Issues in California Workers Compensation Michele Bernal, FCAS VP & Actuary, American Re 6/15/00.

34

Issues in California Workers Compensation Michele Bernal, FCAS VP & Actuary, American Re 6/15/00

-

Upload

lora-rodgers -

Category

Documents

-

view

215 -

download

1

Transcript of Issues in California Workers Compensation Michele Bernal, FCAS VP & Actuary, American Re 6/15/00.

Issues in CaliforniaWorkers Compensation

Michele Bernal, FCAS

VP & Actuary, American Re

6/15/00

Issues in California Workers Comp

• Overview of the Primary Market

• Trends in Primary Loss Costs

• Development of Primary Losses

• Legislative Initiatives

• Reinsurance Pricing

Issues in California Workers Comp

• Overview of the Primary Market

• Trends in Primary Loss Costs

• Development of Primary Losses

• Legislative Initiatives

• Reinsurance Pricing

Accident Year Combined Loss and Expense Ratios

as of 12/31/99

68%

26%

78%

27%

82%

28%

66%

32%

53%

31%

58%

34%

81%

35%

90%

38%

95%

38%

101%

41%

100%

41%

0%

20%

40%

60%

80%

100%

120%

140%

160%

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

Accident YearLosses Expenses

*

* 1999 Expenses estimated

Source: WCIRB Final Summary of Year-End 1999 Experience

94%105% 110%

98%

84%92%

116%128% 133%

142% 141%

Watch Carrier Projections• WCIRB Estimates a $4.3 billion deficiency

in carried reserves at 12/99 (1999 earned premium was $6.9 billion)

• Carriers are reporting a 72% loss ratio for AY99, compared with the WCIRB’s projection of 100%

• For AY98, carriers initially reported 75% at 12/98, increasing to 91% at 12/99, but still short of the WCIRB’s estimate of 101%

What’s Happening?

California Primary PricingRelative to 1991 Charged Rates

0.5

0.6

0.7

0.8

0.9

1

1.1

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000Policy Year

Pure Premium Rate Charged 20% Increase? 30% Increase?

Source: WCIRB Final Summary of Year-End 1999 Experience

1/1/95 Open Rating

California Primary PricingRelative to Advisory Pure Premium

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000Policy Year

Charged Rates 20% Increase? 30% Increase?

Source: WCIRB Final Summary of Year-End 1999 Experience

1/1/95 Open Rating

Issues in California Workers Comp

• Overview of the Primary Market

• Trends in Primary Loss Costs

• Development of Primary Losses

• Legislative Initiatives

• Reinsurance Pricing

Trend in California Loss Costs

-40%

-20%

0%

20%

40%

60%

80%

100%

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

Accident Year

Total Loss Cost Frequency Severity

Source: WCIRB Final Summary of Year-End 1999 Experience

Trend in Loss Costs

-10%

0%

10%

20%

30%

40%

50%

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

Accident Year

California NCCI States

Sources: WCIRB Final Summary of Year-End 1999 Experience NCCI Annual Issues Symposium

Trend in Indemnity Claim Frequency

-40%

-30%

-20%

-10%

0%

10%

20%

30%

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

Accident Year

California NCCI States

Sources: WCIRB Final Summary of Year-End 1999 Experience NCCI Annual Issues Symposium

Trend in Per Indemnity Claim Average Medical

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

Accident Year

California NCCI States

Sources: WCIRB Final Summary of Year-End 1999 Experience NCCI Annual Issues Symposium

Cost Drivers - Medical

• 9/18/96 Minniear’s Decision– Treating Physician Presumption of Correctness

• 1/1/98 Change in ALAE Definition– Medical Cost Containment now coded with

Medical Losses

• 1/1/99 Medical Fee Schedule

Trend in Per Indemnity Claim Average Indemnity

0%

20%

40%

60%

80%

100%

120%

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

Accident Year

California NCCI States

Sources: WCIRB Final Summary of Year-End 1999 Experience NCCI Annual Issues Symposium

Cost Drivers - Indemnity

• Benefit Changes resulting from 1989 & 1994 reforms– +15% expected impact overall

• 4/1/97 Change in PD Rating Schedule– Presumably for new claims only– Presumably revenue neutral

• Minniears?

Issues in California Workers Comp

• Overview of the Primary Market

• Trends in Primary Loss Costs

• Development of Primary Losses

• Legislative Initiatives

• Reinsurance Pricing

1.00

1.20

1.40

1.60

1.80

2.00

1988 1990 1992 1994 1996 1998

24/12 36/24

Development Year

Loss Development FactorsIncurred Indemnity

Age in Months

Source: WCIRB Actuarial Committee Agenda - 5/31/00

1.50

2.00

2.50

3.00

3.50

4.00

1988 1990 1992 1994 1996 1998

24/12 36/24

Development Year

Loss Development FactorsPaid Indemnity

Age in Months

Source: WCIRB Actuarial Committee Agenda - 5/31/00

1.00

1.10

1.20

1.30

1.40

1.50

1988 1990 1992 1994 1996 1998

24/12 36/24

Development Year

Loss Development FactorsIncurred Medical

Age in Months

Source: WCIRB Actuarial Committee Agenda - 5/31/00

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2.60

1988 1990 1992 1994 1996 1998

24/12 36/24

Development Year

Loss Development FactorsPaid Medical

Age in Months

Source: WCIRB Actuarial Committee Agenda - 5/31/00

Possible Development Drivers

• Schaffer Ambulance (AB1913 & SB1217)– Possible reduction in case reserves in response

to class action suits alleging over-reserving, claiming high X-mods & low dividends as damages

• Optimism regarding Medical Management

• PD Rating Creep

• Claim Inflation

Loss Development Selections

• WCIRB uses latest year paid through 60 months of development, then converts to incurred development

• Development Varies Significantly by Industry Group– Increasing for all industry groups– Development for Professional & Clerical Services

classes substantially higher than for Construction classes

Issues in California Workers Comp

• Overview of the Primary Market

• Trends in Primary Loss Costs

• Development of Primary Losses

• Legislative Initiatives

• Reinsurance Pricing

Legislative Initiatives

• Benefit Increase (SB 996)

• Privacy (AB 435)

• Reinsurance Notification (SB 1959)

Legislative Initiatives

• Benefit Increase (SB 996)– Not likely to pass– $2.6 billion (25% of pure premiums)– Repeal presumption of correctness of treating

physician– Gov. Davis vetoed previous $2.5 billion bill

indicating he would sign if change was less than $1 billion

Legislative Initiatives

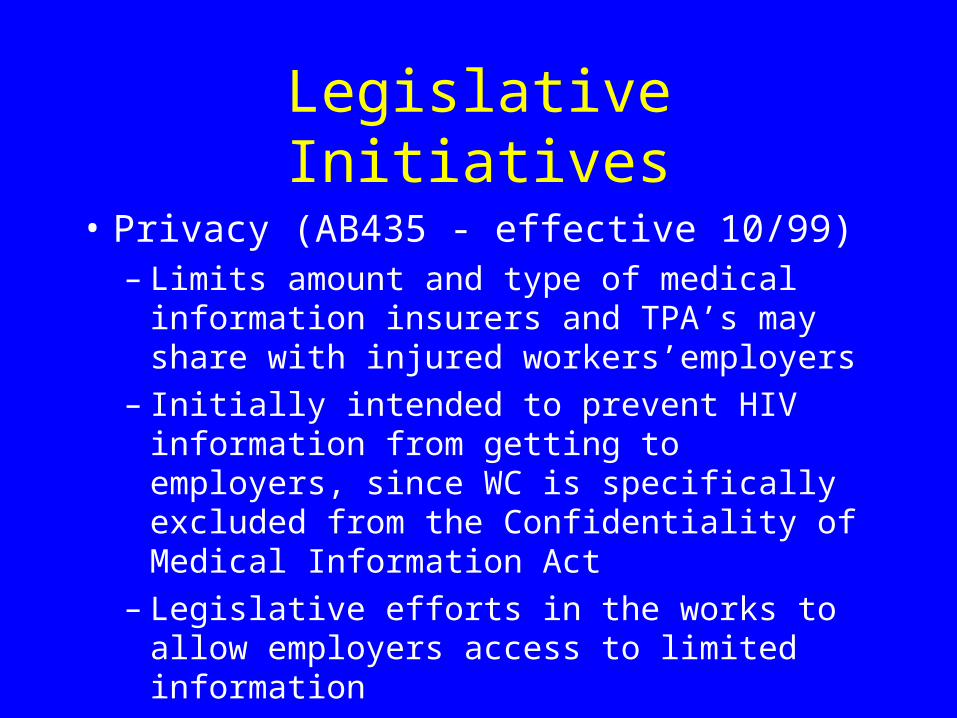

• Privacy (AB435 - effective 10/99)– Limits amount and type of medical information

insurers and TPA’s may share with injured workers’employers

– Initially intended to prevent HIV information from getting to employers, since WC is specifically excluded from the Confidentiality of Medical Information Act

– Legislative efforts in the works to allow employers access to limited information

Legislative Initiatives• Reinsurance Notification (SB 1959)

– Passed Senate; now in Assembly Insurance Committee

– Would require that Reinsurers notify the CDI of their intent to reinsure a workers comp program in the state.

– Current law requires a bond of the PV of estimated future payments at 6% per annum

– Discount rate would change to lower of 6%, or reinsurance company’s IRIS test #5 investment yield

– If reinsurer fails to post bond, ceding company may not claim reinsurance for reserve credit

Issues in California Workers Comp

• Overview of the Primary Market

• Trends in Primary Loss Costs

• Development of Primary Losses

• Legislative Initiatives

• Reinsurance Pricing

Reinsurance Pricing

• 2001 Draft Loss Elimination Ratios– Update of 1997 Tables– Still in Draft Form– Reviewing correlation of Medical & Indemnity

on Large Claims– Still working on Loss & ALAE LER’s– Will be filed with 1/1/01 pure premiums

• New Table M and Table L in 2002

2001 LER’s

• Significant Changes since 1997– Stochastic claim development– Increased claim development– Increased inflation– Update data to Policy Year 1993 & 1994

WCIRB Draft 2001 LER’s

$1M $500k

1997 Non-Stochastic .016 .025

1997 Stochastic .065 .099

2001 Non-Stochastic .022 .041

2001 Stochastic .070 .106

Loss Limit

Source: WCIRB Actuarial Committee Agenda 5/31/00

WCIRB Draft 2001 LER’sAdditional Thoughts

• Now more consistent with LER’s in other states

• Data is based on Policy Year 1993 and 1994, which were almost the best years in California workers comp

• Additional inflation could impact tables quickly

• Increased life expectancies

California WC ReinsuranceFinal Thoughts

• Monitor primary pricing– Pure premium changes aren’t enough– Make sure you obtain schedule credit info

• Make independent projections of ultimate losses

• Watch out for Inflation• Watch incurred loss development

– Use paid development when possible

• Don’t rely exclusively on 1997 LER’s