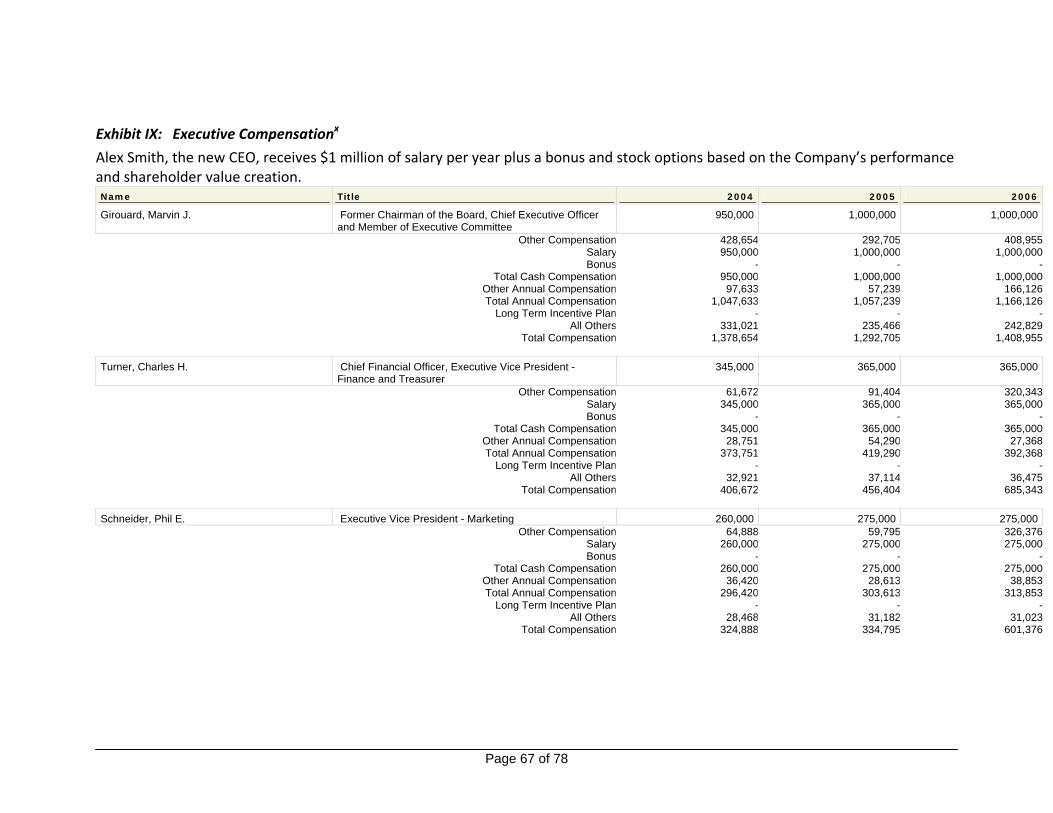

it’s your thing - Turnaround Management Association · · 2007-09-18Marketing Led Strategy ......

78

Company Analysis and Restructuring Plan MGMT 7711‐001 Turnaround Management Professor Laura Resnikoff Columbia Business School Hamid Benbrahim Rich Bozutto Laurent Grossi Geoff Teillon John Ure Originally Submitted: April 30, 2007 Revised: May 30, 2007 it’s your thing

Transcript of it’s your thing - Turnaround Management Association · · 2007-09-18Marketing Led Strategy ......

Company Analysis and Restructuring Plan

MGMT 7711‐001 Turnaround Management Professor Laura Resnikoff Columbia Business School

Hamid Benbrahim Rich Bozutto Laurent Grossi Geoff Teillon John Ure

Originally Submitted: April 30, 2007

Revised: May 30, 2007

it’s your thing

Page 2 of 78

Table of Contents

Executive Summary ............................................................................................................................ 4 Overview....................................................................................................................................... 4 Structure of this paper ................................................................................................................... 4 Recommendations ......................................................................................................................... 5 Summary of financial analysis and valuation .................................................................................... 5

Industry outlook and competitive environment .................................................................................... 7 Industry overview and definition..................................................................................................... 7 Furniture Stores............................................................................................................................. 7 Miscellaneous Home Furnishing Stores............................................................................................ 7 Retail Economics............................................................................................................................ 8

Business ............................................................................................................................................ 9 Company overview ........................................................................................................................ 9 Strategy and operations ............................................................................................................... 11 History ........................................................................................................................................ 13 Pricing......................................................................................................................................... 13 Analysis of Historic Annual Letters from CEO.................................................................................. 13 Primal Code Branding Analysis ...................................................................................................... 20 SWOT Analysis............................................................................................................................. 22 Recent Events.............................................................................................................................. 23

Management and governance........................................................................................................... 25 Executive officers and key employees............................................................................................ 25 Board of directors ........................................................................................................................ 27

Discussion of financial condition........................................................................................................ 31 Historic Stock Performance........................................................................................................... 31 Company Financial Performance ................................................................................................... 35 Liquidity Analysis ......................................................................................................................... 40 Ratings Analysis ........................................................................................................................... 41 Capital Structure.......................................................................................................................... 41 Debt Instruments......................................................................................................................... 42 Operating Lease Obligations ......................................................................................................... 43

Discussion of valuations.................................................................................................................... 45 Liquidation value ......................................................................................................................... 45

Discussion of Alternatives ................................................................................................................. 47 Status quo ................................................................................................................................... 47 Cost Savings Strategy ................................................................................................................... 48 Bankruptcy .................................................................................................................................. 48 Marketing Led Strategy ................................................................................................................ 49

Recommendations ........................................................................................................................... 50 Immediate Action Plan ................................................................................................................. 50 Projected Results ......................................................................................................................... 52

Conclusion ....................................................................................................................................... 55

Page 3 of 78

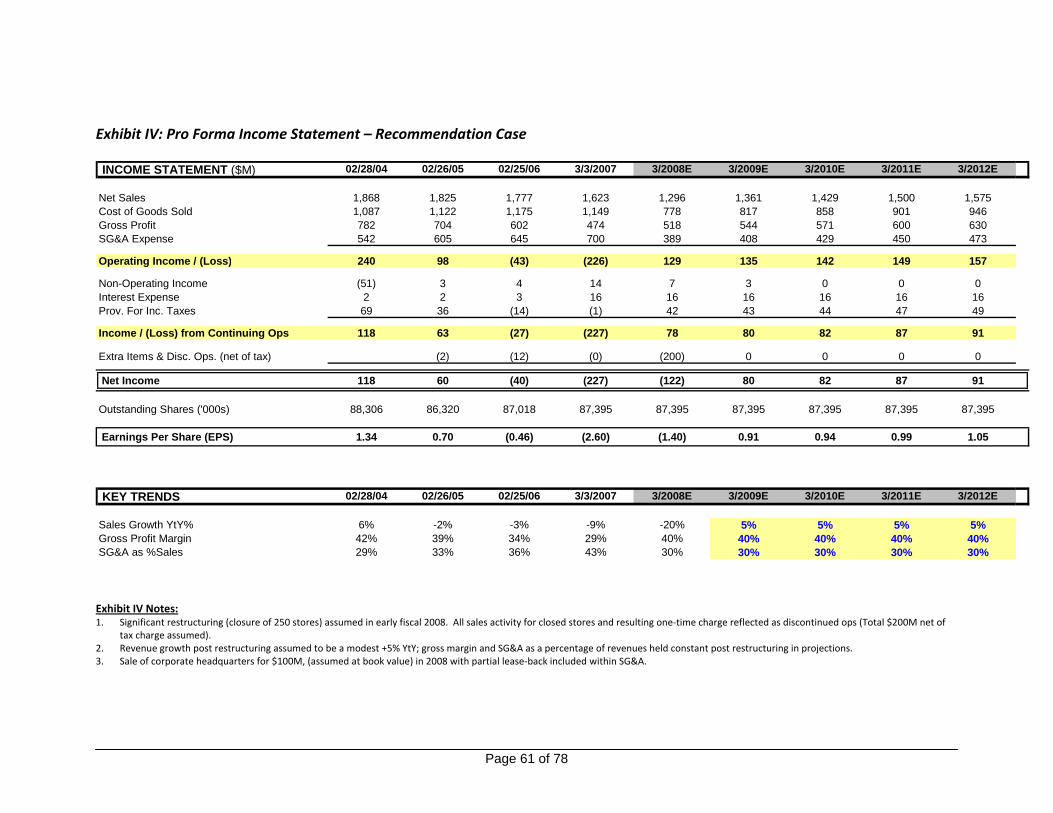

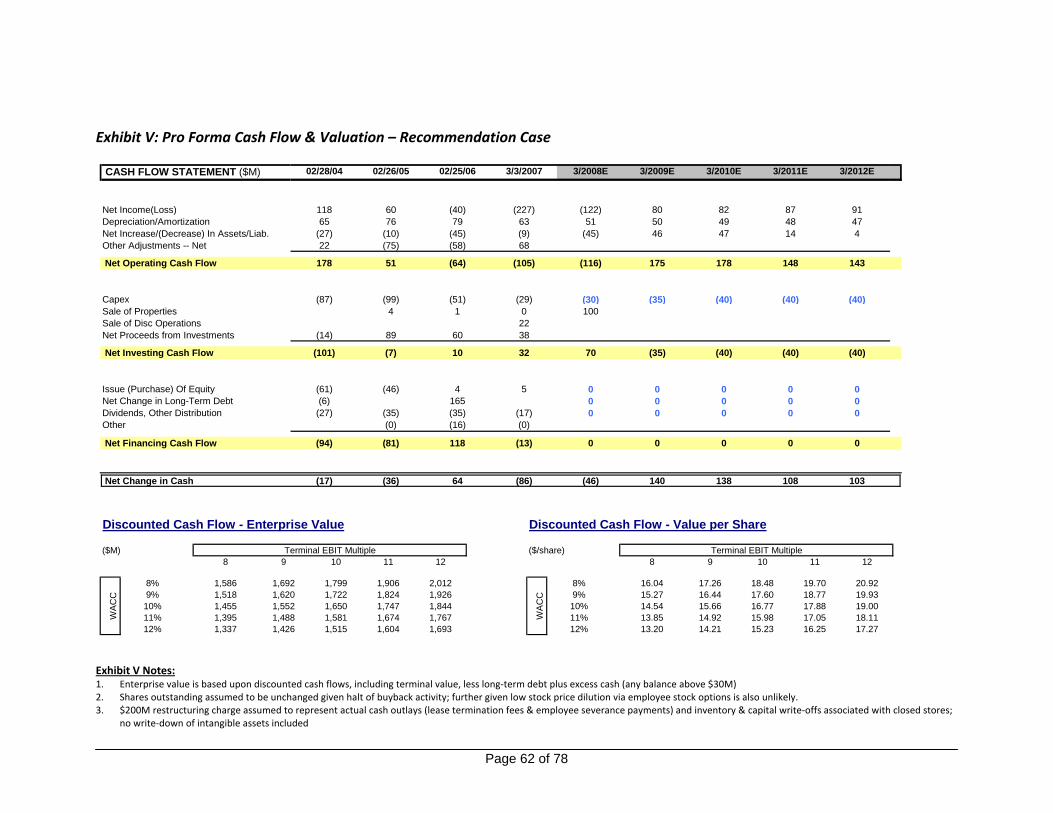

Exhibits ........................................................................................................................................... 56 Exhibit I: Current Market Expectations ‐ Income Statement............................................................. 56 Exhibit II: Current Market Expectations – Cash Flow & Estimated Valuation...................................... 57 Exhibit II (Continued): Estimated Valuation .................................................................................... 58 Exhibit III: Current Market Expectations – Balance Sheet................................................................. 59 Exhibit III Continued: Non‐GAAP Presentation of Key Financials – Current Market Expectations Scenario................................................................................................................................................... 60 Exhibit IV: Pro Forma Income Statement – Recommendation Case .................................................. 61 Exhibit V: Pro Forma Cash Flow & Valuation – Recommendation Case ............................................. 62 Exhibit VI: Pro Forma Non‐GAAP Financials – Recommendation Case............................................... 63 Exhibit VII: Primal Branding.......................................................................................................... 64 Exhibit VIII: Comparable Company Analysis ................................................................................... 65 Exhibit IX: Executive Compensation.............................................................................................. 67 Exhibit X: Sample Products........................................................................................................... 70 Exhibit XI: Store Images ............................................................................................................... 77 Exhibit XII: Bibliography and End Notes......................................................................................... 78

Page 4 of 78

Executive Summary

Overview

Pier 1 Imports, Inc. (“Pier 1” or the “Company”) is North America’s largest

specialty retailer of home furnishings, decorations, gifts, and related items. Items are

imported from over 50 different countries around the world and displayed in over 1,200

Pier 1 Imports stores. The specialty retail operations of Pier 1 consist of retail stores

operating under the names "Pier 1 Imports'' and "Pier 1 Kids'', selling a wide variety of

furniture, decorative home furnishings, dining and kitchen goods, bath and bedding

accessories and other specialty items for the home. Many items are one of kind and not

found in other retail stores. Pier 1’s common stock is listed on the New York Stock

Exchange under the symbol PIR.

Pier 1 specializes in direct importing and is one of the world's largest importers

of rattan and brass. 65% of Pier 1’s merchandise is different each year to drive

increased customer traffic as well as a sense of urgency to make a purchase.

Structure of this paper

In this paper we will take the perspective of an advisor to the board of directors,

with a focus on increasing shareholders’ equity and returning Pier 1 to profitability. We

will first review the overall economics and challenges of the retail furniture and

miscellaneous home furnishing industries. Based on our discussion of the industry we

will explore the history of Pier 1 and specific challenges to the company in areas such as

operations, branding, and strategic direction. Next, we will turn our focus to the

management, financing decisions made along the way and competitive advantages.

Finally, we will review alternatives available to the company and give our proposed

recommendations for a successful turnaround.

Page 5 of 78

Recommendations

Pier 1 must take immediate action to close a significant portion of its

underperforming stores in an effort to stabilize its finances and right‐size its SG&A

expenses. Specifically, at least 20% of its current stores are operating at significant

losses without reasonable hope of improvement, and the company can ill afford to

continue to finance such money losing endeavors. Additionally, Pier 1 should look to

monetize its investment in its corporate headquarters. Further, the company has

confused its customers with its numerous and ever changing marketing campaigns, and

must refocus on its core segment of fashionable furnishings at value price points and

avoid price as a basis of differentiation. Finally, there is an unrealized opportunity for

material savings in Pier 1's supply chain through consolidation of suppliers and

implementation of a Total Cost of Ownership approach to supply chain management.

By implementing these specific action plans, Pier 1 can return to profitability in its fiscal

year ending 2009 and achieve reasonable stock appreciation for its shareholders.

Summary of financial analysis and valuation

In preparing our analysis and recommendations we first modeled full pro forma

financials for the current status quo business case, consistent with current analyst and

market expectations (Exhibits I – III). Also, to better enable our in‐dept analysis we

restated the key financials on a non‐GAAP basis to isolate earnings before interest, tax,

depreciation, and rent (EBITDAR) and capitalize both the considerable off‐balance sheet

asset and liability values associated with Pier 1’s portfolio of operating leases (Exhibit

III). Based upon these projections, Pier 1 will not return to profitability until 2012 and

will need to raise additional debt (approx $50M) to finance its operations beginning in

2010. From a valuation perspective, these operating projections do not justify the

current market valuation of Pier 1. Accordingly, we believe that the current equity

prices reflect the option value associated with the possibility of a material turnaround in

excess of industry analyst expectations or a possible strategic take‐over or sale of the

company.

Page 6 of 78

Next, we modeled the significant restructuring actions that we believe are

required to close the bottom 20% of underperforming stores (target 250 closures in

2008) consistent with our recommendations. We projected these results and the post‐

restructuring pro forma financials through 2012 and believe Pier 1’s current liquidity will

be sufficient to sustain it through this restructuring program, after which we expect a

return to positive cash flow. Further, we performed some valuation analysis and

assuming our plan can be effectively executed, we believe the fair value of Pier 1 shares

should be $12 – 18 per share, well above its current levels.

Page 7 of 78

Industry outlook and competitive environment

Industry overview and definition

Pier 1 Imports is considered part of the “Furniture” and “Miscellaneous Home

Furnishings Stores” industries.i

Furniture Storesii

In 2006, over 28,300 establishments engaged in the retail sale of household

furniture. Several bankruptcies in the early 2000s, such as that of Heilig‐Myers, provided

opportunities for independent stores and larger retailers to gain market share. In the

mid 2000’s companies began to offer a more diverse product set than ever before and

began branching out into related products such as glassware and linens.

As of 2006, the industry employed about 265,000 people and generated an

annual payroll of $7.37 billion. Consumers spent roughly $48.7 billion within this

industry. On the average, consumers spent $1.1 million per retail store. The industry is

made up of large national chains, regional stores and small independent operations. In

recent years, a growing segment of new retailers has emerged who sell household and

office furniture, mattresses and related consumer products. The retailers include large

discount superstores such as Wal‐Mart and Target, warehouse stores like Sam's Club

and Office Depot and one‐stop department stores such as Sears and J.C. Penney. This

competition made the marketplace a much more difficult one for traditional furniture

stores.

Miscellaneous Home Furnishing Storesiii

Miscellaneous Home Furnishing Stores offer everything needed to furnish a

home from kitchenware to linens and lamps and shades to Venetian blinds and window

shades.

Discount stores, as well as department stores, stock a wide variety of items for

the consumer, and their prices vary with the brand name and the type of store that sells

Page 8 of 78

them. Of the several different types of retailers that sell home furnishings, one of the

fastest growing is the specialty retailer that attracts upscale consumers. These stores

may be independent or part of a chain and provide quality merchandise with moderate

price tags. However, price is not all that attracts customers. Specialty retailers tend to

carry unusual and distinctive items that attract consumers who cannot find them

anywhere else.

Retail Economics

The furniture market is closely tied to the performance of the housing industry.

Furniture sales were down in the early 2000’s, but by 2005 many retailers were seeing

upswings, particularly single‐brand vertical retailers such as LA‐Z‐Boy. Office furniture

also was coming out of its prolonged slump, experiencing growth in 2004 and 2005 for

the first time in several years.

However, in 2006, new home construction was down again and this has highly

impacted the furniture and household goods markets. The Business and Institutional

Furniture Manufacturer's Association (BIFMA), in conjunction with Global Insight,

reported an 8.3 percent decrease in retail sales of office furniture. The slow growth was

due to the sluggish economy, and also the lack of office construction.

Page 9 of 78

Business

Company overview

Pier 1 offers a diverse selection of products consisting of approximately 3,000

items imported from over 40 countries around the world. While the broad categories of

Pier 1's merchandise remain constant, individual items within these product groupings

change frequently in order to meet the demands of customers. The principal categories

of merchandise include the following:

2006 Revenues

Furniture, 40%

Decorative Accessories,

26%

Housewares, 13%

Bed & Bath, 15%

Seasonal, 6%

• Furniture – This product group consists of furniture, furniture pads and pillows to

be used on patios and in living, dining, kitchen and bedroom areas, and in sun

rooms. This product group constituted approximately 40% of Pier 1's total North

American retail sales in fiscal year 2006 and 39% in fiscal years 2005 and 2004.

These goods are imported from a variety of countries such as Italy, Malaysia,

Brazil, Mexico, China, the Philippines and Indonesia, and are also obtained from

domestic sources. The furniture is made of metal or handcrafted natural

Page 10 of 78

materials, including rattan, pine, beech, rubberwood and selected hardwoods

with either natural, stained or painted finishes. Pier 1 also sells upholstered

furniture.

• Decorative Accessories – This product group constitutes the broadest category of

merchandise in Pier 1's sales mix and contributed approximately 26% to Pier 1's

total North American retail sales in fiscal year 2006, 25% in fiscal year 2005 and

24% in fiscal year 2004. These items are imported from approximately 35

countries and include brass, marble and wood items, as well as lamps, vases,

dried and silk flowers, baskets, wall decorations and numerous other decorative

items. A majority of these products are handcrafted from natural materials.

• Housewares – This product group is imported mainly from the Far East and

Europe and includes ceramics, dinnerware and other functional and decorative

items. These goods accounted for approximately 13% of Pier 1's total North

American retail sales in fiscal years 2006, 2005 and 2004.

• Bed & Bath – This product group is imported mainly from India, Germany,

Thailand and China and is also obtained from domestic sources. This group

includes bath and fragrance products, candles and bedding. These goods

accounted for approximately 15% of Pier 1's total North American retail sales in

fiscal year 2006, 16% in fiscal year 2005 and 18% in fiscal year 2004.

• Seasonal – This product group consists of merchandise for celebrating holidays

and spring/summer entertaining, imported mainly from Europe, Indonesia,

China, the Philippines and India and also obtained from domestic sources. These

items accounted for approximately 6% of Pier 1's total North American retail

sales in fiscal year 2006, 7% in fiscal year 2005 and 6% in fiscal year 2004.

Since June 2000, Pier 1 has operated an e‐commerce Website, which received an

average of 4.3 million visits per month in fiscal 2006, and can be accessed at

www.pier1.com. This site is a significant marketing vehicle for the Company while

providing customers with access to Pier 1 products and services at their convenience, as

Page 11 of 78

well as access to investor relations information. Customers can shop substantially all of

Pier 1's merchandise assortment, as well as purchase gift cards, create and manage

bridal and gift registries, view interactive catalogs, watch the most recent television

commercials, and sign up for marketing e‐mail and direct mail.

Pier 1 Kids stores offer children's furniture and decorative accessories. The

Company started operating Pier 1 Kids stores in March 2001 when it acquired Cargo, a

21 unit retail chain focused on children’s furniture. Cargo was later rebraded as Pier 1

Kids. Pier 1 Kids utilizes an e‐commerce site, which can be accessed at

www.pier1kids.com to attract customers and provide information regarding placing

orders, sale items and store locations.

In fiscal 2006, Pier 1 Imports, Inc. expanded its specialty retail operations by

opening 65 new Pier 1 stores, four new Pier 1 Kids stores and two new international

stores. The Company closed 32 Pier 1 stores and six Pier 1 Kids stores. Subject to

changes in the retail environment, availability of suitable store sites, lease renewal

negotiations and availability of adequate financing, the Company plans to open

approximately 40 new Pier 1 stores and close approximately 30 Pier 1 and five Pier 1

Kids stores during 2007. Plans for 2007 also include opening approximately seven new

international stores in Mexico and Puerto Rico, primarily in a store within a store

format. On March 20, 2006, Pier 1 Imports, Inc. announced the sale of its subsidiary

based in the United Kingdom, The Pier Retail Group Limited (The Pier). The Pier operates

45 retail stores in the United Kingdom and Ireland, offering decorative home furnishings

and related items in a setting similar to Pier 1 stores. The Pier operates a distribution

facility near London, England.

Strategy and operationsiv

Pier 1 merchandise largely consists of items that require a significant degree of

handcraftsmanship and are mostly imported directly from foreign suppliers. For the

most part, the imported merchandise is handcrafted in cottage industries and small

factories. Pier 1 is not dependent on any particular supplier and has enjoyed long‐

standing relationships with many vendors and agents. The company believes alternative

Page 12 of 78

sources of products could be procured over a relatively short period of time if necessary.

In selecting the source of a product, Pier 1 considers quality, dependability of delivery

and cost. During fiscal 2006, Pier 1 sold merchandise imported from over 40 different

countries with 35% of its sales derived from merchandise produced in China, 14%

derived from merchandise produced in India, 13% derived from merchandise produced

in the United States and 33% derived from merchandise produced in Indonesia, Brazil,

Italy, Thailand, the Philippines, Vietnam and Mexico. The remaining 5% of sales was

from merchandise produced in various Asian, European, Central American, South

American and African countries. Imported merchandise and a portion of domestic

purchases are delivered to the Pier 1 distribution centers, unpacked and made available

for shipment to the various stores in each distribution center's region. Due to the time

delays involved in procuring merchandise from foreign suppliers, Pier 1 maintains a

substantial inventory to assure a sufficient supply of products to its stores.

Pier 1, through certain of its wholly owned subsidiaries, owns a number of

federally registered service marks under which Pier 1 Imports and Pier 1 Kids stores do

business. Additionally, certain subsidiaries of the Company have registered and have

applications pending for the registration of certain other Pier 1 and Pier 1 Kids

trademarks and service marks in the United States and in numerous foreign countries.

The Company believes that its marks have significant value and are important in its

marketing efforts. The Company maintains a policy of pursuing registration of its marks

and opposing any infringement of its marks.

The Company is in the highly competitive specialty retail business and competes

primarily with specialty sections of large department stores, furniture and decorative

home furnishings retailers, small specialty stores, discount stores and catalog and

internet retailers. Management believes that the Company competes on the basis of

price, value, rapidly changing merchandise assortments, visual presentations of its

merchandise, customer service and fashion sense. The Company also believes it

remains competitive with other retailers because of its name recognition and

established vendor relationships. The Company believes that its Pier 1 Kids business

Page 13 of 78

offers an opportunity to take advantage of the growing demand for children's furniture

and accessories. The Company allows customers to return merchandise within a

reasonable time after the date of purchase without limitation as to reason, consistent

with industry standard policies. Most returns occur within 30 days of the date of

purchase. The Company monitors the level of and stated reasons for returns and

maintains a reserve for future returns based on historical experience and other known

factors.

On February 25, 2006, the Company employed approximately 18,200 associates

in North America, of which approximately 8,500 were full‐time employees and 9,700

were part‐time employees.

History

Pier 1 began in 1962 with a single store in San Mateo, California. Since then, they

have grown to over 1,200 locations nationwide.

Pricing

Pier1 has traditionally targeted consumers who are looking for one‐of‐a‐kind

products but who may also be more cost conscious. Due to the fact that Pier 1 suppliers

are in many cases overseas, the company has a need to carry high inventories in

anticipation of seasonal sales. This high inventory, combined with a slowing economic

environment, has lead to a higher number of seasonal sales and discounts to move

inventory as quickly as possible.

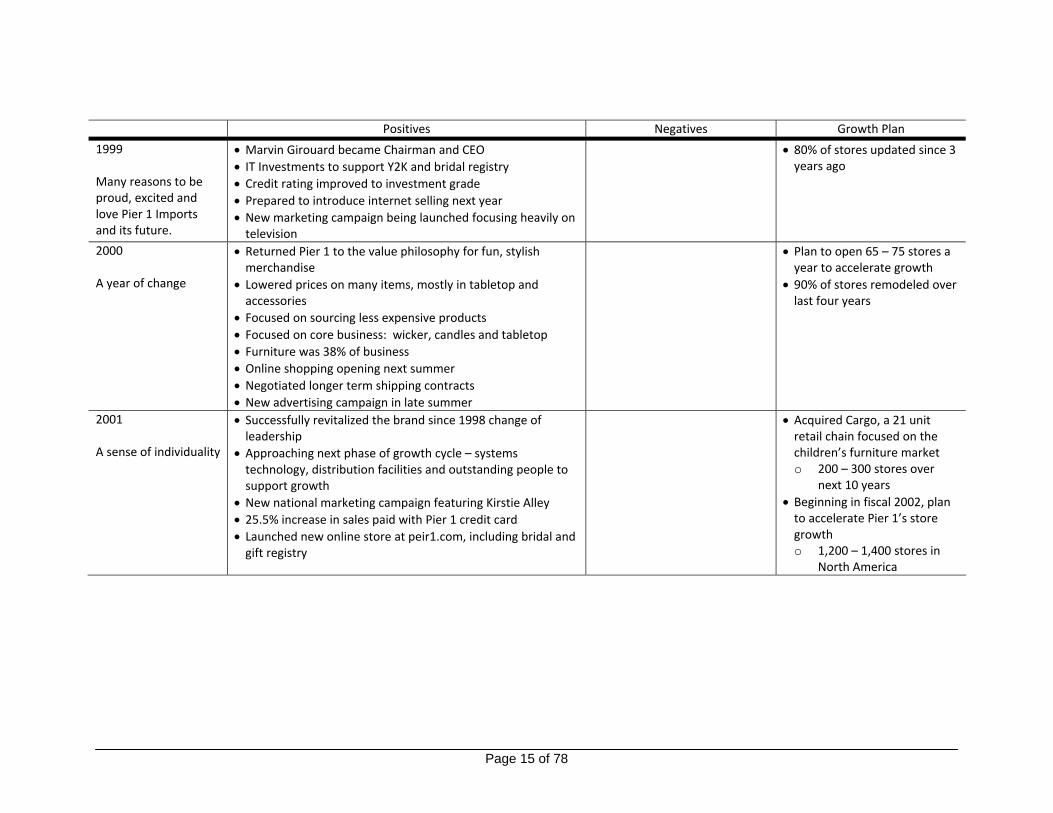

Analysis of Historic Annual Letters from CEO

Analyzing the Annual Letters to Shareholders from the CEO, Pier 1 benefited

from a strong economy but lost its way as it rapidly expanded, especially its SG&A in

anticipation of expanding its store growth. Pier 1 continued to expand at a rapid pace

despite the fact that its comparable store sales were declining. Additionally, the former

CEO Marvin Girouard built a trophy for himself by spending $100 million on a new

building development in Texas for the corporate headquarters, which questions the

level of governance the board of directors was providing management. Despite all of

Page 14 of 78

the troubles that have plagued Pier 1 during the last year, the annual letters from the

CEO remain incredibly upbeat on the future of the Company and its new initiatives. It is

clear that Pier 1 was focused on growth, and could not find its brand image, evidenced

by the continuous repositioning efforts of the company. The following chart outlines

the key points the CEO made in his annual letters.

Page 15 of 78

Positives Negatives Growth Plan

1999 Many reasons to be proud, excited and love Pier 1 Imports and its future.

• Marvin Girouard became Chairman and CEO • IT Investments to support Y2K and bridal registry • Credit rating improved to investment grade • Prepared to introduce internet selling next year • New marketing campaign being launched focusing heavily on television

• 80% of stores updated since 3 years ago

2000 A year of change

• Returned Pier 1 to the value philosophy for fun, stylish merchandise

• Lowered prices on many items, mostly in tabletop and accessories

• Focused on sourcing less expensive products • Focused on core business: wicker, candles and tabletop • Furniture was 38% of business • Online shopping opening next summer • Negotiated longer term shipping contracts • New advertising campaign in late summer

• Plan to open 65 – 75 stores a year to accelerate growth

• 90% of stores remodeled over last four years

2001 A sense of individuality

• Successfully revitalized the brand since 1998 change of leadership

• Approaching next phase of growth cycle – systems technology, distribution facilities and outstanding people to support growth

• New national marketing campaign featuring Kirstie Alley • 25.5% increase in sales paid with Pier 1 credit card • Launched new online store at peir1.com, including bridal and gift registry

• Acquired Cargo, a 21 unit retail chain focused on the children’s furniture market o 200 – 300 stores over

next 10 years • Beginning in fiscal 2002, plan to accelerate Pier 1’s store growth o 1,200 – 1,400 stores in

North America

Page 16 of 78

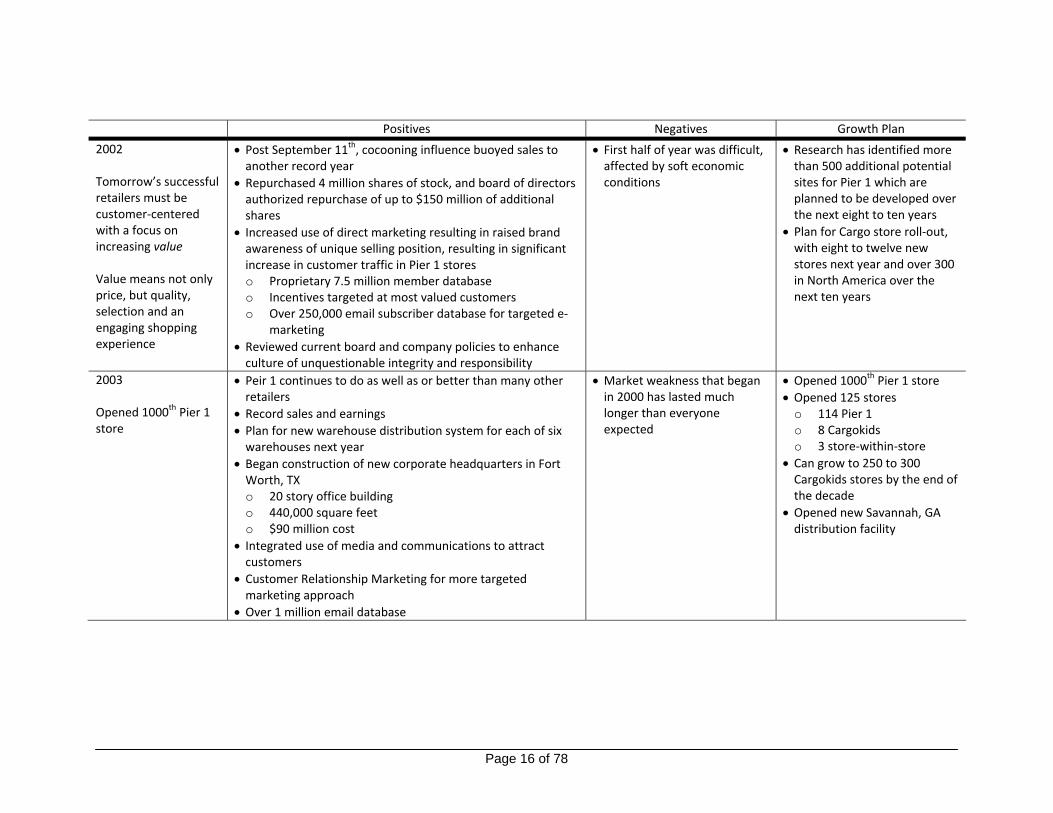

Positives Negatives Growth Plan

2002 Tomorrow’s successful retailers must be customer‐centered with a focus on increasing value Value means not only price, but quality, selection and an engaging shopping experience

• Post September 11th, cocooning influence buoyed sales to another record year

• Repurchased 4 million shares of stock, and board of directors authorized repurchase of up to $150 million of additional shares

• Increased use of direct marketing resulting in raised brand awareness of unique selling position, resulting in significant increase in customer traffic in Pier 1 stores o Proprietary 7.5 million member database o Incentives targeted at most valued customers o Over 250,000 email subscriber database for targeted e‐

marketing • Reviewed current board and company policies to enhance culture of unquestionable integrity and responsibility

• First half of year was difficult, affected by soft economic conditions

• Research has identified more than 500 additional potential sites for Pier 1 which are planned to be developed over the next eight to ten years

• Plan for Cargo store roll‐out, with eight to twelve new stores next year and over 300 in North America over the next ten years

2003 Opened 1000th Pier 1 store

• Peir 1 continues to do as well as or better than many other retailers

• Record sales and earnings • Plan for new warehouse distribution system for each of six warehouses next year

• Began construction of new corporate headquarters in Fort Worth, TX o 20 story office building o 440,000 square feet o $90 million cost

• Integrated use of media and communications to attract customers

• Customer Relationship Marketing for more targeted marketing approach

• Over 1 million email database

• Market weakness that began in 2000 has lasted much longer than everyone expected

• Opened 1000th Pier 1 store • Opened 125 stores

o 114 Pier 1 o 8 Cargokids o 3 store‐within‐store

• Can grow to 250 to 300 Cargokids stores by the end of the decade

• Opened new Savannah, GA distribution facility

Page 17 of 78

Positives Negatives Growth Plan

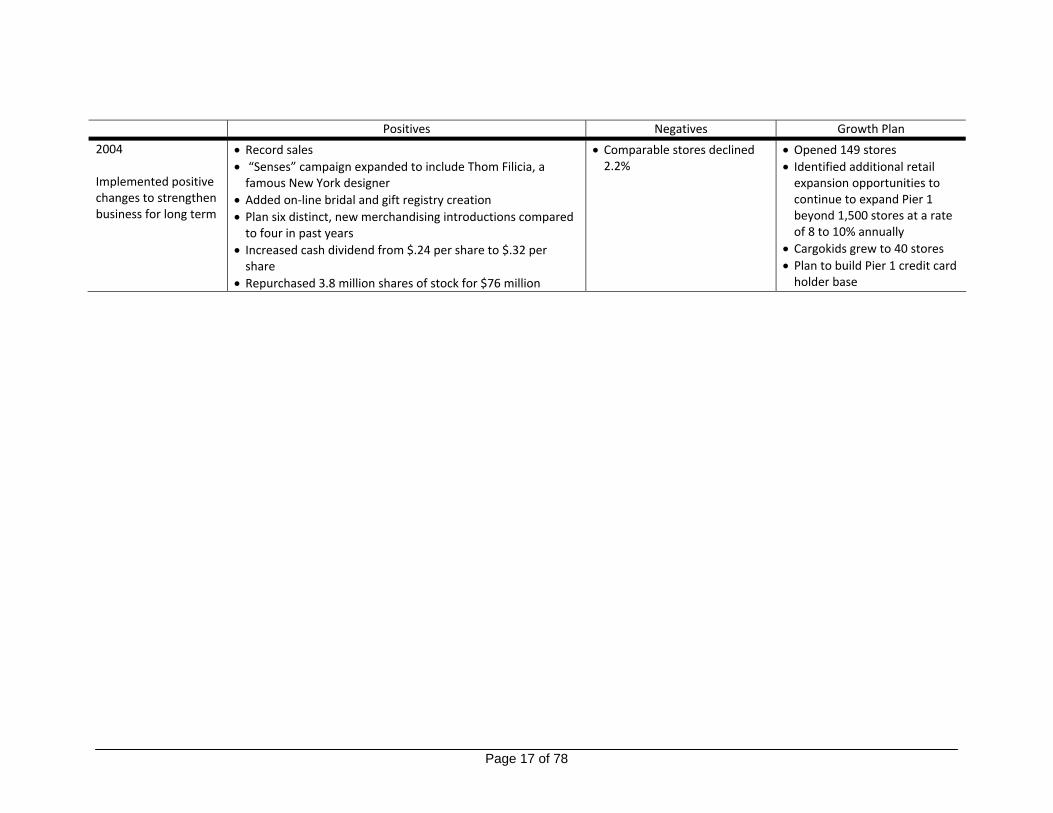

2004 Implemented positive changes to strengthen business for long term

• Record sales • “Senses” campaign expanded to include Thom Filicia, a famous New York designer

• Added on‐line bridal and gift registry creation • Plan six distinct, new merchandising introductions compared to four in past years

• Increased cash dividend from $.24 per share to $.32 per share

• Repurchased 3.8 million shares of stock for $76 million

• Comparable stores declined 2.2%

• Opened 149 stores • Identified additional retail expansion opportunities to continue to expand Pier 1 beyond 1,500 stores at a rate of 8 to 10% annually

• Cargokids grew to 40 stores • Plan to build Pier 1 credit card holder base

Page 18 of 78

Positives Negatives Growth Plan

2005 Disappointment and repositioning

• Hired Deutsch Inc. advertising agency for creative • Hired OMD Midwest for media‐buying • Implementing major marketing, merchandising and store operations initiatives

• Challenged buyers to design, source and buy more distinct, one‐or‐a‐kind merchandise and offer it with competitive retail pricing

• Sped up cycle to develop and bring new products to market • Plan to offer stronger seasonal assortments to increase “sense of urgency” to shoppers

• Plan to differentiate and broaden range of “Good,” “Better,” and “Best” offerings o “Good” – basic items at everyday values o “Better” – products with higher design and quality for

the price o “Best” – merchandise representing unique, design‐

forward collections that broaden a customer’s expectations

• Reduced number of items in Pier 1 stores by 15% to 20% and aggressively discontinued older merchandise collections to allow stores to present a new, stronger visual presentation with less clutter o Gives merchandise more space o Allows showcasing of featured home furnishings

• Goal – lower inventory levels in stores will ensure an easier and more interesting shopping experience for customers with stronger item focus

• Increased payroll hours in stores to allow time to support new merchandising transitions and spend more time with customers

• Converted Cargokids to Pier 1 Kids branding, resulting in increased traffic and dramatically improved sales

• Comparable stores down 5.8%• Lease accounting changes resulted in a one‐time charge of $.04 per share, but did not impact cash flow

• Completely re‐assessed the company mid‐way through the year

• Terminated five year relationship with advertising agency

• Made decision to slow store growth to improve store‐level productivity and grow operating margins

Page 19 of 78

Positives Negatives Growth Plan

2006 Turnaround strategy ‐ reposition for a return to profitability in the core business

• Sold The Pier (UK subsidiary) stores March 20, 2006 and classified as discontinued operations

• New merchandising – Modern Craftsman – with fashion‐forward color palettes and contemporary styles

• More product‐focused national marketing and advertising campaign

• Technology upgrades to allow new direct to consumer channel through catalog distribution

• Restructured and realigned store operations, buying and administrative functions to cut costs and improve efficiencies throughout the organization

• Issued $165 million of convertible debt • Reevaluated real estate portfolio and decided to accelerate closings of underperforming stores during fiscal 2006 and 2007

• Consolidating back offices of Pier 1 and Pier 1 Kids

• Opened distribution center in Washington

Page 20 of 78

Primal Code Branding Analysisv

Strong brands have seven pieces of code that work together to make them

believable and enduring. These areas are highlighted below and there is additional

information on Primal Branding is in the appendix. The table that follows highlights Pier

1’s failure to develop its primal code, which is partially responsible for its current

operating and financial position. Compared to best of breed, Pier 1’s current Primal

Code requires a large investment. The company has changed its advertising message

several times in the last few years, making it difficult for customers, consumers and

employees to know what the brand Pier 1 means and why they want to be a part of it.

Page 21 of 78

Primal Branding Analysis Definition Best of Breed Pier 1 Today Goal

Creation Story The who and why, often involving a mythic quest. The creation story is the first step in providing answers to why people should care about you, your product or service.

GE, Disney, United States of America, Microsoft

Pier 1 started as a single store in San Mateo, California in 1962. The store’s first customers were post‐World War II baby boomers looking for beanbag chairs, love beads and incense.

Who started Pier 1? Why did they start it?

Creed A set of core principles that you believe in and what you want others to believe about you. Defining, understanding and communicating your mission to your customers and employees are the goal of a creed.

“Just do it.” (Nike), “All Men [and women] are created equal” (USA), “The Third Place” (Starbucks)

“it’s your thing” Currently does not speak to Pier 1’s strengths or provide a succinct message. Needs to be reworked.

Icons Quick concentrations of meaning that cause your brand identity and brand values to spontaneously resonate.

Nike swoosh, Coke bottle, smell of Cinnabons

Papasan chair, candles, Kirstie Alley

Icons need to be refreshed and developed with longevity in mind. Papasan chair is dated, candles are a commodity product and Kirstie Alley is out of the spotlight.

Rituals The repeated interactions people have with your enterprise.

Fourth of July parades, stopping at Starbucks, searching on Google

Shop the sale, return gifts received from Pier 1

Shop for all home/novelty gifts at Pier 1. Browse Pier 1 whenever in the neighborhood.

Pagans / Nonbelievers Part of saying who you are and what you stand for is also declaring what you do not stand for.

Apple/Microsoft, Yankees/Red Sox, Democrats/Republicans, New York/LA, Coke/7Up

Pier 1 has plenty of these today! Pottery Barn, Target, Bed, Bath & Beyond

Provide product offerings which will grab a greater percentage of customers’ share of dollar spend.

Sacred Words A set of specialized words that must be learned before people can belong.

Grande, Big Mac, iPod, lol None Need to develop.

Leader The person who is the catalyst, risk taker, visionary, iconoclast who set out against all the odds to re‐create the world according to their own sense of self, community and opportunity.

Richard Branson, Bill Gates, Dr. Martin Luther King, Oprah

Alex Smith New CEO, has an opportunity to be the leader by embracing change and communicating Pier 1 brand message to all constituents.

Page 22 of 78

SWOT Analysis

Strengths

Opportunities Threats

Weaknesses

• Underperforming locations drag profitability

• Gross margin below 30% (40% is a realistic target)

• Significant CAPEX spends to stay afloat

• Strength of management team and corporate governance is questionable given recent performance and lack of accountability (with the exception of the recent CEO change)

• Continued lost market share to old and new competitors

• Trade areas move away from Pier 1 locations as Target and Wal‐Mart stores build new centers

• Lack of product differentiation relative to competition and lower priced competitors such as Target

• Underperforming stores continue to burn cash and drag Company’s energy, distracting from focus on strong stores

• Offer the customer a selection of ever‐changing, unique merchandise priced at a value, innovative marketing, a fun and relaxing shopping experience and outstanding customer service

• Competitive advantage – offering customers new merchandise at a value

• Develop and communicate brand message for customers, suppliers and vendors

• Analysis of distribution facilities and inefficiencies

• Analysis of pricing opportunities

• Analysis of total cost of ownership with a focus on working with suppliers to reduce overall costs and increase gross margin

• Third party real estate market assessment through a combination of Buxton and Geoview geo mapping services

• Close underperforming stores

Top industrydriversSWOTAnalysis

‐

‐

+

+

Page 23 of 78

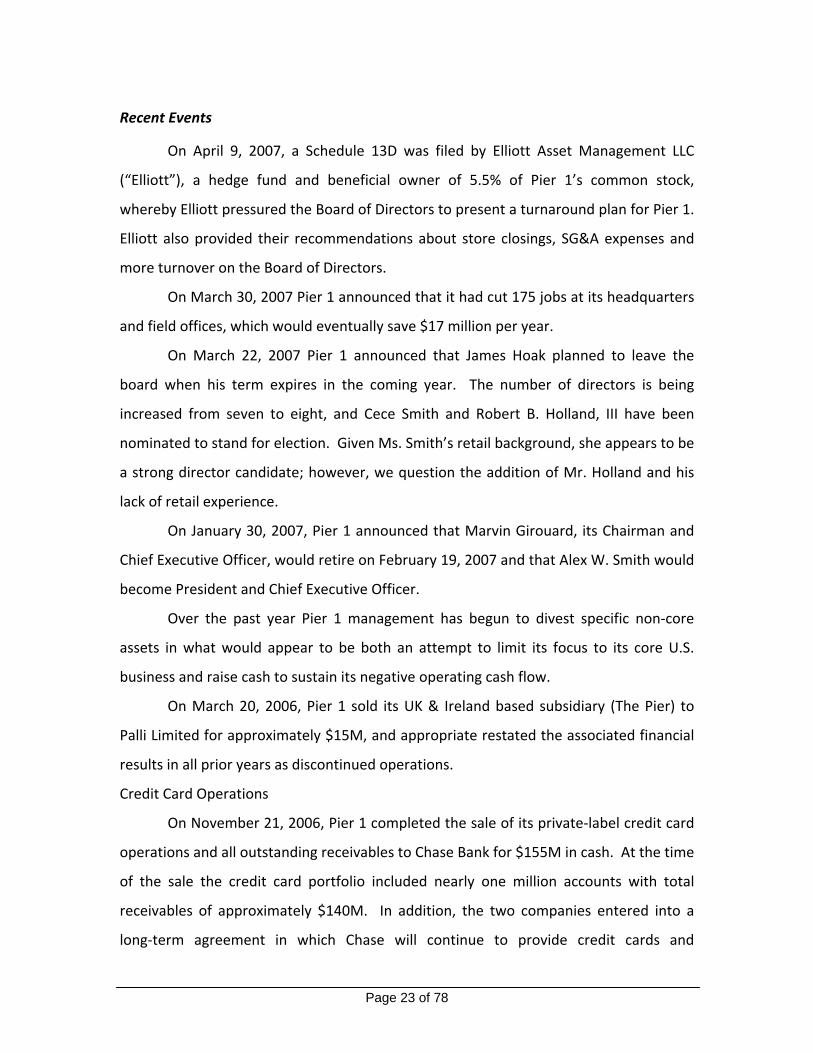

Recent Events

On April 9, 2007, a Schedule 13D was filed by Elliott Asset Management LLC

(“Elliott”), a hedge fund and beneficial owner of 5.5% of Pier 1’s common stock,

whereby Elliott pressured the Board of Directors to present a turnaround plan for Pier 1.

Elliott also provided their recommendations about store closings, SG&A expenses and

more turnover on the Board of Directors.

On March 30, 2007 Pier 1 announced that it had cut 175 jobs at its headquarters

and field offices, which would eventually save $17 million per year.

On March 22, 2007 Pier 1 announced that James Hoak planned to leave the

board when his term expires in the coming year. The number of directors is being

increased from seven to eight, and Cece Smith and Robert B. Holland, III have been

nominated to stand for election. Given Ms. Smith’s retail background, she appears to be

a strong director candidate; however, we question the addition of Mr. Holland and his

lack of retail experience.

On January 30, 2007, Pier 1 announced that Marvin Girouard, its Chairman and

Chief Executive Officer, would retire on February 19, 2007 and that Alex W. Smith would

become President and Chief Executive Officer.

Over the past year Pier 1 management has begun to divest specific non‐core

assets in what would appear to be both an attempt to limit its focus to its core U.S.

business and raise cash to sustain its negative operating cash flow.

On March 20, 2006, Pier 1 sold its UK & Ireland based subsidiary (The Pier) to

Palli Limited for approximately $15M, and appropriate restated the associated financial

results in all prior years as discontinued operations.

Credit Card Operations

On November 21, 2006, Pier 1 completed the sale of its private‐label credit card

operations and all outstanding receivables to Chase Bank for $155M in cash. At the time

of the sale the credit card portfolio included nearly one million accounts with total

receivables of approximately $140M. In addition, the two companies entered into a

long‐term agreement in which Chase will continue to provide credit cards and

Page 24 of 78

associated support to Pier 1 customers, while providing specific payments to Pier 1

based upon account activity.

This arrangement allowed Pier 1 to monetize the value of the credit card

portfolio and associated business without impacting its customers. This sale represents

an optimal outcome given Pier 1’s current financial position and need for cash. In the

past, prior to this sale, Pier 1 frequently securitized and sold its credit card receivables

to raise cash.

Page 25 of 78

Management and governance

Executive officers and key employees

Alex W. Smith (Chief Executive Officer, President and Director)

Before being named CEO and President of Pier 1 in 2007, Alex Smith was Senior

Executive Vice President, Group President of The Tjx Companies Inc. since March 29,

2004. Mr. Smith served as Executive Vice President and Group Executive, International

of TJX Companies Inc. from 2001 to March 29, 2004. Mr. Smith was responsibilities for

The Marmaxx Group, The Tjx Companies Inc.'s HomeGoods division, and the California

Buying Office and oversight of the European Buying Offices. Mr. Smith was Managing

Director of T.K. Maxx from 1995 to 2001. He was Managing Director of Lane Crawford

from 1994 to 1995, Managing Director of Owen Owen plc from 1990 to 1993 and

Merchandise Director from 1987 to 1990.

Charles H. Turner (CFO, Executive Vice President ‐ Finance and Treasurer)

Charles H. Turner has been Executive Vice President, Finance of Pier 1 since April

2002 and Chief Financial Officer and Treasurer since August 1999. Mr. Turner served as

Senior Vice President of Finance of Pier 1 from August 1999 to April 2002. He served as

Senior Vice President of Stores of Pier 1 from August 1994 to August 1999, and served

as Controller and Principal Accounting Officer of Pier 1 from January 1992 to August

1994. He has served as a Director of Elder Beerman Stores Corp. since 2000.

Susan E. Barle (Principal Accounting Officer)

Susan Barley has been promoted to Senior VP of Finance. Barley started at Pier 1

in 1976, when she was hired as Assistant Controller for the Accounting department. She

was promoted to VP/Controller in 1994 and became VP of Finance in 1999.

Page 26 of 78

Michael A. Carter (Senior Vice President , General Counsel and Corporate Secretary)

Michael A. Carter serves as Senior Vice President, General Counsel and

Corporate Secretary of Pier 1.

Phil E. Schneider (Executive Vice President – Marketing)

Phil E. Schneider has been the Executive Vice President of Marketing of Pier 1

since April 2002. Mr. Schneider served as Senior Vice President of Marketing of Pier 1

from May 1993 to April 2002, and served as Vice President of Advertising of Pier 1 from

January 1988 to May 1993.

Gregory S. Humenesky (Executive Vice President of Human Resources)

Gregory S. Humenesky has been Executive Vice President, Human Resources of

Pier 1 since February 2005. Prior to joining Pier 1, Mr. Humenesky served as Senior Vice

President of Human Resources at Zale Corporation from April 1996 to February 2005.

Jay R. Jacobs (Executive Vice President – Merchandising)

Jay R. Jacobs has been the Executive Vice President of Merchandising of Pier 1

since April 2002. Mr. Jacobs served as Senior Vice President of Merchandising of Pier 1

from May 1995 to April 2002. He served as Vice President of Divisional Merchandising

of Pier 1 from May 1993 to May 1995, and served as Director of Divisional

Merchandising of Pier 1 from July 1991 to May 1993.

J. Rodney Lawrence (Executive Vice President of Legal Affairs)

J. Rodney Lawrence has been the Executive Vice President of Legal Affairs of Pier

1 since April 2002 and has served as Secretary of Pier 1 since November 1985. Mr.

Lawrence served as Senior Vice President of Legal Affairs of Pier 1 from June 1992 to

April 2002, and served as Vice President of Legal Affairs of Pier 1 from November 1985

to June 1992.

Page 27 of 78

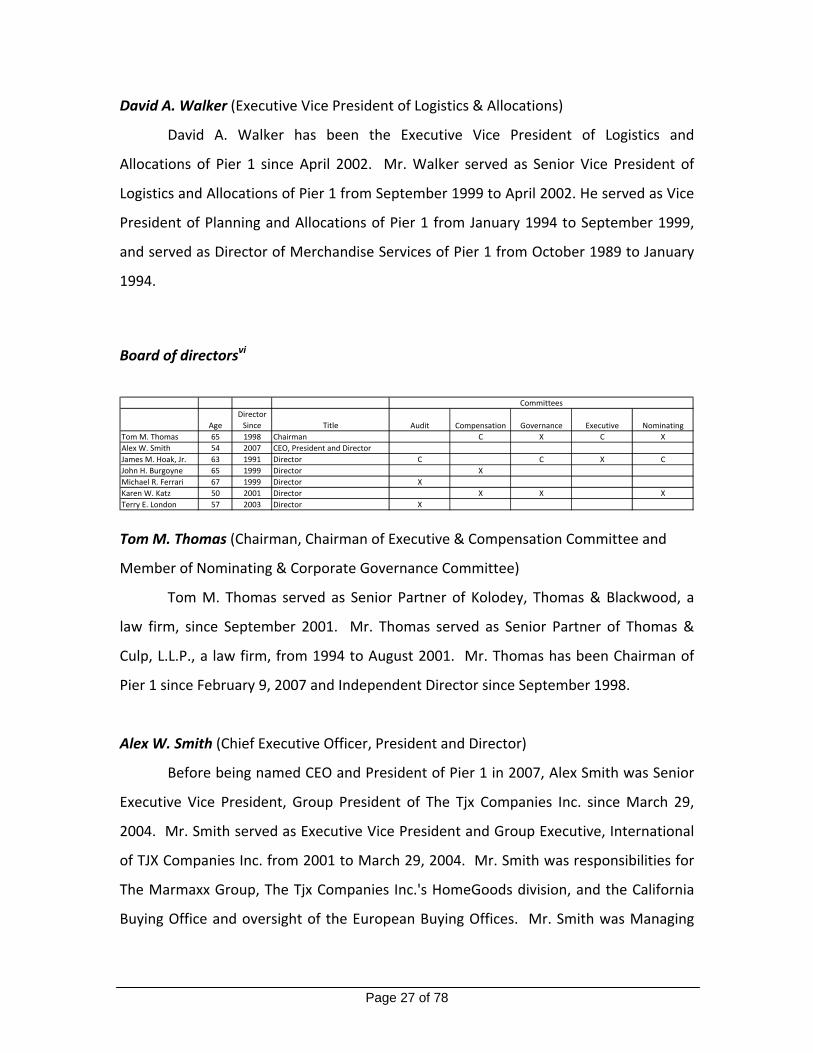

David A. Walker (Executive Vice President of Logistics & Allocations)

David A. Walker has been the Executive Vice President of Logistics and

Allocations of Pier 1 since April 2002. Mr. Walker served as Senior Vice President of

Logistics and Allocations of Pier 1 from September 1999 to April 2002. He served as Vice

President of Planning and Allocations of Pier 1 from January 1994 to September 1999,

and served as Director of Merchandise Services of Pier 1 from October 1989 to January

1994.

Board of directorsvi

Committees

AgeDirector Since Title Audit Compensation Governance Executive Nominating

Tom M. Thomas 65 1998 Chairman C X C XAlex W. Smith 54 2007 CEO, President and DirectorJames M. Hoak, Jr. 63 1991 Director C C X CJohn H. Burgoyne 65 1999 Director XMichael R. Ferrari 67 1999 Director XKaren W. Katz 50 2001 Director X X XTerry E. London 57 2003 Director X Tom M. Thomas (Chairman, Chairman of Executive & Compensation Committee and

Member of Nominating & Corporate Governance Committee)

Tom M. Thomas served as Senior Partner of Kolodey, Thomas & Blackwood, a

law firm, since September 2001. Mr. Thomas served as Senior Partner of Thomas &

Culp, L.L.P., a law firm, from 1994 to August 2001. Mr. Thomas has been Chairman of

Pier 1 since February 9, 2007 and Independent Director since September 1998.

Alex W. Smith (Chief Executive Officer, President and Director)

Before being named CEO and President of Pier 1 in 2007, Alex Smith was Senior

Executive Vice President, Group President of The Tjx Companies Inc. since March 29,

2004. Mr. Smith served as Executive Vice President and Group Executive, International

of TJX Companies Inc. from 2001 to March 29, 2004. Mr. Smith was responsibilities for

The Marmaxx Group, The Tjx Companies Inc.'s HomeGoods division, and the California

Buying Office and oversight of the European Buying Offices. Mr. Smith was Managing

Page 28 of 78

Director of T.K. Maxx from 1995 to 2001. He was Managing Director of Lane Crawford

from 1994 to 1995, Managing Director of Owen Owen plc from 1990 to 1993 and

Merchandise Director from 1987 to 1990.

James M. Hoak, Jr. (Plans to resign from Board when his term expires; Director,

Chairman of Audit Committee, Chairman of Nominating & Corporate Governance

Committee and Member of Executive Committee)

Mr. James M. Hoak, Jr. is the Chairman and Chief Executive Officer at Hoak

Media Corporation since September 1991 and is one of the premier media

entrepreneurs. He also serves as a Value Added Partner of CIC Partners. In 1971, Mr.

Hoak founded Heritage Communications, Inc. In 1991, he co‐founded Crown Media, Inc.

to acquire and operate cable systems, which they sold in 1995. Mr. Hoak served as the

Chief Executive Officer and Chairman of Crown Media, Inc. from February 1991 to

January 1995. From 1971 to 1987, he served as a Chief Executive Officer and President

of Heritage Communications, Inc. and Chairman and Chief Executive Officer from August

1987 to December 1990. Prior to this, Mr. Hoak founded Heritage Media Corporation in

1987 to purchase radio and television properties of Heritage Communications. He is the

Founder and Chairman of the American Association of Entrepreneurs. Mr. Hoak has

been involved with numerous other communications businesses. He has over 30 years

of experience as an entrepreneur, operator, investor and Chief Executive Officer in

various industries. Mr. Hoak has been the Chairman of Hoak Media since its formation

in August 2003. He is a Chairman of the Board at Chaparral Steel Company and serves

on the Executive Committee. He has been a Director of Texas Industries Inc. since 1995.

Mr. Hoak has been a Director of Pier 1 since September 1991 and is Chairman of the

Nominating and Audit Committees and member of the Executive Committee. He has

been a Director of Grande Communications Holdings Inc. since February 2000 and

member of its Finance Committee. Mr. Hoak is a Director Nominee of Panamsat Holding

Corp. and Director of Midwest Resources, Inc.; Texas Industries; Grande

Communications; and HBW Holdings, Inc. He served as a Chairman of HBW Holdings,

Page 29 of 78

Inc. from July 1996 to November 1999 and Heritage Media Corporation from its

inception in August 1987 until its sale in August 1997. Mr. Hoak served as a Director of

TeleCorp PCS Inc. since the merger in November 13, 2000; PanAmSat Holding Corp.

(formerly Panamsat Corp.) from May 1997 to August 2004; Heritage Media Corporation;

and Dynamex, Inc. He was a Governor of the American Stock Exchange. Mr. Hoak

received a B.A. from Yale University in 1966 and a J.D. from Stanford University School

of Law in 1969.

John H. Burgoyne (Independent Director and Member of Compensation Committee)

John H. Burgoyne has been a independent Director of Pier 1 since February 1999

and is a member of the Compensation Committee. Mr. Burgoyne has served as

President of Burgoyne and Associates (an international consulting firm) since March

1996. From May 1995 to March 1996, Mr. Burgoyne served as the General Manager of

IBM's Travel Industry sector for their Asia Pacific Region. Prior to that time, he served as

the President and General Manager of IBM China Corporation Ltd.

Michael R. Ferrari (Independent Director and Member of Audit Committee)

Michael R. Ferrari has been a Director of Pier 1 since February 1999 and is a

member of the Audit Committee. Dr. Ferrari has served as Senior Vice President and

Managing Director of the higher education practice of EFL Associates, an Executive

search firm, since May 2003. He is also the President of Ferrari and Associates LLC, a

higher education consulting firm he established in May 2003. Dr. Ferrari was granted

the title of Chancellor Emeritus of Texas Christian University by the universitys board of

trustees on June 1, 2003. Dr. Ferrari served as Chancellor of Texas Christian University

and Professor of Management in the M. J. Neeley School of Business at Texas Christian

University from July 1998 through May 2003. From 1985 to 1998, he served as

President of Drake University.

Page 30 of 78

Karen W. Katz (Independent Director, Member of Compensation Committee and

Member of Nominating & Corporate Governance Committee)

Karen W. Katz has been President and Chief Executive Officer of Neiman Marcus

Stores, a subsidiary of Neiman Marcus Group Inc. since December 2002. Mrs. Katz

served as President and Chief Executive Officer of Neiman Marcus Direct (a division of

the Neiman Marcus Group) from May 2000 to December 2002. She served as Executive

Vice President of Neiman Marcus Stores from February 1998 to May 2000 and served as

Senior Vice President from September 1996 to February 1998. She served as Vice

President and General Manager of the Dallas NorthPark Neiman Marcus store prior

thereto. She has been an Independent Director of Pier 1 since June 2001 and serves as a

Member of the Nominating and Audit Committees. She served as a Director of Neiman

Marcus Stores from September 1996 to February 1998.

Terry E. London (Independent Director and Member of Audit Committee)

Terry E. London has been President of London Partners LLC since July 2001. Mr.

London established London Partners LLC, a private equity investment firm in 2000.

From May 1997 to July 2000, he served as President and Chief Executive Officer Gaylord

Entertainment Company (“Gaylord”) (hospitality and attractions, creative content and

interactive media). He served as an Executive Vice President and Chief Operating

Officer of Gaylord from March 1997 to May 1997. He served as Chief Financial and

Administrative Officer of Gaylord Entertainment from 1991 to 1997. Mr. London has

been an Independent Director of Pier 1 Imports Inc., since September 25, 2003. Mr.

London has been a Director of Johnson Outdoors Inc. since 1999. He served as a

Director of Gaylord Entertainment Company from May 1997 to July 2000.

We consider only 5 of the 7 board members to be independent. The

independent board members include Hoak, Burgoyne, Ferrari, Katz and London. As

chairman and CEO, we do not consider Alex W. Smith to be independent. The final

board member, Tom Thomas, is a shareholder in a law firm who currently provides legal

Page 31 of 78

services for Pier 1. However, his firm provided less that 2% of the total legal work last

year and Mr. Thomas is less than a 10% shareholder in his company. Although the

relationship between Mr. Thomas and the law firm was deemed to be immaterial by the

board although he is considered to not be independent.

Discussion of financial condition

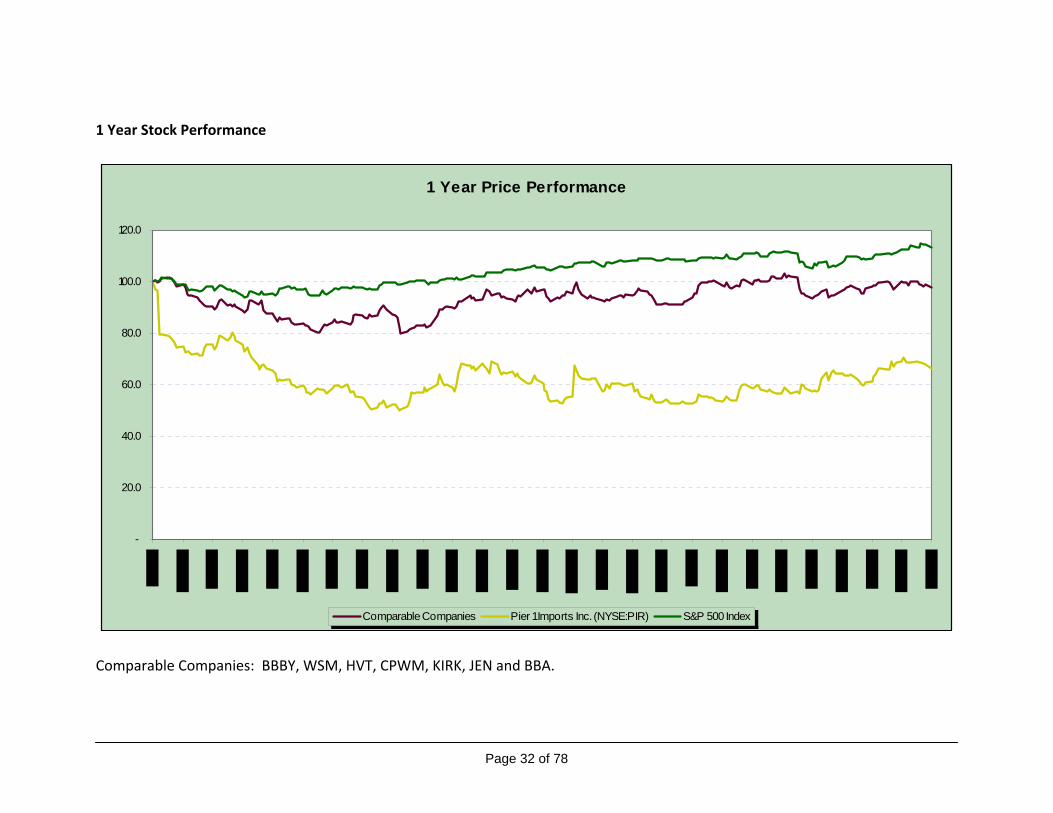

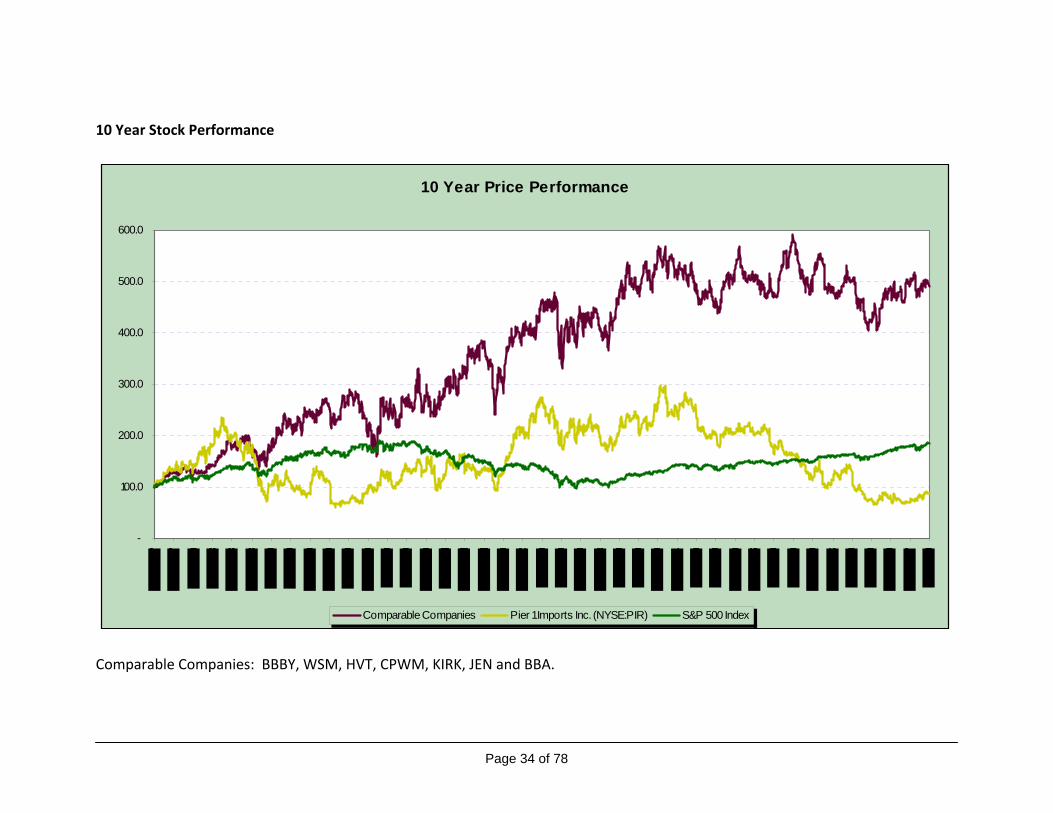

Historic Stock Performancevii

Pier 1’s stock has fallen significantly from the beginning of 2005 through 2007, losing

approximately two‐thirds of its value, following a relatively flat performance the prior

three years. From 1999 to 2002 Pier 1’s stock appreciated significantly as management

pushed its growth initiatives and opened new stores which led to many of the problems

the Company is now facing.

Page 32 of 78

1 Year Stock Performance

1 Year Price Performance

-

20.0

40.0

60.0

80.0

100.0

120.0

Comparable Companies Pier 1 Imports Inc. (NYSE:PIR) S&P 500 Index

Comparable Companies: BBBY, WSM, HVT, CPWM, KIRK, JEN and BBA.

Page 33 of 78

5 Year Stock Performance

5 Year Price Performance

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

Comparable Companies Pier 1 Imports Inc. (NYSE:PIR) S&P 500 Index

Comparable Companies: BBBY, WSM, HVT, CPWM, KIRK, JEN and BBA.

Page 34 of 78

10 Year Stock Performance

10 Year Price Performance

-

100.0

200.0

300.0

400.0

500.0

600.0

Comparable Companies Pier 1 Imports Inc. (NYSE:PIR) S&P 500 Index

Comparable Companies: BBBY, WSM, HVT, CPWM, KIRK, JEN and BBA.

Page 35 of 78

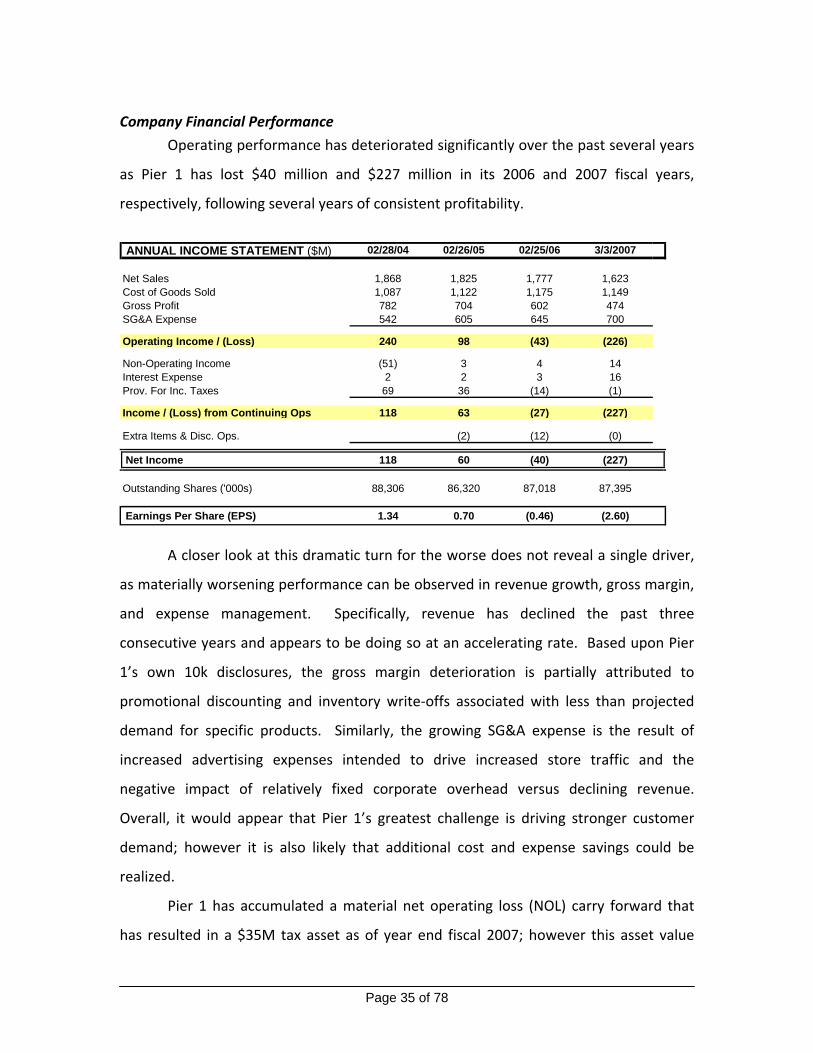

Company Financial Performance

Operating performance has deteriorated significantly over the past several years

as Pier 1 has lost $40 million and $227 million in its 2006 and 2007 fiscal years,

respectively, following several years of consistent profitability.

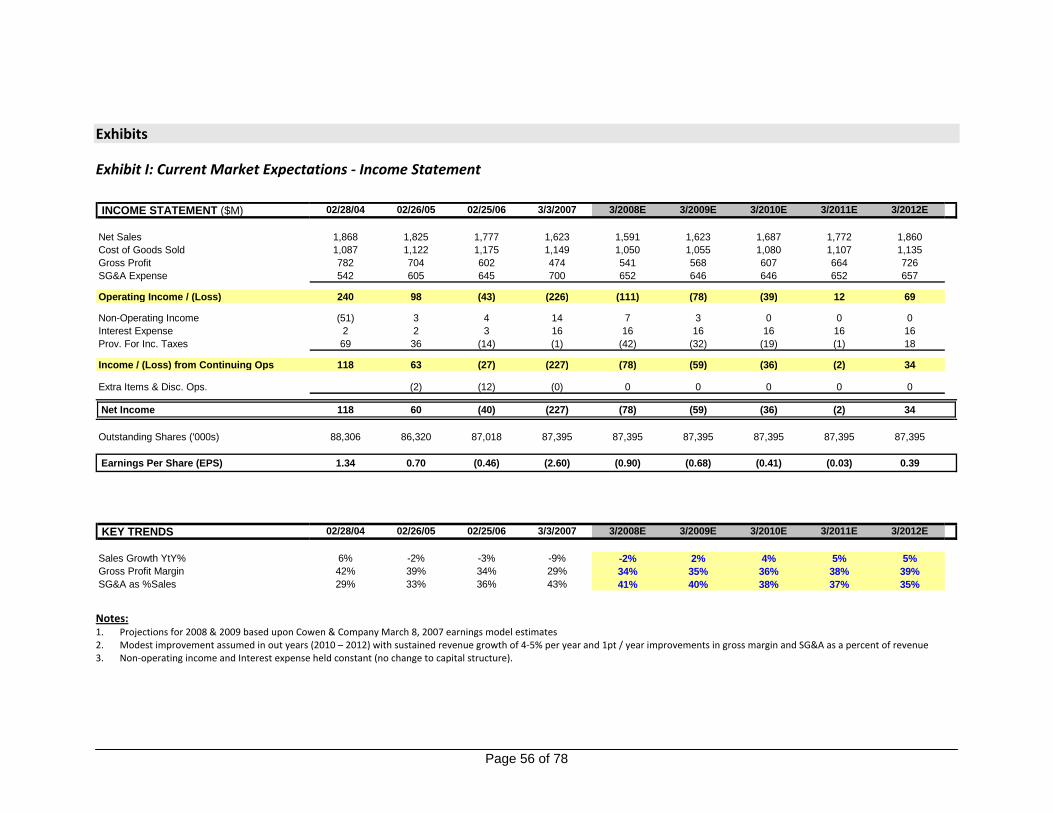

ANNUAL INCOME STATEMENT ($M) 02/28/04 02/26/05 02/25/06 3/3/2007

Net Sales 1,868 1,825 1,777 1,623 Cost of Goods Sold 1,087 1,122 1,175 1,149 Gross Profit 782 704 602 474 SG&A Expense 542 605 645 700

Operating Income / (Loss) 240 98 (43) (226)

Non-Operating Income (51) 3 4 14 Interest Expense 2 2 3 16 Prov. For Inc. Taxes 69 36 (14) (1)

Income / (Loss) from Continuing Ops 118 63 (27) (227)

Extra Items & Disc. Ops. (2) (12) (0)

Net Income 118 60 (40) (227)

Outstanding Shares ('000s) 88,306 86,320 87,018 87,395

Earnings Per Share (EPS) 1.34 0.70 (0.46) (2.60)

A closer look at this dramatic turn for the worse does not reveal a single driver,

as materially worsening performance can be observed in revenue growth, gross margin,

and expense management. Specifically, revenue has declined the past three

consecutive years and appears to be doing so at an accelerating rate. Based upon Pier

1’s own 10k disclosures, the gross margin deterioration is partially attributed to

promotional discounting and inventory write‐offs associated with less than projected

demand for specific products. Similarly, the growing SG&A expense is the result of

increased advertising expenses intended to drive increased store traffic and the

negative impact of relatively fixed corporate overhead versus declining revenue.

Overall, it would appear that Pier 1’s greatest challenge is driving stronger customer

demand; however it is also likely that additional cost and expense savings could be

realized.

Pier 1 has accumulated a material net operating loss (NOL) carry forward that

has resulted in a $35M tax asset as of year end fiscal 2007; however this asset value

Page 36 of 78

cannot be realized unless Pier 1 returns to profitability and will most likely continue to

grow in the short term.

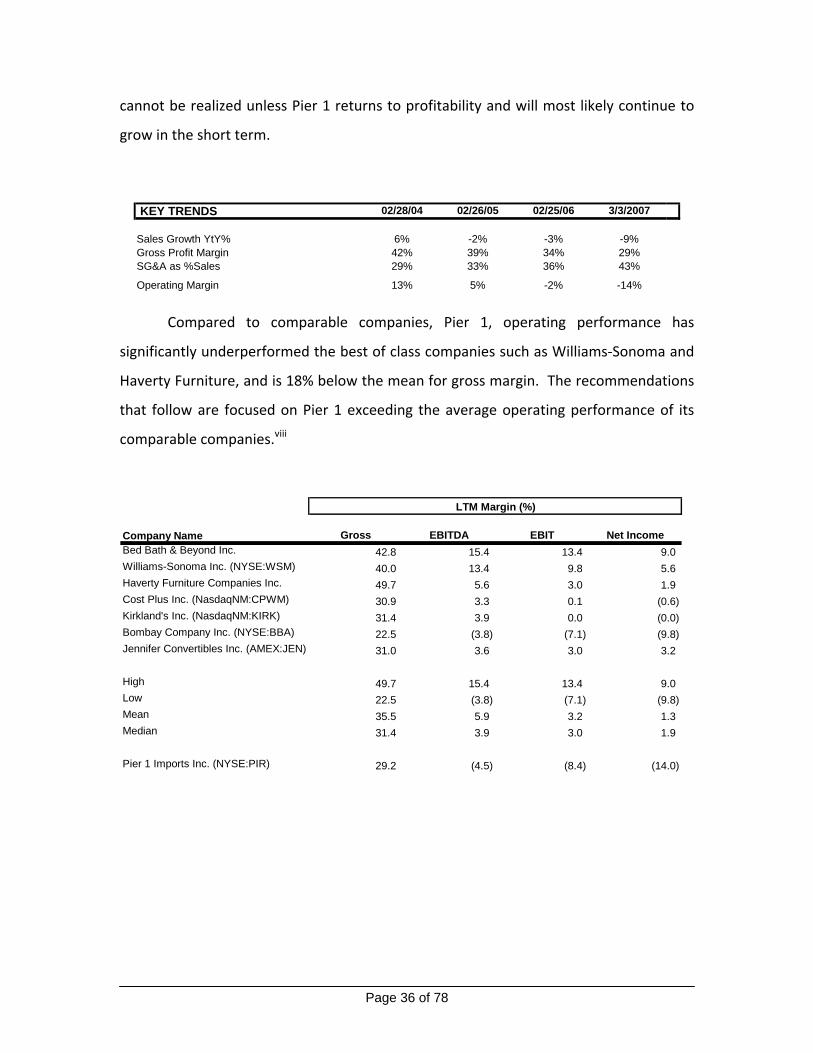

KEY TRENDS 02/28/04 02/26/05 02/25/06 3/3/2007

Sales Growth YtY% 6% -2% -3% -9%Gross Profit Margin 42% 39% 34% 29%SG&A as %Sales 29% 33% 36% 43%

Operating Margin 13% 5% -2% -14%

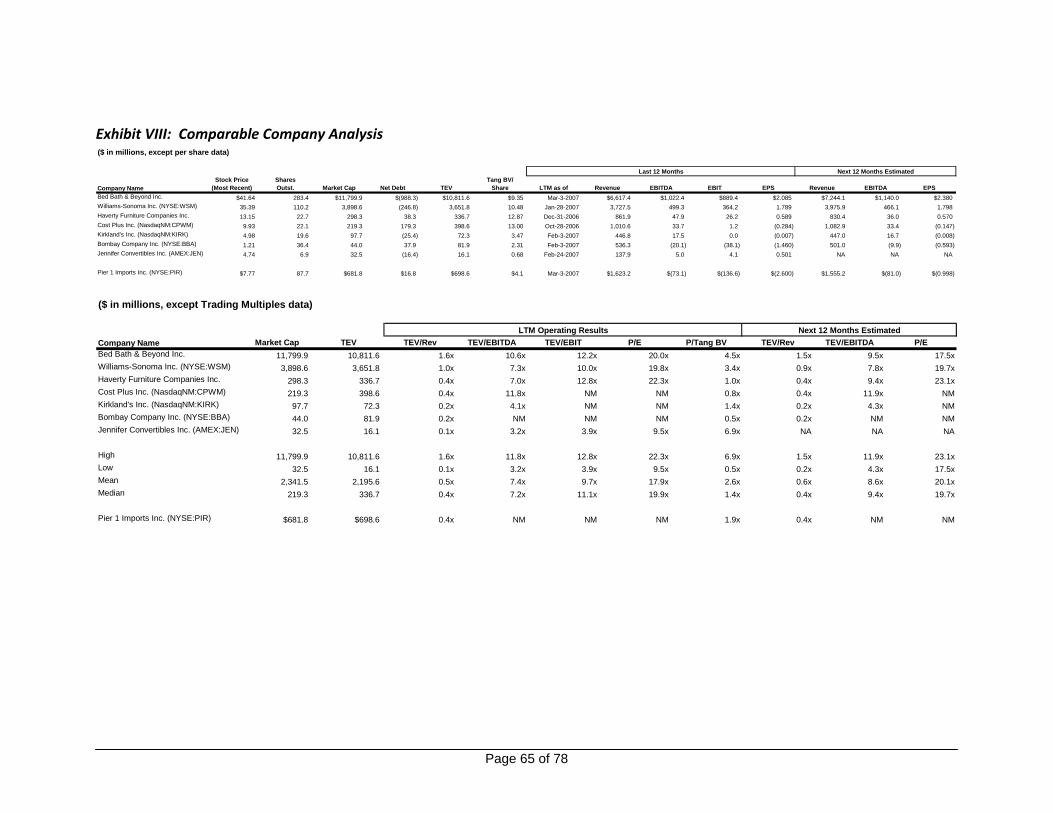

Compared to comparable companies, Pier 1, operating performance has

significantly underperformed the best of class companies such as Williams‐Sonoma and

Haverty Furniture, and is 18% below the mean for gross margin. The recommendations

that follow are focused on Pier 1 exceeding the average operating performance of its

comparable companies.viii

Company Name Gross EBITDA EBIT Net IncomeBed Bath & Beyond Inc. 42.8 15.4 13.4 9.0 Williams-Sonoma Inc. (NYSE:WSM) 40.0 13.4 9.8 5.6 Haverty Furniture Companies Inc. 49.7 5.6 3.0 1.9 Cost Plus Inc. (NasdaqNM:CPWM) 30.9 3.3 0.1 (0.6) Kirkland's Inc. (NasdaqNM:KIRK) 31.4 3.9 0.0 (0.0) Bombay Company Inc. (NYSE:BBA) 22.5 (3.8) (7.1) (9.8) Jennifer Convertibles Inc. (AMEX:JEN) 31.0 3.6 3.0 3.2

High 49.7 15.4 13.4 9.0 Low 22.5 (3.8) (7.1) (9.8) Mean 35.5 5.9 3.2 1.3 Median 31.4 3.9 3.0 1.9

Pier 1 Imports Inc. (NYSE:PIR) 29.2 (4.5) (8.4) (14.0)

LTM Margin (%)

Page 37 of 78

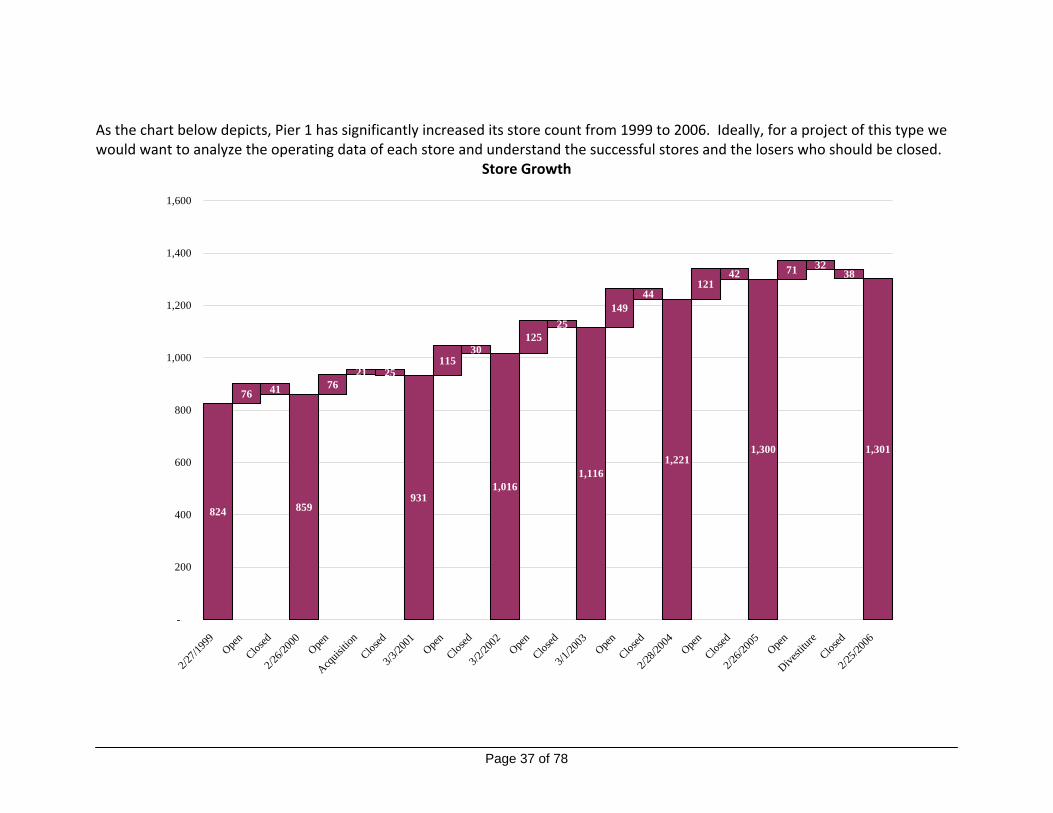

As the chart below depicts, Pier 1 has significantly increased its store count from 1999 to 2006. Ideally, for a project of this type we would want to analyze the operating data of each store and understand the successful stores and the losers who should be closed.

Store Growth

824

76 41

859

7621 25

931

11530

1,016

12525

1,116

14944

1,221

12142

1,300

71 3238

1,301

-

200

400

600

800

1,000

1,200

1,400

1,600

2/27/1

999

Open

Closed

2/26/2

000

Open

Acquis

ition

Closed

3/3/20

01Ope

nClos

ed3/2

/2002

Open

Closed

3/1/20

03Ope

nClos

ed2/2

8/200

4Ope

nClos

ed2/2

6/200

5Ope

nDive

stitur

eClos

ed2/2

5/200

6

Page 38 of 78

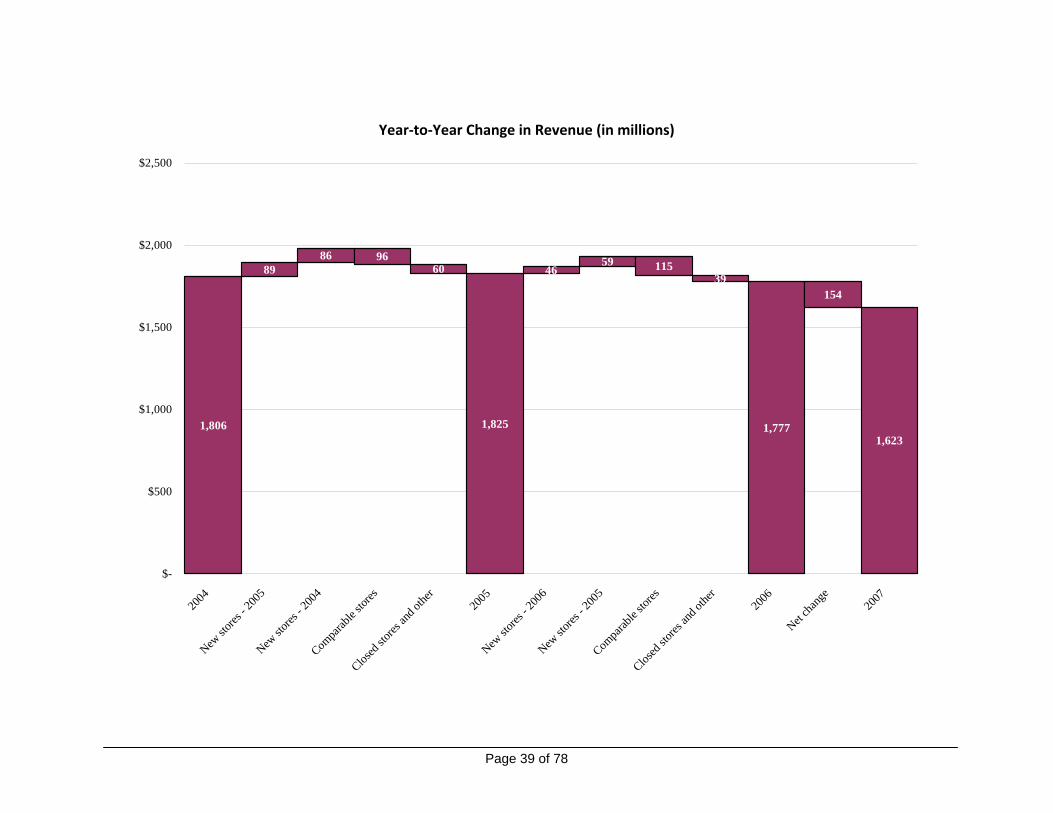

As is the case with most retailers, same store sales represent a key performance

metric given they most accurately reflect the overall health of the brand by excluding

the often material impact of new store openings and/or closings. In the case of Pier 1,

same store sales declined 7.1% for fiscal 2006 and 6.1% for fiscal 2005, representing the

core performance problem driving the overall revenue deterioration. Directly below is a

summary bridge of year‐to‐year revenue dynamics, which highlights the impact of

declining same store sales relative to new store growth and lost revenue from closed

stores. Clearly, the growth from the new stores has been inadequate to offset the

decline in existing stores.

($s millions) 2006

New stores opened during fiscal 2006 46 Sotres opened during fiscal 2005 59 Same Store Sales (115)Closed Stores (39)

Net Decrease in Sales (49)

Change in Revenue YtY

Page 39 of 78

Year‐to‐Year Change in Revenue (in millions)

1,806

8986 96

60 4659 115

39

1,777

154

1,6231,825

$-

$500

$1,000

$1,500

$2,000

$2,500

2004

New sto

res - 2

005

New sto

res - 2

004

Compa

rable

stores

Closed

stores

and o

ther

2005

New sto

res - 2

006

New sto

res - 2

005

Compa

rable

stores

Closed

stores

and o

ther

2006

Net ch

ange

2007

Page 40 of 78

Pier 1 has made significant capital expenditures in the last few years as it has

increased its store base. In 2006, Pier 1 made $51 million of capital expenditures, $31.5

million of which were for fixtures and leasehold improvements, $15.8 million were for

information systems enhancements and $3.5 million were for distribution centers.

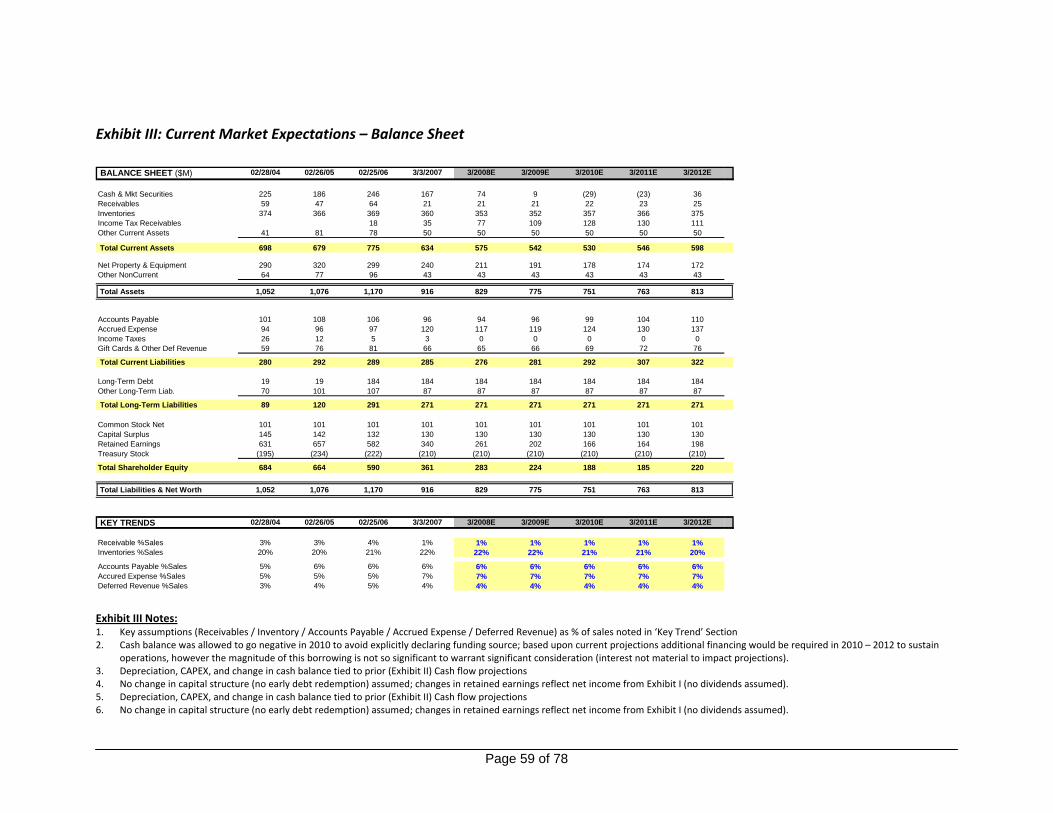

Liquidity Analysis

Pier 1 has consistently maintained a significant balance of cash and/or

marketable securities of approximately $200M over the past 5 years, likely in

recognition of the risks inherent to the retail industry given the volatility in consumer

tastes and fixed cost structure. Despite its recent poor performance, Pier 1

management has been able to generate additional cash to sustain this cash reserve

through the sale of its credit card operations in the fall of 2006, and finished its 2007

fiscal year (ended 3/3/07) with $167M of cash on hand. Based upon analyst estimates

and the company’s current cash burn‐rate, we project that this cash on hand should be

sufficient to sustain operations for at least 12 ‐ 18 months (raw projections indicate 2

years, however we believe there may be additional risk and seasonal working capital

requirements).

($M) 2008 2009 2010

Beginning Cash 167 74 13

-Less Net Cash Flow (93) (61) (40)

Ending Cash Balance 74 13 (27)

Projected Cash Burn

Also of note, Pier 1 ceased paying dividends in November 2006 and we do not

expect that management will resume payments until performance improves

significantly, alleviating $35M of prior cash flow obligations until operations can be

stabilized. Further, Pier 1 did execute a modest share buyback (250,000 shares for $4M)

in 2006. Although, $107M of authorized share repurchases remains available, we do

not expect that management will continue this activity given the current financial

condition (these assumptions included in above ‘cash burn’ projection).

Page 41 of 78

Finally, Pier 1’s business does have a moderate seasonal skew, as 25% of full year

revenue is earned in November and December. Accordingly, significant working capital

is required to support the necessary inventory build‐up in September – October. Given

the company’s current strong cash position, we do not believe that the 2007 holiday

season will present a liquidity problem, however if overall performance does not

improve the 2008 holiday season will likely represent a potential tipping point in which

Pier 1 will require additional financing.

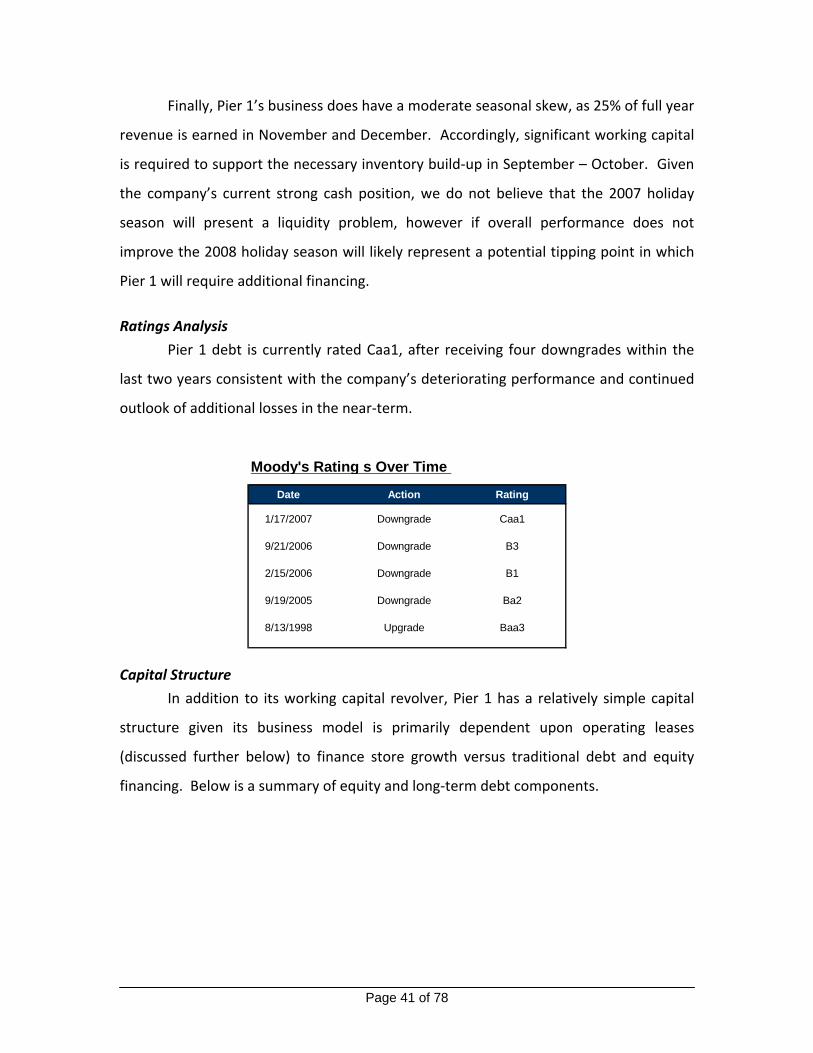

Ratings Analysis

Pier 1 debt is currently rated Caa1, after receiving four downgrades within the

last two years consistent with the company’s deteriorating performance and continued

outlook of additional losses in the near‐term.

Date Action Rating

1/17/2007 Downgrade Caa1

9/21/2006 Downgrade B3

2/15/2006 Downgrade B1

9/19/2005 Downgrade Ba2

8/13/1998 Upgrade Baa3

Moody's Rating s Over Time

Capital Structure

In addition to its working capital revolver, Pier 1 has a relatively simple capital

structure given its business model is primarily dependent upon operating leases

(discussed further below) to finance store growth versus traditional debt and equity

financing. Below is a summary of equity and long‐term debt components.

Page 42 of 78

EQUITYMarket Value

-Current Share Price (4/20) 7.76 -Shares Outstanding ('000s) 87,395 Equity Value / Mkt Cap ($M) 678

DEBTBook Value

-Convertible Senior Notes (6.375%) 165 -Industrial revenue bonds 19 Total LT Debt ($M) 184

Total Enterprise Value 862

Total Sharehold Equity & Debt Obligations

Debt Instruments

Pier 1 has historically not been very active in the capital markets as its debt

needs were minimal and its profitable operations allowed it to begin repurchasing stock.

However, as performance began to deteriorate, management sought debt financing in

early 2006, in the form of a $165M convertible bond offering. This timing was

somewhat fortuitous, as it preceded additional Moody’s downgrades and secured a

significant amount of long term financing on advantageous terms.

• Convertible Bonds – Issued in February 2006, these convertible senior notes (due

2036) carry an interest rate of 6.375% through 2011 and a rate of 6.125%

thereafter. Interest is payable semi‐annually in arrears. The notes are

convertible into shares of common stock, or equivalent cash, at an initial

conversion rate of 65.8 shares per $1,000 principal amount of Notes (implied

share price of $15.20 / share). However, this conversion can only be executed

under specific circumstances which require that the stock price trade above

$19.75 / share for at least 20 trading days in the period of 30 consecutive trading

days. Further, the notes may be redeemed by the company on or after February

2011 at par value.

• Industrial revenue bonds – These bonds were initially issued in 1987 to construct

three warehouse/distribution facilities. These tax‐exempt bonds mature in 2026

Page 43 of 78

and carry floating interest rates pegged to municipal debt interest rates resulting

in extremely low effective interest rates (4.1% in 2006).

• Secured Line of Credit – In addition to the $184M of long‐term debt, Pier 1 also

has an unutilized $325M secured credit facility which matures in November

2010. This facility is secured by the company’s inventory and carries an interest

rate of LIBOR +1.0%. Pier 1 has not utilized the cash borrowing from this line

since late 2005 when $38.5M was used to fund the working capital build‐up prior

to the holiday season (October – December) and the balance was paid in fully by

year end and has not been utilized since, likely due to the fact the proceeds from

the sale of the credit card operations have provided adequate liquidity. Pier 1

pays a fee of 1% for standby letters of credit, .5% for trade letters, and a

commitment fee of .25% for unused amounts

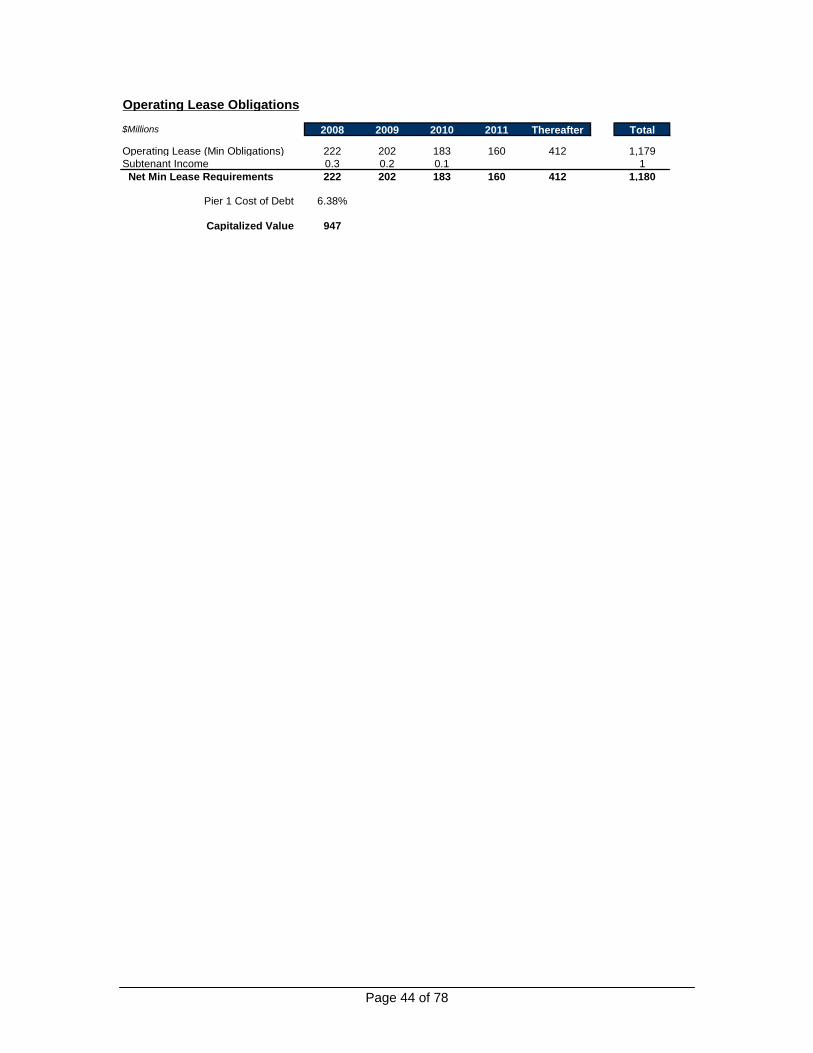

Operating Lease Obligations

Pier 1 has utilized operating lease agreements to finance its stores and

appropriately recognizes the associated rental expenses as costs of goods sold.

However, these leases represent relatively fixed (material fees payable in the event of

early termination) long‐term obligations and represent a significant fixed cost within

Pier 1’s business model. Below is the complete schedule of operating lease obligations

and an estimated current capitalized debt value of $947M.

The company does not disclose adequate information to determine the present

value asset‐value of these same leases; however, given macro real estate trends over

the past 10 years and fact that many under performing stores have already been closed

it is reasonable to assume the fair market value of these leases is greater than the

present value of the current lease obligations. Nevertheless, given these leases are

essential to the continue operation of Pier 1, this potential excess value should only be

considered in the event of company liquidation. Otherwise, this implicit value should be

recognized through the operation of the associated stores.

Page 44 of 78

$Millions 2008 2009 2010 2011 Thereafter Total

Operating Lease (Min Obligations) 222 202 183 160 412 1,179Subtenant Income 0.3 0.2 0.1 1 Net Min Lease Requirements 222 202 183 160 412 1,180

Pier 1 Cost of Debt 6.38%

Capitalized Value 947

Operating Lease Obligations

Page 45 of 78

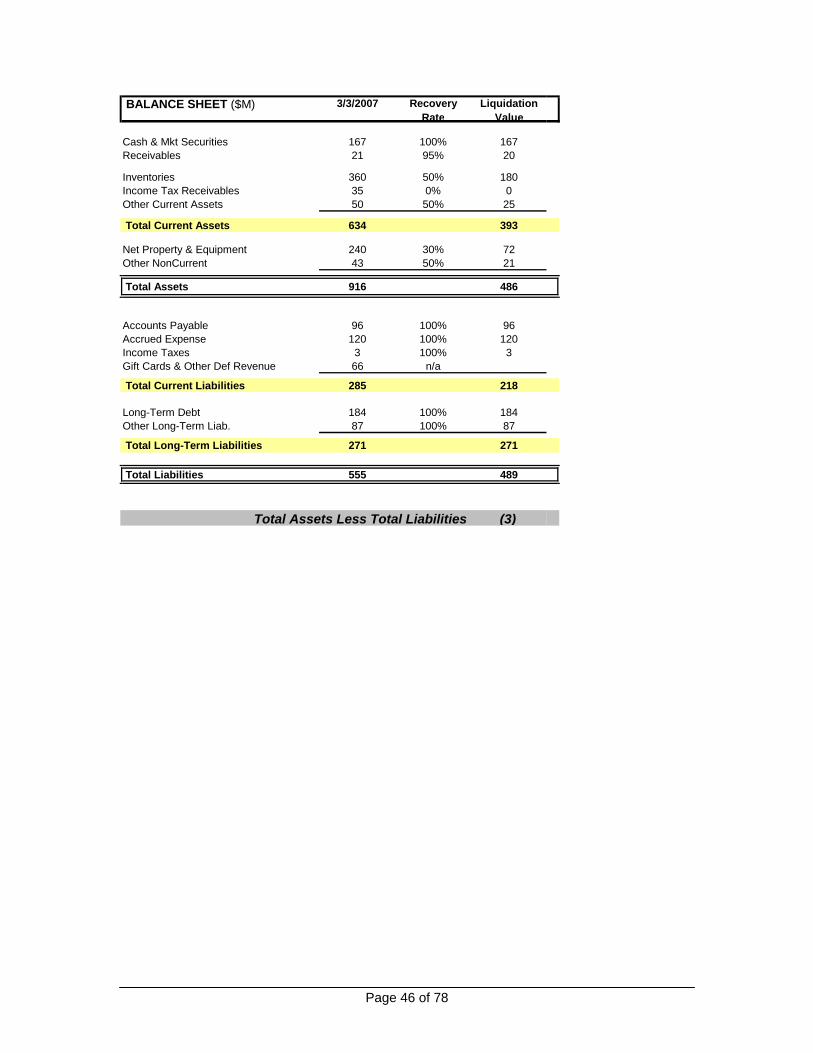

Discussion of valuations

Liquidation value

Liquidating Pier 1 may prove to be challenging, as the company’s most significant

assets: 1) its brand name and associated marketplace equity and 2) its portfolio of real

estate leases cannot easily be monetized. Further, selling the portfolio of leases to

another retailer or real estate interest may preclude the realization of value from the

Pier 1 brand as the brands strength is moderate at best and it is unlikely that any buyer

would be interested in the rights to the name only. It is also unclear as to what the

quality of the aggregate lease portfolio might be; given macro real estate trends over

the past ten years it is very possible that the value of Pier 1’s lease portfolio is greater

than the outstanding obligations, however given its poor financial performance its

equally possible that Pier 1 has made poor real estate decisions in the past and the lease

obligations may exceed their fair market value.

Below is a simple balance sheet liquidation estimate (excluding intangible value

of brand and potential lease value). This analysis would suggest there is little reason to

expect material proceeds in excess of liabilities and debt. Further, the current market

value is implicitly far greater than this liquidation view indicating that the market

continues to recognize the ‘going concern’ value of Pier 1 as being superior to the sum

of its parts from asset proceeds.

Page 46 of 78

BALANCE SHEET ($M) 3/3/2007 Recovery Rate

Liquidation Value

Cash & Mkt Securities 167 100% 167 Receivables 21 95% 20

Inventories 360 50% 180 Income Tax Receivables 35 0% 0 Other Current Assets 50 50% 25

Total Current Assets 634 393

Net Property & Equipment 240 30% 72 Other NonCurrent 43 50% 21

Total Assets 916 486

Accounts Payable 96 100% 96 Accrued Expense 120 100% 120 Income Taxes 3 100% 3 Gift Cards & Other Def Revenue 66 n/a

Total Current Liabilities 285 218

Long-Term Debt 184 100% 184 Other Long-Term Liab. 87 100% 87

Total Long-Term Liabilities 271 271

Total Liabilities 555 489

(3)Total Assets Less Total Liabilities

Page 47 of 78

Discussion of Alternatives

In order to determine the optimal strategy for Pier 1, we have evaluated all of

the potential alternatives available to management.

Status quo

Pier 1’s current strategy has been more dynamic than a simple ‘business as

usual’ strategy; management has clearly recognized the need to drive increased

customer demand and in‐store traffic and has invested accordingly. Further,

management has begun to close several underperforming stores each year, while

simultaneously opening new stores. However, to date, this strategy has not stemmed

the sales decline while management’s various investments in advertising and new stores

have accelerated the losses and negative cash flow.

This strategy would allow management to continue the initiatives already

underway and continue to invest in the Pier 1 brand and updating its product portfolio,

while continuing to pursue new store growth opportunities.

However, we believe that continuing this strategy will provide Pier 1 with a

limited ‘window of opportunity’ to turnaround same store sales before the negative

cash flow would force management to significantly restructure and seek additional

financing, both of which would likely force a cessation of the desired strategy.

Specifically, our estimates indicate that under the current strategy the company would

likely run out of cash by 2010, with potential liquidity risk prior to the 2009 holiday

season. Further, Pier 1’s current secured credit line is set to mature in 2010 prior to the

holiday season, and would likely not be renewed assuming Pier 1 does not outperform

current expectations between now and then, leaving the company with a nearly certain

cash shortfall in 2010 if not sooner. Therefore, we believe this approach to be a risky

proposition given the unpredictable nature of consumer taste and the significant

difficulty management has had to‐date addressing declining sales.

Page 48 of 78

($M) 2008 2009 2010

Beginning Cash 167 74 13

-Less Net Cash Flow (93) (61) (40)

Ending Cash Balance 74 13 (27)

Projected Cash Burn

Cost Savings Strategy

Clearly, there are significant opportunities to reduce costs. First, management

has yet to slash corporate overhead spending; in fact it continues to increase. Also, the

rate of store closure could be accelerated with the goal of closing the 10 – 20% of

bottom performing stores. Next, staffing within stores could be scaled back to more

accurately match anticipated store traffic. Finally marketing expenses could be scaled

back, as the company’s current on‐and‐off approach to television advertising is likely not

optimal. These actions, although somewhat draconian, would likely stem the operating

losses in the near‐term and provide Pier 1 with several years of continued operation.

However, Pier 1 risks further sales reductions as a result of reduced employees and

marketing expenses.

However, this strategy may only succeed in enabling a ‘slow death’ as the cost

savings would clearly slow the drain on cash, but ultimately may prevent success in a

retail business where marketing and product investments are required to drive demand.

Bankruptcy

In the case of Pier 1, bankruptcy is unlikely to offer significant proceeds as there

are few tangible assets outside of the brand identity itself. Although it is possible that

the portfolio of store leases may have value to another retail chain or investor willing to

re‐sell them, it is extremely unlikely that this value would represent an accretive

solution for shareholders relative to Pier 1’s current market capitalization and our prior

liquidity analysis that indicated zero net proceeds would be available to equity holders

based upon tangible asset sales.

Page 49 of 78

Despite Pier 1’s considerable financial challenges, the company remains far from

bankruptcy given its strong cash position. The company’s current stock price (Market

Cap of $678M) would appear to re‐affirm this position and accordingly bankruptcy

would not appear to be an optimal solution at this point.

Marketing Led Strategy

Clearly, driving customer demand is critical in all retail industries. One possible

strategy for Pier 1 would be to dramatically increase direct marketing efforts while

investing in store updates and new product lines. This would clearly be an extremely

aggressive strategy and in the very near term would accelerate the cash burn rate, but

would likely offer the greatest upside if successful.

However, there is little evidence that the current management team (or any

industry analyst) fully understands how to quickly reverse Pier 1’s fortunes with its core

customer base. Accordingly, pursuing this strategy would likely be the equivalent to

placing one large bet with what remains of the company’s resources.

Page 50 of 78

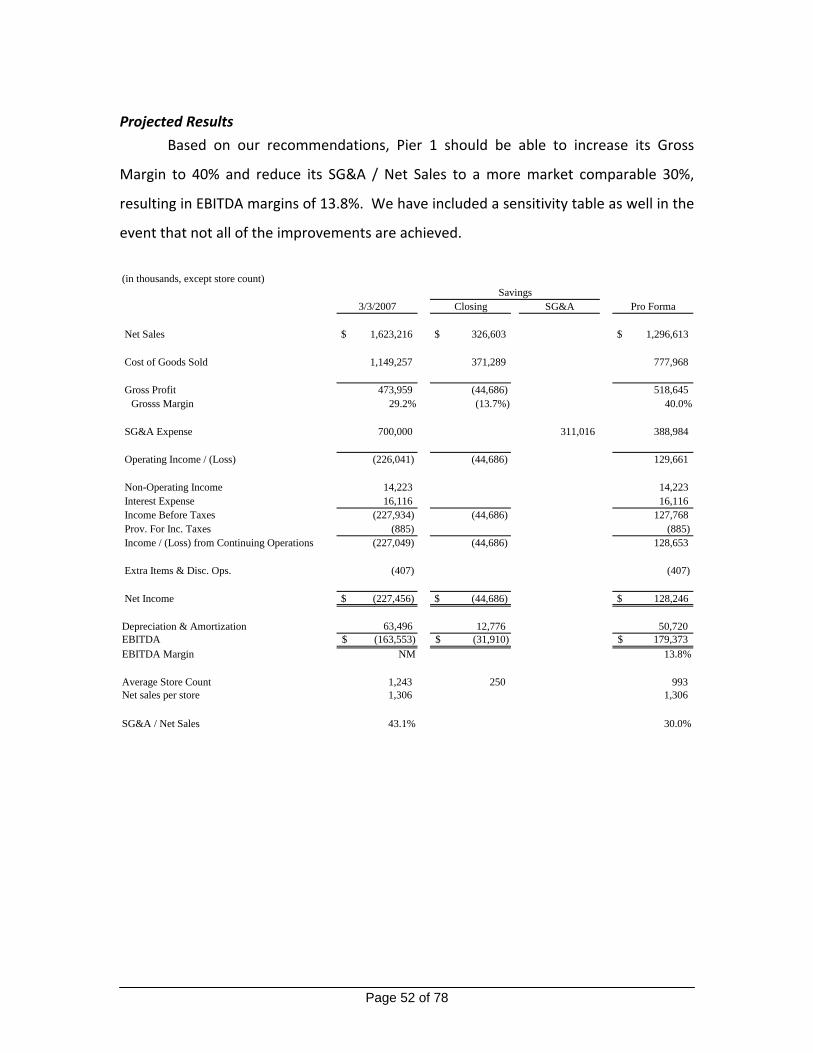

Recommendations

Immediate Action Plan

Pier 1 must take immediate action to close a significant portion of its

underperforming stores in an effort to stabilize its finances and right‐size its SG&A

expenses. Specifically, at least 20% of its current stores are operating at significant

losses without reasonable hope of improvement, and the company can ill afford to

continue to finance such money losing endeavors. Additionally, Pier 1 should look to

monetize its investment in its corporate headquarters. Further, the company has

confused its customers with its numerous and ever changing marketing campaigns, and

must refocus on its core segment of fashionable furnishings at value price points and