January 2014 Islamic Finance Bulletin - Lancaster … Finance Bulletin January 2014...

21

Islamic Finance Bulletin January 2014 lums.lancs.ac.uk/research/centres/golcer Gulf One Lancaster Centre For Economic Research

Transcript of January 2014 Islamic Finance Bulletin - Lancaster … Finance Bulletin January 2014...

Islamic Finance Bulletin

January 2014

lums.lancs.ac.uk/research/centres/golcer

Gulf One Lancaster Centre For Economic Research

Page 2

From the Editor

The turn of the year has been all about the financial markets taking breath, momentarily away from the anxieties that have surrounded them, particularly regarding the tapering now due of the monetary medicine that has been dosed by the US Federal Reserve.

Whether the world’s economies are ready to take responsibility for sustaining growth momentum, besides by way of the stimulus of cheap money, is still somewhat in doubt.

The Asian region especially has experienced fallout from international flows returning to the US dollar, but also from the concerns brewing over accumulated debt afflicting the Chinese financial system, and over that economy’s growth prospects.

Stock markets have experienced some profit-taking as if somewhat overbought, bonds and sukuk have not reacted well to the signs of American recovery, while oil and base metals have seemed unconvinced of rising demand projections relative to the supply outlook. Gold has suffered from the lack of either deflationary or inflationary pressures on aggregate.

In this edition we feature two summary viewpoints from international banks surveying the global investment stage, as pointers for asset allocation, at this very uncertain juncture.

We also track developments, as usual, across the Islamic finance sector, with news and focused comment. In addition, Indonesia receives the spotlight in the feature space -- a country set to pursue a Shariah-compliant agenda both in its financial industry and in serving the all-pervasive, though small-scale, entrepreneurial dimension of its economic growth and development.

ContentsHIGHLIGHTS (p.3)

RECENT DEVELOPMENTS (p.4)

VIEWPOINT (p.7)

VIEWPOINT (p.8)

FEATURE (p.9)

STOCK MARKETS (p.12)

COMMODITIES (p.15)

BOND AND CDS MARKETS (p.16)

PERSPECTIVE (p.19)

DIARY (p.20)

Page 3

Egyptian Markets: The improvement in Egypt’s stock

and bond markets, while international counterparts have

been affected by uncertainty, is to some extent testament

to the separation of financial assets from concurrent

economic and political realities, but also to the volatility

and recovery trend that can follow sharp downturns. The

recent uptrend has related particularly to the implied

stability of an overwhelming referendum result towards a

new constitution, although sporadic outbursts of violence

have claimed many lives and continued to disfigure an

already severely fractured society. Economic growth is

quickening, but inflation may become a threat.

Asset Allocation: The new year has presented a difficult

juncture for the reassessment of portfolio investment.

Stocks have been inclined to pause and reflect on whether

corporate earnings will catch up with elevated market

indices, so particularly attuned to the results season due

now. The possibility that the extremes of the easy money

era -- that has dominated sentiment, from US benchmarks

to the rest of the world -- might draw to a close has also

concentrated minds. Bond markets have begun to reflect

rising yields, although fund flows returning to the US apply a

moderating influence on US Treasures, by way of their effect

on the dollar.

Indonesia: Far behind Malaysia in terms of developing

Islamic finance capability, Indonesia should have

significant weight behind the sector’s potential growth,

not least the largest Muslim population in the world

(some 210 million). Bankers perceive Shariah-compliant

business as a priority objective, while government intends

both infrastructural and poverty alleviation needs to

be addressed by the sector, in a country dominated by

small and micro enterprises. Analysts reckon still that

regulatory and tax adjustments need to be made to

provide necessary impetus. Attention is needed also to

maintaining control of a fast-paced economy.

Highlights

Recent Developments in the Islamic Finance Industry

New global strategy for sukuk

According to HSBC, the bank that managed the most

sukuk sales in 2013, many governments worldwide are

now seeking to take the opportunity to utilise sukuk to

cut financing costs, a driver which is expected to drive

sales in 2014/15. Sukuk markets and their growth

are very likely to feature in the upcoming period

as governments from Dubai to Malaysia compete

to promote Shariah-compliant bonds and become

centres for Islamic finance. London has now joined the

game, aiming to introduce new instruments to help the

securities compete with conventional bonds. Islamic

bond sales fell 9.5% in 2013 to $42bn after reaching a

record $46.4bn the previous year, according to data

compiled by Bloomberg. Expectations are for $60bn

of sukuk to be issued in 2014, to be dominated by

Malaysia and the Gulf countries.

Source: Bloomberg, December 25th

GOLCER thinks 2014 will witness expansion in current

sukuk markets worldwide apart from the joining of new

issuers. Many countries in late 2013 announced plans

to sell Islamic bonds as part of efforts to grab a greater

share of the Islamic finance industry. Announcements

from countries like the UK and UAE have added

significantly to awareness among international markets

of the sukuk product.

Qatar issuance plans as debt market forms

Qatar has announced the offer of more than $6.6bn

in local currency bonds and sukuk. This represents the

largest sale in three years, since the issue of 50m riyals

of securities in 2011, as the country seeks to deepen

its domestic debt market in the lead-up to hosting the

World Cup. The plan is for the central bank to sell 11bn

riyals ($3 bn) of sukuk and 13 bn riyals of non-Shariah

compliant bonds. Qatar’s plan is to establish a local

currency debt market, with the aim of incentivising

banks to release some part of the liquidity they hold.

Source: Khaleej Times, January 15th, and Islamic

Global.com January 14th

GOLCER considers Qatar, the world’s largest

exporter of liquefied natural gas (LNG), to be

showing serious interest since the late of 2013 to

develop its capital market through Islamic finance

instruments, in an attempt to find ways to cover

government debt. The country last month sold 500m

riyals of Islamic bonds due 2018 with a profit rate of

3%. Yet, this strategy to finance big projects through

sukuk will have to be handled carefully, owing to the

risk of any sudden drop in the prices of oil and gas,

and hence fall in government revenues, which could

threaten the whole process.

IILM to expand sukuk issuance to $860m

Malaysia-based International Islamic Liquidity

Management Corp (IILM), a consortium of central

banks from Asia, the Middle East and Africa,

has announced an expansion of its Islamic bond

programme by $370m to $860m. This will increase

its issuance of short-term sukuk for the first time since

its launch last year, these being designed to meet a

shortage of highly liquid, investment-grade financial

instruments, which Islamic banks can trade to manage

their short-term funding needs. The IILM will conduct

the auction of 3-mth sukuk by the end of January.

Shareholders of the IILM are the central banks of

Indonesia, Kuwait, Luxembourg, Malaysia, Mauritius,

Nigeria, Qatar, Turkey and the UAE, as well as the

Page 4

Recent Developments in the Islamic Finance Industry

Jeddah-based Islamic Development Bank.

Source: ArabianBusiness.com, January 16th

GOLCER finds this initiative a novel method for

boosting liquidity management in many Islamic

banks, which have been struggling to compete with

conventional counterparts. We believe that even

under this initiative, still substantial challenges still

await the industry across many countries, given the

short history of sukuk issuance and the restrictions

imposed on liquidity management in Islamic banking

under the limited access to market funds in compliance

to Shariah (see Focus section).

Brunei’s takaful growth meeting ambitions

Assets held by the Islamic insurance (takaful) sector

in Brunei have shown tremendous growth while

those of conventional types of insurance have been

declining, a report from the country’s central bank has

shown. That comes as part of the country’s strategy

to diversify Brunei’s economy as well as wean itself off

dependence on oil reserves, which are expected to run

out in about two decades. According to the monthly

report by Brunei’s monetary authority (AMBD), takaful

assets rose 21% to 425m Brunei dollars ($336m), while

conventional insurers saw a drop of 1.3% in assets

during the same 12-mth period to end-September

2013, with the takaful market accounting for 33% of

total insurance assets, up from 29% during 2012.

Source: Reuters, January 15th

GOLCER finds these figures promising for the fast-

growing takaful sector, and, if continued, this pattern

would enable Brunei to lead in the global industry

and progress further towards its goal of creating

Islamic products. The country, which has the highest

per-capita income in the region after Singapore, has

announced its interest in competing in Islamic finance

with the regional leaders in the sector, Malaysia and

Indonesia.

UAE led Islamic indices in 2013

During 2013 UAE’s Islamic index led international

stock-market performance tables. Its TR (total return)/

IdealRatings GCC Islamic Index was up nearly 26%

on the year, with the TR UAE Islamic Index up 97%.

The top five performing GCC Shariah-compliant

stocks were from the financial sector: Union Properties

(+239%), Deyaar (201%), Dubai Islamic Bank (187%),

Al Salam Bank (167%) and RAK Properties (164%) --

hence, four of the top performers were from the UAE.

Still, however, the Gulf’s pre-eminence in composite

measures was challenged by a Malaysian index

which seeks to attract GCC-based Shariah-compliant

investors. In 2013 Malaysia’s Securities Commission

introduced three financial ratios for Shariah screening

-- the vetting process for selecting companies in which

to invest -- to be phased in this year to avoid Islamic

portfolio destabilisation. The Malaysia TR Islamic Index

was up 9.6% for 2013, the conventional TR Malaysia

index 14.3%.

Source: Khaleej Times, January 12th, and Islamic

Global.com, January 14th

GOLCER finds that the launch of Malaysia’s indexes

provides an important reference for investors to

negatively screen companies whose activities are not

Shariah-compliant. Meanwhile, it is unclear whether

the UAE stock market’s outperformance last year

represents a one-off event or will be an ongoing trend,

given the country’s outstanding plans for the 2020

Expo, underlined by its winning bid.

Libya plans to expand Islamic banking

Libya is now moving towards a gradual transformation

of its banking and economic system to comply fully

with Shariah by 2015, as announced this month by

the economy minister and other officials. The growth

of Islamic banking was not encouraged during the

rule of Muammar Gaddafi, owing to governmental

conservatism. Two years after his ousting, current prime

minister Ali Zeidan’s government has announced the

country’s interest in attracting foreign investment and

Page 5

Page 6

developing the non-oil sector of the economy. However,

these objectives are subject to the continuing struggle to

overcome political instability.

Source: Reuters, January 15th

GOLCER views that this agenda for Shaiah-compliance,

while it supports the country catching up in the race for

Islamic banking expansion and its international industry

recognition in that respect, might add to the political turmoil

in Libya. At the same time, since Libya has become too

dependent on its oil sector and needs to boost investment to

upgrade its infrastructure, sukuk could provide a way to help

achieve that objective.

Morocco adopts Islamic finance law

Morocco’s government has finally adopted the existing

proposal for Islamic banks and sukuk after months of

discussions and delays. This approval of the law represents

the last step before establishing fully-fledged Islamic banks

in the country, which has been seeking to develop Islamic

finance for about two years, partly in an attempt to attract

Gulf money and cover a huge budget deficit. With the

sensitivity of the Moroccan political elite to Islamism, this

process of adoption has been slowed. Morocco’s central

bank has now started talks with Islamic scholars to establish a

central Shariah board to oversee the fledgling Islamic finance

industry.

Source: EIN news, January 19th

GOLCER finds this step to ratification of the Islamic sector as

an important measure which may bring more Gulf investment

into the country. During 2013 Moroccan deputies approved

legislation allowing the government to issue sovereign sukuk,

but it has not yet moved ahead to raise its first Islamic bonds.

FocusAs reported by The Sun Daily, Malaysia, in his keynote

address at the Islamic Financial Intelligence Summit

November 2013, Dr Nazrin Shah, financial ambassador of

the Malaysian International Islamic Financial Centre, said

the lack of secondary trading in the global sukuk market

resulted from the ‘buy-and-hold’ mentality of investors.

There was a need “to develop more depth and breadth

to allow sukuk to grow as an important liquidity

management tool”, he said, observing that there is also

“a stark imbalance in sukuk infrastructure development

between jurisdictions, that has curtailed cross-border

transactions”. That condition “limits the ability of sukuk

to be at par with conventional fixed-income securities,

which are traded extensively on a global scale,” he

said. “There needs to be greater integration among the

various Islamic financial jurisdictions.”

The November 2013 edition of The Banker magazine

remarked that the IILM’s debt issuance in August,

while “a significant milestone” would “hardly dent the

industry’s short-term liquidity management issues, which

are hampering [its] growth”. To this date many Islamic

banks “place their surplus funds with conventional

banks by means of bilateral murabaha transactions

based on goods, for example, commodities or metals,

and services not connected to the underlying business of

the financed party”.

The withdrawal by the Saudi Arabian Monetary

Agency (central bank) from the IILM in April 2013

was “likely to limit trade participation in the sukuk by

Saudi institutions”, the periodical claimed. Another

challenge was the international regulatory order. “The

Basel III liquidity requirements, in particular the liquidity

coverage ratio, stipulates institutions hold a sufficient

buffer of high-quality liquid assets to cover liquidity

outflows for a one-month stress period. With their

[currently] limited range of short-term instruments, this

requirement places Islamic institutions in a somewhat

compromised position.”

Euromoney magazine’s December 2013 issue reflected

that when the IILM was established [in October

2010], it represented a widespread recognition that

Islamic banking “might have run into serious trouble

in the global financial crisis had there been a loss of

confidence in inter-bank liquidity”. Islamic banks then

did not have any instruments available in the capital

markets to bolster liquidity, particularly cross-border.

As the equity markets have roared in the New Year, we think some signs of exhaustion in the current rally may emerge in late January. The US Federal Reserve could taper its quantitative easing (QE) programme further. Also, the US government debt ceiling has to be raised by end-month, and this could lead to some friction in Congress. Emerging markets (with the exception of GCC areas) are still under-performing the developed world, as long-term USD interest rates rise.

While we are cautious about the markets in the immediate month ahead, by April 2014 we expect another leg up in the GCC equity markets ahead of the formal inclusion of the UAE and Qatar stock markets into the MSCI emerging market indices.

We do not anticipate any market crashes in 2014. This is because major central banks and the IMF are still vigilant about deflationary threats to the global economy, and will likely extend a lifeline to markets if any sign of a precipitate decline in market indices is in the offing. The US economic recovery is well under way. US growth accelerated in 2013Q4, and most recent data releases show more of the same. Japan’s growth is also robust, as the yen remains weak, but an impending increase in consumer sales taxes in April/May 2014 make quiet markets for a while. However, we think the Bank of Japan will quell any uncertainty on this score by persisting with its QE programme. Europe is expected to expand, entering its first year of economic growth according to forecasts, after a long recession, but the growth rate is quite lacklustre. In general emerging market (EM) imbalances should prevent outperformance of EM risky assets. In China a

tightening macro-policy is restraining equities in spite of their cheapness.

We remain overweight on US equities. Multiples are not stretched despite the recent run owing to earnings growth, forecast to be between 8% and 12% for US companies in 2014. The comparison with government bonds is still favourable to equities, as long as yields rise gently and in line with economic growth.

Oil and gold prices could see another leg down by mid-2014. Various reports have estimated that total US crude oil production would increase to 8.5 million barrels per day this year, which is an increase of 1 million from 2013. The expectation of Iran coming into the mainstream of supply, along with Libya and Iraq committed to increase their production, could create a glut of supply. Furthermore, growth in shale oil development will likely continue to keep prices skewed on the downside.

We like to accumulate USD on dips against other currencies. Trading currencies versus the dollar should be done in a very opportunistic way, with a short-term, technically-driven view in the first half of the year. But as the tapering of asset purchases by the Fed progresses, and the economic recovery pushes US yields higher, the dollar should gain momentum.

This is an abbreviated version of the CIO newsletter from Emirates NBD wealth management

A mild markets dip soon to follow a stellar 2013

by Arjuna Mahendran, Chief Investment Officer, Emirates NBD Wealth Management

Viewpoint

Page 7

2013 was a great year for equities and risky assets in general. It was also a remarkable year for the financial community, as the Nobel Prize in Economics was attributed to Professors Eugene Fama, Lars Peter Hansen and Robert Shiller “for their empirical analysis on asset prices”. According to our records, it has been 23 years since the Nobel Academy last distinguished a work that relates to investor needs in terms of investments, asset allocation, or strategy.

2014 appears to be a year of further economic “normalisation”, which should remain supportive for cyclical and risky assets especially in advanced economies.

The call for better economic prospects remains unchanged, but our confidence is now higher. There is clearly better visibility, with fewer identified uncertainties: geopolitical tensions have greatly eased, Eurozone sovereign stress has waned, the US fiscal dispute is over, etc.

In fact, there are even more potential positive surprises ahead: Japan’s economic policies may prove a success thanks to innovative initiatives, Eurozone structural reforms on internal competitiveness could be decided, and China might surprise the world by succeeding in a smooth transition from its planned export-driven economy to a liberalised consumer-driven economy, averting a hard landing.

International investors increasingly share the sentiment of better visibility, currently driving asset prices higher. This trend should continue. In a world of low interest rates and abundant liquidity, stocks and high yield bonds still have room to appreciate further.

Yet, we cannot help tempering our optimism for 2014 with some reminders of caution. The world is, of course, full of uncertainties and surprises!

Keeping in mind Robert Shiller’s impressive record of tracking investor exuberance by warning for bubbles in 2000 and again in 2005-2007, we have to remember his conclusions:

o Long-term asset returns are conditioned by structural equilibrium in economic conditions, such as interest rates, growth rate, corporate profitability, etc. This equilibrium prevails over cyclical fluctuations, and over long periods, the main economic drivers such as unemployment, profits, or inflation, revert to their average trends.

o Therefore, relevant predictors of long-term returns are not short-term trends but valuation metrics that show the relationship between asset price and a long-term average of an economic indicator such as stock index/GDP, stock prices/tangible assets, stock prices/profits, bond yield/average inflation. Note that these metrics do not give any valuable information for short-term returns.

o Bubbles do exist, and appear when investors fall prey to “irrational exuberance”, confusing short-term market trends with long-term expected returns.

Beware of possible market exuberance building up in 2014, as global growth accelerates, and thus be ready to reverse positions.

Most asset prices could perform well, given current economic and financial conditions, but this is not a guarantee of extraordinary long-term returns, especially if the current conditions are themselves extraordinary.

Green Light, but Mind the Speed Limit!

by Xavier Denis, Global Strategist at Societe Generale Private Banking

Viewpoint

Page 8

Formed of thousands of islands, Indonesia is South-east Asia’s biggest economy, and has the world’s largest Muslim population (12.7% of the world total).

Oxford Business Group has described the country as “a vast, diverse nation, with a rapidly growing economy, extensive natural resources and a range of sectors ripe for investment”. It also has relative political stability, though periodically marred by secessionist and terrorist issues.

In the PwC publication World in 2050, it was projected that Indonesia’s economy in purchasing power parity (PPP) terms could be bigger than that of Germany, France or the UK by mid-century.

Indonesia regained its investment grade rating from Fitch in late 2011 and Moody’s in early 2012, after being deprived of that status in late 1997 owing to the Asian financial crisis. (S&P has yet to reinstate that level of approval.)

However, the country in the past year has arguably suffered the most from the recent emerging market turmoil. The Financial Times suggested that policymakers had “turned complacent” and failed to implement the reforms needed to provide a buffer against falling commodity prices.

Equities and the rupiah reacted badly to the Fed-ignited exodus from emerging markets generally last year, with local economic fundamentals in doubt. As the current account deficit widened and inflation rose, the central bank hiked interest rates.

The government still expects GDP growth of 5.5% in 2014, but pending general and presidential elections have trimmed expectations of inward investment, despite presidential plans to build power stations, roads, bridges and ports to attract investors.

Additional factors in the mix have been the

Islamic finance report card: Indonesia

by Rachel Latham and Andrew Shouler

Feature

Page 9

Page 10

announcements in December of (a) new rules to ease some restrictions on foreign ownership, but (b) the banning of mineral ore exports, including bauxite and nickel, from mid-January in an effort to spur investment in mineral processing, intended to boost long-term state revenues by converting the nation into a manufacturer of higher-value products.

As to Indonesia’s banking sector, it has some key, enviable advantages: serving a population of well over 200m, with one of the lowest penetration rates in the region, and a high level of profitability based on interest rate spreads of around 7%.

According to The Economist, the banks have high capital ratios, at an average of almost 17% for the country’s commercial lenders. Credit growth of some 20% annually in recent years has been funded mostly by deposits rather than wholesale borrowing, and non-performing loans (NPLs) are only 2% of total lending. Rating agencies have even suggested that monetary policy tightening will help check risky exposures.

A 2013 report by PwC found that banks are “generally positive with the growth outlook”, subject to the increase in regulatory requirements and the growth in competition in the market. Smaller enterprises in particular will be a significant driver.

Slow developer

Indonesia was a latecomer to the Islamic finance

sector, in fact some 25 years behind Malaysia in that respect. The passing of the Shariah Banking Law in July 2008, however, was followed by a tripling of Islamic bank assets in the subsequent five years, increasing by over 30% per annum.

The number of Islamic banking outlets has jumped from under 250 to over 500, comprising 11 fully Shariah-compliant banks (compared with 120 conventional lenders), 24 Islamic banking units and 158 Shariah-compliant rural banks. Even so, in common with typical shares internationally, Islamic financial service providers account for only 4-5% of total banking sector assets.

In fact, reviewing the sector in 2012, Reuters said that Islamic finance in Asia has been “a distinctly Malaysian affair; Indonesia does not even figure”. It argued that, by addressing this shortcoming, it could solve two of its biggest financing challenges: funding infrastructure and reducing its dependency on foreign borrowing. Indeed, Indonesia could learn from Malaysia’s experience and “even exploit the deep liquidity pool that Malaysia has built”.

The news provider noted that about 210m of Indonesia’s 240m people are Muslims, a natural source of demand for Islamic finance products. “It is the government, however, that needs to provide the top-down part of the equation in the form of the necessary regulations and tax incentives that will ensure Islamic finance becomes a viable option.” In that regard, a key change is due in adjusting to the distinction between beneficial and legal ownership, to allow sukuk to become a viable project financing tool.

“The Islamic financial sector entertains hopes

that a mix of state-backed infrastructure projects and regulatory reforms

will maintain the sector’s momentum.”

“Equities and the rupiah reacted badly to the Fed-

ignited exodus from emerging markets generally

last year, with local economic fundamentals in doubt.”

Page 11

The Islamic financial sector in Indonesia entertains hopes that a mix of state-backed infrastructure projects and regulatory reforms will maintain the sector’s momentum.

Poverty alleviation

Equally, policy discussions have prioritised the issue of increasing financial access -- especially to micro, small, and medium enterprises (MSMEs) – to alleviate poverty. Indonesia has more than 50 million MSMEs, representing some 97% of all enterprises, contributing around 30% of GDP growth (2012). Many do not have sufficient access to financing with which to grow their businesses.

The basis is clearly there for the sector to continue growing at twice the rate of conventional finance. Just over one-third of bankers surveyed have nominated Shariah-compliant banking as a high priority in their strategy.

With the unbanked accounting for over 50% of the population, the potential is “immense”, according to Edy Setiadi, Head of the Islamic Banking Department at Bank Indonesia (BI), the country’s central bank.

BI is accelerating reforms, including the development of liquidity instruments and capital markets, he has asserted. This month all financial institutions (Islamic included) will come under the supervision of the Financial Services Authority (FSA). By 2020, one in five banks may be Shariah-compliant.

The authorities plan to bring enabling policies, ranging from regulating foreign exchange markets, and introducing Islamic repurchase agreements to aid liquidity management (a persistent bugbear for the industry), as well as education and promotion initiatives.

The central bank’s deputy governor has forecast that Islamic banking could account for 15-20% of Indonesia’s banking industry within a decade, although a slowdown in the accumulation of assets could be seen this year because of the testing economic conditions. Developing an Islamic lender of last resort would help Islamic banks during periods of financial stress.

As for the insurance industry, a draft law is with parliament for the development of the takaful sector, which currently is dominated by window services. Legislation to require that those units be divested is likely to be sidelined this year, overtaken by other business.

Still, the Islamic finance industry’s overall impetus seems well-founded, with news emanating month by month. As an example, this January PT Bank Panin Syariah Tbk , a division of Indonesia’s seventh-largest bank, has raised 475bn rupiah ($39.3m) with an IPO of shares, so becoming the first fully-fledged Islamic lender listed on the Indonesian stock exchange.

Sources: Oxford Business Group, PwC, The Economist, BBC, Reuters, Bloomberg, Financial Times, Fitch Ratings, Standard & Poor’s

Rachel Latham is a freelance writer

GCCGCC equity markets extended their rally in December.

For 2013 as a whole, the composite S&P measure

recorded an increase of 30.1%, dominated by the

UAE’s Dubai and Abu Dhabi bourses, up 108% and

63% respectively. Kuwait was the worst performer,

with a yearly gain of 8.4%.

Dubai’s DFM Index showed buoyancy across all

sectors, except for a modest retreat by insurance.

Banks and real estate gave returns of 16.4% and

19.7% in turn. The heavyweight Saudi Tadawul rose

by around a quarter, led by retail, hospitality and

petrochemicals, while Qatar’s index, comparatively

subdued in recent months, still climbed 28% over the

year. While some disappointment attached to Q3

earnings made little impression on the collective surge,

a closer look was expected to be made of Q4 data

due from mid-January. Retail investors especially still

seemed oriented to dividend stocks, with sentiment

overall leaning to the optimistic, despite global

concerns over the US Fed’s ‘tapering’ plans.

MENA

Reflecting the special situation of the Egyptian case,

Cairo’s benchmark EGX 30 Index outshone other

Middle Eastern bourses, which retreated overall. In

fact, Bloomberg reported its surge of 8% on the month

as the second highest across over 90 indices tracked,

next to Dubai’s, heading for a three-year peak. Given

that only relative stability had been procured since

the mid-year ouster of president Morsi, that was

quite a remarkable performance. CNBC suggested

that investors had “largely taken repeated protests

and pervasive violence in their stride”, comforted

by the imminence of the mid-January constitutional

referendum that would pave the way for parliamentary

and presidential elections. The toughening

of legislation on public gatherings generated

nervousness, however. Another government stimulus

package, worth $4.4bn, was greater than anticipated.

The market has been boosted by a succession of

interest rate cuts supporting the economy, although at

the price of rising inflation. FX reserves slipped slightly.

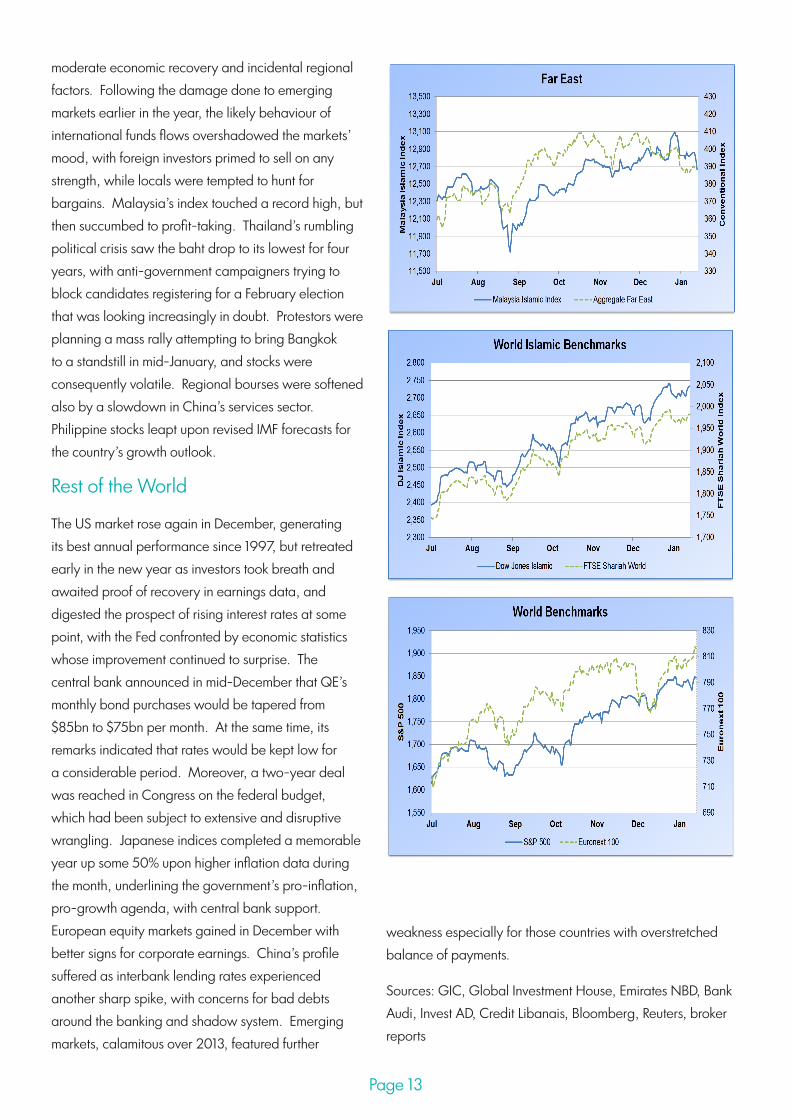

Far EastAsian stocks were mixed in the face of confused

expectations of the Fed’s intentions towards tapering

its QE monetary stimulus programme, the US’s

Stock Markets

Page 12

moderate economic recovery and incidental regional

factors. Following the damage done to emerging

markets earlier in the year, the likely behaviour of

international funds flows overshadowed the markets’

mood, with foreign investors primed to sell on any

strength, while locals were tempted to hunt for

bargains. Malaysia’s index touched a record high, but

then succumbed to profit-taking. Thailand’s rumbling

political crisis saw the baht drop to its lowest for four

years, with anti-government campaigners trying to

block candidates registering for a February election

that was looking increasingly in doubt. Protestors were

planning a mass rally attempting to bring Bangkok

to a standstill in mid-January, and stocks were

consequently volatile. Regional bourses were softened

also by a slowdown in China’s services sector.

Philippine stocks leapt upon revised IMF forecasts for

the country’s growth outlook.

Rest of the World

The US market rose again in December, generating

its best annual performance since 1997, but retreated

early in the new year as investors took breath and

awaited proof of recovery in earnings data, and

digested the prospect of rising interest rates at some

point, with the Fed confronted by economic statistics

whose improvement continued to surprise. The

central bank announced in mid-December that QE’s

monthly bond purchases would be tapered from

$85bn to $75bn per month. At the same time, its

remarks indicated that rates would be kept low for

a considerable period. Moreover, a two-year deal

was reached in Congress on the federal budget,

which had been subject to extensive and disruptive

wrangling. Japanese indices completed a memorable

year up some 50% upon higher inflation data during

the month, underlining the government’s pro-inflation,

pro-growth agenda, with central bank support.

European equity markets gained in December with

better signs for corporate earnings. China’s profile

suffered as interbank lending rates experienced

another sharp spike, with concerns for bad debts

around the banking and shadow system. Emerging

markets, calamitous over 2013, featured further

Page 13

weakness especially for those countries with overstretched

balance of payments.

Sources: GIC, Global Investment House, Emirates NBD, Bank

Audi, Invest AD, Credit Libanais, Bloomberg, Reuters, broker

reports

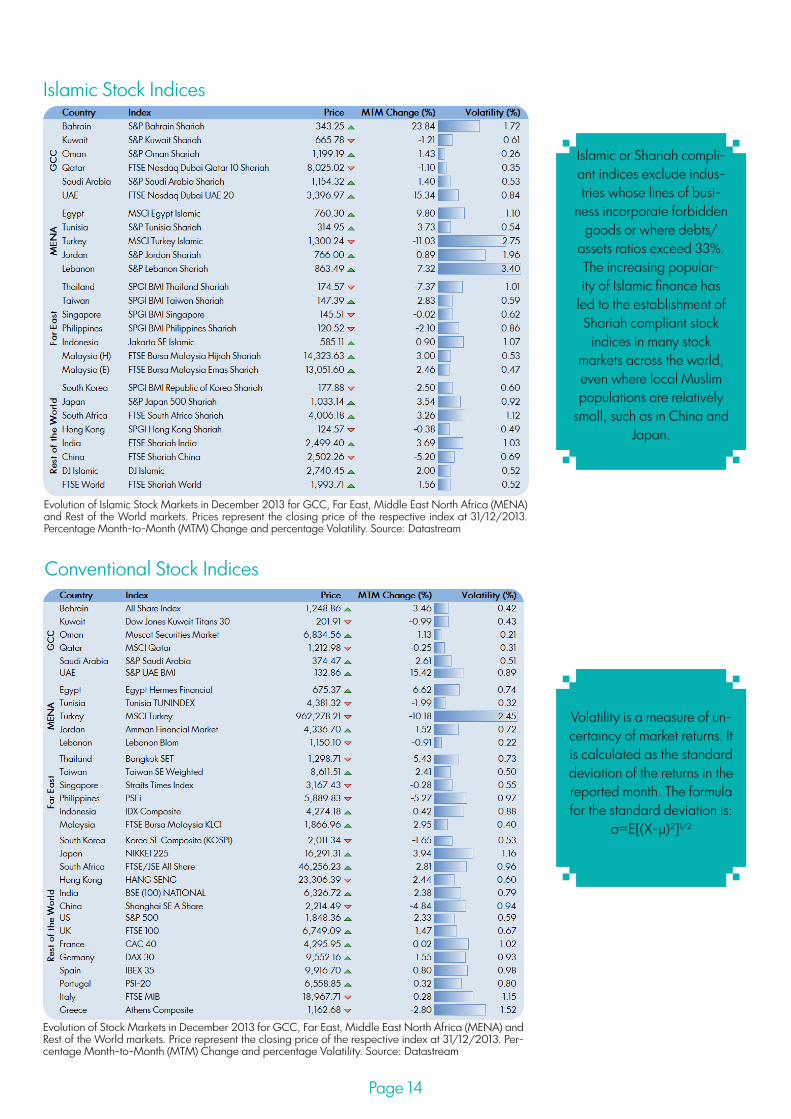

Islamic or Shariah compli-ant indices exclude indus-tries whose lines of busi-

ness incorporate forbidden goods or where debts/

assets ratios exceed 33%. The increasing popular-ity of Islamic finance has

led to the establishment of Shariah compliant stock

indices in many stock markets across the world, even where local Muslim populations are relatively

small, such as in China and Japan.

Volatility is a measure of un-certaincy of market returns. It is calculated as the standard deviation of the returns in the reported month. The formula for the standard deviation is:

σ=E[(X-μ)2]1/2

Islamic Stock Indices

Conventional Stock Indices

Evolution of Islamic Stock Markets in December 2013 for GCC, Far East, Middle East North Africa (MENA) and Rest of the World markets. Prices represent the closing price of the respective index at 31/12/2013. Percentage Month-to-Month (MTM) Change and percentage Volatility. Source: Datastream

Evolution of Stock Markets in December 2013 for GCC, Far East, Middle East North Africa (MENA) and Rest of the World markets. Price represent the closing price of the respective index at 31/12/2013. Per-centage Month-to-Month (MTM) Change and percentage Volatility. Source: Datastream

Page 14

CommoditiesOilOverall, volatility in crude markets was low in 2013, and the pattern continued through the end of the year, leaning eventually to the downside, with Iran’s potential return to the market with elevated volumes a suppressive factor, also the gradual escalation of US shale production, plus talk that the Libyan authorities may use force to free ports for exporting. Brent prices eased by 4.3% on the year upon these global influences, while WTI perked up towards year-end in response to a mixture of faster US growth data and distillate fuel supplies dwindling with bad weather bolstering demand for heating.

GoldGold slumped 28% in 2013, prolonging the decline in place since peaking in excess of $1,900 an ounce in August 2011. The latest depressive news was the Fed’s decision to taper QE from this month, whereby the $1200 level was breached, threatening heavier selling if technical points were broken around the recent low of $1180. Steadily improving global economic data, without sparking inflation, have proven anathema for the precious metal, geared to safe haven appeal, and analysts (though seriously awry with their forecasts last year) generally have sideways expectations this year. Some short-covering, with physical demand prompted by the pending Chinese new year, were thought liable to give limited support.

Copper/Base MetalsWhile copper prices underwent a 7.2% annual decline, with inventories climbing for the first time in four years, stronger trends arising from the US locomotive to the world economy gave the market a lift in December. Hedge funds turned to betting on higher prices, with stockpiles lately under some pressure, though 14% up on the year. Scheduled mining production increases around the world are likely to create a surplus of 127,000 tonnes in 2014,

Page 15

Barclays forecast. Still, although the key customer of China has continued to experience yearly slowdowns,

a tightness in scrap, disruptions at smelters and Chinese strategic buying (in connection with financing deals) gave prices a positive tilt. Indonesia’s decision

to curb exports has also compromised the outlook.

Sources: OPEC, Reuters, Bloomberg

GCC

Regional debt showed a muted, though variable, response to the mid-December announcement of the US Federal Reserve that it would trim its monthly bond purchases to $75bn from the $85bn that had prevailed for an extended period. While Fed policy was a dominant factor in driving market trends globally, the decision itself had been widely foreshadowed. Moreover, GCC issues have benefited from the firmer financial fundamentals enjoyed by the region. GIC suggested that Gulf markets were “nicely placed, with strong credit metrics and relatively low correlation with US Treasuries”. Invest AD advised that Middle East credit markets had remained strong in 2013 owing to positive local news flow (e.g. Expo 2020 being awarded to the UAE), and slower than anticipated primary issuance.

Egypt / MENA

Egyptian sovereigns rode the same investor wave as equities during December and into January, culminating in the apparent boost to stability from the 98% referendum vote in favour of a revised constitution. Prior to that bonds had fallen in reaction to explosions in Cairo incurring fatalities ahead of the third anniversary of the uprising that ousted President Mubarak. Local-currency bond prices improved alongside the state’s 2020 and 2040 international issues. Like stocks, fixed-income in the country has, generally speaking, been supported by the $15bn of aid pledged from Gulf countries, the pound consequently being kept fairly stable, and GDP growth showing some acceleration. A credit outlook uprating was given by Fitch early in January. Tensions have persisted, however, continually clouding the state of the market.

Malaysia / Far East

Malaysian bonds had a sideways feel to them, but a negative tone, in December, before picking

Bonds and CDS markets

up in the new year. Since funds flew from emerging markets in mid-2013 the impression of international repatriation to the US dollar has hung particularly over Asian markets. The ringgit subsided month on month accordingly, also reacting to rising inflation data, while growth forecasts also have been lifted. Moody’s issued a positive rating outlook in regard of improved prospects for fiscal consolidation and

Page 16

Credit Default Swap Markets

Sovereign Bond Markets

Evolution of Bond Markets in December 2013 relative to the previous month. The table reports the price index on which the MTM Change is calculated (month-to-month) and the Yield of sovereign bond maturities typically between 6 months and 25 years. Data as at 31/12/2013.

Evolution of CDS Spreads in December 2013 relative to the previ-ous month. The index reported here represents the average ba-sis points (bp) of a 5-year CDS for protection against sovereign bonds. Data as at 31/12/2013. MTM Change refers to the change relative to the previous month.

reform, while acknowledging the “credit pressures” facing the whole region because of the Fed’s tapering exercise. Local bond portfolio managers were said to remain optimistic, with bonds offering stable income. Foreign investors too have shown little sign of abandoning Malaysia in terms of outright capital flight.

Global Benchmarks

US Treasuries ended 2013 in pretty despondent mood, seeming to suggest the prolonged bull run was over now that the Fed would be turning off the monetary taps, albeit slowly, and the economy was showing distinct signs of life. The central bank’s insistence that further tapering would be “in measured steps” came as scant consolation. Economic indicators leant clearly towards a change of pace in activity, whether in non-farm payrolls or consumer confidence or retail sales. Inflation, meanwhile, remained subdued, extending some support to fixed-income. In Europe data were not as constructive as to recovery, but the lingering threat of deflation was in some sense bond-supportive. Ironically, peripheral eurozone bonds gained relative to core issues in 2013, having lost the most during crisis times. JGBs were range-bound in December, feeling the knock-on from the US lead, but restrained by the dominance of BoJ over the market.

Source: GIC, InvestAD, Capital Economics, Bloomberg, Financial Times, broker reports

Page 17

Islamic Bonds (Sukuk)

Sukuk markets were relatively quiet as year-end approached, partly reflecting a degree of uncertainty over the prospects for fixed-income in 2014, yields already having reacted to signs of economic recovery and the Fed’s QE tapering noises.

In the GCC a flattish trend outturned, mostly governed by international stories. Islamic bonds (-0.29%) underperformed conventional (-0.01%). HSBC Nasdaq- Dubai’s USD Sukuk TR Index (Bloomberg:SKBI) eased a fraction to close at 147.45, while the HSBC Nasdaq-Dubai GCC Conventional USD Bond TR Index (Bloomberg:GCBI) slipped marginally to 161.28.

Primary issuance was limited in the seasonal lull. KFH Research reported that the total for the month of December (at $14.1bn) brought the overall figure for 2013 to about $120bn, some 9% down on the year.

Pengurusan Air SPV sold MYR1.2bn ($360.4m) of dual-tranche sukuk bonds at tenors of five and seven years, the MYR1bn five-year government-guaranteed tranche yielding 4.16%, at the top of guidance.

Saudi Electricity Co completed a 4.5 billion riyal ($1.2bn) 10-year floating-rate sukuk offer, priced at 70 basis points over Saibor.

Supranational agency International Islamic Liquidity Management Corp (IILM) auctioned $860m in 3-mth Islamic bonds, the 0.556% yield a touch below the 0.562% paid at the time of the organization’s debut $490m 3-mth issue last August.

Malaysia’s state-backed mortgage lender Cagamas Bhd doubled its annual issuance of bonds for 2013 with a year-end sukuk worth 500 million Malaysian ringgit ($151.9m). A jittery market was blamed for a less than average subscription rate, with bank products of the same tenor said to offer higher yields.

Sukuk is the Arabic name for financial certificates, but commonly refers to the Islamic equivalent of bonds. Since fixed income, interest bearing bonds are not permissible in Islam, Sukuk securities

are structured to comply with the Islamic law and its investment principles, which

prohibits the charging, or paying of interest. Financial assets that comply with the Islamic law can be classified in ac-

cordance with their tradability and non-tradability in the secondary markets.

Telekom Malaysia Bhd announced it had made its first issuance of IMTN of 200 million ringgits, with a 7yr tenor, in accordance with the wakalah programmes of an earlier announcement. The proceeds are to meet the company’s capital expenditure and business operating requirements, including high-speed broadband services that are intended to be Shariah-compliant.

Sources: GIC, Invest AD, Bloomberg, Reuters, broker reports

Page 18

Perspective

With the US Federal Reserve’s quantitative easing (QE) programme moving quietly into retreat in 2014, with it goes the great hope of investors in gold that the plunging price of the past year might be promptly reversed.

It seems as if economic growth is being recovered without propelling inflation and entailing the rapid debasement of the dollar. In fact, rising bond yields look likely to curtail any sign of overheating that might encourage optimism towards the precious metal again.

Equally, this apparent muddling through -- away from the depths of despair that threatened to overwhelm Western economies five or six years ago, which provoked policymakers to engage in drastic monetary stimulus – even removes the safe-haven factor associated with global panic.

The passage of time has not been on gold’s side, in terms of waiting for an inflationary breakout that would spark a rush for real assets; and the absence of a running yield becomes excessively costly, certainly in comparison with equity markets that have exhibited a charge instead into risk-bearing financial assets.

Institutional investors and speculators withdrew some 800 tonnes from gold-backed exchange-traded funds (ETFs) in 2013, the first yearly outflow for thirteen years, and gold dropped by its steepest amount for over thirty years, from around $1675 to $1200 per ounce.

Either side of the new year, technical support at $1180 was approached but not breached, and a modest rebound has been seen.

QE is of course not confined to the US. Europe may not be playing along, given the eurozone central bank’s non-reflationist modus operandi, but Japan has entered the arena with a vengeance.

The Japanese government’s Abenomics strategy involves a tremendous expansion of the money supply. That said, the country’s ability to overcome the debilitating effects of inured structural restraints and so sponsor dynamic growth seems distinctly limited.

Thus, the weight of accumulated debt upon both governments and households around the world continues to bear down on consumption and investment, impeding the multiplier driving aggregate demand. At the same time, oversupply of gold itself has followed the highs of past price trends.

The physical markets of India and China, meanwhile, offer mixed signals. The Indian government’s tariff on gold imports, in an attempt to pare back the current account deficit, has had an impact. In contrast, China may absorb more than 1000 tonnes of bullion this year, whether for retail jewellery purposes or state hoarding.

Sentiment overall remains loaded against gold. Apart from short-term influences that can create a localized bounce from time to time, it’s difficult to foresee the circumstances driving a long-term revival, or even an interim surge.

That’s not to say it won’t happen, since serious dangers lurk in the globalized financial system of the world economy. It just means that analysts, in the main, don’t have any very different idea for the gold price in 2014 than the kind of level it currently occupies.

Gold’s appeal tarnished by global emergence from crisis by Andrew Shouler

Page 19

Call for PaPers4th Islamic Banking and Finance Conference (IBF 2014)

23rd to 24th June 2014Venue: Lancaster University Management School

Keynote Speaker

Thorsten BeckProfessor of Banking and Finance, Cass Business School

The constraints applied by Islamic banks rendered them more resilient in the recent financial crisis compared to their con-ventional counterparts. This has attracted the attention of market participants and researchers to their liquidity buffers, leverage ratios, managerial efficiency and bespoke financial products. Islamic banking products are now offered in more than twenty countries and their expanding suite includes bonds, equity indices and insurance. The sector is estimated to exceed $1trillion in value, while growing at about 15% per annum. Among many issues still subject to debate is the purity of Islamic finance in practice, given the need to compete and to operate with customers whose expectations have been formed by conventional banking practices.EIBF centre at Aston Business School in collaboration with GOLCER Lancaster University Management School is organis-ing a conference on Islamic Banking and Finance. The conference aims to provide a forum for an exchange of views on recent developments and to identify key issues/challenges underlying the paradigm of Islamic Banking and Finance in the 21st century.

Original contributions are invited on any of the listed topics:

• Financial risk and stability • Risk Management, Accountability and auditing• Transparency, governance and corporate social responsibility • Competition• Earnings management and impression management • Microfinance and SMEs• Performance, efficiency and convergence • Behavioural finance• Mutual funds

Special IssueJournal of Economic Behaviour and Organisation (JEBO)

Ana Timberlake Best paper Research Award: £500

Co-editors for the JEBO Special IssueOmneya Abdelsalam, Aston UniversityMohammed El-Komi, American University of CairoAna-Maria Fuertes, Cass Business SchoolStergios Leventis, International Hellenic UniversityGerald Steele, Lancaster University

Scientific committeeOmneya Abdelsalam (Aston University), Nathan Berg (University of Otago), Rachel Croson (University of Texas at Dallas), Mahmoud El-Gamal (Rice University), Mohamed El-Komi, (American University Cairo), Meryem Fethi (Leicester University), Ana-Maria Fuertes (Cass Business School), Mohamed Shahid Ibrahim (Bangor University), Marwan Izzeldin (Lancaster University), Jill Johnes (Lancaster University), Stergios Leventis (In-ternational Hellenic University), Kent Mathews (Cardiff Business School), Khelifa Mazouz (Bradford Business School), Philip Molyneux (University of Bangor), Andrew Mullineux (University of Bournemouth), Steven Ongena (University of Zurich), Vasileios Pappas (Lancaster University), Mo-hamed Shaban (Leicester University), Mustapha Sheikh (Leeds University), Gerald Steele (Lancaster University), Emili Tortosa-Ausina (Jaume I University), Mike Tsionas (Lancaster University)

Conference Organisers: Dr Omneya Abdelsalam (Aston University), Dr Marwan Izzeldin (Lancaster University)

Important DatesConference Abstract Submission

Conference Full Paper Submission

Submission for JEBO Special Issue

Special Issue Publication

31st March 2014 27th April 2014 1st October 2014 October 2015

Statistics • Econometrics • ForecastingT IMB ERL A K E

For paper submissions please email Marwa Elnahass: [email protected]

Page 20

Global Forum on Islamic Finance 2014 ConferenceDevelopments and The Way Forward

March 10-12, 2014Lahore, Pakistan

Organised byDepartment of Management Sciences

COMSATS Institute of Information Technology (CIIT)http://gfif.citilahore.edu.pk/

Research TeamGerry Steele

Vasileios [email protected]

Marwa El [email protected]

Marwan IzzeldinDirector

DISCLAIMER

This report was prepared by Gulf One Lancaster Centre for Economic Research (GOLCER) and is of a general nature and is not intended to provide specific advice on any matter, nor is it intended to be comprehensive or to address the circumstances of any particular individual or entity. This material is based on current public information that we consider reliable at the time of publication, but it does not provide tailored investment advice or recommendations. It has been prepared without regard to the financial circumstances and objectives of persons and/or organisations who receive it. The GOLCER and/or its members shall not be liable for any losses or damages incurred or suffered in connection with this report including, without limitation, any direct, indirect, incidental, special, or consequential damages. The views expressed in this report do not necessarily represent the views of Gulf One or Lancaster University. Redistribution, reprinting or sale of this report without the prior consent of GOLCER is strictly forbidden.

Andrew ShoulerEditor