximately 2% of the global total. Virtuallyall of this DFI has been in the transportation service sector, namely flag-ship rights for Japanese vessels. In the Middle East, DFI flows to Iran,Saudi Arabia and Kuwait accounted for more than 52 of global flows duringthe 1970s but dwindled to less than 1% in the 1980s. Investments wereprimarily in the petroleum sector, although Iran received some manufactur-ing DFI in the 19709. Factors contributing to this region's decline in the1980s have been the Persian Gulf war and the sagging oil market.

C. Cnnclusion

3.21 Table 111.7 summarizes fundamental regional and sectoral shiftsin Japanese DFI between 1976 and 1986, showing that chree striking changesin Japanese DFI patterns took place during that time. First, mining DFIflows shrank an average 4% annually. The proportion received by Asiadeclined by 45% points, and Africa by 12% points, while Japanese DFI inmining increased in Oceania, North America and Latin America. Second,manufacturing sector DFI gr- by an annual average of 14%. North America'sshare in the manufacturing iector increased from 22% to 58%, and Europe'sfrom 5% to 10%. The proportion of manufacturing OFt decreased in LatinAmerica (24% to 7%) and the Middle East (17% to 0%). Third, finance andinsurance DFI increased by an average of 42%, and "other service" DFI(including real estate and t. -asportation) increased by an average 17% peryear. In the dynamic finance and insurance sector, Latin America's globalshare increased from 5% to 35% while North America's dropped from 52% to28% over the 12 years. Regions Z shares in other services expanded by 40%points in North America and 9% points in Latin America, while decreasing in

Europe, the M4iddle- East and Africa.

3.22 These patterns of sectoral growth and regional shifts in JapaneseDFI can be attributed to four main causes. The first and most important isJapan's own changing industrial structure. In scarcely more than a decade,

the focus of the Japanese economy, and the core of its international com-petitiveness, moved from natural resources and light manufacturing tohigher technology, capital-intensive manufacturing and services. Thisshift is reflected in the changing proportion of these sectors' contribu-tion to Japan's GDP and share in DFI. As DFI in higher technology andservice segments replaced labor intensive manufacturing and naturalresources, the overall level of Japanese DFI increased sharply and shiftedfrom developing to developed countries. Second, Japan's large and growingtrade surplus with its U.S. and European trading partners resulted inprotectionist measures against Japanese exports in key sectors. Thismotivated many Japanese firms to set up manufacturing facilities in NorthAmerica and Europe to minimize trade friction and protect market share.

- 22 -

Table 111.7: REGIONAL DISTRIBUrION OF JAPANESE DFI FLOWS BY SECTOR, FY1976(% share)

Agriculture/ Comm rce/ Finance/Fisheries Mining Manuf. Trade Insurance Other a/ Total

North America 18.8 3.3 21.7 56.3 51.8 17.2 21.6Europe 0.0 0.7 4.8 23.1 30.9 16.7 9.7Oceania 21.9 0.5 4.1 2.7 1.8 12.2 4.7

Total; DevelopedCountries 40.6 4.5 30.6 82.1 84.5 46.1 36.0

Asia 32.8 80.3 27.8 9.9 10.0 9.4 36.0Latin America 20.3 2.7 24.1 7.7 4.5 10.6 12.1Middle East 0.0 0.5 17.2 0.2 0.9 13.2 8.0Africa 6.3 11.9 0.4 0.0 0.0 20.7 7.9

Total: DevelopingCountries 59.4 95.5 69.4 17.9 15.5 53.9 64.0

World Total 100.0 100.0 100.0 100.0 100.0 100.0 100.0

rEGIONAL DISIRIBUION OF JAPANESE DFI FLOWS BY SECTOR, FY1986(% share)

Agriculture/ Commerce/ Finance/Fisheries Mining Manuf. Trade Insurance Other a/ Total

North America 26.1 17.6 57.8 56.3 28.4 57.0 46.8Europe 0.0 4.0 9.7 20.9 31.5 4.6 15.5Oceania 13.0 28.8 4.0 4.5 1.3 5.4 4.4

Total: DevelopedCountries 39.1 50.5 71.5 81.6 61.2 67.0 66.8

Asia 13.0 35.6 21.1 11.3 4.0 9.0 10.4Latin America 30.4 13.9 7.2 7.0 34.8 20.0 21.2Middle East 0.0 0.0 0.0 0.0 0.0 0.5 0.2Africa 17.4 0.0 0.2 0.0 0.0 3.4 1.4

Total: DevelopingCountries 60.9 49.5 28.5 18.4 38.8 33.0 33.2

World Total 100.0 100.0 100.0 100.0 100.0 100.0 100.0

a/ Includes real estate, transporcation, and other miscellaneous service DFI.

Source: MITI, 1987 Survey.

- 23 -

3.23 Third, the rapid appreciation of the yen accelerated DFI flows tothe U.S. and, to a lesser extent, to Europe. Fourth, the relative economicperformance of developing cenuntries has led to regional shifts in JapaneseDFI. Poor economic performance among developing countries in Lacin Americaand Africa, and the declining economic importance of the Middle East, havediminished Japanese DFI flows to these regions. In many cases, economicdeterioration has been accompanied by political instability and risk. Theexceptions to the overall negative trend of Japanese DFI in these regionshave been rapidly growing tax-related financial and shipping rights invest-ments in Liberia, Panama and the Caribbean. At the same time, the strongeconomic performance of many Asian developing countries and NICs has drawnincreasing amounts of Japanese DFI, particularly in machinery and finance.

- 24 -

IV. CHARACTERISTICS OF JAPANESE DFI

A. Nature of Investors

4.01 Four types of Japanese firms are involved in direct foreigninvestment: general trading companies, small and modium scale firms, largemanufacturing enterprises and financial institutions. General tradingcompanies hold a pivotal place in the Japanese economy, having made largeoverseas investments themselves and acting as promoters of other firms'DFI. Small and medium scale firms-mostly manufacturing-activelyparticipated in DFI in the early 1970s, experienced some downturn there-after, but gained increasing importance after the currency appreciation.Major manufacturers, such as Sony and Nissan, have made DFI part of theirglobal strategy, and the role of such firms is increasing compared togeneral trading companies. Since 1985, insurance companies and banks havebeen large sources of Japanese DFI. About 30% of total Japanese DFI flowis in the finance and insurance sector (Chaptar III). Most of this DFI hasgone to expand portfolio and other financial activities in the U.S., theU.K. and some Caribbean countries, through acquisition or establishment ofsubsidiaries.l/ Since this report is primarily concerned with the impli-cations and trends of directly productive DFI in developing countries,further analysis of financial institutions will not be included in thissection.

4.02 General trading companies have been the leading multinationals inJapan's trading investment ventures (Table IV.1). In 1979, the cop fourforeign investors were general trading companies--namely, Mitsui & Co.,Mitsubishi Corporation, Marubeni Corporation and C. Itoh and Company. Ninetrading companies were among the 25 largest investors and had a share of55%. In 1987, Nissan Motor Company, which is not a general trading compa-ny, moved to second place. The share of general trading companies amongthe top 25 companies decreased to 48%, with the top four general tradingcompanies' share decreasing from 42% in 1979 to 28% in 1987. Althoughtheir share is decreaeing, trading companies still maintain an importantposition in japanese DFI, particularly if insurance companies are excluded.

4.03 Since the primary objective of general trading companies' invest-ment is to expand trade, a large share of their investment has been made toset up sales and import subsidiaries. About 60% of the subsidiaries ofgeneral trading companies are in sales and trade. General trading compa-nies, also invest in the manufacturing sector, often uncovering opportuni-ties to add value and expand sales through manufacturing activities. Forexample, in ASEAN countries, 45% of the subsidiaries of the general tradingcompanies are in manufacturing, while only 11 percent of Japanese subsidia-ries in the U.S. are engaged in manufacturing.

1/ In the U.S., for example, Nippon Life Insurance bought US$538 millionstock of Shearson Lehman Brothers, Inc. in 1987. In developingcountries such as Panama, the Cayman Islands and the Bahamas, forexample, Japanese financial sector DFI is attracted by preferential taxtreatment and other incentives encouraging offshore banking. It isquestionable how much of this DFI is subsequently filtered throughother sectors of the host country economy.

lable IV.1: DFI BY MAJOR CORPORATIONS(In Yen 100 million)

1 99 1 9 8 7 */

Cumulative CumulativeRanking Company Name Investment Ranking Company Name Investmnt

I Mitsui & Co * 2,353 1 Mitsubishi Corp * 6,0672 Mitsubishi Corporation * 1,581 2 Nissan Motor 3,9283 Marubeni Corporation * 1,552 3 Nisshi-Iwai * 3,7044 C. Itoh 6 Co. * 1,262 4 Harubeni Corp. * 3,3245 Japan Asahan Aluminium 870 5 Mitsui & Co.* 3,2446 Sumitoo Corporation * S88 6 Japan Asaban Aluminium 2,7227 Matsushita Electric Industries 674 7 Sumitamo Corp.* 2,3268 Nissan Motor 569 8 C. Itch 6 Co.* 2,2899 Nissho-Iwai * 569 9 Isuzu Motors 2,200

10 Toray 568 10 Mitsui Real Estate Development 1,70011 Tomen* 478 11 Tokyo Lease 1,52512 Honda Motor 439 12 Japan Oil Development 1,48613 Kawasaki Steel 422 13 Yoshida Kogyo 1,30814 Sanyo Electric 386 14 Sony 1,30115 Shin Nihon Steel 381 15 Nippon Kokan 1,16116 Sony 376 16 Nichimen Jitsugyo * 1,08917 Mitsubishi Heavy Industries 353 17 Nippon Amazon Aluminium 1,03918 Ishikawajima-Harima Heavy Industries 350 18 Kanematsu Gosho * 94319 KanematstA Copho * 340 19 Toshiba Corp. 92420 Japan Usiminus 325 20 Koto Oil Development 90021 Kawasaki Heavy Industries 314 21 Matsushita Electric 90022 Tokyo Kyuku Dentetsu 300 22 NEC Corp. 90023 Teijin 293 23 Tomen * 81324 Nichimen Jitsugyo * 289 24 Dianippon Ink & Chemical 78425 Tokyo Shib-ura Electric 282 25 Sharp 698

* General Trading Companies.a/ Exclude insurance companies and banks.

Source: K. Kojima and T. Ozawa "Japan's General Trading Companies" 1984.Toyo Kezai, "Japanese Overseas Investment 1988."

(D-264a)

- 26 -

4.04 Since general trading companies are major importers of naturalresources for Japan, they often engage in joint partnerships with majorconsumers for natural resource development projects. Trading companieshave the needed global information and marketing networks, and are able tomobilize major financing for projects that require large investment andsophisticated organizational skills. General trading companies alsosupport other Japanese investors through information gathering and dissemi-nation, loans, and organization of startup activities for less experiencedfirms.

4.05 Small and medium scale Japanese firm 4have had substantialinvestments in the manufacturing sectors of developing countries.2/Assisted by general trading companies in market intelligence, sales anddistribution, smaller firms have concentrated on developing strong produc-tion facilities. Most overseas manufacturing ventures set up by the smalland medium scale firms have been in technologically standardized, rela-tively labor-intensive subsectors, such as textiles, metal products, basicchemicals and miscellaneous goods (toys, glasses and shoes). As theJapanese economy became more technologically sophisticated, the investmentshare of small and medium scale industries decreased from 40X in the early1970s to 20Z by 1984. Since the dramatic yen appreciation began in 1985,many Japanese export-oriented small and medium scale firms have had severefinancial problems and have moved their production facilities to countrieswith lower factory costs. Since 1983, figures or the share of Japanesesmall and medium scale industrial investment show an upward trend.

Table IV.2: ShARE OF SMALL AND MEDIUM INVESTORSIN JAPANESE DFI, FY1973-85

(x)

Year Small to Medium Large Total

1973 43.3 56.7 100.01974 36.3 63.7 100.01975 37.9 62.1 100.01976 36.5 63.5 100.01977 30.2 66.3 100.01978 33.7 66.3 100.01979 33.4 66.6 100.C1980 30.7 69.3 100.01981 30A8 69.2 100.01982 27.1 72.9 100.01983 22.1 77.9 100.01984 22.9 77.1 100.01985 25.3 74.7 100.0

Source: Annual Survey on Overseas Investment, MITI, 1987.

2/ Small and medium scale firms are defined by the size of capital:Agriculture, mining, construction, manufacturing: below Y 100 million.Wholesale : below Y 30 million.Retail and service : below Y 10 million.

- 27 -

4.08 Large manufacturing companies. As large Japanese manufacturingcompanies gained capabilities in gathering information, marketing, andsetting up production abroad, they expanded investment in foreign manufac-turing and distribution facilities. Major --rnational players are theautomobile companies (Nissan, Toyota, Honda) ctrical appliancecompanies (Sony, Toshiba), and steel and heav, .,.schinery companies (NipponKokan, Kawasaki Steel). The number of subsidiaries as of 1987 (Table IV.3)gives a rough indication of the relative importance of large manufacturingcompanies in Japanese DFI. Large manufacturing companies represent 3,148foreign subsidiaries, with an average of 4.7 subsidiaries per firm.Electric and electronics companies lead with 800 subsidiaries, followed byautomobile companies with 405 subsidiaries. Steel companies, representing167 subsidiaries, have the highest average number of subsidiaries per firm(15.2). The general trading companies have a total of 2,051 subsidiaries,and an average 7.2 subsidiaries per firm. Most small and medium scaleparent companies have only one subsidiary each.

Table IV.3: NUMBER oF SUBSIDIARES BY TYPE OF PARENT 0MPANY, FY1985

Small and MediumSectors Large Companies Scale Firms Total

Agriculture, Fishery, Forest 60 (8.6) 12 (1.5) 72 (4.8)Mining 42 (1.9) 0 (0.0) 42 (1.9)Construction 188 (3.8) 8 (4.0) 196 (3.8)Manufacturing total 3,148 (4.7) 28" (1.2) 3,435 (3.8)

Food products 104 (3.1) 20 (1.3) 124 (2.5)Textiles 210 (6.0) 18 (1.2) 228 (4.6)Wood products 45 (2.0) 6 (1.0) 51 (1.8)Chemicals 388 (3.6) 14 (1.1) 402 (3.4)Steel 167 (15.2) 12 (1.1) 179 (8.1)Non-ferrous metal 106 (4.2) 2 (1.0) 108 (4.0)General machinery 384 (4.5) 28 (1.2) 412 (3.8)Electric machinery 800 (5.7) 57 (1.3) 857 (4.6)Transport equipment 405 (5.6) 10 (1.4) 415 (5.3)Precision machinery 135 (5.0) 29 (1.4) 164 (3.4)Petroleum products 18 (2.6) 1 (1.0) 19 (2.4)Other manufacturing 386 (3.6) 90 (1.1) 476 (2.6)

Trade/Sales a/ 2,051 (7.2) 75 (1.3) 2,126 (6.2)Service 139 (2.8) 1Q (1.3) 149 (2.6)Others 197 (3.1) 36 (1.4) 233 (2.6)

TOTAL 5,825 (5.1) 428 (1.3) 6,253 (4.2)

( ) - average number of subsidiaries per parent company.a/ Includes general trading companies.

Source: Annual Survey on Overseas Investment, MITI, 1987.

- 28 -

4.09 Large Japanese manufacturing companies have expanded DFI in tradeand other comercial activities traditionally considered the areas ofexpertis of general trading companies. About 30% of Japanese largemanufacturing companies' subsidiaries were in trade and sales in 1985(Table IV.4). In developed countries, only about half of their subsidia-ries were in manufacturing, with the other half focused on sales activi-ties. However, in developing regions such as Latin America and Asia, largemanufacturing companies concentrated on production. In Asia, over 80% ofJapanese foreign manufacturers' subsidiaries were in manufacturing, and thepercentage was 68% in Latin America. This would seem to indicate thattrading companies still have a major role in Japanese DFI startup andcoiercial functions in developing countries.

Table IV.4: SHARE OF SALES SUBSIDIARIES AMONG TOTAL SUBSIDIARIESOF JAPANESE MANUFACTURING COMPANIES, FY1985

Sales Subsidiaries a/ (7) (Manufacturing Subsidiaries)

North America 48.2 40.3Europe 57.4 37 8OCEANIA 51.2 34.4Latin America 15.0 68.2Asia 16.0 80.5Middle East 13.8 51.7Africa 0.0 61.0World 32.6 59.2

Number of sales subsidiaries of manufacturing holding companiesa! - x 100

Number of subsidiaries by manufacturing holding companies

Source: Annual Survey on Foreign Direct Investment, MITI, 1987.

4.10 Japanese DPI formerly was dominated by general trading companiesactive in sales, manufacturing, and coordination of DEI for small andmedium scale firms. The trend in the 1980s seems to be toward an increas-ing share of DFI by large manufacturing enterprises as Japanese DFI becomesmore concentrated in industries characterized by rapid technologicalchange: automobiles, electronics and machinery (Chapter III). Evidence ofthe increasing importance of large companies can be seen in their averageinvestment size, growing from approximately US$2 million in the 1970s toalmost US$8 million in 1987 (Chart II.1). Several points, however, shouldbe noted with regard to this trend. The change is more substantial indeveloped countries, and DFI in developing countries still has characteris-tics associated with smaller scale firms and activities of trading compa-nies. The yen appreciation of 1985 and Japan's structural adjustmenteffort also have been factors in the recent upturn of DFI by small andmedium firms.

- 29 -

S. Objectives of Japanese DFI

4.11 The main objective of Japanese firms in DFI is expanding salesto local and third country markets (Table IV.5). A survey of Japaneseinvestors indicated other significant motivations: access to market andtechnology intelligence (16.4%), inexpensive labor and reduction of cost(12.02), and favorable host country policies to promote and protect DFI(10.02). Other reasons included; procurement of raw materials, collectionof royalty payments, abundant local resources, and increase in local pro-duction and reduction of exports to avoid trade friction. It,," notablethat avoidance of trade friction, generally thought to be a major reasonfor Japanese DFI, was cited as one of the least important motivations forJapanese foreign investment (some self-censorship is possible in theresponses).

Table IV.5: JAPANESE DPI OBJECTIVES BY REGION, FY1987(Number of firms and % share by Region)

North LatinAmerica Europe Asia America World

Procurement of raw materials 136 19 145 55 472(6.3) (1.5) (3.7) (7.3) (5.4)

Easy local production due to 70 9 70 50 229abundant national resources (3.2) (0.1) (1.8) (6.6) (2.6)

Utilization of inexpensive labor 33 15 892 86 1,056and reduction of cost (1.5) (1.1) (22.9) (11.4) (12.0)

Host government policies to 38 50 593 132 886promote and protect DFI (1.8) (3.8) (15.2) (17.5) (10.0)

Expansion of sales to local and 1,187 841 1,604 299 4,218third markets (54.8) (64.2) (41.2) (39.7) (48.0)

Gathering information 568 309 373 97 1,441(26.2) (23.6) (9.6) (12.9) (16.4)

Staggering exports due to trade friction 78 25 55 7 167

Royalties 56 41 161 27 321(2.6) (3.1) (4.1) (3.6) (3.7)

TOTAL 2,166 1,309 3,893 573 8,790(100.0) (100.0) (100.0) (100.0) (100.0)

a/ Survey results of the response of Japanese firms* Miltiples objectives are listed foa single investment.

Source: Toyo Kezai Shinposha, Japanese Overseas Investment 1988: A Complete Listing ofFirms.

- 30 -

4.12 In all regions, expanding sles was the most important objective,but other motivations varied among regions. In North America, gatheringinformation (26.2%) was the second most important objective, procuringlocal raw material (6.32) the third, and avoiding trade friction (3.6%) thefourth. In Europe, gathering information (23.6%) also ranked second,followed by benefits from government policies toward DFI (3.8%), andgaining royaltios (3.1%). In Asia, tapping inoxpensive labor (22.9%) wasthe second motivation, host government policy (15.2%) third, and gatheringinformation (9.62) the fourth. In Latin America, host government policy(17.52) was the secood ranking objective, followed by gathering information(12.9Z) q0 low labor costs (11.4%).

4.13 Differences in motivations for DFI also vary according to type ofinvestor. A survey on important factors in selecting overseas sites (ChartIV.1) inditead that large firAs are more interested in the overall marketthan are s*all firms (41.2% vs. 28.7%). This may reflect the fact thatsmall and medium firms rely on other firms to fulfill marketing functions,through subcontracting or using sales networks of general trading compa-nies. Small and medium firms regard the local political climate as animportant factor (12.3% of responses), but large firms are less concerned(4.5%). The tax system of the host government is more important for smallfirms than large firms, which implies that small firms are more vulnerableto host government politics and DFI-specific regulations.

CHART IV.1 IMPORTANT FACTORS IN SELECTING OVERSEAS SITES (%)LARGE FIRMS SMALL FIRMS

~~ MAR~~KETS LABOR SITUATIONRKS(1.2%) (1 8.02) MARKErS

LABORSITUAT. TAX SYSTEr M(1 8.9%) OTHERS (17.2%) OTHERS

(14.72) (1 2.3X)

TAX S _ ' POUTICAL SITLIATION (4.52)(12.3%) sccu~~~ MATERLALS SECURtING OUTICAL SITUATION(I 2.3X) SECUING MATtRL(4 MATERIALS (1 2.3%)

(8.4x) (1 1.52)

Source: The Long Term Credit Bank of Japan, 1987 Survey on Japanese OFI.

- 31 -

C. Difficulties Perceived by Japanese Firms in DFI Operations

4.14 The main problems for Japanese investors in developed countriesare associated with market conditions. Those in developing countriesoriginate from government policies and political and economic instabilities(Table IV.6). Problem areas differ by region. In North America, more thanhalf the Japanese investors cited market competition (52.22), shortage ofqualified labor (11.8X), and local employment requirements (10 ), partic-ularly in Canada, as the three main concerns. Inflation (5.OZ.*4 an indica-tor of overall macroeconomic performance, was the fourth most citedproblea.3/ In Europe, increasing market competition was viewed as themain problem (55.1%); inflation (8.5%), labor supply (8.1%), and localemployment requirements (6.7%) also were cited.

4.15 In Asia, market competition (24.22) was the most importantconcern for Japanese DPI. Inflation was the second ranking problem(10.4%), and difficulties in acquiring qualified labor the third (9.5%).Local employment requirements (8.7%) and foreign equity participation(6.5%) ranked fourth and fifth. In Latin America, inflation was cited asthe most important problem (28.8%). Government restrictions on imports ofraw materials and parts (13.6%) and on remitting dividends (8.7%) rankedsecond and third; government regulations have a more adverse impact inLatin America than in Asia. Market competition and political risk rankedfourth as a problem in Latin America (8.0%)

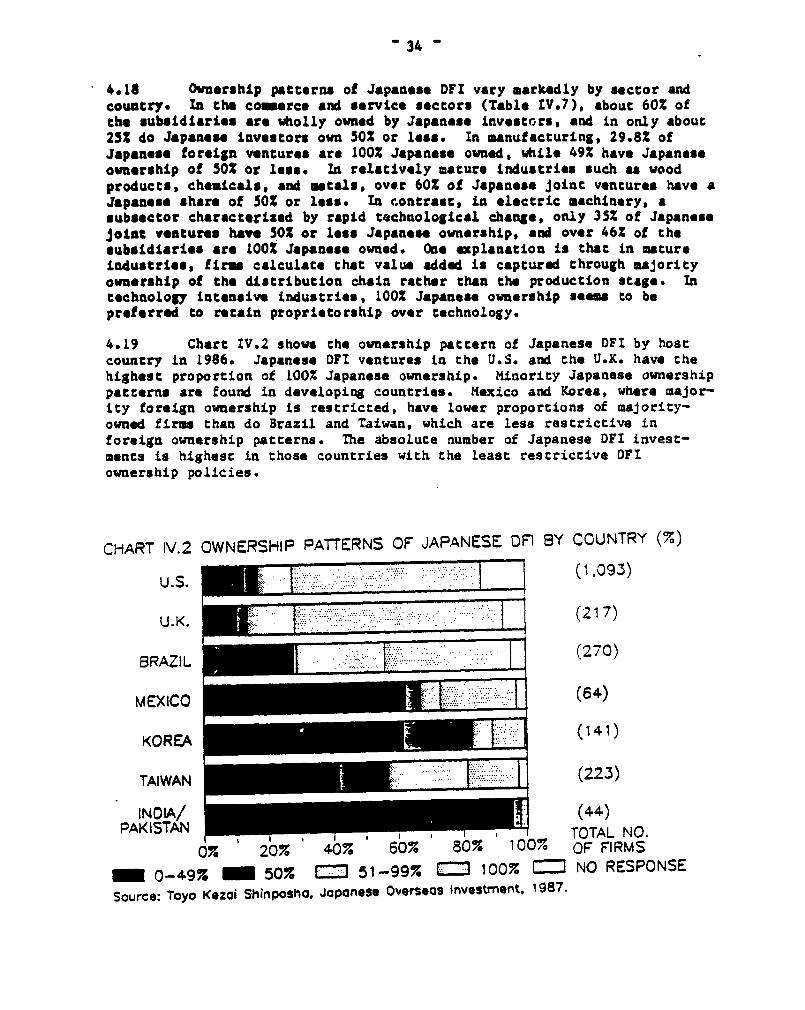

4.16 In Africa, the three most serious problems were governmentregulations restricting imports (14.3%), remitting dividends (13.5%), andlocal employment requirements (12.2%). Inflation (12.0%) and increasingmarket competition (9.8%) were slightly less serious problems. In theMiddle East, local employment requirements (20.2%) was the most importantproblem, followed by scarcity of qualified labor (11.5%). Increasingmarket competition (11.3%), political risk (11.1%) and restrictions onforeign participation (7.8%) were addicional difficulties cited forJapanese DFI operating in the Middle East.

D. Ownership Patterns of Japanese DFI

4.17 Most Japanese investors in foreign subsidiaries do not have 100%ownership. Joint ventures with local partners are common, with Japanesepartners having minority ownership. In 1985, only about 30% of Japanesemanufacturing subsidiaries were wholly owned by the Japanese investors; inabout half of the manufacturing subsidiaries, Japanese equity was 50% orless (Table IV.7). This is a distinctive feature of Japanese DFI;multinational corporations in ocher countries prefer majority ownership toensure control. The greater willingness of Japanese firms to acceptminority ownership reflects the importance of small and medium scale firmsin Japanese DFI. Small firms often lack the funds, market foothold andexpertise necessary in the local market. Thus, joint ventures and minorityshares in Japanese DFI are important for dealing with developing countries,many of which have legislation and practices that preclude or discouragemajority foreign ownership.

3/ Ignoring "other problems" in Table IV.6 which represents the sum of

various miscellaneous problems.

Table [V.6; PROBLE4S IN DFI OPERATION BY ROGION(Survey Result of Japanese Subsidiaries)

North Latin fiddle Z abrldProblems America Europe Oceania Asia America Africa Eat Total

Host Government Regulation on:

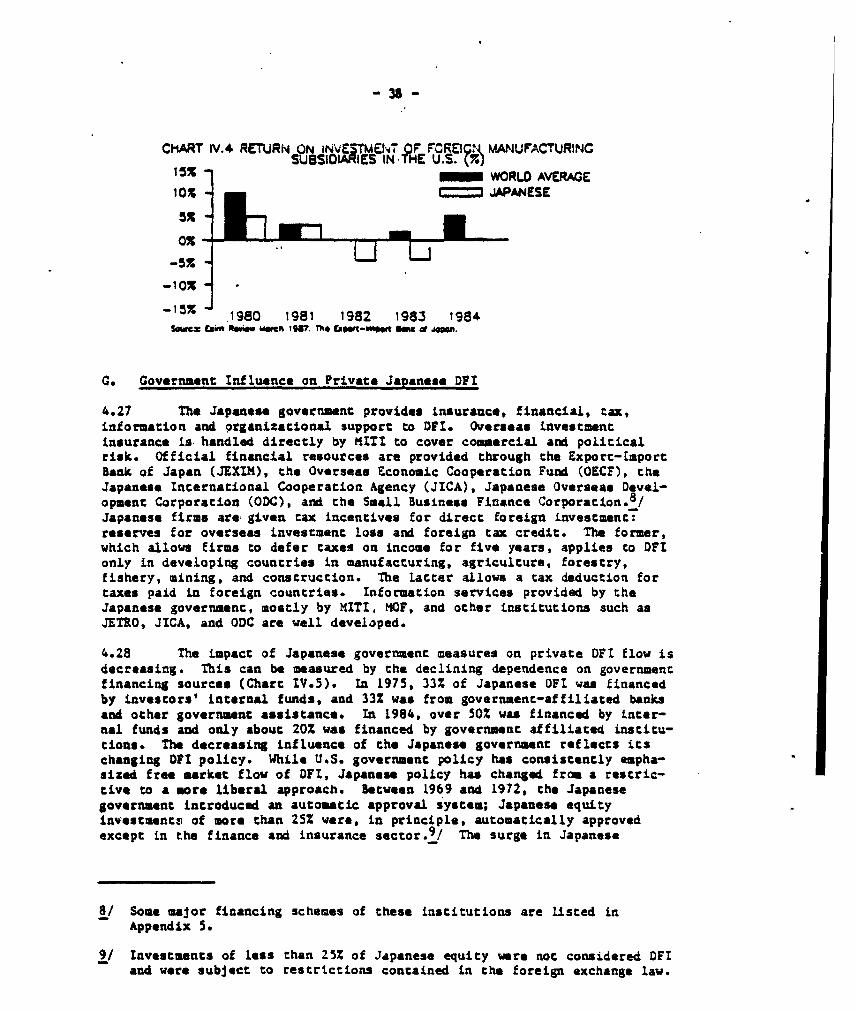

1. Remittance of dividends 1.2 0.7 1.0 2.7 8.7 13.5 5.4 3.02. Local financing 0.6 0.6 2.2 3.8 1.7 2.2 0.9 2.33. Restrictions on foreigners'equity participation 0.7 0.1 2.6 6.5 2.9 4.7: 7.8 3.84. Local employment requirements 10.3 6.7 6.7 8.7 6.7 12.2 20.2 8.75. Domestic content requirements 0.4 0.9 2.6 2.9 3.1 0.4 6.7 2.1b. Restriction on Imports(of Inputs) 1.3 2.4 1.5 4.6 13.6 14.3 4.1 4.87. Export requirements 0.3 0.4 0.9 2.9 1.5 2.2 0.9 1.78. Licensing agreements 0.1 0.2 0.0 0.8 1.8 0.2 0.0 0.69. Others 0.6 0.4 3.0 0.9 1.0 2.2 0.4 0.9Subtotal 1-9 (15.5) (12.4) (20.5) (33.8) (41.0) (51.9) (46.4) (27.9)

10. Political risk 0.1 1.2 0.8 7.1 8.0 7.8 11.1 4.711. Inflation ,.0 8.5 8.8 10.4 28.8 12.0 2.4 11.212. Immature distribution system 1.0 1.8 2.0 2.3 0.9 2.7 1.7 1.813. Increasing market competition 52.2 55.1 39.7 24.2 8.0 9.8 11.3 32.414. Lack of infrastructure 0.4 0.4 3.1 1.5 2.1 3.3 3.5 1.415. Subcontracting difficulties 2.2 0.9 2.7 4.1 1.7 0.8 3.0 2.816. Labor dispute 1.1 1.5 4.4 0.4 0.5 0.2 0.0 0.917. Labor supply(quality and quantity) 11.8 8.1 7.3 9.5 4.3 7.6 11.5 9.018. Conflict with partners 2.4 1.9 5.8 4.1 2.0 3.5 5.4 3.319. Residents' provoke 0.3 0.2 0.7 0.1 0.1 0.0 0.0 0.220. Other problems 8.0 8.0 4.4 2.5 2.6 0.4 3.5 4.5TOTAL 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

Source: Second Basic Survey on Overseas Investmuent, ITI, 1986.

(D-264a)

Table IV.7: (UEW &IP PAT 1 AIG JAPAWSE D[ AFFEJLA , FY1985(Umber of Affiliates by % C3pital by Indistry)

Belw 50% 50% Fram 51-99 l(lit Total

Nter Share tNwer Share Nler Share Total Share NI&dr Shie

1,469 29.6% 312 6.3X 810 16.3Z 2,371 47.U 4,962 100.(1

Manufacturigx 868 41.2X 165 7.8% 444 21.12 628 29.8% 2,105 10041Food products 36 36.4% 9 9.1% 23 23.2% 31 31.3X 99 10DA0Textiles 81 47.4% 7 4.1% 50 29.2% 33 19.3% 171 100.(1Wod products 29 52.7% 4 7.3X 11 20.0% 11 20D( 55 10D.CK(liancals 137 48.1% 36 12.6% 48 16.&% 64 22.5X 2h5 I0O.(Metals iO5 66.5% 6 3.8% 36 22.8% 11 7 AR 158 1004Non-electric machinery 55 32.7% 16 9.5% 41 24.4% 56 33.3 168 100.CtElectric machinery 147 28.7% 32 6.2X 97 18.9% 237 46.22 513 10D.02Transport equipsnt 139 54.9% 13 5.1% 47 18.6% 54 21.3X 253 1004.Other anrufacturig 139 34.5% 42 10.4% 91 22.6X 131 32.5% 403 100.41

Resource Develo3!Ent 82 48.% 7 4.2% 22 13.1X 57 33.92 168 100.01Agriculture/Forestry/Fisheries 43 58.9% 4 5.5% 13 17.8% 13 17.8 73 100.41Minirg 39 41.1% 3 3.2X 9 9.5% 44 46.3X 95 100AK.

cuerce & Services 519 19.37 140 5.2% 344 12.8% 1,686 62.72 2,611 100.41Coinstruction 65 40.6% 12 7.5% 31 19.4% 52 32.5X 160 IOD.G1Trade/Sales 286 15.3 77 4.1% 253 13.5% 1,259 67.1% 1,8I5 100.4Services 72 29.1% 14 5.7% 23 9.3% 138 55.92 247 100.4Other wrnufacturing 96 23.6% 37 9.1% 37 9.1% 237 58.2Z% 407 100.41

Source: Aral Survey ao Overseas Investnamt, MITI, 1987.

(D-264a)

34

4.18 Ownership patterns of Japanese DFI vary markedly by setor andcountry. In the coerceo and service sectors (Table IV.7), about 60% ofthe subsidiaries are wholly owned by Japanese investors, and in only about251 do Japanese investors own 50 or less. In manufacturing, 29.8% ofJapanese foreign ventures are 100% Japanese owned, while 49% have Japaneseownership of 50Z or lass. In relatively mature industries such as woodproducts, chemicals, and matals, over 60% of Japanese joint ventures have aJapanese share of 50X or less. In contrast, in electric machinery, asubsector characterixed by rapid technological change, only 35% of Japanesejoint ventures have 501 or less Japanese ownership, and over 46% of thesubsidiaries sre 100t Japanese owned. One explanation is that in matureindustries, firm calculate that value added is captured through majorityownership of the distribution chain rather than the production stage. Intechnology intensive industries, 100% Japanese ownership see5m to bepreferred to retain proprietorship over technology.

4.19 Chart IV.2 shows the ownership pattern of Japanese DFI by hostcountry in 1986. Japanese DFI ventures in the U.S. and the U.K. have thehighest proportion of 100% Japanese ownership. Minority Japanese ownershippatterns are found in developing countries. Mexico and Korea, where major-ity foreign ownership is restricted, have lower proportions of majority-owned firms than do Brazil and Taiwan, which are less restrictive inforeign ownership patterns. The absolute number of Japanese DFI invest-ments is highest in those countries with the least restrictive DFIownership policies.

CHART IV.2 OWNERSHIP PATTERNS OF JAPANESE OF] BY COUNTRY (7w)

U.S. _=(t03

U.K. r~. (217)

BRAZIL (270)

MEXICO (64)

KOREA (141)

TAIWAN (223)

INOA/ (44)PAKISTAN T TOTAL NO.

%7 20% 40% 60% 80P 100% OF FIRMS0-497_ 507. 51-99% = 100% = NO RESPONSE

Source: Toyo Kezai Shinposho, Japanese Overseas Investment, 1987.

- 35 -

4.20 As Japanese DFI expands in the trade and service sectors and intechnology intensive manufacturing industries, Japanes investors' insist-ance on majority or sole ownership is expected to increase. As the focusshifts toward finding flexible technical labor pools and gaining footholdsin increaingly protected industrialized markets, developing countryrestrictions on majority ownership will further diminish the appeal ofdeveloping countries as sources and as markets.

E. Market Destination of Japanese Hanufacturing Subsidi-ry

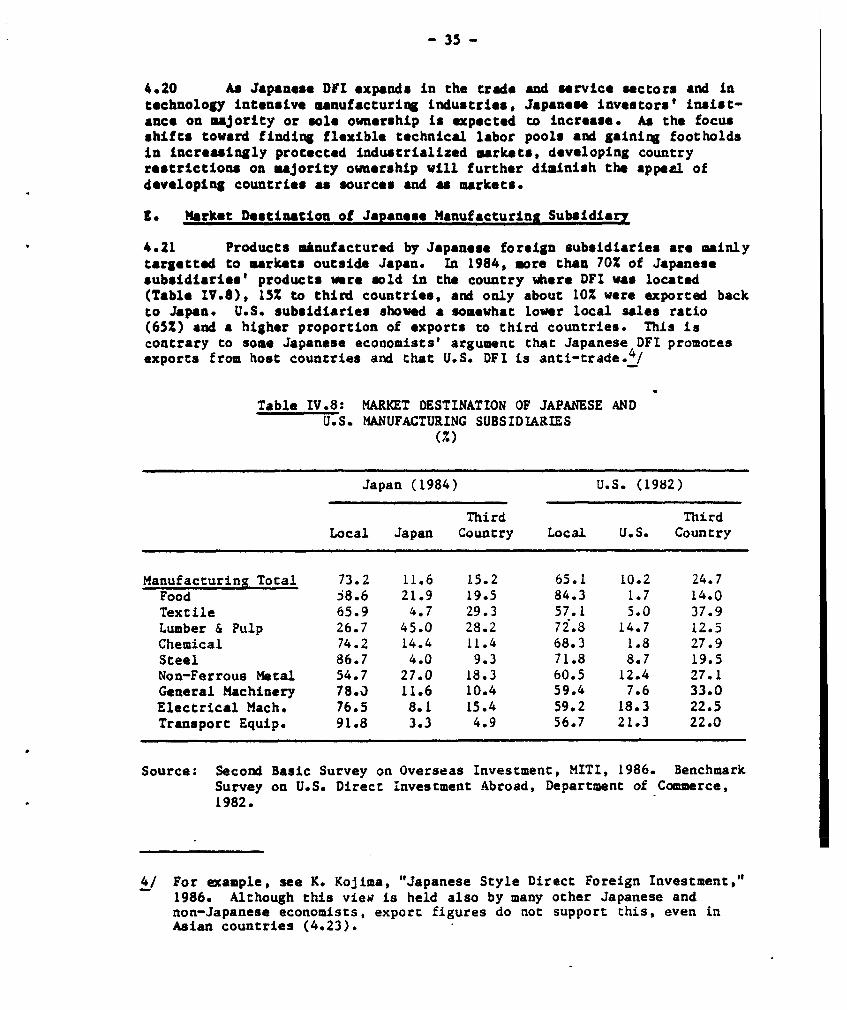

4.21 Products minufactured by Japanese foreign subsidiaries are mainlytargetted to markets outside Japan* In 1984, more than 70% of Japanesesubsidiaries' products were sold in the country where DFI was located(Table IV.8), 15% to third countries, and only about 10% were exported backto Japan. U.S. subsidiaries showed a somewhat lower local sales ratio(65%) and a higher proportion of exports to third countries. This iscontrary to some Japanese economists' argument that Japanese DFI promotesexports from host countries and that U.S. OFI is anti-trade.4/

Table IV.8: MARKET DESTINATION OF JAPANESE ANDU.S. MANUFACTURING SUBSIDIARIES

(%)

Japan (1984) U.S. (1982)

Third ThirdLocal Japan Country Local U.S. Country

Manufacturing Total 73.2 11.6 15.2 65.1 10.2 24.7Food j8.6 21.9 19.5 84.3 1.7 14.0Textile 65.9 4.7 29.3 57.1 5.0 37.9Lumber & Pulp 26.7 45.0 28.2 72.8 14.7 12.5Chemical 74.2 14.4 11.4 68.3 1.8 27.9Steel 86.7 4.0 9.3 71.8 8.7 19.5Non-Ferrous Metal 54.7 27.0 18.3 60.5 12.4 27.1General Machinery 78.0 11.6 10.4 59.4 7.6 33.0Electrical Mach. 76.5 8.1 15.4 59.2 18.3 22.5Transport Equip. 91.8 3.3 4.9 56.7 21.3 22.0

Source: Second Basic Survey on Overseas Investment, MITI, 1986. BenchmarkSurvey on U.S. Direct investment Abroad, Department of Commerce,1982.

4/ For example, see K. Kojima, "Japanese Style Direct Foreign Investment,"1986. Although this vies is held also by many other Japanese andnon-Japanese economists, export figures do not support this, even inAsian countries (4.23).

- 36 -

4.22 Japanese DFI in natural resource related industries sell a lowpercentage of output in the host country: lumber and pulp (26.7% soldlocally), non-ferrous metal (54.7%) and food (58.6Z). Transport equipment(91.8%), steel (86.7%), general machinery (78.0%), electrical machinery(76.5%) all show high local sales percentages. The textile industry isnotable for its high proportion of third country exports (28.3%), withJapanesa DFI utilizing the host countries as export bases. In contrastsU.S. DFI has a higher export ratio in capital and technology-intensivesectors than in natural resource-related subsectors. Most notable is theU.S. transport equipment subsector, which sold 21.3% of its products backto the U.S. and 22.02 to third countries; and electrical machinery, whichsold 18.3% to the U.S. and 22.5% to third countries. U.S. subsidiaries(particularly in automobile and electrical machinery) tend to use foreignproduction facilities as a component of the parent companies' globalproduction system, while Japanese subsidiaries, tend to produce the finalproduct for the local market.