Issues in RCM & CENVAT Credit · –Independent Liability of Service Provider and Recipient ......

29

Issues in RCM & CENVAT Credit CA Sunil Gabhawalla

Transcript of Issues in RCM & CENVAT Credit · –Independent Liability of Service Provider and Recipient ......

Issues in RCM & CENVAT Credit

CA Sunil Gabhawalla

Indirect Tax : Textbook Example

Persons Invoice Raised for Transaction Government Collects Tax

Net Tax Gross Output Tax Credit Net Paid

A → B 100 10 110 10 0 10

B → C 120 12 132 12 -10 2

C → D 140 14 154 14 -12 2

D → E 160 16 176 16 -14 2

Total Tax Collected 52 -36 16

Denial of Credit on Policy / Documentation Grounds

Full RCM breaks the chain

Can the Govt. collect tax twice?

Will this continue in GST?

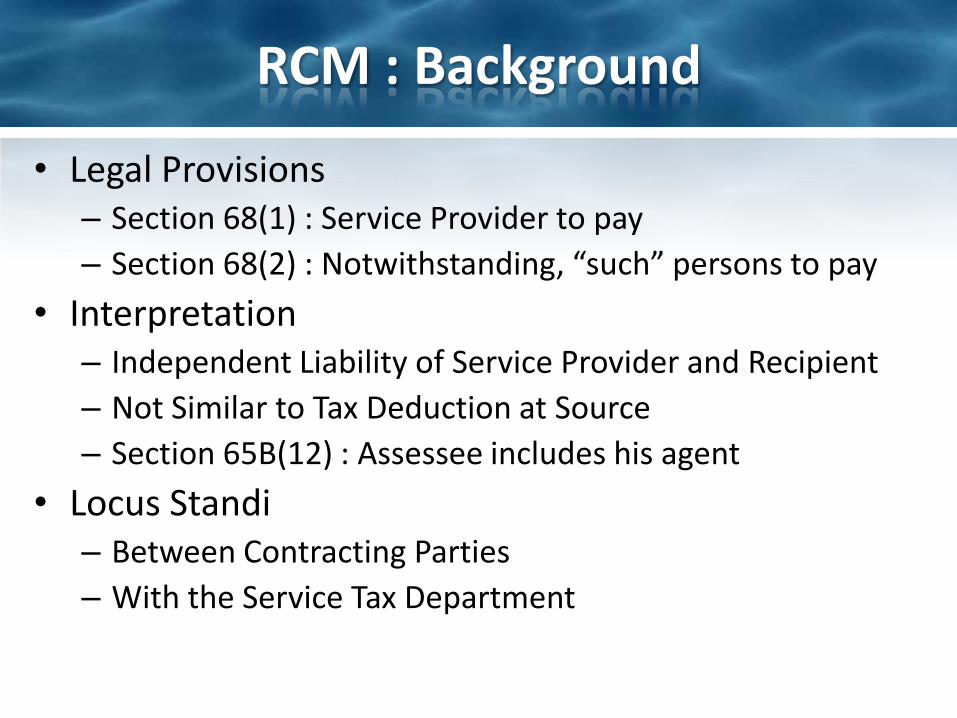

RCM : Background

• Legal Provisions – Section 68(1) : Service Provider to pay

– Section 68(2) : Notwithstanding, “such” persons to pay

• Interpretation – Independent Liability of Service Provider and Recipient

– Not Similar to Tax Deduction at Source

– Section 65B(12) : Assessee includes his agent

• Locus Standi– Between Contracting Parties

– With the Service Tax Department

Variations…R

ever

se C

har

ge M

ech

anis

m

Full Reverse Charge Mechanism

Selective

Abated Value

Goods Transport Agency Services 3.09 %

Rent a Cab Scheme Operator Services 4.944 %

Full Value Sponsorship Services 12.36 %

Comprehensive

Abated Value

Full Value

Insurance Auxiliary Services 12.36 %

Recovery Agent Services 12.36 %

Import of Services 12.36 %

Legal Services 12.36 %

Directors Services 12.36 %

Support Services by Government 12.36 %

Partial Reverse Charge Mechanism

Selective

Abated Value

Works Contract Services (Original Works) 2.472 % 2.472 %

Works Contract Services (Others) 4.326 % 4.326 %

Full Value

Supply of Manpower Services 3.09 % 9.27 %

Security Services 3.09 % 9.27 %

Rent a Cab Services 6.18 % 6.18 %

Directors’ Services

• Service means any activity carried out by a person for another for consideration …..

• When a director attends a Board Meeting,– Does he attend for earning “sitting fees” OR – Are “sitting fees” paid for attending the meeting

• Is there a difference between:– Activity carried out for consideration AND– Consideration paid for an activity

• INCOME and SERVICE are not similar concepts !!

Education Guide (Relevant Extracts)

The concept 'activity for a consideration' involves anelement of contractual relationship wherein the persondoing an activity does so at the desire of the person forwhom the activity is done in exchange for aconsideration. An activity done without such arelationship i.e. without the express or impliedcontractual reciprocity of a consideration would not bean 'activity for consideration' even though such anactivity may lead to accrual of gains to the personcarrying out the activity.

Para 2.3

Directors – Variations

• Service excludes a provision of service by an employee to the employer in the course of or in relation to his employment

• Whether all services covered ?– Comparison between legal services, employment,

etc. mere coincidence?

– Can a director have any other capacity vis-à-vis the company?

– Companies Act recognizes the professional capacity of directors

RCM & Basic Exemption Limit - Issues

• Is the service recipient eligible for basic exemption limit?

• Is the service provider eligible for basic exemption limit?

– Will the value be excluded in the case of FRCM?

– What value will be considered in PRCM?

RCM & Basic Exemption Limit : Legal Provisions

Notification 33/2012-ST exempts taxable services of aggregate value not exceeding ten lakh rupees inany financial year from the whole of the service tax leviable thereon under section 66B of the saidFinance ActProvided that nothing contained in this notification shall apply to,-

(i) …. or(ii) such value of taxable services in respect of which service tax shall be paid by such person

and in such manner as specified under sub-section (2) of section 68 of the said Finance Actread with Service Tax Rules, 1994.

3. For the purposes of determining aggregate value not exceeding ten lakh rupees, to avail exemptionunder this notification, in relation to taxable service provided by a goods transport agency, thepayment received towards the gross amount charged by such goods transport agency under section 67of the said Finance Act for which the person liable for paying service tax is as specified under sub-section (2) of section 68 of the said Finance Act read with Service Tax Rules, 1994, shall not be takeninto account.

Explanation. - For the purposes of this notification,-(A) ….(B) “aggregate value” means the sum total of value of taxable services charged in the firstconsecutive invoices issued during a financial year but does not include value charged in invoices issuedtowards such services which are exempt from whole of service tax leviable thereon under section 66B ofthe said Finance Act under any other notification.”

RCM & Basic Exemption Limit –Education Guide

If the service provider is exempted being a SSI (turnover lessthan Rs. 10 lakhs), how will the reverse charge mechanismwork?

The liability of the service provider and service recipient aredifferent and independent of each other. Thus in case theservice provider is availing exemption owing to turnoverbeing less than Rs. 10 lakhs, he shall not be obliged to payany tax. However, the service recipient shall have to payservice tax which he is obliged to pay under the partialreverse charge mechanism.

Para 10.1.3 of the Education Guide

Some Answers

Legal Provisions

Education Guide

Conclusion

Is the service recipient eligible for basic exemption limit?

No No No

Is the service provider eligible for basic exemption limit?

No? Yes Beneficial & PurposiveInterpretation to be given.

Will the value be excluded in the case of FRCM?

?? Only Exclusion for GTA

No

What value will be considered in PRCM?

?? No Specific Mention

Gross Value and not proportionate value

Legal Consultancy Services

(1) Subject to the provisions of this Chapter, where service tax is chargeable on any taxable service with reference to its value, then such value shall, —(i) in a case where the provision of service is for a

consideration in money, be the gross amount charged by the service provider for such service provided or to be provided by him;

(ii) in a case where the provision of service is for a consideration not wholly or partly consisting of money, be such amount in money as, with the addition of service tax charged, is equivalent to the consideration;

(iii) in a case where the provision of service is for a consideration which is not ascertainable, be the amount as may be determined in the prescribed manner

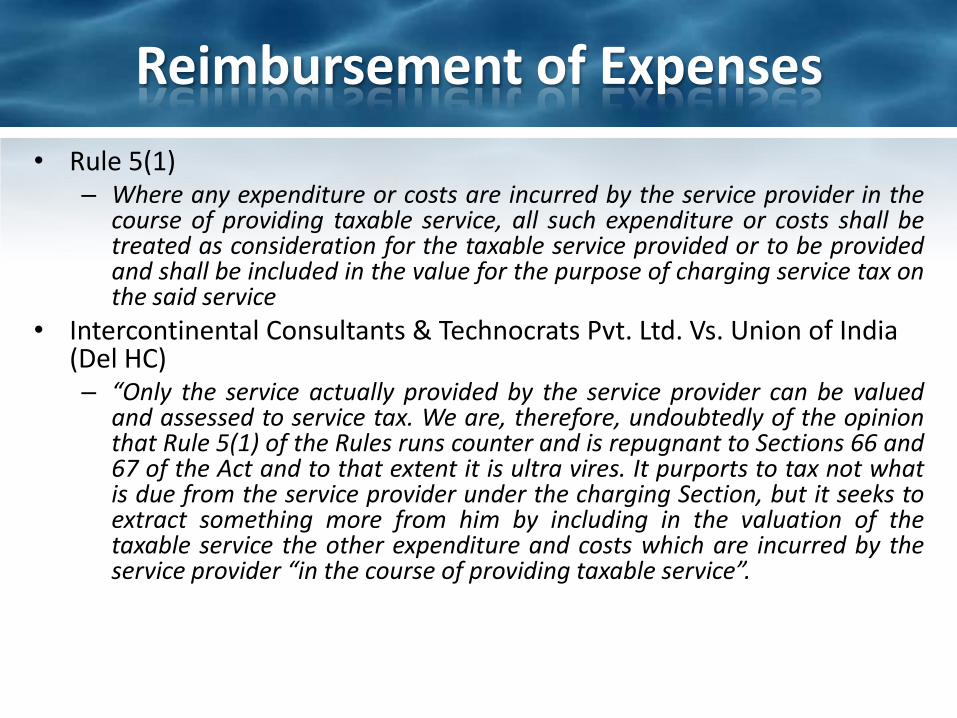

Reimbursement of Expenses

• Rule 5(1) – Where any expenditure or costs are incurred by the service provider in the

course of providing taxable service, all such expenditure or costs shall betreated as consideration for the taxable service provided or to be providedand shall be included in the value for the purpose of charging service tax onthe said service

• Intercontinental Consultants & Technocrats Pvt. Ltd. Vs. Union of India (Del HC)– “Only the service actually provided by the service provider can be valued

and assessed to service tax. We are, therefore, undoubtedly of the opinionthat Rule 5(1) of the Rules runs counter and is repugnant to Sections 66 and67 of the Act and to that extent it is ultra vires. It purports to tax not whatis due from the service provider under the charging Section, but it seeks toextract something more from him by including in the valuation of thetaxable service the other expenditure and costs which are incurred by theservice provider “in the course of providing taxable service”.

Issues to consider:

• Whether Rule 5 is valid?

• Whether it will also apply in RCM cases?

• Whether direct expenditure linked with the service can be considered as non monetary consideration?

– If specified in the contract

– If generally mentioned in the contract

– If not specified in the contract

Business Entity

• Section 65B(17)

– “business entity” means any person ordinarilycarrying out any activity relating to industry,commerce or any other business or profession

• Section 2(13) of Income Tax Act

– Business includes any trade, commerce ormanufacture or any adventure in the nature of trade,commerce or manufacture

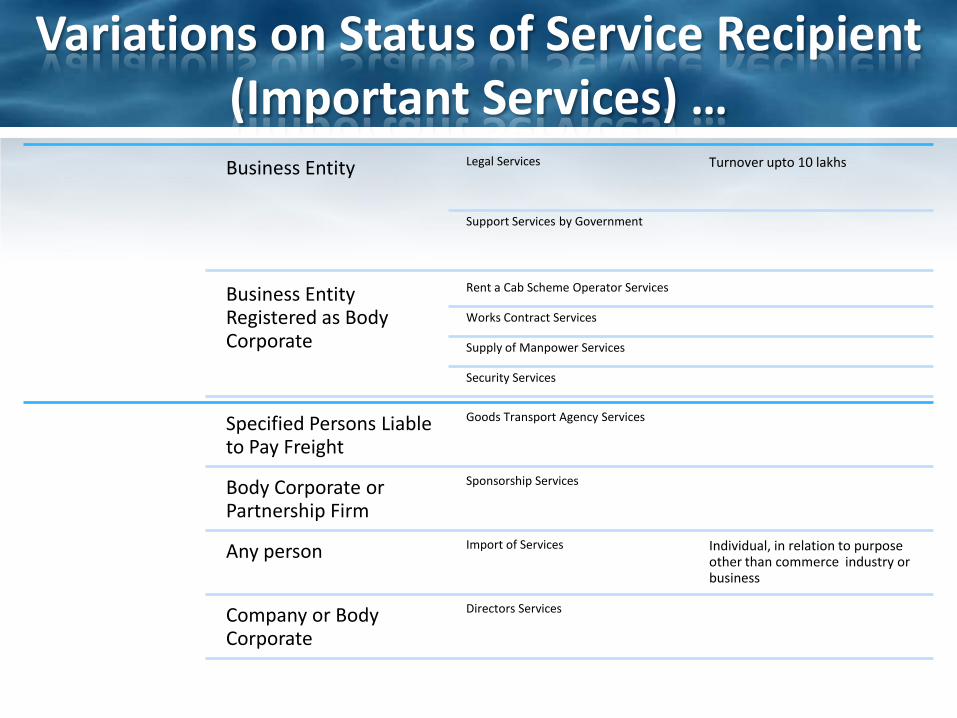

Variations on Status of Service Recipient (Important Services) …Business Entity Legal Services Turnover upto 10 lakhs

Support Services by Government

Business Entity Registered as Body Corporate

Rent a Cab Scheme Operator Services

Works Contract Services

Supply of Manpower Services

Security Services

Specified Persons Liable to Pay Freight

Goods Transport Agency Services

Body Corporate or Partnership Firm

Sponsorship Services

Any person Import of Services Individual, in relation to purpose other than commerce industry or business

Company or Body Corporate

Directors Services

LLP – Whether body corporate?

• Rule 2(bc) – “body corporate” has the meaning assigned to it in clause (7) of section 2 of the Companies Act, 1956

• Rule 2(cd) – “partnership firm” includes a limited liability partnership

• Tie Breaker Test Applicable? If yes, when?

Manpower Supply / Security Services

• What is manpower supply service?

– “supply of manpower” means supply of manpower, temporarily or otherwise, to another person to work under his superintendence or control – Rule 2(a)

• What is the test to determine whether supply of manpower?

Sponsorship Service

• Old Law– Section 65(15) : broadcasting” has the meaning assigned to it in

clause (c) of section 2 of the Prasar Bharti (Broadcasting Corporation of India) Act, 1990 (25 of 1990) and also includes ……obtaining sponsorships for broadcasting of any programme ……;

– Section 65(99a) “sponsorship” includes naming an event after the sponsor, displaying the sponsor’s company logo or trading name, giving the sponsor exclusive or priority booking rights, sponsoring prizes or trophies for competition; but does not include any financial or other support in the form of donations or gifts, given by the donors subject to the condition that the service provider is under no obligation to provide anything in return to such donors

• New Law – Both the above definitions repealed– What would be the position?

Sponsorship & CENVAT

• “output service” means any service provided by a provider of service located in the taxable territory but shall not include a service,—– specified in section 66D of the Finance Act; or– where the whole of service tax is liable to be paid by the recipient of service

• “exempted service” means a—– taxable service which is exempt from the whole of the service tax leviable thereon;

or– service, on which no service tax is leviable under section 66B of the Finance Act; or– taxable service whose part of value is exempted on the condition that no credit of

inputs and input services, used for providing such taxable service, shall be taken;

but shall not include a service which is exported in terms of rule 6A of the Service Tax Rules, 1994

Sponsorship == NOT OUTPUT SERVICE BUT NOT EXEMPTED SERVICE EITHER

Implications on CENVAT Credit – Identified Credits and Common Credits

CENVAT CREDIT RULES

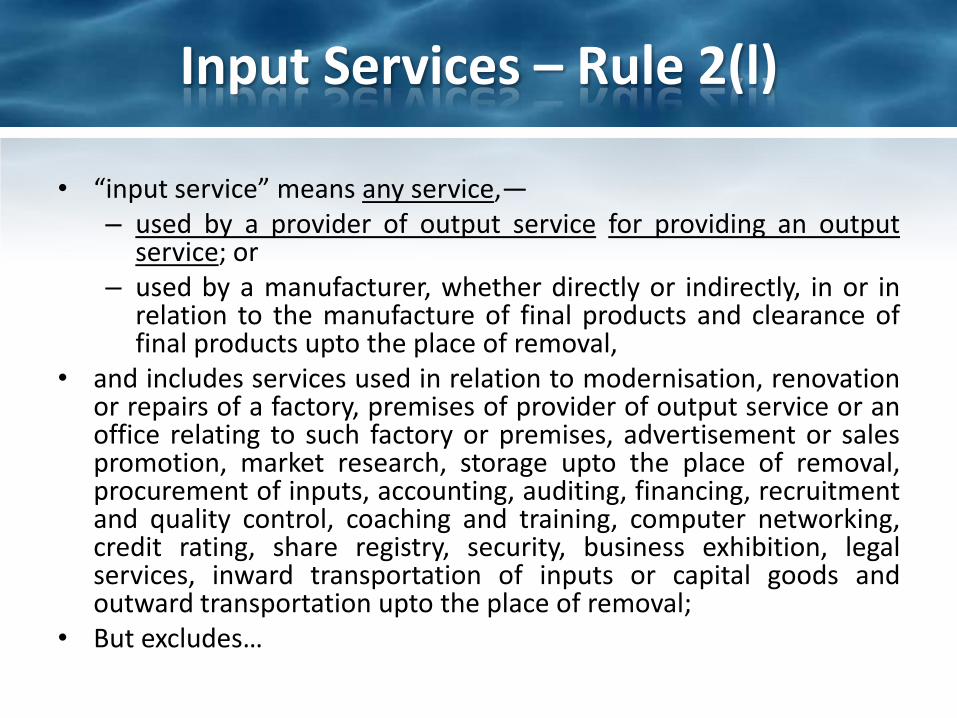

Input Services – Rule 2(l)

• “input service” means any service,—– used by a provider of output service for providing an output

service; or– used by a manufacturer, whether directly or indirectly, in or in

relation to the manufacture of final products and clearance offinal products upto the place of removal,

• and includes services used in relation to modernisation, renovationor repairs of a factory, premises of provider of output service or anoffice relating to such factory or premises, advertisement or salespromotion, market research, storage upto the place of removal,procurement of inputs, accounting, auditing, financing, recruitmentand quality control, coaching and training, computer networking,credit rating, share registry, security, business exhibition, legalservices, inward transportation of inputs or capital goods andoutward transportation upto the place of removal;

• But excludes…

Issues

• Whether there is a service?

– Recovery of Electricity Charges by Landlord ~6-b

– Commission Paid to Business Intermediaries ~6-e

• Is the service used by the service provider?

– Software ~6-f

– Mobile Phones ~6-a

• Is it used for providing output service?

– Artificial Bundling of Banquet with Gaming Service ~7

Input Services – Rule 2(l) {Contd}

• but excludes —

– service portion in the execution of a works contract and construction services including service listedunder clause (b) of section 66E of the Finance Act (hereinafter referred as specified services) in so faras they are used for—

• construction or execution of works contract of a building or a civil structure or a part thereof; or

• laying of foundation or making of structures for support of capital goods,

• except for the provision of one or more of the specified services; or

– services provided by way of renting of a motor vehicle, in so far as they relate to a motor vehiclewhich is not a capital goods; or

– service of general insurance business, servicing, repair and maintenance, in so far as they relate to amotor vehicle which is not a capital goods, except when used by—

• a manufacturer of a motor vehicle in respect of a motor vehicle manufactured by such person;or

• an insurance company in respect of a motor vehicle insured or reinsured by such person; or]

– such as those provided in relation to outdoor catering, beauty treatment, health services, cosmeticand plastic surgery, membership of a club, health and fitness centre, life insurance, health insuranceand travel benefits extended to employees on vacation such as Leave or Home Travel Concession,when such services are used primarily for personal use or consumption of any employee

Issues

• Construction and Architectural Services ==

– Whether the exclusion clause refers to construction as a “VERB” or as “SUBJECT”?

– Is it really excluded?

• Factory Canteen Contractor

– Primarily for personal use or consumption of employee?

• Group Mediclaim Policy

– Primarily for personal use or consumption of employee?

• Professional Indemnity Policy – no specific exclusion

Issues: Renting vs. Transport vs. Tour

• Negative List includes service of transportation of passengers, with or without accompanied belongings, by—– (i) a stage carriage;– (ii) railways in a class other than– (iii) metro, monorail or tramway;– (iv) inland waterways;– (v) public transport, other than predominantly for tourism

purpose, in a vessel between places located in India; and– *“(vi) metered cabs or auto rickshaws;]

• Hiring of Cars – specifically excluded• Hiring of Radio Taxies – no specific exclusion• Transportation of Employees

– Primarily for personal use or consumption of employee?– Is it Rent-a-Cab or Tour Operator?

When to avail the credit?

Nature of Eligibility

When can credit be claimed (EarliestPoint)

Upto what time it can be claimed? (Latest Point)

Conditions

Input Services –Domestic

On Receipt of Invoice – Rule 4(7)

6 months from the date of invoice

Payment to be made within 3 months –Otherwise, reverse with re-credit

Input Services –Partial ReverseCharge

On Payment of Value and Tax

6 months from the date of invoice/challan

InputServices –Full Reverse Charge

On Payment of Tax 6 months from the date of challan

What is the onus?

• Input Service == NEXUS (Used) == Output Service• Document of Availment – Rule 9(1) r/w Rule 4A • Time of Availment• Payment to the Service Provider • Payment by the Service Provider to the Government• Records to be maintained

• Strict Outer Time Limit of 6 months– Retrospective?– Retroactive?– Incorrect? – Unfair?

THANK YOU

![Cenvat Accounting[1]](https://static.fdocuments.us/doc/165x107/54193e3a7bef0a05088b4642/cenvat-accounting1.jpg)