January 2016 - Vingroup Release/2016... · Sources: Economist Intelligence Unit, CBRE reports,...

45

VINGROUP JOINT STOCK COMPANY Corporate Presentation January 2016

Transcript of January 2016 - Vingroup Release/2016... · Sources: Economist Intelligence Unit, CBRE reports,...

VINGROUP JOINT STOCK COMPANY

Corporate Presentation January 2016

CORPORATE PRESENTATION2

Contents

A. Vietnam Macroeconomic Updates 3 - 7

B. Introduction to Vingroup 8 - 13

C. Business Strategy 14 - 16

D. Key Investment Highlights 17 - 27

E. Financial Overview - VAS 28 - 34

F. Financial Overview - IFRS 35 - 41

G. Trading Performance 42 - 43

CORPORATE PRESENTATION3

A. Vietnam Macroeconomic Updates

CORPORATE PRESENTATION4

Improving Macroeconomic Conditions Supporting Growth

Sources: Economist Intelligence Unit, CBRE reports, General Statistics Office of Vietnam, State Bank of Vietnam, IMF, Bloomberg

Inflation and interest rates have eased considerably

6.2%

5.2% 5.4%6.0%

6.7%

2011 2012 2013 2014 2015

Real GDP growth remains strong

(US$ bn)

Disbursed FDI stays robust

11.0 10.5 11.5

12.4

14.5

2011 2012 2013 2014 2015

Driven by power & fuel price surges, devaluation of the currency in February and a

minimum wage hike in October

Exchange rate: VND remains resilient

20,649 20,859 21,017 21,189 22,495

2011 2012 2013 2014 2015

Currency has remained stable for

the past 5 years

(VND)

18.7%

9.1%6.6%

4.1% 0.6%

17.0%

13.5%

10.4%8.7% 8.4%

2011 2012 2013 2014 2015

Inflation Lending Interest Rate

Average devaluation: 2.1% p.a

CORPORATE PRESENTATION5

0

20

40

60

80

100

19

60

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

14

8.2%

4.1%4.9% 5.2%

6.1%

2010 2011 2012 2013 2014

Favorable Long-term Outlook for Consumption and Real Estate

Region’s lowest retail space(3)

Catching up with Regional Peers in Urbanization(2)

Rising income levels(4)

(GDP per capita, US$)Modern retail space in SEA cities (thousand sqm), 2014

Singapore–100%

Malaysia–74%

Philippines–49%

Vietnam–32%

(%)

Sources:

(1) General Statistics Office of Vietnam

(2) World Bank, Urbanization Data, 2014

(3) CBRE

(4) Economist Intelligence Unit

Private consumption growth(1)

India–32%

Indonesia–52%China–53%

Thailand–35%

0

2,000

4,000

6,000

8,000

Ba

ng

kok

Sin

ga

pore

Ma

nila

Ku

ala

Lu

mpu

r

Jakarta

Han

oi

Ho C

hi M

inh

City

Ph

no

m P

en

h

Ya

ng

oo

n

1,2771,507

1,7221,866

2,010 2,050 2,120 2,2502,430

2010A 2011A 2012A 2013A 2014A 2015E 2016E 2017E 2018E

CORPORATE PRESENTATION6

89.3100.4

111.6122.3

129.8143.3

160.1

2011 2012 2013 2014 2015E 2016E 2017E

5.05.6

6.57.3

8.09.0

10.3

2011 2012 2013 2014 2015E 2016E 2017E

8.59.6

10.511.4 11.9

13.014.3

2011 2012 2013 2014 2015E 2016E 2017E

8.910.0

11.312.6

13.615.1

17.1

2011 2012 2013 2014 2015E 2016E 2017E

Source: Economist Intelligence Unit as of 18 February 2016.

(1) Total Consumer Spending includes Consumer Expenditure on Housing, Tourism and Healthcare, amongst other sub-categories

(US$ bn) (US$ bn)

Consumer Expenditure on Housing Consumer Expenditure on Tourism

(US$ bn) (US$ bn)

Consumer Expenditure on Hospital Total Consumer Spending(1)

Integrated Platform Focused on the Vietnamese Urban Consumer

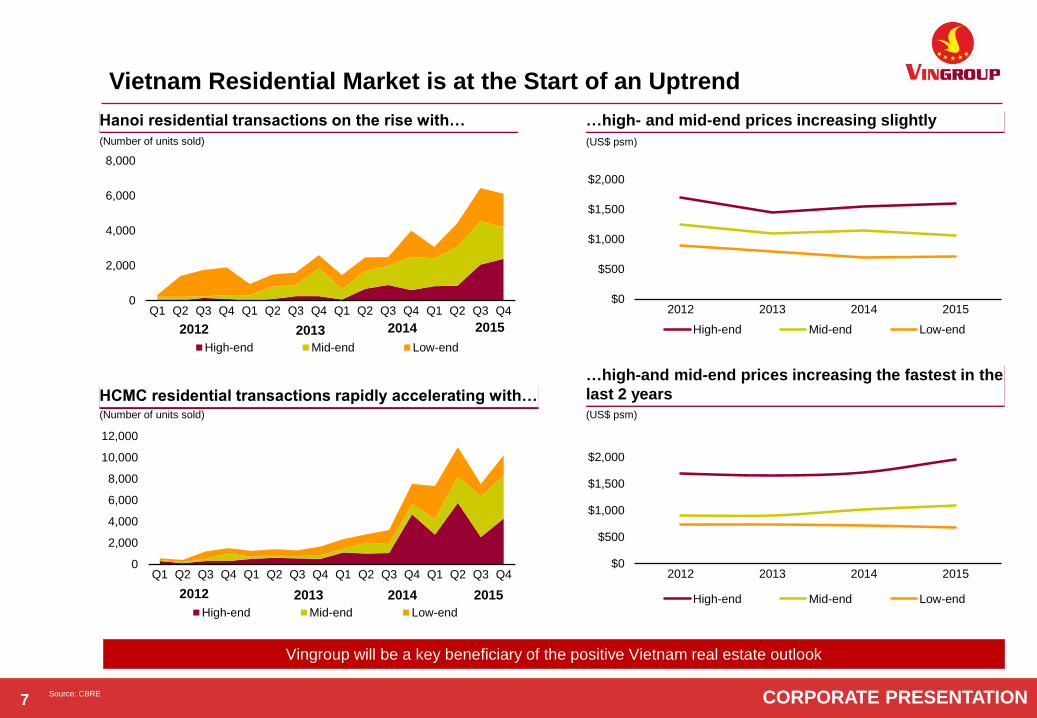

CORPORATE PRESENTATION7Source: CBRE

Vingroup will be a key beneficiary of the positive Vietnam real estate outlook

0

2,000

4,000

6,000

8,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

High-end Mid-end Low-end

20152012 2013 2014

0

2,000

4,000

6,000

8,000

10,000

12,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

High-end Mid-end Low-end

20152012 2013 2014

Vietnam Residential Market is at the Start of an Uptrend

(US$ psm)(Number of units sold)

Hanoi residential transactions on the rise with… …high- and mid-end prices increasing slightly

$0

$500

$1,000

$1,500

$2,000

2012 2013 2014 2015

High-end Mid-end Low-end

$0

$500

$1,000

$1,500

$2,000

2012 2013 2014 2015

High-end Mid-end Low-end

(Number of units sold) (US$ psm)

HCMC residential transactions rapidly accelerating with…

…high-and mid-end prices increasing the fastest in the

last 2 years

CORPORATE PRESENTATION8

B. Introduction to Vingroup

CORPORATE PRESENTATION9

Evolution of Vingroup

Note:

Financials for years 2008 – 2014 are presented based on IFRS and financials for earlier years and 2015 are presented based on VAS

Revenue (US$ mn) = Revenue (bn VND)/ Exchange rate VND/USD as of 31 December each year

9 34 1111

92 180109

305

863

1,293

1,499

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Total Assets ($ mm)

Vinpearl Land Nha Trang

Listed on HOSE

(largest real estate co.)

$100 mm convertible bond

Vincom – Vinpearl merger

$300 mm convertible bond

Vinmec Times City International

Hospital (Hanoi) opened

$472 mm sale of Vincom Center A HCMC mall

$150 mm international credit facility

$200 mm international bond

$200 mm Warburg Pincus investment in Vincom Retail

Vincom Mega Mall Royal City & Vincom Mega Mall Times City

Vinschool Royal City, Times City opened

Vincom Center

Ba Trieu

Vinpearl Resort

Nha Trang

Vincom JSC

Vinpearl JSC

1993 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Revenues ($ mm)

$70 mm equity placement

Vinpearl Phu Quoc

Vincom Plaza Ha Long

Vinhomes Central Park construction

started

$100 mm Warburg Pincus

follow-on investment in

Vincom Retail

10 new Vincom shopping

malls:

- Vincom Center Nguyen Chi

Thanh (HN)

- Vincom Mega Mall Thao

Dien (HCMC)

- 8 Vincom Plazas in Thu Duc,

Da Nang, Can Tho, Dong

Nai, Quang Trung (HCMC),

Hai Phong, etc

3 new Vinpearl resorts:

- Nha Trang Bay Resort &

Villas

- Ha Long Bay Resort

- Phu Quoc Resort & Golf

2 new Vinmec Int’l hospitals

in:

- Central Park (HCMC)

- Phu Quoc

“Start-up spirit”

Technocom

Vincom Plaza Long Bien

3 new Vinpearl resorts:

- Vinpearl Luxury Nha Trang

- Vinpearl Golf Club – Nha Trang

- Vinpearl Da Nang Resort & Villas

CORPORATE PRESENTATION10

Largest Listed Real Estate Company with Diversified Consumer

Sector Exposure

Villas and Apartments (Vinhomes) Resorts (Vinpearl) and Amusement Parks (Vinpearlland)

Re

sid

en

tial Golf Courses, Gyms and Spas

Healthcare (Vinmec)

Agriculture (VinEco)Education (Vinschool)

Shopping Malls (Vincom Center, Vincom Mega Mall

and Vincom Plaza)

Supermarkets (VinMart), Electronic Retailing (VinPro), Specialities stores

(VinDS) and E-commerce (Adayroi)

Ho

sp

itality

Re

tail

,Co

mm

erc

e

Oth

ers

“To create a better life for the Vietnamese people”

CORPORATE PRESENTATION11

Significant Focus on Recurring Revenue Streams

45 58 84 97 109 45 56 75 99 125

19

186

7 16

60

147

90 121 174

276

567

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Retail rental Hospitality & Entertainment Consumer retail Education, Heathcare & Others

…with profitability resilient through economic cycles(1)

(1) Source: Audited IFRS Consolidated Financial Statement for 2011, 2012, 2013, 2014 and

Unaudited VAS 2015

(2) Consolidation for 2010 and 2011 sourced from management accounts. Prepared for

comparability purposes

(US$ mm)

Recurring revenue streams continue to grow(1)…

(3) Includes negative gross profit from non-recurring revenue of (US$4.4mm) in 2012 and

(US$2.7mm) in 2013

(4) On 26 October 2015, Vingroup announced an acquisition of Maximark, a popular retail brand

with a large portfolio of malls and supermarkets concentrated in South Vietnam

Portfolio of commercial real estate continues to ramp up with…(4)

35 46 62 69 59

14 19

34 41

21

23

16 32

49 65

96

126 135

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Retail rental Hospitality & Entertainment Consumer retail Education, Healthcare & Others(2)

(US$ mm)(% of total)

Strategic shift towards a greater percentage of revenues coming from recurring income streams such as retail, hospitality, healthcare, and schools enhances the resilience of the business model.

(2)

(3)

(3)

19%

22%

33%

26%

(% of total)

44%

16%

17%

24%

…17 Vincom shopping malls, 8 Vinpearl resorts & 2 Vinpearl Land

amusement parks…3 Vinmec hospitals and 5 Vinschools

CORPORATE PRESENTATION12

Strong Residential Sales: New Projects(1)

(1) As of 31 December 2015

(2) Pre-Sale launched

Prime location along the western bank of the Saigon River,

falling within the western border of the city center area, just

4km from the city’s business center in District 1

Total site area: 422,000 sqm

6,702 apartment units sold in 2015

82% of all residential units sold to date

Total contract value: US$1,367 mm, received US$1,011 mm

First delivery: Q4 2016

Vin

ho

mes

Cen

tral P

ark

Nov-14(2)

Mixed-use project in Tu Liem, Hanoi. Located in one of the

most prime locations of My Dinh - Hanoi's modern commercial

and administrative center, and well connected with

transportation infrastructure

Total site area: 176,300 sqm

Sales launched: Jan 2016

Total Units: Over 360 villas, shophouses & 2,000 apartments

First delivery: TBD

Vin

ho

mes G

ard

en

ia

Jan-162)

1,433 1,433

4,099

7,319

9,295

939 1,160

2,552

6,543 7,641

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Cumulative units launched Cumulative units sold

Villas & Shophouses in Nha Trang, Phu Quoc, Ho Chi Minh

City, Ha Tinh & Hai Phong

1,082 units sold in 2015

60% of all units sold to date

Total contract value: US$986 mm, received US$709 mm

First delivery: Q3 2015 264

1,016

1,795

138

702

1,082

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Cumulative units launched Cumulative units sold

Located just 4 km from Hanoi City center, adopting the eco-

friendly architectural design of the island country of

Singapore

Total site area: 140,643 sqm

3,925 units sold in 2015

78% of all residential units sold to date

Total contract value: US$587 mm, received US$492 mm

First delivery: Q4 2016

594

2,446

3,867

5,019

268

1,455

2,987

3,925

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

Cumulative units launched Cumulative units sold

Vin

ho

mes

Tim

es

Cit

y -

Park

Hill

Mar-15(2)

Villa

& S

ho

ph

ou

se

Pro

jects

Apr-15(2)

PRE-SALE LAUNCHED IN JANUARY 2016…

…TO BE UPDATED

CORPORATE PRESENTATION13

Overview of Land Acquisition and Sale Process

Understanding the development and presales process is a crucial part in appreciating Vingroup’s de-risked business model for residential projects

DeliveryPresalesLand Acquisition

1. Obtaining approval-in-principle

Acquire an “approval-in-principle”

from the local people’s committee

Indicates the approval of a

specific project

2. Investment Registration

Certificate

Can be obtained once “approval-

in-principle” received

After the investment certificate

obtained, a developer may

proceed to:

o Get approval on the land

clearance plan

o Commence the land

clearance process

o Start construction of the project

Delivery of property

upon completion

Buyer has to pay the remaining

~30% of contract value

upon delivery depending on

SPA

Revenue can be recognized by

the Group for sale of property

Property is delivered to buyer

and removed

from inventory

Obtain and deliver the land use

right certificate to buyers

First Stage of Presale –

Signing of SPA

When foundation work or

first floor area is complete

A deposit of c.5,000 USD is

required to be placed whilst

the SPA is being prepared

The first SPA payment is

about 25-30% of the

purchase price

Stage 1 – Sale & Purchase

Contract(1)

Stage 2 – Apportioned

Pre-sales Before

Completion

Second Stage -Installments

Subsequent installment

payments made – depending

on SPA terms

Installment payments of 5-

30% are made in varying

stages depending on SPA

(1) Vietnamese law requires the completion of either the foundation of a building or its 1st floor area before a sale and purchase agreement can be entered into. Sales prior to this completion

may some times be made in the form of a loan agreement, which gets converted into an SPA once conditions to signing SPAs are fulfilled.

CORPORATE PRESENTATION14

C. Business Strategy

CORPORATE PRESENTATION15

What Differentiates Vingroup?

VINGROUP’S DIFFERENTIATION

CREATES COMPETITIVE ADVANTAGES

Strong brand equity and

network of shopping malls,

resorts, amusement parks

and retail centers throughout

Vietnam that attracts

premium tenants, buyers &

clients

Premium pricing for new

projects focused on upper

and middle class Vietnamese

consumers

A pioneering established

corporation that leads the

development of real estate,

retail and services sectors.

Maintain large market share

especially with the upper and

mass affluent segments

Expands into new retail

business segments to lead

consumer trends in Vietnam

Expansion into

complementary businesses

to enhance the Group's

recurring revenue and

profitability

Leveraging nation-wide

network and brand equity to

achieve leadership position

in all business segments in

the near term

Realise synergies among

consumers of focused

segments

Higher percentage of

recurring revenues over time

driven by a growing

operational portfolio

Asset sales allow efficient

capital recycling into new

investments and generation

of RoE

Leading Privately Sponsored

Listed Company In Vietnam

with Premium Brand Names in

Commercial, Residential,

Hospitality, Education and

Retail with Demonstrated

Quality and Prestige

Fully Integrated Real Estate

Owner and Developer of

Large-Scale and Mixed-Used

Properties, with Exposure in

Key Consumer Segments

Established and Demonstrated

Track Record

Leverage Vingroup's Network,

Financial Capacity and

Resources to Develop an

Ecosystem of Complementary

Brands, Products and Services

CORPORATE PRESENTATION16

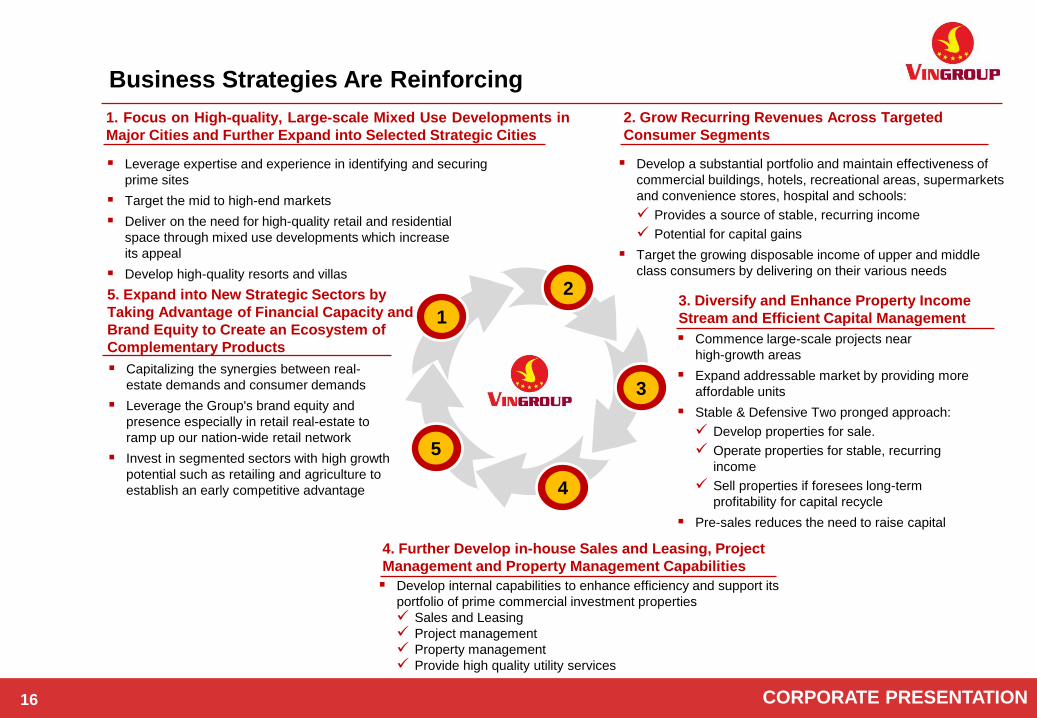

Business Strategies Are Reinforcing

Leverage expertise and experience in identifying and securing

prime sites

Target the mid to high-end markets

Deliver on the need for high-quality retail and residential

space through mixed use developments which increase

its appeal

Develop high-quality resorts and villas

Develop a substantial portfolio and maintain effectiveness of

commercial buildings, hotels, recreational areas, supermarkets

and convenience stores, hospital and schools:

Provides a source of stable, recurring income

Potential for capital gains

Target the growing disposable income of upper and middle

class consumers by delivering on their various needs

Develop internal capabilities to enhance efficiency and support its

portfolio of prime commercial investment properties

Sales and Leasing

Project management

Property management

Provide high quality utility services

Commence large-scale projects near

high-growth areas

Expand addressable market by providing more

affordable units

Stable & Defensive Two pronged approach:

Develop properties for sale.

Operate properties for stable, recurring

income

Sell properties if foresees long-term

profitability for capital recycle

Pre-sales reduces the need to raise capital

1. Focus on High-quality, Large-scale Mixed Use Developments in

Major Cities and Further Expand into Selected Strategic Cities

2. Grow Recurring Revenues Across Targeted

Consumer Segments

4. Further Develop in-house Sales and Leasing, Project

Management and Property Management Capabilities

3. Diversify and Enhance Property Income

Stream and Efficient Capital Management

5

2

3

4

1

5. Expand into New Strategic Sectors by

Taking Advantage of Financial Capacity and

Brand Equity to Create an Ecosystem of

Complementary Products

Capitalizing the synergies between real-

estate demands and consumer demands

Leverage the Group's brand equity and

presence especially in retail real-estate to

ramp up our nation-wide retail network

Invest in segmented sectors with high growth

potential such as retailing and agriculture to

establish an early competitive advantage

CORPORATE PRESENTATION17

D. Key Investment Highlights

CORPORATE PRESENTATION18

1 Vietnam’s Largest Listed Real Estate Developer

2Capital Efficient Real Estate Platform with Track Record of Successful Asset

Disposals

3 One of the Largest Landbank in Prime Locations Across Vietnam

7 Proven Track Record of Access to Capital Markets

8 Highly Experienced Management and Good Corporate Governance

6 Well-recognized Premium Brand Names in Vietnam

Investment Highlights

4 Ecosystem of Complementary Products and Services

5 Nation-wide Retail Network

CORPORATE PRESENTATION19

Largest Vietnamese Developer Offering ‘Pure-play’ Exposure

(1) Market data as of 31 January 2016

(2) As of 31 December 2015, Vingroup has 61 projects in Vietnam, of which, controlling interest in

60 projects, except Vinhomes La Seine

Vingroup (rated B+ by Fitch and B by S&P) is the largest listed real estate company in Vietnam by market capitalization with

controlling interest in over 40 developments, which are in prime urban and high growth areas in key cities throughout Vietnam

Proven ability to secure prime sites in the Central Business Districts

of Hanoi and Ho Chi Minh City

Quality properties that operate under the Vingroup brand names

Growing portfolio of investment properties: A critical contributor of

recurring revenues

Track record of successful project development, sales and

property management

Repeated successful launches of residential and commercial

projects

1

61 Projects(2) across VietnamThe Largest Listed Real-estate(1) Company in Vietnam

A Clear Leader in Vietnamese Real Estate

(US$ mm)

One of the largest-

listed companies in

Vietnam

High-quality

commercial,

residential,

hospitality and

mixed-used

properties

Mass market

residential builder

Furniture and

granite business

Diversifying into

agriculture, mining

& hydropower

Primarily

industrial parks

developer

Infrastructure

development

Telecom &

network

development

Developer of

industrial and

business parks

and high-end

hotels

Also invests in

energy, mining

and education

3,945

287 249 166

Vingroup #2 #3 #4

34 projects at prime central

locations in key cities27 projects at key

tourist destinations

Hanoi Vincom Center Ba Trieu Vincom Plaza Long Bien Vinmec Times City Int’l Hospital Royal City Times City (phase 1) Vinhomes Riverside

Vinhomes Times City – Park Hill

Vinhomes Nguyen Chi Thanh

Vinhomes Smart City

Vinhomes Riverside 2

Green City – Dan Phuong

Vinhomes Gardenia

Vincom Center Pham Ngoc Thach

Ho Chi Minh City Vincom Center Dong Khoi 307 – 309 Vo Van Ngan Vincom Plaza Thu Duc Vincom Mega Mall Thao Dien

Vinhomes Central Park

Vinhomes La Seine (Green City Sai

Gon)

North Vietnam (Excluding Hanoi)

Vincom Plaza Ha Long

Vincom Plaza Le Thanh Tong, Hai

Phong

Vincom Plaza Ly Bon, Thai Binh

Vincom Plaza Viet Tri, Phu Tho

Vincom Plaza Ly Thai To, Bac Ninh

Dream City, Hung Yen

Vinmec Medical University,

Hung Yen

South Vietnam (Excluding HCM city) Vincom Plaza Long Xuyen, An Giang Vincom Plaza Hung Vuong, Can Tho

Vincom Plaza Xuan Khanh, Can Tho

Vincom Plaza Rach Gia, Kien Giang

Central Vietnam Vincom Plaza Ngo Quyen, Da Nang Vincom Plaza Hung Vuong, Hue

Vincom Plaza Ha Huy Tap, Ha Tinh

Vincom Plaza Buon Ma Thuot South Vietnam (Excluding Nha Trang, Khanh Hoa) Vinpearl Phu Quoc Resort Vinpearl Land – Phu Quoc Vinpearl Golf Club – Phu Quoc Vinmec Phu Quoc Int’l Hospital Vinpearl Phu Quoc Resort & Golf

Vinpearl Cam Ranh, Khanh Hoa

Vinpearl Bai Dai, Cam Ranh

Vinpearl Da Lat

Vinpearl Quy Nhon, Binh Dinh

Central Vietnam Vinpearl Da Nang Resort & Villas

Lang Van, Da Nang

Da Nang 2, Da Nang

Vinpearl Resort Hoi An

Nha Trang, Khanh Hoa Vinpearl Nha Trang Resort Vinpearl Land Nha Trang Vinpearl Luxury Nha Trang Vinpearl Golf Club – Nha Trang Vinpearl Nha Trang Bay Resort & Villas

Vinpearl Golf Land Resort & Villas

Vinpearl Villas Hon Tre – Nha

Trang

Vinpearl Phu Quy

Vinpearl Hon Mot

Vinmec Nha Trang

North Vietnam

Vinpearl Ha Long Bay Resort

Vinmec Ha Long

Vinmec Hai Phong

Vu Yen Island, Hai Phong

Operating Project

Under construction and pipeline projects

CORPORATE PRESENTATION20

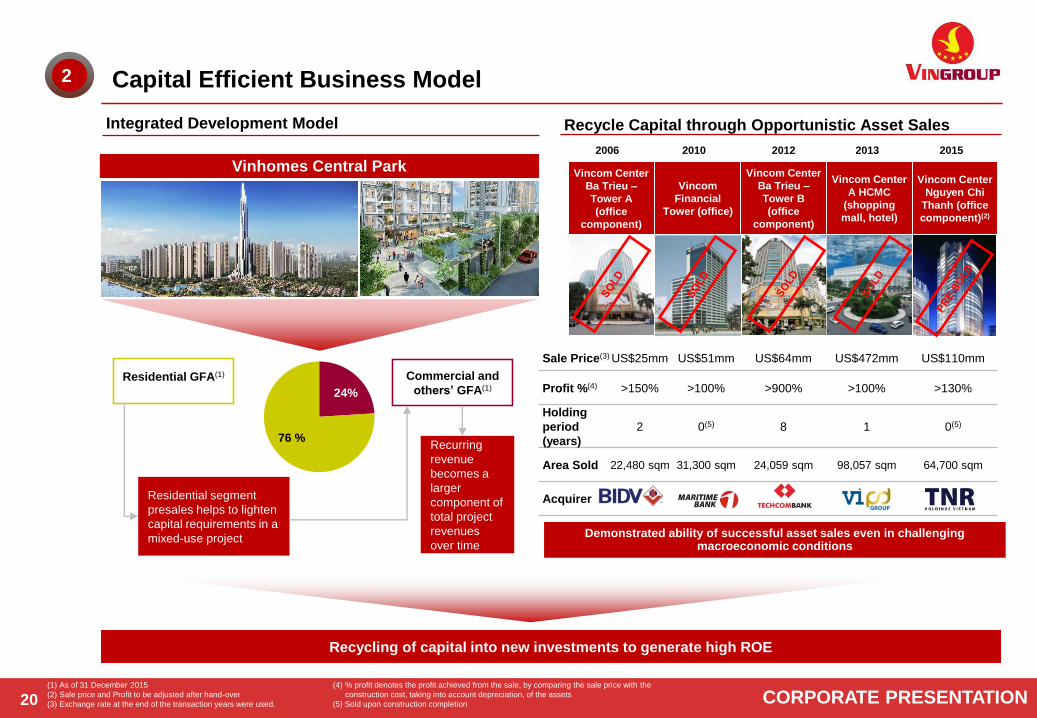

Capital Efficient Business Model

Demonstrated ability of successful asset sales even in challenging macroeconomic conditions

(1) As of 31 December 2015

(2) Sale price and Profit to be adjusted after hand-over

(3) Exchange rate at the end of the transaction years were used.

Recycling of capital into new investments to generate high ROE

2

Sale Price(3) US$25mm US$51mm US$64mm US$472mm US$110mm

Profit %(4) >150% >100% >900% >100% >130%

Holding

period

(years)

2 0(5) 8 1 0(5)

Area Sold 22,480 sqm 31,300 sqm 24,059 sqm 98,057 sqm 64,700 sqm

Acquirer

Integrated Development Model

Vinhomes Central Park

24%

76 %

Residential GFA(1)

Residential segment

presales helps to lighten

capital requirements in a

mixed-use project

Commercial and

others’ GFA(1)

Recurring

revenue

becomes a

larger

component of

total project

revenues

over time

Recycle Capital through Opportunistic Asset Sales

Vincom Center

Ba Trieu –

Tower A

(office

component)

Vincom

Financial

Tower (office)

Vincom Center

Ba Trieu –

Tower B

(office

component)

Vincom Center

A HCMC

(shopping

mall, hotel)

Vincom Center

Nguyen Chi

Thanh (office

component)(2)

2006 2010 2012 2013 2015

(4) % profit denotes the profit achieved from the sale, by comparing the sale price with the

construction cost, taking into account depreciation, of the assets

(5) Sold upon construction completion

CORPORATE PRESENTATION21

Beach Villas26%

High rise 23%

Commercial 7%

Hotel 5%

Hospital 9%

School 3%

Entertainment 1%

Villas, Shophouses

27%

(1) As of 31 December 2015, Landbank and GFA of under-development projects are subject to change

(2) GFA does not include (i) agricultural land, (ii)leased retail areas, or (iii) parking, public areas,

infrastructure and roads in projects

(mm sqm)

Vinhomes and Vincom Retail Projects Vinpearl Projects

(,mm sqm)

Total GFA: 27,846,807 sqm

One of the Largest Landbanks in Prime Locations Across Vietnam(1)

Landbank Breakdown by Construction Status GFA Breakdown(2)

Planned GFA Breakdown by Construction Status(1)(2)

13.2 mm sqm 76.8 mm sqm

17.5mm sqm 10.3 mm sqm 90 mm sqm of landbank is sufficient for at least 10 years of

development

Only look for land at prime locations in major cities

Proactive in infrastructure development to support accessibility of

own projects

Seek to acquire land adjacent to existing mixed-use projects to

benefit from economies of scale and increase the critical mass of

existing projects

2.2 0.9

10.1 4.9

18.8

53.2

Completed Underconstruction

Development Completed Underconstruction

Development

3.1 3.3

11.1

0.6

2.6

7.1

Completed Underconstruction

Development Completed Underconstruction

Development

3

Land Banking Strategy

CORPORATE PRESENTATION22

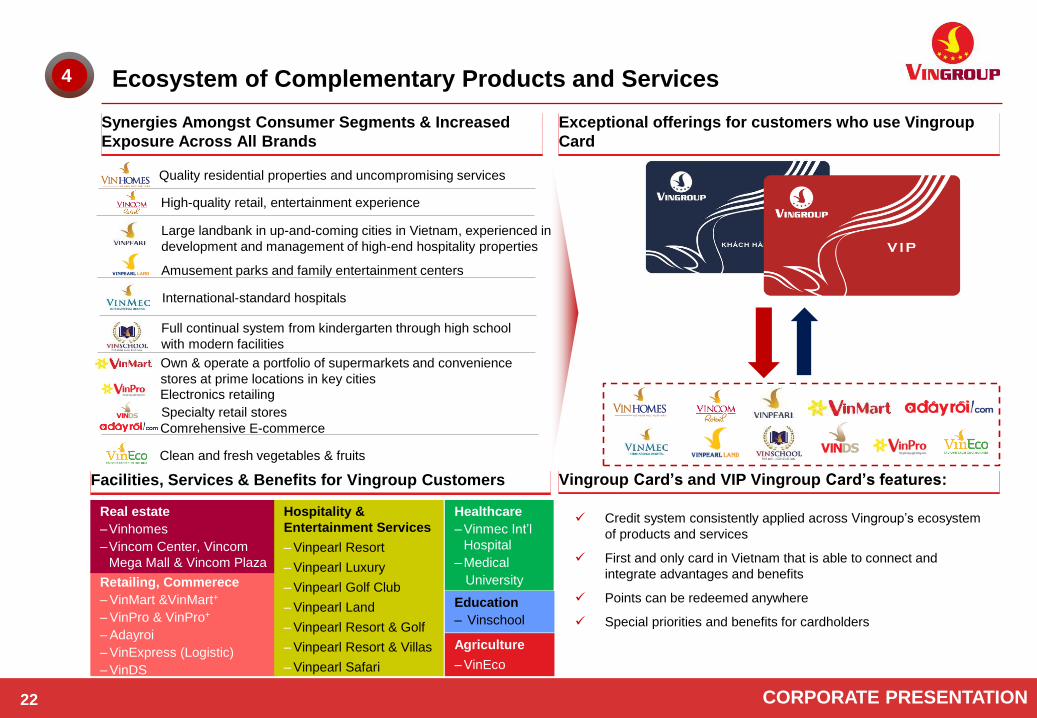

Ecosystem of Complementary Products and Services4

Synergies Amongst Consumer Segments & Increased

Exposure Across All Brands

Exceptional offerings for customers who use Vingroup

Card

Facilities, Services & Benefits for Vingroup Customers

Large landbank in up-and-coming cities in Vietnam, experienced in

development and management of high-end hospitality properties

Amusement parks and family entertainment centers

Retailing, Commerece

– VinMart &VinMart+

– VinPro & VinPro+

– Adayroi

– VinExpress (Logistic)

– VinDS

Healthcare

– Vinmec Int’l

Hospital

– Medical

University

Agriculture

– VinEco

Education

– Vinschool

Real estate

–Vinhomes

–Vincom Center, Vincom

Mega Mall & Vincom Plaza

High-quality retail, entertainment experience

International-standard hospitals

Full continual system from kindergarten through high school

with modern facilities

Quality residential properties and uncompromising services

Own & operate a portfolio of supermarkets and convenience

stores at prime locations in key cities

Electronics retailing

Comrehensive E-commerce

Clean and fresh vegetables & fruits

Specialty retail stores

Credit system consistently applied across Vingroup’s ecosystem

of products and services

First and only card in Vietnam that is able to connect and

integrate advantages and benefits

Points can be redeemed anywhere

Special priorities and benefits for cardholders

Vingroup Card’s and VIP Vingroup Card’s features:

Hospitality &

Entertainment Services

– Vinpearl Resort

– Vinpearl Luxury

– Vinpearl Golf Club

– Vinpearl Land

– Vinpearl Resort & Golf

– Vinpearl Resort & Villas

– Vinpearl Safari

CORPORATE PRESENTATION23(1) Excludes stores in Hanoi

(2) Excludes stores in Ho Chi Minh City

Proven execution capability and capital resources from Vingroup

Leveraging existing supplier relationships and attracting new quality

retailers

Expanding portfolio of shopping malls allows participating brands to

achieve rapid expansion

Relentless focus on quality products and customer service excellence

… Objectives:

Hundreds of retail stores throughout Vietnam in the near term

Seamless online-offline collaboration to deliver quality goods to

customers’ doorstep

5

Key Retail Brands

More Quality Choices for Vietnamese Consumers

Comprehensive E-commerce

Retail network at the end of December 2015

Nation-wide Retail Network

Robust investment in supermarkets, convenience stores, department stores at central locations throughout Vietnam.

Leveraging Vingroup’s financial capacity and relationships with suppliers to build brand equity.

Hanoi

12 VinMart181 VinMart+

4 VinPro5 VinPro+

North Vietnam(1)

6 VinMart3 VinPro

20 VinPro+

Central Vietnam

1 VinMart13 VinMart+

1 VinPro23 VinPro+

South Vietnam(2)

15 VinMart3 VinPro

22 VinPro+

Ho Chi Minh City

12 VinMart114 VinMart+

4 VinPro28 VinPro+

46 VinMart, 308 VinMart+, 15 VinPro, 98 VinPro+ storesVinPro & VinPro+VinMart

& VinMart+VinDS

Vinmart (>3,000 m2

supermarkets) and

Vinmart+ (100–300 m2

convenience stores)

Vinpro (electronics and

appliances)

VinDS (Specialty retail

stores specializing in

cosmetics, shoes,

sportswear, furniture &

household appliances)

CORPORATE PRESENTATION24

Well-recognized Premium Brand Names in Vietnam

(1) In February 2013, Vingroup transferred 100% interest in Vincom Center A Ho Chi Minh City to a real-estate investment company.

As of 31 May 2013, the cash proceeds have been received in full

6

Best Villa Development (Vietnam) for Vinhomes

Riverside

South East Asia Property Awards 2012

Successful in identifying and developing premium

hospitality projects

Hosted large national and international events e.g. Miss

Vietnam World 2008, Miss Universe 2010 and Miss Earth

2010, Miss Vietnam 2014

World-class full-serviced general hospital and clinics at

urban center in Hanoi and Ho Chi Minh city

International standard facility equipped with modern test,

diagnostic and operating facilities Best Retail Developer in Vietnam

Euromoney Real Estate Awards 2012

Euromoney Real Estate Awards 2014

Best Mixed – use Development (Asia) for Vinhomes

Riverside – 2013

Best Retail Development (Vietnam) for Vincom

Mega Mall Royal City - 2014

Asia Pacific Property Awards

Best Developer (Vietnam)

South East Asia Property Awards 2012

South East Asia Property Awards 2014

Educational philosophy behind Vinschool focuses on

the overall development of students from an early

stage in order to develop and shape the future

generations of Vietnam

Best Condominium Development (Vietnam) for

Royal City

South East Asia Property Awards 2013

Leveraging Vingroup’s retail network and experience,

VinEcom aims to focus on first class customer care, and to

create a best-in-class online retail experience in Vietnam

Secured 2 out of the 20 Golden Sites in Vietnam in 2010(1)

Vingroup develops its commercial, retail, residential and

mixed-use properties under the Vincom brand name

Demonstrated ability to sell residential and commercial real

estate even in difficult times in 2010 and 2011

Proven execution skills: Completion of large scale projects

under CBRE’s estimation of construction time

Rapidly expanding supermarket and convenience store

network at central locations in key cities in Vietnam

Wide range of electronics and household appliances

Clean and fresh vegetables and fruits to the mass market

International products and concepts, targeting local consumers

Top 100 ASEAN Companies 2014 by Standard

and Poor’s (S&P)

Region’s Best Borrower 2014 – Vietnam by

FinanceAsia

Vinhomes – the most valuable real estate brand in

Vietnam in 2015

Vincom Retail & Vinpearl – Top 50 most valuable

brands in Vietnam in 2015

Numerous Awards from Independent Media is a

Testimony of the Group’s Brand Name Strong Brands Across Segments

CORPORATE PRESENTATION25

Dong Nai

Retail

GFA(2):

25,785 sqm

Hanoi

Total Retail GFA(2):

481,327 sqm

Well-recognized Premium Brand Names in Vietnam (cont’)6

Vingroup’s brand names are instrumental in securing new sites, achieving premium pricing and attracting global

brand tenants

(1) Tenants for Vincom Center and Vincom Mega Mall in Ho Chi Minh City and Hanoi

(2) GFA as of 31 December 2015

Prime Retail Malls Strategically Located in Key Cities …with a High Quality and Diversified Tenant Base(1)

Ho Chi Minh City

Total Retail GFA(2):

130,622 sqm

Vincom

Mega Mall

Times City

Vincom

Center

Ba Trieu

Vincom

Plaza

Long Bien

Vincom

Mega Mall

Royal City

Ha Long

Retail

GFA(2):

30,777 sqm

Vincom Plaza

Ha Long

Can Tho

Retail

GFA(2):

16,000 sqm

Da Nang

Retail

GFA(2):

34,000 sqm

Hai Phong

Retail

GFA(2):

16,355 sqm

Vincom Plaza

Le Thanh

Tong

Vincom

Center Nguyen

Chi Thanh

Phu Tho

Retail

GFA(2):

22,500 sqm

Vincom Plaza

Viet Tri

Vincom Plaza

Hung Vuong

Vincom

Center

Dong Khoi

Vincom

Plaza

Thu Duc

Vincom

Plaza

Quang Trung

Vincom Plaza

Ngo Quyen

Vincom

Plaza

Bien Hoa

An Giang

Retail

GFA(2):

13,832 sqm

Vincom Plaza

Long Xuyen

Golden sites

Vincom

Mega Mall

Thao Dien

CORPORATE PRESENTATION26

Track Record in Accessing International Capital Markets7

(1) 290.3 mm of US$300 mm CBs were converted into shares by 18 February 2016

More than 1 billion USD raised internationally through 6 pioneering transactions since 2009

Holistic cooperation with local banks, including

facilitation of mortgage financings for customers and

transactional banking services at Vingroup

commercial properties

Good relationship with all leading domestic banks

with repeat loan and bond issuance

Cash & short-term investments sufficient to cover

any near term debt maturities independent of any

new capital raising

Strong cash balance maintained to service working

capital and interest payments

Demonstrated ability to create onshore liquidity

through capital recycling of non-core assets

Strong control over capital expenditures allow flexibility

around liquidity management

Best Capital Markets Deal 2012

Convertible Bonds

Apr & Jul 2012

USD300mm(2)

Best Vietnam Deal 2012

Best Vietnam Deal 2012

Secondary

Placement of

Ordinary Shares

April 2014

USD70mm

International

Syndicated Loan

October 2013

USD150mm

RegS/144A

International Senior

Unsecured Notes

October 2013

USD200mm

Best Vietnam Deal 2013

2013 Real-estate Deal of the Year

Vietnam Capital Markets Deal 2013

Best Vietnam Deal 2013

Best Vietnam Deal 2013

Issuer that matter

May 2013

USD200mm

June 2015

USD100mm

Private Equity

Investment by

February 2016

VND3,000 trln

Domestic Senior

Unsecured Notes,

guaranteed by

CORPORATE PRESENTATION27

Experienced Management Team, Good Corporate Governance and

Strong Sponsor8

Mr. Pham Nhat Vuong

Chairman of the Board of Management

Holds a Bachelors Degree in Geological Economic Engineering, graduated from Moscow Geology University in Russia

Long track record as an entrepreneur both in and out of Vietnam, founded Technocom Limited Company in Ukraine, which was sold to Nestle S.A. in 2010

Established Vinpearl in 2001 and Vincom in 2002

Major shareholder of Vingroup

In 2012, he was recognized as Vietnam’s first billionaire by Forbes Magazine, and continued to maintain this sole position in 2013 and 2014.

Ms. Pham Thuy Hang

Vice Chairwoman

Ms. Vu Tuyet Hang

Vice Chairwoman cum Deputy CEO

Mr. Marc Villiers Townsend(1)

Independent Member

Ms. Pham Thu Huong

Vice Chairwoman

Mr. Le Khac Hiep

Vice Chairman

Mr. Joseph Gagnon(2)

Independent Member

Ms. Nguyen Dieu Linh

Vice Chairwoman cum Deputy CEO

Ms. Mai Huong Noi

Member cum Deputy CEO

Prof. Ling Chung Yee Roy(3)

Independent Member

Board of Management

Ms. Mai Huong Noi

Board member and Deputy CEO

25 years experience

9 years with Vingroup

Mr. Dang Thanh Thuy

Deputy CEO of Vingroup JSC and

General Director of Vinpearl

20 years experience

11 years with Vinpearl

Ms. Tran Thi Khanh Van

Chief Accountant

24 years experience

8 years with Vinpearl

Ms. Nguyen Thi Huyen Tran

Deputy CEO of Vinpearl

18 years with Vingroup

Pro. Nguyen Thanh Liem

CEO Vinmec Times City Int’l

Hospital

39 years experience

2 years with Vinmec

Mr. Nguyen Manh Duc

Chief Accountant

15 years experience

3 years with Vinmec

Ms. Le Thuy Anh

CEO

16 years experience

3 years with Vinmec

Ms. Nguyen Dieu Linh

Vice Chairwoman & Deputy CEO

Over 20 years experience

10 years with Vingroup

Key Executives

Ms. Duong Thi Mai Hoa

CEO

Over 20 years experience

2 years with Vingroup

Ms. Nguyen Thi Diu

Deputy CEO

Over 20 years experience

Joined Vingroup in 2014

Ms. Vu Tuyet Hang

Vice Chairwoman & Deputy CEO

Over 20 years experience

10 years with Vingroup

Mr. Pham Van Khuong

Deputy CEO

Over 28 years experience

12 years with Vingroup

(1) Mr. Marc Villiers Townsend is the Managing Director of CBRE Vietnam

(2) Mr. Joseph Gagnon is a Managing Director of Warburg Pincus

(3) Pro. Ling Chung Yee Roy is the Managing Director of RL Capital Management

CORPORATE PRESENTATION28

E. Financial Overview - VAS

(1) Source: VAS Consolidated Financial Statement for 2015

Based on exchange rate of US$1 = VND 22,540 as of 31 December 2015

CORPORATE PRESENTATION29

(US$ mm)

Debt profile overview

Debt maturity

Average borrowing cost

Source: 2015 VAS Consolidated Financial Statement

As of 19 February 2016, US$290.3mm of CBs have been converted or submitted for

conversion to equity.

11.3% 10.8%9.9% 9.4%

Dec-12 Dec-13 Dec-14 Dec-15

Note: Based on exchange rate of US$1 = VND 22,540 as of 31 December 2015

As of 31 Dec 2015:

• Average debt maturity: 3.6 years

648

342

106

20

26

222

129

1113662

976

491

111

Less than 1 year 1-3 years 3-5 years More than 5 years

Corporate bonds Convertible bond Convertible loan Long-term borrowings Short-term debts

CORPORATE PRESENTATION30

Debt Mix Analysis

Total: VND36,959 Bn (US$1.64Bn)

Diversified Funding Sources(1)

Note:

Based on exchange rate of US$1 = VND 22,540 as of 31 December 2015 (applied to 2015 financials)

(1) Based on VAS Consolidated FS as of 31 December 2015

(2) Including Convertible loan & Loan from Associate

Debt Breakdown(1)

By Currency

By Interest Rate

Domestic bond, 48.6%

International bond, 11.8%

Convertible bond, 6.4%

Bank loans, 30.7%

Others(2), 2.5%

VND, 80.6%

USD, 19.4%

Floating, 78.7%

Fixed, 21.3%

CORPORATE PRESENTATION31

5187

138

177

63

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

84

184282

401

239

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

65252

6921,019 933

44

121

176

278 567

109

373

868

1,297

1,500

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Sales of properties Recurring income

(US$ mm)

(1) Dec-13 includes fair value adjustment realized when the Group sold

Vincom Center A Ho Chi Minh City

(2) Includes profit after tax of discontinued operations

(US$ mm)

(US$ mm) (US$ mm)

Income Statement Highlights

Revenue

EBITDA(1)

Gross Profit

Profit for the Year(1)(2)

Source: Audited VAS Consolidated Financial Statements for 2011, 2012, 2013, 2014 and Unaudited VAS 2015

Note: CAGR from 2011 to 2015

Based on exchange rate of US$1 = VND 22,540 as of 31December 2015 (applied to 2015 financials)

266

548

Adjustment for sale of Vincom Center A HCMC Adjustment for sale of Vincom Center A HCMC

48

180

332

488 508

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

200

338

CORPORATE PRESENTATION32

45

62

102

136145

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

NA

56

75

99

125

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

65

252

692

1,019933

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

109

373

867

1,297

1,500

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

NA

7

14

3134

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

(US$ mm)

Total Revenue

(US$ mm) (US$ mm)

(US$ mm) (US$ mm)

Rental(1) Sale of Properties

Hospitality & Entertainment Services Healthcare

Revenue Performance

Source: Audited VAS Consolidated Financial Statements for 2011, 2012, 2013, 2014 and Unaudited VAS 2015

Note: CAGR from 2011 to 2015

Based on exchange rate of US$1 = VND 22,540 as of 31 December 2015 (applied to 2015 financials)

(1) Include rental from Group’s Subsidiaries

CORPORATE PRESENTATION33

29 41

58 66 71

65% 67%57%

49% 49%

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Gross Margin

(4) (3)

8 9

(63%)

(21%)

25% 28%

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Gross Margin

19 34 39

21

34%

46%

40%

17%

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Gross Margin

19 126 248

377 373

29%

50%

36% 37%40%

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Gross Margin

48

180

332

488508

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

(US$ mm)

Total Gross Profit

(US$ mm) (%) (US$ mm) (%)

Rental(1) Sale of Properties

Hospitality & Entertainment Services Healthcare

Profitability –Gross Profit and Margin

Source: Audited VAS Consolidated Financial Statements for 2011, 2012, 2013 ,2014 and Unaudited VAS 2015

Note: CAGR from 2011 to 2015

Based on exchange rate of US$1 = VND 22,540 as of 31 December 2015 (applied to 2015 financials)

(1) Include rental from Group’s Subsidiaries

(US$ mm) (%) (US$ mm) (%)

CORPORATE PRESENTATION34

36%

60%

44% 41%

31%

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

1,676

2,634

3,5754,205

6,480

389 513878

1,2761,662

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Total Assets Total Equity

58 76

355 356 339197 183

260 291

541

255 259

616 647

880

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Cash and cash eq. ST investments

473

1,030

1,292

1,5321,640

218

771676

885760

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

(US$ mm)

(In US$m)

(1) Total debt is equal to interest-bearing loans and borrowings, plus financial

liabilities designated as at fair value through profit or loss

(2) Net debt is equal to total debt less cash and cash equivalents and short-term

investments

(US$ mm)

Balance Sheet Highlights

Total Cash and Short-Term Investments

Total Assets & Total Equity

Total Debt(1) and Net Debt(2)

Source: Audited VAS Consolidated Financial Statements for 2011, 2012, 2013, 2014 and Unaudited VAS 2015

Note: Based on exchange rate of US$1 = VND 22,540 as of 30 December 2015 (applied to 2015 financials)

Net Debt(2) / Net Debt + Total Equity

CORPORATE PRESENTATION35

F. Financial Overview - IFRS(1)

(1) Source: IFRS Consolidated Financial Statement for H1/ 2015

Based on exchange rate of US$1 = VND 21,840 as of 30 June 2015

CORPORATE PRESENTATION36

86

487352

144

78

342

151

60

170

973

523

60

Less than 1 year 1-3 years 3-5 years More than 5 years

Corporate bonds Convertible bond Convertible loan Long-term borrowings Short-term debts Total

(US$ mm)

Debt profile overview

Debt maturity

Average borrowing cost

11.6%11.0%

10.0% 9.5%

Dec-12 Dec-13 Dec-14 Jun-15

As of 30 Jun 2015:

• Average debt maturity: 3.8 years

Source: IFRS Interim Consolidated Financial Statement H1 201

Based on exchange rate of US$1 = VND 21,840 as of 30 June 2015 (applied to 2015 financials)

CORPORATE PRESENTATION37

Debt Mix Analysis

Total: VND37,681 Bn (US$1.73Bn)

Diversified Funding Sources(1)

Notes:Based on exchange rate of US$1 = VND 21,840 as of 30 June 2015 (applied to 2015 financials)

(1) As of 30 June 2015

(2) Including Convertible loan & Loan from Associate

Debt Breakdown(1)

By Currency

By Interest Rate

Domestic bond, 42.6%

International bond, 11.1%

Convertible bond, 8.3%

Bank loans, 36.9%

Others(2), 1.1%

VND, 72.3%

USD, 27.7%

Floating, 79.4%

Fixed, 20.6%

CORPORATE PRESENTATION38

53

127

341

507

255207

Dec-11 Dec-12 Dec-13 Dec-14 Jun-14 Jun-15

136 148279

252

181

42

Dec-11 Dec-12 Dec-13 Dec-14 Jun-14 Jun-15

116

230342

473

263

159

Dec-11 Dec-12 Dec-13 Dec-14 Jun-14 Jun-15

64184

6881,017

52135445

121

175

276

124231

109

305

863

1,293

645 585

Dec-11 Dec-12 Dec-13 Dec-14 Jun-14 Jun-15

Sales of properties Recurring income

(US$ mm) (US$ mm)

(US$ mm) (US$ mm)

Income Statement Highlights

Revenue

EBITDA(1)

Gross Profit

Profit for the Year(1)(2)

265

607

8

287

Adjustment for sale of Vincom Center A HCMC Adjustment for sale of Vincom Center A HCMC

(1) EBITDA excludes valuation gains / losses of investment property and investment property under construction

(2) Dec-13 EBITDAs and Profits include fair-value adjustment realised when the Group sold Vincom Center A HCMC

(3) Includes profit after tax of discontinued operations

Source: IFRS Consolidated Financial Statements for 2011, 2012,

2013, H1 2014, 2014 and H1 2015

Note: Based on exchange rate of US$1 = VND 21,840 as of 30 June

2015 (applied to 2015 financials)

CORPORATE PRESENTATION39

NA

56

75

99

5060

Dec-11 Dec-12 Dec-13 Dec-14 Jun-14 Jun-15

4662

102

134

65 70

Dec-11 Dec-12 Dec-13 Dec-14 Jun-14 Jun-15

NA

7

13

31

15 15

Dec-11 Dec-12 Dec-13 Dec-14 Jun-14 Jun-15

64184

688

1,017

521

354

Dec-11 Dec-12 Dec-13 Dec-14 Jun-14 Jun-15

(US$ mm)

Total Revenue

(US$ mm) (US$ mm)

(US$ mm) (US$ mm)

Rental(1) Sale of Properties

Hospitality & Entertainment Services Healthcare

Revenue Performance

Source: IFRS Consolidated Financial Statements for 2011, 2012, 2013, H1 2014, 2014 and H1 2015

Note: Based on exchange rate of US$1 = VND 21,840 as of 30 June 2015 (applied to 2015 financials)

(1) Include rental from Group’s Subsidiaries

109

305

863

1,293

645

585

Dec-11 Dec-12 Dec-13 Dec-14 Jun-14 Jun-15

CORPORATE PRESENTATION40

(US$ mm)

Total Gross Profit

(US$ mm) (%) (US$ mm) (%)

Rental(1) Sale of Properties

Hospitality & Entertainment Services Healthcare

Profitability – Gross Profit and Margin

Source: IFRS Consolidated Financial Statements for 2011, 2012, 2013, H1 2014, 2014 and H1 2015

Note: Based on exchange rate of US$1 = VND 21,840 as of 30 June 2015 (applied to 2015 financials)

(1) Include rental from Group’s Subsidiaries

53

127

341

507

255

207

Dec-11 Dec-12 Dec-13 Dec-14 Jun-14 Jun-15

(US$ mm) (%) (US$ mm) (%)

(4) (3)

84 3

(63%)

(21%)

26%29%

24%

Dec-11 Dec-12 Dec-13 Dec-14 Jun-14 Jun-15

Gross Margin

CORPORATE PRESENTATION41

25%

49%

37% 37% 36%

Dec-11 Dec-12 Dec-13 Dec-14 Jun-15

2,435

3,299

4,0244,612

5,515

783 7651,095

1,521 1,658

Dec-11 Dec-12 Dec-13 Dec-14 Jun-15

Total Assets Total Equity

58 76

354 356 404155 180

258 284

419

213256

612 640

823

Dec-11 Dec-12 Dec-13 Dec-14 Jun-15

Cash and cash eq. ST investments

468

997

1,259

1,550

1,769

256

741647

909 947

Dec-11 Dec-12 Dec-13 Dec-14 Jun-15

(US$ mm)

(In US$m)

(US$ mm)

Balance Sheet Highlights

Total Cash and Short-Term Investments

Total Assets & Total Equity

Total Debt(1) and Net Debt(2)

Net Debt(2) / Net Debt + Total Equity

Source: IFRS Consolidated Financial Statements for 2011, 2012, 2013, H1 2014, 2014 and H1 2015

Note: Based on exchange rate of US$1 = VND 21,840 as of 30 June 2015 (applied to 2015 financials)

(1) Total debt is equal to interest-bearing loans and borrowings, plus financial liabilities designated as at fair value through profit or loss.

(2) Net debt is equal to total debt less cash and cash equivalents and short-term investments

CORPORATE PRESENTATION42

G. Trading Performance

CORPORATE PRESENTATION43

Price VND47,600 as of 31 Jan 2016 10 Day 20 Day 30 Day 1 mth 3 mth 6 mth 12 mth 24 mth 36 mth 48 mth 60 mth

Average daily volume ('000) 2,211 2,202 1,999 2,202 1,359 1,253 1,162 1,267 1,139 943 857

Average daily trading value (VND mm) 105,249 104,669 92,975 104,669 61,995 55,291 49,285 51,833 44,853 36,439 32,652

Average daily trading value (US$'000) 4,669 4,644 4,125 4,644 2,750 2,453 2,187 2,300 1,990 1,617 1,449

Total volume traded (mm) 22.1 44.0 60.0 44.0 87.0 160.4 288.1 629.5 846.3 942.3 1,066.0

% of total shares outstanding 1.2% 2.4% 3.2% 2.4% 4.7% 8.6% 15.4% 33.7% 45.3% 50.4% 57.1%

% of free float 2.6% 5.1% 7.0% 5.1% 10.1% 18.6% 33.5% 73.2% 98.4% 109.6% 123.9%

Share price

Highest traded price (VND) 49,100 49,100 49,100 49,100 49,100 49,100 49,100 49,100 49,100 49,100 49,100

Lowest traded price (VND) 45,000 45,000 40,000 45,000 40,000 37,900 35,930 32,342 31,807 27,637 25,156

Performance over the period 0.2% 0.2% 19.0% 4.2% 4.6% 10.4% 24.8% 16.4% 32.9% 33.1% 59.2%

Index outperformance over the period (1) (3.4%) 5.3% 23.0% 10.0% 14.8% 22.6% 30.1% 18.4% 20.1% (6.4%) 52.4%

Average closing price (VND) 47,820 47,820 46,210 47,820 44,658 43,484 41,657 40,106 38,482 36,853 36,414

Volume weighted average price (VND) 47,599 47,530 46,510 47,530 45,602 44,124 42,420 40,925 39,379 38,632 38,103

Market cap as of 31 Jan 2016 (US$ mm) 3,945.2

Total number of shares (mm) 1,868.2

Share Price Performance over the Last 12 Months

Source: Bloomberg as of 31 January 2016.

(1) Performance against the VN Index.

32,000

37,000

42,000

47,000

52,000

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Jan-16Dec-15Nov-15Sep-15Aug-15Jun-15May-15Mar-15Feb-15

Sh

are

Pri

ce (

VN

D)

Vo

lum

e (m

)

Vingroup Share Volume Vingroup Share Price VN Index rebased

CORPORATE PRESENTATION44

This presentation may contain forward-looking statements that involve risks and uncertainties. Actual future performance,

outcomes, and results may differ materially from those expressed in forward-looking statements as a result of a number of

risks, uncertainties and assumptions. Representative examples of these factors include (without limitation) general industry

and economic conditions, interest rate trends, cost of capital and capital availability, cost of construction, availability of real

estate properties and land, competition from other companies and venues for the sale/distribution of goods and services, shifts

in customer demands, customers and partners, changes in operation expenses, including employee wages, benefits and

training, governmental and public policy changes and the continued availability of financing in the amounts and the terms

necessary to support future business. You are cautioned not to place undue reliance on these forward-looking statements,

which are based on current view of management on future events.

Disclaimer

CORPORATE PRESENTATION45

Vingroup JSC

Vingroup Office Tower, Vinhomes Riverside Eco-Urban Area

Long Bien District, Hanoi, Vietnam

Tel: +84 (4) 3974 9999 ext. 759

Fax: +84 (4) 3974 8888

Website: http://www.vingroup.net

E-mail: [email protected]

Investor Relations Department