J10 u Return ofPrivate Foundation Treated asa Private...

41

J10 _ u Form 990-PF Department of the Treasury I n t ernal Revenue Service Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Treated as a Private Foundation Note . The foundation may be able to use a copy of thi s return to satisfy state reporting r OMB No 1545-0052 2009 For calendhr year 2009 , or tax year beginning SEP 1, 2009 , and ending AUG 18 , 2010 G Check all that apply. Initial return 0 Initial return of a former public charity ® Final return Amended return El Address chance Name cha nge Use the IRS Name of foundation A Employer identification number label. STUDENTS HOUSE, INCORPORATED Otherwise , /O NIXON PEABODY LLP ( BETHANY WOODS ) 04-2105949 print Number and street (or P O box number if is not delivered to street address) Room/suite B Telephone number (o f'' -3 S-/ o f or type . 100 SUMMER STREET 6 4-7-24-2-49" See Specific City or town, state, and ZIP code C If exemption application is pending , check here Instructions . OSTON MA 02110 D 1 - Forei gn or g anizations, check here H Check type of organization: ®Section 501(c)(3) exempt private foundation 2' Foreign attach computa on 5% test, 0 Section 4947 ( a )( 1 ) nonexem p t charitable trust 0 Other taxable p rivate foundation rivate foundation status was terminated E If I Fair market value of all assets at end of year J Accounting method: 0 Cash 0 Accrual p under section 507(b)(1)(A), check here (from Part II, col. (c), line 16) ® Other (specify) MODIFIED ACCRUAL F If the foundation is in a 60-month termination 1114 0 . (Part I, column (d) must be on cash basis) under section 507 ( b )( 1 ) B check here llimE] Part I Analysis of Revenue and Expenses (a) Revenue and (b ) Net investment (c) Adjusted net (d) Disbursements (The total of amounts in columns (b), (c), and (d) may not necessarily equal the amounts in column (a)) expenses per books income income for charitable purposes (cash basis only) 1 Contributions, gifts, grants, etc., received N / A 2 dthetuundabofl is not required to attach Sch B Interest on savings and temporary 3 cash investments 4 , 260 . 4 , 260 . S TATEMENT 1 4 Dividends and interest from securities 35 , 926. 35 , 926. S TATEMENT 2 5a Gross rents b Net rental income or Qoss) 6a Net gain or (loss) from sale of assets not on line 10 861 , 629 . Gross sales price for all b assets on brie Ba 1,329,713. ------^ d Capital gain net income (from Part IV, line 2) 7 14 616 29 - 4' 1 8 Net short-term capital gain r----"'" 9 Income modifications I o Gross sales less returns 10a and allowances `J L r' 1(J 8 0)1V b Less Cost of goods sold ILI c Gross profit or (loss) 11 Other income 12 Total. Add lines 1 throu g h 11 901 , 815 . 901 , 815. 13 Compensation of officers, directors, trustees, etc 0. 0. 0. 14 Other employee salaries and wages 15 Pension plans, employee benefits 0 16a Legal fees STMT 3 10 , 676. 0. 0. b Accounting fees STMT 4 6 , 140. 0. 6 , 140. CL W c Other professional fees STMT 5 13 , 465. 11 , 865. 1 , 600. > 17 Interest 18 Taxes STMT 6 10 , 545. 229. 0. 19 Depreciation and depletion E 20 Occupancy v < 21 Travel, conferences, and meetings r- 22 Printing and publications 0 23 Other expenses STMT 7 1 0 7 0. 0. 70. 24 Total operating and administrative a expenses . Add lines 13 through 23 41 , 896. 12 , 094. 7 , 810. 0 25 Contributions, gifts, grants paid 1 , 545 , 642. 1 , 545 , 642. 26 Total expenses and disbursements. Add lines 24 and 25 1 , 587 , 538. 12 , 094. 1 , 553 , 452. 27 Subtract line 26 from line 12: a Excess of revenue over expenses and disbursements -685 1 723. 1 b Net investment income (if negative, enter -0-) 889 , 721. c Adjusted net income (if negative, enter-0-) N / A V 3 rr C M 6k c oz-0z-11o LHA For Privacy Act and Paperwork Reduction Act Notice , see the instructions . Form 990-PF (2009) 1 (!^ 10290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001 Z

-

Upload

phungkhanh -

Category

Documents

-

view

215 -

download

2

Transcript of J10 u Return ofPrivate Foundation Treated asa Private...

J10 _ u

Form 990-PF

Department of the Treasury

I n t ernal Revenue Service

Return of Private Foundationor Section 4947(a)(1) Nonexempt Charitable Trust

Treated as a Private FoundationNote . The foundation may be able to use a copy of thi s return to satisfy state reporting r

OMB No 1545-0052

2009For calendhr year 2009 , or tax year beginning SEP 1, 2009 , and ending AUG 18 , 2010

G Check all that apply. Initial return 0 Initial return of a former public charity ® Final return

Amended return El Address chance Name change

Use the IRS Name of foundation A Employer identification number

label. STUDENTS HOUSE, INCORPORATEDOtherwise , /O NIXON PEABODY LLP ( BETHANY WOODS ) 04-2105949

print Number and street (or P O box number if is not delivered to street address) Room/suite B Telephone number (o f'' -3 S-/ of

or type . 100 SUMMER STREET 6 4-7-24-2-49"See Specific

City or town, state, and ZIP code C If exemption application is pending , check hereInstructions .

OSTON MA 02110 D 1 - Forei gn or g anizations, check here

H Check type of organization: ®Section 501(c)(3) exempt private foundation 2'Foreign

attach computaii

on5%test,

0 Section 4947 ( a )( 1 ) nonexem p t charitable trust 0 Other taxable p rivate foundation rivate foundation status was terminatedE IfI Fair market value of all assets at end of year J Accounting method: 0 Cash 0 Accrual

punder section 507(b)(1)(A), check here

(from Part II, col. (c), line 16) ® Other (specify) MODIFIED ACCRUAL F If the foundation is in a 60-month termination

1114 0 . (Part I, column (d) must be on cash basis) under section 507( b )( 1 ) B check here llimE]Part I Analysis of Revenue and Expenses (a) Revenue and (b ) Net investment (c) Adjusted net (d) Disbursements

(The total of amounts in columns (b), (c), and (d) may notnecessarily equal the amounts in column (a)) expenses per books income income for charitable purposes

(cash basis only)

1 Contributions, gifts, grants, etc., received N /A2 dthetuundabofl is not required to attach Sch B

Interest on savings and temporary3 cash investments 4 , 260 . 4 , 260 . STATEMENT 1

4 Dividends and interest from securities 35 , 926. 35 , 926. STATEMENT 25a Gross rents

b Net rental income or Qoss)

6a Net gain or (loss) from sale of assets not on line 10 861 , 629 .Gross sales price for all

b assets on brie Ba 1,329,713. ------^d Capital gain net income (from Part IV, line 2)7 14616 29 - 4' 1

8 Net short-term capital gain r----"'"

9 Income modifications I oGross sales less returns

10a and allowances`J L r' 1(J 8 0)1V

b Less Cost of goods sold ILI

c Gross profit or (loss)

11 Other income

12 Total. Add lines 1 throu g h 11 901 , 815 . 901 , 815.13 Compensation of officers, directors , trustees, etc 0. 0. 0.

14 Other employee salaries and wages

15 Pension plans, employee benefits

0 16a Legal fees STMT 3 10 , 676. 0. 0.b Accounting fees STMT 4 6 , 140. 0. 6 , 140.

CLW c Other professional fees STMT 5 13 , 465. 11 , 865. 1 , 600.> 17 Interest

18 Taxes STMT 6 10 , 545. 229. 0.19 Depreciation and depletion

E 20 Occupancyv< 21 Travel, conferences, and meetings

r- 22 Printing and publications

0 23 Other expenses STMT 7 1 0 7 0. 0. 70.24 Total operating and administrative

a expenses . Add lines 13 through 23 41 , 896. 12 , 094. 7 , 810.0 25 Contributions, gifts, grants paid 1 , 545 , 642. 1 , 545 , 642.

26 Total expenses and disbursements.

Add lines 24 and 25 1 , 587 , 538. 12 , 094. 1 , 553 , 452.27 Subtract line 26 from line 12:

a Excess of revenue over expenses and disbursements -685 1 723. 1

b Net investment income (if negative, enter -0-) 889 , 721.

c Adjusted net income (if negative, enter-0-) N/A

V

3

rr

C

M

6k

c

oz-0z-11o LHA For Privacy Act and Paperwork Reduction Act Notice , see the instructions . Form 990-PF (2009)

1 (!^

10290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001 Z

STUDENTS HOUSE, INCORPORATEDForm 990-PF (2009) r 1n NTXl1N PRARf1W T.T.P (RF'PTTANV W()nG 1 (1 d- 21 (1 S 4 d q Pane 2

onBalance Sheetsedsche anda ountsinthed eon

Beginning of year End of yearPartll c m dbe s1 for end -of-year

y (a) Book Value (b) Book Value (c) Fair Market Value

I Cash - non-interest-bearing

2 Savings and temporary cash investments 216 , 087.

3 Accounts receivable ►Less: allowance for doubtful accounts ►

4 Pledges receivable ►Less: allowance for doubtful accounts ►

5 Grants receivable

6 Receivables due from officers, directors, trustees, and other

disqualified persons

7 Other notes and loans receivable ►

Less: allowance for doubtful accounts ►8 Inventories for sale or use

9 Prepaid expenses and deferred charges

10a Investments - U.S. and state government obligations 99 , 883.b Investments - corporate stock 268 , 128.c Investments - corporate bonds _ 99 , 965.

11 Investments - land,buddinps , and equipment basis ►

Less accumulated depreciation ►

12 Investments - mortgage loans

13 Investments - other

14 Land, buildings, and equipment basis ►Less accumulated depreciation ►

15 Other assets (describe ► ) 1 , 660. 0. 0.

16 Total assets ( to be com p leted b y all filers ) 685 , 723. 0. 0.17 Accounts payable and accrued expenses

18 Grants payable

ca 19 Deferred revenue

- 20 Loans from officers, directors, trustees, and other disqualified persons

21 Mortgages and other notes payable

22 Other liabilities (describe ►

23 Total liabilities ( add lines 17 throu g h 22 ) 0. 0.

Foundations that follow SFAS 117, check here ►and complete lines 24 through 26 and lines 30 and 31.

24 Unrestricted

0 25 Temporarily restricted

co 26 Permanently restricted

Foundations that do not follow SFAS 117, check here ►it`l and complete lines 27 through 31.

y 27 Capital stock, trust principal, or current funds 0. 0.

IUD) 28 Paid-in or capital surplus, or land, bldg., and equipment fund 0. 0.U)

29 Retained earnings, accumulated income, endowment, or other funds 685 , 723. 0.

01Z 30 Total net assets or fund balances 685 , 723. 0. 1

31 Total liabilities and net assets/fund balances 685 , 723. 0. 1

Part III Analysis of Changes in Net Assets or Fund Balances

1 Total net assets or fund balances at beginning of year - Part II, column (a), line 30

(must agree with end-of-year figure reported on prior year's return) _

2 Enter amount from Part I, line 27a

3 Other increases not included in line 2 (itemize) ►4 Add lines 1, 2, and 3

5 Decreases not included in line 2 (itemize) ►

92351102-02-10

685,723.

0.

Form 990-PF (2009)

210290820 758606 70772000 2009.04011 STUDENTS HOUSE , INCORPORATE 70772001

STUDENTS HOUSE, INCORPORATEDForm 990-PF (2009) C O NIXON PEABODY LLP ( BETHANY WOODS ) 04-2105949 Page 3Part IV Capital Gains and Losses for Tax on Investment Income

.(a) List and describe the kind(s) of property sold (e.g., real estate,2-story brick warehouse; or common stock, 200 shs. MLC Co.

(b How acquiredPurchase

D Donation

(c Date acquired(lino., day, yr.)

(d) Date sold(mo., day, yr.)

la 4

b SEE ATTACHED STATEMENTSCd

e

(e) Gross sales price (f) Depreciation allowed(or allowable)

(g) Cost or other basisplus expense of sale

(h) Gain or (loss)(e) plus (f) minus (g)

a

b

c

d

1e 1 , 329 , 713. 468 084. 861 629.Complete only for assets showin g gain in column (h) and owned by the foundati on on 12/31/69 (I) Gains (Col. (h) gain minus

(i) F.M.V. as of 12/31/69(j) Adjusted basisas of 12/31/69

(k) Excess of col. (i)over col. (I), if any

col. (k), but not less than -0-) orLosses (from col. (h))

a

b

c

d

e 861 629.

2 Capital gain net income or (net capital loss)If gain, also enter in Part I, line 7If (loss), enter -0- in Part I, line 7 2 861 , 629.

3 Net short-term capital gain or (loss) as defined in sections 1222(5) and (6):If gain, also enter in Part I, line 8, column (c).If loss enter -0- in Part I line 8 3 N /A

Part V I Qualification Under Section 4940(e) for Reduced Tax on Net Investment Income

(For optional use by domestic private foundations subject to the section 4940(a) tax on net investment income.)

If section 4940(d)(2) applies, leave this part blank.

Was the foundation liable for the section 4942 tax on the distributable amount of any year in the base period? 0 Yes ® No

If 'Yes,' the foundation does not qualify under section 4940 (e). Do not complete this part

1 Enter the appropriate amount in each column for each year see instructions before making any entries.

Base period yearsCalendar year ( or tax year beginning m (bAdjusted qualifying distributions

MNet value of noncharitable-use assets

Distribution ratio(col. (b) divided by col. (c))

2008 82 , 735. 1 , 688 , 362. .0490032007 112 232. 1 , 768 , 984. .0634442006 112 491. 1 , 791 , 869. .0627792005 112 403. 1 , 759 , 000. .0639022004 112 846. 1 , 804 , 445. .062538

2 Total of line 1, column (d) 2 .301666

3 Average distribution ratio for the 5-year base period - divide the total on line 2 by 5,

the foundation has been in existence if less than 5 years

or by the number of years

3 . 0 6 0 3 3 3

4 Enter the net value of noncharitable-use assets for 2009 from Part X, line 5 4 1 , 774 , 609.

5 Multiply line 4 by line 3 5 107 , 067.

6 Enter 1% of net investment income (1% of Part I, line 27b) 6 8 , 897.

7 Add lines 5 and 6 7 115 , 964.

8 Enter qualifying distributions from Part XII, line 4 8 1 553 , 452.If line 8 is equal to or greater than line 7, check the box in Part VI , line 1b, and complete that part using a 1% tax rate.See the Part VI instructions.

923521 02-02-10 Form 990-PF (2009)3

10290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS HOUSE, INCORPORATEDForm 990-PF (2009) C / O NIXON PEABODY LLP ( BETHANY WOODS ) 04-2105949 Page 4Part VI Excise Tax Based on Investment Income (Section 4940(a). 4940(b). 4940(e). or 4948 - see instructions)

la Exempt operating foundations described in section 4940(d)(2), check here ►U and enter'WA' on line 1.

Date of ruling or determination letter. ( attach copy of letter if necessary-see instructions)

b Domestic foundations that meet the section 4940(e) requirements in Part V, check here ►® and enter 1%

of Part I, line 27b

c All other domestic foundations enter 2% of line 27b. Exempt foreign organizations enter 4% of Part I, line 12, col. (b)

2 Tax under section 511 (domestic section 4947(a)(1) trusts and taxable foundations only. Others enter -0-) 2

3 Add lines 1 and 2 3

4 Subtitle A (income) tax (domestic section 4947(a)(1) trusts and taxable foundations only. Others enter -0-) 4

5 Tax based on investment income . Subtract line 4 from line 3. If zero or less, enter -0- 5

6 Credits/Payments:

a 2009 estimated tax payments and 2008 overpayment credited to 2009 6a 8 , 899.

b Exempt foreign organizations - tax withheld at source 6b

c Tax paid with application for extension of time to file (Form 8868) 6c

d Backup withholding erroneously withheld 6d

7 Total credits and payments. Add lines 6a through 6d 7

8 Enter any penalty for underpayment of estimated tax Check here ® if Form 2220 is attached 8

9 Tax due . If the total of lines 5 and 8 is more than line 7, enter amount owed ► 9

10 Overpayment . If line 7 is more than the total of lines 5 and 8, enter the amount overpaid ► 10

11 Enter the amount of line 10 to be: Credited to 2010 estimated tax 11110, 0 . Refunded 11Part VII-A Statements Regarding Activities

la During the tax year, did the foundation attempt to influence any national, state, or local legislation or did it participate or intervene in

any political campaign?

b Did it spend more than $100 during the year (either directly or indirectly) for political purposes (see instructions for definition)?

If the answer is "Yes" to j a or ib attach a detailed description of the activities and copies of any materials published or

distributed by the foundation in connection with the activities.

c Did the foundation file Form 1120-POL for this year?

d Enter the amount (if any) of tax on political expenditures (section 4955) imposed during the year:

(1) On the foundation. ► $ 0. (2) On foundation managers. ► $ 0.

e Enter the reimbursement (if any) paid by the foundation during the year for political expenditure tax imposed on foundation

managers. ► $ 0.

2 Has the foundation engaged in any activities that have not previously been reported to the IRS?

If "Yes," attach a detailed description of the activities.

3 Has the foundation made any changes, not previously reported to the IRS, in its governing instrument, articles of incorporation, or

bylaws, or other similar instruments? If "Yes," attach a conformed copy of the changes

4a Did the foundation have unrelated business gross income of $1,000 or more during the year

b If 'Yes, has it filed a tax return on Form 990-T for this year? N/A

5 Was there a liquidation, termination, dissolution, or substantial contraction during the year?

If 'Yes,' attach the statement required by General Instruction T.

6 Are the requirements of section 508(e) (relating to sections 4941 through 4945) satisfied either:

• By language in the governing instrument, or

• By state legislation that effectively amends the governing instrument so that no mandatory directions that conflict with the state law

remain in the governing instrument?

7 Did the foundation have at least $5,000 in assets at any time during the year?

If 'Yes,' complete Part II, col. (c), and Part XV.

8a Enter the states to which the foundation reports or with which it is registered (see instructions) ►MA

b If the answer is 'Yes' to line 7, has the foundation furnished a copy of Form 990-PF to the Attorney General (or designate)

of each state as required by General Instruction G' If 'No," attach explanation

9 Is the foundation claiming status as a private operating foundation within the meaning of section 4942(j)(3) or 4942(I)(5) for calendar

year 2009 or the taxable year beginning in 2009 (see instructions for Part XIV)? If 'Yes,' complete Part XIV

10 Did any persons become substantial contributors during the tax year? lf "ves.• attach a schedule listina their names and addresses

8.897.

8.897.

7.

2.0.

0.

Yes No

la X

1b X

1c X

2 X

3 X

4a X

4b

5 X

6 X7 X

91 IX

Form 990-PF (2009)

92353102-02-10

410290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS HOUSE, INCORPORATEDForm 990-PF (2009) C/O NIXON PEABODY LLP (BETHA

1c

Part VII-A Statements Regarding Activities (continued)

11 At any time during the year, did the foundation, directly or indirectly, own a controlled entity within the meaning of

section 512(b)(13)? If 'Yes, attach schedule (see instructions)

12 Did the foundation acquire a director indirect interest in any applicable insurance contract before

August 17 , 2008? 12 X

13 Did the foundation comply with the public inspection requirements for its annual returns and exemption application? 13 X

Website address ► N/A

14 The books are in care of ► NIXON PEABODY LLP Telephone no. ► 617 - 3 4 5 -1-3-7-6Located at ► 10 0 SUMMER STREET , BOSTON , MA ZIP+4 ►0 2110

15 Section 4947 ( a)(1) nonexempt charitable trusts filing Form 990-PF in lieu of Form 1041 - Check here ►0and enter the amount of tax-exempt interest received or accrued durinn the year ► I 15 I N / A

Part VII-B Statements Regarding Activities for Which Form 4720 May Be RequiredFile Form 4720 if any item is checked in the "Yes" column, unless an exception applies. Yes No

la During the year did the foundation (either directly or indirectly):

(1) Engage in the sale or exchange, or leasing of property with a disqualified person? Yes ® No

(2) Borrow money from, lend money to, or otherwise extend credit to (or accept it from)

a disqualified person? Yes ® No

(3) Furnish goods, services, or facilities to (or accept them from) a disqualified person? Yes ® No

(4) Pay compensation to, or pay or reimburse the expenses of, a disqualified person? 0 Yes ® No

(5) Transfer any income or assets to a disqualified person (or make any of either available

for the benefit or use of a disqualified person)? 0 Yes ® No

(6) Agree to pay money or property to a government official? ( Exception . Check "No'

if the foundation agreed to make a grant to or to employ the official for a period after

termination of government service, if terminating within 90 days. ) =Yes ®No

b If any answer is 'Yes'to la ( 1)-(6), did any of the acts fail to qualify under the exceptions described in Regulations

section 53 .4941(d )-3 or in a current notice regarding disaster assistance (see page 20 of the instructions)? N/A

Organizations relying on a current notice regarding disaster assistance check here ►c Did the foundation engage in a prior year in any of the acts described in la, other than excepted acts, that were not corrected

before the first day of the tax year beginning in 2009?

Taxes on failure to distribute income ( section 4942 ) ( does not apply for years the foundation was a private operating foundation

defined in section 4942 (l )(3) or 4942 ( j)(5)):

a At the end of tax year 2009, did the foundation have any undistributed income (lines 6d and 6e, Part XIII) for tax year(s) beginning

before 2009? 0 Yes ® No

It 'Yes,' list the years ►b Are there any years listed in 2a for which the foundation is not applying the provisions of section 4942(a)(2) (relating to incorrect

valuation of assets) to the year's undistributed income? (If applying section 4942(a)(2) to all years listed, answer 'No' and attach

statement - see instructions.) N/A

c If the provisions of section 4942(a)(2) are being applied to any of the years listed in 2a, list the years here.

3a Did the foundation hold more than a 2% direct or indirect interest in any business enterprise at any time

during the year? El Yes ® No

b If 'Yes,' did it have excess business holdings in 2009 as a result of (1) any purchase by the foundation or disqualified persons after

May 26 , 1969; (2) the lapse of the 5-year period ( or longer period approved by the Commissioner under section 4943( c)(7)) to dispose

of holdings acquired by gift or bequest; or (3) the lapse of the 10 -, 15-, or 20 -year first phase holding period? (Use Schedule C,

Form 4720, to determine if the foundation had excess business holdings in 2009) N/A

4a Did the foundation invest during the year any amount in a manner that would jeopardize its charitable purposes?

b Did the foundation make any investment in a prior year ( but after December 31, 1969) that could jeopardize its charitable purpose that

had not been removed from ieooardv before the first day of the tax year beamnina in 2009?

92354102-02-10

Page 5

X

X

I4b 1 I XForm 990-PF (2009)

510290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS HOUSE, INCORPORATEDrorm aau-Ft[uu i %- / U tv IAVty rariD jj z LILJr aa-i tnsii'i i wvvLa V' - L i U J 7 % 7 ra e oPart VII-B Statements Regarding Activities for Which Form 4720 May Be Required (continued)

5a During the year did the foundation pay or incur any amount to:

(1) Carry on• propaganda, or otherwise attempt to influence legislation ( section 4945(e))? Yes ® No

(2) Influence the outcome of any specific public election (see section 4955 ); or to carry on , directly or indirectly,

ahy voter registration drive? E]Yes ® No

(3) Provide a grant to an individual for travel , study, or other similar purposes? Yes ® No

(4) Provide a grant to an organization other than a charitable, etc., organization described in section

509(a )( 1), (2), or (3 ), or section 4940(d)(2)7 El Yes ® No

(5) Provide for any purpose other than religious, charitable , scientific , literary , or educational purposes, or for

the prevention of cruelty to children or animals? 0 Yes ® No

b If any answer is 'Yes' to 5a(1)-(5), did any of the transactions fail to qualify under the exceptions described in Regulations

section 53.4945 or in a current notice regarding disaster assistance ( see instructions ) ? N/A 5b

Organizations relying on a current notice regarding disaster assistance check here ►c If the answer is 'Yes' to question 5a(4), does the foundation claim exemption from the tax because it maintained

expenditure responsibility for the grant? N/A 0 Yes 0 No

If "Yes," attach the statement required by Regulations section 53. 4945-5(d).

6a Did the foundation , during the year, receive any funds, directly or indirectly, to pay premiums on

a personal benefit contract? 0 Yes ® No

b Did the foundation , during the year, pay premiums , directly or indirectly , on a personal benefit contract? 6b X

If "Yes" to 6b, file Fomi 8870.

7a At any time during the tax year, was the foundation a party to a prohibited tax shelter transactions 0 Yes ® No

b If yes, did the foundation receive any proceeds or have any net income attributable to the transactions N/A 7b

Part VIIIInformation About Officers, Directors , Trustees, Foundation Managers, Highly

a Paid Employees , and Contractors1 List all officers_ directors. trustees. foundation manaaers and their comoensation.

a) Name and address(b) Title, and average

hours p er week devotedto position

(c) Compensation

(If not p aidenter-0

(d ) Contnbubons tobenefit pla nsAlanddeferred

combn

(e)Expenseaccounotherallowances

SEE STATEMENT 9 0. 0. 0.

2 Compensation of five hiahest-naid emolovees (other than those included on line 11. If none. enter "NONE."

(a) Name and address of each employee paid more than $50,000(b) Title, and average

hours per weekdevoted to position

(c) Compensation(d) Contnbubonsto

benefit

s

eterne plansempandpencomation

(e)Expenseaccounotherallowances

NONE

Total number of other employees paid over $50,000 ► 1 0Form 990-PF (2009)

92355102-02-10

610290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS HOUSE, INCORPORATEDForm 990-PF (2009) C/O NIXON PEABODY LLP (BETHANY WOODS) 04-2105949 Page 7

Part VIII Information About Officers , Directors , Trustees , Foundation Managers , HighlyPaid Employees , and Contractors (continued)

3 Five highest-paid independent contractors for professional services. If none, enter "NONE."

(a) Name and address of each person paid more than $50,000 (b) Type of service (c) Compensation

NONE

Total number of others receivin g over $50 ,000 for p rofessional services ► 0Part IX-A Summary of Direct Charitable Activities

List the foundation's four largest direct charitable activities during the tax year. Include relevant statistical information such as thenumber of organizations and other beneficiaries served, conferences convened, research papers produced, etc. Expenses

1 N /A

2

3

4

Part IX-B Summary of Program -Related InvestmentsDescribe the two largest program-related investments made by the foundation during the tax year on lines 1 and 2. Amount

1 N/A

2

All other program-related investments. See instructions.

3

Total. Add lines 1 through 3 ► 0.

Form 990-PF (2009)

92356102-02-10

7

10290820 758606 70772000 2009.04011 STUDENTS HOUSE , INCORPORATE 70772001

STUDENTS HOUSE, INCORPORATEDForm 990-PF (2009) C/O NIXON PEABODY LLP (BETHANY WOODS) 04-2105949 Page 8

Part X Minimum Investment Return (All domestic foundations must complete this part . Foreign foundations, see instructions.)

1 Fair market value of assets not used ( or held for use ) directly in carrying out charitable, etc., purposes:

a Averagb monthly fair market value of securities 1 a 1 , 557 , 923b Average of monthly cash balances 1 b 241 , 800c Fair market value of all other assets 1c 1 911.d Total (add lines la, b, and c) 1 d 1 801 634.e Reduction claimed for blockage or other factors reported on lines la and

1c (attach detailed explanation) le 0.

2 Acquisition indebtedness applicable to line 1 assets 2 0 .

3 Subtract line 2 from line 1d 3 1 , 801 , 634 .4 Cash deemed held for charitable activities. Enter 1 1/2% of line 3 (for greater amount, see instructions ) 4 27 , 025 .

5 Net value of noncharitable - use assets Subtract line 4 from line 3. Enter here and on Part V, line 4 5 1 , 774 , 609 .6 Minimum investment return . Enter 5% of line 5 ADJUSTED FOR SHORT TAX PERIOD 6 85 , 570.

Part XIDistributable Amount (see instructions) (Section 4942( l)(3) and ( 1)(5) private operating foundatiforeign organizations check here ► Eland do not complete this part)

ons and certain

1 Minimum investment return from Part X, line 6 1 85 , 570.2a

b

c

Tax on investment income for 2009 from Part VI, line 5 2a

Income tax for 2009. (This does not include the tax from Part VI.) 2b

Add lines 2a and 2b

8 , 897.

2c 8 , 897.3 Distributable amount before adjustments. Subtract line 2c from line 1 3 76 , 673 .4 Recoveries of amounts treated as qualifying distributions 4 0 .

5 Add lines 3 and 4 5 76 , 673 .6 Deduction from distributable amount (see instructions) 6 0 .

7 Distributable amount as ad j usted. Subtract line 6 from line 5. Enter here and on Part XIII , line 1 7 76 , 673 .

Part XII Qualifying Distributions (see instructions)

1

a

Amounts paid (including administrative expenses) to accomplish charitable, etc., purposes:

Expenses, contributions, gifts, etc. - total from Part I, column (d), line 26 la 1 , 553 , 452.b Program-related investments - total from Part IX-B lb 0.

2 Amounts paid to acquire assets used (or held for use) directly in carrying out charitable, etc., purposes 2

3

a

Amounts set aside for specific charitable projects that satisfy the:

Suitability test (prior IRS approval required) 3a

b Cash distribution test (attach the required schedule) 3b

4 Qualifying distributions . Add lines la through 3b. Enter here and on Part V, line 8, and Part XIII, line 4 4 1 , 553 , 4525 Foundations that qualify under section 4940(e) for the reduced rate of tax on net investment

income. Enter 1% of Part I, line 27b 5 8 , 897.6 Adjusted qualifying distributions . Subtract line 5 from line 4 6 1 , 544 , 555.

Note The amount on line 6 will be used in Part V, column (b), in subsequent years when calculating whether the foundation q4940(e) reduction of tax in those years.

ualifie s for the section

Form 990-PF (2009)

92357102-02-10

810290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS HOUSE, INCORPORATEDForm 990-PF (2009) C/O NIXON PEABODY LLP (BETHANY WOODS) 04-2105949 Page 9

Part XIII Undistributed Income (see instructions)

(a) (b) (c) (d)Corpus Years prior to 2008 2008 2009

1 Distributable amount for 2009 from Part XI,

line? 76 , 673.2 Undistributed income, if any, as of the end of 2009

a Enter amount for 2008 only 0.

b Total for prior years:

0.3 Excess distributions carryover, if any, to 2009:

a From 2004 23 , 378.bFrom2005 25 , 207.c From 2006 23 , 726.d From 2007 24 , 589.e From 2008 174.

f Total of lines 3a throug h a 97 , 074.

4 Qualifying distributions for 2009 from

Part Xl 1, line 4: 1 , 553 , 452.a Applied to 2008, but not more than line 2a 0.

b Applied to undistributed income of prior

years (Election required - see instructions) 0.

c Treated as distributions out of corpus

(Election required - see instructions) 0.

d Applied to 2009 distributable amount 76 , 673.

e Remaining amount distributed out of corpus 1 , 476 , 779.5 Excess distributions carryover applied to 2009 0. 0.

Of an amount appears in column (d), the same amount

must be shown in column (a) )

6 Enter the net total of each column asindicated below:

a Corpus Add lines 3f, 4c, and 4e Subtract line 5 1 , 573 , 853.b Prior years' undistributed income. Subtract

line 4b from line 2b 0.

c Enter the amount of prior years'undistributed income for which a notice ofdeficiency has been issued, or on whichthe section 4942(a) tax has been previouslyassessed 0

d Subtract line 6c from line 6b. Taxable

amount - see instructions 0e Undistributed income for 2008. Subtract line

4a from line 2a. Taxable amount - see instr. 0

f Undistributed income for 2009. Subtract

lines 4d and 5 from line 1. This amount must

be distributed in 2010 0

7 Amounts treated as distributions out of

corpus to satisfy requirements imposed by

section 170(b)(1)(F) or 4942(g)(3) 0

8 Excess distributions carryover from 2004

not applied on line 5 or line 7 23 , 378.9 Excess distributions carryover to 2010.

Subtract lines 7 and 8 from line 6a 1 , 550 , 475.10 Analysis of line 9:

a Excess from 2005 25 , 207.b Excess from 2006 23 , 72 6.

c Excess from 2007 24 , 589 .

d Excess from 2008 174 .

e Excess from 2009 1 4 7 6 779 .

Form 990-PF (2009)92358102-02-10

910290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS HOUSE, INCORPORATEDForm 990-PF 2009 C / O NIXON PEABODY LLP ( BETHANY WOODS ) 04-2105 949 Page 10

Part XIV Private Operating Foundations (see instructions and Part VII-A, question 9) N/A

1 a If the foundation has received a ruling or determination letter that it is a private operating

foundation, and the ruling is effective for 2009 , enter the date of the ruling ►b Check box to indicate whether the foundation is a p rivate o eratm foundation described in section 0 4942 (j)( 3 ) or 0 4942 (j)( 5 )

2 a Enter the lesser of the adjusted net Tax year Prior 3 years

income from Part I or the minimum (a) 2009 ( b) 2008 (c) 2007 (d) 2006 (e) Total

investment return from Part X for

each year listed

b 85% of line 2a

c Qualifying distributions from Part XII,

line 4 for each year listed

d Amounts included in line 2c not

used directly for active conduct of

exempt activities

e Qualifying distributions made directly

for active conduct of exempt activities.

Subtract line 2d from line 2cComplete 3a, b, or c for thealternative test relied upon:

a 'Assets' alternative test - enter:(1) Value of all assets

(2) Value of assets qualifyingunder section 4942(I)(3)(B)(i)

b 'Endowment' alternative test - enter2/3 of minimum investment returnshown in Part X, line 6 for each yearlisted

c 'Support' lternative test - enter:

(1) Total support other than grossinvestment income (interest,dividends, rents, payments onsecurities loans (section512(a)(5)), or royalties)

(2) Support from general publicand 5 or more exemptorganizations as provided insection 4942(t)(3)(B)(ui)

(3) Largest amount of support from

an exempt organization

Part XV Supplementary Information (Complete this part only if the foundation had $5,000 or more in assetsat any time during the year-see the instructions.)

1 Information Regarding Foundation Managers:

a List any managers of the foundation who have contributed more than 2% of the total contributions received by the foundation before the close of any taxyear (but only if they have contributed more than $5,000). (See section 507(d)(2).)

NONE

b List any managers of the foundation who own 10% or more of the stock of a corporation (or an equally large portion of the ownership of a partnership orother entity) of which the foundation has a 10% or greater interest

NONE

2 Information Regarding Contribution , Grant, Gift, Loan , Scholarship , etc., Programs:Check here ►® if the foundation only makes contributions to preselected charitable organizations and does not accept unsolicited requests for funds. Ifthe foundation makes gifts, grants, etc. (see instructions) to individuals or organizations under other conditions, complete items 2a, b, c, and d.

a The name, address, and telephone number of the person to whom applications should be addressed:

b The form in which applications should be submitted and information and materials they should include:

c Any submission deadlines:

d Any restrictions or limitations on awards, such as by geographical areas, charitable fields, kinds of institutions, or other factors:

923601 02 -02-10 Form 990-PF (2009)10

10290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS HOUSE, INCORPORATEDForm 990-PF (2009) C / O NIXON PEABODY LLP ( BETHANY WOODS ) 04-2105949 Page 11Part XV Supplementary Information (continued)

3 Grants and Contributions Paid During the Year or Approved for Future Payment

Recipient If recipient is an individual,show any relationship to Foundation Purpose of grant or

Name and address (home or business) any foundation manageror substantial contributor

status ofrecipient

contribution Amount

a Paid dung the year

NEW ENGLAND CONSERVATORY ONE COLLEGE CONTRIBUTION 772,821.OF MUSIC290 HUNTINGTON AVEBOSTON, MA 02115

SCHOOL OF THE MUSEUM OF ONE SCHOOL CONTRIBUTION 772,821.FINE ARTS230 THE FENWAY BOSTON,MA 02115

Total ► 3a 1545642.b Approved for future payment

NONE

► 3b 1 0923611 02-02-10 Form 990-PF (2009)

1110290820 758606 70772000 2009.04011 STUDENTS HOUSE , INCORPORATE 70772001

STUDENTS HOUSE, INCORPORATEDForm 990-PF (2009) C/O NIXON PEABODY LLP (BETHANY WOODS) 04-210594 9 Page 12

Part XVI-A Analysis of Income-Producing Activities

Enter I

1 Pro

a

b

c

d

e

f

9

2 Me

3 Int

inv

4 Div

5 Net

a

b

6 Net

pro

7 0th

8 Gal

tha

9 Net

10 Gr

11 Ot

a

b

c

d

e

12 Su

13 Total . Add line 12, columns (b), (d), and (e) 13 901,815.

(See worksheet in line 13 instructions to verify calculations.)

Part XVI-B Relationship of Activities to the Accomplishment of Exempt Purposes

boss amounts unless otherwise indicated Unrelate d business income Exclu ded by section 512, 513, or 514 (e).

gram service revenue:

(a)Businesscode

(b)Amount

Exc „̂_5codede

(d)Amount

Related or exempt

function income

Fees and contracts from government agencies

mbership dues and assessments

rest on savings and temporary cashestments 14 4 , 260.idends and interest from securities 14 35 , 926.rental income or (loss) from real estate:

Debt-financed property

Not debt-financed property

rental income or (loss) from personal

perty

er investment income

n or (loss) from sales of assets other

n inventory 18 861 , 629.income or (loss) from special events

ss profit or (loss) from sales of inventory

er revenue:

)total. Add columns (b) , (d), and (e) 0 . 9 01 815.

B

a

h

0 .

1210290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

92362102-02-10 Form 990-PF (2009)

STUDENTS HOUSE, INCORPORATEDForm 990-PF 2009 C / O NIXON PEABODY LLP ( BETHANY WOODS ) 04-2105949 Pag e 13Part XVII Information Regarding Transfers To and Transactions and Relationships With Noncharitable

Exempt Organizations

Did the organization directly or indirectly engage in any of the following with any other organization described in section 501(c) of Yes No

the Cdde (other than section 501(c)(3) organizations) or in section 527, relating to political orgamzations7

a Transfers from the reporting foundation to a nonchantable exempt organization of

(1) Cash la ( l ) X

(2) Other assets ia ( 2 ) X

b Other transactions:

(1) Sales of assets to a noncharitable exempt organization 1b 1 X

(2) Purchases of assets from a noncharitable exempt organization lb ( 2 )1 X

(3) Rental of facilities, equipment, or other assets lb ( 3 ) X

(4) Reimbursement arrangements _ lb(4) X

(5) Loans or loan guarantees lb ( 5 ) X

(6) Performance of services or membership or fundraising solicitations lb ( 6 ) X

Sharing of facilities, equipment, mailing lists, other assets, or paid employees 1c X

If the answer to any of the above is 'Yes, complete the following schedule. Column (b) should always show the fair market value of the goods, other assets

or services given by the reporting foundation. If the foundation received less than fair market value in any transaction or sharing arrangement, show in

(a) Name of organization (b) Type of organization (c) Description of relationship

N/A

Under penalties of perjury, I declare that I have examined this return , including accompanying schedules and statements , and to the best of my knowledge and belief, it is true, correct,

and complete ecla ation of preparer (other than taxpayer or fiduciary ) is based on all information of which preparer has any knowledge

ignature of o er or trustee p

= Preparer's

N E signature' JASON GOLOBOYma Rim 's name (or yours KEVIN P. MARTIN A 0 I

00 if self-employed ), 10 FORBES WESTaddress, and ZIP code BRAINTREE MASSACHUSE S'

U

92382202-02-10

10290820 758606 70772000 2009.04011

2a Is the foundation directly or indirectly affiliated with, or related to, one or more tax-exempt organizations described

in section 501(c) of the Code ( other than section 501(c)(3 )) or in section 5279 0 Yes 0 No

b If 'Yes,' complete the following schedule.

STUDENTS HOUSE, INCORPORATED CONTINUATION FOR 990-PF, PART IVC/O NIXON PEABODY LLP ( BETHANY WOODS ) 04-2105949 PAGE 1 OF 3Part IV Capital Gains a nd Losses for Tax on Investment Income

(a) List and describe the kind (s) of property sold, e . g., real estate ,2-story brick warehouse ; or common stock, 200 shs. MLC Co.

( b How acquiredD - PurchaseD - Donation

( c) Date acquired(mo., day, yr.)

( d) Date sold(mo., day, yr.)

1a BP PLC SPONSORED ADR P 04/24/90 06/09/10b DELMONTE FOODS CO P 12/31/87 08/02/10cMERCK & CO P 09/01/93 08/02/10d VERIZON COMMUNCIATIONS INC P 09/01/93 08/02 / 10e BRISTOL MYERS SQUIBB P 05/19/92 08/02/10f 3M CO P 12/31/87 08/02/10STRYKER CORP P 01/18/00 08/02/10

hROYAL DUTCH SHELL PLD-ADR P 04/24/90 08/02/10iABBOTLABS P 02/12/09 08/02/10

UALCOMM INC P 02/12/09 09/02/10k PROCTOR & GAMBLE CO P 12/31/87 08/02 / 10INORFOLK SOUTHERN CORP P 02/12/09 08/02 / 10m MEDCO HEALTH SOLUTIONS INC P 08/01/93 08/02/10n MCDONALDS CORP P 02/12/09 08/02/10oAUTOMATIC DATA PROCESSING INC P 102 / 12 / 09 108 / 02 / 10

(e) Gross sales price ( f) Depreciation allowed(or allowable )

(g) Cost or other basisplus expense of sale

( h) Gain or (loss)( e) plus (f) minus (g)

a 13 , 277. 7 , 750o 5 , 527.b 7 , 394. 491. 6 , 903.c 34 , 989. 20 , 192. 14 , 797.d 18 , 051. 12 , 066. 5 , 985.e 20 , 312. 14 , 215. 6 , 097.f 69 , 863. 4 , 782. 65 , 081.9 18 , 961. 7 757. 11 , 204.h 23 , 144. 7 , 492. 15 , 652.1 13 , 654. 15 , 1371 -1 , 483.

15 , 492._

14 , 252. 1 , 240.k 104 939. 4 , 846. 100 093.1 22 , 816. 14 , 744. 8 , 072.m 11 , 402. 1 , 141. 10 , 261.n 17 , 512. 14 , 156. 3 , 356.o 16 , 692. 15 , 029. 1 , 663.

Complete only for assets showing gain in column ( h) and owned by the foundation on 12/31/69 (I) Losses (from col. (h))

(i) F.M.V. as of 12/31/69(j) Adjusted basisas of 12/31/69

(k) Excess of col. (i)over col . (1), if any

Gains ( excess of col. (h) gain over col. (k),but not less than '-0-")

a 5 , 527.b 6 , 903.c 14 , 797.d 5 , 985.e 6 , 097.f 65 , 081.

11 , 204.h 15 , 652.

-1 , 483.1,240.

k 100 093.1 8 , 072.m 10 , 261.n 3 , 356.0 1 , 663.

2 Capital gain net income or (net capital loss) If (loss ),a l soenter t0 ^nin

Part 1, line 7Part I, line 7 1 2

3 Net short -term capital gain or ( loss) as defined in sections 1222( 5) and (6):If gain, also enter in Part I, line 8, column (c).If (loss), enter '-0 ' in Part I, line 8 3

92359104-24-09

1410290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS HOUSE, INCORPORATED CONTINUATION FOR 990-PF, PART IVC / O NIXON PEABODY LLP ( BETHANY WOODS ) 04-2105949 PAGE 2 OF 3Part IV Capital Gains and Losses for Tax on Investment Income

(a) List and describe the kind (s) of property sold, e . g., real estate,2-story brick warehouse ; or common stock , 200 shs. MLC Co.

(b How acquiredD - PurchaseD - Donation

( c Date acquired(mo., day, yr.)

(d) Date sold(mo., day, yr.)

la AT&T INC P 09/01/93 08/02/10b LILY ELI & CO P 12/31/87 08/02/10c JOHNSON & JOHNSON P 12/31/87 08/02/10d INTL BUSINESS MACHINES CORP P 12 / 31/87 08 / 02 /10e INTEL CORP P 12/07/95 08/02/10(IMPERIAL OIL LTD P 02/12/09 08/02/10g HONEYWELL INTL INC P 01/18/00 08/02/10h HEINZ H J CO P 12/31/87 08/02/10i GENERAL MILL INC P 12 / 31/87 08/02 10GENERAL ELECTRIC CO P 12/31/87 08/02 / 10

k FRONTIER COMMUNICATIONS CORP P 09/01/93 08/02/10IEXXON MOBIL CORP P 05/19/92 08 / 02 / 10m COMCAST CORP CL A P 12/31/87 08 / 02 / 10nUS TREASURY NOTE P 03/04/09 08/02/10o DUPONT E I DE NEMOURS & CO P .07 / 14 / 0 04 30 10

(e) Gross sales price (f) Depreciation allowed(or allowable )

( g) Cost or other basisplus expense of sale

(h) Gain or (loss)(e) plus ( f) minus (g)

a 44 , 582. 11 , 598. 32 , 984.b 28 , 856. 3 , 120. 25 , 736.c 202 098. 7 , 049. 195 049.d 156 513. 28 , 847. 127 666.e 33 , 871. 12 , 400. 21 , 471.f 18 , 871. 14 , 896. 3 , 975.

8 , 736. 12 , 0801 -3 , 344.h 53 , 683. 4 , 535. 49 , 148.

110 334. 7 , 546. 102 788.13 , 032. 782. 12 , 250.

k 1 , 120. 813. 307.43 , 056. 8 , 275. 34 , 781.

m 5 , 608. 2 , 139. 3 , 469.n 100 328. 99 , 954. 374.o 50 , 000. 50 000. 0.

Complete only for assets showing gain in column (h) and owned by the foundation on 12/31/69 (I) Losses (from col. (h))

(i) F.M V. as of 12/31/69( j) Adjusted basisas of 12/31/69

( k) Excess of col. (i)over col. (I), if any

Gains (excess of col. (h) gain over col. (k),but not less than'-0-')

a 32 , 984.b 25 , 736.c 195 049.d 127 666.e 21 , 471.f 3 , 975.

-3 , 344.In 49 , 148.

102 788.12 , 250.

k 307.34 , 781.

m 3 , 469.n 374.0 0.

IfCapital am net income or capital loss)

f gain, also enter in Part I, line 7g (net p ( f (loss ), enter' -0-' in Part I, line 7 ) 2

3 Net short -term capital gain or (loss ) as defined in sections 1222(5 ) and (6):If gain, also enter in Part I, line 8, column (c).If (loss), enter '-0-' in Part I, line 8 3

92359104-24-09

1510290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS HOUSE, INCORPORATED CONTINUATION FOR 990-PF, PART IVC / O NIXON PEABODY LLP ( BETHANY WOODS ) 04-2105949 PAGE 3 OF 3Part IV Capital Gains and Losses for Tax on Investment Income

(a) List and describe the kind(s) of property sold, e.g., real estate,2-story brick warehouse; or common stock, 200 shs. MLC Co.

(b How acquiredD - PurchaseD - Donation

(c) Date acquired(mo., day, yr.)

(d) Date sold(mo., day, yr.)

la GENERAL ELECTRIC CAP CO P 07/14 / 04 08/02 / 10b MONEY MARKET OBLIG TR TAX FREE Pc MONEY MARKET OBLIG TR TAX FREE Pd

e

f

h

k

I

m

n

0

(e) Gross sales price (f) Depreciation allowed(or allowable)

(g) Cost or other basisplus expense of sale

(h) Gain or (loss)(e) plus (f) minus (g)

a 50 , 500. 50 000. 500.b 18. 18.c 9. 9.d

ef

h

k

I

mn

0Complete only for assets showing gain in column (h) and owned by the foundation on 12/31/69 (I) Losses (from col. (h))

(i) F.M.V. as of 12/31/69(j) Adjusted basisas of 12/31/69

(k) Excess of col. (i)over col. (1), if any

Gains (excess of col. (h) gain over col. (k),but not less than'-0- )

a 500.b 18.c 9.d

e

f

h

k

m

n

0

2 Capital net income or net ca dal lossJ If gain, also enter in Part I, line 7

gain ( p ) l If (loss), enter'-0- in Part I line 7 } 2 861 , 629.,

3 Net short-term capital gain or (loss) as defined in sections 1222(5) and (6):If gain, also enter in Part I, line 8, column (c).If (loss), enter'-0' in Part I, line 8 3 N /A

92359104-24-09

1610290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS, HOUSE, INCORPORATED C/O NIXON P

FORM 990-PF INTEREST ON SAVINGS AND TEMPORARY CASH INVESTMENTS STATEMENT 1

SOURCE

CORPORATE BONDSUS GOVERNMENT OBLIGATIONSUS GOVERNMENT TAX MANAGEMENT FUND

TOTAL TO FORM 990-PF, PART I, LINE 3, COLUMN A

3,381.875.

4.

AMOUNT

4,260.

FORM 990-PF DIVIDENDS AND INTEREST FROM SECURITIES STATEMENT 2

SOURCE

DIVIDEND INCOME

TOTAL TO FM 990-PF, PART I, LN 4

(A) (B) (C) (D)EXPENSES NET INVEST- ADJUSTED CHARITABLE

PER BOOKS MENT INCOME NET INCOME PURPOSES

0. 35,926.

FORM 990-PF LEGAL FEES STATEMENT 3

DESCRIPTION

LEGAL FEES - CASNER &

EDWARDS LLP 10,676. 0. 0.

TO FM 990-PF, PG 1, LN 16A 10,676. 0. 0.

FORM 990-PF ACCOUNTING FEES STATEMENT 4

DESCRIPTION

(A) (B) (C) (D)EXPENSES NET INVEST- ADJUSTED CHARITABLEPER BOOKS MENT INCOME NET INCOME PURPOSES

GROSS AMOUNT

35,926.

COLUMN (A)

AMOUNT

35,926.

35,926.

KEVIN P. MARTIN &

ASSOCIATES

TO FORM 990-PF, PG 1, LN 16B

6,140.

6,140.

CAPITAL GAINS

DIVIDENDS

0.

0.

0.

04-2105949

6,140.

6,140.

17 STATEMENT(S) 1, 2, 3, 4

10290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS, HOUSE, INCORPORATED C/O NIXON P 04-2105949

FORM 990-PR OTHER PROFESSIONAL FEES STATEMENT 5

(A) (B) (C) (D)EXPENSES NET INVEST- ADJUSTED CHARITABLE

DESCRIPTION PER BOOKS MENT INCOME NET INCOME PURPOSES

FIDUCIARY FEES - NIXONPEABODY 13,465. 11,865. 1,600.

TO FORM 990-PF, PG 1, LN 16C 13,465. 11,865. 1,600.

FORM 990-PF TAXES STATEMENT 6

(A) (B) (C) (D)EXPENSES NET INVEST- ADJUSTED CHARITABLE

DESCRIPTION PER BOOKS MENT INCOME NET INCOME PURPOSES

FOREIGN TAXES WITHHELD AT

SOURCE 229. 229. 0.FEDERAL EXCISE TAXES PAID 10,316. 0. 0.

TO FORM 990-PF, PG 1, LN 18 10,545. 229. 0.

FORM 990-PF OTHER EXPENSES STATEMENT 7

(A) (B) (C) (D)

EXPENSES NET INVEST- ADJUSTED CHARITABLE

DESCRIPTION PER BOOKS MENT INCOME NET INCOME PURPOSES

FILING FEES 70. 0. 70.MISC TAX PREPARATION 1,000. 0. 0.

TO FORM 990-PF, PG 1, LN 23 1,070. 0. 70.

FOOTNOTES STATEMENT 8

DOCUMENTS ATTACHED TO FORM 990PF AND PC

COMPLAINT FOR VOLUNTARY DISSOLUTION

INTERLOCUTORY ORDER

18 STATEMENT(S) 5, 6, 7, 810290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS,HOUSE, INCORPORATED C/O NIXON P

MOTION FOR ENTRY OF INTERLOCUTORY ORDER

VOTE FOR ADOPTION BY THE BOARD OF TRUSTEES

REGARDING DISSOLUTION OF THE CORPORATION

04-2105949

19 STATEMENT(S) 8

10290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

STUDENTS, HOUSE, INCORPORATED C/O NIXON P 04 -2105949

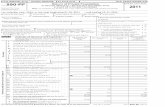

FORM 990-PF PART VIII - LIST OF OFFICERS, DIRECTORS STATEMENT 9TRUSTEES AND FOUNDATION MANAGERS

EMPLOYEETITLE AND COMPEN- BEN PLAN EXPENSE

NAME AND ADDRESS AVRG HRS/WK SATION CONTRIB ACCOUNT

MRS HIROSHI H. NISHINO PRESIDENT AND TRUSTEEC/O NIXON PEABODY LLP, 100 SUMMER

STREET 0.00 0. 0. 0.BOSTON, MA 02110

MRS ROLF STUTZ VICE PRESIDENT AND TRUSTEEC/O NIXON PEABODY LLP, 100 SUMMERSTREET 0.00 0. 0. 0.BOSTON, MA 02110

BETHANY M. WOODS TREASURER AND CLERK

C/O NIXON PEABODY LLP, 100 SUMMERSTREET 0.00 0. 0. 0.BOSTON, MA 02110

MRS THOMAS S. BARROWS TRUSTEE

C/O NIXON PEABODY LLP, 100 SUMMERSTREET 0.00 0. 0. 0.BOSTON, MA 02110

MRS R. WILLIS LEITH, JR TRUSTEEC/O NIXON PEABODY LLP, 100 SUMMERSTREET 0.00 0. 0. 0.BOSTON, MA 02110

MRS. H. BURTON POWERS TRUSTEEC/O NIXON PEABODY LLP, 100 SUMMERSTREET 0.00 0. 0. 0.BOSTON, MA 02110

MRS RICHARD B. CARLTON TRUSTEEC/O NIXON PEABODY LLP, 100 SUMMER

STREET 0.00 0. 0. 0.BOSTON, MA 02110

TOTALS INCLUDED ON 990- PF, PAGE 6, PART VIII 0. 0. 0.

20 STATEMENT(S) 910290820 758606 70772000 2009.04011 STUDENTS HOUSE, INCORPORATE 70772001

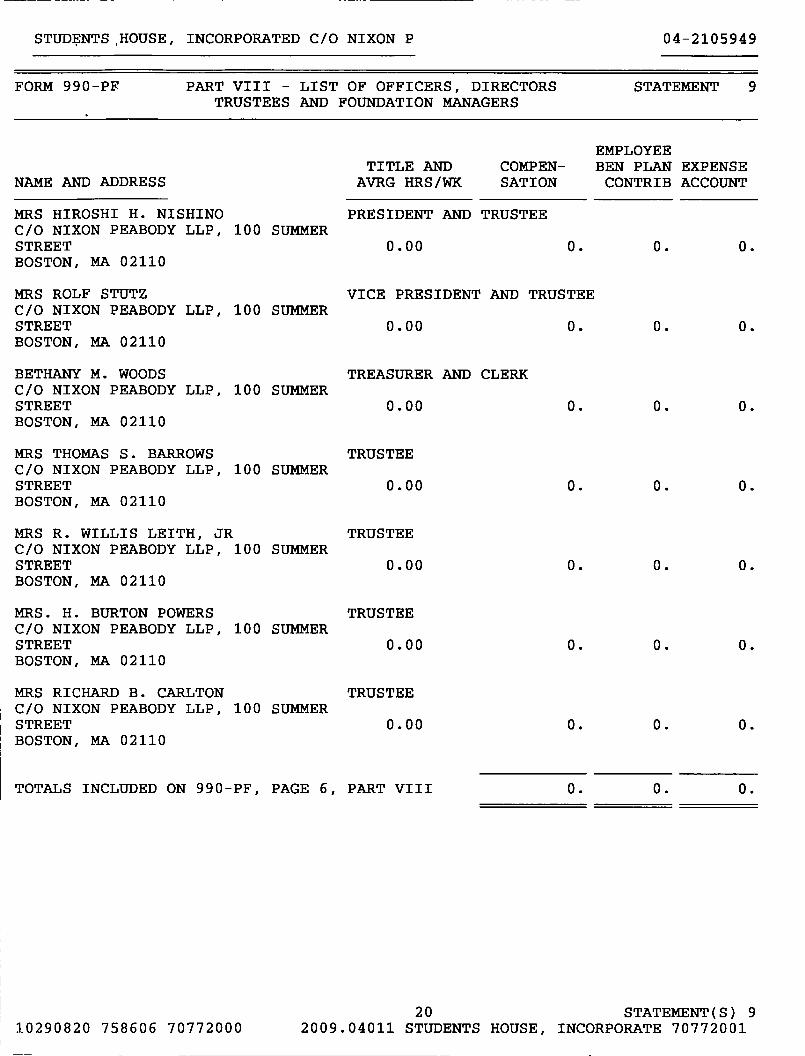

COMMONWEALTH OF MASSACHUSETTS

SUFFOLK, SS. SUPREME JUDICIAL COURTEQUITY NO.

STUDENTS HOUSE INCORPORATED,

Plaintiff,

V.

MARTHA COAKLEY, as she isTHE ATTORNEY GENERAL OF THECOMMONWEALTH OF MASSACHUSETTS,

and

NEW ENGLAND CONSERVATORY OFMUSIC, and MUSEUM OF FINE ARTS,

Defendants.

COMPLAINT FOR VOLUNTARY DISSOLUTION

The Plaintiff, Students House Incorporated, respectfully requests dissolution

pursuant to G.L. c . 180, Section 11 A as follows:

1. Martha Coakley is the duly elected and qualified Attorney General of the

Commonwealth of Massachusetts.

2. The Plaintiff is a corporation for charitable purposes, organized and

existing pursuant to Chapter 180 of the Massachusetts General Laws.

3. Defendant New England Conservatory of Music is a corporation for

charitable purposes, organized and existing pursuant to Chapter 180 of the Massachusetts

General Laws.

4. Defendant Museum of Fine Arts is a corporation for charitable purposes,

organized and existing pursuant to Chapter 180 of the Massachusetts General Laws.

The charitable purposes of the Plaintiff, as set forth in the Plaintiffs

Articles of Organization as amended , are, in pertinent part, as follows:

To benefit young women engaged in the study of any branch of art,

science or higher education in the City of Boston, and to do any

and all acts consistent with the foregoing purpose permitted by the

laws of the Commonwealth of Massachusetts to a charitable

corporation organized under Chapter 180; including, furnishing a

home for them and a place for their rest, recreation and

entertainment under circumstances and surroundings which will

promote their mental, moral and physical welfare; maintaining a

registry of suitable lodgings for such young women; and providing

financial assistance to them, by grant, loan or aid in any other

manner, for expenses connected with their education, including

tuition, room and board.

6. Defendant New England Conservatory of Music operates a school of

music for performance and teaching.

7. Defendant Museum of Fine Arts operates a fine arts museum and related

programs, including the School of the Museum of Fine Arts, a school dedicated to

educating artists.

8. In the 1970's, the Plaintiff ceased providing housing and related services

for women attending college, sold its real estate , and used the proceeds as a fund from

which each year it has issued grants in furtherance of its charitable mission.

9. In recent years the Board of Trustees has determined that the best and most

efficient means of fulfilling the Plaintiff's charitable mission is to issue grants in

approximately equal amounts to the New England Conservatory of Music and the School

of the Museum of Fine Arts (the "School" or "Schools"), for financial assistance to

women with respect to the expenses of their education at such School, including tuition,

room and board, with a preference for assistance based on financial need.

10. As a result, in recent years the Plaintiff s sole activity has been to issue

such grants in approximately equal amounts to the New England Conservatory of Music

and the School of the Museum of Fine Arts for such purpose;

11. The Board of Trustees of the Plaintiff has examined and considered the

present and future capacity of the Plaintiff, as presently constituted, to fulfill its charitable

mission;

12. The Board of Trustees of the Plaintiff has determined, after careful

consideration, that the Plaintiff's charitable mission would be fulfilled most efficiently,

effectively and economically if the Plaintiff were to dissolve, with distribution of the

Plaintiffs net assets in equal portions to the New England Conservatory of Music and the

School of the Museum of Fine Arts, for financial assistance to women with respect to the

expenses of their education at such School, including tuition, room and board, with a

preference for assistance based on financial need;

13. After due deliberation, Plaintiffs Board of Trustees, which is its

governing body, by unanimous written consent, determined that it is in the best interest of

the Plaintiff and its charitable mission that the Plaintiff be dissolved, with distribution of

the Plaintiffs net assets in equal portions to the New England Conservatory of Music (the

"Conservatory") and the School of the Museum of Fine Arts (the "School") to be used as

set forth below, and that this Complaint for Dissolution be presented to the Supreme

Judicial Court:

As a fund for financial assistance to women with respect to the

expenses of their education at such Conservatory or School,

including tuition, room and board, with a preference for assistance

based on financial need. Such fund shall be designated the

"Students House Scholarship Fund." The Students House

Scholarship Fund (the "Fund") shall be held and invested as an

endowment, provided that a portion of the original amount

received pursuant to the dissolution (herein referred to as the

"Principal" ofthe Fund) may be expended to the extent that in any

year such expenditure of Principal is necessary in order for there to

be available a total of four percent of the then-current market value

of the Fund for scholarships and administrative expenses, or such

higher percentage as required by a generally applicable endowment

spending policy of the organization.

A true copy of the text of said vote is annexed as Exhibit A.

14. Defendant New England Conservatory of Music and Defendant Museum

of Fine Arts have agreed to accept the Plaintiff's funds and assets for the purposes as

stated in the Plaintiffs vote described above, subject to the authorization of the Supreme

Judicial Court pursuant to the provisions of Section 11A of Chapter 180 of the

Massachusetts General Laws, as amended, and to expend or use said funds, assets and

property solely in furtherance of said stated purposes and in accordance with the

authorization of the Supreme Judicial Court.

15. As appears in Plaintiffs latest annual report (Form PC and Form 990-PF)

and an Affidavit of Financial Activity filed herewith reflecting subsequent financial

activity, Plaintiff has assets of approximately $1,576,000, and has accrued and anticipated

liabilities , including costs of dissolution and final tax returns and annual reports, of

$15,000 . Plaintiff anticipates that its net assets available for distribution will be

approximately $1,561,000. A true copy of said Form PC is annexed hereto as

4

Exhibit B-1, a true copy of said Form 990-PF is annexed hereto as Exhibit B-2, and said

Affidavit of Financial Activity is annexed hereto as Exhibit C .

16. Plaintiff avers that to the best of its knowledge, information and belief, all

of the funds received by the Plaintiff since its inception were donated or accumulated for

Plaintiffs general purposes with no restriction of any kind placed upon them by donors.

17. Plaintiff anticipates that all outstanding debts, liabilities and obligations to

creditors will be satisfied in full and discharged, and avers that funds have been prudently

reserved therefore.

REMAINDER OF PAGE INTENTIONALLY BLANK

WHEREFORE, the Plaintiff respectfully prays that the Court:

1. enter an Interlocutory Order declaring:

That the transfer by Plaintiff in equal portions to Defendant

New England Conservatory of Music and Museum of Fine

Arts of the funds, assets and property remaining after

satisfaction of Plaintiff's existing debts, obligations,

liabilities and final expenses be authorized, such funds,

assets and property to be used for the purposes described in

Paragraph 13 of this Complaint.

2. Upon the filing of affidavits by Plaintiff and Defendant New England

Conservatory of Music and Defendant Museum of Fine Arts attesting to the

consummation of said transfer, enter a final order declaring:

That Plaintiff is dissolved as an existing Massachusettscorporation in accordance with the provisions of Section11A of Chapter 180 of the Massachusetts General Laws, asamended.

Date: 27 2010

8861 0/414816 1

M

STUDENTS HOUSE INCORPORATED

By its Attorne

Richard C. Alen, Esq.B.B.O. # 015720Casner & Edwards, LLP303 Congress StreetBoston, MA 02210(617) 426-5900 x 339

6

COMMONWEALTH OF MASSACHUSETTS

SUFFOLK , so. SUPREME JUDICIAL COURTFOR SUFFOLK COUNTYNo. SJ-2010-0355

STUDENTS HOUSE INCORPORATED

va.

MARTHA•COAKLEY, as She is the ATTORNEY GENERALof the COMMONWEALTH of MASSACHUSETTS and NEW ENGLAND CONSERVATORY

OF MUSIC and MUSEUM OF FINE ARTS

INTERLOCUTORY ORDER

On Plaintiff's-Motion for Entry of Interlocutory order, it

appearing that the Defendants Martha Coakley, Attorney General of

the-Commonwealth, and New England Conservatory of Music and

Museum of Fine Arts, have assented thereto,

NOW, THEREFORE, it is adjudged and ordered:

That the Plaintiff transfer to in equal portions to New

England Conservatory of Music and to Museum of Fine Arts the

Plaintiffs net funds, property and assets remaining after

satisfaction of its lawful debts, obligations, liabilities and

expenses, such assets to be used by New England Conservatory of

Music and Museum of Fine Arts as follows:

As.a fund for financial assistance to women withrespect to the expenses of their education at suchConservatory.or School, including tuition, room andboard, with preference for assistance based onfinancial need. Such fund shall be designated the"Students House Scholarship Fund." The Students HouseScholarship Fund (the "Fund") shall be held andinvested as an endowment, provided that a portion ofthe original amount received pursuant to the

dissolution (herein referred to an the "Principal" ofthe Fund) may be expended to the extent that in anyyear such expenditure of Principal is necessary inorder for there to be available a total of four percentof the then-current market value of the Fund forscholarships and administrative expenses, or suchhigher percentage as required by a generally applicableendowment spending policy of the organization.

By th rt, (G J

Maura S. Doyle

ENTERED: Augu9t 2, 2010

COMMONWEALTH OF MASSACHUSETTS

SUFFOLK, SS. SUPREME JUDICIAL COURTEQUITY NO.

STUDENTS HOUSE INCORPORATED, )

Plaintiff,

v. )

MARTHA COAKLEY, as she is )

THE ATTORNEY GENERAL OF THE )

COMMONWEALTH OF MASSACHUSETTS, )

)and }

)NEW ENGLAND CONSERVATORY OF )MUSIC, and MUSEUM OF FINE ARTS, )

)Defendants. )

INTERLOCUTORY ORDER

On Plaintiffs Motion for Interlocutory Order, it appearing that the Defendants

Martha Coakley, Attorney General of the Commonwealth, and New England

Conservatory of Music and Museum of Fine Arts have assented thereto,

NOW, THEREFORE, IT IS ADJUDGED AND ORDERED:

That the Plaintiff transfer to in equal portions to New England Conservatory of

Music and to Museum of Fine Arts the Plaintiffs net funds, property and assets

remaining after satisfaction of its lawful debts, obligations, liabilities and expenses, such

}

assets to be used by New England Conservatory of Music and Museum of Fine Arts as

follows:

As a fund for financial assistance to women with respect to theexpenses of their education at such Conservatory or School,

including tuition, room and board, with a preference for assistance

based on financial need. Such fund shall be designated the

"Students House Scholarship Fund." The Students HouseScholarship Fund (the "Fund}}) shall be held and invested as anendowment, provided that a portion of the original amount

received pursuant to the dissolution (herein referred to as the"Principal " of the Fund) may be expended to the extent that in anyyear such expenditure of Principal is necessary in order for there tobe available a total of four percent of the then-current market valueof the Fund for scholarships and administrative expenses , or suchhigher percentage as required by a generally applicable endowmentspending policy of the organization.

By the Court:

DATED:

8861.01431107.1

, 2010

2

COMMONWEALTH OF MASSACHUSETTS

SUFFOLK, SS. SUPREME JUDICIAL COURTEQUITY NO.

STUDENTS HOUSE INCORPORATED, )

Plaintiff,

V. )

MARTHA COAKLEY, as she is )

THE ATTORNEY GENERAL OF THE )

COMMONWEALTH OF MASSACHUSETTS, )

and

NEW ENGLAND CONSERVATORY OF )

MUSIC, and MUSEUM OF FINE ARTS, )

Defendants. )

MOTION FOR ENTRY OF INTERLOCUTORY ORDER

Now comes the Plaintiff, Students House Incorporated, and moves that the Courtenter an Interlocutory Order in the form attached hereto.

Assented to:

MARTHA COAKLEYATTORNEY GENERAL

Le Ben^eltAssistant Attorney GeneralNon-Profit Organizations/

Public Charities DivisionOffice of the Attorney GeneralOne Ashburton PlaceBoston, MA 02108617-963-2120BBO # 644403

STUDENTS HOUSE INCORPORATEDBy its Attorney

R+

Richard C. Allen, Esq.Casner & Edwards, LLP303 Congress Street

Boston, MA 02210(617) 426-5900 x 339BBO. # 015720

DATED : July 27, 2010

Assented to:

NEW ENGLAND CONSERVATORYOF MUSIC _

By:

Title

MUSEUM OF FINE ARTS

By.

Title:

DATED: 12010

8861.0/431094 1

2

Assented to:

NEW ENGLAND CONSERVATORYOF MUSIC

By:

Title:

MUSEUM OF FINE ARTS

By: _"-&o

cl '(, ( re^^^

Title: OeftuaL

DATED: 22010

8861.0/431094.1

STUDENTS HOUSE INCORPORATED

Vote for adoption by the Board of Trusteesregarding dissolution of the Corporation

WHEREAS, the charitable mission of Students House Incorporated (the

"Corporation"), as set forth in the Corporation's Articles of Organization and Bylaws, is

as follows:

To benefit young women engaged in the study of anybranch of art, science or higher education in the City ofBoston, and to do any and all acts consistent with theforegoing purpose permitted by the laws of theCommonwealth ofMassachusetts to a charitablecorporation organized under Chapter 180; including,furnishing a home for them and a place for their rest,recreation and entertainment under circumstances andsurroundings which will promote their mental, moral andphysical welfare; maintaining a registry of suitablelodgings for such young women; and providing financialassistance to them, by grant, loan or aid in any othermanner, for expenses connected with their education,including tuition, room and board.

WHEREAS, in recent years the Board of Trustees has determined that the bestand most efficient means of fulfilling the Corporation's charitable mission is to issuegrants in approximately equal amounts to the New England Conservatory of Music andthe School ofthe Museum ofFine Arts (the "School" or "Schools"), for financialassistance to women with respect to the expenses oftheir education at such School,including tuition, room and board, with a preference for assistance based on financialneed;

WHEREAS, as a result, in recent years the Corporation's sole activity has been toissue such grants in approximately equal amounts to the New England Conservatory ofMusic and the School ofthe Museum ofFine Arts;

WHEREAS, the Board of Trustees of the Corporation has examined andconsidered the present and ham capacity of the Corporation, as presently constituted, tofulfill its charitable mission;

WHEREAS, the Board of Trustees of the Corporation has determined, aftercareful consideration, that the Corporation's charitable mission would be fulfilled mostefficiently, effectively and economically if the Corporation were to dissolve, withdistribution of the Corporation's assets in equal portions to the New England

Conservatory of Music and the School of the Museum ofFine Arts, for financialassistance to women with respect to the expenses of their education at such School,including tuition, room and board, with a preference for assistance based on financialneed;

WHEREAS, the Board of Trustees ofthe Corporation has determined, aftercareful consideration, that it is in the best interest of the Corporation and its charitablemission that the Corporation be dissolved, with distribution of the Corporation's netassets in equal portions to the New England Conservatory of Music and the School of theMuseum of Fine Arts, for financial assistance to women with respect to the expenses oftheir education at such School, including tuition, room and board, with a preference forassistance based on financial need

NOW, THEREFORE, IT IS RESOLVED AND VOTED AS FOLLOWS:

1. That Students House Incorporated (the "Corporation") shall be dissolved.

2. That, in accordance with Massachusetts law, a complaint for dissolution oftheCorporation shall be presented to the Office of the Attorney General and theMassachusetts Supreme Judicial Court, with the New England Conservatory ofMusic (the "Conservatory") and the School of the Museum ofFine Arts (the"School") identified as carrying on the Corporation's mission as the recipients, inequal portions, of the Corporation's net assets to be used as follows:

As a fund for financial assistance to women with respect to the expensesof their education at such Conservatory or School, including tuition, roomand board, with a preference for assistance based on financial need. Suchfund shall be designated the "Students House Scholarship Fund." TheStudents House Scholarship Fund (the "Fund') shall be held and investedas an endowment, provided that a portion of the original amount receivedpursuant to the dissolution (herein referred to as the "Principal" of theFund) may be expended to the extent that in any year such expenditure ofPrincipal is necessary in order for there to be available a total of fourpercent of the then-current market value of the Fund for scholarships andadministrative expenses, or such higher percentage as required by agenerally applicable endowment spending policy of the organization.

3. That the officers of the Corporation, acting jointly or alone, are hereby authorizedand directed, for and on behalf ofthe Corporation and in its corporate name, toexecute and deliver any court pleadings, instruments, documents, and certificates,with such changes in the terms and provisions thereof as the officer executing thesame deems necessary or desirable, and to do and perform such acts and deeds asthey or any ofthem may deem necessary or desirable to effect the purposes of theforegoing resolutions.

2

12912675

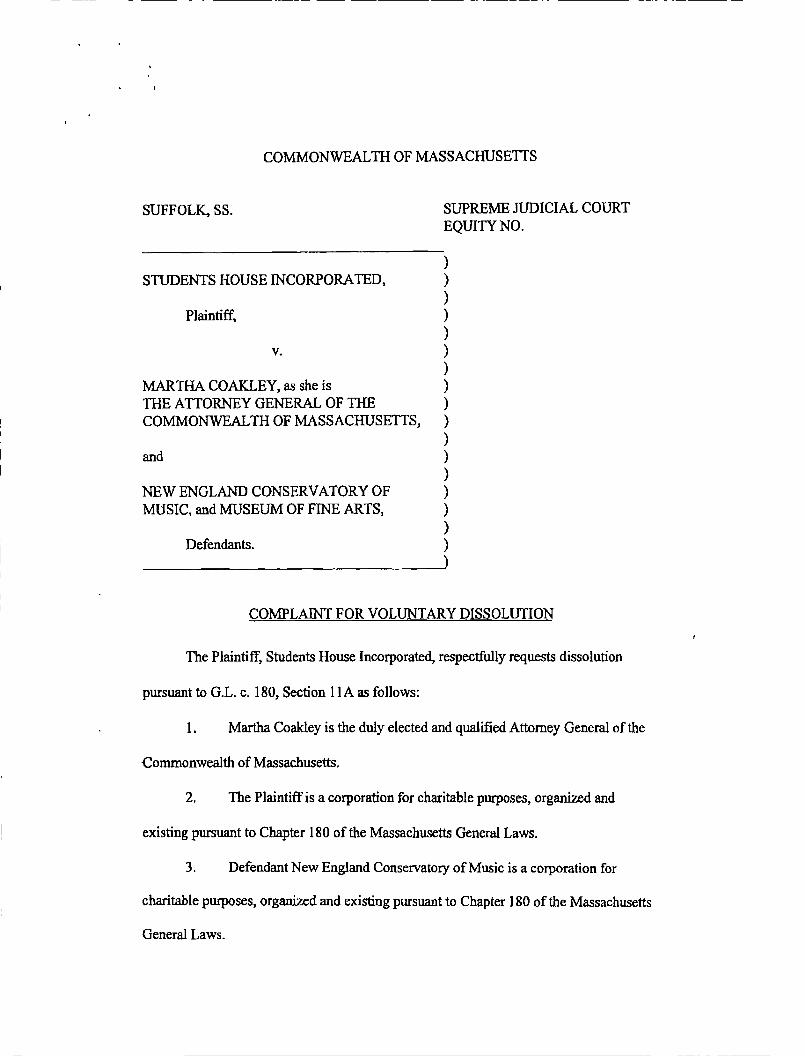

This written consent may be executed in any number of counterparts, each ofwhichshall be deemed an original but an of which together shall constitute one and the sameinstrument and shall be filed with the records ofthe meetings ofthe Board of Trustees ofthe Corporation.

Director: )0.6stmr.w Date: )4 a c4 T Lo i eKatherine M. Barrows

Director:Phyllis Carlton

Director:Barbara B. Leith

Director:Emiko Nishino

Director:Anne L. Powers

Director.Nancy S. Stutz

3

12912675

Date:

Date:

Date:

Date:

Date:

This written consent may be executed in any number ofcounterparts, each ofwhichshall be deemed an original but all of which together shall constitute one and the sameinstrument and shall be filed with the records of the meetings of the Board ofTrustees ofthe Corporation.

Director: Date:Katherine M. Barrows

Director. Date: fold&4P 's Carlton

Director: Date:Barbara B. Leith

Director. Date:Emiko Nishino

Director Date:Anne L. Powers

Director: Date:Nancy S. Stutz

3

12912675

This written consent may be executed in any number of counterparts, each ofwhichshall be deemed an original but all of which together shall constitute one and the sameinstrument and shall be filed with the records ofthe meetings of the Board of Trustees ofthe Corporation.

Director:Katherine M. Barrows

Director:Phyllis Carlton

Director:Barbara B. Leith

Director:Emiko Nishino

Drector:Anne L. Powers

Director:Nancy S. Stutz

Director:William V. Tripp III

Date:

Date:

Date : ^eA 2a o ^o

Date:

Date:

Date:

Date:

3

This written consent may be executed in any number of counterparts, each ofwhichshall be deemed an original but all ofwhich together shall constitute one and the sameinstrument and shall be filed with the records of the meetings of the Board of Trustees ofthe Corporation.

Director.Katherine M. Barrows

Director.Phyllis Carlton

Director.Barbara B. Leith

Director. tvvu- t__ nt7Emiko Nishino

Director.Anne L. Powers

Director.Nancy S. Stutz

3

12912675

Date:

Date:

Date:

Date : WLMakI C^.`, D ! (^

Date:

Date:

..

This written consent may be executed in any number of counterparts, each ofwhichshall be deemed an original but all of which together shall constitute one and the sameinstrument and shall be filed with the records of the meetings of the Board of Trustees ofthe Corporation.

Director: Date:Katherine M. Barrows

Director:Phyllis Carlton

Director.Barbara B. Leith

Director.Emiko Nishino

Director : ! L' v 4 0d-WWAnne L. Powers

Director:Nancy S. Stutz

3

Date:

Date:

Date:

Date: 3 WI a

Date:

12912675

This written consent may be executed in any number ofcowiterparb, each ofwhichshall be deemed an original but all ofwhich together shall constitute one and the sameinstrument and shall be filed with the records of the meetings of the Board ofTrustees ofthe Corporation.

Director:Katherine M. Barrows

Director:Phyllis Carlton

Director:Barbara B. Leith

Director:Emiko Nishino

Director.Anne L. Powers

Director.Nancy S. Stutz

3

12912675

Date:

Date:

Date:

Date:

Date:

Date: (C^