ITTIZAN (BALANCED FUND) ISTIQRAR (STABLE … · e above mentioned funds will be professionally...

12

ITTIZAN (BALANCED FUND) ISTIQRAR (STABLE CAPITAL FUND) IHFAZ EQUITY INDEX FUND ITTIHAD GROWTH FUND ISTIFAD BLUE CHIPS FUND IRAD DIVIDEND FUND IHSAN BALANCED FUND

Transcript of ITTIZAN (BALANCED FUND) ISTIQRAR (STABLE … · e above mentioned funds will be professionally...

ITTIZAN (BALANCED FUND)

ISTIQRAR (STABLE CAPITAL FUND)

IHFAZ EQUITY INDEX FUND

ITTIHAD GROWTH FUND

ISTIFAD BLUE CHIPS FUND

IRAD DIVIDEND FUND

IHSAN BALANCED FUND

This document provides detailed features, investment objectives, strategy and approach of the 7 Shariah-compliant funds and all other

important information that you will need to know regarding these investment funds.

1. ITTIZAN (BALANCED FUND)

2. ISTIQRAR (STABLE CAPITAL FUND)

3. IHFAZ EQUITY INDEX FUND

4. ITTIHAD GROWTH FUND

5. ISTIFAD BLUE CHIPS FUND

6. IRAD DIVIDEND FUND

7. IHSAN BALANCED FUND

The choice of funds should be based on, among others, your tolerance to risk. Please seek advice from your Takaful Financial

Consultants of the company on your tolerance to risk. For Ittizan and Istiqrar, the funds are no longer being offered for new

investment.

The above mentioned funds will be professionally managed by the Investment Division of Syarikat Takaful Malaysia Berhad. The

investment team comprises of a group of professional portfolio managers and investment research analysts who possess an average

of 15 years experience in fund management and has previously managed more than RM7 billion worth of funds.

Note: The selection of investible securities is conducted in a systematic manner where the investment process is governed by internal

policies. In addition to that, the systematic investment process is strictly guided by the Company’s Shariah Advisory Body to ensure

that the Shariah principles are not compromised in every investment decision made.

MARKET REVIEW & OUTLOOK

MAY 2012

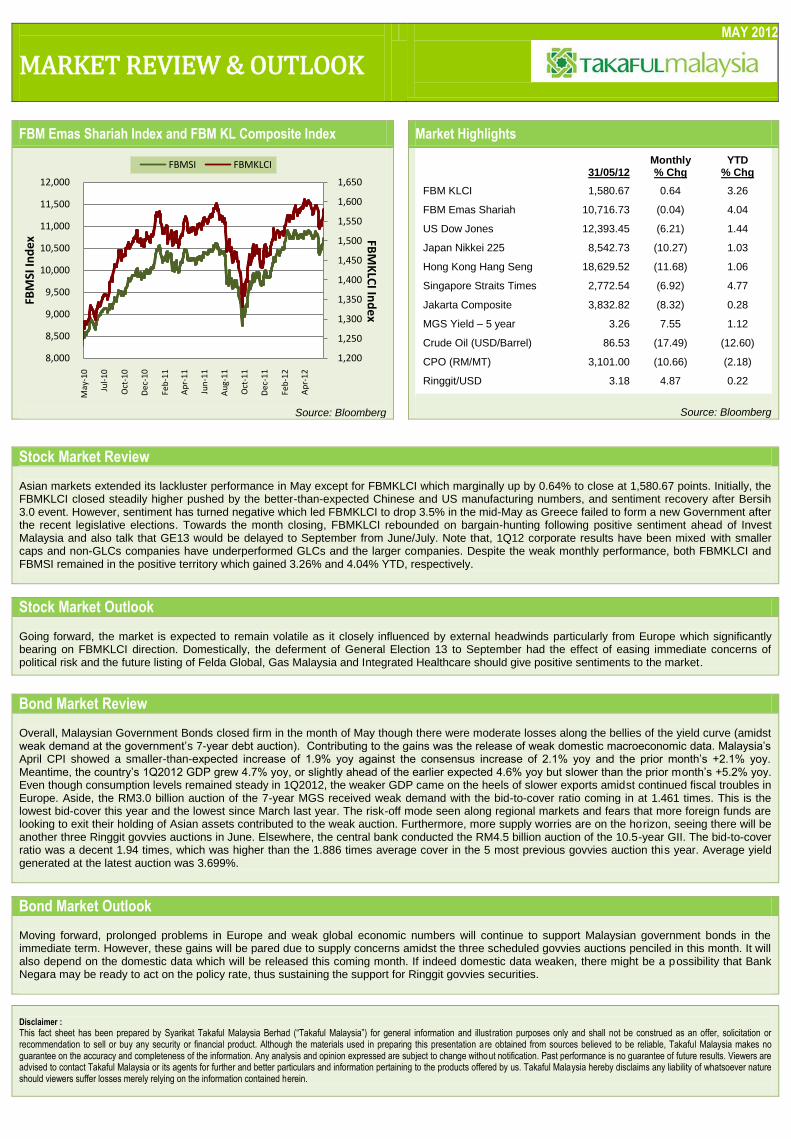

FBM Emas Shariah Index and FBM KL Composite Index Market Highlights

Source: Bloomberg

31/05/12

Monthly % Chg

YTD % Chg

FBM KLCI 1,580.67 0.64 3.26

FBM Emas Shariah 10,716.73 (0.04) 4.04

US Dow Jones 12,393.45 (6.21) 1.44

Japan Nikkei 225 8,542.73 (10.27) 1.03

Hong Kong Hang Seng 18,629.52 (11.68) 1.06

Singapore Straits Times 2,772.54 (6.92) 4.77

Jakarta Composite 3,832.82 (8.32) 0.28

MGS Yield – 5 year 3.26 7.55 1.12

Crude Oil (USD/Barrel) 86.53 (17.49) (12.60)

CPO (RM/MT) 3,101.00 (10.66) (2.18)

Ringgit/USD 3.18 4.87 0.22

Source: Bloomberg

Stock Market Review Asian markets extended its lackluster performance in May except for FBMKLCI which marginally up by 0.64% to close at 1,580.67 points. Initially, the FBMKLCI closed steadily higher pushed by the better-than-expected Chinese and US manufacturing numbers, and sentiment recovery after Bersih 3.0 event. However, sentiment has turned negative which led FBMKLCI to drop 3.5% in the mid-May as Greece failed to form a new Government after the recent legislative elections. Towards the month closing, FBMKLCI rebounded on bargain-hunting following positive sentiment ahead of Invest Malaysia and also talk that GE13 would be delayed to September from June/July. Note that, 1Q12 corporate results have been mixed with smaller caps and non-GLCs companies have underperformed GLCs and the larger companies. Despite the weak monthly performance, both FBMKLCI and FBMSI remained in the positive territory which gained 3.26% and 4.04% YTD, respectively.

Stock Market Outlook Going forward, the market is expected to remain volatile as it closely influenced by external headwinds particularly from Europe which significantly bearing on FBMKLCI direction. Domestically, the deferment of General Election 13 to September had the effect of easing immediate concerns of political risk and the future listing of Felda Global, Gas Malaysia and Integrated Healthcare should give positive sentiments to the market.

Bond Market Review Overall, Malaysian Government Bonds closed firm in the month of May though there were moderate losses along the bellies of the yield curve (amidst weak demand at the government’s 7-year debt auction). Contributing to the gains was the release of weak domestic macroeconomic data. Malaysia’s April CPI showed a smaller-than-expected increase of 1.9% yoy against the consensus increase of 2.1% yoy and the prior month’s +2.1% yoy. Meantime, the country’s 1Q2012 GDP grew 4.7% yoy, or slightly ahead of the earlier expected 4.6% yoy but slower than the prior month’s +5.2% yoy. Even though consumption levels remained steady in 1Q2012, the weaker GDP came on the heels of slower exports amidst continued fiscal troubles in Europe. Aside, the RM3.0 billion auction of the 7-year MGS received weak demand with the bid-to-cover ratio coming in at 1.461 times. This is the lowest bid-cover this year and the lowest since March last year. The risk-off mode seen along regional markets and fears that more foreign funds are looking to exit their holding of Asian assets contributed to the weak auction. Furthermore, more supply worries are on the horizon, seeing there will be another three Ringgit govvies auctions in June. Elsewhere, the central bank conducted the RM4.5 billion auction of the 10.5-year GII. The bid-to-cover ratio was a decent 1.94 times, which was higher than the 1.886 times average cover in the 5 most previous govvies auction this year. Average yield generated at the latest auction was 3.699%.

Bond Market Outlook Moving forward, prolonged problems in Europe and weak global economic numbers will continue to support Malaysian government bonds in the immediate term. However, these gains will be pared due to supply concerns amidst the three scheduled govvies auctions penciled in this month. It will also depend on the domestic data which will be released this coming month. If indeed domestic data weaken, there might be a possibility that Bank Negara may be ready to act on the policy rate, thus sustaining the support for Ringgit govvies securities.

Disclaimer :

This fact sheet has been prepared by Syarikat Takaful Malaysia Berhad (“Takaful Malaysia”) for general information and illustration purposes only and shall not be construed as an offer, solicitation or recommendation to sell or buy any security or financial product. Although the materials used in preparing this presentation are obtained from sources believed to be reliable, Takaful Malaysia makes no guarantee on the accuracy and completeness of the information. Any analysis and opinion expressed are subject to change without notification. Past performance is no guarantee of future results. Viewers are advised to contact Takaful Malaysia or its agents for further and better particulars and information pertaining to the products offered by us. Takaful Malaysia hereby disclaims any liability of whatsoever nature should viewers suffer losses merely relying on the information contained herein.

1,200

1,250

1,300

1,350

1,400

1,450

1,500

1,550

1,600

1,650

8,000

8,500

9,000

9,500

10,000

10,500

11,000

11,500

12,000

May

-10

Jul-

10

Oct

-10

Dec

-10

Feb

-11

Ap

r-1

1

Jun

-11

Au

g-1

1

Oct

-11

Dec

-11

Feb

-12

Ap

r-1

2

FBM

SI In

de

x

FBMSI FBMKLCI

FBM

KLC

I Ind

ex

ITTIZAN (Balanced Fund)

MAY 2012

Investment Objective To achieve reasonable returns and capital growth opportunities through selected investment in Shariah approved shares listed in Bursa Malaysia and Shariah compliant Islamic debt securities.

Investment Strategy Invest in a balanced asset allocation comprising of Shariah compliant equities and Islamic debt securities.

Asset Allocation Equity : 30% - 70% Sukuk/Cash : 30% - 70%

Fund Manager Investment Division of Syarikat Takaful Malaysia Berhad

Performance Benchmark Combination of

70% FBM Emas Shariah Index (FBMSI)

30% one-month return Maybank General Investment Account Rate (GIA)(source: FBMSI from Bloomberg, GIA from Maybank)

Fees & Charges Fund management fee

Max 1.5% of fund’s NAV per annum

Custodian fee 0.03% of fund’s NAV per annum

Risk Profile Moderate As the Fund’s investment involved marketable securities such as stocks and Islamic debt securities (IDS)/sukuk, the investors should be prepared to accept some interim price volatility. Investment in IDS carries some risks such as changes in interest rate and credit rating of the issuer. An increase in interest rate or downgrading of credit rating of the issuer would result to the fall in bond prices; hence impacted the performance of the Fund. The key risks for this Fund are market risk, interest rate risk, credit/default risk, specific security risk, liquidity risk, operational risk, reclassification of Shariah status risk. Please refer to Appendix 1 for further details.

Risk Management Proper asset allocation, diversification and liquidity management are among the methods can be adopted by the Fund Manager to manage the Fund risks. If there is high possibility that the equity market may fall, the exposure in equity investment would be reduced to a lower level and vice versa. In managing the investment risks for IDS, the Fund Manager will adopt extensive research and analysis on the issuer, credit rating, maturity factor, liquidity and selected yield measures. The Fund Manager will also constantly monitor the macro economic factors that may impact the interest rate environment.

Target Market The fund is no longer being offered for new investment.

Basis & Frequency of Unit Valuation Please refer to Appendix 2.

Exceptional Circumstances Please refer to Appendix 2.

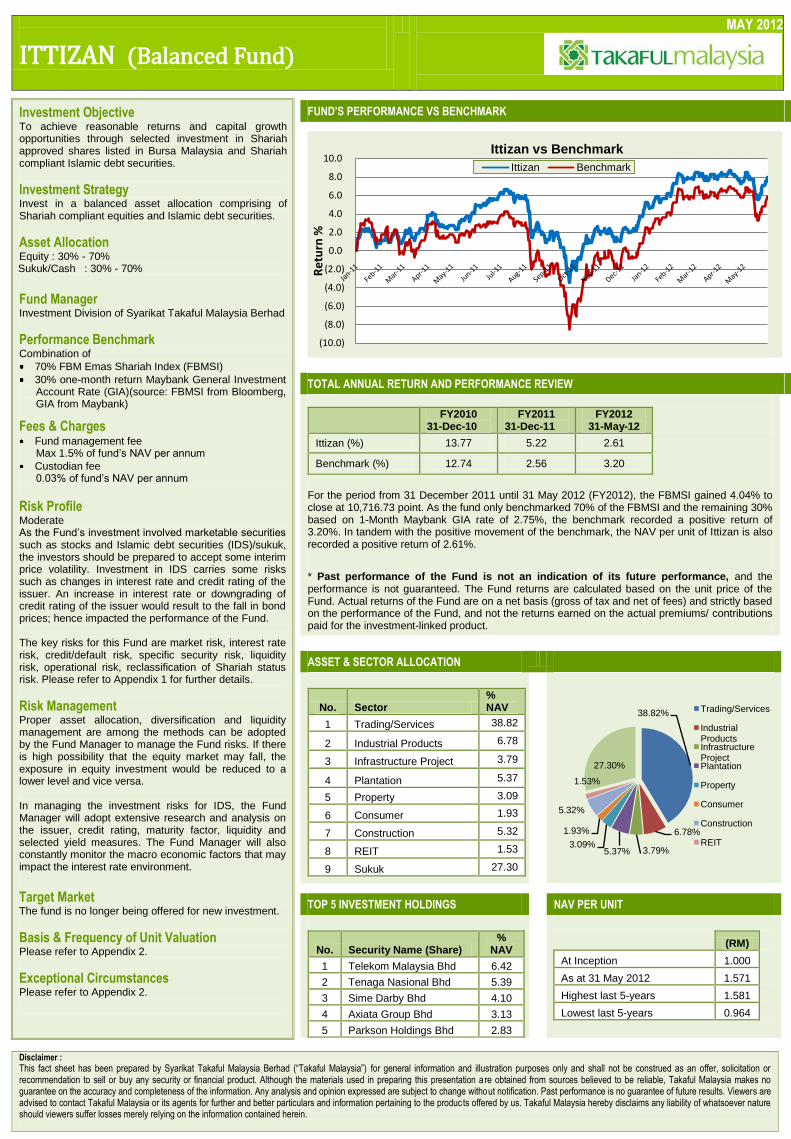

FUND’S PERFORMANCE VS BENCHMARK

TOTAL ANNUAL RETURN AND PERFORMANCE REVIEW

FY2010

31-Dec-10 FY2011

31-Dec-11 FY2012

31-May-12

Ittizan (%) 13.77 5.22 2.61

Benchmark (%) 12.74 2.56 3.20

For the period from 31 December 2011 until 31 May 2012 (FY2012), the FBMSI gained 4.04% to close at 10,716.73 point. As the fund only benchmarked 70% of the FBMSI and the remaining 30% based on 1-Month Maybank GIA rate of 2.75%, the benchmark recorded a positive return of 3.20%. In tandem with the positive movement of the benchmark, the NAV per unit of Ittizan is also recorded a positive return of 2.61%.

* Past performance of the Fund is not an indication of its future performance, and the performance is not guaranteed. The Fund returns are calculated based on the unit price of the Fund. Actual returns of the Fund are on a net basis (gross of tax and net of fees) and strictly based on the performance of the Fund, and not the returns earned on the actual premiums/ contributions paid for the investment-linked product.

ASSET & SECTOR ALLOCATION

No. Sector % NAV

1 Trading/Services 38.82

2 Industrial Products 6.78

3 Infrastructure Project 3.79

4 Plantation 5.37

5 Property 3.09

6 Consumer 1.93

7 Construction 5.32

8 REIT 1.53

9 Sukuk 27.30

TOP 5 INVESTMENT HOLDINGS NAV PER UNIT

No. Security Name (Share) %

NAV

1 Telekom Malaysia Bhd 6.42

2 Tenaga Nasional Bhd 5.39

3 Sime Darby Bhd 4.10

4 Axiata Group Bhd 3.13

5 Parkson Holdings Bhd 2.83

(RM)

At Inception 1.000

As at 31 May 2012 1.571

Highest last 5-years 1.581

Lowest last 5-years 0.964

Fund’s Performance vs Benchmark

Disclaimer :

This fact sheet has been prepared by Syarikat Takaful Malaysia Berhad (“Takaful Malaysia”) for general information and illustration purposes only and shall not be construed as an offer, solicitation or recommendation to sell or buy any security or financial product. Although the materials used in preparing this presentation are obtained from sources believed to be reliable, Takaful Malaysia makes no guarantee on the accuracy and completeness of the information. Any analysis and opinion expressed are subject to change without notification. Past performance is no guarantee of future results. Viewers are advised to contact Takaful Malaysia or its agents for further and better particulars and information pertaining to the products offered by us. Takaful Malaysia hereby disclaims any liability of whatsoever nature should viewers suffer losses merely relying on the information contained herein.

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

0.0

2.0

4.0

6.0

8.0

10.0

Re

turn

%

Ittizan vs Benchmark

Ittizan Benchmark

38.82%

6.78%

3.79%5.37%3.09%

1.93%

5.32%

1.53%

27.30%

Trading/Services

Industrial ProductsInfrastructure Project Plantation

Property

Consumer

Construction

REIT

ISTIQRAR (Stable Capital Fund)

MAY 2012

Investment Objective To achieve relatively stable pattern of investment returns over medium term trough selected investment in Shariah approved shares listed in Bursa Malaysia and Shariah-compliant fixed income securities.

Investment Strategy Invest in a balanced asset allocation comprising mainly in Islamic debt securities with smaller exposure in Shariah-compliant equity.

Asset Allocation Equity : up to 35% Sukuk/Cash : 65% - 100%

Fund Manager Investment Division of Syarikat Takaful Malaysia Berhad

Performance Benchmark Combination of

30% FBM Emas Shariah Index (FBMSI)

70% one-month return Maybank General Investment Account Rate (GIA)

(source: FBMSI from Bloomberg, GIA from Maybank)

Fees & Charges Fund management fee

Max 1.5% of fund’s NAV per annum

Custodian fee 0.03% of fund’s NAV per annum

Risk Profile Low As the Fund’s investment involved marketable securities such as stocks and Islamic debt securities (IDS)/sukuk, the investors should be prepared to accept some interim price volatility. Investment in IDS carries some risks such as changes in interest rate and credit rating of the issuer. An increase in interest rate or downgrading of credit rating of the issuer would result to the fall in bond prices; hence the impacted performance of the Fund. The key risks for this Fund are market risk, interest rate risk, credit/default risk, specific security risk, liquidity risk, operational risk, reclassification of Shariah status risk. Please refer to Appendix 1 for further details.

Risk Management Proper asset allocation, diversification and liquidity management are among the methods can be adopted by the Fund Manager to manage the Fund risks. If there is high possibility that the equity market may fall, the exposure in equity investment would be reduced to a lower level and vice versa. In managing the investment risks for IDS, the Fund Manager will adopt extensive research and analysis on the issuer, credit rating, maturity factor, liquidity and selected yield measures. The Fund Manager will also constantly monitor the macro economic factors that may impact the interest rate environment.

Target Market The fund is no longer being offered for new investment.

Basis & Frequency of Unit Valuation Please refer to Appendix 2.

Exceptional Circumstances Please refer to Appendix 2.

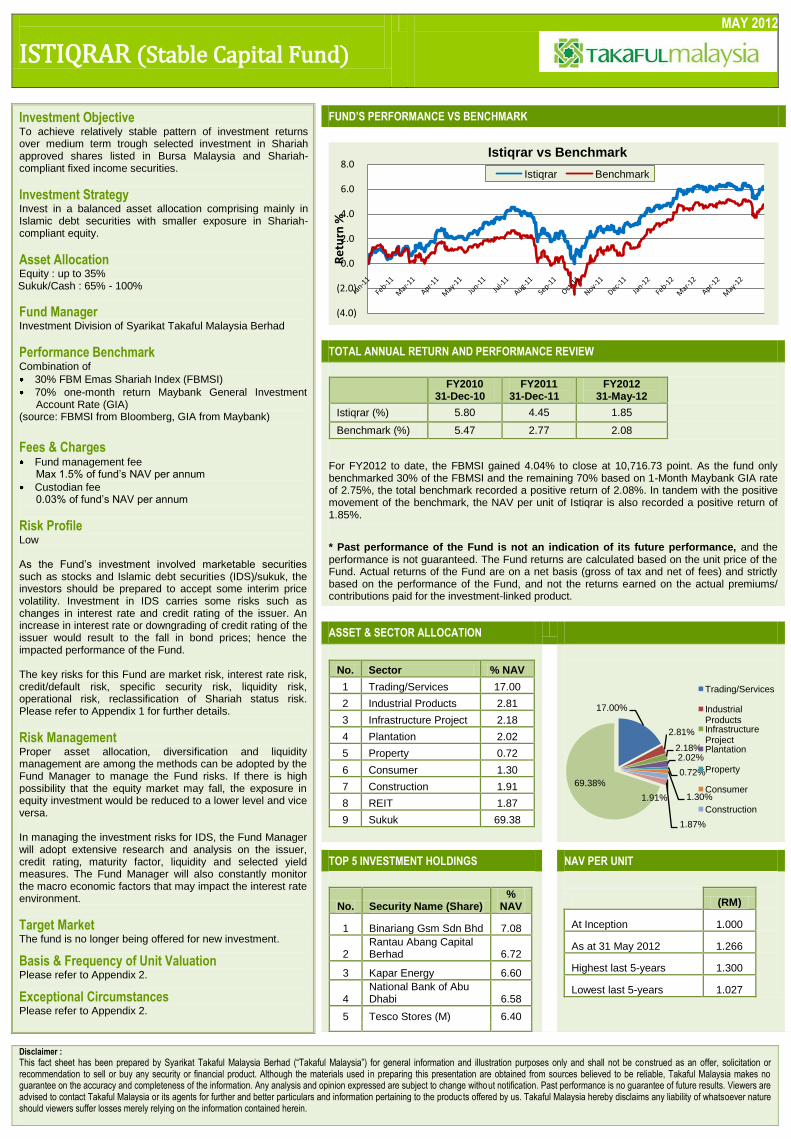

FUND’S PERFORMANCE VS BENCHMARK

TOTAL ANNUAL RETURN AND PERFORMANCE REVIEW

FY2010

31-Dec-10 FY2011

31-Dec-11 FY2012

31-May-12

Istiqrar (%) 5.80 4.45 1.85

Benchmark (%) 5.47 2.77 2.08

For FY2012 to date, the FBMSI gained 4.04% to close at 10,716.73 point. As the fund only benchmarked 30% of the FBMSI and the remaining 70% based on 1-Month Maybank GIA rate of 2.75%, the total benchmark recorded a positive return of 2.08%. In tandem with the positive movement of the benchmark, the NAV per unit of Istiqrar is also recorded a positive return of 1.85%.

* Past performance of the Fund is not an indication of its future performance, and the performance is not guaranteed. The Fund returns are calculated based on the unit price of the Fund. Actual returns of the Fund are on a net basis (gross of tax and net of fees) and strictly based on the performance of the Fund, and not the returns earned on the actual premiums/ contributions paid for the investment-linked product.

ASSET & SECTOR ALLOCATION

No. Sector % NAV

1 Trading/Services 17.00

2 Industrial Products 2.81

3 Infrastructure Project 2.18

4 Plantation 2.02

5 Property 0.72

6 Consumer 1.30

7 Construction 1.91

8 REIT 1.87

9 Sukuk 69.38

TOP 5 INVESTMENT HOLDINGS NAV PER UNIT

No. Security Name (Share) %

NAV

1 Binariang Gsm Sdn Bhd 7.08

2 Rantau Abang Capital Berhad 6.72

3 Kapar Energy 6.60

4 National Bank of Abu Dhabi 6.58

5 Tesco Stores (M) 6.40

(RM)

At Inception 1.000

As at 31 May 2012 1.266

Highest last 5-years 1.300

Lowest last 5-years 1.027

Fund’s Performance vs Benchmark

Disclaimer :

This fact sheet has been prepared by Syarikat Takaful Malaysia Berhad (“Takaful Malaysia”) for general information and illustration purposes only and shall not be construed as an offer, solicitation or recommendation to sell or buy any security or financial product. Although the materials used in preparing this presentation are obtained from sources believed to be reliable, Takaful Malaysia makes no guarantee on the accuracy and completeness of the information. Any analysis and opinion expressed are subject to change without notification. Past performance is no guarantee of future results. Viewers are advised to contact Takaful Malaysia or its agents for further and better particulars and information pertaining to the products offered by us. Takaful Malaysia hereby disclaims any liability of whatsoever nature should viewers suffer losses merely relying on the information contained herein.

(4.0)

(2.0)

0.0

2.0

4.0

6.0

8.0

Re

turn

%

Istiqrar vs Benchmark

Istiqrar Benchmark

17.00%

2.81%

2.18%2.02%

0.72%

1.30%1.91%

1.87%

69.38%

Trading/Services

Industrial ProductsInfrastructure Project Plantation

Property

Consumer

Construction

IHFAZ EQUITY INDEX FUND

MAY 2012

Investment Objective To achieve returns that tracks the performance of FBM Emas Shariah Index.

Investment Strategy Invest mainly in the top of the Index component stocks; closely tracking the movement of the Benchmark in the medium to long term;

Constant rebalancing of the component stocks to closely track the benchmark performance.

Asset Allocation Equity : 90% - 95% Money Market : 5% - 10%

Fund Manager Investment Division of Syarikat Takaful Malaysia Berhad

Performance Benchmark FBM Emas Shariah Index (FBMSI) (source : Bloomberg)

Fees & Charges Fund management fee

1.0% - 1.5% of fund’s NAV per annum

Custodian fee 0.03% of fund’s NAV per annum

Risk Profile Moderate As the Fund’s stock investment consist of the top forty of the index component stocks which including blue chip and growth stocks, the investors should be prepared to accept some interim price volatility with possibility of a severe downturn in the equity markets. The key risks for this Fund are market risk, specific security risk, liquidity risk, operational risk, reclassification of Shariah status risk. Please refer to Appendix 1 for further details.

Risk Management Proper asset allocation, diversification and liquidity management are among the methods can be adopted by the Fund Manager to manage the Fund risks such as market risk, specific security risk and liquidity risk. If there is high possibility that the equity market may fall, the exposure in equity investment would be reduced to a lower level and vice versa. The Fund Manager will also adopt a prudent investment selection process by investing in selected stock universe after undergoing some screening process.

Target Market Customers who prefer moderate risk investment profile with a moderate expected return.

Basis & Frequency of Unit Valuation Please refer to Appendix 2.

Exceptional Circumstances Please refer to Appendix 2.

Tracking Error (TE) TE is a measure of the deviation from the benchmark. It measures of how closely a portfolio follows the index to which it is benchmark. The closer its track the benchmark, the lesser is the amount of TE.

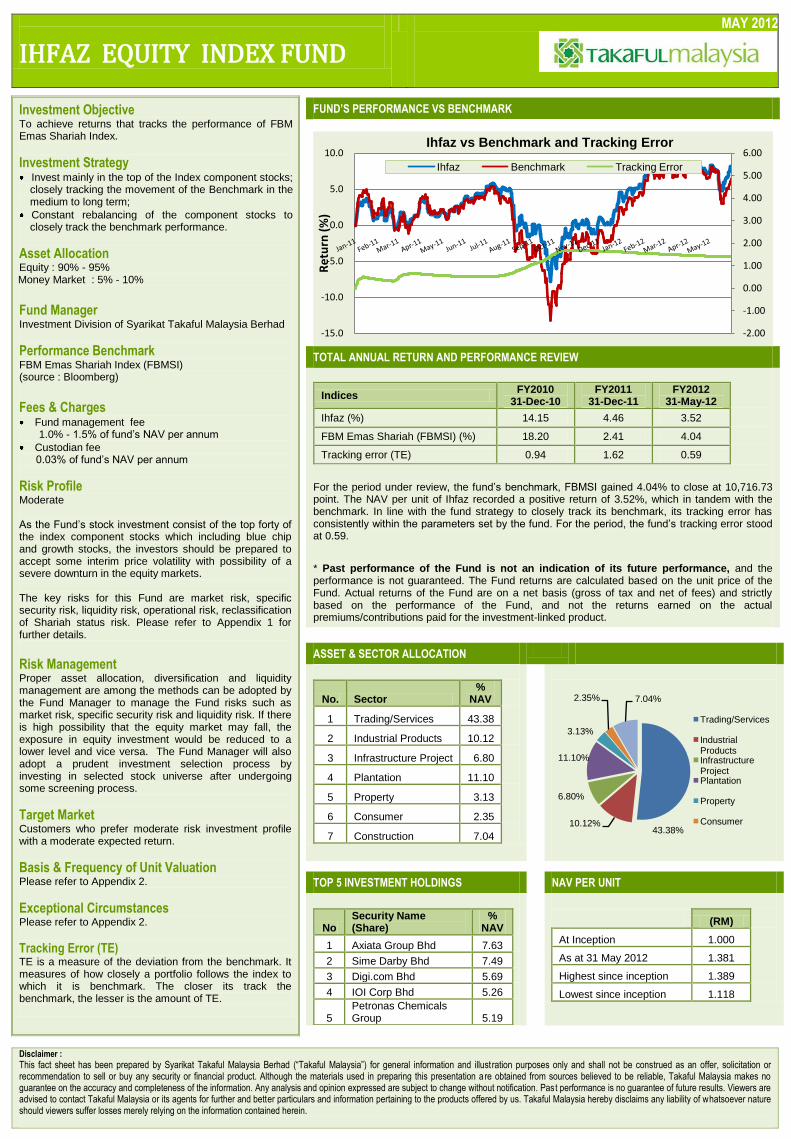

FUND’S PERFORMANCE VS BENCHMARK

TOTAL ANNUAL RETURN AND PERFORMANCE REVIEW

Indices FY2010

31-Dec-10 FY2011

31-Dec-11 FY2012

31-May-12

Ihfaz (%) 14.15 4.46 3.52

FBM Emas Shariah (FBMSI) (%) 18.20 2.41 4.04

Tracking error (TE) 0.94 1.62 0.59

For the period under review, the fund’s benchmark, FBMSI gained 4.04% to close at 10,716.73 point. The NAV per unit of Ihfaz recorded a positive return of 3.52%, which in tandem with the benchmark. In line with the fund strategy to closely track its benchmark, its tracking error has consistently within the parameters set by the fund. For the period, the fund’s tracking error stood at 0.59.

* Past performance of the Fund is not an indication of its future performance, and the performance is not guaranteed. The Fund returns are calculated based on the unit price of the Fund. Actual returns of the Fund are on a net basis (gross of tax and net of fees) and strictly based on the performance of the Fund, and not the returns earned on the actual premiums/contributions paid for the investment-linked product.

ASSET & SECTOR ALLOCATION

No. Sector %

NAV

1 Trading/Services 43.38

2 Industrial Products 10.12

3 Infrastructure Project 6.80

4 Plantation 11.10

5 Property 3.13

6 Consumer 2.35

7 Construction 7.04

TOP 5 INVESTMENT HOLDINGS NAV PER UNIT

No Security Name (Share)

% NAV

1 Axiata Group Bhd 7.63

2 Sime Darby Bhd 7.49

3 Digi.com Bhd 5.69

4 IOI Corp Bhd 5.26

5 Petronas Chemicals Group 5.19

(RM)

At Inception 1.000

As at 31 May 2012 1.381

Highest since inception 1.389

Lowest since inception 1.118

Fund’s Performance vs Benchmark

Disclaimer :

This fact sheet has been prepared by Syarikat Takaful Malaysia Berhad (“Takaful Malaysia”) for general information and illust ration purposes only and shall not be construed as an offer, solicitation or recommendation to sell or buy any security or financial product. Although the materials used in preparing this presentation are obtained from sources believed to be reliable, Takaful Malaysia makes no guarantee on the accuracy and completeness of the information. Any analysis and opinion expressed are subject to change without notification. Past performance is no guarantee of future results. Viewers are advised to contact Takaful Malaysia or its agents for further and better particulars and information pertaining to the products offered by us. Takaful Malaysia hereby disclaims any liability of whatsoever nature should viewers suffer losses merely relying on the information contained herein.

-2.00

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

-15.0

-10.0

-5.0

0.0

5.0

10.0

Re

turn

(%

)

Ihfaz vs Benchmark and Tracking Error

Ihfaz Benchmark Tracking Error

43.38%10.12%

6.80%

11.10%

3.13%

2.35% 7.04%

Trading/Services

Industrial ProductsInfrastructure Project Plantation

Property

Consumer

-15.0

-10.0

-5.0

0.0

5.0

10.0

Re

turn

(%

)

Ihfaz vs Benchmark and Tracking Error

Ihfaz Benchmark Tracking Error

ITTIHAD GROWTH FUND

MAY 2012

Investment Objective To achieve capital growth opportunities and dividend income through selective investments in Shariah approved shares listed in Bursa Malaysia.

Investment Strategy Invest primarily in selected Shariah compliant equities that comprise of a diversified portfolio of index-linked companies, blue-chip stocks and companies with growth prospects and attractive dividend yields that are listed on Bursa Malaysia;

Active portfolio management - constant review on asset allocation and stocks holding. Stock/portfolio turnover would be practically high in search for opportunities in capital gain and dividend yield stocks.

Asset Allocation Equity : 50% - 95% Cash/Sukuk : 5% - 50%

Fund Manager Investment Division of Syarikat Takaful Malaysia Berhad

Performance Benchmark FBM Emas Shariah Index (FBMSI) (source : Bloomberg)

Fees & Charges Fund management fee

1.0% - 1.5% of fund’s NAV per annum

Custodian fee 0.03% of fund’s NAV per annum

Risk Profile High Since the fund investment also consist of growth stocks which are normally more volatile in prices as compared to blue chips and high dividend yield stocks, the investors should be prepared to accept some interim price volatility, of which sometimes can be significant to achieve that higher return. The key risks for this Fund are market risk, specific security risk, interest rate risk, credit/default risk, liquidity risk, operational risk, reclassification of Shariah status risk. Please refer to Appendix 1 for further details.

Risk Management Proper asset allocation, diversification and liquidity management are among the methods can be adopted by the Fund Manager to manage the Fund risks. If there is high possibility that the equity market may fall, the exposure in equity investment would be reduced to a lower level and vice versa. The Fund Manager will also adopt a prudent investment selection process by investing in selected stock universe after undergoing some screening process. In managing the investment risks for IDS, the Fund Manager will adopt extensive research and analysis on the issuer, credit rating, maturity factor, liquidity and selected yield measures. The Fund Manager will also constantly monitor the macro economic factors that may impact the interest rate environment.

Target Market Customers who prefer a high risk investment profile with a high expected return.

Basis & Frequency of Unit Valuation Please refer to Appendix 2.

Exceptional Circumstances Please refer to Appendix 2.

FUND’S PERFORMANCE VS BENCHMARK

TOTAL ANNUAL RETURN AND PERFORMANCE REVIEW

FY2010

31-Dec-10 FY2011

31-Dec-11 FY2012

31-May-12

Ittihad (%) 7.71 3.23 0.63

FBM Emas Shariah (FBMSI) (%) 18.20 2.41 4.04

For the period under review, the fund’s benchmark, FBMSI gained 4.04% to close at 10,716.73 point. In tandem with the positive movement of the benchmark, the NAV per unit of Ittihad also recorded a positive return of 0.63%.

* Past performance of the Fund is not an indication of its future performance, and the performance is not guaranteed. The Fund returns are calculated based on the unit price of the Fund. Actual returns of the Fund are on a net basis (gross of tax and net of fees) and strictly based on the performance of the Fund, and not the returns earned on the actual premiums/ contributions paid for the investment-linked product.

ASSET & SECTOR ALLOCATION

No. Sector %

NAV

1 Trading/Services 43.35

2 Industrial Products 6.31

3 Infrastructure Project 3.94

4 Plantation 9.64

5 Property 5.84

6 Construction 7.86

7 Consumer 2.31

TOP 5 INVESTMENT HOLDINGS NAV PER UNIT

No. Security Name (Share) %

NAV

1 Axiata Group Bhd 5.51

2 Tenaga Nasional Bhd 5.17

3 Sapura Kencana Petroleum Bhd 4.74

4 Telekom Malaysia Bhd 4.24

5 Kuala Lumpur Kepong 3.88

(RM)

At Inception 1.000

As at 31 May 2012 1.126

Highest since inception 1.161

Lowest since inception 0.972

Fund’s Performance vs Benchmark

Disclaimer :

This fact sheet has been prepared by Syarikat Takaful Malaysia Berhad (“Takaful Malaysia”) for general information and illustration purposes only and shall not be construed as an offer, solicitation or recommendation to sell or buy any security or financial product. Although the materials used in preparing this presentation are obtained from sources believed to be reliable, Takaful Malaysia makes no guarantee on the accuracy and completeness of the information. Any analysis and opinion expressed are subject to change without notification. Past performance is no guarantee of future results. Viewers are advised to contact Takaful Malaysia or its agents for further and better particulars and information pertaining to the products offered by us. Takaful Malaysia hereby disclaims any liability of whatsoever nature should viewers suffer losses merely relying on the information contained herein.

-15.0

-10.0

-5.0

0.0

5.0

10.0

Re

turn

(%

)

Ittihad vs Benchmark Ittihad Benchmark

43.35%6.31%3.94%

9.64%

5.84%

7.86%2.31%

Trading/Services

Industrial ProductsInfrastructure Project Plantation

Property

Construction

ISTIFAD BLUE CHIPS FUND

MAY 2012

Investment Objective To achieve consistent capital growth in the long run through investments in Shariah Compliant Blue Chip Shares.

Investment Strategy Invest primarily in Shariah compliant equities with higher market capitalisation to achieve long term capital growth;

Active portfolio management - constant review on asset allocation and stock holding in search of stocks that meet the objective of the Fund.

Asset Allocation Equity : 40% - 90% Money Market : 10% - 60%

Fund Manager Investment Division of Syarikat Takaful Malaysia Berhad

Performance Benchmark FBM Emas Shariah Index (FBMSI) (source : Bloomberg)

Fees & Charges Fund management fee

1.0% - 1.5% of fund’s NAV per annum

Custodian fee 0.03% of fund’s NAV per annum

Risk Profile Moderate As the Fund’s stock investment focus mainly in blue chip stocks whose prices normally do not fluctuate as much as growth stocks, the investors should be willing to accept some moderate growth in principal. The key risks for this Fund are market risk, specific security risk, liquidity risk, operational risk, reclassification of Shariah status risk. Please refer to Appendix 1 for further details.

Risk Management Proper asset allocation, diversification and liquidity management are among the methods can be adopted by the Fund Manager to manage the Fund risks. If there is high possibility that the equity market may fall, the exposure in equity investment would be reduced to a lower level and vice versa. The Fund Manager will also adopt a prudent investment selection process by investing in selected stock universe after undergoing some screening process.

Target Market Customers who prefer moderate risk investment profile with a high expected return.

Basis & Frequency of Unit Valuation Please refer to Appendix 2.

Exceptional Circumstances Please refer to Appendix 2.

FUND’S PERFORMANCE VS BENCHMARK

TOTAL ANNUAL RETURN AND PERFORMANCE REVIEW

FY2010

31-Dec-10 FY2011

31-Dec-11 FY2012

31-May-12

Istifad (%) 7.01 2.23 2.36

FBM Emas Shariah (FBMSI) (%) 18.20 2.41 4.04

For the period under review, the fund’s benchmark, FBMSI gained 4.04% to close at 10,716.73 point. In tandem with the positive movement of the benchmark, the NAV per unit of Istifad is also recorded a positive return of 2.36%.

* Past performance of the Fund is not an indication of its future performance, and the performance is not guaranteed. The Fund returns are calculated based on the unit price of the Fund. Actual returns of the Fund are on a net basis (gross of tax and net of fees) and strictly based on the performance of the Fund, and not the returns earned on the actual premiums/ contributions paid for the investment-linked product.

ASSET & SECTOR ALLOCATION

No. Sector %

NAV

1 Trading/Services 41.10

2 Industrial Products 7.49

3 Infrastructure Project 4.73

4 Plantation 8.29

5 Property 6.05

6 Consumer 3.04

7 Construction 8.18

TOP 5 INVESTMENT HOLDINGS NAV PER UNIT

No. Security Name (Share)

% NAV

1 Tenaga Nasional Bhd 6.34

2 Telekom Malaysia Bhd 5.14

3 Petronas Chemicals Group Bhd 5.09

4 Sime Darby Bhd 4.66

5 Kuala Lumpur Kepong 4.53

(RM)

At Inception 1.000

As at 31 May 2012 1.127

Highest since inception 1.138

Lowest since inception 0.975

Fund’s Performance vs Benchmark

Disclaimer :

This fact sheet has been prepared by Syarikat Takaful Malaysia Berhad (“Takaful Malaysia”) for general information and illust ration purposes only and shall not be construed as an offer, solicitation or recommendation to sell or buy any security or financial product. Although the materials used in preparing this presentation are obtained from sources believed to be reliable, Takaful Malaysia makes no guarantee on the accuracy and completeness of the information. Any analysis and opinion expressed are subject to change without notification. Past performance is no guarantee of future results. Viewers are advised to contact Takaful Malaysia or its agents for further and better particulars and information pertaining to the products offered by us. Takaful Malaysia hereby disclaims any liability of whatsoever nature should viewers suffer losses merely relying on the information contained herein.

-15.0

-10.0

-5.0

0.0

5.0

10.0

Re

turn

(%

)

Istifad vs Benchmark

Istifad Benchmark

41.10%7.49%

4.73%

8.29%

6.05%

3.04%

8.18%Trading/Services

Industrial ProductsInfrastructure Project Plantation

Property

Consumer

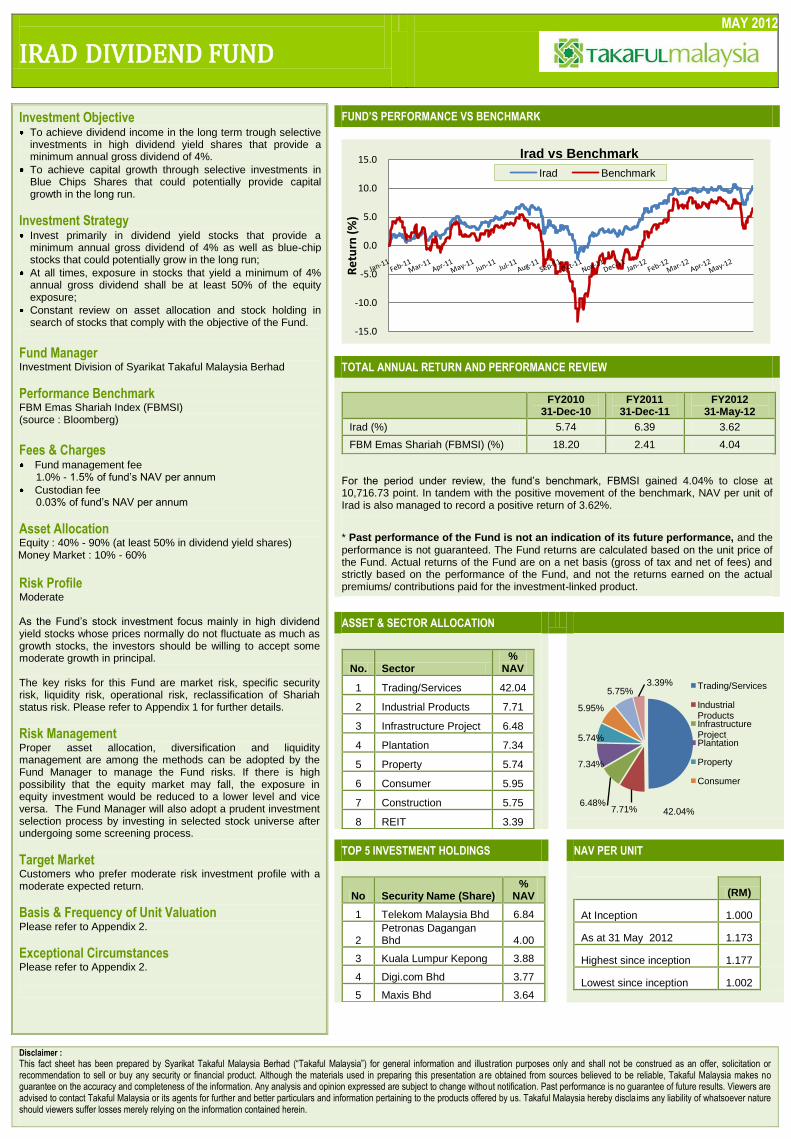

IRAD DIVIDEND FUND

MAY 2012

Investment Objective To achieve dividend income in the long term trough selective investments in high dividend yield shares that provide a minimum annual gross dividend of 4%.

To achieve capital growth through selective investments in Blue Chips Shares that could potentially provide capital growth in the long run.

Investment Strategy Invest primarily in dividend yield stocks that provide a minimum annual gross dividend of 4% as well as blue-chip stocks that could potentially grow in the long run;

At all times, exposure in stocks that yield a minimum of 4% annual gross dividend shall be at least 50% of the equity exposure;

Constant review on asset allocation and stock holding in search of stocks that comply with the objective of the Fund.

Fund Manager Investment Division of Syarikat Takaful Malaysia Berhad

Performance Benchmark FBM Emas Shariah Index (FBMSI) (source : Bloomberg)

Fees & Charges Fund management fee

1.0% - 1.5% of fund’s NAV per annum

Custodian fee 0.03% of fund’s NAV per annum

Asset Allocation Equity : 40% - 90% (at least 50% in dividend yield shares) Money Market : 10% - 60%

Risk Profile Moderate As the Fund’s stock investment focus mainly in high dividend yield stocks whose prices normally do not fluctuate as much as growth stocks, the investors should be willing to accept some moderate growth in principal. The key risks for this Fund are market risk, specific security risk, liquidity risk, operational risk, reclassification of Shariah status risk. Please refer to Appendix 1 for further details.

Risk Management Proper asset allocation, diversification and liquidity management are among the methods can be adopted by the Fund Manager to manage the Fund risks. If there is high possibility that the equity market may fall, the exposure in equity investment would be reduced to a lower level and vice versa. The Fund Manager will also adopt a prudent investment selection process by investing in selected stock universe after undergoing some screening process.

Target Market Customers who prefer moderate risk investment profile with a moderate expected return.

Basis & Frequency of Unit Valuation Please refer to Appendix 2.

Exceptional Circumstances Please refer to Appendix 2.

FUND’S PERFORMANCE VS BENCHMARK

TOTAL ANNUAL RETURN AND PERFORMANCE REVIEW

FY2010

31-Dec-10 FY2011

31-Dec-11 FY2012

31-May-12

Irad (%) 5.74 6.39 3.62

FBM Emas Shariah (FBMSI) (%) 18.20 2.41 4.04

For the period under review, the fund’s benchmark, FBMSI gained 4.04% to close at 10,716.73 point. In tandem with the positive movement of the benchmark, NAV per unit of Irad is also managed to record a positive return of 3.62%.

* Past performance of the Fund is not an indication of its future performance, and the performance is not guaranteed. The Fund returns are calculated based on the unit price of the Fund. Actual returns of the Fund are on a net basis (gross of tax and net of fees) and strictly based on the performance of the Fund, and not the returns earned on the actual premiums/ contributions paid for the investment-linked product.

ASSET & SECTOR ALLOCATION

No. Sector %

NAV

1 Trading/Services 42.04

2 Industrial Products 7.71

3 Infrastructure Project 6.48

4 Plantation 7.34

5 Property 5.74

6 Consumer 5.95

7 Construction 5.75

8 REIT 3.39

TOP 5 INVESTMENT HOLDINGS NAV PER UNIT

No Security Name (Share) %

NAV

1 Telekom Malaysia Bhd 6.84

2 Petronas Dagangan Bhd 4.00

3 Kuala Lumpur Kepong 3.88

4 Digi.com Bhd 3.77

5 Maxis Bhd 3.64

(RM)

At Inception 1.000

As at 31 May 2012 1.173

Highest since inception 1.177

Lowest since inception 1.002

Fund’s Performance vs Benchmark

Disclaimer :

This fact sheet has been prepared by Syarikat Takaful Malaysia Berhad (“Takaful Malaysia”) for general information and illust ration purposes only and shall not be construed as an offer, solicitation or recommendation to sell or buy any security or financial product. Although the materials used in preparing this presentation are obtained from sources believed to be reliable, Takaful Malaysia makes no guarantee on the accuracy and completeness of the information. Any analysis and opinion expressed are subject to change without notification. Past performance is no guarantee of future results. Viewers are advised to contact Takaful Malaysia or its agents for further and better particulars and information pertaining to the products offered by us. Takaful Malaysia hereby discla ims any liability of whatsoever nature should viewers suffer losses merely relying on the information contained herein.

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

Re

turn

(%

)

Irad vs Benchmark

Irad Benchmark

42.04%7.71%6.48%

7.34%

5.74%

5.95%

5.75%3.39% Trading/Services

Industrial ProductsInfrastructure Project Plantation

Property

Consumer

IHSAN BALANCED FUND

MAY 2012

Investment Objective To achieve moderate streams of income and consistent capital growth over the medium-to-long term period by investing in a diversified portfolio of investments;

To construct a diversified portfolio containing a balanced mixture of equities and fixed income securities.

Investment Strategy Invest in a balanced asset allocation comprising of Shariah-compliant equity, debt securities and money market.

Asset Allocation Equity : 10% - 40% Sukuk/cash : 10% - 60%

Fund Manager Investment Division of Syarikat Takaful Malaysia Berhad

Performance Benchmark Combination of

40% FBM Emas Shariah Index (FBMSI)

60% 12-month return Maybank General Investment Account Rate (GIA) (source: FBMSI from Bloomberg, GIA from Maybank)

Fees & Charges Fund management fee :

1.0% - 1.2% of fund’s NAV per annum

Custodian fee : 0.03% of fund’s NAV per annum

Risk Profile Low As the Fund’s investment involved marketable securities such as stocks and Islamic debt securities (IDS), the investors should be prepared to accept some interim price volatility. Investment in IDS carries some risks such as changes in interest rate and credit rating of the issuer. An increase in interest rate or downgrading of credit rating of the issuer would result to the fall in bond prices; hence impacted the performance of the Fund. The key risks for this Fund are market risk, interest rate risk, credit/default risk, specific security risk, liquidity risk, operational risk, reclassification of Shariah status risk. Please refer to Appendix 1 for further details.

Risk Management Proper asset allocation, diversification and liquidity management are among the methods can be adopted by the Fund Manager to manage the Fund risks. If there is high possibility that the equity market may fall, the exposure in equity investment would be reduced to a lower level and vice versa. In managing the investment risks for IDS, the Fund Manager will adopt extensive research and analysis on the issuer, credit rating, maturity factor, liquidity and selected yield measures. The Fund Manager will also constantly monitor the macro economic factors that may impact the interest rate environment. Target Market Customers who prefer a moderate risk investment profile with a moderate expected return.

Basis & Frequency of Unit Valuation Please refer to Appendix 2.

Exceptional Circumstances Please refer to Appendix 2.

FUND’S PERFORMANCE VS BENCHMARK

TOTAL ANNUAL RETURN AND PERFORMANCE REVIEW

FY2011

31-Dec-11 FY2012

31-May-12

Ihsan (%) 2.56 1.54

Benchmark (%) 2.81 2.41

For the period under review, FBMSI gained 4.04%. Being the balanced fund, the fund only benchmarked 40% of the FBMSI and the remaining 60% based on 12-Months Maybank GIA rate of 3.19%, hence the total benchmark recorded a return of 2.41%. In tandem with the positive movement of FBMSI, the NAV performance of Ihsan is also recorded a positive return of 1.54%.

* Past performance of the Fund is not an indication of its future performance, and the performance is not guaranteed. The Fund returns are calculated based on the unit price of the Fund. Actual returns of the Fund are on a net basis (gross of tax and net of fees) and strictly based on the performance of the Fund, and not the returns earned on the actual premiums/ contributions paid for the investment-linked product.

ASSET & SECTOR ALLOCATION

No. Sector % NAV

1 Trading/Services 17.08

2 Industrial Products 4.10

3 Infrastructure Project 2.87

4 Plantation 4.21

5 Property 2.00

6 Construction 2.87

7 Consumer 2.33

8 Sukuk 54.66

TOP 5 INVESTMENT HOLDINGS NAV PER UNIT

No Security Name (Sukuk/bond) %

NAV

1 Binariang GSM Sdn Bhd 7.48

2 Padiberas Nasional Bhd 6.97

3 National Bank of Abu Dhabi 6.96

4 Projek Lebuhraya Usahasama Bhd 6.95

5 Lingkaran Trans Kota Sdn Bhd 6.81

(RM)

At Inception 1.000

As at 31 May 2012 1.056

Highest since inception 1.062

Lowest since inception 0.996

Fund’s Performance vs Benchmark

Disclaimer :

This fact sheet has been prepared by Syarikat Takaful Malaysia Berhad (“Takaful Malaysia”) for general information and illustration purposes only and shall not be construed as an offer, solicitation or recommendation to sell or buy any security or financial product. Although the materials used in preparing this presentation are obtained from sources believed to be reliable, Takaful Malaysia makes no guarantee on the accuracy and completeness of the information. Any analysis and opinion expressed are subject to change without notification. Past performance is no guarantee of future results. Viewers are advised to contact Takaful Malaysia or its agents for further and better particulars and information pertaining to the products offered by us. Takaful Malaysia hereby disclaims any liability of whatsoever nature should viewers suffer losses merely relying on the information contained herein.

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

Re

turn

(%

)

Ihsan vs Benchmark

Ihsan Benchmark

17.08%

4.10%

2.87%

4.21%

2.00%

2.87%2.33%

54.66%Trading/Services

Industrial ProductsInfrastructure Project Plantation

Property

Construction

Consumer

Appendix 1 MAY 2012

Definition of Risks and Risk Management Techniques

1. Market risk

Refers to potential impact arising from adverse price movements that affects the market values of the investments due to changes in economic

cycles, financial market conditions, currency and interest rate. The risk may also arise due to changes in any political and regulatory forms.

Market risk is managed through portfolio diversification and asset allocation whereby the securities exposure is monitored / reduced in the event of

anticipated market weaknesses.

2. Liquidity risk

Refers to potential impact of not being able to convert Shariah compliant investment into cash at or near its fair value, which primarily depends on the

volume traded for that particular Shariah compliant investments in the market.

The investment policy is to always maintain a prudent level of liquid assets so as to reduce liquidity risk.

3. Interest rate risk

Refers to potential impact affecting the market values of investment into Islamic debt securities arising from adverse movement in interest rates.

When interest rate rise, the value of Islamic debt securities fall and vice versa, thus affecting the market value of the fund. Although the fund does not

invest in conventional bonds, any changes in interest rate trend could also affect the price and yield of Islamic debt securities as conventional interest

rate is generally used as indicative rate to determine the profit rate for the Islamic debt securities.

In managing the risks, the Fund Manager will adopt an active investment management by constantly review the fund’s strategy and portfolio.

4. Credit/Default risk

Refers to potential decrease in credit worthiness of the issuers for Islamic debt investments in the event that the issuer is faced with unexpected

financial difficulties. In the worst case scenario, the issuer may default in the payment of principal and profits for the Islamic debt securities issued,

decreasing the prices and value of that particular Islamic debt securities and thus affecting the market value of the fund.

The Fund Manager manages the risk by setting internal counterparty limits and undertaking internal credit evaluation to minimise such risk.

5. Specific security risk

Refers to the risk of individual security including stock or Islamic debt security invested in the portfolio. A major price change of any particular security,

which is a component of the fund’s portfolio, would affect the NAV and daily prices of the Fund.

The mechanism employed to minimize the risk is through the process of portfolio diversification and prudent investment selection process by the

Fund Manager.

6. Operational risk

Refers to the risk that the Company fails to fulfill its obligation or perform other required actions because of inadequate policies and procedures,

human resources, information systems or internal control.

To minimize the risks, the Fund Manager will work with the Fund‘s Trustee, internal compliance unit and other divisions to ensure compliance with all

relevant legislations and policies and procedures are put in place at all the time.

7. Reclassification of Shariah status risk

Refers to potential revision on the status of Shariah compliant securities in the fund to become non-Shariah compliant in the periodic review by the

SAC.

The Fund Manager will take the necessary steps to dispose such securities in accordance with the advice from the SAC and the Shariah Advisor.

The Fund Manager will manage the investment-linked funds according to the fund strategy and target asset allocation policy. Nevertheless, the Fund Manager

may take temporary steps which may not be consistent with the stated strategy and asset allocation policy in attempting to respond to adverse market,

economic conditions.

Fund’s Performance vs Benchmark

Appendix 2

MAY 2012

Basis & Frequency of Unit Valuation The Unit Price on any Valuation Date of the Investment Linked Fund shall be obtained by dividing the NAV on the business day before the Valuation Date by

the number of Units in issue of the Investment Linked Fund.

In order to determine the Unit Price of each Unit on a Valuation Date, the Net Asset Value (NAV) of the Fund shall be calculated as follows:

(a) the amount for which in the opinion of the Company after taking such independent advice as they consider appropriate, the investments of the

Investment Linked Fund could be transacted in the open market on the Valuation Date by reference where applicable to the market dealing prices

quoted on a recognized stock exchange selected by the Company with the addition of expenses which would be incurred, plus

(b) in respect of the interests in the nature of land and other securities or properties of whatsoever nature held in the Investment Linked Fund the amount

which in the opinion of the Company after taking such independent advice as they consider appropriate is the value of such interests on the Valuation

Date with the addition of the expenses which would be incurred if such interests were transacted on the day, plus

(c) the amount of cash held uninvested in the Investment Linked Fund on the Valuation Date, less

(d) the amount (if any) which the Company shall determine on the Valuation Date shall be treated as liabilities of the Investment Linked Fund, less

(e) such amount as the Company shall consider to be just and equitable in respect of costs of valuation of any interests in the nature of land which are

comprised in the Investment Linked Fund and other expenses and outgoings properly attributable to such interest, less

(f) the applicable Fund Management Charge

There shall be deductions from the Investment Linked Fund of such amounts as the Company in its absolute discretion considers appropriate, as due

allowances for any levy, tax, duties or any other charges of whatsoever nature arising in respect of which the Fund may become liable.

To ensure fair treatment to all certificate owners of the fund, the Company may impute the transaction costs of acquiring or disposing of assets of the fund, if the

costs are significant. To recoup the cost of acquiring and disposing of assets, the company may make a dilution or transaction cost adjustment to the NAV per

unit to recover any amount which the fund had already paid or reasonably expects to pay for the creation or cancellation of units.

The Investment-linked Funds are valued on each business day. However, the Company may alter the frequency and date on which the Unit Price shall be

calculated by giving three (3) calendar months prior written notice to the Certificate Owner.

Exceptional Circumstances The Company reserves the right to take the following actions that may become necessary due to change of circumstances, as a means to protect the interest of

the certificate owner.

Subject to at least three (3) months written notice, the Company may:

(a) close any of the Unit Fund or cease to allow the allocation of additional Contribution or to transfer the assets to a new fund which has similar

investment objectives;

(b) change the name of the Unit Funds;

(c) split or combine existing units of Unit Funds;

(d) make any changes that may be required due to regulatory requirement and/or the legislation.

The Company may also choose to, without prior notice, suspend unit pricing and Certificate transactions if any of the exchanges in which the Unit Fund is

invested is temporarily suspended for trading;

In circumstances considered by the Company in its absolute discretion, to be prejudicial to the interests of participants, the Company reserves the right to

defer Partial Withdrawal and Surrender payment for a period not exceeding six (6) months from the date of redemption.

Issued by Syarikat Takaful Malaysia Berhad

Syarikat Takaful Malaysia Berhad was incorporated on 29 November 1984 and commenced operations in July 1985. It has an authorised capital of RM500 Million and a

paid up capital of RM162 Million. The Company was listed on the Main Board of the Malaysian Stock Exchange on 30 July 1996. In accordance with the Takaful Act 1984,

Syarikat Takaful Malaysia Berhad provides two types of Takaful business namely Family Takaful Business and General Takaful Business. Syarikat Takaful Malaysia

Berhad has 23 branches, 10 Takaful myCare Centres, 1 Retail Centre and 6 Takaful myDesks nationwide with total assets of RM4.9 Billion at Group level.

Tel : 603 - 2268 1984, 1300-8-TAKAFUL(825 2385)

Fax : 603 - 2274 0237

Email : [email protected] Website : takaful-malaysia.com.my

Fund’s Performance vs Benchmark