Item 11A - Santa Monica · their payment of School District Special Bond Tax Surcharge Measure ......

26

1 SANTA MONICA RENT CONTROL BOARD MEMORANDUM TO: Santa Monica Rent Control Board FROM: J. Stephen Lewis, General Counsel FOR MEETING OF: January 25, 2018 RE: Amendments to Regulations 3105, 3106, 3108, and 3109, and addition of new Regulation 3120, respecting limitations on rent surcharges for local taxes and local voted indebtedness. Subject Matter The Santa Monica Rent Control Board will hold a public hearing to consider whether to: adopt proposed new Regulation 3120 to specify that surcharges for local taxes and voted indebtedness may not be added to the rent for any controlled unit whose initial rental rate was established on or after September 1, 2017, or that is reassessed as the result of sale or improvement; and amend Board Regulations 3105, 3106, 3108, and 3109 to be consistent with proposed new Regulation 3120. How this Item was Initiated At its January 11 regular meeting, the Board held a public discussion about how to begin to phase out surcharges resulting from local taxes and voted indebtedness in view of the 2012 amendment to Charter Section 1805—which eliminated the authority under which such surcharges were authorized—without creating undue hardship for owners. After hearing from the public and deliberating, the Board directed staff to return at the next regular meeting, January 25, with amendments to existing surcharge regulations to immediately eliminate surcharges for new tenancies, Item 11A

Transcript of Item 11A - Santa Monica · their payment of School District Special Bond Tax Surcharge Measure ......

1

SANTA MONICA RENT CONTROL BOARD MEMORANDUM TO: Santa Monica Rent Control Board FROM: J. Stephen Lewis, General Counsel FOR MEETING OF: January 25, 2018 RE: Amendments to Regulations 3105, 3106, 3108, and

3109, and addition of new Regulation 3120, respecting limitations on rent surcharges for local taxes and local voted indebtedness.

Subject Matter

The Santa Monica Rent Control Board will hold a public hearing to consider

whether to:

adopt proposed new Regulation 3120 to specify that surcharges for local

taxes and voted indebtedness may not be added to the rent for any

controlled unit whose initial rental rate was established on or after

September 1, 2017, or that is reassessed as the result of sale or

improvement; and

amend Board Regulations 3105, 3106, 3108, and 3109 to be consistent

with proposed new Regulation 3120.

How this Item was Initiated

At its January 11 regular meeting, the Board held a public discussion about

how to begin to phase out surcharges resulting from local taxes and voted

indebtedness in view of the 2012 amendment to Charter Section 1805—which

eliminated the authority under which such surcharges were authorized—without

creating undue hardship for owners.

After hearing from the public and deliberating, the Board directed staff to

return at the next regular meeting, January 25, with amendments to existing

surcharge regulations to immediately eliminate surcharges for new tenancies,

Item 11A

2

and tenancies in buildings that are reassessed due to a qualifying transfer of

ownership or significant improvements.

Background

Until December 2012, Article XVIII (the portion of the Charter that includes the

city’s rent control law) included the following sentence, in Section 1805,

subdivision (b):

Each year the Board shall generally adjust rents … upward by

granting landlords a utility and tax increase adjustment for actual

increases in the City of Santa Monica for taxes and utilities.

Over the years, the Board accomplished this in two different ways. It adjusted

rents to account for some tax increases, and nearly all utility-cost increases, by

incorporating them into the formula that it used when deciding the percentage by

which annual rents could increase. It adjusted rents to account for other taxes

(and bonds) in a less subtle fashion: by enacting regulations allowing owners to

add them to tenant’s rents directly, as a surcharge on a unit’s maximum

allowable rent. All of the surcharges at issue here are the result of that approach.

The regulations allowing those surcharges are as follows:

Regulation 3105, allowing a surcharge by which owners can recoup

their payment of School District Special Bond Tax Surcharge Measure

ES, approved by the voters in 1990, and Community College District

Special Bond Measure T, approved by the voters in 1992;

Regulation 3106, allowing a surcharge by which owners can recoup

their payment of the Stormwater Management User Fee, enacted by

the City Council in 1995;

Regulation 3108, allowing a surcharge by which owners can recoup

their payment of the Clean Beaches and Ocean Parcel Tax, enacted by

the City Council in 2006.

Regulation 3109, allowing a surcharge by which owners can recoup

their payment of a School District Special Tax approved by the voters in

2008.

At some point, the Board neglected to account for certain new taxes and

voted indebtedness, either as a component of the annual general adjustment

formula, or as a surcharge added to controlled rents. The Board was sued, and

settled that lawsuit by agreeing to allow owners of controlled units to recover their

overhead resulting from local taxes or voted indebtedness, “unless Section

3

1805(b) is changed by voter amendment to the Rent Control Law.” As noted

above, that change occurred in 2012.

Under Charter Section 1805’s current iteration, the annual general adjustment

is now a simple percentage of the Consumer Price Index. Gone is any

requirement—and any allowance—for additions to rents in the form of pass-

throughs.1 Nothing in the current iteration of the City Charter, and nothing in the

2011 lawsuit settlement, requires the Board to continue to permit them. Indeed,

the City Attorney’s impartial analysis of Measure GA—the ballot measure by

which the voters amended Charter Section 1805—specifically notes that the

amendment was intended to do away with the inclusion of specific landlord

expenses, including those related to taxes, in the computation of controlled rents.

A copy of that analysis is included with this staff report as Exhibit A.

The Board has also heard from numerous tenants who have complained of

the hardships caused by increases in their rents due to surcharges. New tenants,

whose landlords have already established their rents at market level, have

complained that they have been surprised when, a year after their tenancies

began, their landlords not only imposed annual inflationary adjustments, but

added surcharges—sometimes in the amount of several hundred dollars

annually—to rents that presumably already include a full accounting for the

owner’s overhead. Longer-term tenants, including some on fixed incomes, have

informed the Board of annual rent increases amounting to several hundred

dollars above the annual general adjustment, resulting from tax-based

surcharges imposed after their buildings were sold and reassessed.

In view of these legal and factual realities, the Board has announced its

intention to “sunset,” or phase out, existing surcharges. As a first step to doing

so, it directed staff to draft proposed regulations to disallow surcharges for any

unit as to which any of the following three things are true:

1. The unit’s rent was established as the result of a new tenancy after the

unit had been vacated;

2. The unit is in a building that was reassessed as the result of an

ownership transfer; or

1 Members of the public have approached the Board to allow for pass throughs of various

expenses, such as earthquake-retrofitting costs, new voted indebtedness, and utility costs. In view of the voters’ elimination of the sole Charter provision under which such pass-throughs could have been authorized, the Board has clarified that they are not authorized.

4

3. The unit is on a property that was reassessed as the result of significant

improvements.

Proposed regulation 3120, attached to this report as Exhibit B, includes these

provisions, as well as amendments to existing surcharge regulations as

necessary to be consistent with the proposed new regulation.

With respect to each of the above three categories, the Board stated at its last

meeting that it wished to have the inability to collect rent surcharges go into effect

“immediately.” As drafted, each of them does so, by specifying that it goes into

effect on February 1. In order to provide information to all affected landlords and

tenants before the changes go into effect, staff has also proposed an alternative

recommendation, under which the changes would go into effect on March 1.

Proposed Regulation 3120(c) specifies that the “new tenancies” to which it

would apply are those that began since the last time the Board allowed the

imposition of an annual general adjustment—September 1, 2017. This is to

prevent new tenants, whose landlords have recently established their rents at

market rates, from having surcharges added to their rents in addition to next

year’s general adjustment. This change would be prospective only, however.

While any landlord who has been collecting a surcharge since a new tenancy’s

inception would be required to reduce the affected unit’s rent by the amount of

the surcharge going forward, no collection of a surcharge occurring before

February 1 of this year would constitute an overcharge.

With respect to reassessments resulting from ownership changes, proposed

Regulation 3120(d)(1) references California Constitution Article XIIIA § 1

(Proposition 13). This is to clarify that only actual ownership changes—not, for

example, the transfer of a property into a revocable living trust for estate planning

purposes—that result in a reassessment, would thus result in the loss of ability to

collect rent surcharges.

With respect to reassessments resulting from significant improvements,

proposed Regulation 3120(d)(2) references California Constitution Article XVIIIA

§ 2 and California Revenue & Taxation Code § 70. These references clarify that

surcharges will no longer be permitted for properties reassessed as the result of

“new construction,” but that “new construction” includes all significant

improvements warranting a property’s reassessment, as specified by state tax

law.

5

Finally, the Board directed staff to present with the attached proposed

regulatory amendments a sample of what the general adjustment calculation

sheet would look like, if the proposed amendments were adopted. That sample is

attached to this report as Exhibit C.

Recommendation

Staff recommends that the Board hear from the public, and then publicly

deliberate, about whether to adopt the proposed regulatory amendments as

presented in Exhibit B.

Alternative Recommendation

Alternatively, if, after hearing from the public and deliberating, the Board opts

to adopt the proposed substantive regulatory changes, but wishes to provide time

for staff to inform the affected public of those changes, staff recommends that the

Board adopt the amended and new regulations as proposed, with the exception

that they would be effective March 1, rather than February 1, 2018.

EXHIBIT A

1/18/2018 Measure GA - Ballot Measures - SMVote

City of

Santa Monica® MENU

Impartial Analysis

Text

Argument in Favor

Espai1ol

Measure GA Shall the City Charter be amended to allow the annual rent control general adjustment to be

based on 75% of the annual percentage change in the Consumer Price Index, but limited to an

adjustment between 0% and 6%; and to give the Rent Control Board discretion, after a public

hearing, to impose a dollar limit, within the 0-6% range, calculated using the same formula

employed when imposing a limit under the existing general adjustment formula?

CITY ATI'ORNEY'S IMPARTIAL ANALYSIS OF MEASUREGA

BALLOT MEASURE AMENDING CITY CHARTER PROVISIONS GOVERNING THE COMPUTATION, APPLICATION AND

http://www.smvote.org/ballotmeasures/detail.aspx?id=35051#1mpartia1Analysis 1/8

1/18/2018 Measure GA - Ballot Measures - SMVote

ANNOUNCEMENT OF THE ANNUAL GENERAL ADJUSTMENT OF RENT CEILINGS FOR CONTROLLED RENTAL UNITS

This proposed measure would amend City Charter Sections 1803, 1804 and 1805 in order to

change the way that the Rent Control Board establishes the annual general adjustment to rent

ceilings for rent controlled units in Santa Monica.

At present, the City Charter does not specify a particular formula for use in computing the

annual general adjustment. Instead, Charter Section 1805 requires the Board to adjust rents

upward due to actual increases in landlords' utility, tax and maintenance expenses or downward

due to actual decreases in landlords' tax costs. Additionally, Section 1805 allows the Rent

Control Board to adjust ceilings up or down either for all controlled units or for particular

categories of units and also allows the Board to postpone the effective date of the change.

The formula that the Rent Control Board currently utilizes to compute the general adjustment is

known as the "component ratio to gross rent" formula. It is intended, in part, to yield a general

adjustment reflecting changes in landlords' actual costs; and the formula has the advantage of

capturing some of those changes. However, the formula is complex; and the results it yields are

consequently difficult to predict. Moreover, the results may not accurately reflect changes in

landlords' actual costs since reliable data about some cost categories is unavailable.

Additionally, the Rent Board's authority to make adjustments by category and to postpone the

effective date both increase the difficulty of making accurate predictions about the general

adjustment.

The proposed measure would establish a new adjustment formula and incorporate it into the

City Charter. That formula would tie the general adjustment to the inflation rate by basing the

adjustment on 75% of the annual percentage change in the Consumer Price Index for the Los

Angeles area, subject to two limitations. First, the proposal would limit the annual adjustment to

a range of zero to no more than six percent. Second, it would grant the Rent Control Board the

authority, after holding a public hearing, to impose a dollar limit on any year's general

adjustment according to a specified formula. Additionally, the proposed measure would make

the general adjustment uniformly applicable to all controlled units and would require that the

amount of the adjustment be announced, annually, by June 30th to be effective September 1st.

If the proposed City Charter amendment is adopted, future general adjustments would become

more predictable and computations would be more readily verifiable. Thus, the process would

be more transparent; and uncertainty would be reduced for both tenants and owners.

http://www.smvote.org/ballotmeasures/detail.aspx?id=35051#1mpartia1Analysis 2/8

EXHIBIT B

1

3105. School District Special Bond Tax Surcharge Santa Monica

Community College District Special Bond Surcharge

(a) The surcharges provided by this regulation are meant to reimburse owners of

controlled residential rental properties for the cost of the School District

Special Bond Tax Surcharge (Proposition ES) as approved by the voters on

November 6, 1990, and for the cost of the Santa Monica Community College

District Special Bond (Proposition T) approved by the voters in November,

1992.

(b) Duration of Surcharge

In addition to the monthly rentExcept as limited by Regulation 3120,

subdivisions (c) and (d), a landlord may collect a monthly surcharge in

accordance with this section on any controlled rental unit for each month

from January 1, 1992 until December 31, 2020. The actual surcharge for

each fiscal year beginning July 1 may be collected in monthly installments

commencing the following January 1, or any month within the same calendar

year, and continuing for the next twelve months thereafter.

(c) Determination of Surcharge

(1) The monthly surcharge shall not exceed an amount equal to the amount

of the yearly school bond property tax assessment as determined by the

Santa Monica-Malibu Unified School District, plus the amount of the

yearly Santa Monica Community College District Special Bond

assessment, divided by the total number of units on the parcel divided

into twelve monthly payments.

(2) For purposes of this subsection, the term "units" includes, but is not

limited to, all units in a controlled rental property that are used for

residential rental purposes or for commercial purposes, are owner-

occupied or relative occupied, are occupied pursuant to a Section 8

housing agreement, and/or are participating in the Incentive Housing

program.

(3) The yearly tax surcharge per parcel will change each fiscal year based

on the actual assessed values, the timing of the sale of the bonds and

the interest rates on any bonds sold. The owner of each assessed

parcel will receive notice from the County Assessor's Office and/or the

School District and/or the Community College District of the amount of

the yearly School Bond Tax Surcharge and the yearly Santa Monica

Community College District Special Bond Surcharge.

2

(4) Upon notice by the County Assessor's Office of any change in the

assessed valuation of the parcel which affects the surcharges, the

landlord shall recalculate the surcharges as provided in this regulation

and give notice to the tenants of the change in the rent as set forth in

subsection (d) of this regulation. Any reassessment in the property tax

that results in a reduction of the School Bond Tax Surcharge and/or the

Santa Monica Community College District Special Bond Surcharge must

be recalculated and renoticed within thirty days of the receipt of the

notice of reassessment by the County Assessor's office.

(d) Notice Requirements

(1) Before imposing any surcharge under this section, A landlord shall must

notify each the affected tenant of a rent increase pursuant to this

regulation. The notice must comply with all noticing requirements set

forth in Civil Code Section 827.

(2) The Board shall promulgate a form for the notice required by this

regulation.

(3) The notice shall contain the following information: the amount of the

School Bond Tax Surcharge and/or Santa Monica Community College

District Special Bond Surcharge for the property; the number of units on

the property; the amount of the monthly per-unit surcharge; and, the

amount of the maximum lawful rent, including all fees and surcharges. A

copy of the portions of the Joint Consolidated Tax Bill or other official

notification that reflects the School Bond Tax Assessment, and/or Santa

Monica Community College District Special Bond Assessment, and the

parcel number shall be attached to the notice.

(4) Failure to comply with the notice requirements set forth above shall

render any increase excess rent within the meaning of Chapter 8.

3106. Stormwater Management User Fee Surcharge

(a) The surcharge provided by this regulation is meant to reimburse owners of

controlled residential rental properties for the cost of the Stormwater

Management User Fee established pursuant to City Ordinance 1811 (CCS),

enacted by the Santa Monica City Council on July 25, 1995.

(b) Duration of Surcharge

In addition to the monthly rent, a landlord may collect a monthly surcharge in

3

accordance with this section on any controlled rental unit for each month no

earlier than January 1, 1996, and which shall expire upon the repeal or

expiration of Santa Monica City Ordinance 1811 (CCS). Except as limited by

Regulation 3120, subdivisions (c) and (d), the actual surcharge for each

fiscal year beginning July 1, 1996 may be collected in monthly installments

commencing the following January 1, or any month within the same calendar

year, and continuing for the next twelve months thereafter.

(c) Determination of Surcharge

(1) The monthly surcharge shall not exceed an amount equal to the amount

of the Stormwater Management User Fee, as determined by Ordinance

1811, divided by the total number of units on the parcel, divided into

twelve monthly payments.

(2) For purposes of this subsection, the term "units" includes, but is not

limited to, all units in a controlled rental property that are used for

residential rental purposes or for commercial purposes, including owner-

occupied or relative occupied units, units occupied pursuant to a Section

8 housing agreement, and/or units participating in the Incentive Housing

program.

(3) Upon notice by the County Assessor's Office of the Stormwater

Management Fee, the landlord shall calculate the surcharge provided in

this regulation and give notice to the tenants of the amount of the per

unit surcharge as set forth in subsection (d) of this regulation.

(d) Notice Requirements

(1) Before imposing any surcharge under this section, Aa landlord shall

must notify each affected tenant of the amount of the Stormwater

Management User Fee surcharge pursuant to this regulation. The notice

must comply with all noticing requirements set forth in Civil Code

Section 827.

(2) The notice shall contain the following information: the amount of the

Stormwater Management User Fee for the property; the number of units

on the property; the amount of the monthly per-unit surcharge; and, the

amount of the maximum lawful rent, including all fees and surcharges. A

copy of the portions of the Joint Consolidated Tax Bill or other official

notification that reflects the School Bond Tax Assessment, and/or Santa

Monica Community College District Special Bond Assessment, and the

parcel number shall be attached to the notice.

4

(3) Failure to comply with the notice requirements set forth above shall

render any surcharge excess rent within the meaning of §1809 of the

Charter and Chapter 8 of the Board's regulations.

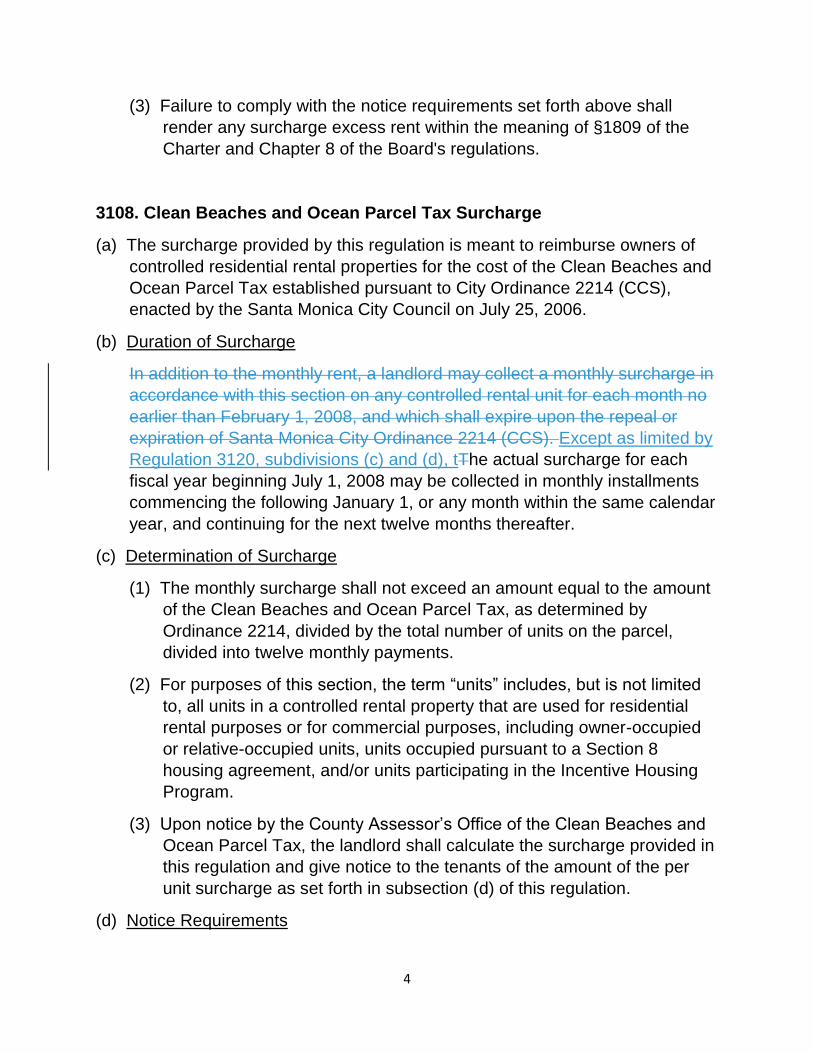

3108. Clean Beaches and Ocean Parcel Tax Surcharge

(a) The surcharge provided by this regulation is meant to reimburse owners of

controlled residential rental properties for the cost of the Clean Beaches and

Ocean Parcel Tax established pursuant to City Ordinance 2214 (CCS),

enacted by the Santa Monica City Council on July 25, 2006.

(b) Duration of Surcharge

In addition to the monthly rent, a landlord may collect a monthly surcharge in

accordance with this section on any controlled rental unit for each month no

earlier than February 1, 2008, and which shall expire upon the repeal or

expiration of Santa Monica City Ordinance 2214 (CCS). Except as limited by

Regulation 3120, subdivisions (c) and (d), tThe actual surcharge for each

fiscal year beginning July 1, 2008 may be collected in monthly installments

commencing the following January 1, or any month within the same calendar

year, and continuing for the next twelve months thereafter.

(c) Determination of Surcharge

(1) The monthly surcharge shall not exceed an amount equal to the amount

of the Clean Beaches and Ocean Parcel Tax, as determined by

Ordinance 2214, divided by the total number of units on the parcel,

divided into twelve monthly payments.

(2) For purposes of this section, the term “units” includes, but is not limited

to, all units in a controlled rental property that are used for residential

rental purposes or for commercial purposes, including owner-occupied

or relative-occupied units, units occupied pursuant to a Section 8

housing agreement, and/or units participating in the Incentive Housing

Program.

(3) Upon notice by the County Assessor’s Office of the Clean Beaches and

Ocean Parcel Tax, the landlord shall calculate the surcharge provided in

this regulation and give notice to the tenants of the amount of the per

unit surcharge as set forth in subsection (d) of this regulation.

(d) Notice Requirements

5

(1) Before imposing any surcharge under this section, Aa landlord mustshall

notify each affected tenant of the amount of the Clean Beaches and

Ocean Parcel Tax surcharge pursuant to this regulation. The notice

must comply with all noticing requirements set forth in Civil Code section

827.

(2) The notice shall contain the following information: the amount of the

Clean Beaches and Ocean Parcel Tax for the property; the number of

units on the property; the amount of the monthly per-unit surcharge;

and, the amount of the maximum lawful rent, including all fees and

surcharges. A copy of the portions of the Joint Consolidated Tax Bill or

other official notification that reflects the Clean Beaches and Ocean

Parcel Tax, and the parcel number shall be attached to the notice.

(3) Failure to comply with the notice requirements set forth above shall

render any surcharge excess rent within the meaning of section 1809 of

the Charter and Chapter 8 of the Board’s regulations.

(e) Exemptions

(1) Section 7.64.060 of the Santa Monica Municipal Code authorizes the

City Council to establish by resolution special exemption procedures

and eligibility criteria based on income, age or disability for the Clean

Beaches and Ocean Tax. The City Council established special

exemption procedures for low-income residents in Resolution 10248

(CCS). All property owners and renters who meet the Clean Beaches

and Ocean Tax Exemption eligibility criteria are exempt from the Clean

Beaches and Ocean Tax.

(2) The maximum dollar amount of gross household income for single-

person households for purposes of Clean Beaches and Ocean Parcel

Tax Exemption eligibility shall be twenty five thousand and two dollars

($25,002).

(3) The maximum dollar amount of gross household income for households

of two or more persons for purposes of Clean Beaches and Ocean

Parcel Tax Exemption eligibility shall be twenty eight thousand six

hundred and fifty dollars ($28,650).

(4) On July 1, 2008 and in subsequent years on the same date thereafter,

the maximum dollar amounts of gross household income for single and

two-or-more person households for purposes of Clean Beaches and

Ocean Parcel Tax Exemption eligibility as set forth above shall be

6

adjusted by the Los Angeles-Riverside-Orange County Consumer Price

Index for Wage Earners and Clerical Workers (CPI-W) for the previous

calendar year.

(5) Application for determination of eligibility for fee waiver under this section

must be on a form provided by the City.

3109. School District Qualified Special Tax Surcharge (Measure R)

(a) The surcharge provided by this regulation is to reimburse owners of

controlled residential rental properties for the cost of the School District

Qualified Special Tax of $346 per year, per parcel, adjusted annually for

inflation, as approved by the voters on February 5, 2008.

(b) Duration of Surcharge

In addition to the monthly rentExcept as limited by Regulation 3120,

subdivisions (c) and (d), a landlord may collect a monthly surcharge in

accordance with this section on any controlled rental unit starting no earlier

than January 1, 2009. The surcharge shall expire upon the repeal of School

District Qualified Special Tax (Measure R). The actual surcharge for each

fiscal year beginning July 1, 2008 may be collected in monthly installments

commencing the following January 1, or any month within the same calendar

year, and continuing for the next twelve months thereafter. The landlord shall

not collect this surcharge for any year for which the landlord has obtained a

senior exemption to the qualified special tax for the parcel from the Board of

Education of the District. The landlord shall not collect this surcharge during

any month in which the landlord has not paid this tax and the payment is

overdue.

(c) Determination of Surcharge

(1) The monthly surcharge shall not exceed an amount equal to the amount

of the School District Qualified Special Tax, divided by the total number

of units on the parcel, divided into twelve monthly payments.

(2) For purposes of this subsection, the term "units" includes, but is not

limited to, all units in a controlled rental property that are used for

residential rental purposes or for commercial purposes, including owner-

occupied or relative-occupied units, units occupied pursuant to a Section

8 housing agreement, and/or units participating in the Incentive Housing

program.

7

(3) Upon notice by the County Assessor's Office of the School District

Qualified Special Tax, the landlord shall calculate the surcharge

provided in this regulation and give notice to the tenants of the amount

of the per-unit surcharge as set forth in subsection (d) of this regulation.

(d) Notice Requirements

(1) Before imposing any surcharge under this section, Aa landlord shall

must notify each affected tenant of the amount of the School District

Qualified Special Tax surcharge pursuant to this regulation. The notice

must comply with all noticing requirements set forth in Civil Code

Section 827.

(2) The notice shall contain the following information: the amount of the

School District Qualified Special Tax for the parcel; the number of units

on the parcel; the amount of the monthly per-unit surcharge; and, the

amount of the maximum lawful rent, including all fees and surcharges.

(3) Failure to comply with the notice requirements set forth above shall

render any surcharge excess rent within the meaning of section 1809 of

the Charter and Chapter 8 of the Board's regulations.

3120. Limitation on Surcharges

(a) The Board finds and declares that permitting landlords to add surcharges to

rents in order to recoup their payment of local taxes and voted indebtedness

is inconsistent with the Board’s twin mandates, stated in Charter Section

1800, to regulate rents so that they will not be increased unreasonably, and

to ensure that landlords will receive no more than a fair return.

(b) The Board further finds and declares that:

(1) Because the majority of past and existing regulations allowing

landlords to add surcharges to rents in order to recoup their payment

of local taxes and voted indebtedness were enacted before landlords

had the right to establish initial rents for new tenancies, the Board

reasonably concluded, at those times, that permitting the surcharges

was consistent with Charter Section 1800;

(2) Regardless of whether permitting surcharges for landlords’ local tax

liabilities was consistent with Charter Section 1800, until 2012, Charter

Section 1805 required the Board to account for those liabilities when

establishing annual across-the-board rent increases;

8

(3) When the electors of the City of Santa Monica amended Charter

Section 1805 in 2012, they eliminated the provision authorizing the

Board to account for landlords’ local tax liabilities as part of its

calculation of annual general adjustments;

(4) Since 1999, initial rents for units in roughly 90% of controlled buildings

were established at market level, with the result that nearly every

owner of controlled units is currently earning more than the

constitutionally-required fair return;

(5) The Rent Control Law continues to provide any landlord who can

demonstrate that he or she is not earning a fair return to petition for

rent increases sufficient to provide one.

(c) Beginning February 1, 2018, no surcharge may be added to a unit’s rent—

other than a charge to recover fifty percent of registration fees, as permitted

under Charter Section 1803(n)—for any unit with an initial rent that was

established on or after September 1, 2017.

(d) No surcharge may be added to a unit’s rent—other than a charge to recover

fifty percent of registration fees, as permitted under Charter Section

1803(n)—for any unit on a parcel about which either of the following is true:

(1) The parcel was reassessed, as authorized by California Constitution

Article XIIIA, § 1 et seq. (Proposition 13), as the result of a change of

ownership occurring on or after February 1, 2018;

(2) An improvement on the parcel was reassessed, as authorized by

California Constitution Article XIIIA, § 2 and California Revenue and

Taxation Code § 70, on the basis of new construction that was

completed on or after February 1, 2018.

EXHIBIT C

Blank form provided by the Santa Monica Rent Control Board

NOTICE OF CHANGE IN TERMS OF TENANCY 2018

To:

tenant(s) in possession

, Santa Monica, CA

address unit number zip code

According to Santa Monica Rent Control Regulation 3035 and Board Resolution 18-XXX, you are hereby notified that thirty days after serving you with this notice (but not before September 1, 2018), the monthly rent for the premises you occupy will be increased as indicated below. NOTE: If your tenancy started on or after September 1, 2017, your unit is not eligible for the 2018 General Adjustment.

Enter the 2017-2018 Maximum Allowable Rent (MAR) ............................................................. $ .00

The registration fee and other surcharges are not included in the MAR.

If Line 1 is $X,XXX or less, multiply amount on Line 1 by .0X (X.0%) ........................................... $

If Line 1 is $X,XXX or more, enter $XX.

Add lines 1 and 2 and round to a whole dollar amount (for $0.50 or more, round up).

This is your 2018–2019 MAR ....................................... $ .00

Enter $8.25 (tenant’s share of Registration Fee) or $0.00 (if fee waiver is in effect) …….......... . $

Calculate surcharges Amount on Tax Bill

Calculate Adjustment

Adjusted Tax

Enter Total # of Units

Divide by 12 Months

Surcharge per Unit

5a Community College Bond1 $ ÷ ÷ 12 $

5b Unified Schools Bond1 $ x 0.6262 $ ÷ ÷ 12 $

5c Stormwater Management User Fee1 $ ÷ ÷ 12 $

5d Clean Beaches & Ocean Parcel Tax1,2 $ ÷2

÷ 12 $

5e School District Parcel Tax3 $ ÷ ÷ 12 $

Total Surcharges per Unit… $

❻ Add lines , and This is your 2018–2019 Maximum Lawful Rent …..…. ❻ $

The undersigned hereby verifies that the 2018–2019 Santa Monica Rent Control registration fees, as well as all past fees and penalties, were paid in full by August 1, 2018, as required by Regulation 11200. The undersigned further certifies that this unit and the property’s common areas are not subject to any uncorrected citation or notice of violation of any state or local housing, health or safety law issued by a government official or agency.

Date: , 2018

By: /

print owner/agent name signature of owner/agent

address of owner/agent

1 Owners must provide a copy of the property tax bill to the tenant to pass through this tax. Regulations 3105, 3106 and 3108. 2 Divide only by the number of units without an exemption from this tax. 3 This is a flat fee of $XXX.XX (“SMMUSD-MEAS-R” on tax bill). Regulation 3109.

COMPLETE THE FOLLOWING TWO QUESTIONS BEFORE PROCEEDING TO SECTION 5 - SURCHARGES

1. Did this tenancy begin on or after Sept. 1, 2017? No Yes

2. Was this property purchased or was the property value reassessed pursuant to elective improvements on

or after Feb. 1, 2018? No Yes

If you answered No to both questions, you may complete Section 5.

If you answered Yes to either question, surcharges may not be added. Enter $0 on Line 5.

The following pages are written

communications that have been received from

the public on this item of the Jan. 25 agenda

and are part of the Board record.

1

From: Ann Maggio [mailto:[email protected]] Sent: Monday, January 22, 2018 12:28 PM To: RentControl Mailbox <[email protected]> Subject: Jan 25th Meeting ‐ Hearing on pass‐throughs

Dear Rent Control Board, This is not a case of better late than never. We brought this issue to your attention prior to the 2016 election when we realized the displacement effects taking a toll on renters when properties were being flipped to proportionally increase taxes paid by renters. What excuse is there for not having acted immediately to stem the negative impacts real estate investors and Real Estate Investment Trusts (REIT's) have had on Santa Monica's huge rental community? It is with great disappointment that this agenda item has taken so long to surface. This discussion should have taken place well over a year ago. We hope you immediately begin tracking the negative impacts this delay has caused on our neighbors. Additionally, it is imperative that staff NOT change the RCB report format every year in order to obfuscate pertinent data from public oversight. If the Rent control board seeks additional information on an annual basis, increase the size and scope of the report. The public deserves a consistent format that can be compared with ease on an annual basis. Sincerely, Ann Maggio Thanawalla 90403 "Unthinking respect for authority is the greatest enemy of truth." - Albert Einstein

Item 11A - Public Comment

1

From: The Millers [mailto:[email protected]] Sent: Tuesday, January 23, 2018 4:39 PM To: RentControl Mailbox <[email protected]> Subject: Public Comment on Item 11A, SMRCB Meeting on Jan. 25, 2018

Dear Commissioners, I am a Santa Monica resident, voter and housing provider. I am writing to comment on Item 11A (Voted Assessments Passed Through to Tenants) on the Rent Control Board’s Agenda for January 25, 2018. Parts of the proposal make good sense (for example, that a tenant’s pass through amounts should not be increased if the building is sold). However, the proposal would establish an inequitable, unfair and undemocratic policy with respect to future local taxes that are approved by voters. With this proposal, the Board is establishing a policy that tenants can vote for a new tax (say, for libraries or schools) and tenants can enjoy the benefits of the new tax (say, better schools, or cleaner beaches), but that tenants do not have to pay for the new tax. Isn’t this very bad policy? How is it fair or equitable for tenants to vote for a new tax and not have to pay their fair share? Do we abandon the principle that voters are responsible for their fair share of new taxes because one tenant moved out and another tenant moved in? It just seems fundamentally unfair that all citizens should not pay their fair share of future voted taxes. Sincerely, David Miller

Item 11A - Public Comment

Item 11A Public Comment

1

From: Diane Drake [mailto:[email protected]] Sent: Thursday, January 25, 2018 2:57 PM To: Lonnie Guinn <[email protected]> Subject: Fwd: Surcharge Pass Throughs

Dear Mr. Guinn, As a tenant of a rent-controlled apartment building on Ocean Ave. which was relatively recently sold (December, 2016, after having been held by the previous owner since the 1970s), I’m writing to express my concern about the astronomical increases in surcharge pass throughs that some tenants in the city are seeing. It’s my understanding that four of the five tax surcharges are, in fact, tied to assessed property value. Our current surcharges are in the neighborhood of about $13/month, and given that this rate is below the City average of about $28, a small increase seems fair. Even a doubling of the charge would seem a reasonable fee for the city to add to our already annual rent increases. Instead, I’m told that some tenants in neighboring buildings are seeing their rates go up by 10 times or more. This type of sudden exponential increase would represent a formidable economic burden to many, and one that seems at odds with the City’s stated goals to maintain a diverse population and to not drive even more working people out of Santa Monica. It’s my hope that the Board will carefully weigh its options and in its decision continue to look out for the welfare of those of us in rental housing who wish to remain a part of the City. Sincerely, Diane Drake

Screenwriter | Author | Consultant | Educator www.dianedrake.com Get Your Story Straight

Item 11A Public Comment

1

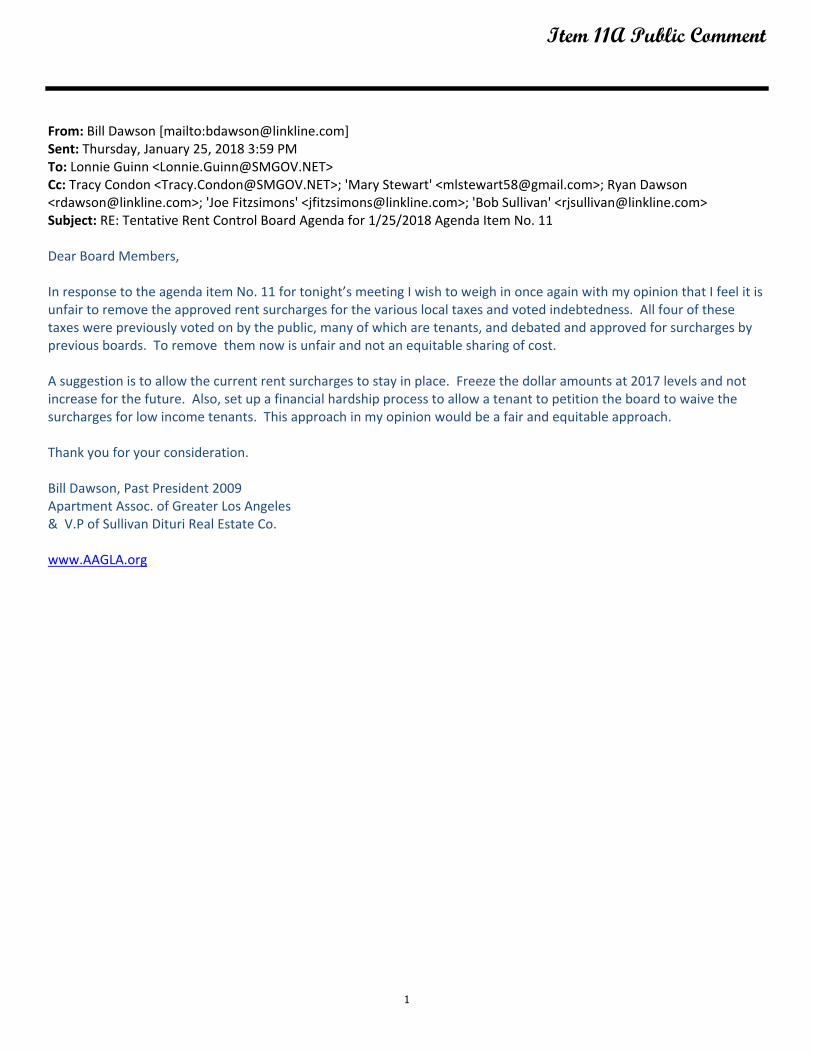

From: Bill Dawson [mailto:[email protected]] Sent: Thursday, January 25, 2018 3:59 PM To: Lonnie Guinn <[email protected]> Cc: Tracy Condon <[email protected]>; 'Mary Stewart' <[email protected]>; Ryan Dawson <[email protected]>; 'Joe Fitzsimons' <[email protected]>; 'Bob Sullivan' <[email protected]> Subject: RE: Tentative Rent Control Board Agenda for 1/25/2018 Agenda Item No. 11 Dear Board Members, In response to the agenda item No. 11 for tonight’s meeting I wish to weigh in once again with my opinion that I feel it is unfair to remove the approved rent surcharges for the various local taxes and voted indebtedness. All four of these taxes were previously voted on by the public, many of which are tenants, and debated and approved for surcharges by previous boards. To remove them now is unfair and not an equitable sharing of cost. A suggestion is to allow the current rent surcharges to stay in place. Freeze the dollar amounts at 2017 levels and not increase for the future. Also, set up a financial hardship process to allow a tenant to petition the board to waive the surcharges for low income tenants. This approach in my opinion would be a fair and equitable approach. Thank you for your consideration. Bill Dawson, Past President 2009 Apartment Assoc. of Greater Los Angeles & V.P of Sullivan Dituri Real Estate Co. www.AAGLA.org

Item 11A Public Comment